|

시장보고서

상품코드

1775083

지형공간 영상 분석 시장 : 용도별, 데이터 모달리티별, 데이터 소스별, 제공별, 업계별, 지역별 - 예측(-2030년)Geospatial Imagery Analytics Market by Offering (Image Processing, Object Tracking, Change Detection), Data Source (Satellite Imagery, SAR, UAV/Drones), Application (Disaster Management, Precision Farming, Urban Planning) - Global Forecast to 2030 |

||||||

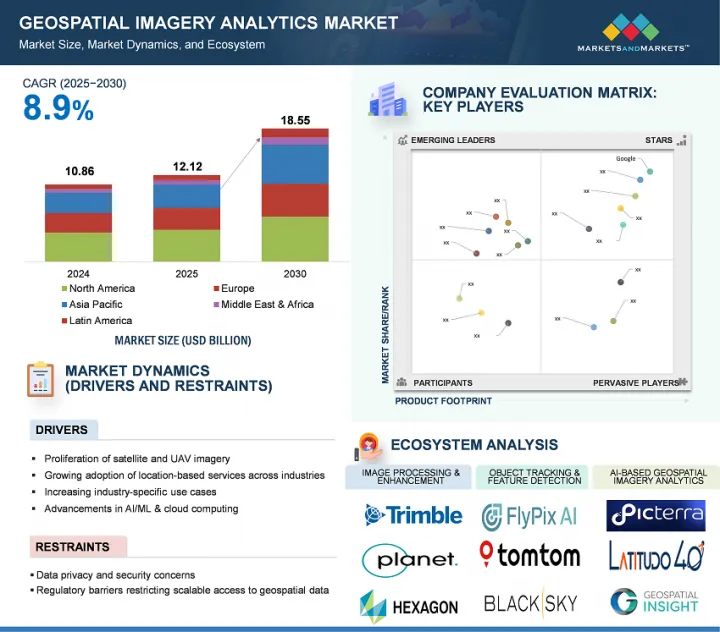

지형공간 영상 분석 시장 규모는 예측 기간 동안 8.9%의 CAGR로 확대되어 2025년 121억 2,000만 달러에서 2030년에는 185억 5,000만 달러로 성장할 것으로 예측됩니다.

이 시장은 농업, 국방, 도시 계획, 재난 관리 등의 분야에서 위성 및 드론 기반 영상 처리에 대한 수요가 증가하고 있으며, AI와 머신러닝의 혁신으로 이미지 해석이 강화되어 보다 빠르고 정확한 의사결정을 내릴 수 있게 되면서 견고한 성장세를 보이고 있습니다. 정부와 민간 기업은 인프라 모니터링, 기후 분석, 보안 감시를 위해 지형공간 데이터에 대한 의존도를 높이고 있습니다. 클라우드 통합과 실시간 분석은 사용 편의성과 확장성을 더욱 확대합니다. 그러나 시장은 높은 초기 투자 비용, 신흥국 지역의 고해상도 데이터에 대한 접근성 제한, 상시 모니터링 및 지리적 공간 추적과 관련된 프라이버시 우려 증가 등의 제약 요인에 직면해 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2020-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 달러(100만 달러) |

| 부문 | 용도별, 데이터 모달리티별, 데이터 소스별, 제공별, 업계별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

지속가능성, 재해 대책, 기후 복원력에 대한 전 세계의 관심이 높아짐에 따라 지형공간 영상 분석 시장에서는 환경 모니터링 및 기후변화 분야가 용도별로 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 정부, NGO, 국제기구는 삼림 벌채, 빙하 융해, 해수면 상승과 같은 환경 변화를 정확하게 추적할 수 있는 기술에 많은 투자를 하고 있습니다. 지형공간 영상은 지속적으로 넓은 지역을 커버하기 때문에 빠르게 진화하는 생태계의 상황을 실시간으로 파악할 수 있습니다. 또한, 환경 규제 강화와 기후변화 협약으로 인해 데이터에 기반한 집행과 보고의 필요성이 증가하고 있습니다. 이러한 고유한 요구가 이 특정 응용 분야의 성장을 가속화하고 있습니다.

실시간 위험 평가, 사기 탐지, 효율적인 보험금 청구 관리에 대한 수요가 증가함에 따라 보험 산업은 예측 기간 동안 지형공간 영상 분석 시장에서 가장 빠르게 성장할 것으로 예상됩니다. 위성 및 드론 이미지를 포함한 지리공간 데이터를 통해 보험사는 재산 상태, 재해 영향, 환경적 위험을 보다 정확하게 평가할 수 있습니다. 기후 관련 이벤트가 빈번하게 발생함에 따라 보험사들은 손실을 줄이고 업무를 간소화하기 위해 고도의 분석에 눈을 돌리고 있습니다. 또한, AI 및 머신러닝과 같은 기술은 이미지 해석을 더욱 강화하여 지리적 공간 솔루션을 인수 및 포트폴리오 모니터링에 매우 매력적으로 만들고 있습니다. 보험 업계의 디지털 전환에 대한 규제 당국의 지원도 이러한 성장에 힘을 실어주고 있으며, 보험 업계는 지리적 공간 분석 도구의 주요 채택자로 자리매김하고 있습니다.

아시아태평양은 신흥 기술 채택 증가, 인프라 투자 증가, 스마트 시티 및 디지털 전환을 추진하려는 정부의 노력으로 인해 지형공간 영상 분석 시장에서 가장 빠른 성장을 보일 것으로 예측됩니다. 중국, 인도, 일본, 한국 등의 국가에서는 도시계획, 농업, 재난관리, 국방 등에 지형공간 기술을 활용하고 있습니다. 이 지역에서는 스마트폰, 위성 서비스, 드론의 보급으로 데이터 수집 능력이 향상되고, 인공지능(AI)과 클라우드 컴퓨팅의 발전으로 실시간 분석과 실용적인 인사이트를 촉진하고 있습니다. 기술 스타트업의 성장과 민관 협력도 업계 전반의 기술 혁신에 박차를 가하고 있으며, 이는 이 지역의 시장 확대를 더욱 가속화시키고 있습니다.

