|

시장보고서

상품코드

1782042

3D 직물 시장 예측(-2030년) : 제품 유형(유리섬유, 복합섬유, 스페이서, 탄소섬유, 커스터마이즈드 3D 방직기), 용도별(구조 부품, 보호 재료, 보강재, 단열 및 방음재, 열보호)3D Weaving Market by Glass Fiber, Composite Textile, Spacer, Carbon Fiber, Customized 3D Weaving, Structural Components, Protective Materials, Reinforcements, Insulation, Thermal Protective Applications - Global Forecast to 2030 |

||||||

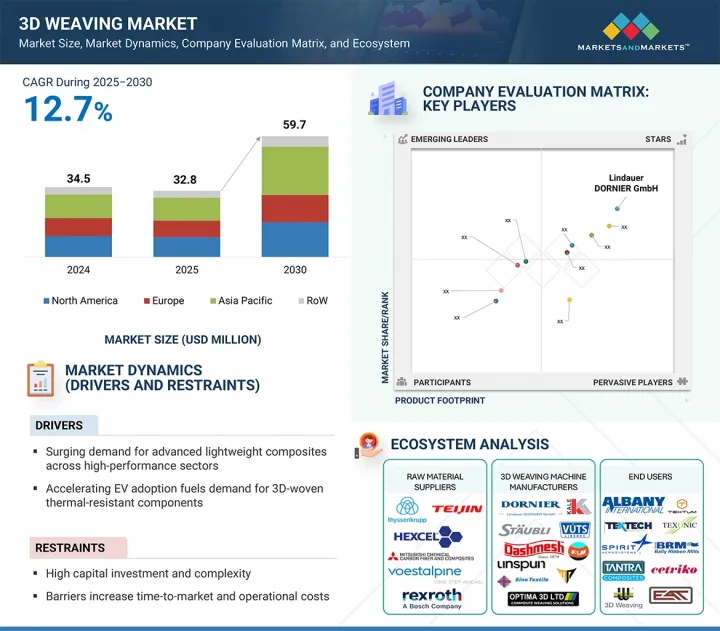

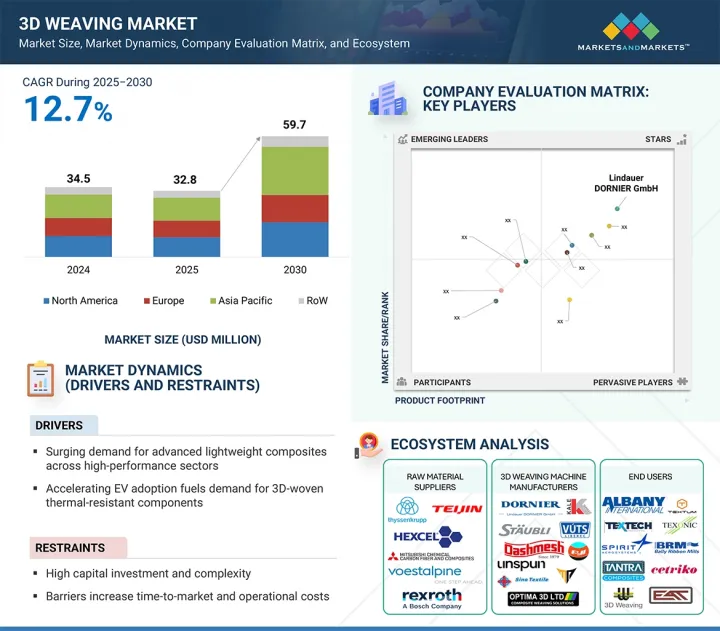

3D 직물 시장 규모는 2025년 3,280만 달러에서 예측 기간 중 12.7%의 CAGR로 추이하며, 2030년에는 5,970만 달러로 성장할 것으로 예측됩니다.

가볍고 고강도 소재에 대한 수요 증가가 3D 직기 도입을 촉진하는 주요 요인으로 작용하고 있습니다. 항공우주, 국방, 자동차 분야에서는 기계적 강도를 유지하거나 향상시키면서 구조물의 경량화를 도모하는 것이 연비 향상, 적재량 증가, 시스템 전체 성능 향상을 위해 필수적입니다. 기존의 복합재료 제조 기술로는 복잡하고 다방향에서 보강 구조를 만드는 것이 어렵다는 문제점이 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상연도 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러) |

| 부문별 | 제품 유형·최종사용자 산업·용도·지역별 |

| 대상 지역 | 북미·유럽·아시아태평양·기타 지역 |

그러나 3D 직조기는 완전히 통합된 다층 직조 구조를 만들 수 있으며, 우수한 강도 대 중량비, 박리 저항성, 높은 하중 지지력을 실현합니다. 이러한 특성은 항공기 날개 스퍼 및 기체 구조, 군용 장갑 시스템, 자동차 차체 구조와 같은 용도에서 특히 중요합니다. 이러한 산업들이 성능 향상과 지속가능성을 점점 더 중요시하는 가운데, 3D 직조기는 완성형에 가까운 첨단 프리폼을 효율적이고 비용 효율적으로 제조할 수 있다는 장점으로 차세대 소재 제조에 있으며, 매우 중요한 기술로 평가받고 있습니다.

"유리섬유 직조기 부문이 2024년가장 큰 점유율을 차지할 것입니다. "

2024년, 유리섬유 직조기는 광범위한 산업 응용, 높은 비용 효율성 및 재료로서의 우수한 특성으로 인해 가장 큰 시장 점유율을 차지했습니다. 유리섬유는 강도, 내구성, 열 안정성, 경량성을 겸비하여 자동차, 건설, 해양, 재생에너지 등의 분야에 이상적인 소재입니다. 탄소섬유나 아라미드 섬유에 비해 저렴한 비용으로 복잡하고 고성능의 복합재료를 제조할 수 있으며, 채택이 확대되고 있습니다. 또한 다축 제어, 자동화, 정확도 향상과 같은 기술 혁신을 통해 효율성과 생산 확장성을 높여 가볍고 지속가능한 소재에 대한 전 세계적인 수요에 대응하고 있습니다. 아시아태평양과 같이 산업과 인프라가 빠르게 성장하는 지역에서는 저렴한 가격의 복합재료 솔루션에 대한 수요가 유리섬유 직조기의 우위를 지원하고 있습니다.

"최종사용자 산업별로는 항공우주 및 방위 부문이 예측 기간 중 가장 높은 CAGR을 보일 것으로 예측됩니다. "

항공우주 및 방위 산업은 예측 기간 중 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 이는 동 분야에서 고성능과 안전성이 중시되는 용도에 대해 첨단 복합소재에 대한 의존도가 높아지고 있기 때문입니다. 항공기 제조업체 및 방산 관련 기업이 구조 효율 향상, 경량화, 연비 개선을 위해 3D 섬유복합재에 대한 수요가 크게 증가하고 있습니다. 이 소재들은 높은 강도 대 중량비, 내충격성, 박리 감소와 같은 우수한 기계적 특성을 가지고 있으며, 기체 패널, 날개 대들보, 터빈 블레이드, 방탄복과 같은 부품에 적합합니다.

3D 직조기는 정밀하고 일관된 복잡한 다방향 섬유 구조의 제조에 필수적이며, 니어 네트 모양 성형 및 재료 폐기물을 줄일 수 있습니다. 또한 국방 장비의 고도화에 대한 투자 확대, 차세대 항공기 생산 증가, 경량 군 장비에 대한 전 세계적인 관심 증가는 전문 3D 섬유 기술에 대한 수요를 촉진하고 있습니다. 앞으로도 항공우주 및 국방 분야는 소재기술의 발전과 함께 가장 역동적이고 성장성이 높은 3D 직조기 도입 분야가 될 것으로 예측됩니다.

세계의 3D 직물 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인의 분석, 기술·특허의 동향, 법규제 환경, 사례 연구, 시장 규모 추이·예측, 각종 구분·지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

- 시장 역학

- 촉진요인

- 억제요인

- 기회

- 과제

- 고객 사업에 영향을 미치는 동향/혼란

- 공급망 분석

- 에코시스템 분석

- 기술 분석

- 특허 분석

- 무역 분석

- 관세와 규제 상황

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 생성형 AI/AI가 3D 직물 시장에 미치는 영향

- 2025년 미국 관세의 영향 : 3D 직물 시장

제6장 3D 직물 시장 : 제품 유형별

- 유리섬유 방직기

- 복합섬유 방직기

- 스페이서방직기

- 탄소섬유 방직기

- 커스터마이즈드 3D 방직기

제7장 3D 직물 시장 : 용도별

- 구조 부품

- 보호재

- 보강재

- 단열·방음재

- 내하중 복합재료

- 장식/디자인

- 열보호

제8장 3D 직물 시장 : 최종사용자 산업별

- 항공우주·방위

- 자동차

- 건설·인프라

- 스포츠 용품

- 에너지 & 상품

- 헬스케어

- 기타

제9장 3D 직물 시장 : 지역별

- 북미

- 거시경제 전망

- 미국

- 캐나다

- 멕시코

- 유럽

- 거시경제 전망

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 기타

- 아시아태평양

- 거시경제 전망

- 중국

- 일본

- 인도

- 기타

- 기타 지역

- 중동 및 아프리카

- 남미

제10장 경쟁 구도

- 개요

- 주요 참여 기업의 전략/강점

- 시장 점유율 분석

- 제품/브랜드 비교

- 기업 평가 매트릭스 : 주요 기업

- 경쟁 시나리오

제11장 기업 개요

- 주요 기업

- LINDAUER DORNIER GMBH

- STAUBLI INTERNATIONAL AG

- UNSPUN

- DASHMESH JACQUARD AND POWERLOOM PVT. LTD.

- VUTS A.S.

- HEFEI FANYUAN INSTRUMENT CO., LTD.

- SINO TEXTILE MACHINERY

- OPTIMA 3D LTD

- KALE TEXNIQUE

- MARJAN POLYMER INDUSTRIES

- 기타 기업

- ALBANY INTERNATIONAL CORP.

- TEX TECH INDUSTRIES

- TEXONIC

- TEXTUM OPCO, LLC

- SPIRIT AEROSYSTEMS, INC.

- BALLY RIBBON MILLS

- TANTRA COMPOSITE TECHNOLOGIES PVT. LTD.

- CETRIKO

- EAT GMBH

- 3D WEAVING

제12장 부록

KSA 25.08.11The 3D weaving market is projected to grow from USD 32.8 million in 2025 to USD 59.7 million by 2030, at a CAGR of 12.7%. The increasing demand for lightweight and high-strength materials is a major factor driving the adoption of 3D weaving machines. In aerospace, defense, and automotive sectors, reducing structural weight while maintaining or improving mechanical strength is essential for better fuel efficiency, higher payload capacity, and improved overall system performance. Traditional composite manufacturing approaches often face challenges in producing complex, multi-directional reinforcements.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By product type, end-use industry, application, and region |

| Regions covered | North America, Europe, APAC, RoW |

However, 3D weaving machines enable the creation of fully integrated, multilayer woven structures that offer excellent strength-to-weight ratios, delamination resistance, and load-bearing capabilities. These features are especially valuable in aerospace components like wing spars, fuselage sections, military armor systems, and automotive body structures. As these industries continue to focus on performance and sustainability, the ability of 3D weaving machines to produce advanced, near-net-shape preforms efficiently and cost-effectively makes them a crucial technology for next-generation material manufacturing.

"Glass fiber weaving machines accounted for the largest market share in 2024"

In 2024, glass fiber weaving machines held the largest market share, driven by their wide industrial use, cost efficiency, and favorable material qualities. Glass fiber combines strength, durability, thermal stability, and lightness, making it ideal for automotive, construction, marine, and renewable energy sectors. Its ability to produce complex, high-performance composites at lower costs than carbon or aramid fibers has boosted adoption. Technological advances, like multi-axis control, automation, and improved precision, have increased efficiency and scalability, meeting the global demand for lightweight, sustainable materials. In regions like the Asia Pacific, with rapid industrial and infrastructure growth, the demand for affordable composite solutions sustains the dominance of glass fiber weaving machines.

"Aerospace & defense end-use industry is projected to register the highest CAGR during the forecast period."

The aerospace and defense end-use industry is expected to see the highest CAGR during the forecast period in the 3D weaving market, driven by the sector's increasing dependence on advanced composite materials for high-performance and safety-critical applications. As aircraft manufacturers and defense contractors aim to improve structural efficiency, reduce weight, and enhance fuel economy, the demand for 3D woven composites has risen significantly. These materials provide superior mechanical properties, such as high strength-to-weight ratios, impact resistance, and reduced delamination, making them ideal for components like fuselage panels, wing spars, turbine blades, and ballistic armor.

3D weaving machines are essential for creating complex, multi-directional fiber structures with high precision and consistency. They support near-net-shape manufacturing and help reduce material waste. Additionally, increased investments in defense upgrades, growing production of next-generation aircraft, and a rising global focus on lightweight military gear further boost demand for specialized 3D weaving technology. As aerospace and defense fields expand material capabilities, the industry is expected to remain the most dynamic and fastest-growing segment for 3D weaving machine adoption in the coming years.

"China is estimated to lead growth in the Asia Pacific 3D weaving market during the forecast period."

China is expected to dominate the growth of the Asia Pacific 3D weaving market during the forecast period, thanks to its robust industrial foundation, cost-effective manufacturing, and strategic investments in advanced sectors like aerospace, defense, automotive, and energy. Government initiatives such as "Made in China 2025" are boosting domestic innovation and the adoption of high-performance composite technologies. With increasing demand for lightweight, durable materials and a growing emphasis on R&D in material science and textile engineering, China remains well-positioned to be the leading force behind regional market growth.

Breakdown of Primaries

Various executives from key organizations operating in the 3D weaving market, including CEOs, marketing directors, and innovation and technology directors, were interviewed.

- By Company Type: Tier 1-35%, Tier 2- 40%, and Tier 3-25%

- By Designation: C-level Executives-30%, Directors-40%, and Others-30%

- By Region: North America-40%, Asia Pacific-32%, Europe-23%, and RoW-5%

The 3D weaving market is led by globally established players such as Lindauer DORNIER GmbH (Germany), Staubli International AG (Switzerland), Unspun (US), Dashmesh Jacquard and Powerloom Pvt. Ltd. (India), VUTS a.s. (Czech Republic), Hefei Fanyuan Instrument Co., Ltd. (China), Sino Textile Machinery (China), Optima 3D Ltd (UK), Kale Texnique (India), Marjan Polymer Industries (Pakistan), Albany International Corp. (US), Tex Tech Industries (US), Texonic (Canada), Textum OPCO, LLC (US), Spirit AeroSystems, Inc. (US), Bally Ribbon Mills (US), Tantra Composite Technologies Pvt. Ltd. (India), Cetriko (Spain), EAT GmbH (Germany), and 3D Weaving (Belgium). The study provides an in-depth competitive analysis of these key players in the 3D weaving market, including their company profiles, recent developments, and major market strategies.

Study Coverage

The report segments the 3D weaving market and forecasts its size by product type, end-use industries, application, and region. It also discusses the drivers, restraints, opportunities, and challenges related to the market. Additionally, it provides a detailed view of the market across four main regions-North America, Europe, Asia Pacific, and RoW. A supply chain analysis is included, along with key players and their competitive analysis of the 3D weaving ecosystem.

Key Benefits of Buying the Report

- Analysis of key drivers (enhanced structural integrity and minimized material waste), restraints (high capital investment and operational complexity), opportunities (emergence of hybrid composites and smart textiles), and challenges (extended product development and qualification cycles) influencing the growth of the 3D weaving market

- Products/Solution/Service Development/Innovation: Detailed insights into upcoming technologies and R&D activities in the 3D weaving market

- Market Development: Comprehensive information about lucrative markets-the report analyses the 3D weaving market across varied regions

- Market Diversification: Exhaustive information about new products/solutions/services, untapped geographies, recent developments, and investments in the 3D weaving market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Lindauer DORNIER GmbH (Germany), Staubli International AG (Switzerland), Unspun (US), Hefei Fanyuan Instrument Co., Ltd (China), and VUTS a.s. (Czech Republic) among others

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.1.2 List of key secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 List of primary interview participants

- 2.1.2.3 Breakdown of primaries

- 2.1.2.4 Key industry insights

- 2.1.3 SECONDARY AND PRIMARY RESEARCH

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION METHODOLOGY

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.4 RISK ANALYSIS

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN 3D WEAVING MARKET

- 4.2 3D WEAVING MARKET, BY END-USE INDUSTRY

- 4.3 3D WEAVING MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Surging demand for advanced lightweight composites across high-performance sectors

- 5.2.1.2 Accelerating EV adoption fuels demand for 3D-woven thermal-resistant components

- 5.2.1.3 Customization and complex geometry capabilities

- 5.2.1.4 Enhanced structural integrity and minimized material waste

- 5.2.2 RESTRAINTS

- 5.2.2.1 High capital investment and operational complexity

- 5.2.2.2 Regulatory and certification barriers increase time-to-market and operational costs

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Emergence of hybrid composites and smart textiles

- 5.2.3.2 Sustainable production through advanced 3D weaving technology

- 5.2.3.3 Rising demand for customized military and tactical gear

- 5.2.3.4 Expansion into marine and subsea engineering applications

- 5.2.4 CHALLENGES

- 5.2.4.1 Cybersecurity vulnerabilities threaten operational continuity in digitized 3D weaving environments

- 5.2.4.2 Intensifying competition, market saturation, profitability, and differentiation

- 5.2.4.3 Extended product development and qualification cycles

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 TECHNOLOGY ANALYSIS

- 5.6.1 KEY TECHNOLOGIES

- 5.6.1.1 Real-Time Monitoring & Feedback Control

- 5.6.1.2 Computer-Aided Design & Manufacturing (CAD/CAM)

- 5.6.2 COMPLEMENTARY TECHNOLOGIES

- 5.6.2.1 Simulation & Digital Twin Technology

- 5.6.2.2 AI & Machine Learning Algorithms

- 5.6.3 ADJACENT TECHNOLOGIES

- 5.6.3.1 Braiding Machines

- 5.6.1 KEY TECHNOLOGIES

- 5.7 PATENT ANALYSIS

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT DATA FOR HS CODE 8446

- 5.8.2 EXPORT DATA FOR HS CODE 8446

- 5.9 TARIFF AND REGULATORY LANDSCAPE

- 5.9.1 TARIFF ANALYSIS

- 5.9.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.9.3 KEY REGULATIONS

- 5.10 PORTER'S FIVE FORCE ANALYSIS

- 5.10.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.10.2 THREAT OF SUBSTITUTES

- 5.10.3 BARGAINING POWER OF BUYERS

- 5.10.4 BARGAINING POWER OF SUPPLIERS

- 5.10.5 THREAT OF NEW ENTRANTS

- 5.11 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.11.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.11.2 BUYING CRITERIA

- 5.12 IMPACT OF GEN AI/AI ON 3D WEAVING MARKET

- 5.13 IMPACT OF 2025 US TARIFFS-3D WEAVING MARKET

- 5.13.1 INTRODUCTION

- 5.13.2 KEY TARIFF RATES

- 5.13.3 PRICE IMPACT ANALYSIS

- 5.13.4 IMPACT ON COUNTRIES/REGIONS

- 5.13.4.1 US

- 5.13.4.2 Europe

- 5.13.4.3 Asia Pacific

- 5.13.5 IMPACT ON END-USE INDUSTRIES

6 3D WEAVING MARKET, BY PRODUCT TYPE

- 6.1 INTRODUCTION

- 6.2 GLASS FIBER WEAVING MACHINES

- 6.2.1 COST-EFFECTIVENESS, DURABILITY, AND SUSTAINABLE COMPOSITES TO DRIVE ADOPTION

- 6.3 COMPOSITE TEXTILE WEAVING MACHINES

- 6.3.1 VERSATLIITY AND MULTI-FIBER 3D FABRIC PRODUCTION TO DRIVE GROWTH

- 6.4 SPACER WEAVING MACHINES

- 6.4.1 SPACER WEAVING MACHINES OFFER BREATHABLE, CUSHIONED, AND STRUCTURALLY ADAPTIVE 3D FABRICS

- 6.5 CARBON FIBER WEAVING MACHINES

- 6.5.1 HIGH-PRECISION CARBON FIBER WEAVING MACHINES FOR LIGHTWEIGHT AND HIGH STRENGTH 3D STRUCTURES

- 6.6 CUSTOMIZED 3D WEAVING MACHINES

- 6.6.1 CUSTOMIZED MACHINES MEET COMPLEX, SPECIALIZED, AND HIGH PRECISION FABRICATION NEEDS

7 3D WEAVING MARKET, BY APPLICATION

- 7.1 INTRODUCTION

- 7.2 STRUCTURAL COMPONENTS

- 7.2.1 PRECISION-ENGINEERED 3D WOVEN PREFORMS FOR HIGH STRENGTH STRUCTURAL COMPONENT APPLICATIONS ACROSS CRITICAL INDUSTRIES

- 7.3 PROTECTIVE MATERIALS

- 7.3.1 3D WOVEN PROTECTIVE MATERIALS FOR IMPACT AND SAFETY APPLICATIONS

- 7.4 REINFORCEMENTS

- 7.4.1 REINFORCEMENT FABRICS MADE WITH 3D WEAVING FOR STRONGER COMPOSITES

- 7.5 INSULATION

- 7.5.1 3D WOVEN MATERIALS FOR THERMAL AND SOUND INSULATION USES

- 7.6 LOAD-BEARING COMPOSITES

- 7.6.1 DURABLE 3D WOVEN COMPOSITES FOR SUPPORTING HEAVY LOADS

- 7.7 DECORATIVE/DESIGN APPLICATIONS

- 7.7.1 CUSTOM 3D WOVEN FABRICS FOR AESTHETIC AND FUNCTIONAL DESIGN NEEDS

- 7.8 THERMAL PROTECTION APPLICATIONS

- 7.8.1 HEAT-RESISTANT 3D WOVEN MATERIALS FOR HIGH TEMPERATURE ENVIRONMENTS

8 3D WEAVING MARKET, BY END-USE INDUSTRY

- 8.1 INTRODUCTION

- 8.2 AEROSPACE & DEFENSE

- 8.2.1 LEADING DEMAND FOR LIGHTWEIGHT AND HIGH-STRENGTH COMPOSITE STRUCTURES

- 8.3 AUTOMOTIVE

- 8.3.1 ACCELERATING ADOPTION OF 3D WOVEN COMPONENTS IN LIGHTWEIGHT VEHICLE PLATFORMS

- 8.4 CONSTRUCTION & INFRASTRUCTURE

- 8.4.1 ENHANCING STRUCTURAL DURABILITY WITH 3D WOVEN REINFORCEMENTS

- 8.5 SPORTING GOODS

- 8.5.1 SUPPORTING PERFORMANCE AND SAFETY IN LIGHTWEIGHT EQUIPMENT DESIGN

- 8.6 ENERGY & GOODS

- 8.6.1 DELIVERING DURABLE COMPOSITES FOR WIND AND THERMAL APPLICATIONS

- 8.7 HEALTHCARE

- 8.7.1 ENABLING ERGONOMIC, BREATHABLE, AND BIOCOMPATIBLE COMPOSITE PRODUCTS

- 8.8 OTHER END-USE INDUSTRIES

9 3D WEAVING MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 NORTH AMERICA

- 9.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 9.2.2 US

- 9.2.2.1 Technological leadership and high-value application demand

- 9.2.3 CANADA

- 9.2.3.1 Emerging market with R&D-driven growth showcases opportunities

- 9.2.4 MEXICO

- 9.2.4.1 Industrial expansion and localization of composite manufacturing

- 9.3 EUROPE

- 9.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 9.3.2 UK

- 9.3.2.1 Advanced R&D and aerospace-centric adoption

- 9.3.3 GERMANY

- 9.3.3.1 Automotive lightweighting and infrastructure composites

- 9.3.4 FRANCE

- 9.3.4.1 Energy sector composites and advanced protective materials

- 9.3.5 SPAIN

- 9.3.5.1 Renewable energy infrastructure and technical construction materials

- 9.3.6 ITALY

- 9.3.6.1 Design-centric innovation and marine industry adoption to support demand

- 9.3.7 REST OF EUROPE

- 9.4 ASIA PACIFIC

- 9.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 9.4.2 CHINA

- 9.4.2.1 Industrial scaling and infrastructure-based demand

- 9.4.3 JAPAN

- 9.4.3.1 Precision engineering and consumer electronics applications

- 9.4.4 INDIA

- 9.4.4.1 Defense innovation and infrastructure growth to propel adoption

- 9.4.5 REST OF ASIA PACIFIC

- 9.5 REST OF THE WORLD

- 9.5.1 MIDDLE EAST & AFRICA

- 9.5.1.1 Emerging applications and strategic infrastructure focus driving market growth

- 9.5.2 SOUTH AMERICA

- 9.5.2.1 Localized innovation and sustainable manufacturing drive adoption

- 9.5.1 MIDDLE EAST & AFRICA

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2024-2025

- 10.3 MARKET SHARE ANALYSIS, 2024

- 10.4 PRODUCT/BRAND COMPARISON

- 10.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.5.1 STARS

- 10.5.2 EMERGING LEADERS

- 10.5.3 PERVASIVE PLAYERS

- 10.5.4 PARTICIPANTS

- 10.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.5.5.1 Company footprint

- 10.5.5.2 Region Footprint

- 10.5.5.3 Product Type Footprint

- 10.5.5.4 Application Footprint

- 10.5.5.5 End-use Industry footprint

- 10.6 COMPETITIVE SCENARIO

- 10.6.1 DEALS

11 COMPANY PROFILES

- 11.1 INTRODUCTION

- 11.2 KEY PLAYERS

- 11.2.1 LINDAUER DORNIER GMBH

- 11.2.1.1 Business overview

- 11.2.1.2 Products/Solutions/Services offered

- 11.2.1.3 MnM view

- 11.2.1.3.1 Key strengths/Right to win

- 11.2.1.3.2 Strategic choices

- 11.2.1.3.3 Weaknesses/Competitive threats

- 11.2.2 STAUBLI INTERNATIONAL AG

- 11.2.2.1 Business overview

- 11.2.2.2 Products/Solutions/Services offered

- 11.2.2.3 MnM view

- 11.2.2.3.1 Key strengths/Right to win

- 11.2.2.3.2 Strategic choices

- 11.2.2.3.3 Weaknesses/Competitive threats

- 11.2.3 UNSPUN

- 11.2.3.1 Business overview

- 11.2.3.2 Products/Solutions/Services offered

- 11.2.3.3 Recent developments

- 11.2.3.3.1 Deals

- 11.2.3.4 MnM view

- 11.2.3.4.1 Key strengths/Right to win

- 11.2.3.4.2 Strategic choices

- 11.2.3.4.3 Weaknesses/Competitive threats

- 11.2.4 DASHMESH JACQUARD AND POWERLOOM PVT. LTD.

- 11.2.4.1 Business overview

- 11.2.4.2 Products/Solutions/Services offered

- 11.2.4.3 MnM view

- 11.2.4.3.1 Key strengths/Right to win

- 11.2.4.3.2 Strategic choices

- 11.2.4.3.3 Weaknesses/Competitive threats

- 11.2.5 VUTS A.S.

- 11.2.5.1 Business overview

- 11.2.5.2 Products/Solutions/Services offered

- 11.2.5.3 MnM view

- 11.2.5.3.1 Key strengths/Right to win

- 11.2.5.3.2 Strategic choices

- 11.2.5.3.3 Weaknesses/Competitive threats

- 11.2.6 HEFEI FANYUAN INSTRUMENT CO., LTD.

- 11.2.6.1 Business overview

- 11.2.6.2 Products/Solutions/Services offered

- 11.2.7 SINO TEXTILE MACHINERY

- 11.2.7.1 Business overview

- 11.2.7.2 Products/Solutions/Services offered

- 11.2.8 OPTIMA 3D LTD

- 11.2.8.1 Business overview

- 11.2.8.2 Products/Solutions/Services offered

- 11.2.9 KALE TEXNIQUE

- 11.2.9.1 Business overview

- 11.2.9.2 Products/Solutions/Services offered

- 11.2.10 MARJAN POLYMER INDUSTRIES

- 11.2.10.1 Business overview

- 11.2.10.2 Products/Solutions/Services offered

- 11.2.1 LINDAUER DORNIER GMBH

- 11.3 OTHER PLAYERS

- 11.3.1 ALBANY INTERNATIONAL CORP.

- 11.3.2 TEX TECH INDUSTRIES

- 11.3.3 TEXONIC

- 11.3.4 TEXTUM OPCO, LLC

- 11.3.5 SPIRIT AEROSYSTEMS, INC.

- 11.3.6 BALLY RIBBON MILLS

- 11.3.7 TANTRA COMPOSITE TECHNOLOGIES PVT. LTD.

- 11.3.8 CETRIKO

- 11.3.9 EAT GMBH

- 11.3.10 3D WEAVING

12 APPENDIX

- 12.1 INSIGHTS FROM INDUSTRY EXPERTS

- 12.2 DISCUSSION GUIDE

- 12.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.4 CUSTOMIZATION OPTIONS

- 12.5 RELATED REPORTS

- 12.6 AUTHOR DETAILS