|

시장보고서

상품코드

1800741

지능형 교통 시스템(ITS) 시장 : 도로, 철도, 항공, 해상, 첨단 교통 관리 시스템, 징수 및 주차 관리 시스템, 보안 및 감시 시스템, 스마트 티켓팅 시스템 - 예측(-2030년)Intelligent Transportation System Market by Roadways, Railways, Aviation, Maritime, Advanced Traffic Management Systems, Tolling & Parking Management Systems, Security & Surveillance Systems, Smart Ticketing Systems - Global Forecast to 2030 |

||||||

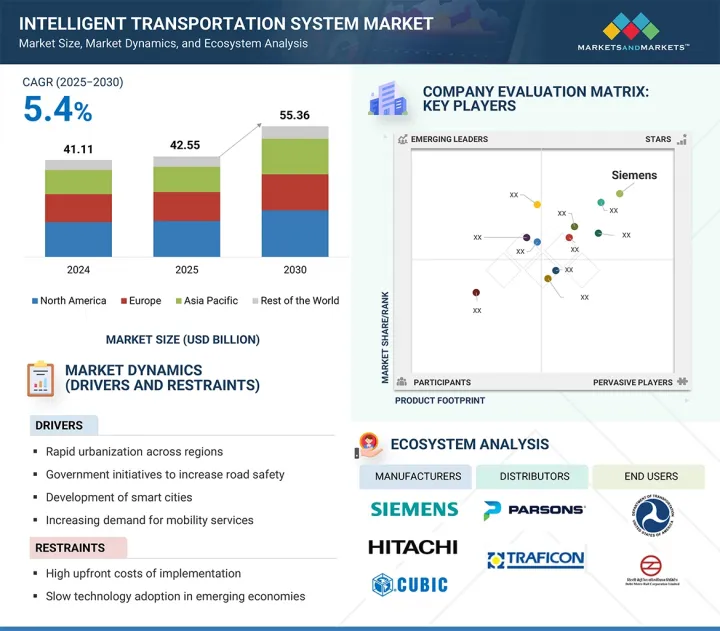

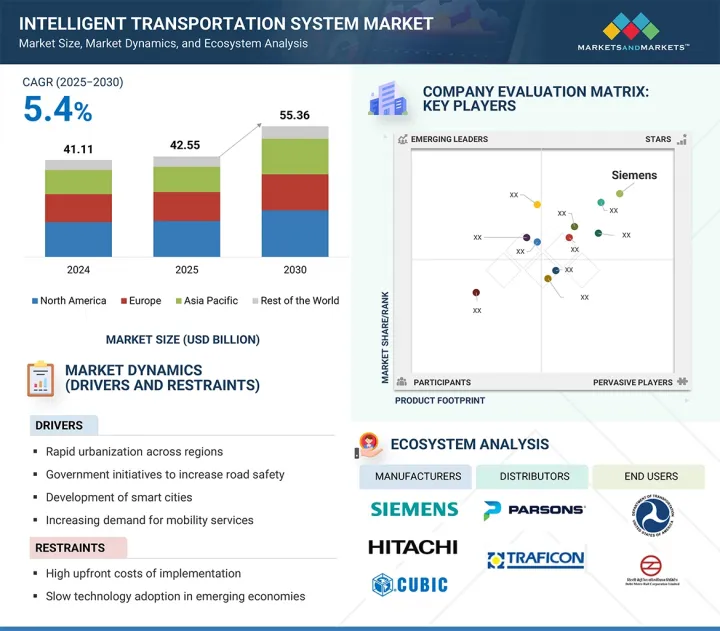

세계의 지능형 교통 시스템(ITS) 시장 규모는 2025년에 425억 5,000만 달러, 2030년까지 553억 6,000만 달러에 이를 것으로 예측되며, 예측 기간에 CAGR 5.4%의 성장이 전망됩니다.

도시 교통 체증 증가`, 자동차 보유량 급증, 스마트하고 지속 가능한 모빌리티 솔루션에 대한 수요 증가 등으로 인해 각 지역별로 강력한 성장세를 보이고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 10억 달러 |

| 부문 | 방식, 용도, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

스마트시티 개발 및 대중교통 인프라 개선을 위한 정부의 이니셔티브는 ITS 기술 도입을 더욱 가속화할 것입니다. ITS 솔루션은 교통안전 강화, 이동시간 단축, 교통흐름 최적화, 환경영향 최소화에 중요한 역할을 하고 있습니다. 첨단 교통 관리 시스템, 스마트 주차, 전자 요금 징수, 실시간 승객 정보 시스템 등의 용도는 도로 및 대중 교통 네트워크에서 널리 채택되고 있습니다.

"방식별로는 철도 부문이 예측 기간 동안 두 번째로 큰 시장 점유율을 차지할 것으로 예측됩니다. "

철도 부문은 철도 인프라 현대화, 고속철도 및 도시 교통 시스템에 대한 투자 증가, 안전 및 운영 효율성 향상에 대한 수요 증가로 인해 예측 기간 동안 지능형 교통 시스템(ITS) 시장에서 두 번째로 큰 시장 규모를 차지할 것으로 예측됩니다. 철도 인프라의 현대화는 자동 신호, 실시간 모니터링, 예지보전 등 첨단 ITS 기술의 도입을 촉진하여 운행 효율을 높이고 운행 중단 시간을 단축하는 데 기여합니다. 또한, 선진국과 신흥 경제권을 막론하고 고속철도 및 도시 교통 프로젝트에 대한 투자가 증가함에 따라 스마트 발권 시스템, 중앙교통관제센터, 다이나믹 여객정보 디스플레이 등의 ITS 솔루션이 대규모로 전개되고 있습니다. 이러한 시스템은 원활한 통합, 스케줄링 최적화, 출퇴근 경험 향상을 보장합니다. 또한, 안전과 시스템 신뢰성 향상에 대한 요구가 높아짐에 따라 장애물 감지, 지능형 모니터링, 자동 제동 등의 기술 도입이 가속화되고 있으며, 이 모든 것이 보다 안전하고 효율적인 철도 운영에 기여하고 있습니다.

"용도별로는 발권 부문이 예측 기간 동안 두 번째로 높은 CAGR을 나타낼 것으로 보입니다. "

비접촉식 디지털 결제 솔루션에 대한 수요 증가, 자동요금징수(AFC) 시스템 보급 확대, 승객 편의성 향상과 경영비용 절감에 대한 관심 증가로 인해 예측 기간 동안 지능형 교통 시스템(ITS) 시장에서 티켓팅 부문이 두 번째로 높은 CAGR을 나타낼 것으로 예측됩니다. 예측됩니다. 비접촉식 디지털 결제 솔루션에 대한 수요가 증가함에 따라 스마트카드, 모바일 발권 앱, QR 코드 기반 시스템의 채택이 증가하고 있으며, 물리적 상호 작용의 필요성을 줄이고 통근자의 경험을 향상시키면서 더 빠르고 안전하며 위생적인 결제 옵션을 제공합니다. 제공합니다. 버스, 기차, 지하철 서비스 전체에 AFC 시스템이 도입되면 효율적이고 오류 없는 실시간 요금 처리가 가능해집니다. 이는 교통 사업자의 수익 보장을 향상시킬 뿐만 아니라 대규모 복합 교통 네트워크에서 이러한 시스템의 확장성을 지원합니다. 또한, 승객의 편의성 향상과 운영 비용 절감에 대한 관심이 높아지면서 교통 기관은 수동 발권에서 디지털 발권 솔루션으로의 전환을 추진하고 있으며, 이는 승차 프로세스를 간소화하고 인건비를 절감하며 전체 서비스의 신뢰성을 향상시켜 이 부문의 견조한 성장에 박차를 가하고 있습니다. 성장에 박차를 가하고 있습니다.

"북미가 예측 기간 동안 두 번째로 높은 CAGR을 나타낼 것입니다. "

북미는 첨단 교통 인프라의 강력한 존재감, 스마트 모빌리티 및 자율주행차 기술에 대한 투자 확대, 지속 가능하고 효율적인 교통 시스템에 대한 정부 지원 증가로 인해 예측 기간 동안 지능형 교통 시스템(ITS) 시장에서 두 번째로 높은 CAGR을 나타낼 것으로 예측됩니다. 이 지역의 잘 구축된 교통망은 지능형 교통 관리, 실시간 사고 감지, 적응형 신호 제어 등 첨단 ITS 솔루션의 통합을 위한 강력한 기반을 제공합니다.

세계의 지능형 교통 시스템(ITS) 시장에 대해 조사 분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 지견

- 지능형 교통 시스템(ITS) 시장 기업에 있어서 매력적인 기회

- 지능형 교통 시스템(ITS) 시장 : 방식별

- 지능형 교통 시스템(ITS) 시장 : 용도별

- 지능형 교통 시스템(ITS) 시장 : 지역별

- 지능형 교통 시스템(ITS) 시장 : 국가별

제5장 시장 개요

- 서론

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 가격 결정 분석

- 서멀 카메라 평균 판매 가격 동향 : 지역별(2021년-2024년)

- 차량 감지 센서 평균 판매 가격 동향 : 지역별(2021년-2024년)

- 서멀 카메라 평균 판매 가격 : 주요 기업별(2024년)

- 차량 감지 센서 평균 판매 가격 : 주요 기업별(2024년)

- 밸류체인 분석

- 생태계 분석

- 기술 분석

- 주요 기술

- 보완 기술

- 인접 기술

- 특허 분석

- 무역 분석

- 수입 데이터(HS코드 8530)

- 수출 데이터(HS코드 8530)

- 주요 컨퍼런스 및 이벤트(2025년-2026년)

- 사례 연구

- 투자 및 자금조달 시나리오

- 관세 및 규제 상황

- 관세 분석(HS코드 8530)

- 규제기관, 정부기관 및 기타 조직

- 표준

- Porter의 Five Forces 분석

- 주요 이해관계자와 구입 기준

- 지능형 교통 시스템(ITS) 시장에 대한 AI/생성형 AI의 영향

- 지능형 교통 시스템(ITS) 시장에 대한 2025년 미국 관세의 영향

- 서론

- 주요 관세율

- 가격 영향 분석

- 국가/지역에 대한 영향

- 용도에 대한 영향

제6장 지능형 교통 시스템(ITS)용 프로토콜

- 서론

- 단거리

- WAVE(IEEE 802.11)

- WPAN(IEEE 802.15)

- 장거리

- WIMAX(IEEE 802.11)

- OFDM

- IEEE 1512

- TMDD(TRAFFIC MANAGEMENT DATA DICTIONARY)

- 기타 프로토콜

제7장 지능형 교통 시스템(ITS) 시장 : 방식별

- 서론

- 도로

- 철도

- 항공

- 해상

제8장 도로용 지능형 교통 시스템(ITS) 시장 : 시스템 유형별, 제공별

- 서론

- 도로용 지능형 교통 시스템(ITS) 시장 : 시스템 유형별

- 첨단 교통 관리 시스템

- 첨단 승객 정보 시스템

- 징수 및 주차 관리 시스템

- 보안 및 감시 시스템

- 도로용 지능형 교통 시스템(ITS) 시장 : 제공 별

- 하드웨어

- 소프트웨어

- 서비스

제9장 철도용 지능형 교통 시스템(ITS) 시장 : 시스템 유형별, 제공별

- 서론

- 철도용 지능형 교통 시스템(ITS) 시장 : 시스템 유형별

- 철도 운행 시스템

- 승객 정보 시스템

- 스마트 티켓팅 시스템

- 기타 철도 시스템 유형

- 철도용 지능형 교통 시스템(ITS) 시장 : 제공 별

- 하드웨어

- 소프트웨어

- 서비스

제10장 항공용 지능형 교통 시스템(ITS) 시장 : 시스템 유형별, 제공별

- 서론

- 항공용 지능형 교통 시스템(ITS) 시장 : 시스템 유형별

- 항공기 관리 시스템

- 보안 및 감시 시스템

- 스마트 티켓팅 시스템

- 정보 관리 시스템

- 항공용 지능형 교통 시스템(ITS) 시장 : 제공 별

- 하드웨어

- 소프트웨어

- 서비스

제11장 해상용 지능형 교통 시스템(ITS) 시장 : 시스템 유형별, 제공별

- 서론

- 해상용 지능형 교통 시스템(ITS) 시장 : 시스템 유형별

- 자동 식별 시스템

- 선박 교통 관리 시스템

- 정보 시스템

- 기타 해상 시스템 유형

- 해상용 지능형 교통 시스템(ITS) 시장 : 제공 별

- 하드웨어

- 소프트웨어

- 서비스

제12장 지능형 교통 시스템(ITS) 시장 : 용도별

- 서론

- 보안 및 감시

- 교통 관리

- 정보 관리

- 티켓팅

- 기타 용도

제13장 지능형 교통 시스템(ITS) 시장 : 지역별

- 서론

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 멕시코

- 유럽

- 유럽의 거시경제 전망

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 벨기에

- 덴마크

- 오스트리아

- 스웨덴

- 기타 유럽

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 기타 지역

- 기타 지역 거시경제 전망

- 중동

- 아프리카

- 남미

제14장 경쟁 구도

- 개요

- 주요 시장 진출기업의 전략/강점(2020년-2025년)

- 시장 점유율 분석(2024년)

- 매출 분석(2020년-2024년)

- 기업 평가와 재무 지표

- 브랜드/제품 비교

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업 평가 매트릭스 : 스타트업/중소기업(2024년)

- 경쟁 시나리오

제15장 기업 개요

- 서론

- 주요 기업

- SIEMENS

- HITACHI, LTD.

- CUBIC CORPORATION

- CONDUENT INCORPORATED

- KAPSCH TRAFFICCOM AG

- THALES

- TELEDYNE TECHNOLOGIES INCORPORATED

- INDRA SISTEMAS, S.A.

- MUNDYS

- VERRA MOBILITY

- TOMTOM INTERNATIONAL BV

- 기타 기업

- SWARCO

- ST ENGINEERING

- ITERIS, INC.

- Q-FREE

- SERCO GROUP PLC

- EFKON GMBH

- LANNER ELECTRONICS

- SENSYS GATSO GROUP AB

- TAGMASTER

- RICARDO

- TRANSMAX PTY LTD.

- DAKTRONICS, INC.

- GEOTOLL

- CELLINT

- ALSTOM SA

- CLEVER DEVICES LTD

- ETA TRANSIT

- FURUNO ELECTRIC CO., LTD

- TRANSCORE

- ADAPTIVE RECOGNITION INC

- ECONOLITE

- MIOVISION TECHNOLOGIES INCORPORATED

- ELOVATE

제16장 부록

LSH 25.09.05The global intelligent transportation system market was valued at USD 42.55 billion in 2025 and is projected to reach USD 55.36 billion by 2030, at a CAGR of 5.4% during the forecast period. The market is experiencing robust growth across regions, driven by increasing urban traffic congestion, a surge in vehicle ownership, and the rising demand for smart and sustainable mobility solutions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Mode, Intelligent Transportation System Market for Roadways, Intelligent Transportation System Market for Railways, Intelligent Transportation System Market for Aviation, Intelligent Transportation System Market for Maritime, By Application, and Region |

| Regions covered | North America, Europe, APAC, RoW |

Government initiatives aimed at developing smart cities and improving public transport infrastructure further accelerate ITS technology deployment. ITS solutions play a crucial role in enhancing road safety, reducing travel time, optimizing traffic flow, and minimizing environmental impact. Applications such as advanced traffic management systems, smart parking, electronic toll collection, and real-time traveler information systems are being widely adopted across roadways and public transit networks.

"Based on mode, the railways segment is expected to account for the second-largest market share during the forecast period."

The railways segment is expected to hold the second-largest market size in the intelligent transportation system market during the forecast period due to the modernization of rail infrastructure, increasing investments in high-speed rail and urban transit systems, and rising demand for enhanced safety and operational efficiency. Modernization of rail infrastructure drives the adoption of advanced ITS technologies such as automated signaling, real-time monitoring, and predictive maintenance, which help enhance operational efficiency and reduce service downtime. Additionally, increasing investments in high-speed rail and urban transit projects across both developed and developing economies are leading to the large-scale deployment of ITS solutions like smart ticketing systems, centralized traffic control centers, and dynamic passenger information displays. These systems ensure seamless integration, optimized scheduling, and improved commuter experiences. Moreover, the rising demand for improved safety and system reliability is accelerating the implementation of technologies such as obstacle detection, intelligent surveillance, and automated braking, all of which contribute to safer and more efficient rail operations.

"Based on application, the ticketing segment is projected to register the second-highest CAGR during the forecast period."

The ticketing segment is projected to register the second-highest CAGR in the intelligent transportation system market during the forecast period due to the growing demand for contactless and digital payment solutions, increasing deployment of automated fare collection (AFC) systems, and rising focus on improving passenger convenience and reducing operational costs. Growing demand for contactless and digital payment solutions is driving the adoption of smart cards, mobile ticketing apps, and QR-code-based systems, offering faster, more secure, and hygienic payment options that enhance the commuter experience while reducing the need for physical interactions. The increasing deployment of AFC systems across buses, trains, and metro services enables efficient, error-free, and real-time fare processing. This not only improves revenue assurance for transit operators but also supports the scalability of these systems across large, multimodal transport networks. Additionally, the rising focus on enhancing passenger convenience and reducing operational costs encourages transport agencies to transition from manual to digital ticketing solutions, which streamline boarding processes, cut down on labor expenses, and improve overall service reliability, fueling the segment's robust growth.

"North America to register second-highest CAGR during forecast period"

North America is projected to register the second-highest CAGR in the intelligent transportation system market during the forecast period due to the strong presence of advanced transport infrastructure, growing investments in smart mobility and autonomous vehicle technologies, and increasing government support for sustainable and efficient transportation systems. The region's well-established transportation network provides a strong foundation for the integration of advanced ITS solutions, such as intelligent traffic management, real-time incident detection, and adaptive signal control. Additionally, government initiatives supporting eco-friendly and efficient urban transportation, including congestion pricing, electric vehicle (EV) integration, and data-driven traffic optimization, further drive the adoption of ITS. These factors combined are fostering an environment conducive to the rapid implementation and expansion of intelligent transportation systems, positioning North America as a key growth region in the global market.

Extensive primary interviews were conducted with key industry experts in the intelligent transportation system market to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below.

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

- By Company Type - Tier 1 - 55%, Tier 2 - 25%, and Tier 3 - 20%

- By Designation - Directors - 50%, Managers - 30%, and Others - 20%

- By Region - North America - 45%, Europe - 30%, Asia Pacific - 20%, and RoW - 5%

The intelligent transportation system market is dominated by a few globally established players, such as Siemens (Germany), Hitachi Ltd. (Japan), Mundys (Italy), Indra Sistemas S.A. (Spain), Verra Mobility (US), Cubic Corporation (US), Conduent, Inc. (US), Kapsch Trafficcom AG (Austria), Thales (France), Teledyne Technologies Incorporated (US), Swarco (Austria), ST Engineering (Singapore), Iteris, Inc (US), Q-Free (Norway), SERCO GROUP PLC (UK).

The study includes an in-depth competitive analysis of these key players in the intelligent transportation system market, with their company profiles, recent developments, and key market strategies.

Study Coverage:

The report segments the intelligent transportation system market and forecasts its size by mode (roadways, railways, aviation, maritime), intelligent transportation system market for roadways (advanced traffic management systems, advanced traveler information systems, tolling & parking management systems, security & surveillance systems), intelligent transportation system market for railways (rail operation systems, passenger information systems, smart ticketing systems, others), intelligent transportation system market for aviation (aircraft management systems, security & surveillance systems, smart ticketing systems, information management systems), intelligent transportation system market for maritime (automatic identification systems, vessel traffic management systems, information systems, others), application (security & surveillance, traffic management, information management, ticketing, others). It also discusses the market's drivers, restraints, opportunities, and challenges. It gives a detailed view of the market across four main regions (North America, Europe, Asia Pacific, and RoW). The report includes a value chain analysis of the key players and their competitive analysis in the intelligent transportation system ecosystem.

Key Benefits of Buying the Report:

- Analysis of key drivers (Rapid urbanization across regions, Government initiatives to increase road safety, Rising development of smart cities globally, Increasing demand for mobility services), restraints (High upfront costs of implementation, Slow technology adoption in emerging economies), opportunities (Growing public-private partnerships, Growing demand for emerging economies), challenges (Complexity of data management and privacy)

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the intelligent transportation system market

- Market Development: Comprehensive information about lucrative markets - the report analyses the intelligent transportation system market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the intelligent transportation system market

- Competitive Assessment: In-depth assessment of market shares and growth strategies of leading players, such as Siemens (Germany), Hitachi Ltd. (Japan), Mundys (Italy), Indra Sistemas S.A. (Spain), Verra Mobility (US), Cubic Corporation (US), Conduent, Inc. (US), Kapsch Trafficcom AG (Austria), Thales (France), Teledyne Technologies Incorporated (US), Swarco (Austria), ST Engineering (Singapore), Iteris, Inc (US), Q-Free (Norway), SERCO GROUP PLC (UK).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of key secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 List of primary interview participants

- 2.1.2.2 Breakdown of primary interviews

- 2.1.2.3 Key data from primary sources

- 2.1.2.4 Key industry insights

- 2.1.3 SECONDARY AND PRIMARY RESEARCH

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to estimate market size using top-down analysis (supply side)

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 FACTOR ANALYSIS

- 2.3.1 DEMAND-SIDE ANALYSIS

- 2.3.2 SUPPLY-SIDE ANALYSIS

- 2.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RISK ASSESSMENT

- 2.7 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INTELLIGENT TRANSPORTATION SYSTEM MARKET

- 4.2 INTELLIGENT TRANSPORTATION SYSTEM MARKET, BY MODE

- 4.3 INTELLIGENT TRANSPORTATION SYSTEM MARKET, BY APPLICATION

- 4.4 INTELLIGENT TRANSPORTATION SYSTEM MARKET, BY REGION

- 4.5 INTELLIGENT TRANSPORTATION SYSTEM MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing migration from rural to urban areas

- 5.2.1.2 Government-led initiatives to increase road safety

- 5.2.1.3 Rapid development of smart cities

- 5.2.1.4 Increasing demand for mobility services

- 5.2.2 RESTRAINT

- 5.2.2.1 Substantial investments in deploying advanced technologies

- 5.2.2.2 Infrastructure limitations and budgetary constraints in developing countries

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing public-private partnerships

- 5.2.3.2 Pressing need for smart mobility solutions

- 5.2.4 CHALLENGES

- 5.2.4.1 Complexities associated with data management and privacy

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND OF THERMAL CAMERAS, BY REGION, 2021-2024

- 5.4.2 AVERAGE SELLING PRICE TREND OF VEHICLE DETECTION SENSORS, BY REGION, 2021-2024

- 5.4.3 AVERAGE SELLING PRICE OF THERMAL CAMERAS, BY KEY PLAYER, 2024

- 5.4.4 AVERAGE SELLING PRICE OF VEHICLE DETECTION SENSORS, BY KEY PLAYER, 2024

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 ECOSYSTEM ANALYSIS

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 KEY TECHNOLOGIES

- 5.7.1.1 Global navigation satellite systems

- 5.7.1.2 Automatic number plate recognition

- 5.7.2 COMPLEMENTARY TECHNOLOGIES

- 5.7.2.1 Digital twin

- 5.7.3 ADJACENT TECHNOLOGIES

- 5.7.3.1 RFID

- 5.7.1 KEY TECHNOLOGIES

- 5.8 PATENT ANALYSIS

- 5.9 TRADE ANALYSIS

- 5.9.1 IMPORT DATA (HS CODE 8530)

- 5.9.2 EXPORT DATA (HS CODE 8530)

- 5.10 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.11 CASE STUDIES

- 5.11.1 PUBLIC TRANSPORTATION IN DEHRADUN ADOPT REAL-TIME MONITORING AND DIGITAL TICKETING TO OPTIMIZE TRAVEL PATTERNS

- 5.11.2 SHENZHEN TRANSPORTATION HUBS ENHANCE SURVEILLANCE WITH ANALOG AND DIGITAL SYSTEMS

- 5.11.3 MERIDA DEPLOYS SMART CITY SOLUTIONS TO REDUCE DELAY AND IMPROVE MOBILITY WITH CUBIC'S INTELLIGENT TRAFFIC PLATFORM

- 5.11.4 EGYPT IMPLEMENTS INTELLIGENT TRANSPORT SYSTEM TO IMPROVE SAFETY, ENHANCE MOBILITY, AND REDUCE CONGESTION

- 5.12 INVESTMENT AND FUNDING SCENARIO

- 5.13 TARIFF AND REGULATORY LANDSCAPE

- 5.13.1 TARIFF ANALYSIS (HS CODE 8530)

- 5.13.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13.3 STANDARDS

- 5.14 PORTER'S FIVE FORCES ANALYSIS

- 5.14.1 THREAT OF NEW ENTRANTS

- 5.14.2 THREAT OF SUBSTITUTES

- 5.14.3 BARGAINING POWER OF SUPPLIERS

- 5.14.4 BARGAINING POWER OF BUYERS

- 5.14.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDER IN BUYING PROCESS

- 5.15.2 BUYING CRITERIA

- 5.16 IMPACT OF AI/GEN AI ON INTELLIGENT TRANSPORTATION SYSTEM MARKET

- 5.16.1 INTRODUCTION

- 5.17 IMPACT OF 2025 US TARIFF ON INTELLIGENT TRANSPORTATION SYSTEM MARKET

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 IMPACT ON COUNTRY/REGION

- 5.17.4.1 US

- 5.17.4.2 Europe

- 5.17.4.3 Asia Pacific

- 5.17.5 IMPACT ON APPLICATIONS

6 PROTOCOLS FOR INTELLIGENT TRANSPORTATION SYSTEMS

- 6.1 INTRODUCTION

- 6.2 SHORT RANGE

- 6.2.1 WAVE (IEEE 802.11)

- 6.2.2 WPAN (IEEE 802.15)

- 6.3 LONG RANGE

- 6.3.1 WIMAX (IEEE 802.11)

- 6.3.2 OFDM

- 6.4 IEEE 1512

- 6.5 TRAFFIC MANAGEMENT DATA DICTIONARY

- 6.6 OTHER PROTOCOLS

7 INTELLIGENT TRANSPORTATION SYSTEM MARKET, BY MODE

- 7.1 INTRODUCTION

- 7.2 ROADWAYS

- 7.2.1 RISING NEED FOR REAL-TIME VEHICLE TRACKING TO FOSTER MARKET GROWTH

- 7.3 RAILWAYS

- 7.3.1 INTEGRATION WITH ONBOARD DIAGNOSTICS AND CLOUD COMMUNICATION TO OFFER LUCRATIVE GROWTH OPPORTUNITIES

- 7.4 AIRWAYS

- 7.4.1 DRONE INTEGRATION INTO COMMERCIAL AIRSPACE TO FUEL MARKET GROWTH

- 7.5 MARITIME

- 7.5.1 EVOLUTION OF SMART LOGISTICS HUBS TO DRIVE MARKET

8 INTELLIGENT TRANSPORTATION SYSTEM MARKET FOR ROADWAYS, BY SYSTEM TYPE AND OFFERING

- 8.1 INTRODUCTION

- 8.2 INTELLIGENT TRANSPORTATION SYSTEM MARKET FOR ROADWAYS, BY SYSTEM TYPE

- 8.2.1 ADVANCED TRAFFIC MANAGEMENT SYSTEMS

- 8.2.1.1 Adaptive traffic signal control systems

- 8.2.1.1.1 Shift toward smart and responsive traffic ecosystems to drive market

- 8.2.1.2 Ramp metering systems

- 8.2.1.2.1 Rising emphasis on smart mobility and congestion mitigation to boost demand

- 8.2.1.3 Variable speed limit systems

- 8.2.1.3.1 Transition toward intelligent and connected infrastructure to support segmental growth

- 8.2.1.4 Incident detection systems

- 8.2.1.4.1 Increasing demand for scalable, automated, and reliable detection solutions to foster market growth

- 8.2.1.1 Adaptive traffic signal control systems

- 8.2.2 ADVANCED TRAVELER INFORMATION SYSTEMS

- 8.2.2.1 Dynamic signboards

- 8.2.2.1.1 Growing emphasis on connectivity, automation, and energy efficiency to drive market

- 8.2.2.2 Transit information systems

- 8.2.2.2.1 Global push for sustainable and integrated mobility to support market growth

- 8.2.2.3 Weather information systems

- 8.2.2.3.1 Shift toward AI-powered forecasting and edge computing capabilities to drive market

- 8.2.2.1 Dynamic signboards

- 8.2.3 TOLLING & PARKING MANAGEMENT SYSTEMS

- 8.2.3.1 Rising digital infrastructure investments to boost demand

- 8.2.4 SECURITY & SURVEILLANCE SYSTEMS

- 8.2.4.1 Growing emphasis on smart city infrastructure to drive market

- 8.2.1 ADVANCED TRAFFIC MANAGEMENT SYSTEMS

- 8.3 INTELLIGENT TRANSPORTATION SYSTEM MARKET FOR ROADWAYS, BY OFFERING

- 8.3.1 HARDWARE

- 8.3.1.1 Increasing focus on developing energy-efficient, ruggedized, and low-maintenance equipment to boost demand

- 8.3.2 SOFTWARE

- 8.3.2.1 Improved roadway efficiency and safety to fuel market growth

- 8.3.3 SERVICES

- 8.3.3.1 Shift toward cloud-based traffic management platforms and AI-powered analytics to offer lucrative growth opportunities

- 8.3.1 HARDWARE

9 INTELLIGENT TRANSPORTATION SYSTEM MARKET FOR RAILWAYS, BY SYSTEM TYPE AND OFFERING

- 9.1 INTRODUCTION

- 9.2 INTELLIGENT TRANSPORTATION SYSTEM MARKET FOR RAILWAYS, BY SYSTEM TYPE

- 9.2.1 RAIL OPERATION SYSTEMS

- 9.2.1.1 Signaling solutions

- 9.2.1.1.1 Growing emphasis on high-speed rail and urban metro networks to foster market growth

- 9.2.1.2 Control & supervision systems

- 9.2.1.2.1 Increasing demand for high-capacity and low-latency control solutions to drive market

- 9.2.1.3 Rail traffic management systems

- 9.2.1.3.1 Growing sophistication of rail traffic management platforms to boost demand

- 9.2.1.1 Signaling solutions

- 9.2.2 PASSENGER INFORMATION SYSTEMS

- 9.2.2.1 Shift toward cloud-based architectures and AI-driven analytics to support market growth

- 9.2.3 SMART TICKETING SYSTEMS

- 9.2.3.1 Increasing investments in smart city infrastructure to fuel market growth

- 9.2.4 OTHER RAILWAYS SYSTEM TYPES

- 9.2.1 RAIL OPERATION SYSTEMS

- 9.3 INTELLIGENT TRANSPORTATION SYSTEM MARKET FOR RAILWAYS, BY OFFERING

- 9.3.1 HARDWARE

- 9.3.1.1 Growing demand for high-speed rail and smart rail infrastructure to drive market

- 9.3.2 SOFTWARE

- 9.3.2.1 Reduced operational delays with data-driven and AI-enhanced software platforms to foster market growth

- 9.3.3 SERVICES

- 9.3.3.1 Growing complexity of rail networks and increasing emphasis on digital transformation to support market growth

- 9.3.1 HARDWARE

10 INTELLIGENT TRANSPORTATION SYSTEM MARKET FOR AIRWAYS, BY SYSTEM TYPE AND OFFERING

- 10.1 INTRODUCTION

- 10.2 INTELLIGENT TRANSPORTATION SYSTEM MARKET FOR AIRWAYS, BY SYSTEM TYPE

- 10.2.1 AIRCRAFT MANAGEMENT SYSTEMS

- 10.2.1.1 Air traffic control systems

- 10.2.1.1.1 Increasing complexity of manned and unmanned aircraft operations to drive market

- 10.2.1.1.2 Other aircraft management systems

- 10.2.1.1 Air traffic control systems

- 10.2.2 SECURITY & SURVEILLANCE SYSTEMS

- 10.2.2.1 Seamless integration with centralized command and control systems to drive market

- 10.2.3 SMART TICKETING SYSTEMS

- 10.2.3.1 Emphasis on modernizing global air travel systems to boost demand

- 10.2.4 INFORMATION MANAGEMENT SYSTEMS

- 10.2.4.1 Expanding ecosystem of eVTOL aircraft to support market growth

- 10.2.1 AIRCRAFT MANAGEMENT SYSTEMS

- 10.3 INTELLIGENT TRANSPORTATION SYSTEM MARKET FOR AIRWAYS, BY OFFERING

- 10.3.1 HARDWARE

- 10.3.1.1 Advancements in sensor miniaturization and edge computing to offer lucrative growth opportunities

- 10.3.2 SOFTWARE

- 10.3.2.1 Shift toward interoperable, scalable, and secure software systems to foster market growth

- 10.3.3 SERVICES

- 10.3.3.1 Increasing investments in smart airport infrastructure to boost demand

- 10.3.1 HARDWARE

11 INTELLIGENT TRANSPORTATION SYSTEM MARKET FOR MARITIME, BY SYSTEM TYPE AND OFFERING

- 11.1 INTRODUCTION

- 11.2 INTELLIGENT TRANSPORTATION SYSTEM MARKET FOR MARITIME, BY SYSTEM TYPE

- 11.2.1 AUTOMATIC IDENTIFICATION SYSTEMS

- 11.2.1.1 Shift toward autonomous navigation and digital port infrastructure to boost demand

- 11.2.2 VESSEL TRAFFIC MANAGEMENT SYSTEMS

- 11.2.2.1 Need to optimize vessel turnaround times and reduce fuel consumption to foster market growth

- 11.2.3 INFORMATION SYSTEMS

- 11.2.3.1 Rising need to implement sustainable shipping practices to foster market growth

- 11.2.4 OTHER MARITIME SYSTEM TYPES

- 11.2.1 AUTOMATIC IDENTIFICATION SYSTEMS

- 11.3 INTELLIGENT TRANSPORTATION SYSTEM MARKET FOR MARITIME, BY OFFERING

- 11.3.1 HARDWARE

- 11.3.1.1 Growing adoption of digital and automated maritime operations to drive market

- 11.3.2 SOFTWARE

- 11.3.2.1 Need to optimize maritime logistics and enhance safety to fuel market growth

- 11.3.3 SERVICES

- 11.3.3.1 Reduced operational downtime and improved safety to drive market

- 11.3.1 HARDWARE

12 INTELLIGENT TRANSPORTATION SYSTEM MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 SECURITY & SURVEILLANCE

- 12.2.1 RISING DEMAND FOR AI-POWERED SECURITY & SURVEILLANCE TO DRIVE MARKET

- 12.3 TRAFFIC MANAGEMENT

- 12.3.1 NEED TO OPTIMIZE TRAFFIC FLOW AND REDUCE CONGESTION TO FUEL MARKET GROWTH

- 12.4 INFORMATION MANAGEMENT

- 12.4.1 GROWING COMPLEXITY OF URBAN MOBILITY TO DRIVE MARKET

- 12.5 TICKETING

- 12.5.1 SHIFT TOWARD INTEGRATED MOBILITY-AS-A-SERVICE MODELS TO FUEL MARKET GROWTH

- 12.6 OTHER APPLICATIONS

13 INTELLIGENT TRANSPORTATION SYSTEM MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 13.2.2 US

- 13.2.2.1 Need to control traffic congestion and reduce pollution to boost demand

- 13.2.3 CANADA

- 13.2.3.1 Favorable government initiatives to drive market

- 13.2.4 MEXICO

- 13.2.4.1 Expanding transportation networks to offer lucrative growth opportunities

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 13.3.2 GERMANY

- 13.3.2.1 Growing emphasis on creating sustainable and future-proof transportation systems to fuel market growth

- 13.3.3 FRANCE

- 13.3.3.1 Implementation of Mobility 3.0 program to offer lucrative growth opportunities

- 13.3.4 UK

- 13.3.4.1 Growing investments to develop and deploy ITS to drive market

- 13.3.5 ITALY

- 13.3.5.1 Improved fleet management and passenger information to support market growth

- 13.3.6 SPAIN

- 13.3.6.1 Increasing emphasis on improving safety in road operations and maintenance to boost demand

- 13.3.7 BELGIUM

- 13.3.7.1 Growing demand for emission-free public transportation systems to fuel market growth

- 13.3.8 DENMARK

- 13.3.8.1 Rising adoption of EVs to offer lucrative growth opportunities

- 13.3.9 AUSTRIA

- 13.3.9.1 Increasing decarbonization efforts to drive market

- 13.3.10 SWEDEN

- 13.3.10.1 Promotion of sustainable and smart transportation initiatives to support market growth

- 13.3.11 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 13.4.2 CHINA

- 13.4.2.1 Rising need to tackle traffic congestion and pollution to fuel market growth

- 13.4.3 JAPAN

- 13.4.3.1 Growing demand for connected and autonomous vehicles to foster market growth

- 13.4.4 INDIA

- 13.4.4.1 Increasing need to boost efficiency of urban transportation networks to support market growth

- 13.4.5 SOUTH KOREA

- 13.4.5.1 Emphasis on developing smart mobility infrastructure and reducing urban congestion to support market growth

- 13.4.6 AUSTRALIA

- 13.4.6.1 Public-private collaborations to boost demand

- 13.4.7 REST OF ASIA PACIFIC

- 13.5 ROW

- 13.5.1 MACROECONOMIC OUTLOOK FOR ROW

- 13.5.2 MIDDLE EAST

- 13.5.2.1 GCC

- 13.5.2.1.1 Rising initiatives to promote sustainable mobility to drive market

- 13.5.2.2 Rest of Middle East

- 13.5.2.1 GCC

- 13.5.3 AFRICA

- 13.5.3.1 Shift toward intelligent urban mobility and sustainable transport development to boost demand

- 13.5.4 SOUTH AMERICA

- 13.5.4.1 Increasing emphasis on developing smart cities to offer lucrative growth opportunities

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020-2025

- 14.3 MARKET SHARE ANALYSIS, 2024

- 14.4 REVENUE ANALYSIS, 2020-2024

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 BRAND/PRODUCT COMPARISON

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Mode footprint

- 14.7.5.4 Offering footprint

- 14.7.5.5 Application footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

15 COMPANY PROFILES

- 15.1 INTRODUCTION

- 15.2 KEY PLAYERS

- 15.2.1 SIEMENS

- 15.2.1.1 Business overview

- 15.2.1.2 Products/Solutions/Services offered

- 15.2.1.3 Recent developments

- 15.2.1.3.1 Developments

- 15.2.1.4 MnM view

- 15.2.1.4.1 Key strengths/Right to win

- 15.2.1.4.2 Strategic choices

- 15.2.1.4.3 Weaknesses/Competitive threats

- 15.2.2 HITACHI, LTD.

- 15.2.2.1 Business overview

- 15.2.2.2 Products/Solutions/Services offered

- 15.2.2.3 Recent developments

- 15.2.2.3.1 Product launches

- 15.2.2.3.2 Deals

- 15.2.2.3.3 Other developments

- 15.2.2.4 MnM view

- 15.2.2.4.1 Key strengths/Right to win

- 15.2.2.4.2 Strategic choices

- 15.2.2.4.3 Weaknesses/Competitive threats

- 15.2.3 CUBIC CORPORATION

- 15.2.3.1 Business overview

- 15.2.3.2 Products/Solutions/Services offered

- 15.2.3.3 Recent developments

- 15.2.3.3.1 Product launches

- 15.2.3.3.2 Deals

- 15.2.3.3.3 Expansions

- 15.2.3.4 MnM view

- 15.2.3.4.1 Key strengths/Right to win

- 15.2.3.4.2 Strategic choices

- 15.2.3.4.3 Weaknesses/Competitive threats

- 15.2.4 CONDUENT INCORPORATED

- 15.2.4.1 Business overview

- 15.2.4.2 Products/Solutions/Services offered

- 15.2.4.3 Recent developments

- 15.2.4.3.1 Product launches

- 15.2.4.3.2 Other developments

- 15.2.4.4 MnM view

- 15.2.4.4.1 Key strengths/Right to win

- 15.2.4.4.2 Strategic choices

- 15.2.4.4.3 Weaknesses/Competitive threats

- 15.2.5 KAPSCH TRAFFICCOM AG

- 15.2.5.1 Business overview

- 15.2.5.2 Products/Solutions/Services offered

- 15.2.5.3 Recent developments

- 15.2.5.3.1 Product launches

- 15.2.5.3.2 Other developments

- 15.2.5.4 MnM view

- 15.2.5.4.1 Key strengths/Right to win

- 15.2.5.4.2 Strategic choices

- 15.2.5.4.3 Weaknesses/Competitive threats

- 15.2.6 THALES

- 15.2.6.1 Business overview

- 15.2.6.2 Products/Solutions/Services offered

- 15.2.6.3 Recent developments

- 15.2.6.3.1 Product launches

- 15.2.7 TELEDYNE TECHNOLOGIES INCORPORATED

- 15.2.7.1 Business overview

- 15.2.7.2 Products/Solutions/Services offered

- 15.2.7.3 Recent developments

- 15.2.7.3.1 Product launches

- 15.2.7.3.2 Deals

- 15.2.8 INDRA SISTEMAS, S.A.

- 15.2.8.1 Business overview

- 15.2.8.2 Products/Solutions/Services offered

- 15.2.8.2.1 Deals

- 15.2.9 MUNDYS

- 15.2.9.1 Business overview

- 15.2.9.2 Products/Solutions/Services offered

- 15.2.9.3 Recent developments

- 15.2.9.3.1 Product launches

- 15.2.10 VERRA MOBILITY

- 15.2.10.1 Business overview

- 15.2.10.2 Products/Solutions/Services offered

- 15.2.11 TOMTOM INTERNATIONAL BV

- 15.2.11.1 Business overview

- 15.2.11.2 Products/Solutions/Services offered

- 15.2.11.3 Recent developments

- 15.2.11.3.1 Product launches

- 15.2.1 SIEMENS

- 15.3 OTHER PLAYERS

- 15.3.1 SWARCO

- 15.3.2 ST ENGINEERING

- 15.3.3 ITERIS, INC.

- 15.3.4 Q-FREE

- 15.3.5 SERCO GROUP PLC

- 15.3.6 EFKON GMBH

- 15.3.7 LANNER ELECTRONICS

- 15.3.8 SENSYS GATSO GROUP AB

- 15.3.9 TAGMASTER

- 15.3.10 RICARDO

- 15.3.11 TRANSMAX PTY LTD.

- 15.3.12 DAKTRONICS, INC.

- 15.3.13 GEOTOLL

- 15.3.14 CELLINT

- 15.3.15 ALSTOM SA

- 15.3.16 CLEVER DEVICES LTD

- 15.3.17 ETA TRANSIT

- 15.3.18 FURUNO ELECTRIC CO., LTD

- 15.3.19 TRANSCORE

- 15.3.20 ADAPTIVE RECOGNITION INC

- 15.3.21 ECONOLITE

- 15.3.22 MIOVISION TECHNOLOGIES INCORPORATED

- 15.3.23 ELOVATE

16 APPENDIX

- 16.1 INSIGHTS FROM INDUSTRY EXPERTS

- 16.2 DISCUSSION GUIDE

- 16.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.4 CUSTOMIZATION OPTIONS

- 16.5 RELATED REPORTS

- 16.6 AUTHOR DETAILS