|

시장보고서

상품코드

1936010

의약품 여과 시장 : 제품별, 기술별, 용도별, 유형별, 사업 규모별, 최종사용자별, 지역별 - 세계 예측(-2030년)Pharmaceutical Filtration Market by Product (Membrane filter, Depth filter, Virus filter, Air Filter, Assemblies, Systems (Single-use)), Technique (Ultrafiltration), Type (Sterile), Application (API, Protein), Scale, End User - Global Forecast to 2030 |

||||||

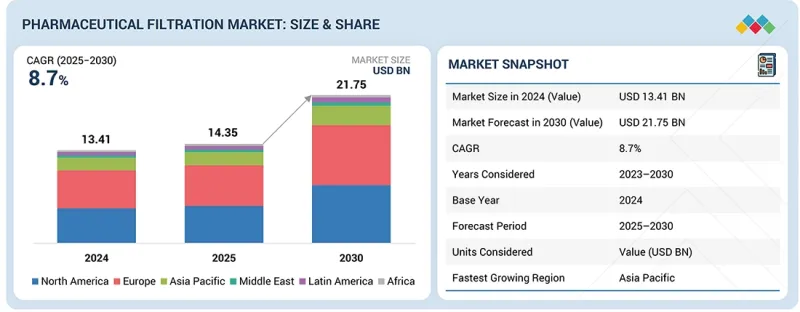

세계의 의약품 여과 시장 규모는 2025년 추정 143억 5,000만 달러에서 2030년까지 217억 5,000만 달러에 달할 것으로 예측됩니다.

2025년부터 2030년까지 연평균 성장률(CAGR)은 8.7%로 예상됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2023-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품별, 기술별, 용도별, 유형별, 사업 규모별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

의약품 여과 시장의 확대는 주로 무균 및 바이러스 안전에 대한 세계 규제 요건의 강화로 인해 촉진되었습니다. 그러나 기술적 제약이 시장 성장을 제한할 것으로 예상됩니다.

무균 여과 부문은 첨단 치료 솔루션 개발에 대한 관심 증가와 생물 의학 연구의 급속한 발전으로 인해 유형별 제약 여과 시장에서 가장 빠르게 성장하는 부문이 되었습니다. 연구 활동이 확대됨에 따라 의약품 개발 및 제조 과정에서 엄격한 무균 환경을 유지해야 할 필요성이 점점 더 중요해지고 있습니다. 이는 미생물 오염을 방지하고 제품의 무결성을 유지하며 엄격한 규제 표준을 준수하는 데 중요한 역할을 하는 무균 여과 기술의 채택을 크게 촉진하고 있습니다. 이러한 시스템은 특히 세포배양 준비, 업스트림 공정, 최종 제형화 등 다양한 생산 단계에서 바이오의약품의 품질을 보호하는 데 필수적입니다.

이 부문의 성장을 이끄는 또 다른 요인은 생물학적 제제 및 바이오시밀러의 승인 건수 증가입니다. 더 복잡하고 섬세한 생물학적 분자가 시장에 진입함에 따라 무균 보증을 손상시키지 않고 고처리량 워크플로우를 관리할 수 있는 신뢰할 수 있는 무균 여과 방법에 대한 수요가 증가하고 있습니다. 이러한 생물학적 제제는 구조적 안정성과 치료 효과를 유지하면서 미생물을 효율적으로 제거할 수 있는 강력한 여과 공정이 필요합니다.

또한, 전염병 및 새로운 건강 위협에 대한 대응 요구에 힘입어 전 세계적으로 백신 생산이 확대되면서 무균 여과에 대한 수요가 더욱 강화되고 있습니다. 백신 생산은 오염물질을 제거하고 안전하고 무균적인 최종 제품을 보장하기 위해 고성능 여과 시스템에 크게 의존하고 있습니다. 이러한 요인들이 복합적으로 작용하여 무균 여과는 제약 여과 시장에서 가장 빠르게 성장하는 분야로 자리매김하고 있습니다.

2024년에는 최종 제품 처리 부문이 응용 분야에서 가장 큰 점유율을 차지했습니다.

응용 분야별로 제약 여과 시장은 최종 제품 처리, 원료 여과, 세포 분리, 물 정화, 공기 정화 등으로 분류됩니다.

2024년, 최종 제품 처리는 제약 여과 산업에서 가장 크고 가장 빠르게 성장하는 응용 분야로 부상했습니다. 이러한 우위는 주로 의약품 제조의 최종 단계에서 제품 순도, 무균성 보장 및 오염 제어에 대한 규제 요건이 강화됨에 따라 주도되고 있습니다. 바이오의약품 분야, 특히 단클론항체, 세포 및 유전자 치료, 백신 플랫폼의 생산이 빠르게 확대되면서 고성능 여과 솔루션에 대한 수요가 크게 증가하고 있습니다. 또한, 생물학적 제제 및 바이오시밀러 생산이 꾸준히 증가함에 따라 일관된 품질과 규제 준수를 보장하기 위한 효율적이고 검증된 여과 시스템에 대한 요구가 더욱 높아지고 있습니다. 이러한 요인들이 결합되어 세계 제약 여과 시장에서 최종 제품 처리 부문의 견조한 성장 궤도를 더욱 강화하고 있습니다.

2024년 북미는 세계 의약품 여과 시장에서 가장 큰 시장 점유율을 차지했습니다.

북미는 강력한 바이오의약품 제조 생태계와 첨단 여과 기술의 신속한 도입으로 의약품 여과 시장에서 우위를 점하고 있습니다. 이 지역에는 세계 유수의 제약회사, 혁신적인 생명공학 기업, 대규모 CDMO(위탁개발생산기관)가 다수 위치하고 있으며, 이들 모두 바이오의약품, 백신, 세포 및 유전자 치료제의 생산을 지원하기 위해 고성능 여과 시스템이 필요합니다. 미국 식품의약국(FDA)의 엄격한 규제 기준은 멤브레인 기술, 무균 여과 시스템, 자동화된 품질 관리 도구의 지속적인 업그레이드를 촉진하고 있습니다. 연구개발에 대한 막대한 투자와 대규모 임상시험이 결합되어 최첨단 여과 솔루션에 대한 안정적인 수요를 뒷받침하고 있습니다. 북미는 또한 잘 구축된 제약 인프라, 숙련된 바이오 공정 기술자, 주요 여과 공급업체들의 대규모 생산능력 확장의 혜택을 누리고 있습니다. 바이오 제조의 탄력성 강화, 팬데믹 대응, 차세대 치료법을 촉진하기 위한 정부의 노력은 이 지역의 리더십을 더욱 강화하여 제약 여과 분야의 지속적인 기술 발전과 시장 성장을 보장하고 있습니다.

본 보고서에서 다룬 주요 기업 개요

제약 여과 시장의 주요 기업으로는 Merck KGaA(독일), Danaher Corporation(미국), Sartorius AG(독일), Solventum(미국), Repligen Corporation(미국), Parker Hannifin Corporation(미국),Eaton Corporation plc(아일랜드),Thermo Fisher Scientific Inc.(미국),Donaldson Company, Inc. Corporate AB(스웨덴), Corning Incorporated(미국), MANN+HUMMEL(독일), Saint-Gobain(프랑스), STERIS plc(미국), Asahi Kasei Corporation(일본).

조사 범위

본 조사 보고서는 의약품 여과 시장을 제품별, 기술별, 유형별, 용도별, 사업 규모별, 최종사용자별로 분류하고, 2030년까지 전 세계 예측을 제시하고 있습니다.

이 보고서의 조사 범위는 의약품 여과 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 저해요인, 도전과제, 기회 등)에 대한 상세한 정보를 포함하고 있습니다. 이 보고서는 주요 업계 진입기업에 대한 상세한 분석을 통해 각 기업의 사업 개요, 제품, 솔루션, 주요 전략, 제휴, 파트너십, 계약에 대한 인사이트를 제공합니다. 의약품 여과 시장과 관련된 신규 승인 및 출시, 제휴, 인수 및 최근 동향에 대해서도 다루고 있습니다.

본 보고서 구매의 주요 이점:

이 보고서는 전체 제약 여과 시장과 그 하위 부문의 수익 수치에 대한 가장 정확한 근사치를 제공함으로써 시장 리더와 신규 진입자에게 도움을 줄 수 있습니다. 또한, 이해관계자들이 경쟁 상황을 더 깊이 이해하고, 자신의 비즈니스를 적절히 포지셔닝하고, 적절한 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 이 보고서를 통해 이해관계자들은 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 기회 및 과제에 대한 정보를 얻을 수 있습니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인 분석(바이오의약품 및 바이오시밀러 개발 및 상업화 증가, 무균 및 바이러스 안전에 대한 세계 규제 요건 강화, 일회용 여과 시스템 및 어셈블리 채택 확대, 무균 및 고농도 의약품에 대한 수요 증가, 연속 생산 공정 채택), 억제요인(첨단 여과 기술 및 일회용 시스템의 높은 비용, 기술적 제약), 기회(스마트 여과와 디지털화 및 AI 기반 프로세스의 통합, 지속가능하고 친환경적인 여과 솔루션에 대한 관심 증가), 도전 과제(엄격한 규제 준수, 기술적 및 운영상의 문제, 숙련된 인력 부족)를 제공합니다.

- 제품 개발/혁신 : 제약 여과 시장의 신기술 동향, 연구개발 활동에 대한 심층 분석

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 시장을 분석합니다.

- 시장 다각화 : 미개척 지역, 최근 동향, 제약 여과 시장 투자에 대한 종합 정보

- 경쟁사 평가 : 주요 기업의 시장 점유율, 성장 전략, 제품 제공에 대한 상세한 평가. 주요 업계 진출 기업들에 대한 상세한 분석, 주요 전략, 제품 출시 및 승인 현황, 파이프라인 분석, 인수, 제휴, 계약, 협업, 기타 최근 동향, 투자 및 자금 조달 활동, 브랜드 및 제품 비교 분석, 제약 여과 시장의 벤더 평가 및 재무 지표에 대한 인사이트를 제공합니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황과 지속가능성에 관한 대처

제8장 고객 상황과 구매 행동

제9장 의약품 여과 시장(제품별)

제10장 의약품 여과 시장(기술별)

제11장 의약품 여과 시장(유형별)

제12장 의약품 여과 시장(용도별)

제13장 의약품 여과 시장(사업 규모별)

제14장 의약품 여과 시장(최종사용자별)

제15장 의약품 여과 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

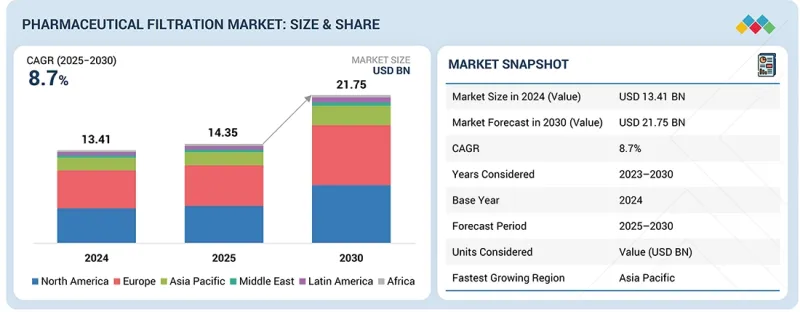

KSM 26.03.05The global pharmaceutical filtration market is projected to reach USD 21.75 billion by 2030 from an estimated USD 14.35 billion in 2025, at a CAGR of 8.7% from 2025 to 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product, Technique, Type, Application, Scale of Operation, End User. |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, the Middle East, and Africa |

The expansion of the pharmaceutical filtration market has been predominantly fueled by the tightening global regulatory expectations for sterility and viral safety. However, technological limitations are expected to restrict the market.

In 2024, sterile filtration was the fastest-growing segment in the pharmaceutical filtration market by type.

The sterile filtration segment was the fastest-growing segment in the pharmaceutical filtration market, by type, primarily because of the growing emphasis on developing advanced therapeutic solutions and the rapid progress being made in biomedical research. As research activities expand, the need to maintain strictly sterile environments during drug development and manufacturing becomes increasingly critical. This has significantly boosted the adoption of sterile filtration technologies, which play a vital role in preventing microbial contamination, preserving product integrity, and ensuring compliance with stringent regulatory standards. These systems are essential for safeguarding the quality of biopharmaceuticals at various stages of production, particularly during cell culture preparation, upstream processing, and final formulation.

Another major contributor to the segment's growth is the rising number of approvals for biologics and biosimilars. As more complex and sensitive biological molecules enter the market, demand intensifies for reliable sterile filtration methods capable of managing high-throughput workflows without compromising sterility assurance. These biologics require robust filtration processes to remove microorganisms efficiently while maintaining structural stability and therapeutic effectiveness.

Additionally, global expansion in vaccine manufacturing, driven by the need to address infectious diseases and emerging health threats, has further strengthened the demand for sterile filtration. Vaccine production heavily depends on high-performance filtration systems to eliminate contaminants and ensure safe, sterile end products. Together, these factors have firmly positioned sterile filtration as the fastest-growing segment within the pharmaceutical filtration market.

The final product processing segment reported the highest share of the application segment in 2024.

Within the application segment, the pharmaceutical filtration market is divided into final product processing, raw material filtration, cell separation, water purification, and air purification.

In 2024, final product processing emerged as both the largest and the fastest-expanding application area in the pharmaceutical filtration industry. This dominance is primarily driven by rising regulatory expectations for product purity, sterility assurance, and contamination control throughout the final stages of drug manufacturing. As the biopharmaceutical sector continues to expand rapidly, particularly in the production of monoclonal antibodies, cell- and gene-based therapies, and vaccine platforms, the need for high-performance filtration solutions has grown significantly. Additionally, the steady increase in biologics and biosimilar production has intensified the requirement for efficient and validated filtration systems to ensure consistent quality and regulatory compliance. Collectively, these factors reinforce the strong growth trajectory of the final product processing segment within the global pharmaceutical filtration market.

North America accounted for the largest market share in the global pharmaceutical filtration market in 2024.

North America maintains its dominant position in the pharmaceutical filtration market due to its strong biopharmaceutical manufacturing ecosystem and rapid adoption of advanced filtration technologies. The region hosts numerous global pharma leaders, innovative biotech firms, and large CDMOs, all of which require high-performance filtration systems to support biologics, vaccines, and cell and gene therapy production. Strict regulatory standards imposed by the FDA drive continuous upgrades in membrane technologies, sterile filtration systems, and automated quality-control tools. Significant investment in R&D, coupled with a high volume of clinical trials, supports steady demand for cutting-edge filtration solutions. North America also benefits from a well-established pharmaceutical infrastructure, skilled bioprocessing talent, and extensive capacity expansions by major filtration suppliers. Government initiatives promoting biomanufacturing resilience, pandemic preparedness, and next-generation therapies further strengthen the region's leadership, ensuring sustained technological advancement and market growth in pharmaceutical filtration.

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Supply Side-70% and Demand Side-30%

- By Designation: Managers-45%, CXO and Directors-30%, and Executives-25%

- By Region: North America-40%, Europe-25%, the Asia Pacific-25%, Latin America-5%, and the Middle East & Africa-5%

Key Companies Profiled in the Report

Key players in the Pharmaceutical filtration market include Merck KGaA (Germany), Danaher Corporation (US), Sartorius AG (Germany), Solventum (US), Repligen Corporation (US), Parker Hannifin Corporation (US), Eaton Corporation plc (Ireland), Thermo Fisher Scientific Inc. (US), Donaldson Company, Inc. (US), Porvair PLC (UK), Alfa Laval Corporate AB (Sweden), Corning Incorporated (US), MANN+HUMMEL (Germany), Saint-Gobain (France), STERIS plc (US), Asahi Kasei Corporation(Japan).

Research Coverage

This research report categorizes the Pharmaceutical Filtration Market by Product (Membrane filter, Depth filter, Virus filter, Air Filter, Assemblies, Systems [Single-use]), Technique (Ultrafiltration), Type (Sterile), Application (API, Protein), Scale, End User - Global Forecast to 2030.

The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the pharmaceutical filtration market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products, solutions, key strategies, collaborations, partnerships, and agreements. New approvals/launches, collaborations, acquisitions, and recent developments associated with the pharmaceutical filtration market.

Key Benefits of Buying the Report:

The report will help market leaders and new entrants by providing them with the closest approximations of the revenue numbers for the overall pharmaceutical filtration market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to better position their businesses and make suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide them with information on the key market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

- Analysis of key drivers (Increasing development and commercialization of biologics and biosimilars, tightening global regulatory expectations for sterility and viral safety, growing adoption of single-use filtration systems and assemblies, rising need for sterile and high-concentration drug products, and Adoption of continuous manufacturing process), restraints (High cost of advanced filtration technologies and single-use systems, technological limitations), opportunities (Integration of smart filtration with digitalization and AI-driven process and growing focus on sustainable and eco-friendly filtration solutions) and Challenges (Stringent regulatory compliance, technical and operational challenges, lack of skilled workforce).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities in the pharmaceutical filtration market

- Market Development: Comprehensive information about lucrative markets - the report analyses the market across varied regions.

- Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the pharmaceutical filtration market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players. A detailed analysis of the key industry players has been done to provide insights into their key strategies, product launches/approvals, pipeline analysis, acquisitions, partnerships, agreements, collaborations, other recent developments, investment and funding activities, brand/product comparative analysis, and vendor valuation and financial metrics of the pharmaceutical filtration market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 PHARMACEUTICAL FILTRATION MARKET OVERVIEW

- 3.2 NORTH AMERICA: PHARMACEUTICAL FILTRATION MARKET, BY TYPE & COUNTRY

- 3.3 PHARMACEUTICAL FILTRATION MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rapid growth in development and commercialization of biologics and biosimilars

- 4.2.1.2 Increasing global regulatory demands for sterility and viral safety

- 4.2.1.3 Growing adoption of single-use filtration systems & assemblies

- 4.2.1.4 Rising need for sterile, high-concentration drugs

- 4.2.1.5 Adoption of continuous manufacturing process

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost of advanced filtration technologies and single-use systems

- 4.2.2.2 Technological limitations

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Smart filtration with digitalization and innovation

- 4.2.3.2 Growing focus on sustainable and eco-friendly filtration solutions

- 4.2.4 CHALLENGES

- 4.2.4.1 Stringent regulatory compliance

- 4.2.4.2 Technical and operational challenges

- 4.2.4.3 Lack of skilled workforce

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.2.3 TRENDS IN GLOBAL PHARMACEUTICAL FILTRATION MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY PRODUCT, 2022-2024

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2024

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA FOR HS CODE 8421, 2020-2024

- 5.6.2 EXPORT DATA FOR HS CODE 8421, 2020-2024

- 5.6.3 EXPORT VOLUME FOR HS CODE 8421, 2020-2024

- 5.6.4 IMPORT VOLUME FOR HS CODE 8421, 2020-2024

- 5.7 KEY CONFERENCES & EVENTS

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT/FUNDING ACTIVITY

- 5.9.1 VC/PRIVATE EQUITY INVESTMENT TRENDS & STARTUP LANDSCAPE

- 5.10 CASE STUDY ANALYSIS

- 5.11 IMPACT OF 2025 US TARIFF ON PHARMACEUTICAL FILTRATION MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

- 5.11.5.1 Pharmaceutical & biotechnology companies

- 5.11.5.2 CROs and CDMOs/CMOs

- 5.11.5.3 Academic & research institutes

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Microfiltration

- 6.1.1.2 Ultrafiltration

- 6.1.1.3 Nanofiltration

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Electrospun microfibers

- 6.1.2.2 Photocatalytic filtration

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Chromatography

- 6.1.3.2 Microfluidics

- 6.1.1 KEY TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 PATENT ANALYSIS

- 6.3.1 TOP APPLICANTS/OWNERS (COMPANIES) FOR PHARMACEUTICAL FILTRATION PATENTS, 2014-2024

- 6.4 FUTURE APPLICATIONS

- 6.5 IMPACT OF AI/GEN AI ON PHARMACEUTICAL FILTRATION MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 CASE STUDIES OF AI IMPLEMENTATION IN PHARMACEUTICAL FILTRATION MARKET

- 6.5.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN PHARMACEUTICAL FILTRATION MARKET

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.3 CERTIFICATIONS, LABELING, & ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA, BY END USER

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 PHARMACEUTICAL FILTRATION MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 CONSUMABLES

- 9.2.1 FILTERS

- 9.2.1.1 Membrane filters

- 9.2.1.1.1 Polyethersulfone (PES)

- 9.2.1.1.1.1 Wide use of hydrophilic PES membranes in sterilizing applications to drive growth

- 9.2.1.1.2 Polyvinylidene difluoride (PVDF)

- 9.2.1.1.2.1 Nontoxic nature to increase demand for PVDF filters

- 9.2.1.1.3 Nylon

- 9.2.1.1.3.1 Increased endotoxin adsorption capacity of nylon filters to drive growth

- 9.2.1.1.4 Polytetrafluoroethylene (PTFE)

- 9.2.1.1.4.1 PTFE membrane filters offer retention of ratings as fine as 0.01μ

- 9.2.1.1.5 Mixed cellulose ester & cellulose acetate (MCE & CA)

- 9.2.1.1.5.1 MCE membranes widely used in analytical and research applications

- 9.2.1.1.6 Polycarbonate track-etched (PCTE)

- 9.2.1.1.6.1 PCTE membrane filters widely used in cell biology and analytical testing applications

- 9.2.1.1.7 Other materials

- 9.2.1.1.1 Polyethersulfone (PES)

- 9.2.1.2 Depth filters

- 9.2.1.2.1 Diatomaceous Earth

- 9.2.1.2.1.1 Increasing use in biotechnology industry for cell clarification to drive market

- 9.2.1.2.2 Cellulose

- 9.2.1.2.2.1 Cost-effectiveness of cellulose-based depth filters to drive adoption

- 9.2.1.2.3 Activated carbon

- 9.2.1.2.3.1 Widely used in pharmaceutical industry to remove range of soluble impurities from process streams containing APIs

- 9.2.1.2.4 Perlite

- 9.2.1.2.4.1 Better suited for separating coarse micro-particles from liquids with high solids loading

- 9.2.1.2.5 Other depth filter media

- 9.2.1.2.1 Diatomaceous Earth

- 9.2.1.3 Air filters

- 9.2.1.4 Virus filters

- 9.2.1.5 Other filters

- 9.2.1.1 Membrane filters

- 9.2.2 OTHER CONSUMABLES

- 9.2.2.1 FILTRATION ASSEMBLIES

- 9.2.2.1.1 Microfiltration assemblies

- 9.2.2.1.1.1 Growing demand for high-quality products to support segment growth

- 9.2.2.1.2 Ultrafiltration assemblies

- 9.2.2.1.2.1 Stringent regulatory requirements to support segment growth

- 9.2.2.1.3 Nanofiltration assemblies

- 9.2.2.1.3.1 Increasing demand for high-purity biopharmaceuticals to propel market

- 9.2.2.1.4 Other filtration assemblies

- 9.2.2.1.1 Microfiltration assemblies

- 9.2.2.2 FILTER HOLDERS

- 9.2.2.2.1 Filter holders provide structural support to membrane filters

- 9.2.2.3 FILTRATION ACCESSORIES

- 9.2.2.3.1 Increasing adoption of pharmaceutical filtration products to support growth

- 9.2.2.1 FILTRATION ASSEMBLIES

- 9.2.1 FILTERS

- 9.3 SYSTEMS

- 9.3.1 SINGLE-USE SYSTEMS

- 9.3.1.1 Reduced need for product validation and minimized cross-contamination risk to boost adoption

- 9.3.2 REUSABLE SYSTEMS

- 9.3.2.1 Widely used for large-scale manufacturing to drive adoption

- 9.3.1 SINGLE-USE SYSTEMS

10 PHARMACEUTICAL FILTRATION MARKET, BY TECHNIQUE

- 10.1 INTRODUCTION

- 10.2 MICROFILTRATION

- 10.2.1 INCREASED ADOPTION OF MICROFILTRATION TO PROPEL GROWTH

- 10.3 ULTRAFILTRATION

- 10.3.1 ADOPTION OF FINE FILTRATION TECHNIQUES TO DRIVE GROWTH

- 10.4 NANOFILTRATION

- 10.4.1 RISING DEMAND IN BIOTECHNOLOGY INDUSTRY TO SUPPORT MARKET GROWTH

- 10.5 OTHER TECHNIQUES

11 PHARMACEUTICAL FILTRATION MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.2 STERILE FILTRATION

- 11.2.1 ADVANTAGES OF STERILE FILTERS OVER NON-STERILE FILTERS TO DRIVE GROWTH

- 11.3 NON-STERILE FILTRATION

- 11.3.1 GROWTH IN PHARMA R&D ACTIVITIES TO PROPEL MARKET

12 PHARMACEUTICAL FILTRATION MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 FINAL PRODUCT PROCESSING

- 12.2.1 ACTIVE PHARMACEUTICAL INGREDIENT FILTRATION

- 12.2.1.1 Continuous requirement for API filtration to drive market

- 12.2.2 PROTEIN PURIFICATION

- 12.2.2.1 Recent advancements in protein therapeutic drugs to propel growth

- 12.2.3 VACCINE AND ANTIBODY PROCESSING

- 12.2.3.1 Development of vaccines for viral diseases to drive growth

- 12.2.4 FORMULATION AND FILLING SOLUTIONS

- 12.2.4.1 Demand for aseptic filling and bioburden reduction to propel growth

- 12.2.5 VIRAL CLEARANCE

- 12.2.5.1 Growing development of therapeutic monoclonal antibodies to drive market

- 12.2.1 ACTIVE PHARMACEUTICAL INGREDIENT FILTRATION

- 12.3 RAW MATERIAL FILTRATION

- 12.3.1 MEDIA AND BUFFER FILTRATION

- 12.3.1.1 Growth in manufacturing of biopharmaceuticals to drive market

- 12.3.2 PREFILTRATION

- 12.3.2.1 Membrane fouling issues to drive growth

- 12.3.3 BIOBURDEN TESTING

- 12.3.3.1 Strict quality control of biopharmaceuticals to drive growth

- 12.3.1 MEDIA AND BUFFER FILTRATION

- 12.4 CELL SEPARATION

- 12.4.1 GROWTH IN PERSONALIZED MEDICINE AND CELL THERAPIES TO PROPEL MARKET

- 12.5 WATER PURIFICATION

- 12.5.1 REQUIREMENT IN RESEARCH AND FORMULATION TO DRIVE MARKET

- 12.6 AIR PURIFICATION

- 12.6.1 INCREASING ADOPTION OF GMP PRACTICES TO DRIVE GROWTH

13 PHARMACEUTICAL FILTRATION MARKET, BY SCALE OF OPERATION

- 13.1 INTRODUCTION

- 13.2 MANUFACTURING-SCALE

- 13.2.1 GROWTH IN BIOLOGICS AND BIOSIMILARS MANUFACTURING TO DRIVE MARKET

- 13.3 PILOT-SCALE

- 13.3.1 INCREASED OUTSOURCING OF PILOT-SCALE BIOPROCESS DEVELOPMENT TO DRIVE MARKET

- 13.4 R&D-SCALE

- 13.4.1 INCREASING INVESTMENTS IN R&D OF BIOLOGICS TO PROPEL GROWTH

14 PHARMACEUTICAL FILTRATION MARKET, BY END USER

- 14.1 INTRODUCTION

- 14.2 PHARMACEUTICAL & BIOPHARMACEUTICAL COMPANIES

- 14.2.1 GROWING BIOLOGICS PRODUCTION TO PROPEL DEMAND

- 14.3 CROS & CMOS

- 14.3.1 GROWTH IN PHARMA R&D ACTIVITIES TO DRIVE MARKET

- 14.4 ACADEMIC & RESEARCH INSTITUTES

- 14.4.1 RISING DEMAND FOR LABORATORY FILTRATION ACROSS CROS AND RESEARCH INSTITUTES TO PROPEL MARKET

15 PHARMACEUTICAL FILTRATION MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 NORTH AMERICA: MACROECONOMIC ANALYSIS

- 15.2.2 US

- 15.2.2.1 US to dominate North America market during forecast period

- 15.2.3 CANADA

- 15.2.3.1 Growing government support for expanding biologics manufacturing facilities to support market growth

- 15.3 EUROPE

- 15.3.1 EUROPE: MACROECONOMIC ANALYSIS

- 15.3.2 GERMANY

- 15.3.2.1 Growing pharmaceutical R&D and manufacturing to drive market

- 15.3.3 UK

- 15.3.3.1 Increased awareness of drug quality led to greater use of filtration products in drug discovery laboratories

- 15.3.4 FRANCE

- 15.3.4.1 Government investment in pharmaceutical industry to drive growth

- 15.3.5 ITALY

- 15.3.5.1 Investment in biotechnology R&D to boost market growth

- 15.3.6 SPAIN

- 15.3.6.1 Expansion of biomanufacturing facilities to support market growth

- 15.3.7 SWITZERLAND

- 15.3.7.1 Presence of key pharmaceutical and biopharmaceutical companies to support market growth

- 15.3.8 REST OF EUROPE

- 15.4 ASIA PACIFIC

- 15.4.1 ASIA PACIFIC: MACROECONOMIC ANALYSIS

- 15.4.2 CHINA

- 15.4.2.1 China to dominate Asia Pacific market during forecast period

- 15.4.3 JAPAN

- 15.4.3.1 Stringent regulatory guidelines to create need for advanced filtration products

- 15.4.4 INDIA

- 15.4.4.1 Favorable scenario for foreign direct investment to favor market growth

- 15.4.5 SOUTH KOREA

- 15.4.5.1 Increased export of drugs to support market growth

- 15.4.6 AUSTRALIA

- 15.4.6.1 Increasing demand for innovative filtration solutions to propel market

- 15.4.7 REST OF ASIA PACIFIC

- 15.5 LATIN AMERICA

- 15.5.1 LATIN AMERICA: MACROECONOMIC ANALYSIS

- 15.5.2 BRAZIL

- 15.5.2.1 Increased government investments in pharmaceutical R&D to drive market

- 15.5.3 MEXICO

- 15.5.3.1 Rising demand for chronic disease treatment to support market growth

- 15.5.4 REST OF LATIN AMERICA

- 15.6 MIDDLE EAST

- 15.6.1 MIDDLE EAST: MACROECONOMIC ANALYSIS

- 15.6.2 GCC COUNTRIES

- 15.6.2.1 Saudi Arabia

- 15.6.2.1.1 Growing healthcare expenditure to boost market growth

- 15.6.2.2 UAE

- 15.6.2.2.1 Adoption of more efficient and precise filtration processes to aid market growth

- 15.6.2.3 Rest of GCC Countries

- 15.6.2.1 Saudi Arabia

- 15.6.3 REST OF MIDDLE EAST

- 15.7 AFRICA

- 15.7.1 AFRICA: MACROECONOMIC ANALYSIS

16 COMPETITIVE LANDSCAPE

- 16.1 INTRODUCTION

- 16.2 STRATEGIES ADOPTED BY KEY PLAYERS

- 16.3 REVENUE SHARE ANALYSIS

- 16.4 MARKET SHARE ANALYSIS

- 16.5 COMPANY EVALUATION MATRIX: KEY PLAYERS

- 16.5.1 STARS

- 16.5.2 EMERGING LEADERS

- 16.5.3 PERVASIVE PLAYERS

- 16.5.4 PARTICIPANTS

- 16.5.5 COMPETITIVE BENCHMARKING: KEY PLAYERS, 2024

- 16.5.5.1 Company footprint

- 16.5.5.2 Product footprint

- 16.5.5.3 Technique footprint

- 16.5.5.4 Application footprint

- 16.5.5.5 Regional footprint

- 16.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES

- 16.6.1 PROGRESSIVE COMPANIES

- 16.6.2 RESPONSIVE COMPANIES

- 16.6.3 DYNAMIC COMPANIES

- 16.6.4 STARTING BLOCKS

- 16.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 16.6.5.1 Detailed list of key startups/SMEs, 2024

- 16.6.5.2 Competitive benchmarking of key startups/SMEs, 2024

- 16.7 VALUATION AND FINANCIAL METRICS OF PHARMACEUTICAL FILTRATION VENDORS

- 16.8 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 16.8.1 BRAND/PRODUCT COMPARATIVE ANALYSIS, BY PRODUCT

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 MERCK KGAA

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Expansions

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 DANAHER CORPORATION

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Deals

- 17.1.2.3.3 Expansions

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 SARTORIUS AG

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches

- 17.1.3.3.2 Deals

- 17.1.3.3.3 Expansions

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses and competitive threats

- 17.1.4 SOLVENTUM

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches

- 17.1.4.3.2 Deals

- 17.1.4.3.3 Other developments

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 PARKER HANNIFIN CORPORATION

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 MnM view

- 17.1.5.3.1 Key strengths

- 17.1.5.3.2 Strategic choices

- 17.1.5.3.3 Weaknesses and competitive threats

- 17.1.6 REPLIGEN CORPORATION

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches

- 17.1.6.3.2 Deals

- 17.1.7 EATON CORPORATION PLC

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches

- 17.1.8 THERMO FISHER SCIENTIFIC, INC.

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Deals

- 17.1.8.3.2 Expansions

- 17.1.9 DONALDSON COMPANY, INC.

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Deals

- 17.1.9.3.2 Expansions

- 17.1.10 PORVAIR PLC

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches

- 17.1.11 ALFA LAVAL CORPORATE AB

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Product launches

- 17.1.12 CORNING INCORPORATED

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.13 MANN+HUMMEL

- 17.1.13.1 Business overview

- 17.1.13.2 Products offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Deals

- 17.1.14 SAINT-GOBAIN

- 17.1.14.1 Business overview

- 17.1.14.2 Products offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Product launches

- 17.1.14.3.2 Expansions

- 17.1.15 STERIS PLC

- 17.1.15.1 Business overview

- 17.1.15.2 Products offered

- 17.1.16 ASAHI KASEI CORPORATION

- 17.1.16.1 Business overview

- 17.1.16.2 Products offered

- 17.1.16.3 Recent developments

- 17.1.16.3.1 Product launches

- 17.1.16.3.2 Deals

- 17.1.16.3.3 Expansions

- 17.1.1 MERCK KGAA

- 17.2 OTHER PLAYERS

- 17.2.1 MEISSNER FILTRATION PRODUCTS, INC.

- 17.2.2 AMAZON FILTERS LTD.

- 17.2.3 GRAVER TECHNOLOGIES, LLC

- 17.2.4 MMS AG

- 17.2.5 ERTELALSOP

- 17.2.6 KASAG SWISS AG

- 17.2.7 FREUDENBERG FILTRATION TECHNOLOGIES SE & CO. KG

- 17.2.8 ANTYLIA SCIENTIFIC

- 17.2.9 FILTROX AG

- 17.2.10 MEMBRANE SOLUTIONS

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.2 PRIMARY DATA

- 18.2 MARKET ESTIMATION METHODOLOGY

- 18.2.1 MARKET SIZE ESTIMATION

- 18.2.2 INSIGHTS OF PRIMARY EXPERTS

- 18.2.3 TOP-DOWN APPROACH

- 18.3 MARKET GROWTH RATE PROJECTIONS

- 18.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 18.5 RESEARCH ASSUMPTIONS

- 18.6 RESEARCH LIMITATIONS

- 18.7 RISK ANALYSIS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS