|

시장보고서

상품코드

1788513

동물용 진단 시장(-2030년) : 제품별, 기술별, 동물 유형별, 용도별, 지역별 예측Veterinary Diagnostics Market by Technology, Product, Animal, Application - Global Forecast to 2030 |

||||||

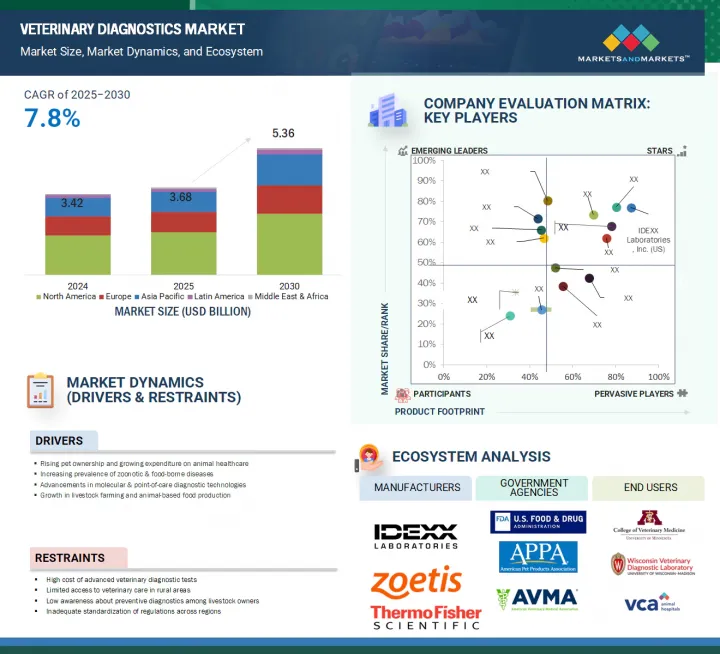

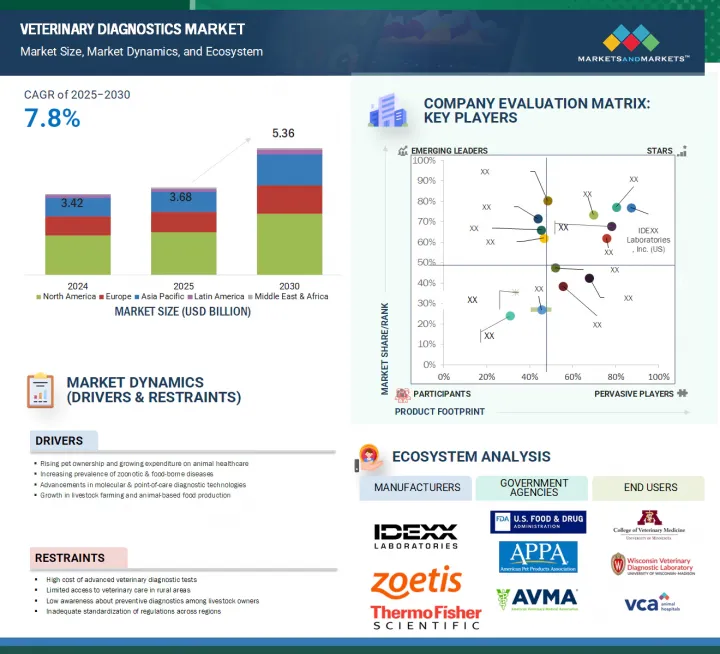

세계의 동물용 진단 시장 규모는 2025년 36억 8,000만 달러에서 2030년에는 53억 6,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR은 7.8%를 달성할 것으로 예상됩니다.

시장 성장의 주요 촉진요인으로는 특히 도시 및 고소득 지역에서의 동물 사육수 증가나 가축화를 들 수 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상연도 | 2024-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 조사 단위 | 금액(10억 달러) |

| 부문별 | 제품별, 기술별, 동물 유형별, 용도별 : 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동, 아프리카, 라틴아메리카 |

반려동물의 주인은 예방 진단, 정기적인 건강 진단, 질병 모니터링과 같은 고품질의 동물 의료가 필요합니다. 조류 인플루엔자, 렙토스피라증, 브루셀라증, 광견병과 같은 인수 공통 감염의 유행도 시장 성장에 기여하고 있습니다. 실시간 PCR, 차세대 시퀀싱(NGS), 마이크로플루이딕스공학, 휴대용 진단 분석기, 인공지능 등의 기술 발전으로 진단 검사의 정확성, 속도 및 접근성이 향상되었습니다.

제품별로 시장은 소모품과 기기로 구분됩니다. 기기 분야는 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예측됩니다. 기기에는 진단 검사용 분석 장치와 휴대용 분석 장치가 포함됩니다. 이러한 분석계는 동물의 체액(혈액, 혈청, 혈장, 소변)과 대변에 존재하는 생리학적으로 중요한 물질을 측정합니다. 기술 개발 및 동물 진단을 위한 AI 대응 기기의 개발은 예측 기간 동안 이 분야에서 시장 성장을 촉진할 것으로 예측됩니다.

기술별로, 분자진단 분야는 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예측됩니다. 이 부문에는 PCR 검사, 마이크로어레이 검사, 핵산 시퀀싱 기술이 포함됩니다. 이 부문의 성장률이 높아지는 이유는 인수 공통 감염의 발생률이 증가하여 정확하고 신속한 진단 솔루션에 대한 수요가 더욱 높아지고 있기 때문입니다. 분자진단은 특정 병원체, 유전자 질환, 항균제 내성을 확인할 수 있게 해주며, 다양한 질병의 적시 치료에 필수적입니다. PCR 및 차세대 시퀀싱과 같은 분자진단 검사의 기술적 진보도 시장 성장에 기여합니다.

시장은 지역별로 북미, 유럽, 아시아태평양, 라틴아메리카, 중동, 아프리카로 구분됩니다. 아시아태평양은 동물 건강에 대한 의식 증가, 1인당 소득 증가, 반려동물 사육에 대한 정부의 적극적인 노력, 신흥 국가에서의 축산물 생산 증가 등으로 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예측됩니다. 또한 중국, 인도, 인도네시아, 한국 등 급속히 도시화가 진행되는 경제권에서의 반려동물 사육률 상승도 예측 기간 중 시장 성장을 가속할 것으로 예측됩니다.

본 보고서에서는 세계의 동물용 진단 시장에 대해 조사했으며, 제품별, 기술별, 동물 유형별, 용도별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 시장 역학

- 업계 동향

- 기술 분석

- Porter's Five Forces 분석

- 규제 상황

- 특허 분석

- 무역 분석

- 가격 분석

- 상환 분석

- 2025-2026년의 주요 회의와 이벤트

- 주요 이해 관계자와 구매 기준

- 최종 사용자의 시점과 요구

- 동물용 진단 시장에 미치는 AI의 영향

- 에코시스템/시장 지도

- 밸류체인 분석

- 공급망 분석

- 인접 시장

- 투자 및 자금 조달 시나리오

- 트럼프 관세가 동물용 진단 시장에 미치는 영향

제6장 동물용 진단 시장(제품별)

- 소개

- 소모품

- 기기

제7장 동물용 진단 시장(기술별)

- 소개

- 면역진단

- 임상생화학

- 분자진단

- 혈액학

- 소변검사

- 기타

제8장 동물용 진단 시장(동물 유형별)

- 소개

- 반려동물

- 가축

제9장 동물용 진단 시장(용도별)

- 소개

- 감염증

- 내분비학

- 심장병학

- 종양학

- 기타

제10장 동물용 진단 시장(최종 사용자별)

- 소개

- 수의학 연구소

- 동물병원 및 클리닉

- 포인트 오브 케어/사내 검사

- 수의학 연구기관 및 대학

제11장 동물용 진단 시장(지역별)

- 소개

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 기타

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 중국

- 일본

- 인도

- 호주

- 한국

- 뉴질랜드

- 베트남

- 기타

- 라틴아메리카

- 라틴아메리카의 거시경제 전망

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- 중동 및 아프리카의 거시경제 전망

- GCC 국가

- 기타

제12장 경쟁 구도

- 개요

- 주요 진입기업의 전략/강점

- 수익 분석(2020-2024년)

- 시장 점유율 분석

- 기업평가 매트릭스 : 주요 진입기업(2024년)

- 기업평가 매트릭스 : 스타트업/중소기업(2024년)

- 브랜드/제품 비교 분석

- 주요 기업의 연구 개발비

- 기업평가와 재무 측정항목

- 경쟁 시나리오

제13장 기업 프로파일

- 주요 진출기업

- IDEXX LABORATORIES, INC.

- ZOETIS SERVICES LLC

- THERMO FISHER SCIENTIFIC INC.

- ANTECH DIAGNOSTICS, INC.

- BIOMERIEUX

- NEOGEN CORPORATION

- BIO-RAD LABORATORIES, INC.

- VIRBAC

- FUJIFILM HOLDINGS CORPORATION

- SHENZHEN MINDRAY ANIMAL MEDICAL TECHNOLOGY CO., LTD.

- INDICAL BIOSCIENCE GMBH

- BIONOTE

- BIOGAL

- AGROLABO SPA

- INNOVATIVE DIAGNOSTICS

- 기타 기업

- RANDOX LABORATORIES LTD.

- BIOCHEK

- FASSISI, GMBH

- ALVEDIA

- SKYER, INC.

- SHENZHEN BIOEASY BIOTECHNOLOGY, INC.

- PRECISION BIOSENSOR, INC.

- EUROIMMUN MEDIZINISCHE LABORDIAGNOSTIKA AG

- GOLD STANDARD DIAGNOSTICS

- SKYLA CORPORATION

제14장 부록

CSM 25.08.19The global veterinary diagnostics market is projected to reach USD 5.36 billion by 2030 from USD 3.68 billion in 2025, at a CAGR of 7.8% during the forecast period. A key growth driver for market growth includes rising ownership and the domestication of animals, particularly in urban and high-income regions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | BY PRODUCT, TECHNOLOGY, ANIMAL TYPE, END USER |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

Pet owners require high-quality animal medical care, including preventive diagnostics, routine health screenings, and disease monitoring. The increasing prevalence of zoonotic diseases, such as avian influenza, leptospirosis, brucellosis, and rabies, also contributes to the market's growth. Technological advancements in real-time PCR, next-generation sequencing (NGS), microfluidics, portable diagnostic analyzers, and artificial intelligence are enhancing the accuracy, speed, and accessibility of diagnostic testing.

By product, the instruments segment is projected to grow at the highest CAGR during the forecast period.

By product, the market is segmented into consumables and instruments. The instruments segment is projected to grow at the highest CAGR during the forecast period. The instruments include diagnostic test analyzers and portable analyzers. These analyzers measure the physiologically significant substances present in body fluids (blood, serum, plasma, and urine) and feces of animals. Increasing technological advancements and the development of AI-enabled instruments for veterinary diagnostics are expected to fuel the market adoption in this segment during the forecast period.

By technology, the molecular diagnostics segment is estimated to grow at the highest CAGR during the forecast period.

By technology, the molecular diagnostics segment is expected to grow at the highest CAGR during the forecast period. This segment includes PCR tests, microarray tests, and nucleic acid sequencing technologies. The high growth rate of this segment is attributed to the increasing incidence of infectious and zoonotic diseases, which further increases the demand for precise and rapid diagnostic solutions. Molecular diagnostics allow the identification of specific pathogens, genetic disorders, and antimicrobial resistance, which is critical for the timely treatment of various diseases. Technological advancements in molecular diagnostic tests, such as PCR and next-generation sequencing, also contribute to the market's growth.

By region, the Asia Pacific market is expected to grow at the highest CAGR during the forecast period.

The market is segmented by region into North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. The Asia Pacific region is projected to grow at the highest CAGR during the forecast period owing to the rising awareness about animal health, the increasing per capita income, favorable government initiatives for pet adoption, and the increasing production of livestock products in emerging economies. The rising pet ownership in rapidly urbanizing economies such as China, India, Indonesia, and South Korea is also expected to drive the market growth during the forecast period.

Breakdown of supply-side primary interviews:

- By Company Type: Tier 1 (45%), Tier 2 (20%), and Tier 3 (35%)

- By Designation: C-level Executives (35%), Directors (25%), and Other Designations (40%)

- By Region: North America (40%), Europe (25%), the Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

- By Company Type: Veterinary Reference Laboratories (40%), Veterinary Hospitals & Clinics (25%), POC/In-house Testing (20%), and Veterinary Research Institutes & Universities (15%)

- By Designation: Veterinary Healthcare Professionals (35%), Department Heads (27%), Procurement Heads (22%), and Other Designations (16%)

- By Region: North America (40%), Europe (25%), the Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Research Coverage:

The market study covers the veterinary diagnostics market across various segments. It aims to estimate the market size and the growth potential across different segments by product, application, technology, animal type, end user, and region. The study also includes an in-depth competitive analysis of the key players in the market, their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall veterinary diagnostics market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (rise in companion animals, growing demand for products derived from animals, increased zoonotic disease cases, increase in pet insurance, increase in disease control and disease prevention measures), restraints (rising pet cost care and high cost of diagnostic tests), opportunities (high growth potential of emerging economies), and challenges (lack of animal health awareness and shortage of veterinary practitioners) influencing the growth of the veterinary diagnostics market

- Market Penetration: Comprehensive information on product portfolios offered by the top players in the global veterinary diagnostics market. The report analyzes this market by product, application, technology, animal type, end user, and region.

- Product Enhancement/Innovation: Detailed insights into upcoming trends and product launches in the global veterinary diagnostics market.

- Market Development: Comprehensive information on the lucrative emerging markets by product, technology, animal type, application, end user, and region.

- Market Diversification: Exhaustive information about new products, growing geographies, recent developments, and investments in the global veterinary diagnostics market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product and service offerings, and capabilities of leading players in the global veterinary diagnostics market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS & EXCLUSIONS

- 1.2.2 MARKETS & REGIONS COVERED

- 1.2.3 YEARS CONSIDERED

- 1.3 MARKET STAKEHOLDERS

- 1.4 LIMITATIONS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- 2.2 RESEARCH METHODOLOGY DESIGN

- 2.2.1 SECONDARY RESEARCH

- 2.2.1.1 Key data from secondary sources

- 2.2.2 PRIMARY DATA

- 2.2.2.1 Key data from primary sources

- 2.2.2.2 Key industry insights

- 2.2.1 SECONDARY RESEARCH

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- 2.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.5 MARKET SHARE ANALYSIS

- 2.6 RESEARCH ASSUMPTIONS

- 2.6.1 GROWTH RATE ASSUMPTIONS

- 2.7 RISK ASSESSMENT

- 2.8 RESEARCH LIMITATIONS

- 2.8.1 METHODOLOGY-RELATED LIMITATIONS

- 2.8.2 SCOPE-RELATED LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 VETERINARY DIAGNOSTICS MARKET OVERVIEW

- 4.2 ASIA PACIFIC: VETERINARY DIAGNOSTICS MARKET, BY PRODUCT & COUNTRY (2024)

- 4.3 VETERINARY DIAGNOSTICS MARKET: REGIONAL MIX

- 4.4 VETERINARY DIAGNOSTICS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.5 VETERINARY DIAGNOSTICS MARKET: DEVELOPED MARKETS VS. EMERGING ECONOMIES

5 MARKET OVERVIEW

- 5.1 MARKET DYNAMICS

- 5.1.1 DRIVERS

- 5.1.1.1 Growth in companion animal population

- 5.1.1.2 Increasing demand for animal-derived food products

- 5.1.1.3 Growing concerns about infectious zoonotic diseases

- 5.1.1.4 Rising demand for pet insurance and growing animal health expenditure

- 5.1.1.5 Increasing number of veterinary practitioners and rising income levels in developed markets

- 5.1.1.6 Growing focus on disease control & prevention measures

- 5.1.2 RESTRAINTS

- 5.1.2.1 Rising pet care costs

- 5.1.2.2 High cost of veterinary diagnostic tests

- 5.1.3 OPPORTUNITIES

- 5.1.3.1 Growth potential of emerging economies

- 5.1.3.2 Integration of AI & ML

- 5.1.4 CHALLENGES

- 5.1.4.1 Low animal healthcare awareness in emerging countries

- 5.1.4.2 Shortage of veterinary practitioners in emerging economies

- 5.1.1 DRIVERS

- 5.2 INDUSTRY TRENDS

- 5.2.1 ADOPTION OF MULTIPLE TEST PANELS

- 5.2.2 OUTSOURCING OF VETERINARY DIAGNOSTIC TESTING SERVICES

- 5.2.3 GROWING SCALE OF VETERINARY BUSINESSES

- 5.3 TECHNOLOGY ANALYSIS

- 5.3.1 KEY TECHNOLOGIES

- 5.3.1.1 Portable instruments for POC diagnostic services

- 5.3.1.2 Biosensor-based diagnostic systems

- 5.3.2 ADJACENT TECHNOLOGIES

- 5.3.2.1 Wearable biosensors & remote monitoring devices

- 5.3.2.2 Development of rapid & sensitive veterinary diagnostic kits

- 5.3.2.3 Breath & saliva-based diagnostic tools

- 5.3.2.4 Microfluidics & Lab-on-chip devices

- 5.3.3 COMPLEMENTARY TECHNOLOGIES

- 5.3.3.1 AI-driven diagnostic platforms

- 5.3.3.2 Next-generation Sequencing (NGS)

- 5.3.1 KEY TECHNOLOGIES

- 5.4 PORTER'S FIVE FORCES ANALYSIS

- 5.4.1 THREAT OF NEW ENTRANTS

- 5.4.2 THREAT OF SUBSTITUTES

- 5.4.3 BARGAINING POWER OF SUPPLIERS

- 5.4.4 BARGAINING POWER OF BUYERS

- 5.4.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.5 REGULATORY LANDSCAPE

- 5.5.1 REGULATORY ANALYSIS

- 5.5.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.5.2.1 North America

- 5.5.2.2 Europe

- 5.5.2.3 Rest of the world

- 5.6 PATENT ANALYSIS

- 5.6.1 PATENT PUBLICATION TRENDS FOR VETERINARY DIAGNOSTICS

- 5.6.2 JURISDICTION & TOP APPLICANT ANALYSIS

- 5.7 TRADE ANALYSIS

- 5.7.1 TRADE DATA FOR HS CODE 9018

- 5.7.1.1 Import data for HS Code 9018

- 5.7.1.2 Export data for HS Code 9018

- 5.7.1 TRADE DATA FOR HS CODE 9018

- 5.8 PRICING ANALYSIS

- 5.8.1 AVERAGE SELLING PRICE TREND, BY PRODUCT, 2022-2024

- 5.8.1.1 Average selling price trend of key players, by product, 2022-2024

- 5.8.2 AVERAGE SELLING PRICE, BY REGION

- 5.8.2.1 Average selling price of clinical chemistry analyzers and blood gas & electrolyte analyzers, by region, 2024

- 5.8.2.2 Average selling price trend of clinical chemistry reagent clips & cartridges, by region, 2022-2024

- 5.8.2.3 Average selling price trend of clinical chemistry analyzers, by region, 2022-2024

- 5.8.2.4 Average selling price trend of blood glucose strips, by region, 2022-2024

- 5.8.2.5 Average selling price trend of glucose monitors, by region, 2022-2024

- 5.8.2.6 Average selling price trend of blood gas & electrolyte reagent clips/cartridges, by region

- 5.8.2.7 Average selling price trend of blood gas & electrolyte analyzers, by region, 2022-2024

- 5.8.1 AVERAGE SELLING PRICE TREND, BY PRODUCT, 2022-2024

- 5.9 REIMBURSEMENT ANALYSIS

- 5.10 KEY CONFERENCES & EVENTS, 2025-2026

- 5.11 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.11.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.11.2 BUYING CRITERIA

- 5.12 END-USER PERSPECTIVE & UNMET NEEDS

- 5.13 IMPACT OF AI ON VETERINARY DIAGNOSTICS MARKET

- 5.13.1 INTRODUCTION

- 5.13.2 MARKET POTENTIAL IN VETERINARY DIAGNOSTICS ECOSYSTEM

- 5.13.3 AI-USE CASES

- 5.13.4 KEY COMPANIES IMPLEMENTING AI IN VETERINARY DIAGNOSTICS

- 5.14 ECOSYSTEM/MARKET MAP

- 5.15 VALUE CHAIN ANALYSIS

- 5.16 SUPPLY CHAIN ANALYSIS

- 5.17 ADJACENT MARKETS

- 5.18 INVESTMENT & FUNDING SCENARIO

- 5.19 TRUMP TARIFF IMPACT ON VETERINARY DIAGNOSTICS MARKET

- 5.19.1 INTRODUCTION

- 5.19.2 KEY TARIFF RATES

- 5.19.3 PRICE IMPACT ANALYSIS

- 5.19.4 IMPACT ON COUNTRY/REGION

- 5.19.5 IMPACT ON END-USE INDUSTRIES

6 VETERINARY DIAGNOSTICS MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- 6.2 CONSUMABLES

- 6.2.1 RECURRING NATURE TO BOOST DEMAND

- 6.3 INSTRUMENTS

- 6.3.1 INCREASING DEMAND FOR POC ANALYZERS TO DRIVE MARKET

7 VETERINARY DIAGNOSTICS MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- 7.2 IMMUNODIAGNOSTICS

- 7.2.1 LATERAL FLOW ASSAYS

- 7.2.1.1 Lateral flow rapid tests

- 7.2.1.1.1 Ability to provide real-time insights to drive market

- 7.2.1.2 Lateral flow strip readers

- 7.2.1.2.1 Rising need for readers to determine analyte quantity to fuel adoption

- 7.2.1.1 Lateral flow rapid tests

- 7.2.2 ELISA

- 7.2.2.1 Cost-effectiveness and ease of use to drive market

- 7.2.3 ALLERGEN-SPECIFIC IMMUNODIAGNOSTIC TESTS

- 7.2.3.1 Increasing incidence of allergies in companion animals to fuel market

- 7.2.4 IMMUNOASSAY ANALYZERS

- 7.2.4.1 High sensitivity & specificity for biomarker detection to drive market

- 7.2.5 RADIOIMMUNOASSAYS

- 7.2.5.1 Measurement of hormone levels and detection of specific proteins to fuel market

- 7.2.6 OTHER IMMUNODIAGNOSTIC PRODUCTS

- 7.2.1 LATERAL FLOW ASSAYS

- 7.3 CLINICAL BIOCHEMISTRY

- 7.3.1 CLINICAL CHEMISTRY ANALYSIS

- 7.3.1.1 Clinical chemistry reagent clips & cartridges

- 7.3.1.1.1 Rising number of screening tests to fuel market

- 7.3.1.2 Clinical chemistry analyzers

- 7.3.1.2.1 Increasing installation of clinical chemistry analyzers to propel market

- 7.3.1.1 Clinical chemistry reagent clips & cartridges

- 7.3.2 GLUCOSE MONITORING

- 7.3.2.1 Blood glucose strips

- 7.3.2.1.1 Growing demand in home care settings to fuel market

- 7.3.2.2 Glucose monitors

- 7.3.2.2.1 Growing incidence of diabetes in pet animals to fuel adoption

- 7.3.2.3 Urine glucose strips

- 7.3.2.3.1 Increasing risk of DKA in animals to propel market

- 7.3.2.1 Blood glucose strips

- 7.3.3 BLOOD GAS & ELECTROLYTE ANALYSIS

- 7.3.3.1 Blood gas & electrolyte reagent clips & cartridges

- 7.3.3.1.1 Easy availability of animal species-specific preloaded reagent clips to boost market

- 7.3.3.2 Blood gas & electrolyte analyzers

- 7.3.3.2.1 Determination of blood oxygen & carbon dioxide levels to drive market

- 7.3.3.1 Blood gas & electrolyte reagent clips & cartridges

- 7.3.1 CLINICAL CHEMISTRY ANALYSIS

- 7.4 MOLECULAR DIAGNOSTICS

- 7.4.1 PCR TESTS

- 7.4.1.1 Increased laboratory usage in proteomics & genomics to support growth

- 7.4.2 MICROARRAYS

- 7.4.2.1 Growing applications of biochips in identifying infectious diseases to drive market

- 7.4.3 NUCLEIC ACID SEQUENCING

- 7.4.3.1 Identification of pathogens to fuel market

- 7.4.4 OTHER MOLECULAR DIAGNOSTIC PRODUCTS

- 7.4.1 PCR TESTS

- 7.5 HEMATOLOGY

- 7.5.1 HEMATOLOGY CARTRIDGES

- 7.5.1.1 Complete blood analysis capabilities to fuel market

- 7.5.2 HEMATOLOGY ANALYZERS

- 7.5.2.1 Adoption by veterinary hospitals & clinics to support market growth

- 7.5.1 HEMATOLOGY CARTRIDGES

- 7.6 URINALYSIS

- 7.6.1 URINALYSIS CLIPS & CARTRIDGES/PANELS

- 7.6.1.1 Detection of electrolytes to boost adoption

- 7.6.2 URINE ANALYZERS

- 7.6.2.1 Development of advanced analyzers for POC testing to support market growth

- 7.6.3 URINE TEST STRIPS

- 7.6.3.1 Increasing prevalence of CKD in cats & dogs to drive market

- 7.6.1 URINALYSIS CLIPS & CARTRIDGES/PANELS

- 7.7 OTHER TECHNOLOGIES

8 VETERINARY DIAGNOSTICS MARKET, BY ANIMAL TYPE

- 8.1 INTRODUCTION

- 8.2 COMPANION ANIMALS

- 8.2.1 DOGS

- 8.2.1.1 High insurance coverage and availability of reimbursements to drive market

- 8.2.2 CATS

- 8.2.2.1 Increasing pet cat population to support market uptake

- 8.2.3 HORSES

- 8.2.3.1 Growing awareness regarding equine health to fuel market

- 8.2.4 OTHER COMPANION ANIMALS

- 8.2.1 DOGS

- 8.3 LIVESTOCK

- 8.3.1 CATTLE

- 8.3.1.1 Growing consumption of dairy products to drive market

- 8.3.2 PIGS

- 8.3.2.1 Increasing incidence of infectious diseases to fuel market

- 8.3.3 POULTRY

- 8.3.3.1 Increasing demand for poultry meat contributes to market growth

- 8.3.4 OTHER LIVESTOCK ANIMALS

- 8.3.1 CATTLE

9 VETERINARY DIAGNOSTICS MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 INFECTIOUS DISEASES

- 9.2.1 BACTERIAL INFECTIONS

- 9.2.1.1 Rapid spread of E. Coli to drive market

- 9.2.2 VIRAL INFECTIONS

- 9.2.2.1 High mutation rate to ensure continued demand for diagnostics

- 9.2.3 PARASITIC INFECTIONS

- 9.2.3.1 Presence of parasitic infections to fuel market

- 9.2.4 OTHER INFECTIONS

- 9.2.1 BACTERIAL INFECTIONS

- 9.3 ENDOCRINOLOGY

- 9.3.1 GROWING RISK OF DIABETES TO BOOST DEMAND

- 9.4 CARDIOLOGY

- 9.4.1 INCREASING CASES OF CVD IN DOGS TO FUEL MARKET

- 9.5 ONCOLOGY

- 9.5.1 HIGH INCIDENCE OF CANINE CANCER TO DRIVE MARKET

- 9.6 OTHER APPLICATIONS

10 VETERINARY DIAGNOSTICS MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 VETERINARY REFERENCE LABORATORIES

- 10.2.1 LARGE VOLUME OF TESTING SAMPLES AND AVAILABILITY OF SKILLED WORKFORCE TO PROPEL MARKET

- 10.3 VETERINARY HOSPITALS & CLINICS

- 10.3.1 GROWING PET OWNERSHIP AND SPENDING ON PET CARE TO DRIVE MARKET

- 10.4 POINT-OF-CARE/IN-HOUSE TESTING

- 10.4.1 COST-EFFECTIVENESS AND RAPID RESULTS TO BOOST DEMAND

- 10.5 VETERINARY RESEARCH INSTITUTES & UNIVERSITIES

- 10.5.1 INCREASING COLLABORATIONS BETWEEN PRIVATE COMPANIES AND RESEARCH INSTITUTES TO SUPPORT GROWTH

11 VETERINARY DIAGNOSTICS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 11.2.2 US

- 11.2.2.1 High veterinary healthcare expenditure to drive market

- 11.2.3 CANADA

- 11.2.3.1 Growing pet adoption to drive market

- 11.3 EUROPE

- 11.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 11.3.2 GERMANY

- 11.3.2.1 Rising awareness of zoonotic diseases to fuel market

- 11.3.3 UK

- 11.3.3.1 Increasing pet ownership to drive market

- 11.3.4 FRANCE

- 11.3.4.1 Willingness of pet owners to spend on pet health to drive market

- 11.3.5 ITALY

- 11.3.5.1 Growing consumption of meat & dairy products to drive market

- 11.3.6 SPAIN

- 11.3.6.1 Growing demand for poultry products to fuel market

- 11.3.7 NETHERLANDS

- 11.3.7.1 Developments in veterinary diagnostic products to support market growth

- 11.3.8 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 11.4.2 CHINA

- 11.4.2.1 Increasing incidence of zoonotic diseases to propel market

- 11.4.3 JAPAN

- 11.4.3.1 Increasing pet expenditure to support market growth

- 11.4.4 INDIA

- 11.4.4.1 Increasing demand for dairy products to drive market

- 11.4.5 AUSTRALIA

- 11.4.5.1 Rise in pet ownership to support market growth

- 11.4.6 SOUTH KOREA

- 11.4.6.1 Rising need for specialized veterinary services to drive market

- 11.4.7 NEW ZEALAND

- 11.4.7.1 Focus on pet insurance to aid market

- 11.4.8 VIETNAM

- 11.4.8.1 Growing focus on disease surveillance to drive market

- 11.4.9 REST OF ASIA PACIFIC

- 11.5 LATIN AMERICA

- 11.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 11.5.2 BRAZIL

- 11.5.2.1 Growth in livestock industry to boost demand

- 11.5.3 MEXICO

- 11.5.3.1 Increasing focus on poultry-associated products to support market growth

- 11.5.4 REST OF LATIN AMERICA

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 MACROECONOMIC OUTLOOK FOR THE MIDDLE EAST & AFRICA

- 11.6.2 GCC COUNTRIES

- 11.6.2.1 Kingdom of Saudi Arabia (KSA)

- 11.6.2.1.1 Technology advancements in veterinary diagnostics to boost demand

- 11.6.2.2 United Arab Emirates (UAE)

- 11.6.2.2.1 Favorable government support for vet diagnostics to drive market

- 11.6.2.3 Other GCC Countries

- 11.6.2.1 Kingdom of Saudi Arabia (KSA)

- 11.6.3 REST OF MIDDLE EAST & AFRICA

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS, 2020-2024

- 12.4 MARKET SHARE ANALYSIS

- 12.4.1 RANKING OF KEY MARKET PLAYERS

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.5.5.1 Company footprint

- 12.5.5.2 Region footprint

- 12.5.5.3 Product footprint

- 12.5.5.4 Technology footprint

- 12.5.5.5 Animal type footprint

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- 12.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.6.5.1 Detailed list of key startups/SMEs

- 12.6.5.2 Competitive benchmarking of key startups

- 12.7 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 12.8 R&D EXPENDITURE OF KEY PLAYERS

- 12.9 COMPANY VALUATION & FINANCIAL METRICS

- 12.9.1 FINANCIAL METRICS

- 12.9.2 COMPANY VALUATION

- 12.10 COMPETITIVE SCENARIO

- 12.10.1 PRODUCT/SERVICE LAUNCHES, ENHANCEMENTS, AND APPROVALS

- 12.10.2 DEALS

- 12.10.3 EXPANSIONS

- 12.10.4 OTHER DEVELOPMENTS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 IDEXX LABORATORIES, INC.

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product/Service launches, enhancements, and approvals

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses & competitive threats

- 13.1.2 ZOETIS SERVICES LLC

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product/Service launches, enhancements, and approvals

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses & competitive threats

- 13.1.3 THERMO FISHER SCIENTIFIC INC.

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Services offered

- 13.1.3.3 MnM view

- 13.1.3.3.1 Key strengths

- 13.1.3.3.2 Strategic choices

- 13.1.3.3.3 Weaknesses & competitive threats

- 13.1.4 ANTECH DIAGNOSTICS, INC.

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product/Service launches, enhancements, and approvals

- 13.1.4.3.2 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses & competitive threats

- 13.1.5 BIOMERIEUX

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Services offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product/Service launches, enhancements, and approvals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Key strengths

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses & competitive threats

- 13.1.6 NEOGEN CORPORATION

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Services offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product/Service launches, enhancements, and approvals

- 13.1.6.3.2 Deals

- 13.1.6.3.3 Other developments

- 13.1.7 BIO-RAD LABORATORIES, INC.

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Services offered

- 13.1.8 VIRBAC

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Deals

- 13.1.8.3.2 Expansions

- 13.1.9 FUJIFILM HOLDINGS CORPORATION

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Services offered

- 13.1.10 SHENZHEN MINDRAY ANIMAL MEDICAL TECHNOLOGY CO., LTD.

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Services offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product/Service launches, enhancements, and approvals

- 13.1.10.3.2 Expansions

- 13.1.11 INDICAL BIOSCIENCE GMBH

- 13.1.11.1 Business overview

- 13.1.11.2 Products/Services offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Product/Service launches, enhancements, and approvals

- 13.1.12 BIONOTE

- 13.1.12.1 Business overview

- 13.1.12.2 Products/Services offered

- 13.1.12.3 Recent developments

- 13.1.12.4 Product/Service launches, enhancements, and approvals

- 13.1.12.4.1 Deals

- 13.1.13 BIOGAL

- 13.1.13.1 Business overview

- 13.1.13.2 Products/Services offered

- 13.1.14 AGROLABO S.P.A.

- 13.1.14.1 Business overview

- 13.1.14.2 Products/Services offered

- 13.1.15 INNOVATIVE DIAGNOSTICS

- 13.1.15.1 Business overview

- 13.1.15.2 Products/Services offered

- 13.1.1 IDEXX LABORATORIES, INC.

- 13.2 OTHER PLAYERS

- 13.2.1 RANDOX LABORATORIES LTD.

- 13.2.2 BIOCHEK

- 13.2.3 FASSISI, GMBH

- 13.2.4 ALVEDIA

- 13.2.5 SKYER, INC.

- 13.2.6 SHENZHEN BIOEASY BIOTECHNOLOGY, INC.

- 13.2.7 PRECISION BIOSENSOR, INC.

- 13.2.8 EUROIMMUN MEDIZINISCHE LABORDIAGNOSTIKA AG

- 13.2.9 GOLD STANDARD DIAGNOSTICS

- 13.2.10 SKYLA CORPORATION

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 RELATED REPORTS

- 14.4 AUTHOR DETAILS