|

시장보고서

상품코드

1790683

히트 펌프 시장 : 용도별, 최종 사용자별, 정격 용량별, 냉매별, 기술별, 유형별, 지역별 예측(-2030년)Heat Pump Market by Technology, Refrigerant, Type, Rated Capacity, End User, Application, and Region - Global Forecast to 2030 |

||||||

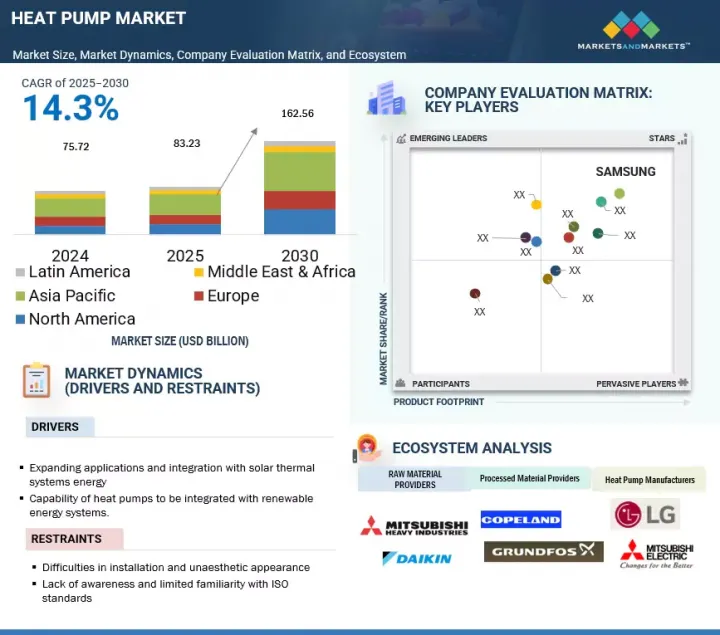

세계의 히트 펌프 시장 규모는 2025년 추정 832억 3,000만 달러에서 2030년까지 1,625억 6,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 14.3%가 될 것으로 보입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 대수 | 금액(100만 달러) 및 대(UNIT) |

| 부문별 | 용도별, 최종 사용자별, 정격 용량별, 냉매별, 기술별, 유형별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

히트 펌프는 태양광 발전 및 풍력 발전과 같은 재생에너지 소스와 통합되어 보다 지속 가능하고 환경 친화적인 냉난방 솔루션을 제공합니다.

ATW(Air to Water) 히트 펌프 부문은 예측 기간 동안 2위 점유율을 차지할 것으로 예측됩니다. 공대수 히트 펌프는 주택 분야 외에도 다양한 용도로 사용됩니다. 공대수 히트 펌프의 사용은 상업용 건물, 산업 환경 및 레크리에이션 시설(수영장)으로 확장되어 이 기술의 보급을 크게 확대하고 있습니다. 이는 공대수 히트 펌프를 이용한 냉난방 용도의 시프트를 의미하며, 전체 지역의 히트 펌프 수요 증가로 이어집니다.

세계의 히트 펌프 시장에서는 가역성 히트 펌프 분야가 예측기간 동안 두 번째로 높은 CAGR을 나타낼 것으로 예측됩니다. 히트 펌프의 성능 계수는 보통 3-5로 높고 에너지 투입량에 대해 300%-500% 많은 냉난방 출력을 얻을 수 있습니다. 따라서 에너지 효율이라는 측면은 주택과 상업 고객 모두에게 중요한 판매 포인트입니다. 장기적인 비용 절감과 환경 친화적 영향이 신흥국 시장에서도 선진국 시장에서도 리버시블 시스템에 대한 수요를 높이고 있습니다.

예측 기간 동안 유럽은 히트 펌프 시장에서 두 번째로 급성장할 것으로 예측됩니다. 이 지역에서는 수입화석연료에 대한 의존도를 줄이고 재생가능에너지 이용을 늘리려는 움직임이 있기 때문에 히트 펌프에 대한 관심이 높아지고 있습니다. 히트 펌프는 특히 태양광 발전과 같은 재생가능한 전력원과 결합할 때 운전 비용이 낮아 주택과 산업 분야에서 보급이 진행되고 있습니다. 유럽의 적극적인 탈탄소화 목표, 정부의 높은 인센티브, 기후 정책, 난방 분야의 기술 진보가 이 지역의 히트 펌프 수요 증가에 박차를 가하고 있습니다.

SAMSUNG(한국), DENSO CORPORATION(일본), Midea(중국), Panasonic Holdings Corporation(일본), Mitsubishi Electric Corporation(일본), LG Electronics(한국), Lennox International Inc.(미국), Fujitsu General(일본), Daikin Industries, Ltd.(일본), Cariler(The) Limited(인도), GEA Group Aktiengesellschaft(독일), Trane Technologies plc(아일랜드), Bosch Thermotechnology Corp.(독일), Guangzhou Sprsun New Energy Technology Development(중국), GLEN DIMPLEX GROUP(아일랜드), NIBE Industry AB(아일랜드), NIBE Industry AB(아일랜드) Hybrid Systems Limited(뉴질랜드), Evo Energy Technologies(호주), Namma Swadeshi(인도), EcoTech Solutions(인도), Dandelion Energy(미국), Zealux Electric Limited(중국)가 히트 펌프 시장의 주요 진출기업입니다. 본 조사에서는 히트 펌프 시장에서 이러한 주요 기업의 기업 프로파일, 최근 동향, 주요 시장 전략 등 상세한 경쟁 분석을 실천하고 있습니다.

본 보고서에서는 세계의 히트 펌프 시장을 기술, 유형, 냉매, 정격용량, 최종 사용자, 용도, 지역별로 정의, 기술, 예측했습니다. 또한 시장의 상세한 질적·양적 분석도 실시했습니다. 조사 범위는 히트 펌프 시장의 성장에 영향을 미치는 시장 촉진요인 및 과제 등 주요 요인에 대한 상세정보를 다룹니다. 주요 업계 진출 기업의 철저한 분석을 통해 사업 개요, 솔루션, 서비스, 계약, 파트너십, 합의, M&A 등 주요 전략, 히트 펌프 시장과 관련된 최근 동향에 대한 통찰력을 제공합니다. 이 보고서는 히트 펌프 생태계의 미래 신흥 기업의 경쟁 분석을 다루고 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 소개

- 시장 역학

- 고객사업에 영향을 주는 동향/혼란

- 가격 분석

- 공급망 분석

- 생태계 분석

- 기술 분석

- 무역 분석

- 2025-2026년의 주된 회의와 이벤트

- 규제 상황

- Porter's Five Forces 분석

- 주요 이해관계자와 구매 기준

- 특허 분석

- 사례 연구 분석

- 투자 및 자금조달 시나리오

- AI/생성형 AI가 히트 펌프 시장에 미치는 영향

- 2025년 미국 관세가 히트 펌프 시장에 미치는 영향

제6장 히트 펌프 시장(용도별)

- 소개

- 가열

- 난방 및 냉방

제7장 히트 펌프 시장(최종사용자별)

- 소개

- 주택

- 상업

- 공업

제8장 히트 펌프 시장(정격 용량별)

- 소개

- 10kW 미만

- 10-20kW

- 20-30kW

- 30kW 이상

제9장 히트 펌프 시장(냉매별)

- 소개

- R410A

- R407C

- R744

- R290

- R717

- 기타

제10장 히트 펌프 시장(기술별)

- 소개

- 공기 대 공기 히트 펌프

- ATW 히트 펌프

- 수원 히트 펌프

- 지열 히트 펌프

- 하이브리드 히트 펌프

- 태양광발전열(PVT) 히트 펌프

제11장 히트 펌프 시장(유형별)

- 소개

- 리버시블 히트 펌프

- 비 리버시블 히트 펌프

제12장 히트 펌프 시장(지역별)

- 소개

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타

- 유럽

- 프랑스

- 이탈리아

- 독일

- 영국

- 스페인

- 기타

- 북미

- 미국

- 캐나다

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타

- 라틴아메리카

- 브라질

- 멕시코

- 기타

제13장 경쟁 구도

- 개요

- 주요 참가 기업이 채용하는 전략(2020-2025년)

- 시장 점유율 분석, 2024년

- 시장 평가 프레임워크(2020-2024년)

- 수익 분석, 2020-2024년

- 브랜드/제품 비교

- 기업평가와 재무지표

- 기업평가 매트릭스 : 주요 진입기업, 2024년

- 기업평가 매트릭스 : 스타트업/중소기업, 2024년

- 경쟁 시나리오

제14장 기업 프로파일

- 주요 진출기업

- SAMSUNG

- DENSO CORPORATION

- MIDEA

- PANASONIC HOLDINGS CORPORATION

- MITSUBISHI ELECTRIC CORPORATION

- LG ELECTRONICS

- LENNOX INTERNATIONAL INC.

- FUJITSU GENERAL

- DAIKIN INDUSTRIES, LTD.

- CARRIER

- JOHNSON CONTROLS

- THERMAX LIMITED

- GEA GROUP AKTIENGESELLSCHAFT

- TRANE TECHNOLOGIES PLC

- BOSCH THERMOTECHNOLOGY CORP.

- 기타 기업

- GUANGZHOU SPRSUN NEW ENERGY TECHNOLOGY DEVELOPMENT CO., LTD.

- GLEN DIMPLEX GROUP

- NIBE

- RHEEM MANUFACTURING COMPANY

- ENERGEN HYBRID SYSTEMS LIMITED

- EVO ENERGY TECHNOLOGIES

- NAMMASWADESHI

- ECOTECH SOLUTIONS

- DANDELION ENERGY

- ZEALUX ELECTRIC LIMITED

제15장 부록

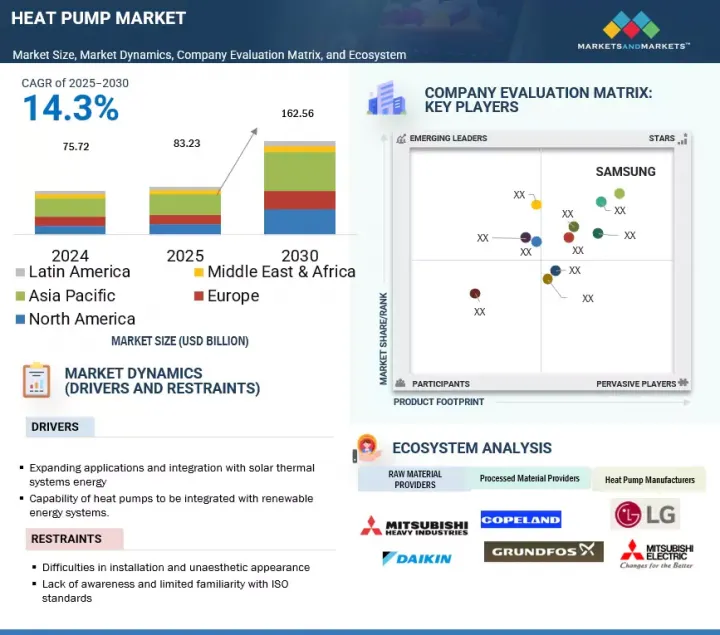

JHS 25.08.20The global heat pump market is estimated to reach USD 162.56 billion by 2030 from an estimated USD 83.23 billion in 2025, at a CAGR of 14.3% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD million) and Volume (Units) |

| Segments | Heat pump market by technology, type, refrigerant, rated capacity, end User, application, and region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

Heat pumps can be integrated with renewable energy sources such as solar and wind power, enabling more sustainable and eco-friendly heating and cooling solutions, which align with the global trend towards renewable energy adoption.

"Air-to-water heat pumps to be fastest-growing segment from 2025 to 2030"

The air-to-water segment is estimated to account for the second-largest share during the forecast period. Air-to-water heat pumps are used for a broader range of applications beyond the residential sector. Use of air-to-water pumps has extended into commercial buildings, industrial settings, and recreation facilities (swimming pools), considerably broadening the uptake of this technology. This signifies a shift in heating and cooling applications using air-to-water heat pumps, leading to the increased demand for heat pumps across the region.

"Reversible heat pumps to be second-fastest growing segment during forecast period"

In the heat pump market, the reversible heat pumps segment is projected to witness the second-highest CAGR during the forecast period. Their high coefficient of performance, normally between 3 and 5, shows that they can gain between 300% and 500% more heating or cooling output than the energy input." Hence, the energy efficiency aspect is a significant selling point for customers on both the residential and commercial sides. The long-term cost savings and eco-friendly impact fuel the demand for reversible systems in both developing and developed markets.

"Europe is expected to be the second-fastest growing region in the heat pump market."

Europe is expected to be the second-fastest growing heat pump market during the forecast period. The region's commitment to reducing reliance on imported fossil fuels and a move toward increasing the use of renewable energy has helped to foster excitement around heat pumps. Heat pumps have lower operating costs, especially when combined with renewable electricity sources such as solar, and are becoming popular in the residential and industrial sectors. Europe's aggressive decarbonization goals, high levels of government incentivization, climate policy, and ongoing advances in technology in the heating sector are fueling the increased demand for heat pumps in the region.

Breakdown of Primaries:

In-depth interviews have been conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among other experts, to obtain and verify critical qualitative and quantitative information and assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1 - 60%, Tier 2 - 25%, and Tier 3 - 15%

By Designation: C-Level - 35%, Director Level - 25%, and Others - 40%

By Region: Americas - 13%, Europe - 16%, Asia Pacific - 56%, Middle East & Africa - 15%

Note: The tiers of the companies are defined based on their total revenues as of 2024. Tier 1: > USD 1 billion, Tier 2: USD 500 million to USD 1 billion, and Tier 3: < USD 500 million.

Others include sales managers, engineers, and regional managers.

SAMSUNG (South Korea), DENSO CORPORATION (Japan), Midea (China), Panasonic Holdings Corporation (Japan), Mitsubishi Electric Corporation (Japan), LG Electronics (South Korea), Lennox International Inc. (US), Fujitsu General (Japan), Daikin Industries, Ltd. (Japan), Carrier (US), Johnson Controls (Ireland), Thermax Limited (India), GEA Group Aktiengesellschaft (Germany), Trane Technologies plc, (Ireland), Bosch Thermotechnology Corp. (Germany), Guangzhou Sprsun New Energy Technology Development Co., Ltd. (China), GLEN DIMPLEX GROUP (Ireland), NIBE Industry AB (Ireland), Rheem Manufacturing Company (US), Energen Hybrid Systems Limited (NewZealand), Evo Energy Technologies (Australia), Namma Swadeshi (India), EcoTech Solutions (India), Dandelion Energy (US), and Zealux Electric Limited (China) are the key players in the heat pump market. The study includes an in-depth competitive analysis of these key players in the heat pump market, with their company profiles, recent developments, and key market strategies.

Study Coverage:

The report defines, describes, and forecasts the global heat pump market by technology, type, refrigerant, rated capacity, end user, application, and region. It also offers a detailed qualitative and quantitative analysis of the market. The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the heat pump market. A thorough analysis of the key industry players has provided insights into their business overview, solutions, and services; key strategies such as contracts, partnerships, agreements, mergers & acquisitions; and recent developments associated with the heat pump market. This report covers the competitive analysis of upcoming startups in the heat pump ecosystem.

Key Benefits of Buying the Report

- The report includes the analysis of key drivers (Growing use of heat pumps beyond traditional heating and cooling applications, Capability of heat pumps to be integrated with renewable energy systems, Implementation of government policies and initiatives to promote use of energy-efficient heating and cooling systems), restraints (Difficulties in installation and unaesthetic appearance, Limited public awareness regarding benefits of heat pumps and lack of knowledge about heat pump standards among system vendors), opportunities (High focus of manufacturers on integrating IoT, ML, and AI technologies into heat pumps, Positive outlook toward use of geothermal energy, Increased sales of heat pumps in Europe), and challenges (Dependency on energy source for heat pump efficiency, High installation cost) influencing the growth of the heat pump market.

- Product Development/Innovation: The heat pump market is witnessing significant product development and innovation, driven by the growing demand for environmentally friendly, safe, and sustainable products. Companies are investing in developing advanced heat pump technologies for various applications.

- Market Development: SAMSUNG announced its partnership with Etopia, a UK-based smart building company, to deploy heat pumps in the residential sector in the UK. SAMSUNG will deploy 6,000 TDS plus heat pumps as part of the five-year smart home project in the UK.

- Market Diversification: Panasonic Holdings Corporation announced that it would invest about USD 150 million in its Czech plant by the fiscal year ending in March 2026 to strengthen the production of air-to-water heat pumps (A2W), which have been experiencing growing demand in Europe.

- Competitive Assessment: It includes an in-depth assessment of market shares, growth strategies, and service offerings of leading players, such as SAMSUNG (South Korea), DENSO CORPORATION (Japan), Midea (China), Panasonic Holdings Corporation (Japan), and Mitsubishi Electric Corporation (Japan), among others, in the heat pump market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.2 PRIMARY AND SECONDARY DATA

- 2.2.1 SECONDARY DATA

- 2.2.1.1 List of major secondary sources

- 2.2.1.2 Key data from secondary sources

- 2.2.2 PRIMARY DATA

- 2.2.2.1 List of primary interview participants

- 2.2.2.2 Key data from primary sources

- 2.2.2.3 Key industry insights

- 2.2.2.4 Breakdown of primaries

- 2.2.1 SECONDARY DATA

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.3.3 SUPPLY-SIDE ANALYSIS

- 2.3.3.1 Supply-side assumptions

- 2.3.3.2 Supply-side calculations

- 2.3.4 DEMAND-SIDE ANALYSIS

- 2.3.4.1 Demand-side assumptions

- 2.3.4.2 Demand-side calculations

- 2.4 GROWTH PROJECTION

- 2.5 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HEAT PUMP MARKET

- 4.2 HEAT PUMP MARKET, BY END USER

- 4.3 HEAT PUMP MARKET, BY TECHNOLOGY

- 4.4 HEAT PUMP MARKET, BY TYPE

- 4.5 HEAT PUMP MARKET, BY APPLICATION

- 4.6 HEAT PUMP MARKET, BY REFRIGERANT TYPE

- 4.7 HEAT PUMP MARKET, BY RATED CAPACITY

- 4.8 HEAT PUMP MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Transition to sustainable heating technologies

- 5.2.1.2 Government-led initiatives to promote use of sustainable and energy-efficient HVAC technologies

- 5.2.2 RESTRAINTS

- 5.2.2.1 High cost of installation

- 5.2.2.2 Space constraints associated with ground-source systems

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Emphasis on embedding IoT, ML, and AI technologies into heat pump systems

- 5.2.3.2 Enhanced performance of CO2 heat pumps

- 5.2.4 CHALLENGES

- 5.2.4.1 High installation cost

- 5.2.4.2 Dependency on energy source

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 PRICING ANALYSIS

- 5.4.1 PRICING RANGE OF HEAT PUMPS, BY TECHNOLOGY, 2024

- 5.4.2 AVERAGE SELLING PRICE TREND OF HEAT PUMPS, BY REGION, 2022-2024

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.5.1 RAW MATERIAL SUPPLIERS

- 5.5.2 ORIGINAL EQUIPMENT MANUFACTURERS (OEMS)

- 5.5.3 DISTRIBUTORS

- 5.5.4 END USERS

- 5.6 ECOSYSTEM ANALYSIS

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 KEY TECHNOLOGIES

- 5.7.1.1 Photovoltaic-thermal solar-assisted heat pump systems

- 5.7.1.2 Hybrid heat pumps

- 5.7.1.3 Air-to-air heat pumps

- 5.7.1.4 Air-to-water heat pumps

- 5.7.1.5 Water-source heat pumps

- 5.7.1.6 Ground-source heat pumps

- 5.7.1.7 Solid-state heat pumps

- 5.7.2 COMPLEMENTARY TECHNOLOGIES

- 5.7.2.1 Thermal storage

- 5.7.2.2 Smart controls and automation technologies

- 5.7.3 ADJACENT TECHNOLOGIES

- 5.7.3.1 Heat recovery ventilation (HRV) systems

- 5.7.3.2 IoT devices

- 5.7.1 KEY TECHNOLOGIES

- 5.8 TRADE ANALYSIS

- 5.8.1 EXPORT SCENARIO (HS CODE 841861)

- 5.8.2 IMPORT SCENARIO (HS CODE 841861)

- 5.9 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.10 REGULATORY LANDSCAPE

- 5.10.1 REGULATIONS

- 5.11 PORTER'S FIVE FORCES ANALYSIS

- 5.11.1 THREAT OF NEW ENTRANTS

- 5.11.2 THREAT OF SUBSTITUTES

- 5.11.3 BARGAINING POWER OF SUPPLIERS

- 5.11.4 BARGAINING POWER OF BUYERS

- 5.11.5 THREAT OF NEW ENTRANTS

- 5.11.6 INTENSITY OF COMPETITIVE RIVALRY

- 5.12 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.12.2 BUYING CRITERIA

- 5.13 PATENT ANALYSIS

- 5.14 CASE STUDY ANALYSIS

- 5.14.1 CITY SUITES HOTEL INSTALLED DAIKIN VRV IV+ HEAT PUMP SYSTEM WITH INDIVIDUAL ROOM CONTROLS TO REDUCE ENERGY CONSUMPTION AND ENHANCE GUEST EXPERIENCE

- 5.14.2 CORONADO BREWING REPLACED FOSSIL BOILERS WITH HTHPS THAT REDUCED CO2 EMISSIONS AND ENERGY COSTS

- 5.14.3 HOTEL DEPLOYED A. O. SMITH VOLTEX HYBRID ELECTRIC HEAT PUMP WATER HEATER TO REDUCE ENERGY CONSUMPTION AND COST

- 5.15 INVESTMENT AND FUNDING SCENARIO

- 5.16 IMPACT OF AI/GEN AI ON HEAT PUMP MARKET

- 5.16.1 ADOPTION OF AI/GEN AI FOR HEAT PUMPS

- 5.16.2 IMPACT OF AI/GEN AI ON HEAT PUMP SUPPLY CHAIN, BY REGION

- 5.17 IMPACT OF 2025 US TARIFF ON HEAT PUMP MARKET

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 IMPACT ON COUNTRIES/REGIONS

- 5.17.4.1 US

- 5.17.4.2 Europe

- 5.17.4.3 Asia Pacific

- 5.17.5 IMPACT ON END USER

6 HEAT PUMP MARKET, BY APPLICATION

- 6.1 INTRODUCTION

- 6.2 HEATING

- 6.2.1 WATER HEATING

- 6.2.1.1 Growing adoption of renewable energy sources to boost segmental growth

- 6.2.2 DISTRICT AND SPACE HEATING

- 6.2.2.1 Pressing need to reduce carbon footprint to fuel market growth

- 6.2.1 WATER HEATING

- 6.3 HEATING AND COOLING

- 6.3.1 IMPLEMENTATION OF ADVANCED TECHNOLOGIES AND SUSTAINABLE METHODS TO OFFER LUCRATIVE GROWTH OPPORTUNITIES

7 HEAT PUMP MARKET, BY END USER

- 7.1 INTRODUCTION

- 7.2 RESIDENTIAL

- 7.2.1 GOVERNMENT INCENTIVES TO BOOST ADOPTION OF HEAT PUMPS TO FUEL MARKET GROWTH

- 7.3 COMMERCIAL

- 7.3.1 GROWING NEED TO ADOPT RENEWABLE ENERGY SOURCES FOR HEATING TO BOOST DEMAND

- 7.4 INDUSTRIAL

- 7.4.1 GLOBAL EFFORTS TO ENHANCE SUSTAINABILITY AND LOWER CARBON EMISSIONS TO FOSTER SEGMENTAL GROWTH

8 HEAT PUMP MARKET, BY RATED CAPACITY

- 8.1 INTRODUCTION

- 8.2 UP TO 10 KW

- 8.2.1 RISING PREFERENCE FOR SUSTAINABLE ALTERNATIVES TO CONVENTIONAL HEATING SYSTEMS TO BOOST DEMAND

- 8.3 10-20 KW

- 8.3.1 GROWING APPLICATION IN LARGE MULTI-FAMILY HOMES AND APARTMENT COMPLEXES TO FUEL MARKET GROWTH

- 8.4 20-30 KW

- 8.4.1 INCREASING DEPLOYMENT IN SMALL COMMERCIAL BUILDINGS TO FOSTER SEGMENTAL GROWTH

- 8.5 ABOVE 30 KW

- 8.5.1 GROWING EMPHASIS ON OFFERING OPTIMAL ENERGY UTILIZATION AND COST-EFFECTIVENESS TO DRIVE MARKET

9 HEAT PUMP MARKET, BY REFRIGERANT

- 9.1 INTRODUCTION

- 9.2 R410A

- 9.2.1 EASE OF HEAT DISSIPATION AND ENHANCED HEAT TRANSFER EFFICIENCY TO BOOST DEMAND

- 9.3 R407C

- 9.3.1 INCREASED USE OF ECO-FRIENDLY REFRIGERANTS IN HEAT PUMPS TO FUEL DEMAND

- 9.4 R744

- 9.4.1 RISING DEPLOYMENT IN NEW-GENERATION HEAT PUMP TECHNOLOGIES TO BOOST DEMAND

- 9.5 R290

- 9.5.1 EXPANDING RETROFIT MARKET FOR HEATING AND COOLING SYSTEMS TO DRIVE DEMAND

- 9.6 R717

- 9.6.1 INCORPORATION OF ADVANCED CONTAINMENT TECHNOLOGIES TO OFFER LUCRATIVE GROWTH OPPORTUNITIES

- 9.7 OTHER REFRIGERANTS

10 HEAT PUMP MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 AIR-TO-AIR HEAT PUMPS

- 10.2.1 RISING DEMAND FOR SMART THERMOSTATS FOR REMOTE MONITORING TO DRIVE MARKET

- 10.3 AIR-TO-WATER HEAT PUMPS

- 10.3.1 GROWING DEMAND FOR CLEAN AND GREEN ALTERNATIVES TO TRADITIONAL FOSSIL FUEL-BASED HEATING METHODS TO DRIVE MARKET

- 10.4 WATER-SOURCE HEAT PUMPS

- 10.4.1 EMPHASIS ON ENHANCING SYSTEM DESIGN AND TECHNOLOGY ADVANCEMENTS TO SUPPORT MARKET GROWTH

- 10.5 GROUND-SOURCE (GEOTHERMAL) HEAT PUMPS

- 10.5.1 GOVERNMENT-LED SUBSIDIES FOR BOOSTING DEPLOYMENT OF GEOTHERMAL HEAT PUMPS TO DRIVE MARKET

- 10.6 HYBRID HEAT PUMPS

- 10.6.1 SEAMLESS INTEGRATION WITH EXISTING INFRASTRUCTURE TO BOOST DEMAND

- 10.7 PHOTOVOLTAIC-THERMAL (PVT) HEAT PUMPS

- 10.7.1 REDUCED RELIANCE ON CENTRALIZED ENERGY SOURCES TO FOSTER MARKET GROWTH

11 HEAT PUMP MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.2 REVERSIBLE HEAT PUMPS

- 11.2.1 GLOBAL EMPHASIS ON IMPLEMENTING ENERGY EFFICIENCY REGULATIONS TO DRIVE MARKET

- 11.3 NON-REVERSIBLE HEAT PUMPS

- 11.3.1 RISING DEMAND FOR COST-EFFECTIVE AND SUSTAINABLE TECHNOLOGIES TO OFFER LUCRATIVE GROWTH OPPORTUNITIES

12 HEAT PUMP MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Expanding industrialization and infrastructure development to boost demand

- 12.2.2 INDIA

- 12.2.2.1 Emphasis on constructing green structures to drive market

- 12.2.3 JAPAN

- 12.2.3.1 Integration of IoT and application of AI and ML in manufacturing and designing process to offer lucrative growth opportunities

- 12.2.4 SOUTH KOREA

- 12.2.4.1 Government-led investments in smart energy infrastructure and integrated energy systems to fuel market growth

- 12.2.5 AUSTRALIA

- 12.2.5.1 Initiatives to phase out gas hot water systems to boost demand

- 12.2.6 REST OF ASIA PACIFIC

- 12.2.1 CHINA

- 12.3 EUROPE

- 12.3.1 FRANCE

- 12.3.1.1 Favorable policies and national climate initiatives to support market growth

- 12.3.2 ITALY

- 12.3.2.1 Government-led initiatives to boost adoption of green energy to fuel market growth

- 12.3.3 GERMANY

- 12.3.3.1 Rising gas prices and energy security concerns to support market growth

- 12.3.4 UK

- 12.3.4.1 Emphasis on achieving net-zero emissions by 2050 to foster market growth

- 12.3.5 SPAIN

- 12.3.5.1 Emphasis on renovating existing buildings to drive market

- 12.3.6 REST OF EUROPE

- 12.3.1 FRANCE

- 12.4 NORTH AMERICA

- 12.4.1 US

- 12.4.1.1 Increasing investments in installation of energy-efficient technologies in new infrastructure development projects to drive market

- 12.4.2 CANADA

- 12.4.2.1 Emphasis on offering market-feasible net-zero energy solutions by 2030 and reducing electricity demand to boost demand

- 12.4.1 US

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 GCC

- 12.5.1.1 Saudi Arabia

- 12.5.1.1.1 Increasing investments in industrial sector to boost demand

- 12.5.1.2 UAE

- 12.5.1.2.1 Growing consciousness about sustainable and environmentally friendly practices to boost demand

- 12.5.1.3 Rest of GCC

- 12.5.1.1 Saudi Arabia

- 12.5.2 SOUTH AFRICA

- 12.5.2.1 Expanding transportation industry to foster market growth

- 12.5.3 REST OF MIDDLE EAST & AFRICA

- 12.5.1 GCC

- 12.6 LATIN AMERICA

- 12.6.1 BRAZIL

- 12.6.1.1 Growing use of non-fossil fuel energy sources to boost demand

- 12.6.2 MEXICO

- 12.6.2.1 Growing demand for energy-efficient devices in residential, commercial, and industrial sectors to fuel market growth

- 12.6.3 REST OF LATIN AMERICA

- 12.6.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 STRATEGIES ADOPTED BY KEY PLAYERS, 2020-2025

- 13.3 MARKET SHARE ANALYSIS, 2024

- 13.4 MARKET EVALUATION FRAMEWORK, 2020-2024

- 13.5 REVENUE ANALYSIS, 2020-2024

- 13.6 BRAND/PRODUCT COMPARISON

- 13.7 COMPANY VALUATION AND FINANCIAL METRICS

- 13.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.8.1 STARS

- 13.8.2 EMERGING LEADERS

- 13.8.3 PERVASIVE PLAYERS

- 13.8.4 PARTICIPANTS

- 13.8.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.8.5.1 Company footprint

- 13.8.5.2 Company market footprint

- 13.8.5.3 Region footprint

- 13.8.5.4 Technology footprint

- 13.8.5.5 Type footprint

- 13.8.5.6 Rated capacity footprint

- 13.8.5.7 Refrigerant footprint

- 13.8.5.8 End user footprint

- 13.8.5.9 Application footprint

- 13.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.9.1 PROGRESSIVE COMPANIES

- 13.9.2 RESPONSIVE COMPANIES

- 13.9.3 DYNAMIC COMPANIES

- 13.9.4 STARTING BLOCKS

- 13.9.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.9.5.1 List of key startups/SMEs

- 13.9.5.2 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.10 COMPETITIVE SCENARIOS

- 13.10.1 PRODUCT LAUNCHES

- 13.10.2 DEALS

- 13.10.3 EXPANSIONS

- 13.10.4 OTHER DEVELOPMENTS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 SAMSUNG

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.3.2 Deals

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths/Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses/Competitive threats

- 14.1.2 DENSO CORPORATION

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.2.1 Expansions

- 14.1.2.3 MnM view

- 14.1.2.3.1 Key strengths/Right to win

- 14.1.2.3.2 Strategic choices

- 14.1.2.3.3 Weaknesses/Competitive threats

- 14.1.3 MIDEA

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches

- 14.1.3.3.2 Deals

- 14.1.3.3.3 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths/Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses/Competitive threats

- 14.1.4 PANASONIC HOLDINGS CORPORATION

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches

- 14.1.4.3.2 Deals

- 14.1.4.3.3 Expansions

- 14.1.4.3.4 Other developments

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths/Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses/Competitive threats

- 14.1.5 MITSUBISHI ELECTRIC CORPORATION

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches

- 14.1.5.3.2 Deals

- 14.1.5.3.3 Expansions

- 14.1.5.3.4 Other developments

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths/Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses/Competitive threats

- 14.1.6 LG ELECTRONICS

- 14.1.6.1 Business overview

- 14.1.6.2 Products/ Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches

- 14.1.6.3.2 Deals

- 14.1.6.3.3 Expansions

- 14.1.6.3.4 Other developments

- 14.1.7 LENNOX INTERNATIONAL INC.

- 14.1.7.1 Business overview

- 14.1.7.2 Products/ Solutions/Services offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches

- 14.1.7.3.2 Deals

- 14.1.8 FUJITSU GENERAL

- 14.1.8.1 Business overview

- 14.1.8.2 Products/ Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Deals

- 14.1.9 DAIKIN INDUSTRIES, LTD.

- 14.1.9.1 Business overview

- 14.1.9.2 Products/ Solutions/Services offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Product launches

- 14.1.9.3.2 Expansions

- 14.1.9.3.3 Other developments

- 14.1.10 CARRIER

- 14.1.10.1 Business overview

- 14.1.10.2 Products/ Solutions/Services offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Product launches

- 14.1.10.3.2 Deals

- 14.1.10.3.3 Expansions

- 14.1.10.3.4 Other developments

- 14.1.11 JOHNSON CONTROLS

- 14.1.11.1 Business overview

- 14.1.11.2 Products/ Solutions/Services offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches

- 14.1.11.3.2 Deals

- 14.1.11.3.3 Expansions

- 14.1.11.3.4 Other developments

- 14.1.12 THERMAX LIMITED

- 14.1.12.1 Business overview

- 14.1.12.2 Products/Solutions/Services offered

- 14.1.13 GEA GROUP AKTIENGESELLSCHAFT

- 14.1.13.1 Business overview

- 14.1.13.2 Products/Solutions/Services offered

- 14.1.13.3 Recent developments

- 14.1.13.3.1 Deals

- 14.1.13.3.2 Other developments

- 14.1.14 TRANE TECHNOLOGIES PLC

- 14.1.14.1 Business overview

- 14.1.14.2 Products/Solutions/Services offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 Product launches

- 14.1.14.3.2 Deals

- 14.1.14.3.3 Expansions

- 14.1.14.3.4 Other developments

- 14.1.15 BOSCH THERMOTECHNOLOGY CORP.

- 14.1.15.1 Business overview

- 14.1.15.2 Products/ Solutions/Services offered

- 14.1.15.3 Recent developments

- 14.1.15.3.1 Product launches

- 14.1.15.3.2 Other developments

- 14.1.1 SAMSUNG

- 14.2 OTHER PLAYERS

- 14.2.1 GUANGZHOU SPRSUN NEW ENERGY TECHNOLOGY DEVELOPMENT CO., LTD.

- 14.2.2 GLEN DIMPLEX GROUP

- 14.2.3 NIBE

- 14.2.4 RHEEM MANUFACTURING COMPANY

- 14.2.5 ENERGEN HYBRID SYSTEMS LIMITED

- 14.2.6 EVO ENERGY TECHNOLOGIES

- 14.2.7 NAMMASWADESHI

- 14.2.8 ECOTECH SOLUTIONS

- 14.2.9 DANDELION ENERGY

- 14.2.10 ZEALUX ELECTRIC LIMITED

15 APPENDIX

- 15.1 INSIGHTS FROM INDUSTRY EXPERTS

- 15.2 DISCUSSION GUIDE

- 15.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.4 CUSTOMIZATION OPTIONS

- 15.5 RELATED REPORTS

- 15.6 AUTHOR DETAILS