한편, 북미는 지형공간 기술의 조기 도입과 대기업의 강력한 존재감으로 시장 규모에서 선두를 유지하고 있습니다. 미국과 캐나다는 국방, 환경 모니터링, 교통, 보험 등을 지원하는 인프라가 잘 구축된 성숙한 시장입니다. 특히 NASA와 USGS와 같은 기관을 통한 정부 지원과 민간 부문의 투자가 이 지역의 리더십을 뒷받침하고 있습니다. 또한, 고도의 기술 통합과 부문을 초월한 고도의 분석에 대한 수요는 시장의 지속적인 우위를 보장하고 있습니다. 아시아태평양 시장이 빠르게 성장하는 동안 북미는 기술 성숙도, 탄탄한 사용자 기반, 일관된 기술 혁신으로 시장 주도권을 유지하고 있습니다.

세계의 지형공간 영상 분석 시장에 대해 조사했으며, 용도별, 데이터 모달리티별, 데이터 소스별, 제공별, 산업별, 지역별 동향, 시장 진입 기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요와 업계 동향

- 소개

- 시장 역학

- 2025년 미국 관세의 영향 - 지형공간 영상 분석 시장

- 지형공간 영상 분석 시장의 진화

- 공급망 분석

- 생태계 분석

- 투자 상황과 자금 조달 시나리오

- 생성형 AI가 지형공간 영상 분석 시장에 미치는 영향

- 사례 연구 분석

- 기술 분석

- 규제 상황

- 특허 분석

- 가격 분석

- 주요 회의와 이벤트(2025-2026년)

- Porter's Five Forces 분석

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 주요 이해관계자와 구입 기준

제6장 지형공간 영상 분석 시장(용도별)

- 소개

- 감시·모니터링

- 환경 모니터링·기후변화

- 토지 이용·토지 피복(LULC) 분류

- 자산·인프라 관리

- 보험 리스크 평가·청구 검증

- 재해 관리·긴급 대응

- 정밀농업·작물 모니터링

- 도시 계획·스마트 시티 디자인

- 타겟 검출·전략 정보

- 공급망·물류 모니터링

- 질병 발생 추적·자원 배분

- 소매점포 입지 선정과 소비자 발자국 매핑

- 기타

제7장 지형공간 영상 분석 시장(데이터 모달리티별)

- 소개

- 이미지 기반

- 비디오 기반

- 멀티모달

제8장 지형공간 영상 분석 시장(데이터 소스별)

- 소개

- 위성 영상

- 합성 개구 레이더(SAR)

- 항공사진

- 무인항공기/드론

- GIS 및 매핑 플랫폼

- 기타

제9장 지형공간 영상 분석 시장(제공별)

- 소개

- 소프트웨어

- 서비스

제10장 지형공간 영상 분석 시장(업계별)

- 소개

- 보험

- 농업

- 건설·부동산

- 광업

- 헬스케어·생명과학

- 에너지·유틸리티

- 정부·방위

- 통신

- 운송·물류

- 미디어·엔터테인먼트

- 기타

제11장 지형공간 영상 분석 시장(지역별)

- 소개

- 북미

- 북미 : 지형공간 영상 분석 시장 성장 촉진요인

- 북미 : 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽 : 지형공간 영상 분석 시장 성장 촉진요인

- 유럽 : 거시경제 전망

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 아시아태평양 : 지형공간 영상 분석 시장 성장 촉진요인

- 아시아태평양 : 거시경제 전망

- 중국

- 일본

- 인도

- 한국

- 호주와 뉴질랜드

- ASEAN

- 기타

- 중동 및 아프리카

- 중동 및 아프리카 : 지형공간 영상 분석 시장 성장 촉진요인

- 중동 및 아프리카 : 거시경제 전망

- 사우디아라비아(KSA)

- 아랍에미리트

- 카타르

- 이스라엘

- 남아프리카공화국

- 기타

- 라틴아메리카

- 라틴아메리카 : 지형공간 영상 분석 시장 성장 촉진요인

- 라틴아메리카 : 거시경제 전망

- 브라질

- 멕시코

- 아르헨티나

- 기타

제12장 경쟁 구도

- 개요

- 주요 진출 기업의 전략/강점, 2022-2025년

- 매출 분석, 2020-2024년

- 시장 점유율 분석, 2024년

- 제품 비교 분석

- 기업 평가와 재무 지표

- 기업 평가 매트릭스 : 주요 진출 기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 경쟁 시나리오와 동향

제13장 기업 개요

- 소개

- 주요 진출 기업

- IBM

- HEXAGON AB

- TOMTOM

- MAXAR TECHNOLOGIES

- TRIMBLE

- CALIPER CORPORATION

- PLANET LABS

- ESRI

- L3HARRIS TECHNOLOGIES

- ORACLE

- NV5 GEOSPATIAL

- RMSI

- MAPLARGE

- FUGRO

- BLACKSKY

- NEARMAP

- SUPERMAP

- 스타트업/중소기업

- EARTHDAILY ANALYTICS

- SPARKGEO

- ORBICA

- CARTO

- MAPBOX

- BLUE SKY ANALYTICS

- LATITUDO40

- ECOPIA.AI

- EOS DATA ANALYTICS

- CATALYST

- SPACEKNOW

- FLYPIX AI

- PICTERRA

- GEOSPATIAL INSIGHT

- UP42

- SIMULARITY

- CAPELLA SPACE

제14장 인접 시장과 관련 시장

제15장 부록

ksm 25.07.29The geospatial imagery analytics market is projected to grow from USD 12.12 billion in 2025 to USD 18.55 billion by 2030 at a CAGR of 8.9% during the forecast period. The market is experiencing robust growth, driven by rising demand for satellite and drone-based imaging across sectors such as agriculture, defense, urban planning, and disaster management. Innovations in AI and machine learning have enhanced image interpretation, enabling faster, more precise decision-making. Governments and private enterprises increasingly rely on geospatial data for infrastructure monitoring, climate analysis, and security surveillance. Cloud integration and real-time analytics further expand usability and scalability. However, the market faces restraints, including high initial investment costs, limited access to high-resolution data in developing regions, and growing privacy concerns related to constant surveillance and geospatial tracking.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | USD (Million) |

| Segments | Offering, Data Modality, Data Source, Application, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

"Environmental monitoring & climate change application segment expected to account for the largest market share during the forecast period"

The environmental monitoring and climate change segment is projected to have the largest market share by application in the geospatial imagery analytics market due to the increasing global focus on sustainability, disaster preparedness, and climate resilience. Governments, NGOs, and international bodies are investing heavily in technologies that can track environmental changes with precision, such as deforestation, melting ice caps, and rising sea levels. Geospatial imagery provides continuous, wide-area coverage, enabling real-time insights into rapidly evolving ecological conditions. Moreover, stricter environmental regulations and climate agreements have amplified the need for data-driven enforcement and reporting. These unique needs are accelerating growth in this specific application segment.

"Insurance vertical segment expected to register the fastest growth rate during the forecast period"

The insurance vertical is poised to experience the fastest growth in the geospatial imagery analytics market during the forecast period due to increasing demand for real-time risk assessment, fraud detection, and efficient claims management. Geospatial data, including satellite and drone imagery, enables insurers to assess property conditions, disaster impact, and environmental risks with greater precision. As climate-related events become more frequent, insurers are turning to advanced analytics to mitigate losses and streamline operations. Additionally, technologies like AI and machine learning further enhance image interpretation, making geospatial solutions highly attractive for underwriting and portfolio monitoring. Regulatory support for digital transformation in insurance also drives this growth, positioning the sector as a key adopter of geospatial analytics tools.

"Asia Pacific market projected to witness rapid growth fueled by innovation and emerging technologies, while North America leads in market size"

Asia Pacific is expected to witness the fastest growth in the geospatial imagery analytics market due to the rising adoption of emerging technologies, increasing investments in infrastructure, and government initiatives promoting smart cities and digital transformation. Countries such as China, India, Japan, and South Korea are leveraging geospatial technologies for urban planning, agriculture, disaster management, and defense. The proliferation of smartphones, satellite services, and drones in the region enhances data collection capabilities, while advancements in artificial intelligence (AI) and cloud computing drive real-time analytics and actionable insights. Growing tech startups and public-private collaborations are also fueling innovation across industries, further accelerating market expansion in the region.

Conversely, North America continues to lead in market size due to the early adoption of geospatial technologies and the strong presence of major players. The US and Canada have mature markets with well-established infrastructure supporting defense, environmental monitoring, transportation, and insurance applications. Government support, especially through organizations like NASA and the USGS, alongside private sector investment, underpins the region's leadership. Additionally, a high level of technological integration and demand for advanced analytics across sectors ensures sustained market dominance. While the Asia Pacific market grows rapidly, North America maintains its market leadership due to technological maturity, an established user base, and consistent innovation.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the geospatial imagery analytics market.

- By Company: Tier I - 35%, Tier II - 44%, and Tier III - 21%

- By Designation: C Level - 50%, Director Level - 30%, and others - 20%

- By Region: North America - 30%, Europe - 30%, Asia Pacific - 25%, Middle East & Africa - 10%, and Latin America - 5%

The report includes the study of key players offering geospatial imagery analytics solutions and services. It profiles major vendors in the geospatial imagery analytics market. The major market players include Google (US), IBM (US), Hexagon AB (Sweden), TomTom (Netherlands), Maxar Technologies (US), Trimble (US), Oracle (US), ESRI (US), RMSI (India), Furgo (Netherlands), Planet Labs (US), BlackSky (US), L3Harris Technologies (US), Mapbox (US), Carto (US), SuperMap (China), NV5 Geospatial (US), Nearmap (Australia), Caliper Corporation (US), EOS Data Analytics (US), Sparkgeo (Canada), Orbica (New Zealand), Blue Sky Analytics (Netherlands), Latitude 40 (Italy), Ecopia.AI (Canada), Catalyst (Canada), SpaceKnow (US), Flypix AI (Germany), Picterra (Switzerland), Geospatial Insight (UK), UP42 (Germany), Simularity (US), MapLarge (US), EarthDaily Analytics (Canada), and Capella Space (US).

Research Coverage

This research report covers the geospatial imagery analytics market, which has been segmented based on offering, data modality, data source, and vertical. The offering segment consists of software and services. The software segment contains software by functionality (image processing & enhancement, object tracking & feature detection, change detection & time-series analysis, predictive modeling & pattern recognition, and AI-based geospatial imagery analytics, and others (anomaly detection and stream analytics)) and software by deployment mode (cloud and on-premises). The services segment consists of professional services (consulting & advisory, deployment & integration, and support & maintenance) and managed services. The data modality segment includes image-based analytics, video-based analytics, and multimodal analytics. The data source segment consists of satellite imagery, synthetic aperture radar (SAR), aerial imagery, UAV/drones, GIS & mapping platforms, and others (crowdsourced imagery and balloon-based systems). The application segment includes surveillance & monitoring, environmental monitoring & climate change, land use & land cover (LULC) classification, asset & infrastructure management, insurance risk assessment & claims validation, disaster management & emergency response, precision farming & crop monitoring, urban planning, smart cities & infrastructure, target detection & strategic intelligence, supply chain & logistics monitoring, disease outbreak tracking & resource allocation, retail site selection & consumer footfall mapping, and other applications (site preservation & monitoring and media & audience mapping, and telecommunications network planning). The vertical segment consists of insurance, agriculture, construction & real estate, mining, healthcare and life sciences, energy & utilities, government & defense, telecommunications, transportation & logistics, media and entertainment, and other verticals (banking & financial services, retail & ecommerce, and manufacturing). The regional analysis of the geospatial imagery analytics market covers North America, Europe, Asia Pacific, the Middle East & Africa (MEA), and Latin America. The report also contains a detailed analysis of investment & funding scenarios, case studies, regulatory landscape, ecosystem analysis, supply chain analysis, pricing analysis, and technology analysis.

Key Benefits of Buying the Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall geospatial imagery analytics market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Proliferation of Satellite and UAV Imagery, Growing adoption of location-based services across industries, increasing Industry-Specific Use Cases, Advancements in AI/ML & Cloud Computing), restraints (Data Privacy and Security Concerns, Regulatory and Airspace Constraints, Complexities in integration and standardization of geospatial data), opportunities (Climate Monitoring and ESG Reporting, Expansion of Commercial Satellite Constellations, Customization and On-Demand Analytics Services), and challenges (Temporal and Spatial Resolution Tradeoffs, Quality and Accuracy Variability).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the geospatial imagery analytics market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the geospatial imagery analytics market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the geospatial imagery analytics market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Google (US), IBM (US), Hexagon AB (Sweden), TomTom (Netherlands), Maxar Technologies (US), Trimble (US), Oracle (US), ESRI (US), RMSI (India), Furgo (Netherlands), Planet Labs (US), BlackSky (US), L3Harris Technologies (US), Mapbox (US), Carto (US), SuperMap (China), NV5 Geospatial (US), Nearmap (Australia), Caliper Corporation (US), EOS Data Analytics (US), Sparkgeo (Canada), Orbica (New Zealand), Blue Sky Analytics (Netherlands), Latitude 40 (Italy), Ecopia.AI (Canada), Catalyst (Canada), SpaceKnow (US), Flypix AI (Germany), Picterra (Switzerland), Geospatial Insight (UK), UP42 (Germany), Simularity (US), MapLarge (US), EarthDaily Analytics (Canada), Capella Space (US) among others in the geospatial imagery analytics market. The report also helps stakeholders understand the pulse of the geospatial imagery analytics market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION AND SCOPE

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primary profiles

- 2.1.2.2 Key industry insights

- 2.2 MARKET BREAKUP AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 STUDY LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN GEOSPATIAL IMAGERY ANALYTICS MARKET

- 4.2 GEOSPATIAL IMAGERY ANALYTICS MARKET: TOP THREE APPLICATIONS

- 4.3 NORTH AMERICA: GEOSPATIAL IMAGERY ANALYTICS MARKET, BY SOFTWARE FUNCTIONALITY AND VERTICAL

- 4.4 GEOSPATIAL IMAGERY ANALYTICS MARKET, BY REGION

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Proliferation of satellite and UAV imagery

- 5.2.1.2 Growing adoption of location-based services across industries

- 5.2.1.3 Increasing industry-specific use cases

- 5.2.1.4 Advancements in AI/ML & cloud computing

- 5.2.2 RESTRAINTS

- 5.2.2.1 Data privacy and security concerns

- 5.2.2.2 Regulatory barriers restricting scalable access to geospatial data

- 5.2.2.3 Complexities in integration and standardization of geospatial data

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Climate monitoring and ESG reporting

- 5.2.3.2 Expansion of commercial satellite constellations

- 5.2.3.3 Customization and on-demand analytics services

- 5.2.4 CHALLENGES

- 5.2.4.1 Temporal and spatial resolution tradeoffs

- 5.2.4.2 Quality and accuracy variability

- 5.2.1 DRIVERS

- 5.3 IMPACT OF 2025 US TARIFF - GEOSPATIAL IMAGERY ANALYTICS MARKET

- 5.3.1 INTRODUCTION

- 5.3.2 KEY TARIFF RATES

- 5.3.3 PRICE IMPACT ANALYSIS

- 5.3.3.1 Strategic shifts and emerging trends

- 5.3.4 IMPACT ON COUNTRY/REGION

- 5.3.4.1 US

- 5.3.4.1.1 Strategic shifts and key observations

- 5.3.4.2 China

- 5.3.4.2.1 Strategic shifts and key observations

- 5.3.4.3 Southeast Asia

- 5.3.4.3.1 Strategic shifts and key observations

- 5.3.4.4 Europe

- 5.3.4.4.1 Strategic shifts and key observations

- 5.3.4.1 US

- 5.3.5 IMPACT ON END-USE INDUSTRIES

- 5.3.5.1 Agriculture and Precision Farming

- 5.3.5.2 Infrastructure & Urban Planning

- 5.3.5.3 Defense and Intelligence

- 5.3.5.4 Environmental Monitoring & Disaster Management

- 5.3.5.5 Oil, Gas, and Mining

- 5.4 EVOLUTION OF GEOSPATIAL IMAGERY ANALYTICS MARKET

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 ECOSYSTEM ANALYSIS

- 5.6.1 IMAGE PROCESSING & ENHANCEMENT

- 5.6.2 OBJECT TRACKING & FEATURE DETECTION

- 5.6.3 CHANGE DETECTION & TIME-SERIES ANALYSIS

- 5.6.4 PREDICTIVE MODELING & PATTERN RECOGNITION

- 5.6.5 AI/ML-BASED GEOSPATIAL ANALYTICS

- 5.6.6 OTHERS (ANOMALY DETECTION AND STREAM ANALYTICS)

- 5.7 INVESTMENT LANDSCAPE AND FUNDING SCENARIO

- 5.8 IMPACT OF GENERATIVE AI ON GEOSPATIAL IMAGERY ANALYTICS MARKET

- 5.8.1 SUPER-RESOLUTION IMAGE ENHANCEMENT

- 5.8.2 SYNTHETIC DATA GENERATION FOR MODEL TRAINING

- 5.8.3 AUTOMATIC FEATURE EXTRACTION AND MAPPING

- 5.8.4 CHANGE DETECTION AND TEMPORAL ANALYSIS

- 5.8.5 DISASTER SCENARIO SIMULATION AND RISK ASSESSMENT

- 5.8.6 AUGMENTED REALITY (AR) AND VISUALIZATION FOR GEOSPATIAL DATA

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 GEOCENTO'S SHIP DETECTION AND MONITORING SEAS

- 5.9.2 CARTO ANALYZED ENGLAND'S RESPONSE TO COVID-19 USING DATA AND MAPS

- 5.9.3 ESRI EMPOWERED INSURANCE INDUSTRY IN INDIA

- 5.9.4 GEOSPIN'S ANALYSIS FOR CHARGING INFRASTRUCTURE

- 5.9.5 L3HARRIS HELPED AUSTRALIAN CITY COUNCIL FOR TREE INVENTORY FOR LEVERAGING DEEP LEARNING

- 5.9.6 PHOTOSAT MONITORED OIL SAND MINES OF ALBERTA, CANADA

- 5.9.7 HEXAGON MONITORED FOREST COVER CHANGES IN MADHYA PRADESH, INDIA

- 5.10 TECHNOLOGY ANALYSIS

- 5.10.1 KEY TECHNOLOGIES

- 5.10.1.1 Remote Sensing

- 5.10.1.2 Machine Learning

- 5.10.1.3 Georeferencing

- 5.10.1.4 Photogrammetry

- 5.10.2 COMPLEMENTARY TECHNOLOGIES

- 5.10.2.1 Edge Computing

- 5.10.2.2 5G

- 5.10.2.3 Cloud Computing

- 5.10.3 ADJACENT TECHNOLOGIES

- 5.10.3.1 Digital Twin Technology

- 5.10.3.2 Autonomous Navigation

- 5.10.3.3 Internet of Things (IoT)

- 5.10.3.4 Blockchain

- 5.10.1 KEY TECHNOLOGIES

- 5.11 REGULATORY LANDSCAPE

- 5.11.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.11.2 REGULATORY FRAMEWORK

- 5.11.2.1 North America

- 5.11.2.1.1 Geospatial Data Act (GDA) of 2018 (US)

- 5.11.2.1.2 Open Government Directive of 2014 (Canada)

- 5.11.2.2 Europe

- 5.11.2.2.1 INSPIRE Directive 2007/2 (European Commission)

- 5.11.2.2.2 General Data Protection Regulation (European Union)

- 5.11.2.2.3 The Copernicus Regulation 2021/696 (European Union)

- 5.11.2.2.4 Geospatial Information Regulation Act 2016 (India)

- 5.11.2.2.5 Surveying and Mapping Law 2002, Revised 2017 (China)

- 5.11.2.2.6 Basic Act on Advancement of Utilizing Geospatial Information, 2007 (Japan)

- 5.11.2.3 Middle East & Africa

- 5.11.2.3.1 Survey and Mapping Law (Saudi Arabia)

- 5.11.2.3.2 Spatial Data Infrastructure Act 54 of 2003 (South Africa)

- 5.11.2.4 Latin America

- 5.11.2.4.1 National Geospatial Data Infrastructure (INDE) Law (Brazil)

- 5.11.2.4.2 Geospatial Data Law 2020 (Mexico)

- 5.11.2.1 North America

- 5.12 PATENT ANALYSIS

- 5.12.1 METHODOLOGY

- 5.12.2 PATENTS FILED, BY DOCUMENT TYPE

- 5.12.3 INNOVATION AND PATENT APPLICATIONS

- 5.13 PRICING ANALYSIS

- 5.13.1 AVERAGE SELLING PRICE OF OFFERING, BY KEY PLAYER, 2025

- 5.13.2 AVERAGE SELLING PRICE, BY APPLICATION, 2025

- 5.14 KEY CONFERENCES AND EVENTS (2025-2026)

- 5.15 PORTER'S FIVE FORCES ANALYSIS

- 5.15.1 THREAT OF NEW ENTRANTS

- 5.15.2 THREAT OF SUBSTITUTES

- 5.15.3 BARGAINING POWER OF SUPPLIERS

- 5.15.4 BARGAINING POWER OF BUYERS

- 5.15.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.16 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.17 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.17.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.17.2 BUYING CRITERIA

6 GEOSPATIAL IMAGERY ANALYTICS MARKET, BY APPLICATION

- 6.1 INTRODUCTION

- 6.1.1 APPLICATION: GEOSPATIAL IMAGERY ANALYTICS MARKET DRIVERS

- 6.2 SURVEILLANCE & MONITORING

- 6.2.1 GEOSPATIAL IMAGERY-BASED SURVEILLANCE AND MONITORING ENHANCING SITUATIONAL AWARENESS AND STRENGTHENING NATIONAL AND ENVIRONMENTAL SECURITY

- 6.3 ENVIRONMENTAL MONITORING & CLIMATE CHANGE

- 6.3.1 BY OFFERING TIMELY INSIGHTS, GEOSPATIAL IMAGERY ANALYTICS TO COMBAT CLIMATE CHANGE AND SUPPORT SUSTAINABLE ENVIRONMENTAL MANAGEMENT

- 6.4 LAND USE & LAND COVER (LULC) CLASSIFICATION

- 6.4.1 WITH GROWING PRESSURE ON LAND AND RESOURCES, ACCURATE AND TIMELY LULC ANALYSIS TO BECOME NECESSITY FOR SUSTAINABLE DEVELOPMENT

- 6.5 ASSET & INFRASTRUCTURE MANAGEMENT

- 6.5.1 GEOSPATIAL IMAGERY TO TRANSFORM INFRASTRUCTURE MANAGEMENT AND ENABLE SMARTER, DATA-DRIVEN ASSET DECISIONS

- 6.6 INSURANCE RISK ASSESSMENT & CLAIMS VALIDATION

- 6.6.1 GEOSPATIAL IMAGERY ANALYTICS BECOMING STRATEGIC ASSET IN MODERNIZING INSURANCE VALUE CHAIN AND IMPROVING CUSTOMER TRUST

- 6.7 DISASTER MANAGEMENT & EMERGENCY RESPONSE

- 6.7.1 GEOSPATIAL IMAGERY ANALYTICS BECOMING INDISPENSABLE IN MANAGING DISASTERS, MINIMIZING RESPONSE TIME, REDUCING LOSS OF LIFE, AND SUPPORTING MORE EFFICIENT RECOVERY OPERATIONS

- 6.8 PRECISION FARMING & CROP MONITORING

- 6.8.1 PRECISION FARMING POWERED BY GEOSPATIAL ANALYTICS TO RESHAPE AGRICULTURE INTO DATA-DRIVEN, ADAPTIVE INDUSTRY

- 6.9 URBAN PLANNING & SMART CITY DESIGN

- 6.9.1 GEOSPATIAL IMAGERY ANALYTICS TO HELP URBAN AREAS ADAPT TO RAPID GROWTH, CLIMATE PRESSURES, AND EVOLVING CITIZEN NEEDS

- 6.10 TARGET DETECTION & STRATEGIC INTELLIGENCE

- 6.10.1 IMAGERY ANALYTICS STRENGTHENING NATIONAL DEFENSE CAPABILITIES BY PROVIDING UNMATCHED LEVEL OF VISIBILITY, ACCURACY, AND FORESIGHT IN HIGH-STAKES ENVIRONMENTS

- 6.11 SUPPLY CHAIN & LOGISTICS MONITORING

- 6.11.1 GEOSPATIAL IMAGERY ANALYTICS TO ENHANCE LOGISTICS EFFICIENCY, MANAGE RISKS, AND MAKE MORE RESILIENT SUPPLY CHAIN DECISIONS

- 6.12 DISEASE OUTBREAK TRACKING & RESOURCE ALLOCATION

- 6.12.1 BY INTEGRATING SATELLITE IMAGERY WITH GEOSPATIAL AND DEMOGRAPHIC DATA, HEALTH AGENCIES CAN MONITOR ENVIRONMENTAL CONDITIONS THAT INFLUENCE DISEASE SPREAD

- 6.13 RETAIL SITE SELECTION & CONSUMER FOOTFALL MAPPING

- 6.13.1 GEOSPATIAL IMAGERY ANALYTICS TO ENABLE BUSINESSES TO ALIGN THEIR PHYSICAL FOOTPRINT WITH ACTUAL DEMAND AND EVOLVING URBAN DYNAMICS

- 6.14 OTHER APPLICATIONS

7 GEOSPATIAL IMAGERY ANALYTICS MARKET, BY DATA MODALITY

- 7.1 INTRODUCTION

- 7.1.1 DATA MODALITY: GEOSPATIAL IMAGERY ANALYTICS MARKET DRIVERS

- 7.2 IMAGE-BASED ANALYTICS

- 7.2.1 WITH INCREASING NEED FOR ACTIONABLE GEOSPATIAL INTELLIGENCE ACROSS SECTORS, IMAGE-BASED ANALYTICS TO WITNESS SUSTAINED GROWTH

- 7.3 VIDEO-BASED ANALYTICS

- 7.3.1 AS SMART CITIES AND INFRASTRUCTURE PROJECTS GROW, DEMAND FOR INTELLIGENT VIDEO ANALYTICS CONTINUES TO EXPAND

- 7.4 MULTIMODAL ANALYTICS

- 7.4.1 FUSING IMAGE AND VIDEO DATA FOR COMPREHENSIVE SITUATIONAL AWARENESS

8 GEOSPATIAL IMAGERY ANALYTICS MARKET, BY DATA SOURCE

- 8.1 INTRODUCTION

- 8.1.1 DATA SOURCE: GEOSPATIAL IMAGERY ANALYTICS MARKET DRIVERS

- 8.2 SATELLITE IMAGERY

- 8.2.1 GROWING ADOPTION OF CLOUD-BASED GEOSPATIAL PLATFORMS AND AI-DRIVEN ANALYTICS TOOLS TO STRENGTHEN UTILITY OF SATELLITE IMAGERY

- 8.3 SYNTHETIC APERTURE RADAR (SAR)

- 8.3.1 VERSATILITY AND RELIABILITY OF SAR IMAGING, ESPECIALLY IN CHALLENGING ENVIRONMENTS, CONTINUE TO POSITION IT AS CRITICAL DATA SOURCE

- 8.4 AERIAL IMAGERY

- 8.4.1 AS TECHNOLOGICAL IMPROVEMENTS LOWER OPERATIONAL COSTS AND IMPROVE RESOLUTION, AERIAL IMAGERY TO MAINTAIN ITS IMPORTANCE

- 8.5 UAV/DRONES

- 8.5.1 AS FLIGHT CONTROL TECHNOLOGIES CONTINUE TO EVOLVE, UAV/DRONES POISED FOR SUSTAINED EXPANSION

- 8.6 GIS & MAPPING PLATFORMS

- 8.6.1 GIS AND MAPPING PLATFORMS TO PLAY CRITICAL ROLE IN CONVERTING RAW IMAGERY DATA INTO ACTIONABLE INSIGHTS

- 8.7 OTHER DATA SOURCES

9 GEOSPATIAL IMAGERY ANALYTICS MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.1.1 OFFERING: GEOSPATIAL IMAGERY ANALYTICS MARKET DRIVERS

- 9.2 SOFTWARE

- 9.2.1 BY FUNCTIONALITY

- 9.2.1.1 Image Processing & Enhancement

- 9.2.1.1.1 As need for timely and accurate spatial insights grows, image processing and enhancement tools to become indispensable for organizations

- 9.2.1.2 Object Tracking and Feature Detection

- 9.2.1.2.1 Object tracking and feature detection are rapidly growing as volume of imagery data grows

- 9.2.1.3 Change Detection & Time-series Analysis

- 9.2.1.3.1 With global climate events and urbanization accelerating change, ability to track and analyze geospatial trends to become essential

- 9.2.1.4 Predictive Modeling & Pattern Recognition

- 9.2.1.4.1 By analyzing recurring spatial behaviors, geospatial systems to generate models that simulate potential outcomes, providing decision-makers with strategic advantage

- 9.2.1.5 AI-based Geospatial Imagery Analytics

- 9.2.1.5.1 As training data becomes more robust and computing resources more accessible, AI-based geospatial imagery analytics to evolve & redefine scope

- 9.2.1.6 Others

- 9.2.1.1 Image Processing & Enhancement

- 9.2.2 BY DEPLOYMENT MODE

- 9.2.2.1 Cloud

- 9.2.2.1.1 As geospatial applications become more dynamic and data-intensive, cloud deployment to remain key growth driver

- 9.2.2.2 On-premises

- 9.2.2.2.1 With increasing concerns around cybersecurity and data governance, on-premises deployment to remain trusted choice for mission-critical operations

- 9.2.2.1 Cloud

- 9.2.1 BY FUNCTIONALITY

- 9.3 SERVICES

- 9.3.1 PROFESSIONAL SERVICES

- 9.3.1.1 Consulting & Advisory

- 9.3.1.1.1 As geospatial technologies evolve rapidly, consulting and advisory services to help organizations stay ahead of curve

- 9.3.1.2 Deployment & Integration

- 9.3.1.2.1 As organizations increasingly rely on high-resolution imagery, demand for reliable, end-to-end deployment and integration support continues to grow

- 9.3.1.3 Support & Maintenance

- 9.3.1.3.1 With organizations increasingly adopting AI-driven and real-time analytics, complexity of maintaining systems grows, driving strong demand for expert support and maintenance

- 9.3.1.1 Consulting & Advisory

- 9.3.2 MANAGED SERVICES

- 9.3.1 PROFESSIONAL SERVICES

10 GEOSPATIAL IMAGERY ANALYTICS MARKET, BY VERTICAL

- 10.1 INTRODUCTION

- 10.1.1 VERTICAL: GEOSPATIAL IMAGERY ANALYTICS MARKET DRIVERS

- 10.2 INSURANCE

- 10.2.1 GEOSPATIAL IMAGERY ANALYTICS TO EMERGE AS STRATEGIC TOOL FOR INSURERS SEEKING TO ENHANCE RESILIENCE, EFFICIENCY, AND COMPETITIVE ADVANTAGE

- 10.3 AGRICULTURE

- 10.3.1 GEOSPATIAL IMAGERY ANALYTICS TO BECOME INDISPENSABLE TOOL FOR ENHANCING PRODUCTIVITY AND PROFITABILITY

- 10.4 CONSTRUCTION & REAL ESTATE

- 10.4.1 GEOSPATIAL IMAGERY SUPPORTS URBAN PLANNING INITIATIVES BY HELPING STAKEHOLDERS VISUALIZE DEVELOPMENT PATTERNS, ZONING IMPACTS, AND ENVIRONMENTAL FACTORS

- 10.5 MINING

- 10.5.1 HIGH-RESOLUTION SATELLITE AND AERIAL IMAGERY TO HELP MINING COMPANIES IDENTIFY MINERAL-RICH ZONES, ANALYZE TERRAIN FEATURES, AND ASSESS SURFACE CHANGES

- 10.6 HEALTHCARE & LIFE SCIENCES

- 10.6.1 AS GLOBAL HEALTH CHALLENGES BECOME INCREASINGLY COMPLEX, GEOSPATIAL IMAGERY ANALYTICS TO OFFER SCALABLE AND DATA-RICH APPROACH TO IMPROVING POPULATION HEALTH MANAGEMENT

- 10.7 ENERGY & UTILITIES

- 10.7.1 ORGANIZATIONS TO USE HIGH-RESOLUTION SATELLITE AND AERIAL IMAGERY TO INSPECT POWER LINES, PIPELINES, AND SUBSTATIONS REMOTELY

- 10.8 GOVERNMENT & DEFENSE

- 10.8.1 FROM NATIONAL DEFENSE TO CIVIC ADMINISTRATION, GEOSPATIAL IMAGERY ANALYTICS TO PROVE INDISPENSABLE FOR ENHANCING DECISION-MAKING, OPERATIONAL EFFICIENCY, AND PUBLIC SAFETY

- 10.9 TELECOMMUNICATIONS

- 10.9.1 AS DEMAND FOR HIGH-SPEED CONNECTIVITY CONTINUES TO GROW, GEOSPATIAL IMAGERY ANALYTICS TO BECOME ESSENTIAL FOR BUILDING SMARTER, MORE RESILIENT TELECOM NETWORKS

- 10.10 TRANSPORTATION & LOGISTICS

- 10.10.1 AS SUPPLY CHAINS BECOME MORE COMPLEX AND CUSTOMER EXPECTATIONS RISE, GEOSPATIAL IMAGERY ANALYTICS TO EMERGE AS KEY ENABLER OF EFFICIENCY, RESILIENCE, AND COMPETITIVENESS

- 10.11 MEDIA & ENTERTAINMENT

- 10.11.1 USING HIGH-RESOLUTION SATELLITE & AERIAL IMAGERY FOR REALISTIC VISUAL WORLDS

- 10.12 OTHER VERTICALS

11 GEOSPATIAL IMAGERY ANALYTICS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: GEOSPATIAL IMAGERY ANALYTICS MARKET DRIVERS

- 11.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 11.2.3 US

- 11.2.3.1 Driving innovation through advanced geospatial imaging and AI integration

- 11.2.4 CANADA

- 11.2.4.1 Leveraging geospatial analytics for environmental stewardship and industrial efficiency

- 11.3 EUROPE

- 11.3.1 EUROPE: GEOSPATIAL IMAGERY ANALYTICS MARKET DRIVERS

- 11.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 11.3.3 UK

- 11.3.3.1 UK accelerating urban and environmental decision-making with advanced imagery analytics

- 11.3.4 GERMANY

- 11.3.4.1 Driving climate and infrastructure intelligence through high-tech geospatial solutions

- 11.3.5 FRANCE

- 11.3.5.1 Fusing AI and policy for scalable, sustainable imagery analytics

- 11.3.6 ITALY

- 11.3.6.1 Leveraging national satellite assets for sector-specific geospatial innovation

- 11.3.7 SPAIN

- 11.3.7.1 Boosting agricultural and coastal resilience with smart imagery integration

- 11.3.8 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: GEOSPATIAL IMAGERY ANALYTICS MARKET DRIVERS

- 11.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 11.4.3 CHINA

- 11.4.3.1 High-resolution satellite constellations fuel China's expanding geospatial analytics ecosystem

- 11.4.4 JAPAN

- 11.4.4.1 Synthetic aperture radar and disaster monitoring drive Japan's imagery analytics innovation

- 11.4.5 INDIA

- 11.4.5.1 Policy reforms and hyperspectral imaging accelerate India's geospatial intelligence growth

- 11.4.6 SOUTH KOREA

- 11.4.6.1 Urban digital twins and AI-backed imagery position South Korea as regional analytics hub

- 11.4.7 AUSTRALIA & NEW ZEALAND

- 11.4.7.1 Environmental monitoring and disaster resilience boost geospatial analytics in Australasia

- 11.4.8 ASEAN

- 11.4.8.1 Regional satellite programs and smart city initiatives propel ASEAN geospatial adoption

- 11.4.9 REST OF ASIA PACIFIC

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 MIDDLE EAST & AFRICA: GEOSPATIAL IMAGERY ANALYTICS MARKET DRIVERS

- 11.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 11.5.3 KINGDOM OF SAUDI ARABIA (KSA)

- 11.5.3.1 Driving smart infrastructure with expanding geospatial imagery analytics capabilities

- 11.5.4 UAE

- 11.5.4.1 Accelerating digital governance through geospatial imagery innovation

- 11.5.5 QATAR

- 11.5.5.1 Empowering urban development with advanced geospatial intelligence

- 11.5.6 ISRAEL

- 11.5.6.1 Advancing regional leadership in high-precision geospatial imagery analytics

- 11.5.7 SOUTH AFRICA

- 11.5.7.1 Strengthening national development with spatial analytics integration

- 11.5.8 REST OF MIDDLE EAST

- 11.6 LATIN AMERICA

- 11.6.1 LATIN AMERICA: GEOSPATIAL IMAGERY ANALYTICS MARKET DRIVERS

- 11.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 11.6.3 BRAZIL

- 11.6.3.1 Substantial government initiatives and strategic investments to help with market growth

- 11.6.4 MEXICO

- 11.6.4.1 Widespread adoption of AI reflecting national trend toward embracing advanced technologies to remain competitive in digital marketplace

- 11.6.5 ARGENTINA

- 11.6.5.1 Market growth driven by need to enhance efficiency and personalization in marketing strategies

- 11.6.6 REST OF LATIN AMERICA

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 12.3 REVENUE ANALYSIS, 2020-2024

- 12.4 MARKET SHARE ANALYSIS, 2024

- 12.4.1 MARKET RANKING ANALYSIS

- 12.5 PRODUCT COMPARATIVE ANALYSIS

- 12.5.1 MAXAR EARTH INTELLIGENCE (MAXAR TECHNOLOGIES)

- 12.5.2 PLANETSCOPE/SKYSAT (PLANET LABS)

- 12.5.3 SPECTRA AI (BLACKSKY)

- 12.5.4 CAPELLA ANALYTICS (CAPELLA SPACE)

- 12.5.5 GOOGLE EARTH ENGINE (GOOGLE)

- 12.6 COMPANY VALUATION AND FINANCIAL METRICS

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.5.1 Company Footprint

- 12.7.5.2 Regional Footprint

- 12.7.5.3 Offering Footprint

- 12.7.5.4 Application Footprint

- 12.7.5.5 Vertical Footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.2 Competitive benchmarking of key startups/SMEs

- 12.9 COMPETITIVE SCENARIO AND TRENDS

- 12.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 12.9.2 DEALS

13 COMPANY PROFILES

- 13.1 INTRODUCTION

- 13.2 KEY PLAYERS

- 13.2.1 GOOGLE

- 13.2.1.1 Business overview

- 13.2.1.2 Products/Solutions/Services offered

- 13.2.1.3 Recent developments

- 13.2.1.3.1 Product launches & enhancements

- 13.2.1.3.2 Deals

- 13.2.1.4 MnM view

- 13.2.1.4.1 Key strengths

- 13.2.1.4.2 Strategic choices

- 13.2.1.4.3 Weaknesses and competitive threats

- 13.2.2 IBM

- 13.2.2.1 Business overview

- 13.2.2.2 Products/Solutions/Services offered

- 13.2.2.3 Recent developments

- 13.2.2.3.1 Product launches & enhancements

- 13.2.2.3.2 Deals

- 13.2.2.4 MnM view

- 13.2.2.4.1 Key strengths

- 13.2.2.4.2 Strategic choices

- 13.2.2.4.3 Weaknesses and competitive threats

- 13.2.3 HEXAGON AB

- 13.2.3.1 Business overview

- 13.2.3.2 Products/Solutions/Services offered

- 13.2.3.3 Recent developments

- 13.2.3.3.1 Product launches & enhancements

- 13.2.3.3.2 Deals

- 13.2.3.4 MnM view

- 13.2.3.4.1 Key strengths

- 13.2.3.4.2 Strategic choices

- 13.2.3.4.3 Weaknesses and competitive threats

- 13.2.4 TOMTOM

- 13.2.4.1 Business overview

- 13.2.4.2 Products/Solutions/Services offered

- 13.2.4.3 Recent developments

- 13.2.4.3.1 Product launches & enhancements

- 13.2.4.3.2 Deals

- 13.2.4.4 MnM view

- 13.2.4.4.1 Key strengths

- 13.2.4.4.2 Strategic choices

- 13.2.4.4.3 Weaknesses and competitive threats

- 13.2.5 MAXAR TECHNOLOGIES

- 13.2.5.1 Business overview

- 13.2.5.2 Products/Solutions/Services offered

- 13.2.5.3 Recent developments

- 13.2.5.3.1 Product launches & enhancements

- 13.2.5.3.2 Deals

- 13.2.5.4 MnM view

- 13.2.5.4.1 Key strengths

- 13.2.5.4.2 Strategic choices

- 13.2.5.4.3 Weaknesses and competitive threats

- 13.2.6 TRIMBLE

- 13.2.6.1 Business overview

- 13.2.6.2 Products/Solutions/Services offered

- 13.2.6.3 Recent developments

- 13.2.6.3.1 Product launches & enhancements

- 13.2.6.3.2 Deals

- 13.2.7 CALIPER CORPORATION

- 13.2.7.1 Business overview

- 13.2.7.2 Products/Solutions/Services offered

- 13.2.7.3 Recent developments

- 13.2.7.3.1 Product launches & enhancements

- 13.2.8 PLANET LABS

- 13.2.8.1 Business overview

- 13.2.8.2 Products/Solutions/Services offered

- 13.2.8.3 Recent developments

- 13.2.8.3.1 Product launches & enhancements

- 13.2.8.3.2 Deals

- 13.2.9 ESRI

- 13.2.9.1 Business overview

- 13.2.9.2 Products/Solutions/Services offered

- 13.2.9.3 Recent developments

- 13.2.9.3.1 Product launches & enhancements

- 13.2.9.3.2 Deals

- 13.2.10 L3HARRIS TECHNOLOGIES

- 13.2.10.1 Business overview

- 13.2.10.2 Products/Solutions/Services offered

- 13.2.11 ORACLE

- 13.2.12 NV5 GEOSPATIAL

- 13.2.13 RMSI

- 13.2.14 MAPLARGE

- 13.2.15 FUGRO

- 13.2.16 BLACKSKY

- 13.2.17 NEARMAP

- 13.2.18 SUPERMAP

- 13.2.1 GOOGLE

- 13.3 SME/STARTUPS

- 13.3.1 EARTHDAILY ANALYTICS

- 13.3.2 SPARKGEO

- 13.3.3 ORBICA

- 13.3.4 CARTO

- 13.3.5 MAPBOX

- 13.3.6 BLUE SKY ANALYTICS

- 13.3.7 LATITUDO40

- 13.3.8 ECOPIA.AI

- 13.3.9 EOS DATA ANALYTICS

- 13.3.10 CATALYST

- 13.3.11 SPACEKNOW

- 13.3.12 FLYPIX AI

- 13.3.13 PICTERRA

- 13.3.14 GEOSPATIAL INSIGHT

- 13.3.15 UP42

- 13.3.16 SIMULARITY

- 13.3.17 CAPELLA SPACE

14 ADJACENT AND RELATED MARKETS

- 14.1 INTRODUCTION

- 14.2 GEOSPATIAL ANALYTICS MARKET - GLOBAL FORECAST TO 2029

- 14.2.1 MARKET DEFINITION

- 14.2.2 MARKET OVERVIEW

- 14.2.2.1 Geospatial Analytics Market, By Offering

- 14.2.2.2 Geospatial Analytics Market, By Technology

- 14.2.2.3 Geospatial Analytics Market, By Data Type

- 14.2.2.4 Geospatial Analytics Market, By Vertical

- 14.2.2.5 Geospatial Analytics Market, By Region

- 14.3 LOCATION ANALYTICS MARKET - GLOBAL FORECAST TO 2028

- 14.3.1 MARKET DEFINITION

- 14.3.2 MARKET OVERVIEW

- 14.3.2.1 Location Analytics Market, By Offering

- 14.3.2.2 Location Analytics Market, By Location Type

- 14.3.2.3 Location Analytics Market, By Application

- 14.3.2.4 Location Analytics Market, By Vertical

- 14.3.2.5 Location Analytics Market, By Region

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS