|

시장보고서

상품코드

1775086

헬스케어 컨설팅 서비스 시장 예측(-2030년) : 서비스 유형별, 최종사용자별, 지역별Healthcare Consulting Services Market by Service Type, End User, Region- Global Forecast to 2030 |

||||||

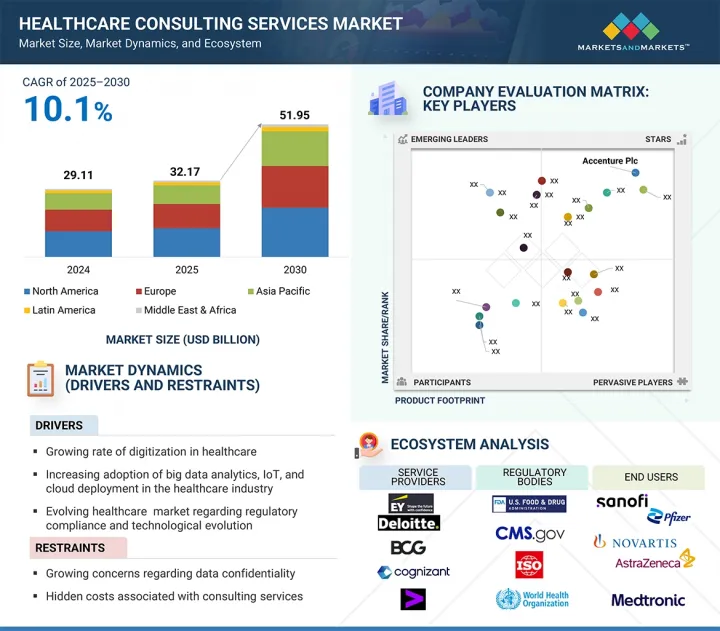

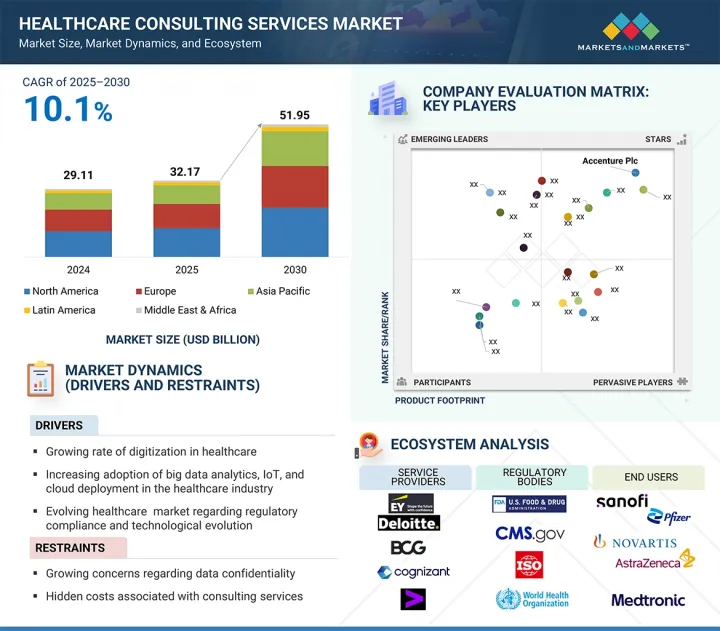

세계의 헬스케어 컨설팅 서비스 시장 규모는 2025년 321억 7,000만 달러에서 2030년까지 519억 5,000만 달러에 달할 것으로 예측되며, 예측 기간에 CAGR로 10.1%의 성장이 전망됩니다.

전자의무기록, 원격의료, 인공지능(AI) 기반 진단에 대한 수요 증가와 더불어 가치 기반 의료로의 전환과 운영 비용에 대한 압박이 전문가 자문 서비스에 대한 수요를 촉진하고 있습니다. 또한 신흥 시장의 의료 인프라 확대와 제약 및 메드테크(MedTech) 분야의 혁신이 시장 성장을 가속하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상연도 | 2024-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2024-2030년 |

| 단위 | 10억 달러 |

| 부문 | 서비스 유형, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

서비스 유형별로는 IT 및 디지털 전환 컨설팅 서비스 부문이 예측 기간 중 시장을 장악할 것으로 예측됩니다.

서비스 유형별로 헬스케어 컨설팅 서비스 시장은 IT 및 디지털 전환 컨설팅 서비스, 전략 컨설팅 서비스, 경영 컨설팅 서비스, 재무 컨설팅 서비스, HR 및 인재 컨설팅 서비스, 마케팅, 영업 및 상업화 컨설팅 서비스, 규제 준수, R&D 컨설팅 서비스, 공공보건 컨설팅 서비스, 기타 서비스로 구분됩니다. 마케팅-영업-상용화 컨설팅 서비스, 규제 준수, 연구개발 컨설팅 서비스, 공공보건 컨설팅 서비스, 기타 서비스로 구분되며, IT 및 디지털 혁신 컨설팅 서비스 부문이 가장 높은 성장률을 보였습니다. 는 전자의무기록(EHR)과 원격의료 플랫폼의 도입 진행, 진단 및 업무에서의 AI 활용, 클라우드 컴퓨팅의 중요성, 사이버 보안 솔루션의 발전으로 인해 가장 높은 성장률을 보였습니다.

최종사용자별로는 제약 및 생명공학 기업이 2024년 가장 큰 시장 점유율을 차지했습니다.

헬스케어 컨설팅 서비스 시장은 최종사용자에 따라 정부 기관, 의료 프로바이더, 의료 보험사, 제약 및 생명공학 기업, 의료기기 기업, 기타 최종사용자로 분류되며, 2024년에는 제약 및 생명공학 기업이 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 이러한 우위는 API 운영, 제형 개발, 공급망 관리에서 비용 최적화에 대한 요구가 증가하고 있기 때문입니다. 또한 이들 기업은 복잡하고 빈번하게 변화하는 규제 요건에 직면하고 있으며, 컴플라이언스, M&A, 제품 출시 전략, 브랜드 관리에 대한 전문가의 도움이 필요한 상황입니다.

지역별로는 북미가 2024년 가장 큰 시장 점유율을 차지했습니다.

세계 헬스케어 컨설팅 서비스 시장은 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카로 구분되며, 2024년에는 북미가 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 이 부문의 큰 점유율은 고도로 발달된 의료 인프라, 막대한 의료비, 디지털 의료 기술의 광범위한 채택, 강력한 규제 프레임워크에 기인합니다. 주요 헬스케어 컨설팅 기업의 존재, 첨단화된 보험자 및 공급자 모델, 가치 기반 의료, AI, 환자 경험에 대한 지속적인 투자로 북미의 리더십이 더욱 강화되고 있습니다.

세계의 헬스케어 컨설팅 서비스 시장에 대해 조사분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 제공하고 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 중요한 인사이트

- 헬스케어 컨설팅 서비스 시장의 개요

- 아시아태평양의 헬스케어 컨설팅 서비스 시장 : 국가별, 최종사용자별

- 헬스케어 컨설팅 서비스 시장 : 지역의 성장 기회

- 헬스케어 컨설팅 서비스 시장 : 지역 구성

- 헬스케어 컨설팅 서비스 시장 : 신흥 시장과 선진 시장

제5장 시장의 개요

- 서론

- 시장 역학

- 촉진요인

- 억제요인

- 기회

- 과제

- 산업 동향

- 의료에서의 디지털 전환

- 가치 기반 케어로의 이동

- 환자 중심 케어에 대한 주목

- 건강의 사회적 결정 요인의 중요성 증가

- 데이터 애널리틱스의 사용 확대

- 정밀의료의 성장

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 참고 가격 분석

- 참고 가격 분석 : 서비스 유형별

- 참고 가격 분석 : 지역별

- 밸류체인 분석

- 에코시스템 분석

- 투자와 자금조달 시나리오

- 기술 분석

- 주요 기술

- 보완 기술

- 인접 기술

- 주요 컨퍼런스와 이벤트(2025-2026년)

- 사례 연구 분석

- 페이퍼리스 프로세스에 의한 환자 체험의 향상

- 인재 관리 능력을 향상시키는 첨단 클라우드 솔루션

- 효과적인 치료를 향한 리스크 관리 계획의 개발

- 규제 상황

- 규제기관, 정부기관, 기타 조직

- 규제 분석

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 비즈니스 모델

- 2025년 미국 관세의 영향

- 서론

- 주요 관세율

- 가격의 영향 분석

- 국가/지역에 대한 영향

- 최종 용도 산업에 대한 영향

제6장 헬스케어 컨설팅 서비스 시장 : 서비스 유형별

- 서론

- IT/디지털 전환 컨설팅

- 전략 컨설팅

- 경영 컨설팅

- 재무 컨설팅

- HR·인재 컨설팅

- 마케팅·세일즈·상업화 컨설팅

- 규제 준수

- 연구개발 컨설팅

- 공중위생 컨설팅

- 기타 컨설팅 서비스

제7장 헬스케어 컨설팅 서비스 시장 : 최종사용자별

- 서론

- 정부기관

- 의료 제공자

- 병원

- 외래 진료 센터

- 장기 케어 시설

- 진단·영상 진단 센터

- 기타 의료 제공자

- 건강보험 사람

- 민간 보험자

- 공적 보험자

- 제약·바이오테크놀러지 기업

- 의료기기 기업

- 기타 최종사용자

제8장 헬스케어 컨설팅 서비스 시장 : 지역별

- 서론

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 일본

- 중국

- 인도

- 기타 아시아태평양

- 라틴아메리카

- 라틴아메리카의 거시경제 전망

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 중동 및 아프리카의 거시경제 전망

- GCC 국가

- 기타 중동 및 아프리카

제9장 경쟁 구도

- 개요

- 주요 참여 기업의 전략/강점

- 매출 분석(2020-2024년)

- 시장 점유율 분석(2024년)

- 기업의 평가와 재무 지표

- 브랜드/소프트웨어의 비교

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업 평가 매트릭스 : 스타트업/중소기업(2024년)

- 경쟁 시나리오

제10장 기업의 개요

- 주요 기업

- ACCENTURE

- COGNIZANT

- DELOITTE

- MCKINSEY & COMPANY

- BOSTON CONSULTING GROUP

- PWC

- EY

- HURON CONSULTING GROUP INC.

- KPMG

- BAIN & COMPANY, INC.

- IQVIA INC.

- L.E.K. CONSULTING

- NTT DATA, INC.

- OLIVER WYMAN, LLC

- SIMON-KUCHER & PARTNERS

- IBM

- CLEARVIEW HEALTHCARE PARTNERS

- ALVAREZ & MARSAL HOLDINGS, LLC

- ZS ASSOCIATES

- CHARTIS

- 기타 기업

- QUALITY CREST HEALTHCARE CONSULTANTS PRIVATE LIMITED

- LUCID HEALTH CONSULTING

- BLUE MATTER CONSULTING

- ISOS CONSULTANCY SERVICES PVT. LTD.

- BACK BAY LIFE SCIENCE ADVISORS

제11장 부록

KSA 25.07.31The healthcare consulting services market is projected to reach USD 51.95 billion by 2030 from USD 32.17 billion in 2025, at a CAGR of 10.1% during the forecast period. The growing demand for adopting electronic health records, telehealth, and AI-driven diagnostics, along with the shift toward value-based care and operational cost pressures, is driving demand for expert advisory services. Additionally, expanding healthcare infrastructure in emerging markets and innovation in pharma and MedTech fuel market growth.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2024-2030 |

| Units Considered | Value (USD billion) |

| Segments | Service Type, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, the Middle East & Africa, and GCC Countries |

By service type, the IT & digital transformation consulting services segment is expected to dominate the market during the forecast period.

By service type, the healthcare consulting services market is segmented into IT & digital transformation consulting services; strategy consulting services; operation consulting services; financial consulting services; HR & talent consulting services; marketing, sales, and commercialization consulting services; regulatory & compliance; R&D consulting services; public health consulting services; and other services. The highest growth rate of the IT & digital transformation consulting services segment is attributed to the increasing adoption of electronic health records (EHRs) and telemedicine platforms; the utilization of AI for diagnostics & operations; the importance of cloud computing; and the advancement of cybersecurity solutions.

By end user, the pharmaceutical & biotechnology companies segment accounted for the largest market share in 2024.

The healthcare consulting services market is segmented by end users into government bodies, healthcare providers, health insurance payers, pharmaceutical & biotechnological companies, medical device companies, and other end users. The pharmaceutical & biotechnological companies segment accounted for the largest market share in 2024. This dominance is driven by their growing need for cost optimization in API operations, formulation development, and supply chain management. These companies also face complex and frequently changing regulatory requirements, necessitating expert guidance on compliance, mergers and acquisitions, product launch strategies, and brand management.

By region, North America accounted for the largest market share in 2024.

The global healthcare consulting services market is segmented into North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2024, North America accounted for the largest market share. The large share of this segment is attributed to the highly developed healthcare infrastructure, substantial healthcare spending, widespread adoption of digital health technologies, and strong regulatory frameworks. The presence of leading healthcare consulting firms, advanced payer-provider models, and continuous investment in value-based care, AI, and patient experience further reinforces North America's leadership in the sector.

The breakdown of primary participants is as mentioned below:

- By Company Type - Tier 1 (31%), Tier 2 (28%), and Tier 3 (41%)

- By Designation - C-level Executives (31%), Director-level (25%), and Managers (44%)

- By Region - North America (45%), Europe (28%), the Asia Pacific (20%), Latin America (4%), and the Middle East & Africa (3%)

Key Players

The prominent players in this market are Accenture Plc (Ireland), Cognizant Technology Solutions Corporation (US), Deloitte (UK), McKinsey & Company (UK), PwC (UK), Ernst & Young Global Limited (EY) (UK), Huron Consulting Group Inc. (US), and KPMG (UK), among others.

Research Coverage

- The report studies the healthcare consulting services market based on service type, end user, and region.

- The report analyzes factors (drivers, restraints, opportunities, and challenges) affecting the market growth.

- The report evaluates the market's opportunities and challenges for stakeholders and details the competitive landscape for market leaders.

- The report studies micro-markets regarding their growth trends, prospects, and contributions to the total healthcare consulting services market.

- The report forecasts the revenue of market segments in five regions.

Reasons to Buy the Report

The report can help established and new entrants/smaller firms gauge the market's pulse, which, in turn, would help them garner a greater share. Firms purchasing the report could use one or a combination of the five strategies mentioned below.

This report provides insights into the following pointers:

- Analysis of key drivers (Growing rate of digitization in healthcare, Increasing adoption of big data analytics, IoT, and cloud deployment in the healthcare industry, changing healthcare landscape with respect to regulatory compliance and technological evolution, decreasing number of in-house experts in the end-use industries, rising level of government support for HCIT solutions, growing need for structural changes and new business models in the healthcare industry, increasing number of patients suffering from various chronic and infectious diseases, and increasing pressure to reduce the rising healthcare costs), restraints (rising number of concerns regarding data confidentiality, increasing number of hidden costs of consulting services), opportunities (growing demand for cloud consulting, increasing potential for healthcare consulting services in the emerging markets, increasing consolidation in the healthcare industry), and challenges (rising number of multi-sourcing approaches, high cost of consulting services) influencing the growth of the healthcare consulting services market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the healthcare consulting services market.

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various healthcare consulting services solutions across regions.

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the Healthcare consulting services market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the healthcare consulting services market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakdown of primary interviews

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 SUPPLY-SIDE ANALYSIS

- 2.2.2 BOTTOM-UP APPROACH

- 2.2.3 COMPANY PRESENTATIONS AND PRIMARY INTERVIEWS

- 2.2.4 GROWTH FORECAST

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.4.1 PARAMETRIC ASSUMPTIONS

- 2.4.2 STUDY-RELATED ASSUMPTIONS

- 2.5 RESEARCH LIMITATIONS

- 2.5.1 METHODOLOGY-RELATED LIMITATIONS

- 2.5.2 SCOPE-RELATED LIMITATIONS

- 2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 HEALTHCARE CONSULTING SERVICES MARKET OVERVIEW

- 4.2 ASIA PACIFIC HEALTHCARE CONSULTING SERVICES MARKET, BY COUNTRY AND END USER

- 4.3 HEALTHCARE CONSULTING SERVICES MARKET: REGIONAL GROWTH OPPORTUNITIES

- 4.4 HEALTHCARE CONSULTING SERVICES MARKET: REGIONAL MIX

- 4.5 HEALTHCARE CONSULTING SERVICES MARKET: EMERGING VS. DEVELOPED MARKETS

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growing trend of digitization

- 5.2.1.2 Increasing adoption of big data analytics, IoT, and cloud deployment

- 5.2.1.3 Changing healthcare landscape

- 5.2.1.4 Rising government support for HCIT solutions

- 5.2.1.5 Emergence of new business models

- 5.2.1.6 Growing incidence of chronic and infectious diseases

- 5.2.1.7 Need for data security

- 5.2.1.8 Increasing pressure to reduce healthcare costs

- 5.2.2 RESTRAINTS

- 5.2.2.1 Data confidentiality concerns

- 5.2.2.2 Hidden costs of consulting services

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rising trend of consolidation

- 5.2.3.2 Opportunities in emerging markets

- 5.2.3.3 Consistent rise in mergers and acquisitions

- 5.2.4 CHALLENGES

- 5.2.4.1 Rising number of multi-sourcing approaches

- 5.2.1 DRIVERS

- 5.3 INDUSTRY TRENDS

- 5.3.1 DIGITAL TRANSFORMATION IN HEALTHCARE

- 5.3.2 SHIFT TOWARD VALUE-BASED CARE

- 5.3.3 FOCUS ON PATIENT-CENTRIC CARE

- 5.3.4 RISING IMPORTANCE OF SOCIAL DETERMINANTS OF HEALTH

- 5.3.5 EXPANDING USE OF DATA ANALYTICS

- 5.3.6 GROWTH OF PRECISION MEDICINE

- 5.4 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.5 INDICATIVE PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICING ANALYSIS, BY TYPE OF SERVICE

- 5.5.2 INDICATIVE PRICING ANALYSIS, BY REGION

- 5.6 VALUE CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Machine learning

- 5.9.1.2 Artificial intelligence

- 5.9.1.3 Cloud computing

- 5.9.1.4 Big data and advanced analytics

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Robotic Process Automation (RPA)

- 5.9.2.2 Natural Language Processing (NLP)

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 Blockchain

- 5.9.3.2 Internet of Things (IoT)

- 5.9.1 KEY TECHNOLOGIES

- 5.10 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 ENHANCED PATIENT EXPERIENCE WITH PAPERLESS PROCESS

- 5.11.2 ADVANCED CLOUD SOLUTION TO IMPROVE HUMAN CAPITAL MANAGEMENT CAPABILITIES

- 5.11.3 DEVELOPMENT OF RISK MANAGEMENT PLANS FOR EFFECTIVE TREATMENT

- 5.12 REGULATORY LANDSCAPE

- 5.12.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.12.2 REGULATORY ANALYSIS

- 5.12.2.1 North America

- 5.12.2.2 Europe

- 5.12.2.3 Asia Pacific

- 5.12.2.4 Middle East & Africa

- 5.12.2.5 Latin America

- 5.13 PORTER'S FIVE FORCES ANALYSIS

- 5.13.1 BARGAINING POWER OF SUPPLIERS

- 5.13.2 BARGAINING POWER OF BUYERS

- 5.13.3 THREAT OF NEW ENTRANTS

- 5.13.4 THREAT OF SUBSTITUTES

- 5.13.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.14 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.14.2 BUYING CRITERIA

- 5.15 BUSINESS MODELS

- 5.16 IMPACT OF 2025 US TARIFF

- 5.16.1 INTRODUCTION

- 5.16.2 KEY TARIFF RATES

- 5.16.3 PRICE IMPACT ANALYSIS

- 5.16.4 IMPACT ON COUNTRY/REGION

- 5.16.4.1 US

- 5.16.4.2 Europe

- 5.16.4.3 Asia Pacific

- 5.16.5 IMPACT ON END-USE INDUSTRIES

6 HEALTHCARE CONSULTING SERVICES MARKET, BY TYPE OF SERVICE

- 6.1 INTRODUCTION

- 6.2 IT/DIGITAL TRANSFORMATION CONSULTING

- 6.2.1 RISING DEMAND FOR MODERNIZATION AND VALUE-BASED CARE DELIVERY TO AID GROWTH

- 6.3 STRATEGY CONSULTING

- 6.3.1 RAPID TECHNOLOGICAL ADVANCEMENTS TO FACILITATE GROWTH

- 6.4 OPERATIONS CONSULTING

- 6.4.1 TRANSITION FROM FEE-FOR-SERVICE TO COORDINATED CARE MODEL TO SUSTAIN GROWTH

- 6.5 FINANCIAL CONSULTING

- 6.5.1 RISING NEED FOR OPTIMIZED REVENUE CYCLE MANAGEMENT TO STIMULATE GROWTH

- 6.6 HR & TALENT CONSULTING

- 6.6.1 ONGOING SHORTAGE OF HEALTHCARE PROFESSIONALS TO PROMOTE GROWTH

- 6.7 MARKETING, SALES, AND COMMERCIALIZATION CONSULTING

- 6.7.1 INNOVATIONS IN DRUG DEVELOPMENT AND MEDICAL TECHNOLOGY TO DRIVE MARKET

- 6.8 REGULATORY & COMPLIANCE

- 6.8.1 RAPID ADOPTION OF DIGITAL HEALTH TECHNOLOGIES TO AUGMENT GROWTH

- 6.9 R&D CONSULTING

- 6.9.1 GROWING DEMAND FOR NEW DRUGS TO BOOST MARKET

- 6.10 PUBLIC HEALTH CONSULTING

- 6.10.1 INCREASING INVESTMENTS IN PUBLIC HEALTH INFRASTRUCTURE TO FOSTER GROWTH

- 6.11 OTHER CONSULTING SERVICES

7 HEALTHCARE CONSULTING SERVICES MARKET, BY END USER

- 7.1 INTRODUCTION

- 7.2 GOVERNMENT BODIES

- 7.2.1 GROWING INVESTMENTS IN MODERNIZING DIGITAL AND TECHNOLOGY INFRASTRUCTURE TO FUEL MARKET

- 7.3 HEALTHCARE PROVIDERS

- 7.3.1 HOSPITALS

- 7.3.1.1 Growing need for telehealth and remote care to propel market

- 7.3.2 AMBULATORY CARE CENTERS

- 7.3.2.1 Rising demand for convenient and patient-centered services to bolster growth

- 7.3.3 LONG-TERM CARE FACILITIES

- 7.3.3.1 Booming geriatric population to contribute to growth

- 7.3.4 DIAGNOSTIC & IMAGING CENTERS

- 7.3.4.1 Rising global demand for early disease detection, precision diagnostics, and outpatient imaging services to favor growth

- 7.3.5 OTHER HEALTHCARE PROVIDERS

- 7.3.1 HOSPITALS

- 7.4 HEALTH INSURANCE PAYERS

- 7.4.1 PRIVATE PAYERS

- 7.4.1.1 Need for regulatory compliance to encourage growth

- 7.4.2 PUBLIC PAYERS

- 7.4.2.1 Growing digital transformation initiatives to boost market

- 7.4.1 PRIVATE PAYERS

- 7.5 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 7.5.1 EVOLVING LIFE SCIENCES LANDSCAPE TO SPUR GROWTH

- 7.6 MEDICAL DEVICE COMPANIES

- 7.6.1 GROWING FOCUS OF MEDICAL DEVICE COMPANIES ON CUTTING-EDGE TECHNOLOGY TO DRIVE MARKET

- 7.7 OTHER END USERS

8 HEALTHCARE CONSULTING SERVICES MARKET, BY REGION

- 8.1 INTRODUCTION

- 8.2 NORTH AMERICA

- 8.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 8.2.2 US

- 8.2.2.1 Advanced infrastructure and high healthcare spending to augment growth

- 8.2.3 CANADA

- 8.2.3.1 Shift toward technology-driven integrated healthcare model to spur growth

- 8.3 EUROPE

- 8.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 8.3.2 GERMANY

- 8.3.2.1 Increasing emphasis on electronic documentation and compliance to spur growth

- 8.3.3 UK

- 8.3.3.1 Need for sectoral restructuring to accelerate growth

- 8.3.4 FRANCE

- 8.3.4.1 Need to ensure interoperability and compatibility among healthcare IT systems to aid growth

- 8.3.5 ITALY

- 8.3.5.1 Expansion of digital health sector to support growth

- 8.3.6 SPAIN

- 8.3.6.1 Growing digitization of healthcare systems to boost market

- 8.3.7 REST OF EUROPE

- 8.4 ASIA PACIFIC

- 8.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 8.4.2 JAPAN

- 8.4.2.1 Increasing adoption of information technology in medical care and home nursing to promote growth

- 8.4.3 CHINA

- 8.4.3.1 Favorable government initiatives to bolster growth

- 8.4.4 INDIA

- 8.4.4.1 Growing adoption of connected healthcare ecosystem to boost market

- 8.4.5 REST OF ASIA PACIFIC

- 8.5 LATIN AMERICA

- 8.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 8.5.2 BRAZIL

- 8.5.2.1 Ongoing efforts to modernize healthcare infrastructure to promote growth

- 8.5.3 MEXICO

- 8.5.3.1 Rising healthcare costs to contribute to growth

- 8.5.4 REST OF LATIN AMERICA

- 8.6 MIDDLE EAST & AFRICA

- 8.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 8.6.2 GCC COUNTRIES

- 8.6.2.1 Increasing investments in healthcare infrastructure to contribute to growth

- 8.6.3 REST OF MIDDLE EAST & AFRICA

9 COMPETITIVE LANDSCAPE

- 9.1 OVERVIEW

- 9.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 9.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN HEALTHCARE CONSULTING SERVICES MARKET

- 9.3 REVENUE ANALYSIS, 2020-2024

- 9.4 MARKET SHARE ANALYSIS, 2024

- 9.5 COMPANY VALUATION AND FINANCIAL METRICS

- 9.6 BRAND/SOFTWARE COMPARISON

- 9.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 9.7.1 STARS

- 9.7.2 EMERGING LEADERS

- 9.7.3 PERVASIVE PLAYERS

- 9.7.4 PARTICIPANTS

- 9.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 9.7.5.1 Company footprint

- 9.7.5.2 Region footprint

- 9.7.5.3 Type of service footprint

- 9.7.5.4 End-user footprint

- 9.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 9.8.1 PROGRESSIVE COMPANIES

- 9.8.2 RESPONSIVE COMPANIES

- 9.8.3 DYNAMIC COMPANIES

- 9.8.4 STARTING BLOCKS

- 9.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 9.8.5.1 Detailed list of key startups/SMEs

- 9.8.5.2 Competitive benchmarking of key startups/SMEs

- 9.9 COMPETITIVE SCENARIO

- 9.9.1 PRODUCT LAUNCHES

- 9.9.2 DEALS

- 9.9.3 EXPANSIONS

- 9.9.4 OTHER DEVELOPMENTS

10 COMPLNY PROFILE

- 10.1 KEY PLAYERS

- 10.1.1 ACCENTURE

- 10.1.1.1 Business overview

- 10.1.1.2 Products/Services/Solutions offered

- 10.1.1.3 Recent developments

- 10.1.1.3.1 Deals

- 10.1.1.4 MnM view

- 10.1.1.4.1 Key strengths

- 10.1.1.4.2 Strategic choices

- 10.1.1.4.3 Weaknesses and competitive threats

- 10.1.2 COGNIZANT

- 10.1.2.1 Business overview

- 10.1.2.2 Products/Services/Solutions offered

- 10.1.2.3 Recent developments

- 10.1.2.3.1 Deals

- 10.1.2.3.2 Expansions

- 10.1.2.4 MnM view

- 10.1.2.4.1 Key strengths

- 10.1.2.4.2 Strategic choices

- 10.1.2.4.3 Weaknesses and competitive threats

- 10.1.3 DELOITTE

- 10.1.3.1 Business overview

- 10.1.3.2 Products/Services/Solutions offered

- 10.1.3.3 Recent developments

- 10.1.3.3.1 Product launches

- 10.1.3.3.2 Deals

- 10.1.3.4 MnM view

- 10.1.3.4.1 Key strengths

- 10.1.3.4.2 Strategic choices

- 10.1.3.4.3 Weaknesses and competitive threats

- 10.1.4 MCKINSEY & COMPANY

- 10.1.4.1 Business overview

- 10.1.4.2 Products/Services/Solutions offered

- 10.1.4.3 Recent developments

- 10.1.4.3.1 Product launches

- 10.1.4.4 Recent developments

- 10.1.4.4.1 Deals

- 10.1.4.5 MnM view

- 10.1.4.5.1 Key strengths

- 10.1.4.5.2 Strategic choices

- 10.1.4.5.3 Weaknesses and competitive threats

- 10.1.5 BOSTON CONSULTING GROUP

- 10.1.5.1 Business overview

- 10.1.5.2 Products/Services/Solutions offered

- 10.1.5.3 Recent developments

- 10.1.5.3.1 Deals

- 10.1.5.4 MnM view

- 10.1.5.4.1 Key strengths

- 10.1.5.4.2 Strategic choices

- 10.1.5.4.3 Weaknesses and competitive threats

- 10.1.6 PWC

- 10.1.6.1 Business overview

- 10.1.6.2 Products/Services/Solutions offered

- 10.1.6.3 Recent developments

- 10.1.6.3.1 Deals

- 10.1.7 EY

- 10.1.7.1 Business overview

- 10.1.7.2 Products/Services/Solutions offered

- 10.1.7.3 Recent developments

- 10.1.7.3.1 Product launches

- 10.1.8 HURON CONSULTING GROUP INC.

- 10.1.8.1 Business overview

- 10.1.8.2 Products/Services/Solutions offered

- 10.1.8.3 Recent developments

- 10.1.8.3.1 Deals

- 10.1.9 KPMG

- 10.1.9.1 Business overview

- 10.1.9.2 Products/Services/Solutions offered

- 10.1.9.3 Recent developments

- 10.1.9.3.1 Product launches

- 10.1.9.3.2 DEALS

- 10.1.10 BAIN & COMPANY, INC.

- 10.1.10.1 Business overview

- 10.1.10.2 Products/Services/Solutions offered

- 10.1.10.3 Recent developments

- 10.1.10.3.1 Deals

- 10.1.11 IQVIA INC.

- 10.1.11.1 Business overview

- 10.1.11.2 Products/Services/Solutions offered

- 10.1.11.3 Recent developments

- 10.1.11.3.1 Product launches

- 10.1.11.4 Recent developments

- 10.1.11.4.1 Deals

- 10.1.12 L.E.K. CONSULTING

- 10.1.12.1 Business overview

- 10.1.12.2 Products/Services/Solutions offered

- 10.1.12.3 Recent developments

- 10.1.12.3.1 Deals

- 10.1.12.3.2 Expansions

- 10.1.13 NTT DATA, INC.

- 10.1.13.1 Business overview

- 10.1.13.2 Products/Services/Solutions offered

- 10.1.13.3 Recent developments

- 10.1.13.3.1 Product launches

- 10.1.13.3.2 Deals

- 10.1.14 OLIVER WYMAN, LLC

- 10.1.14.1 Business overview

- 10.1.14.2 Products/Services/Solutions offered

- 10.1.14.3 Recent developments

- 10.1.14.3.1 Product launches

- 10.1.14.3.2 Deals

- 10.1.15 SIMON-KUCHER & PARTNERS

- 10.1.15.1 Business overview

- 10.1.15.2 Products/Services/Solutions offered

- 10.1.16 IBM

- 10.1.16.1 Business overview

- 10.1.16.2 Products/Services/Solutions offered

- 10.1.16.3 Recent developments

- 10.1.16.3.1 Product launches

- 10.1.16.3.2 Deals

- 10.1.17 CLEARVIEW HEALTHCARE PARTNERS

- 10.1.17.1 Business overview

- 10.1.17.2 Products/Services/Solutions offered

- 10.1.17.3 Recent developments

- 10.1.17.3.1 Other developments

- 10.1.18 ALVAREZ & MARSAL HOLDINGS, LLC

- 10.1.18.1 Business overview

- 10.1.18.2 Products offered

- 10.1.18.3 Recent developments

- 10.1.18.3.1 Product launches

- 10.1.19 ZS ASSOCIATES

- 10.1.19.1 Business overview

- 10.1.19.2 Products/Services/Solutions offered

- 10.1.19.3 Recent developments

- 10.1.19.3.1 Product launches

- 10.1.19.3.2 Deals

- 10.1.20 CHARTIS

- 10.1.20.1 Business overview

- 10.1.20.2 Products/Services/Solutions offered

- 10.1.20.3 Recent developments

- 10.1.20.3.1 Deals

- 10.1.1 ACCENTURE

- 10.2 OTHER PLAYERS

- 10.2.1 QUALITY CREST HEALTHCARE CONSULTANTS PRIVATE LIMITED

- 10.2.2 LUCID HEALTH CONSULTING

- 10.2.3 BLUE MATTER CONSULTING

- 10.2.4 ISOS CONSULTANCY SERVICES PVT. LTD.

- 10.2.5 BACK BAY LIFE SCIENCE ADVISORS

11 APPENDIX

- 11.1 DISCUSSION GUIDE

- 11.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 11.3 CUSTOMIZATION OPTIONS

- 11.4 RELATED REPORTS

- 11.5 AUTHOR DETAILS