|

시장보고서

상품코드

1790687

유세포 분석 시장 : 제공 제품별, 기술별, 용도별, 최종 사용자별, 지역별 예측(-2033년)Flow Cytometry Market by Technology (Cell-based, Bead-Based), Product & Service (Analyzer, Sorter, Consumables (Antibodies, Assays, Kits), Software), Application (Research (Stem Cell), Clinical (Cancer)), End User (Hospital) - Global Forecast to 2033 |

||||||

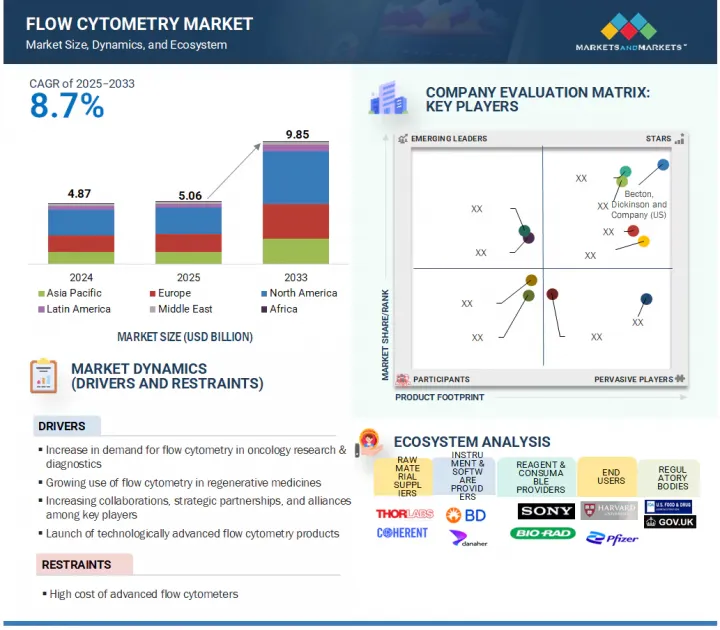

세계의 유세포 분석 시장 규모는 2025년 50억 6,000만 달러에서 2033년까지 98억 5,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 8.7%가 될 것으로 보입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2024-2033년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2033년 |

| 검토 단위 | 금액(10억 달러) |

| 부문 | 제공 제품별, 기술별, 용도별, 최종 사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

형광단 접합 및 특이성 향상과 같은 시약 기술의 발전은 시장을 주도하는 주요 요인 중 하나입니다. 이 분야는 세포 분석에 필수적인 항체, 염료 및 기타 소모품에 대한 지속적인 수요로 인해 시장을 주도하고 있습니다. 연구개발, 임상진단, 의약품 개발에 있어서 유세포 분석의 사용이 확대됨에 따라 고품질 시약에 대한 수요는 꾸준히 증가하고 있습니다.

유세포 분석 시장은 기술에 따라 세포 기반 유세포 분석과 비드 기반 유세포 분석으로 구분됩니다. 2024년에는 세포 기반 유세포 분석 부문이 시장을 주도했습니다. 2024년에는 세포 기반 유세포 분석 부문이 시장을 주도했습니다. 기술 부문에서 세포 기반 유세포 분석의 우위는 다음과 같은 이유 때문입니다.

다양한 세포 유형과 바이오마커 분석에 있어 다재다능함을 자랑합니다. 세포 기반 유세포 분석은 정량적 데이터와 정성적 데이터를 모두 제공하여 생의학 연구, 임상 진단 및 신약 개발 분야에서 수요를 증가시켜 시장 중요성을 높이고 있습니다.

응용 분야별로 유세포 분석 시장은 연구, 임상 및 산업으로 구분됩니다. 연구 용도가 이 부문을 지배하고, 임상 용도는 예측 기간 동안 CAGR로 크게 성장할 것으로 예측됩니다. 면역학, 종양학, 미생물학과 같은 다양한 분야에서의 기초 연구 및 트랜스레이셔널 연구에서 유세포 분석의 광범위한 이용이 이 부문의 성장을 이끌어내는 것으로 예측됩니다.

지역별로 살펴보면 유세포 분석 시장은 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카로 구분됩니다. 2024년 북미는 유세포 분석 시장의 주요 점유율을 차지했습니다. 아시아태평양은 의료 인프라 투자 증가, 생명 과학 연구 개발 활동 활성화, 맞춤형 의료에 대한 의식 증가 등 다양한 요인이 이 성장을 뒷받침하고 있기 때문에 예측 기간 동안 높은 CAGR로 성장할 가능성이 높습니다. 또한, 중국, 일본, 인도, 한국과 같은 국가에서는 연구, 임상 진단, 신약 개발 분야에서 유세포 분석 기술이 활발하게 도입되고 있습니다.

이 보고서는 세계 유세포 분석 시장을 조사했으며, 제공 제품별, 기술별, 용도별, 최종 사용자별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 소개

- 시장 역학

- 고객사업에 영향을 주는 동향/혼란

- 가격 분석

- 밸류체인 분석

- 생태계 분석

- 규제 분석

- Porter's Five Forces 분석

- 주요 이해관계자와 구매 기준

- 기술 분석

- 특허 분석

- 무역 데이터 분석

- 투자 및 자금조달 시나리오

- 2025-2026년의 주된 회의와 이벤트

- 2025년 미국 관세의 영향 : 유세포 분석시장

- AI/생성형 AI가 유세포 분석 시장에 미치는 영향

제6장 유세포 분석 시장(제공 제품별)

- 소개

- 시약 및 소모품

- 기기

- 서비스

- 소프트웨어

- 액세서리

제7장 유세포 분석 시장(기술별)

- 소개

- 셀 기반 유세포 분석

- 비드 기반 유세포 분석

제8장 유세포 분석 시장(용도별)

- 소개

- 연구

- 임상

- 산업

제9장 유세포 분석 시장(최종 사용자별)

- 소개

- 학술연구기관

- 병원 및 임상 검사 기관

- 제약 및 바이오테크놀러지 기업

제10장 유세포 분석 시장(지역별)

- 소개

- 북미

- 거시경제 전망

- 미국

- 캐나다

- 유럽

- 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 거시경제 전망

- 중국

- 일본

- 인도

- 호주

- 한국

- 싱가포르

- 인도네시아

- 기타

- 라틴아메리카

- 거시경제 전망

- 브라질

- 멕시코

- 기타

- 중동

- 거시경제 전망

- GCC 국가

- 기타 중

- 아프리카

- 감염증과 비감염성 질환의 부담 증가가 시장 성장을 가속

- 거시경제 전망

제11장 경쟁 구도

- 개요

- 주요 진입기업의 전략/강점

- 수익 분석

- 시장 점유율 분석

- 기업평가 매트릭스 : 주요 진입기업, 2024년

- 기업평가 매트릭스 : 스타트업/중소기업, 2024년

- 평가 및 재무지표

- 브랜드/제품 비교

- 경쟁 시나리오

제12장 기업 프로파일

- 주요 진출기업

- BECTON, DICKINSON AND COMPANY

- DANAHER CORPORATION

- THERMO FISHER SCIENTIFIC INC.

- AGILENT TECHNOLOGIES, INC.

- SONY CORPORATION

- BIO-RAD LABORATORIES, INC.

- MILTENYI BIOTEC

- ENZO BIOCHEM INC.

- SYSMEX CORPORATION

- CYTEK BIOSCIENCES

- BIOMERIEUX

- CYTONOME/ST, LLC

- SARTORIUS AG

- UNION BIOMETRICA, INC.

- TAKARA BIO INC.

- 기타 기업

- APOGEE FLOW SYSTEMS LTD.

- STRATEDIGM, INC.

- NANOCELLECT BIOMEDICAL

- BIOLEGEND, INC.

- ON-CHIP BIOTECHNOLOGIES CO., LTD.

- NEXCELOM BIOSCIENCE LLC

- BENNUBIO INC.

- ORFLO TECHNOLOGIES

- BAY BIOSCIENCE LLC

- CYTOBUOY

제13장 부록

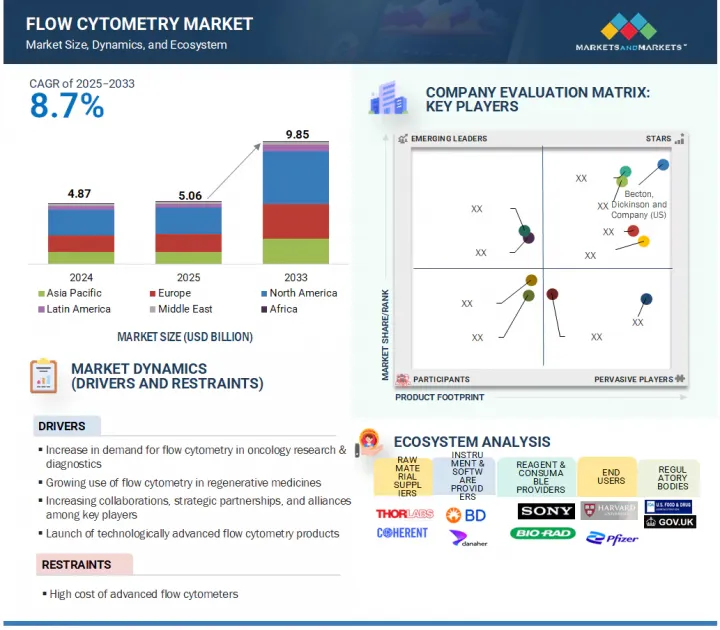

JHS 25.08.20The global flow cytometry market is estimated to reach USD 9.85 billion by 2033 from USD 5.06 billion in 2025, at a CAGR of 8.7% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2033 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Units Considered | Value (USD billion) |

| Segments | Technology, Offering, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

Advancements in reagent technologies, such as fluorophore conjugation and specificity enhancement, are one of the major factors driving the market. This segment dominates due to continuous demand for antibodies, dyes, and other consumables essential for cell analysis. As the use of flow cytometry expands in research, clinical diagnostics, and drug development, the need for high-quality reagents remains constant.

"The cell-based flow cytometry market is likely to grow at a faster pace."

Based on technology, the flow cytometry market is segmented into cell-based and bead-based flow cytometry. The cell-based flow cytometry segment dominated the market in 2024. The

dominance of cell-based flow cytometry in the technology segment is attributed to its

versatility in analyzing various cell types and biomarkers. Cell-based flow cytometry provides both quantitative and qualitative data that has increased its demand in biomedical research, clinical diagnostics, and drug discovery, thus driving its market significance.

"The research application dominated the applications market segment."

Based on application, the flow cytometry market is segmented into research applications, clinical applications, and industrial applications. The research application dominated the segment; however, clinical application is anticipated to grow at a significant CAGR during the forecast period. The extensive use of flow cytometry in basic and translational research across diverse fields such as immunology, oncology, and microbiology is likely to drive the segmental growth.

"The market in Asia Pacific is estimated to witness the fastest growth rate."

Based on region, the flow cytometry market is segmented into North America, Europe, Asia Pacific, Latin America, Middle East, and Africa. In 2024, North America accounted for a major share of the flow cytometry market. The Asia Pacific region is likely to grow at a significant CAGR during the forecast period, owing to various factors such as increasing investment in healthcare infrastructure, rising R&D activities in life sciences, and growing awareness about personalized medicine, which are driving this growth. Moreover, countries like China, Japan, India, and South Korea are witnessing substantial adoption of flow cytometry technologies in research, clinical diagnostics, and drug discovery.

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Tier 1 - 25%, Tier 2 - 35%, and Tier 3 - 40%

- By Designation: C-level Executives - 30%, Directors - 45%, and Others - 25%

- By Region: North America - 35%, Europe - 25%, Asia Pacific - 15%, Latin America - 10%, Middle East - 10%, and Africa - 5%

List of Companies Profiled in the Report:

- Becton, Dickinson and Company (US)

- Danaher Corporation (US)

- Thermo Fisher Scientific Inc. (US)

- Agilent Technologies, Inc. (US)

- Sony Corporation (Japan)

- Bio-Rad Laboratories, Inc. (US)

- Miltenyi Biotec (Germany)

- Enzo Biochem, Inc. (US)

- Sysmex Corporation (Japan)

- bioMerieux (France)

- Cytonome/ST, LLC (US)

- Sartorius AG (Germany)

- Cytek Biosciences (US)

- Union Biometrica, Inc. (US)

- Takara Bio Inc. (Japan)

Research Coverage:

This research report categorizes flow cytometry market by Offering (Reagents and Consumables, Instruments, Services, Software, and Accessories), Technology (Cell-Based Flow Cytometry and Bead-Based Flow Cytometry), Application (Research Applications, Clinical Applications, and Industrial Applications), End User (Pharmaceutical & Biotechnology Companies, Hospitals & Clinical Testing Laboratories, And Academic & Research Institutes), and Region (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa).

The report's scope covers detailed information regarding the primary factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the flow cytometry market. A thorough analysis of the key industry players has been conducted to provide insights into their business overview, solutions, and services; key strategies; new product & service launches, acquisitions, and recent developments associated with the flow cytometry market. This report covers the competitive analysis of upcoming startups in the flow cytometry market ecosystem.

Key Benefits of Buying the Report:

The report will help market leaders/new entrants by providing them with the estimations of the revenue numbers for the overall market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to better position their business and make suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide them with information on the key market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers (Increasing prevalence of chronic diseases, growing use of flow cytometry in regenerative medicines, increasing collaborations, strategic partnerships, and alliances among key players, launch of technologically advanced flow cytometry products), restraints (High cost of advanced flow cytometers ), opportunities (Increased use in clinical applications and infectious disease diagnostics), and challenges (Complexities related to reagent development) influencing the growth of the market.

- Product Development/Innovation: Detailed insights on newly launched products and technological assessment of the flow cytometry market

- Market Development: Comprehensive information about lucrative markets and analysis of the market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the flow cytometry market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players, including Becton, Dickinson and Company (US), Danaher Corporation (US), Thermo Fisher Scientific, Inc. (US), Agilent Technologies, among others, offering products and services for flow cytometry market. Other companies include Apogee Flow Systems Ltd. (UK), Stratedigm, Inc. (US), NanoCellect Biomedical, Inc. (US), and On-chip Biotechnologies, Co., Ltd. (Japan), among others, for the flow cytometry market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 SEGMENTS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.3.3 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakdown of primaries

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 GLOBAL MARKET SIZE ESTIMATION

- 2.2.2 SEGMENTAL MARKET ASSESSMENT

- 2.3 MARKET GROWTH RATE PROJECTION

- 2.3.1 IMPACT ANALYSIS OF SUPPLY- AND DEMAND-SIDE FACTORS

- 2.4 DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FLOW CYTOMETRY MARKET

- 4.2 NORTH AMERICA: FLOW CYTOMETRY MARKET, BY TECHNOLOGY

- 4.3 FLOW CYTOMETRY MARKET SHARE, BY END USER, 2024

- 4.4 FLOW CYTOMETRY MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increase in demand for flow cytometry in oncology research & diagnostics

- 5.2.1.2 Growing use of flow cytometry in regenerative medicines

- 5.2.1.3 Increasing collaborations, strategic partnerships, and alliances among key players

- 5.2.1.4 Launch of technologically advanced flow cytometry products

- 5.2.2 RESTRAINTS

- 5.2.2.1 High cost of advanced flow cytometers (analyzers & cell sorters)

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increased use in clinical applications and infectious disease diagnostics

- 5.2.4 CHALLENGES

- 5.2.4.1 Complexities related to reagent development

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND OF FLOW CYTOMETRY PRODUCTS, BY KEY PLAYER, 2022-2024

- 5.4.2 AVERAGE SELLING PRICE TREND OF FLOW CYTOMETRY PRODUCTS, BY REGION, 2022-2024

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 ECOSYSTEM ANALYSIS

- 5.6.1 INSTRUMENT & SOFTWARE PROVIDERS

- 5.6.2 REAGENT & CONSUMABLE PROVIDERS

- 5.6.3 END USERS

- 5.6.4 REGULATORY BODIES

- 5.7 REGULATORY ANALYSIS

- 5.7.1 REGULATORY LANDSCAPE

- 5.7.1.1 Stringent FDA requirements

- 5.7.1.2 Analyte-specific reagent rules

- 5.7.1.3 Limitations in validation protocols for cell-based assays

- 5.7.1.4 Absence of test guidelines for cell-based fluorescence assays

- 5.7.1.5 IVD CE mark approvals

- 5.7.2 LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.7.2.1 North America: List of regulatory bodies, government agencies, and other organizations

- 5.7.2.2 Europe: List of regulatory bodies, government agencies, and other organizations

- 5.7.2.3 Asia Pacific: List of regulatory bodies, government agencies, and other organizations

- 5.7.2.4 Latin America: List of regulatory bodies, government agencies, and other organizations

- 5.7.2.5 Middle East & Africa: List of regulatory bodies, government agencies, and other organizations

- 5.7.1 REGULATORY LANDSCAPE

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- 5.8.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.8.2 BARGAINING POWER OF SUPPLIERS

- 5.8.3 BARGAINING POWER OF BUYERS

- 5.8.4 THREAT OF SUBSTITUTES

- 5.8.5 THREAT OF NEW ENTRANTS

- 5.9 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.9.2 KEY BUYING CRITERIA

- 5.10 TECHNOLOGY ANALYSIS

- 5.10.1 KEY TECHNOLOGIES

- 5.10.1.1 Spectral flow cytometry

- 5.10.1.2 Mass cytometry

- 5.10.1.3 Imaging flow cytometry

- 5.10.2 ADJACENT TECHNOLOGIES

- 5.10.2.1 Single-cell RNA sequencing

- 5.10.2.2 Microfluidics

- 5.10.2.3 High-content screening

- 5.10.3 COMPLEMENTARY TECHNOLOGIES

- 5.10.3.1 Single-cell analysis

- 5.10.3.2 Spatial analysis

- 5.10.1 KEY TECHNOLOGIES

- 5.11 PATENT ANALYSIS

- 5.11.1 METHODOLOGY

- 5.11.2 PATENTS FILED, BY DOCUMENT TYPE, 2014-2024

- 5.12 TRADE DATA ANALYSIS

- 5.12.1 IMPORT DATA

- 5.12.2 EXPORT DATA

- 5.13 INVESTMENT AND FUNDING SCENARIO

- 5.14 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.15 IMPACT OF 2025 US TARIFF: FLOW CYTOMETRY MARKET

- 5.15.1 KEY TARIFF RATES

- 5.15.2 PRICE IMPACT ANALYSIS

- 5.15.3 KEY IMPACTS ON VARIOUS REGIONS

- 5.15.3.1 US

- 5.15.3.2 Europe

- 5.15.3.3 Asia Pacific

- 5.15.4 END-USE INDUSTRY IMPACT

- 5.15.4.1 Pharmaceutical and biotech companies

- 5.15.4.2 Hospitals & clinical laboratories

- 5.15.4.3 Academic & research institutes

- 5.16 IMPACT OF AI/GEN AI ON FLOW CYTOMETRY MARKET

- 5.16.1 MARKET POTENTIAL OF AI IN FLOW CYTOMETRY

- 5.16.2 AI USE CASES

- 5.16.3 KEY COMPANIES IMPLEMENTING AI/GEN AI

- 5.16.4 FUTURE OF AI/GEN AI IN FLOW CYTOMETRY MARKET

6 FLOW CYTOMETRY MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.2 REAGENTS & CONSUMABLES

- 6.2.1 ANTIBODIES

- 6.2.1.1 Increasing demand for high-specificity antibodies to propel market growth

- 6.2.2 ASSAYS & KITS

- 6.2.2.1 Need for high-precision diagnosis and advancements in personalized medicines to aid market growth

- 6.2.3 OTHER REAGENTS & CONSUMABLES

- 6.2.1 ANTIBODIES

- 6.3 INSTRUMENTS

- 6.3.1 CELL ANALYZERS

- 6.3.1.1 High-range cell analyzers

- 6.3.1.1.1 Better sensitivity, accuracy, and flexibility in designing multicolor experiments to augment segment growth

- 6.3.1.2 Mid-range cell analyzers

- 6.3.1.2.1 Availability of compact and high-performance analyzers to support market growth

- 6.3.1.3 Low-range cell analyzers

- 6.3.1.3.1 Cost-effectiveness and increased commercialization by manufacturers to drive segment

- 6.3.1.1 High-range cell analyzers

- 6.3.2 CELL SORTERS

- 6.3.2.1 High-range cell sorters

- 6.3.2.1.1 High cost and budget constraints among end users to limit market growth

- 6.3.2.2 Mid-range cell sorters

- 6.3.2.2.1 Cost-effectiveness and high availability to spur market growth

- 6.3.2.3 Low-range cell sorters

- 6.3.2.3.1 Increasing commercialization in small-scale laboratories and research facilities to fuel market growth

- 6.3.2.1 High-range cell sorters

- 6.3.1 CELL ANALYZERS

- 6.4 SERVICES

- 6.4.1 RISING FOCUS ON WORKFLOW CONTINUITY AND PERFORMANCE MAXIMIZATION TO BOOST MARKET GROWTH

- 6.5 SOFTWARE

- 6.5.1 INCREASING AVAILABILITY OF DATA ANALYSIS SOFTWARE TO AID MARKET GROWTH

- 6.6 ACCESSORIES

- 6.6.1 HIGH AVAILABILITY OF ADVANCED AND CUSTOMIZED ACCESSORIES TO SUPPORT MARKET GROWTH

7 FLOW CYTOMETRY MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- 7.2 CELL-BASED FLOW CYTOMETRY

- 7.2.1 INCREASED FOCUS ON R&D AND TECHNOLOGICAL ADVANCEMENTS TO PROPEL MARKET GROWTH

- 7.3 BEAD-BASED FLOW CYTOMETRY

- 7.3.1 HIGHER RELIABILITY AND BETTER MEASUREMENT CONSISTENCIES TO SUPPORT MARKET GROWTH

8 FLOW CYTOMETRY MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 RESEARCH APPLICATIONS

- 8.2.1 DRUG DISCOVERY AND DEVELOPMENT

- 8.2.1.1 Drug discovery

- 8.2.1.1.1 Growing use of phenotypic cell-based assays to support market growth

- 8.2.1.2 Stem cell research

- 8.2.1.2.1 Increasing R&D and rising investments for advanced stem cell development to drive segment

- 8.2.1.3 In vitro toxicity testing

- 8.2.1.3.1 Focus on continuous drug development by pharmaceutical & biotechnology companies to aid segment growth

- 8.2.1.1 Drug discovery

- 8.2.2 IMMUNOLOGY

- 8.2.2.1 Growing prevalence of chronic autoimmune diseases to drive market

- 8.2.3 CELL SORTING

- 8.2.3.1 Increasing focus on cell-based research activities to fuel market growth

- 8.2.4 APOPTOSIS

- 8.2.4.1 Increased use in research activities to drive segment

- 8.2.5 CELL CYCLE ANALYSIS

- 8.2.5.1 High accuracy of cytometry products in cell analysis to propel segment growth

- 8.2.6 CELL VIABILITY

- 8.2.6.1 Growing use of cell viability assays in research to support market growth

- 8.2.7 CELL COUNTING

- 8.2.7.1 Rising need for multi-parametric cellular assessments to spur market growth

- 8.2.8 OTHER RESEARCH APPLICATIONS

- 8.2.1 DRUG DISCOVERY AND DEVELOPMENT

- 8.3 CLINICAL APPLICATIONS

- 8.3.1 CANCER DIAGNOSTICS

- 8.3.1.1 Increasing prevalence of cancer to drive segment

- 8.3.2 HEMATOLOGY

- 8.3.2.1 Multi-parametric approach and high-speed cell analyzing capabilities to augment segment growth

- 8.3.3 AUTOIMMUNE DISEASES

- 8.3.3.1 Growing focus on developing treatments for autoimmune diseases to drive segment

- 8.3.4 ORGAN TRANSPLANTATION

- 8.3.4.1 Rising number of organ transplants to propel market growth

- 8.3.5 OTHER CLINICAL APPLICATIONS

- 8.3.1 CANCER DIAGNOSTICS

- 8.4 INDUSTRIAL APPLICATIONS

- 8.4.1 INCREASING USE IN FOOD, DAIRY, ENERGY, AND MICROBIAL INDUSTRIES TO SUPPORT MARKET GROWTH

9 FLOW CYTOMETRY MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.2 ACADEMIC & RESEARCH INSTITUTES

- 9.2.1 RISING PUBLIC-PRIVATE FUNDING AND INCREASING CANCER RESEARCH PROJECTS TO DRIVE MARKET

- 9.3 HOSPITALS & CLINICAL TESTING LABORATORIES

- 9.3.1 GROWING DEMAND FOR EFFECTIVE DISEASE DIAGNOSIS AND TREATMENT TO SPUR MARKET GROWTH

- 9.4 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 9.4.1 INCREASING FOCUS ON PERSONALIZED MEDICINE AND TARGETED THERAPIES TO FUEL MARKET GROWTH

10 FLOW CYTOMETRY MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK

- 10.2.2 US

- 10.2.2.1 US to dominate North American flow cytometry market during study period

- 10.2.3 CANADA

- 10.2.3.1 Ongoing government initiatives for life science research and high incidence of cancer to propel market growth

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK

- 10.3.2 GERMANY

- 10.3.2.1 Increasing public and private funding for advanced cell-based research activities to aid market growth

- 10.3.3 UK

- 10.3.3.1 Growing acceptance of flow cytometry-based diagnostic techniques by healthcare professionals to spur market growth

- 10.3.4 FRANCE

- 10.3.4.1 Increasing government funding for proteomics and genomics research to fuel market growth

- 10.3.5 ITALY

- 10.3.5.1 Large geriatric population and presence of well-developed healthcare system to boost market growth

- 10.3.6 SPAIN

- 10.3.6.1 High incidence of cancer and focus on translational and personalized medicines to augment market growth

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK

- 10.4.2 CHINA

- 10.4.2.1 High incidence of cancer and favorable government policies to support market growth

- 10.4.3 JAPAN

- 10.4.3.1 Technological advancements and high prevalence of chronic diseases to drive market

- 10.4.4 INDIA

- 10.4.4.1 Rising government funding for proteomics research to drive market

- 10.4.5 AUSTRALIA

- 10.4.5.1 Increasing government research funding and growing prevalence of cancer to propel market growth

- 10.4.6 SOUTH KOREA

- 10.4.6.1 Rising number of conferences and growing focus on medical research to spur market growth

- 10.4.7 SINGAPORE

- 10.4.7.1 Increasing availability of data analysis software and growing focus on medical tourism to drive market

- 10.4.8 INDONESIA

- 10.4.8.1 Rising prevalence of HIV and cancer to drive market

- 10.4.9 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 MACROECONOMIC OUTLOOK

- 10.5.2 BRAZIL

- 10.5.2.1 Presence of key market players and increased emphasis on cancer research to boost market growth

- 10.5.3 MEXICO

- 10.5.3.1 Favorable trade agreements and growth of pharmaceutical industry to fuel market growth

- 10.5.4 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST

- 10.6.1 MACROECONOMIC OUTLOOK

- 10.6.2 GCC COUNTRIES

- 10.6.2.1 Saudi Arabia

- 10.6.2.1.1 Growing prevalence of chronic diseases and increasing R&D investments to boost market growth

- 10.6.2.2 UAE

- 10.6.2.2.1 Increased R&D investment and favorable government healthcare policies to drive market

- 10.6.2.3 Rest of GCC countries

- 10.6.2.1 Saudi Arabia

- 10.6.3 REST OF MIDDLE EAST

- 10.7 AFRICA

- 10.7.1 INCREASING BURDEN OF INFECTIOUS AND NON-COMMUNICABLE DISEASES TO PROPEL MARKET GROWTH

- 10.7.2 MACROECONOMIC OUTLOOK

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 11.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN FLOW CYTOMETRY MARKET

- 11.3 REVENUE ANALYSIS

- 11.4 MARKET SHARE ANALYSIS

- 11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- 11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.5.5.1 Company footprint

- 11.5.5.2 Product & service footprint

- 11.5.5.3 Region footprint

- 11.5.5.4 Application footprint

- 11.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- 11.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.7 VALUATION & FINANCIAL METRICS

- 11.7.1 VALUATION OF KEY PLAYERS

- 11.7.2 FINANCIAL METRICS OF KEY PLAYERS

- 11.8 BRAND/PRODUCT COMPARISON

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES & APPROVALS

- 11.9.2 DEALS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 BECTON, DICKINSON AND COMPANY

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Services offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches

- 12.1.1.3.2 Deals

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses & competitive threats

- 12.1.2 DANAHER CORPORATION

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Services offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches

- 12.1.2.3.2 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses & competitive threats

- 12.1.3 THERMO FISHER SCIENTIFIC INC.

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Services offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches

- 12.1.3.3.2 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses & competitive threats

- 12.1.4 AGILENT TECHNOLOGIES, INC.

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Services offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches

- 12.1.5 SONY CORPORATION

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Services offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches

- 12.1.5.3.2 Deals

- 12.1.6 BIO-RAD LABORATORIES, INC.

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Services/Solutions offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches

- 12.1.7 MILTENYI BIOTEC

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Services offered

- 12.1.8 ENZO BIOCHEM INC.

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Services offered

- 12.1.9 SYSMEX CORPORATION

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Services offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Product launches

- 12.1.10 CYTEK BIOSCIENCES

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Services offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Product launches

- 12.1.10.3.2 Deals

- 12.1.11 BIOMERIEUX

- 12.1.11.1 Business overview

- 12.1.11.2 Products/Services offered

- 12.1.12 CYTONOME/ST, LLC

- 12.1.12.1 Business overview

- 12.1.12.2 Products/Services offered

- 12.1.13 SARTORIUS AG

- 12.1.13.1 Business overview

- 12.1.13.2 Products/Services offered

- 12.1.14 UNION BIOMETRICA, INC.

- 12.1.14.1 Business overview

- 12.1.14.2 Products/Services offered

- 12.1.15 TAKARA BIO INC.

- 12.1.15.1 Business overview

- 12.1.15.2 Products/Services offered

- 12.1.1 BECTON, DICKINSON AND COMPANY

- 12.2 OTHER PLAYERS

- 12.2.1 APOGEE FLOW SYSTEMS LTD.

- 12.2.2 STRATEDIGM, INC.

- 12.2.3 NANOCELLECT BIOMEDICAL

- 12.2.4 BIOLEGEND, INC.

- 12.2.5 ON-CHIP BIOTECHNOLOGIES CO., LTD.

- 12.2.6 NEXCELOM BIOSCIENCE LLC

- 12.2.7 BENNUBIO INC.

- 12.2.8 ORFLO TECHNOLOGIES

- 12.2.9 BAY BIOSCIENCE LLC

- 12.2.10 CYTOBUOY

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS