|

시장보고서

상품코드

1777131

의약품 첨가제 시장 : 제품별, 기능별, 제형별, 기능성 용도별, 지역별 예측(-2030년)Pharmaceutical Excipients Market by Product ((Organic, Inorganic)), Functionality, Formulation, Functionality Application - Global Forecast to 2030 |

||||||

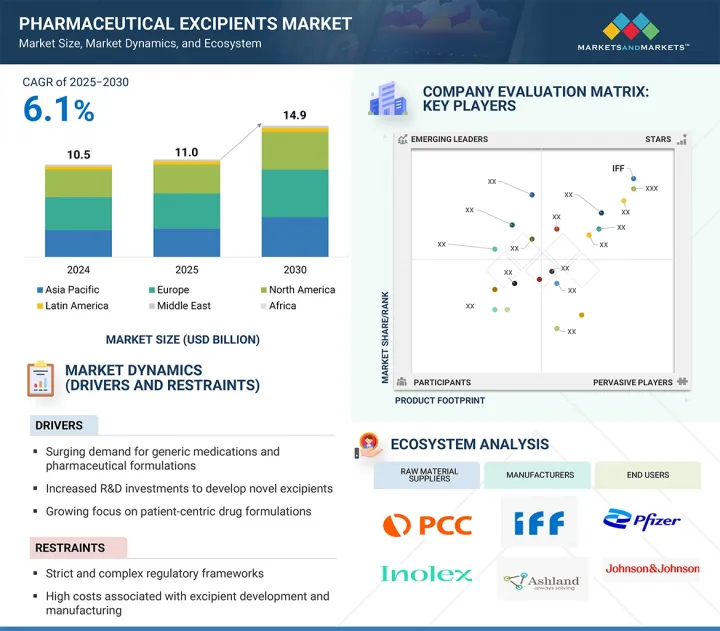

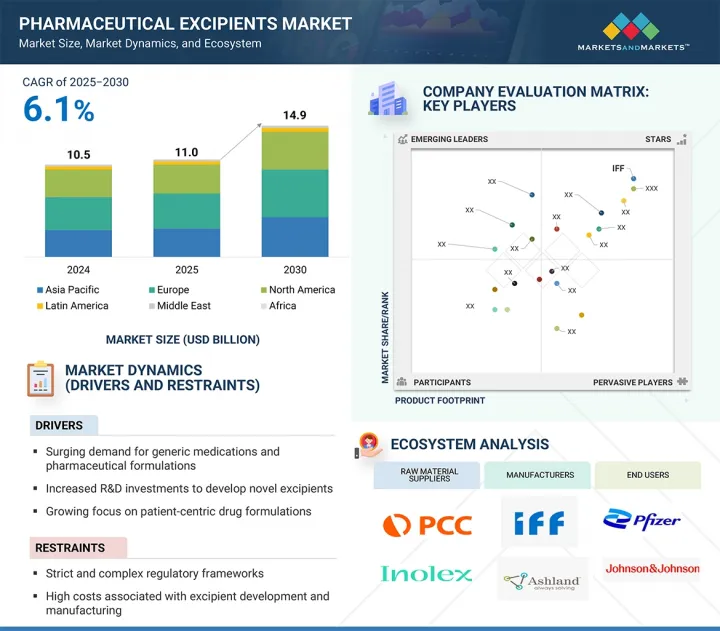

세계의 의약품 첨가제 시장 규모는 2025년 110억 3,000만 달러에서 2030년에는 148억 6,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR은 6.1%를 나타낼 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2023-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(10억 달러) |

| 부문별 | 제품별, 기능성별, 제형별, 기능성 용도별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

의약품 첨가제 시장의 확장은 주로 의약품 및 제네릭 의약품에 대한 수요의 급증에 의해 촉진되었으며, 새로운 첨가제 개발을 위한 R&D 투자가 향후 몇 년 동안 시장을 활성화할 것으로 예상됩니다. 또한, 제약 회사와의 파트너십 및 협력, 그리고 환자 중심 제형에 대한 강조가 증가함에 따라 유리한 시장 성장 기회가 제공될 것입니다. 그러나, 엄격한 규제와 높은 개발 비용이 시장을 제한할 것으로 예상됩니다.

기능별로 분류된 의약품 첨가제 시장에는 결합제, 현탁제 및 점도제, 충전제 및 희석제, 향료 및 감미료, 착색제, 코팅제, 윤활제 및 희석제, 방부제, 분해제, 유화제 및 기타 특수 용도가 포함됩니다. 이 중 충전제와 희석제는 특히 정제 및 캡슐과 같은 고형 경구 제형의 생산에 중요한 역할을 합니다. 경구용 의약품은 투여가 쉽고 환자의 순응도가 높기 때문에 가장 선호되는 투여 경로로 남아 있으며, 이에 따라 이러한 첨가제의 중요성은 계속해서 커지고 있습니다. 충전제 및 희석제는 소량의 활성 의약 성분을 함유한 제형에 부피를 제공하여 정확한 투여량과 함량 균일성을 보장합니다. 제조의 관점에서, 이러한 첨가제는 제형의 안정성, 가공의 용이성 및 대량 생산의 확장성에 크게 기여합니다. 또한, 혼합, 정제, 캡슐화 등의 공정을 단순화하면서 정제의 기계적 강도를 향상시킵니다. 환자의 경우, 이러한 부형제는 소아 및 노인 인구에게 중요한 요소인 입안에서의 느낌, 맛 및 취급성을 개선합니다. 의약품 제형이 점점 복잡해짐에 따라, 제어 방출 및 생체 이용률 향상을 지원하는 고성능의 다기능 충전제 및 희석제에 대한 수요도 증가하고 있으며, 이는 이 부형제 부문에서 상당한 성장 기회를 제시하고 있습니다.

의약품 첨가제 시장은 제형 유형에 따라 경구 제형, 국소 제형, 비경구 제형 및 기타 제형으로 분류됩니다. 이 중 경구 제형 부문은 2024년에 가장 큰 시장 점유율을 차지하며, 가장 널리 사용되고 전통적인 약물 전달 방법으로서의 우위를 반영했습니다. 경구 투여는 편의성, 비용 효율성 및 높은 환자 순응도로 인해 환자와 의료 서비스 제공자에게 선호되는 선택입니다. 이 부문은 정제, 캡슐 및 기타 고형 경구 제형에 대한 수요가 증가함에 따라 계속 확장되고 있습니다. 또한, 바이오 의약품 및 제네릭 의약품 산업의 급속한 성장은 경구 제품에서 의약품의 안정성, 용해도 및 생체 이용률을 향상시키는 고품질 부형제에 대한 수요를 촉진하는 데 중요한 역할을 하고 있습니다. 장기적인 약물 치료가 필요한 만성 질환의 유병률 증가와 의약품의 자가 투여 동향도 이 부문의 성장에 기여하고 있습니다. 그 결과, 제약 회사는 혁신적인 경구용 의약품 제형에 투자하고 있으며, 이러한 요구에 맞는 첨단 부형제의 필요성이 높아지고 있습니다.

아시아태평양 지역의 의약품 첨가제 시장은 예측 기간 동안 모든 지역 중 가장 높은 CAGR을 기록하며 견조한 성장을 보일 것으로 예상됩니다. 여러 가지 상호 관련된 요인들이 이러한 성장을 촉진하고 있습니다. 주요 장점 중 하나는 이 지역의 비용 효율적인 제조 능력으로, 이로 인해 이 지역은 의약품 생산 및 아웃소싱에 매력적인 허브로 자리매김했습니다. 인도, 중국, 한국과 같은 국가들은 풍부한 원자재, 숙련된 노동력, 의약품 R&D 및 수출 지향적 제조를 지원하는 유리한 정부 정책을 제공합니다. 또한, 아시아태평양 지역은 서구 시장에 비해 상대적으로 관대한 규제 체계를 갖추고 있어 제품 개발 및 시장 출시 시간을 단축할 수 있습니다. 1인당 소득의 급속한 증가, 건강 및 웰빙에 대한 인식의 제고, 의료비 지출의 증가는 제네릭 의약품에 대한 수요를 더욱 부추기고 있으며, 이는 의약품 첨가제 수요로까지 확대되고 있습니다. 또한, 생활 습관병의 급증과 고령 인구의 확대는 경구용 고형제 및 국소 제제 등 혁신적인 의약품 제형에 대한 수요를 증가시키고 있습니다. 이러한 동향은 지역 및 세계의 부형제 제조업체들이 사업을 확장하고, 인프라에 투자하며, 증가하는 지역 수요를 충족하기 위해 전략적 파트너십을 형성할 수 있는 중요한 기회를 창출하고 있습니다.

본 보고서에서는 세계의 의약품 첨가제 시장에 대해 조사했으며, 제품별, 기능별, 제형별, 기능성 용도별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 소개

- 시장 역학

- 고객사업에 영향을 주는 동향/혼란

- 가격 분석

- 밸류체인 분석

- 공급망 분석

- 생태계 분석

- 투자 및 자금조달 시나리오

- 기술 분석

- 특허 분석

- 무역 분석

- 주된 회의 및 이벤트(2025-2026년)

- 규제 상황

- Porter's Five Forces 분석

- 주요 이해관계자와 구매 기준

- AI/생성형 AI가 의약품 첨가제 시장에 미치는 영향

- 2025년 미국 관세가 의약품 첨가제 시장에 미치는 영향

제6장 의약품 첨가제 시장(제품별)

- 소개

- 유기 화학물질

- 무기 화학물질

- 기타 화학물질

제7장 의약품 첨가제 시장(기능별)

- 소개

- 충전제 및 희석제

- 현탁제 및 점도제

- 코팅제

- 결합제

- 향료 및 감미료

- 분해제

- 착색제

- 윤활제

- 방부제

- 유화제

- 기타

제8장 의약품 첨가제 시장(제형별)

- 소개

- 경구

- 국소

- 비경구

- 기타

제9장 의약품 첨가제 시장(기능성 용도별)

- 소개

- 안정제

- 미각 마스킹

- 조절 방출

- 용해성과 생체이용률 향상

- 기타

제10장 의약품 첨가제 시장(지역별)

- 소개

- 유럽

- 유럽의 거시경제 분석

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타

- 북미

- 북미의 거시경제 분석

- 미국

- 캐나다

- 아시아태평양

- 아시아태평양의 거시경제 분석

- 중국

- 일본

- 인도

- 한국

- 기타

- 라틴아메리카

- 고령화 인구 증가와 질병 이환율의 상승이 시장 성장을 견인

- 라틴아메리카의 거시 경제 분석

- 브라질

- 멕시코

- 기타

- 중동

- 시장을 활성화시키기 위해, 미포화 시장에 대한 주목이 높아지고 있다

- 중동의 거시경제 분석

- GCC 국가

- 기타

- 아프리카

- 성장을 가속하기 위해 대기업 제약 회사의 존재감을 높이는

- 아프리카의 거시경제 분석

제11장 경쟁 구도

- 소개

- 주요 진입기업의 전략/강점

- 수익 분석(2020-2024년)

- 시장 점유율 분석(2024년)

- 기업평가와 재무지표

- 브랜드/제품 비교

- 기업평가 매트릭스 : 주요 진입기업(2024년)

- 기업평가 매트릭스 : 스타트업/중소기업(2024년)

- 경쟁 시나리오

제12장 기업 프로파일

- 주요 진출기업

- INTERNATIONAL FLAVORS & FRAGRANCES INC.

- ADM

- ROQUETTE FRERES

- BASF SE

- EVONIK

- ASHLAND

- KERRY GROUP PLC

- MERCK

- ASSOCIATED BRITISH FOODS PLC

- WACKER CHEMIE AG

- AIR LIQUIDE

- DOW

- BERKSHIRE HATHAWAY(LUBRIZOL CORPORATION)

- COLORCON, INC.

- DFE PHARMA

- ACTYLIS

- CRODA INTERNATIONAL PLC

- CHEMIE TRADE

- GATTEFOSSE

- J. RETTENMAIER & SOHNE GMBH CO KG

- SHIN-ETSU CHEMICAL CO., LTD.

- 기타 기업

- INNOPHOS

- MEGGLE GMBH & CO. KG

- FUJI CHEMICAL INDUSTRIES CO., LTD.

- COREL PHARMA CHEM

- BIOGRUND

- NITIKA PHARMACEUTICAL SPECIALTIES PVT. LTD.

- RT VANDERBILT HOLDING COMPANY, INC.

- BENEO

- SIAGACHI INDUSTRIES

- JH NANHANG LIFE SCIENCES CO., LTD.

제13장 부록

HBR 25.08.01The global pharmaceutical excipients market is projected to reach USD 14.86 billion by 2030 from USD 11.03 billion in 2025, at a CAGR of 6.1% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | By Product, Functionality, Formulation, Functionality, and Application |

| Regions covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

The expansion of the Pharmaceutical Excipients market has been predominantly driven by the Surging demand for pharmaceutical products and generic medicines, and R&D investments for novel excipient development are predicted to uplift the market in the coming years. Additionally, partnerships and collaboration with pharmaceutical companies and increased emphasis on patient-centric formulations will provide lucrative market growth opportunities. However, regulatory stringency and steep development costs are predicted to restrict the market.

The fillers & diluents functionality held the highest share in the pharmaceutical excipients market.

The pharmaceutical excipients market, segmented by functionality, includes binders, suspending and viscosity agents, fillers and diluents, flavoring agents and sweeteners, colorants, coating agents, lubricants and glidants, preservatives, disintegrants, emulsifying agents, and other specialized roles. Among these, fillers and diluents play a critical role, especially in the production of solid oral dosage forms like tablets and capsules. Their importance continues to grow with the rising demand for oral medications, which remain the most preferred route due to ease of administration and patient compliance. Fillers and diluents provide bulk to formulations containing small amounts of active pharmaceutical ingredients and help ensure accurate dosage and improved content uniformity. From a manufacturing perspective, they contribute significantly to formulation stability, ease of processing, and scalability in mass production. They simplify processes such as blending, tableting, and encapsulation while enhancing the mechanical strength of tablets. For patients, these excipients improve mouthfeel, taste, and handling, which are crucial factors for pediatric and geriatric populations. As drug formulations become more complex, the demand for high-performance, multifunctional fillers and diluents that support controlled release and bioavailability enhancement is also rising, presenting significant growth opportunities in this excipient category.

The oral formulations segment reported the highest share of the formulations segment in 2024.

The pharmaceutical excipients market is categorized based on formulation types into oral formulations, topical formulations, parenteral formulations, and other formulations. Among these, the oral formulations segment held the largest market share in 2024, reflecting its dominance as the most widely used and traditional drug delivery method. The convenience, cost-effectiveness, and high patient compliance associated with oral administration make it a preferred choice for patients and healthcare providers. This segment continues to expand due to the rising demand for tablets, capsules, and other solid oral dosage forms. Furthermore, the rapid growth of the biopharmaceutical and generics industries is playing a pivotal role in driving demand for high-quality excipients that enhance drug stability, solubility, and bioavailability in oral products. The increasing prevalence of chronic conditions requiring long-term medication and the trend toward self-administration of drugs also contribute to the growth of this segment. As a result, pharmaceutical companies are investing in innovative oral drug formulations, boosting the need for advanced excipients tailored to these needs.

Asia Pacific is expected to grow at the highest CAGR in the global pharmaceutical excipients market from 2025 to 2030.

The pharmaceutical excipients market in the Asia Pacific region is expected to grow robustly and register the highest CAGR among all regions during the forecast period. Several interrelated factors are driving this expansion. One of the key advantages is the region's cost-effective manufacturing capabilities, which make it an attractive hub for pharmaceutical production and outsourcing. Countries like India, China, and South Korea offer abundant raw material availability, skilled labor, and favorable government policies that support pharmaceutical R&D and export-oriented manufacturing. Additionally, the Asia Pacific region has relatively lenient regulatory frameworks compared to Western markets, which accelerates product development and time-to-market. The rapid rise in per capita income, growing awareness of health and wellness, and increased healthcare spending are further fueling demand for generic drugs and, by extension, pharmaceutical excipients. Moreover, a surge in lifestyle-related chronic diseases and expanding geriatric populations have led to greater demand for innovative drug formulations, including oral solids and topical applications. These trends create significant opportunities for local and global excipient manufacturers to expand operations, invest in infrastructure, and form strategic partnerships to meet the growing regional demand.

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Supply Side-70% and Demand Side-30%

- By Designation: Managers-45%, CXOs and Directors-30%, and Executives-25%

- By Region: North America-40%, Europe-25%, the Asia Pacific-25%, Latin America-5%, and the Middle East & Africa-5%

List of Key Companies Profiled in the Report

Key players in the pharmaceutical excipients market include International Flavors & Fragrances Inc. (US), Ashland Inc. (US), Evonik Industries AG (Germany), BASF SE (Germany), Kerry Group plc (Ireland), Roquette Freres (France), MERCK KGaA (Germany), Associated British Foods plc (UK), ADM (US), Wacker Chemie AG (Germany), Air Liquide (France), DOW (US), Berkshire Hathaway Inc. (US), Colorcon (US), DFE PHARMA (Germany), Actylis (US), Croda International Plc(UK), Chemie Trade(India), Gattefosse (France), JRS Pharma(US), and Shin-Etsu Chemical Co., Ltd. (Japan).

Research Coverage

This research report categorizes the pharmaceutical excipients market by Product [(Organic (Oleochemicals, Carbohydrates, Petrochemicals, Proteins, and Other Organic Chemicals), Inorganic (Calcium Phosphate, Metal Oxides, Halites, Calcium Carbonate, Calcium Sulfate, Other Inorganic Chemicals), Other chemicals], by Functionality (Fillers & Diluents, Suspending & Viscosity Agents, Coating Agents, Binders, Flavoring Agents & Sweeteners, Disintegrants, Colorants, Lubricants & Glidants, Preservatives, Emulsifying Agents, and Other Functionalities), by formulation (Oral (Tablets, Capsules, Liquid Formulations and other oral formulations), Topical Formulations, Parenteral Formulations, and Other Formulations), by Functionality Application (Stabilizers, Taste Making, Modified Release, Solubility & Bioavailability Enhancement and Other Functionality Applications), and by Region (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa).

The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the pharmaceutical excipients market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products, solutions, key strategies, collaborations, partnerships, and agreements. New approvals/launches, collaborations, acquisitions, and recent developments associated with the pharmaceutical excipients market.

Reasons to Buy this Report

The report will help market leaders and new entrants by providing them with the closest approximations of the revenue numbers for the overall pharmaceutical excipients market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to better position their businesses and make suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide them with information on the key market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers (Surging demand for generic medications and pharmaceutical formulations, Increased R&D investments to develop novel excipients, A growing focus on patient-centric drug formulations, Strategic collaborations and partnerships with pharmaceutical firms), restraints (Strict and complex regulatory frameworks, High costs associated with excipient development and manufacturing), opportunities (Increasing interest in functional and multifunctional excipients, Technological advancements, particularly in nanotechnology, Expansion into emerging economies across Asia Pacific and Latin America), and Challenges (Ongoing concerns about excipient safety and quality standards, Limited availability and fluctuating costs of key raw materials).

- Product Development/Innovation: Detailed insights on upcoming products, research and development activities, and new product approvals/launches in the Pharmaceutical Excipients market.

- Market Development: Comprehensive information about lucrative markets; the report analyses the market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the pharmaceutical excipients market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players. A detailed analysis of the key industry players has been done to provide insights into their key strategies, product launches/ approvals, acquisitions, partnerships, agreements, collaborations, other recent developments, investment and funding activities, brand/product comparative analysis, and vendor valuation and financial metrics of the pharmaceutical excipients market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 REGIONAL SCOPE

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.3.4 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Objectives of secondary research

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakdown of primary interviews

- 2.1.2.2 Key objectives of primary research

- 2.1.1 SECONDARY DATA

- 2.2 MARKET ESTIMATION

- 2.2.1 GLOBAL MARKET ESTIMATION

- 2.2.1.1 Company revenue analysis (Bottom-up approach)

- 2.2.1.2 Revenue share analysis

- 2.2.1.3 MnM repository analysis

- 2.2.1.4 Primary interviews

- 2.2.2 INSIGHTS FROM PRIMARY EXPERTS

- 2.2.3 SEGMENTAL MARKET SIZE ESTIMATION (TOP-DOWN APPROACH)

- 2.2.1 GLOBAL MARKET ESTIMATION

- 2.3 GROWTH RATE PROJECTIONS

- 2.4 DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 PHARMACEUTICAL EXCIPIENTS MARKET OVERVIEW

- 4.2 NORTH AMERICA PHARMACEUTICAL EXCIPIENTS MARKET

- 4.3 PHARMACEUTICAL EXCIPIENTS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.4 PHARMACEUTICAL EXCIPIENTS MARKET: EMERGING VS. DEVELOPED MARKETS, 2025 VS. 2030 (USD MILLION)

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Surging demand for generic medications and pharmaceutical formulations.

- 5.2.1.2 Increased R&D investments to develop novel excipients

- 5.2.1.3 Growing focus on patient-centric drug formulations

- 5.2.1.4 Strategic collaborations and partnerships among pharmaceutical firms

- 5.2.2 RESTRAINTS

- 5.2.2.1 Strict and complex regulatory frameworks

- 5.2.2.2 High cost of excipient development and manufacturing

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing interest in functional and multifunctional excipients

- 5.2.3.2 Technological advancements in nanotechnology

- 5.2.3.3 Market opportunities in emerging economies

- 5.2.4 CHALLENGES

- 5.2.4.1 Ongoing concerns about excipient safety and quality standards

- 5.2.4.2 Limited availability and fluctuating costs of key raw materials

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 PRICING ANALYSIS

- 5.4.1 INDICATIVE PRICING ANALYSIS, BY KEY PLAYER

- 5.4.2 INDICATIVE PRICING ANALYSIS, BY REGION

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Co-processed excipient technology

- 5.9.1.2 Nanotechnology-based excipients

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 3D printing/additive manufacturing

- 5.9.2.2 Process Analytical Technology (PAT)

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 Artificial intelligence in formulation design

- 5.9.3.2 Green chemistry/sustainability tech

- 5.9.1 KEY TECHNOLOGIES

- 5.10 PATENT ANALYSIS

- 5.11 TRADE ANALYSIS

- 5.11.1 TRADE DATA FOR HS CODE 290545

- 5.11.1.1 Import data for HS code 290545

- 5.11.1.2 Export data for HS code 290545

- 5.11.2 TRADE DATA FOR HS CODE 350510

- 5.11.2.1 Import data for HS code 350510

- 5.11.2.2 Export data for HS code 350510

- 5.11.3 TRADE DATA FOR HS CODE 290532

- 5.11.3.1 Import data for HS code 290532

- 5.11.3.2 Export data for HS code 290532

- 5.11.4 TRADE DATA FOR HS CODE 283650

- 5.11.4.1 Import data for HS code 283650

- 5.11.4.2 Export data for HS code 283650

- 5.11.5 TRADE DATA FOR HS CODE 250100

- 5.11.5.1 Import data for HS code 250100

- 5.11.5.2 Export data for HS code 250100

- 5.11.6 TRADE DATA FOR HS CODE 290543

- 5.11.6.1 Import data for HS code 290543

- 5.11.6.2 Export data for HS code 290543

- 5.11.7 TRADE DATA FOR HS CODE 3912

- 5.11.7.1 Import data for HS code 3912

- 5.11.7.2 Export data for HS code 3912

- 5.11.1 TRADE DATA FOR HS CODE 290545

- 5.12 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.13 REGULATORY LANDSCAPE

- 5.13.1 REGULATORY FRAMEWORK

- 5.13.1.1 US

- 5.13.1.2 Europe

- 5.13.1.3 China

- 5.13.1.4 India

- 5.13.1.5 Brazil

- 5.13.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13.1 REGULATORY FRAMEWORK

- 5.14 PORTER'S FIVE FORCES ANALYSIS

- 5.14.1 BARGAINING POWER OF SUPPLIERS

- 5.14.2 BARGAINING POWER OF BUYERS

- 5.14.3 THREAT OF NEW ENTRANTS

- 5.14.4 THREAT OF SUBSTITUTES

- 5.14.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.15.2 KEY BUYING CRITERIA

- 5.16 IMPACT OF AI/GEN AI ON PHARMACEUTICAL EXCIPIENTS MARKET

- 5.16.1 INTRODUCTION

- 5.16.2 MARKET POTENTIAL OF AI ON PHARMACEUTICAL EXCIPIENTS

- 5.16.3 AI USE CASES

- 5.16.4 KEY COMPANIES IMPLEMENTING AI

- 5.16.5 FUTURE OF GENERATIVE AI IN PHARMACEUTICAL EXCIPIENT ECOSYSTEM

- 5.17 IMPACT OF 2025 US TARIFF ON PHARMACEUTICAL EXCIPIENTS MARKET

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 IMPACT ON COUNTRY/REGION

- 5.17.4.1 North America

- 5.17.4.1.1 US

- 5.17.4.2 Europe

- 5.17.4.3 Asia Pacific

- 5.17.4.1 North America

- 5.17.5 IMPACT ON END-USE INDUSTRIES

6 PHARMACEUTICAL EXCIPIENTS MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- 6.2 ORGANIC CHEMICALS

- 6.2.1 OLEOCHEMICALS

- 6.2.1.1 Fatty alcohols

- 6.2.1.1.1 Need for improved drug absorption to augment growth

- 6.2.1.2 Mineral stearates

- 6.2.1.2.1 Wide use of magnesium stearates as excipients in nutraceutical and pharmaceutical formulations to drive market

- 6.2.1.3 Glycerin

- 6.2.1.3.1 Non-toxic, colorless, and odorless properties to encourage growth

- 6.2.1.4 Other oleochemicals

- 6.2.1.1 Fatty alcohols

- 6.2.2 CARBOHYDRATES

- 6.2.2.1 Sugars

- 6.2.2.1.1 Actual sugars

- 6.2.2.1.1.1 Growing use of actual sugars in pediatric formulations to propel market

- 6.2.2.1.1.2 Lactose

- 6.2.2.1.1.3 Sucrose

- 6.2.2.1.1.4 Dextrose (D-Glucose)

- 6.2.2.1.2 Sugar alcohols

- 6.2.2.1.2.1 Surging trend in consumer demand for healthier alternatives to conventional sweeteners to fuel market

- 6.2.2.1.2.2 Sorbitol

- 6.2.2.1.2.3 Mannitol

- 6.2.2.1.2.4 Other sugar alcohols

- 6.2.2.1.3 Artificial sweeteners

- 6.2.2.1.3.1 Increasing use of sugar substitutes to favor growth

- 6.2.2.1.1 Actual sugars

- 6.2.2.2 Cellulose

- 6.2.2.2.1 Microcrystalline cellulose

- 6.2.2.2.1.1 Versatility, safety, and cost-effectiveness to facilitate growth

- 6.2.2.2.2 Cellulose ethers

- 6.2.2.2.2.1 Higher effectiveness than other water-soluble polymers to fuel market

- 6.2.2.2.3 CMC & croscarmellose sodium

- 6.2.2.2.3.1 Growing trend of sourcing CMC from more viable alternatives to boost market

- 6.2.2.2.4 Cellulose esters

- 6.2.2.2.4.1 Increasing focus on targeted and sustained-release drug delivery systems to sustain growth

- 6.2.2.2.1 Microcrystalline cellulose

- 6.2.2.3 Starch

- 6.2.2.3.1 Modified starch

- 6.2.2.3.1.1 Cold-water swelling and gel barrier formation capabilities to fuel market

- 6.2.2.3.2 Dried starch

- 6.2.2.3.2.1 Strong binding and coating properties to augment growth

- 6.2.2.3.3 Converted starch

- 6.2.2.3.3.1 Enhanced solubility and stability for drugs to foster growth

- 6.2.2.3.1 Modified starch

- 6.2.2.1 Sugars

- 6.2.3 PETROCHEMICALS

- 6.2.3.1 Glycols

- 6.2.3.1.1 Polyethylene glycol

- 6.2.3.1.1.1 Solubility, lubricity, and compatibility with APIs to drive market

- 6.2.3.1.2 Propylene glycol

- 6.2.3.1.2.1 Rising use of propylene glycol in oral and injectable formulations to foster growth

- 6.2.3.1.1 Polyethylene glycol

- 6.2.3.2 Povidones

- 6.2.3.2.1 Increasing demand for fast-dissolving tablets to spur growth

- 6.2.3.3 Mineral hydrocarbons

- 6.2.3.3.1 Petrolatum

- 6.2.3.3.1.1 Strong presence in topical pharmaceutical formulations to expedite growth

- 6.2.3.3.2 Mineral waxes

- 6.2.3.3.2.1 Utilization of mineral waxes in solid and semi-solid dosage to foster growth

- 6.2.3.3.3 Mineral oils

- 6.2.3.3.3.1 Extensive use of mineral oils as solvents and emollients to propel market

- 6.2.3.3.1 Petrolatum

- 6.2.3.4 Acrylic polymers

- 6.2.3.4.1 Wide use of acrylic polymers in controlled-release drug formulations to drive market

- 6.2.3.5 Other petrochemicals

- 6.2.3.1 Glycols

- 6.2.4 PROTEINS

- 6.2.4.1 Growing applications of proteins as carriers for microparticles and nanoparticles to propel market

- 6.2.5 OTHER ORGANIC CHEMICALS

- 6.2.1 OLEOCHEMICALS

- 6.3 INORGANIC CHEMICALS

- 6.3.1 CALCIUM PHOSPHATE

- 6.3.1.1 Chemical purity and low incompatibility with drugs to aid growth

- 6.3.2 METAL OXIDES

- 6.3.2.1 Availability of silicon oxides in the hydrophobic, hydrophilic, and granulated forms to aid market growth

- 6.3.3 HALITES

- 6.3.3.1 Increased utilization of halites in vaccines and controlled-release formulations to foster growth

- 6.3.4 CALCIUM CARBONATE

- 6.3.4.1 Short disintegration time and excellent mechanical strength to expedite growth

- 6.3.5 CALCIUM SULFATE

- 6.3.5.1 High quality and cost effectiveness to aid growth

- 6.3.6 OTHER INORGANIC CHEMICALS

- 6.3.1 CALCIUM PHOSPHATE

- 6.4 OTHER CHEMICALS

7 PHARMACEUTICAL EXCIPIENTS MARKET, BY FUNCTIONALITY

- 7.1 INTRODUCTION

- 7.2 FILLERS & DILUENTS

- 7.2.1 IMPROVED COHESION AND DIRECT COMPRESSION TO AMPLIFY GROWTH

- 7.3 SUSPENDING & VISCOSITY AGENTS

- 7.3.1 DRUG STABILITY AND TASTE MASKING ADVANTAGES TO SUSTAIN GROWTH

- 7.4 COATING AGENTS

- 7.4.1 INCREASING USE OF SUSTAINED-RELEASE FORMULATIONS IN PHARMA INDUSTRY TO DRIVE MARKET

- 7.5 BINDERS

- 7.5.1 HIGHER FLUIDITY AND COMPRESSIBILITY TO STIMULATE GROWTH

- 7.6 FLAVORING AGENTS & SWEETENERS

- 7.6.1 NEED TO IMPROVE DRUG PALATABILITY TO ADVANCE GROWTH

- 7.7 DISINTEGRANTS

- 7.7.1 NEED FOR RAPID BREAK-UP OF SOLID DOSAGE FORMS TO FOSTER GROWTH

- 7.8 COLORANTS

- 7.8.1 INCREASING USE OF COLORING IN HARD AND SOFT GELATIN CAPSULES, TABLETS, ORAL LIQUIDS, AND TOPICAL CREAMS TO BOOST MARKET

- 7.9 LUBRICANTS & GLIDANTS

- 7.9.1 NON-TOXIC PROPERTIES TO FAVOR GROWTH

- 7.10 PRESERVATIVES

- 7.10.1 GROWING USE OF PRESERVATIVES IN PHARMACEUTICAL AND NUTRACEUTICAL INDUSTRY TO DRIVE MARKET

- 7.11 EMULSIFYING AGENTS

- 7.11.1 RISING USE OF SOLUBILITY ENHANCEMENT EXCIPIENTS IN LIQUID DRUG FORMULATIONS TO PROMOTE GROWTH

- 7.12 OTHER FUNCTIONALITIES

8 PHARMACEUTICAL EXCIPIENTS MARKET, BY FORMULATION

- 8.1 INTRODUCTION

- 8.2 ORAL FORMULATIONS

- 8.2.1 TABLETS

- 8.2.1.1 High palatability and portability to support growth

- 8.2.2 CAPSULES

- 8.2.2.1 Hard-gelatin capsules

- 8.2.2.1.1 Ease of manufacturing and versatility to boost market

- 8.2.2.2 Soft-gelatin capsules

- 8.2.2.2.1 Quick-release properties to contribute to growth

- 8.2.2.1 Hard-gelatin capsules

- 8.2.3 LIQUID FORMULATIONS

- 8.2.3.1 Rapid absorption from stomach and intestines to foster growth

- 8.2.4 OTHER ORAL FORMULATIONS

- 8.2.1 TABLETS

- 8.3 TOPICAL FORMULATIONS

- 8.3.1 GROWING DEMAND FOR TRANSDERMAL PATCHES AND SELF-ADHERING TRANSDERMAL DRUG DELIVERY SYSTEMS TO FUEL MARKET

- 8.4 PARENTERAL FORMULATIONS

- 8.4.1 EMERGENCE OF BIOLOGICAL MOLECULES TO EXPEDITE GROWTH

- 8.5 OTHER FORMULATIONS

9 PHARMACEUTICAL EXCIPIENTS MARKET, BY FUNCTIONALITY APPLICATION

- 9.1 INTRODUCTION

- 9.2 STABILIZERS

- 9.2.1 IMPROVED DRUG SHELF LIFE AND LESSER MANUFACTURING DEFECTS TO PROMOTE GROWTH

- 9.3 TASTE MASKING

- 9.3.1 GROWING PREFERENCE FOR BETTER-TASTING SOLID DOSAGE FORMS TO PROPEL MARKET

- 9.4 MODIFIED-RELEASE

- 9.4.1 INCREASING USE OF MODIFIED-RELEASE FORMULATIONS IN PHARMA INDUSTRY TO FOSTER GROWTH

- 9.5 SOLUBILITY & BIOAVAILABILITY ENHANCEMENT

- 9.5.1 INCREASING PREFERENCE FOR SOLUBLE COMPOUNDS TO ACCELERATE GROWTH

- 9.6 OTHER APPLICATIONS

10 PHARMACEUTICAL EXCIPIENTS MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 EUROPE

- 10.2.1 MACROECONOMIC ANALYSIS FOR EUROPE

- 10.2.2 GERMANY

- 10.2.2.1 Booming pharmaceutical manufacturing sector to aid growth

- 10.2.3 UK

- 10.2.3.1 Growing adoption of generics and development of novel excipients to fuel market

- 10.2.4 FRANCE

- 10.2.4.1 Large geriatric population to support growth

- 10.2.5 ITALY

- 10.2.5.1 Budgetary constraints and restricted healthcare spending to impede growth

- 10.2.6 SPAIN

- 10.2.6.1 High consumption of biologics to foster growth

- 10.2.7 REST OF EUROPE

- 10.3 NORTH AMERICA

- 10.3.1 MACROECONOMIC ANALYSIS FOR NORTH AMERICA

- 10.3.2 US

- 10.3.2.1 Well-developed healthcare infrastructure and research bases to aid growth

- 10.3.3 CANADA

- 10.3.3.1 Rising prevalence of cancer to contribute to growth

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC ANALYSIS FOR ASIA PACIFIC

- 10.4.2 CHINA

- 10.4.2.1 Emphasis on generics and off-patent drugs to drive market

- 10.4.3 JAPAN

- 10.4.3.1 Rapid growth of elderly population to augment growth

- 10.4.4 INDIA

- 10.4.4.1 High domestic demand for pharmaceuticals and export volume to boost market

- 10.4.5 SOUTH KOREA

- 10.4.5.1 Presence of leading contract research and development organizations to propel market

- 10.4.6 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 GROWING GERIATRIC POPULATION AND RISING DISEASE PREVALENCE ARE DRIVING MARKET GROWTH

- 10.5.2 MACROECONOMIC ANALYSIS FOR LATIN AMERICA

- 10.5.3 BRAZIL

- 10.5.3.1 Emerging opportunities for excipient manufacturers to drive market

- 10.5.4 MEXICO

- 10.5.4.1 Growing demand for affordable therapies to boost market

- 10.5.5 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST

- 10.6.1 GROWING FOCUS ON UNSATURATED MARKETS TO DRIVE MARKET

- 10.6.2 MACROECONOMIC ANALYSIS FOR MIDDLE EAST

- 10.6.3 GCC COUNTRIES

- 10.6.3.1 Expanding healthcare infrastructure expansion and localization of drug manufacturing to bolster growth

- 10.6.4 REST OF MIDDLE EAST

- 10.7 AFRICA

- 10.7.1 INCREASING PRESENCE OF MAJOR PHARMACEUTICAL COMPANIES TO AUGMENT GROWTH

- 10.7.2 MACROECONOMIC ANALYSIS FOR AFRICA

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN PHARMACEUTICAL EXCIPIENTS MARKET, 2022-2024

- 11.3 REVENUE ANALYSIS, 2020-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS

- 11.6 BRAND/PRODUCT COMPARISON

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.7.5 COMPETITIVE BENCHMARKING: KEY PLAYERS, 2024

- 11.7.5.1 Company footprint

- 11.7.5.2 Region footprint

- 11.7.5.3 Product footprint

- 11.7.5.4 Functionality footprint

- 11.7.5.5 Functionality application footprint

- 11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- 11.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.8.5.1 Detailed list of key startups/SMEs

- 11.8.5.2 Competitive benchmarking of key startups/SMEs

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES AND APPROVALS

- 11.9.2 DEALS

- 11.9.3 EXPANSIONS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 INTERNATIONAL FLAVORS & FRAGRANCES INC.

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Deals

- 12.1.1.3.2 Expansions

- 12.1.1.4 MnM view

- 12.1.1.4.1 Key strengths

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 ADM

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Key strengths

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 ROQUETTE FRERES

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches and approvals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 BASF SE

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Deals

- 12.1.4.3.2 Expansions

- 12.1.4.4 MnM view

- 12.1.4.4.1 Key strengths

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 EVONIK

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Expansions

- 12.1.5.4 MnM view

- 12.1.5.4.1 Key strengths

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses and competitive threats

- 12.1.6 ASHLAND

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches and approvals

- 12.1.7 KERRY GROUP PLC

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Deals

- 12.1.8 MERCK

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Deals

- 12.1.9 ASSOCIATED BRITISH FOODS PLC

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Deals

- 12.1.10 WACKER CHEMIE AG

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.11 AIR LIQUIDE

- 12.1.11.1 Business overview

- 12.1.11.2 Products offered

- 12.1.11.3 Recent developments

- 12.1.11.3.1 Product launches and approvals

- 12.1.12 DOW

- 12.1.12.1 Business overview

- 12.1.12.2 Products offered

- 12.1.13 BERKSHIRE HATHAWAY (LUBRIZOL CORPORATION)

- 12.1.13.1 Business overview

- 12.1.13.2 Products offered

- 12.1.13.3 Recent developments

- 12.1.13.3.1 Product launches and approvals

- 12.1.14 COLORCON, INC.

- 12.1.14.1 Business overview

- 12.1.14.2 Products offered

- 12.1.14.3 Recent developments

- 12.1.14.3.1 Product launches and approvals

- 12.1.14.3.2 Deals

- 12.1.14.3.3 Expansions

- 12.1.15 DFE PHARMA

- 12.1.15.1 Business overview

- 12.1.15.2 Products offered

- 12.1.15.3 Recent developments

- 12.1.15.3.1 Deals

- 12.1.16 ACTYLIS

- 12.1.16.1 Business overview

- 12.1.16.2 Products offered

- 12.1.16.3 Recent developments

- 12.1.16.3.1 Deals

- 12.1.17 CRODA INTERNATIONAL PLC

- 12.1.17.1 Business overview

- 12.1.17.2 Products offered

- 12.1.17.3 Recent developments

- 12.1.17.3.1 Deals

- 12.1.17.3.2 Expansions

- 12.1.18 CHEMIE TRADE

- 12.1.18.1 Business overview

- 12.1.18.2 Products offered

- 12.1.19 GATTEFOSSE

- 12.1.19.1 Business overview

- 12.1.19.2 Products offered

- 12.1.20 J. RETTENMAIER & SOHNE GMBH + CO KG

- 12.1.20.1 Business overview

- 12.1.20.2 Products offered

- 12.1.21 SHIN-ETSU CHEMICAL CO., LTD.

- 12.1.21.1 Business overview

- 12.1.21.2 Products offered

- 12.1.21.3 Recent developments

- 12.1.21.3.1 Deals

- 12.1.21.3.2 Expansions

- 12.1.1 INTERNATIONAL FLAVORS & FRAGRANCES INC.

- 12.2 OTHER PLAYERS

- 12.2.1 INNOPHOS

- 12.2.2 MEGGLE GMBH & CO. KG

- 12.2.3 FUJI CHEMICAL INDUSTRIES CO., LTD.

- 12.2.4 COREL PHARMA CHEM

- 12.2.5 BIOGRUND

- 12.2.6 NITIKA PHARMACEUTICAL SPECIALTIES PVT. LTD.

- 12.2.7 R.T. VANDERBILT HOLDING COMPANY, INC.

- 12.2.8 BENEO

- 12.2.9 SIAGACHI INDUSTRIES

- 12.2.10 JH NANHANG LIFE SCIENCES CO., LTD.

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS