|

시장보고서

상품코드

2057475

스케일 방지제 시장 : 유형별, 프로세스 유형별, 용도별, 지역별 - 예측(-2031년)Antiscalants Market by Type Application (Power & Construction, Oil & Gas, Mining, Municipal Water Treatment & Desalination, Food & Beverage, Chemical & Pharmaceutical, Pulp & Paper), Process Type & Region - Global Forecast to 2031 |

||||||

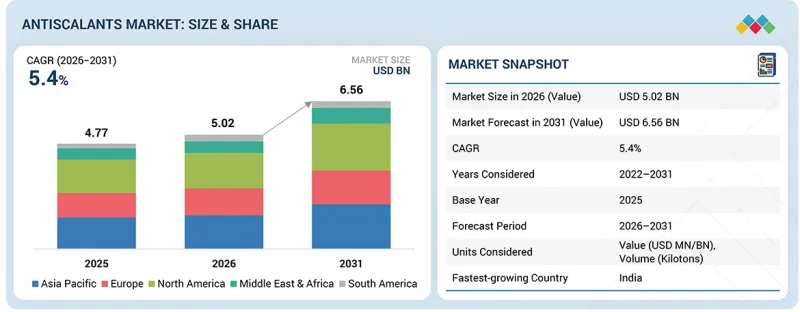

스케일 방지제 시장 규모는 2026년 50억 2,000만 달러에서 2031년까지 65억 6,000만 달러로 성장하고, 예측 기간 중 연평균 복합 성장률(CAGR)은 5.4%를 나타낼 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(100만 달러), 킬로톤 |

| 부문 | 유형별, 프로세스 유형별, 용도별, 지역별 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미 |

예측 기간 동안 이 부문은 시장에서 두 번째로 높은 성장률을 나타낼 것으로 전망됩니다. 이는 카르복실산염/탄산염계 스케일 방지제가 뛰어난 분산성을 보여, 최신 수처리 시스템에서 효과적으로 작용하기 때문입니다. 폴리머계 제제는 스케일 형성을 효과적으로 억제하고 입자 침적을 방지하기 때문에 역삼투, 해수 담수화 및 도시 용수 처리 분야에서 주요한 선택지로 자리 잡고 있습니다. 본 제품은 기존의 포스폰산염계 제품에 비해 환경 부하가 적을 뿐만 아니라, 다양한 수질 조건에서 뛰어난 성능을 발휘하여 시장 수요가 더욱 증가하고 있습니다. 지속 가능하고 친환경적인 수처리 방법에 대한 수요가 증가함에 따라, 각 산업 분야에서 카르복실산계 스케일 방지제의 도입이 확대되고 있습니다.

“유형별로 보면, 결정 개질 유형은 금액 기준으로 두 번째로 급성장하고 있는 부문입니다. '

스케일 방지제 시장은 결정 개질을 통해 가장 빠른 성장세를 보이고 있으며, 이는 두 번째로 중요한 공정 유형으로서 시장 가치를 높이고 있습니다. 이 메커니즘은 시스템의 청정도와 운영 효율을 유지하면서 침전물을 제거할 수 있는 효율적인 시스템을 통해 작동합니다. 역삼투 시스템, 냉각 시스템 및 산업용 수처리 시설에서는 운영 성능 향상과 유지보수 비용 절감이 요구됨에 따라, 결정 개질 기술의 활용이 확대되고 있습니다. 이 시스템은 다양한 수질 구성과 여러 수처리 공정에서 효과적으로 가동될 수 있어 시장 내 보급 범위를 넓혀가고 있습니다. 산업 분야에서 스케일 형성을 제어하기 위한 신뢰성 높은 첨단 기술이 개발됨에 따라, 결정 개질형 스케일 방지제에 대한 수요가 증가하고 있습니다.

“용도별로 보면, 예측 기간 동안 금액 기준으로 두 번째로 빠르게 성장하는 시장은 도시 용수 처리 및 해수 담수화입니다. '

세계적인 물 부족 현상의 심화와 식수 수요 증가로 인해, 스케일 방지제 시장은 상수도 처리 및 해수 담수화 분야에서 시장 규모 측면에서 두 번째로 빠른 성장세를 보이고 있습니다. 정부와 유틸리티자들은 물 부족에 직면한 지역에 해수 담수화 플랜트와 폐수 처리 시설을 건설하기 위해 막대한 자금을 투자하고 있습니다. 역삼투막은 스케일 방지제를 통해 필수적인 보호를 받으며, 이를 통해 시스템의 성능이 향상되는 동시에 유지 관리 비용도 절감됩니다. 엄격한 수질 규제와 배출 기준이 맞물려, 우수한 처리 기술의 도입이 촉진되고 있습니다. 도시화와 인구 증가로 인해 이 시장 부문에 대한 수요가 높아지면서, 스케일 방지제 시장은 급속히 성장하고 있습니다.

“지역별로 보면, 중동 및 아프리카은 금액 기준으로 안티스케일런트 시장에서 두 번째로 빠르게 성장하고 있는 시장입니다. '

중동 및 아프리카은 현재 스케일 방지제 시장에서 두 번째로 빠르게 성장하고 있는 지역이며, 물 부족과 식수 확보를 위해 이 지역이 해수 담수화에 의존하고 있는 점으로 인해 매출 성장이 예상됩니다. 이 지역의 각국에서는 대규모 해수 담수화 시설과 수처리 플랜트가 건설되고 있어, 막을 보호하고 시스템 성능을 향상시키는 첨단 스케일 방지제에 대한 수요가 발생하고 있습니다. 이 지역에서는 석유 및 가스 산업이 널리 전개되고 있어, 운영 시스템을 스케일 침전으로부터 보호하는 스케일 방지제에 대한 수요가 증가하고 있습니다. 시장 확대는 산업 활동의 활성화와 수자원 보전에 대한 일반 시민의 인식 제고라는 두 가지 주요 촉진요인에 힘입어 이루어지고 있습니다. 이러한 요인들로 인해, 해당 지역은 스케일 방지제 시장에서 중요한 성장 시장으로 부상했습니다.

본 보고서에서는 다음 기업 프로파일에 대한 종합적인 분석을 제공합니다.

주요 기업으로는 Dow (US), BASF SE (Germany), Ecolab (US), Solenis (US), Kemira (Finland), Clariant (Switzerland), Syensqo (Belgium), Kurita Water Industries Ltd (Japan), Veolia Group (France), and Italmatch Chemicals SPA (Italy) 등이 있습니다.

조사 범위

본 조사 보고서에서는 스케일 방지제 시장을 유형, 공정 유형, 용도 및 지역별로 분류하고 있습니다. 조사 범위에는 성장 요인, 억제요인, 과제 및 기회 등 스케일 방지제 시장의 성장에 영향을 미치는 주요 요인에 대한 상세 정보가 포함되어 있습니다. 주요 업계 기업들에 대해 철저한 조사를 수행하여, 사업 개요, 솔루션 및 서비스, 주요 전략, 계약, 파트너십, 합의에 관한 인사이트를 제공합니다. 제품 출시, 합병 및 인수, 그리고 스케일 방지제 시장의 최근 동향에 대해서도 다루고 있습니다. 본 보고서에는 스케일 방지제 시장 생태계 내에서 신생 스타트업 기업들의 경쟁 현황에 대한 분석도 포함되어 있습니다.

이 보고서를 구매해야 하는 이유:

본 보고서는 스케일 방지제 시장 전체 및 그 하위 부문의 대략적인 매출 데이터를 제공함으로써, 시장 선도 기업과 신규 진출기업을 지원합니다. 본 보고서는 이해관계자들이 경쟁 구도를 이해하고, 자사의 비즈니스를 더 유리한 위치에 놓으며, 적절한 시장 진출 전략을 수립하는 데 필요한 추가적인 인사이트를 얻는 데 도움이 됩니다. 또한, 본 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움을 주며, 주요 시장 성장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인(수처리 솔루션에 대한 수요 증가, 막 기술의 성장), 제약 요인(화학 물질 배출에 대한 환경적 우려, 대체 기술의 가용성), 기회(친환경 배합 개발, 신흥 시장에서의 확대), 그리고 과제(원자재 가격 변동, 수질별 성능 차이)에 대한 분석

- 제품 개발 및 혁신 : 스케일 방지제 시장의 향후 기술, 연구 개발 활동 및 서비스 출시와 관련된 심층적인 인사이트.

- 시장 개발: 수익성이 높은 시장에 대한 종합적인 정보. 본 보고서에서는 다양한 지역의 스케일 방지제 시장을 분석했습니다.

- 시장의 다각화 : 스케일 방지제 시장의 서비스, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁사 분석 : Dow(미국), BASF SE(독일), Ecolab(미국), Solenis(미국), Kemira(핀란드), Clariant(스위스), Syensqo(벨기에), Kurita Water Industries Ltd(일본), Veolia Group(프랑스), Italmatch Chemicals SPA(이탈리아) 등 주요 기업의 시장 점유율, 성장 전략, 서비스 제공 내용에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 기술 진보, AI의 영향, 특허, 혁신, 그리고 향후 응용

제6장 규제 상황과 지속가능성 이니셔티브

제7장 고객 현황과 구매 행동

제8장 스케일 방지제 시장(유형별)

제9장 스케일 방지제 시장(프로세스 유형별)

제10장 스케일 방지제 시장(용도별)

제11장 스케일 방지제 시장(지역별)

제12장 경쟁 구도

제13장 기업 개요

제14장 조사 방법

제15장 부록

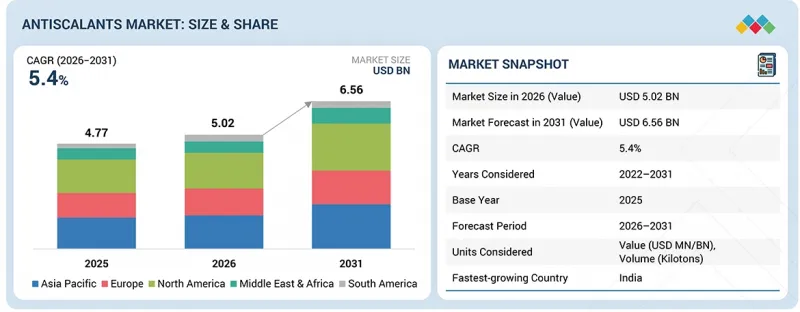

LSH 26.06.23The antiscalants market is projected to grow from USD 5.02 billion in 2026 to USD 6.56 billion by 2031, at a CAGR of 5.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million), Volume (Kilotons) |

| Segments | By Type, Process Type, Application, and Region |

| Regions covered | Europe, North America, Asia Pacific, Middle East & Africa, and South America |

The market will experience its second fastest-growing segment during the forecast period because Carboxylates/carbonates-based antiscalants demonstrate strong dispersion properties, which enable them to work effectively with modern water treatment systems. The polymer-based formulations are the primary choice for reverse osmosis, desalination, and municipal water treatment applications because they effectively control scale formation and prevent particle deposition. The product achieves better performance across different water chemistries while causing less environmental damage than conventional phosphonates, which drives stronger market demand. The growing demand for sustainable, environmentally friendly water treatment methods is driving industries to adopt carboxylate-based antiscalants.

''Based on type, crystal modification type is the second-fastest growing segment, in terms of value.''

The antiscalants market experiences its fastest growth through crystal modification, which generates increasing market value as the second most important process type. The mechanism operates through an efficient system that enables operators to eliminate deposits while maintaining system cleanliness and operational effectiveness. The growing use of crystal modification technology is seen in reverse osmosis systems, cooling systems, and industrial water treatment facilities because these systems require operational performance and reduced maintenance. The system expands its market reach because it can operate effectively across diverse water chemical compositions and various water treatment processes. The need for crystal-modification-based antiscalants is increasing as industries develop reliable, advanced methods to control scale formation.

"Based on application, municipal water treatment & desalination is the second-fastest growing market during the forecast period, in terms of value."

The antiscalants market experiences its second-most rapid growth in municipal water treatment and desalination due to rising global water shortages and increasing demand for potable drinking water. Governments and utilities make substantial financial commitments to build desalination plants and wastewater treatment facilities in areas experiencing water shortages. The reverse osmosis membranes receive essential protection from antiscalants, which also increase system performance while decreasing maintenance expenses. The strict water quality regulations, together with discharge standards, drive the implementation of superior treatment technologies. The antiscalants market experiences significant expansion because urbanization and population growth create rising demand for this market segment.

"Based on region, the Middle East & Africa is the second-fastest-growing market for antiscalants, in terms of value."

The Middle East and Africa region now ranks as the second most rapidly developing antiscalant market, which will generate revenue growth from water shortages and the region's dependence on desalination for drinking water. The countries in the region build substantial desalination facilities and water treatment plants, which create a need for advanced antiscalants that protect membranes and boost system performance. The oil and gas industry operates extensively in the region which increases the need for antiscalants that protect operational systems from scale buildup. The market expansion receives support from two main drivers which are increasing industrial activities and heightened public awareness about water preservation. The region has emerged as a significant developing market for antiscalants because of these factors.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

- By Company Type- Tier 1- 60%, Tier 2- 20%, and Tier 3- 20%

- By Designation- C Level- 33%, Director Level- 33%, and Managers- 34%

- By Region- North America- 20%, Europe- 25%, Asia Pacific- 25%, Middle East & Africa- 15%, and Latin America- 15%

The report provides a comprehensive analysis of several company profiles:

Prominent companies include Dow (US), BASF SE (Germany), Ecolab (US), Solenis (US), Kemira (Finland), Clariant (Switzerland), Syensqo (Belgium), Kurita Water Industries Ltd (Japan), Veolia Group (France), and Italmatch Chemicals SPA (Italy).

Research Coverage

This research report categorizes the antiscalants market by type, process type, application, and region. The scope of the report includes detailed information on the major factors influencing the growth of the antiscalants market, including drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted to provide insights into their business overview, solutions and services, key strategies, contracts, partnerships, and agreements. Product launches, mergers and acquisitions, and recent developments in the antiscalants market are all covered. This report includes a competitive analysis of upcoming startups in the antiscalants market ecosystem.

Reasons to buy this report:

The report will help market leaders/new entrants in this market by providing approximate revenue figures for the overall antiscalants market and its subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Rising demand for water treatment solutions, Growth of membrane-based technologies), restraints (Environmental concerns over chemical discharge, Availability of alternative technologies), opportunities (Development of eco-friendly formulations, Expansion in emerging markets), and challenges (Fluctuating raw material prices, Performance variability with water chemistry)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the antiscalants market.

- Market Development: Comprehensive information about lucrative markets-the report analyses the antiscalants market across varied regions.

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the antiscalants market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Dow (US), BASF SE (Germany), Ecolab (US), Solenis (US), Kemira (Finland), Clariant (Switzerland), Syensqo (Belgium), Kurita Water Industries Ltd (Japan), Veolia Group (France), and Italmatch Chemicals SPA (Italy), among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN ANTISCALANTS MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ANTISCALANTS MARKET

- 3.2 ANTISCALANTS MARKET, BY TYPE

- 3.3 ANTISCALANTS MARKET, BY PROCESS TYPE

- 3.4 ANTISCALANTS MARKET, BY APPLICATION

- 3.5 ANTISCALANTS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing water scarcity and growing adoption of desalination and reverse osmosis (RO) technologies

- 4.2.1.2 Increasing wastewater reuse and reclamation projects

- 4.2.1.3 Declining global availability of water, along with increasing demand for clean water

- 4.2.1.4 Stringent water treatment regulations

- 4.2.2 RESTRAINTS

- 4.2.2.1 Volatility in costs of raw materials

- 4.2.2.2 Chemical discharge risks from desalination concentrates

- 4.2.2.3 Growing shift toward green chemistry

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing use of antiscalants in oil & gas applications

- 4.2.3.2 Development of green and biodegradable antiscalants

- 4.2.3.3 Expansion of antiscalants in developing countries

- 4.2.4 CHALLENGES

- 4.2.4.1 Membrane fouling caused by antiscalants

- 4.2.4.2 High-silica and complex water chemistries

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ANTISCALANTS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

- 4.7 PORTER'S FIVE FORCES ANALYSIS

- 4.7.1 THREAT OF NEW ENTRANTS

- 4.7.2 THREAT OF SUBSTITUTES

- 4.7.3 BARGAINING POWER OF SUPPLIERS

- 4.7.4 BARGAINING POWER OF BUYERS

- 4.7.5 INTENSITY OF COMPETITIVE RIVALRY

- 4.8 VALUE CHAIN ANALYSIS

- 4.8.1 RAW MATERIAL SUPPLIERS

- 4.8.2 MANUFACTURERS

- 4.8.3 DISTRIBUTORS

- 4.8.4 END USERS

- 4.9 ECOSYSTEM ANALYSIS

- 4.10 PRICING ANALYSIS

- 4.10.1 AVERAGE SELLING PRICE OF ANTISCALANTS, BY REGION

- 4.10.2 AVERAGE SELLING PRICE OF ANTISCALANTS, BY KEY PLAYERS

- 4.10.3 AVERAGE SELLING PRICE OF ANTISCALANTS, BY TYPE

- 4.11 MACROECONOMIC INDICATORS

- 4.11.1 GLOBAL GDP TRENDS

- 4.12 IMPACT OF 2025 US TARIFFS ON ANTISCALANTS MARKET

- 4.12.1 INTRODUCTION

- 4.12.2 KEY TARIFF RATES

- 4.12.3 PRICE IMPACT ANALYSIS

- 4.12.4 IMPACT ON COUNTRIES/REGIONS

- 4.12.4.1 North America

- 4.12.4.2 Europe

- 4.12.4.3 Asia Pacific

- 4.12.5 IMPACT ON END-USE INDUSTRIES

- 4.13 TRADE ANALYSIS

- 4.13.1 IMPORT SCENARIO (HS CODE 382499)

- 4.13.2 EXPORT SCENARIO (HS CODE 382499)

- 4.14 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 4.15 INVESTMENT AND FUNDING SCENARIO

- 4.16 CASE STUDY ANALYSIS

- 4.16.1 HUBER GROUP'S USE OF TORAY RUPER ANTISCALANT

- 4.16.2 COMBATING IRON FOULING IN BRACKISH WATER RO SYSTEMS

- 4.16.3 IMPACT OF ROPUR RPI ANTISCALANT AT LOHNEN WATER PLANT

- 4.17 KEY CONFERENCES & EVENTS

5 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 5.1 TECHNOLOGY ANALYSIS

- 5.1.1 KEY TECHNOLOGIES

- 5.1.1.1 Squeeze treatment for antiscalants

- 5.1.1.2 Continuous injection systems

- 5.1.2 COMPLEMENTARY TECHNOLOGIES

- 5.1.2.1 Extended-release scale inhibitor technology

- 5.1.2.2 Biodegradable antiscalant technology

- 5.1.2.3 Dendrimer-based antiscalant technology

- 5.1.3 ADJACENT TECHNOLOGIES

- 5.1.3.1 Electrolytic technology

- 5.1.3.2 Electrochemical technology for scale inhibition

- 5.1.1 KEY TECHNOLOGIES

- 5.2 TECHNOLOGY/PRODUCT ROADMAP

- 5.2.1 SHORT-TERM (2026-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 5.2.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 5.2.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 5.3 PATENT ANALYSIS

- 5.3.1 LEGAL STATUS OF PATENTS

- 5.3.2 JURISDICTION ANALYSIS

- 5.4 FUTURE APPLICATIONS

- 5.4.1 ADVANCED DESALINATION PLANTS

- 5.4.2 WASTEWATER RECYCLING AND REUSE SYSTEMS

- 5.4.3 ZERO LIQUID DISCHARGE (ZLD) SYSTEMS

- 5.4.4 SMART INDUSTRIAL WATER TREATMENT

- 5.4.5 RENEWABLE ENERGY AND GREEN HYDROGEN PLANTS

- 5.5 IMPACT OF AI/GENERATIVE AI ON ANTISCALANTS MARKET

- 5.5.1 TOP USE CASES AND MARKET POTENTIAL

- 5.5.2 BEST PRACTICES IN ANTISCALANTS PROCESSING

- 5.5.3 CASE STUDIES OF AI IMPLEMENTATION IN ANTISCALANTS MARKET

- 5.5.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 5.5.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ANTISCALANTS MARKET

6 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 6.1 REGIONAL REGULATIONS AND COMPLIANCE

- 6.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.1.2 INDUSTRY STANDARDS

- 6.2 SUSTAINABILITY INITIATIVES

- 6.3 IMPACT OF REGULATORY POLICIES AND SUSTAINABILITY INITIATIVES

- 6.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

7 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 7.1 INTRODUCTION

- 7.2 DECISION-MAKING PROCESS

- 7.3 KEY STAKEHOLDERS AND BUYING CRITERIA

- 7.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 7.3.2 BUYING CRITERIA

- 7.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 7.5 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 7.6 MARKET PROFITABILITY

- 7.6.1 REVENUE POTENTIAL

- 7.6.2 COST DYNAMICS

- 7.6.3 MARGIN OPPORTUNITIES IN KEY END-USE SECTORS

8 ANTISCALANTS MARKET, BY TYPE

- 8.1 INTRODUCTION

- 8.2 PHOSPHONATES

- 8.2.1 EXTENSIVE UTILIZATION OF PHOSPHONATES IN WATER TREATMENT AND DESALINATION INDUSTRY TO DRIVE MARKET

- 8.3 CARBOXYLATES/CARBONATES

- 8.3.1 CONTROL OF SCALE BUILDUP IN HIGH-TEMPERATURE OIL FIELDS AND MINING OPERATIONS TO PROPEL MARKET

- 8.4 SULFONATES

- 8.4.1 USE IN OIL & GAS SECTOR FOR DOWNHOLE CHEMICAL INJECTION AND SQUEEZE OPERATION TO DRIVE MARKET

- 8.5 FLUORIDES

- 8.5.1 REMOVAL OF CHALLENGING SILICATE DEPOSITS IN INDUSTRIAL WATER SYSTEMS TO BOOST MARKET

- 8.6 OTHER TYPES

9 ANTISCALANTS MARKET, BY PROCESS TYPE

- 9.1 INTRODUCTION

- 9.2 THRESHOLD INHIBITOR

- 9.2.1 ECONOMIC ATTRACTIVENESS DUE TO LOW COST TO BOOST MARKET

- 9.3 CRYSTAL MODIFICATION

- 9.3.1 DEMAND FOR ADVANCED SOLUTIONS IN OIL & GAS, POWER GENERATION, WATER TREATMENT, AND MINING SECTORS TO DRIVE MARKET

- 9.4 DISPERSION

- 9.4.1 COMPATIBILITY WITH OTHER WATER TREATMENT CHEMICALS ENABLING INTEGRATED SOLUTIONS TO PROPEL MARKET

- 9.5 OTHER PROCESS TYPES

10 ANTISCALANTS MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 POWER & CONSTRUCTION

- 10.2.1 MAINTAINING EQUIPMENT EFFICIENCY AND LIFETIME TO DRIVE MARKET

- 10.3 MINING

- 10.3.1 MITIGATION OF SCALE DEPOSITION IN PIPELINES, DRILLING EQUIPMENT, AND PROCESSING FACILITIES TO BOOST MARKET

- 10.4 OIL & GAS

- 10.4.1 CONTINUOUS PRODUCTION AT OPTIMUM PERFORMANCE AND EFFICIENCY TO PROPEL MARKET GROWTH

- 10.5 MUNICIPAL WATER TREATMENT & DESALINATION

- 10.5.1 REDUCTION IN REQUIREMENT FOR MEMBRANE CLEANING AND OPERATIONAL COSTS TO DRIVE MARKET

- 10.6 FOOD & BEVERAGE

- 10.6.1 EFFICIENCY OF BOILERS, COOLERS, AND SINGLE- AND MULTIPLE-EFFECT EVAPORATORS TO BOOST MARKET

- 10.7 CHEMICAL & PHARMACEUTICAL

- 10.7.1 ACHIEVING OPTIMUM FLOW RATES TO ENABLE PRODUCTIVITY AND HEAT TRANSFER EFFICIENCY TO PROPEL MARKET

- 10.8 PULP & PAPER

- 10.8.1 IMPROVED PAPER QUALITY TO DRIVE MARKET

- 10.9 OTHER APPLICATIONS

- 10.9.1 TEXTILE

- 10.9.2 LEATHER TANNING

- 10.9.3 INDUSTRIAL & INSTITUTIONAL CLEANING

- 10.9.4 HOME CARE

- 10.9.5 ETHANOL PRODUCTION

- 10.9.6 AGRICULTURE

11 ANTISCALANTS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Increase in oil production activities and rising demand for potable drinking water to drive market

- 11.2.2 CANADA

- 11.2.2.1 Increase in food processing establishments to drive market

- 11.2.3 MEXICO

- 11.2.3.1 Growth of manufacturing sector to boost market

- 11.2.1 US

- 11.3 EUROPE

- 11.3.1 GERMANY

- 11.3.1.1 Maintenance of high treatment standards and environmental integrity to fuel market growth

- 11.3.2 ITALY

- 11.3.2.1 Demand from water-intensive industries to drive market

- 11.3.3 FRANCE

- 11.3.3.1 Well-developed industrial infrastructure to lead to market growth

- 11.3.4 UK

- 11.3.4.1 Government focus on sustainability to support market

- 11.3.5 SPAIN

- 11.3.5.1 Surge in demand for desalinated water to drive market

- 11.3.6 REST OF EUROPE

- 11.3.1 GERMANY

- 11.4 ASIA PACIFIC

- 11.4.1 CHINA

- 11.4.1.1 Demand from oil & gas and mining sectors to drive market

- 11.4.2 JAPAN

- 11.4.2.1 Growth of chemical & pharmaceutical industries to boost demand.

- 11.4.3 SOUTH KOREA

- 11.4.3.1 Government initiatives to promote developments in technology and manufacturing activities to boost market

- 11.4.4 INDIA

- 11.4.4.1 Consistently increasing manufacturing output to fuel market growth

- 11.4.5 REST OF ASIA PACIFIC

- 11.4.1 CHINA

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.5.2 SAUDI ARABIA

- 11.5.2.1 Government initiatives for desalinated water to boost consumption

- 11.5.3 QATAR

- 11.5.3.1 Reverse osmosis desalination for seawater to contribute to significant demand

- 11.5.4 UAE

- 11.5.4.1 Increasing demand from end-use industries to lead to significant growth

- 11.5.5 REST OF GCC COUNTRIES

- 11.5.6 REST OF MIDDLE EAST & AFRICA

- 11.6 SOUTH AMERICA

- 11.6.1 BRAZIL

- 11.6.1.1 Expanding textile industry and oil & gas exploration to drive market

- 11.6.2 ARGENTINA

- 11.6.2.1 Growing construction sector to propel market

- 11.6.3 REST OF SOUTH AMERICA

- 11.6.1 BRAZIL

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN, 2022-2026

- 12.3 REVENUE ANALYSIS, 2023-2025

- 12.4 MARKET SHARE ANALYSIS, 2025

- 12.4.1 DOW

- 12.4.2 BASF

- 12.4.3 ECOLAB

- 12.4.4 SOLENIS

- 12.4.5 KEMIRA

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- 12.6 BRAND/PRODUCT COMPARISON

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 12.7.5.1 Company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 Type footprint

- 12.7.5.4 Application footprint

- 12.7.5.5 Process type footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.2 Competitive benchmarking of start-ups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 DOW

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 MnM view

- 13.1.1.3.1 Right to win

- 13.1.1.3.2 Strategic choices

- 13.1.1.3.3 Weaknesses and competitive threats

- 13.1.2 BASF

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 MnM view

- 13.1.2.3.1 Right to win

- 13.1.2.3.2 Strategic choices

- 13.1.2.3.3 Weaknesses and competitive threats

- 13.1.3 ECOLAB

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 MnM view

- 13.1.3.3.1 Right to win

- 13.1.3.3.2 Strategic choices

- 13.1.3.3.3 Weaknesses and competitive threats

- 13.1.4 SOLENIS

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Deals

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 KEMIRA

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Deals

- 13.1.5.3.2 Expansions

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 CLARIANT

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Expansions

- 13.1.6.4 MnM view

- 13.1.7 SYENSQO

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Deals

- 13.1.7.4 MnM view

- 13.1.8 KURITA WATER INDUSTRIES LTD.

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Expansions

- 13.1.8.4 MnM view

- 13.1.9 VEOLIA GROUP

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Deals

- 13.1.9.4 MnM view

- 13.1.10 ITALMATCH CHEMICALS S.P.A.

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product launches

- 13.1.10.4 MnM view

- 13.1.1 DOW

- 13.2 OTHER PLAYERS

- 13.2.1 BIOLAB ARABIA LTD. CO.

- 13.2.2 DUBICHEM

- 13.2.3 REZA INVESTMENT COMPANY LTD.

- 13.2.4 ARIES CHEMICAL, INC.

- 13.2.5 OVIVO

- 13.2.6 AES ARABIA LTD.

- 13.2.7 SNF GROUP

- 13.2.8 ANGEL CHEMICALS PRIVATE LIMITED

- 13.2.9 HYDROVIDA

- 13.2.10 ACCEPTA WATER TREATMENT

- 13.2.11 KING LEE TECHNOLOGIES

- 13.2.12 AMERICAN WATER CHEMICALS, INC.

- 13.2.13 SHANDONG KAIRUI CHEMISTRY CO., LTD.

- 13.2.14 AXEON WATER

- 13.2.15 ACURO ORGANICS LIMITED

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.1.1 List of secondary sources

- 14.1.1.2 Key data from secondary sources

- 14.1.2 PRIMARY DATA

- 14.1.2.1 List of primary interview participants-demand and supply sides

- 14.1.2.2 Key data from primary sources

- 14.1.2.3 Breakdown of primary interviews

- 14.1.2.4 Insights from industry experts

- 14.1.1 SECONDARY DATA

- 14.2 MARKET SIZE ESTIMATION

- 14.2.1 BOTTOM-UP APPROACH

- 14.2.2 TOP-DOWN APPROACH

- 14.3 FORECAST NUMBER CALCULATION

- 14.4 DATA TRIANGULATION

- 14.5 FACTOR ANALYSIS

- 14.6 RESEARCH ASSUMPTIONS

- 14.7 RESEARCH LIMITATIONS AND RISK ASSESSMENT

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS