|

시장보고서

상품코드

1795411

슈퍼커패시터 시장 : 유형별, 정전 용량 범위별, 최종 용도별, 지역별 예측(-2030년)Supercapacitor Market by Type, Capacitance Range, Electrode Material - Global Forecast to 2030 |

||||||

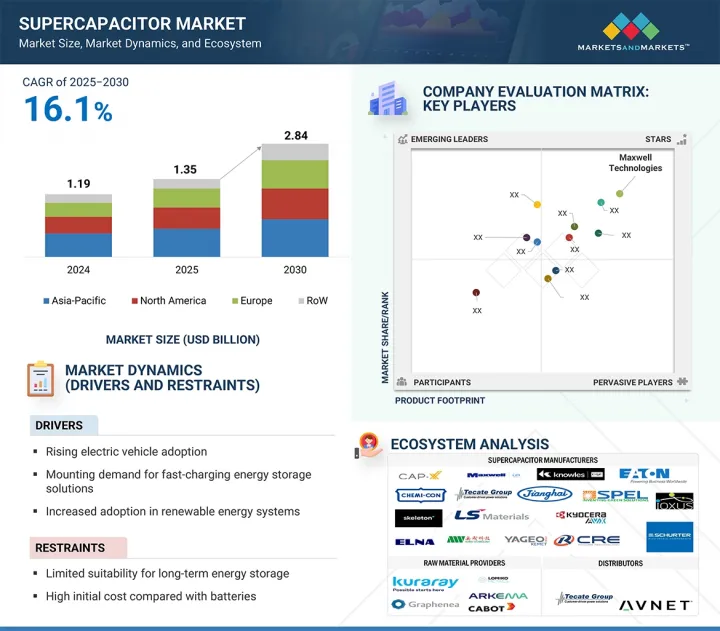

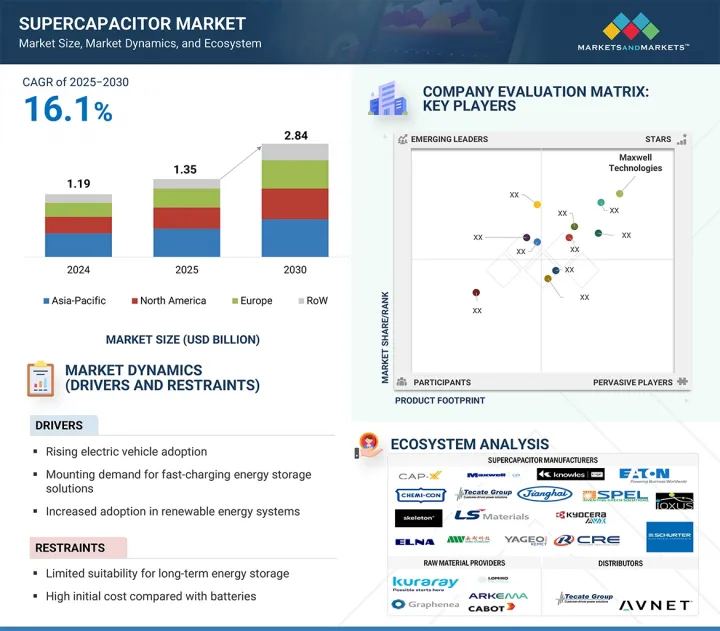

세계의 슈퍼커패시터 시장 규모는 16.1%의 연평균 복합 성장률(CAGR)로 확대되어 2025년 13억 5,000만 달러에서 2030년에는 28억 4,000만 달러로 성장할 것으로 예측되고 있습니다.

자동차 부문이 주요 견인 역할을 계속하고 있으며, 슈퍼커패시터는 급속한 충방전 사이클과 피크 전력 수요를 지원하기 때문에 전기자동차(EV), 하이브리드 시스템, 스타트-스톱 용도에서의 채용이 증가하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(10억 달러) |

| 부문별 | 유형별, 정전용량 범위별, 최종 용도별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양 및 기타 지역 |

모빌리티뿐만 아니라 고전력 밀도, 사이클 수명 연장, 고속 응답이 요구되는 가전, 산업 자동화, 에너지 분야에서도 수요가 높아지고 있습니다. 슈퍼커패시터는 백업 전원 시스템, 전압 안정화, 그리드측 에너지 저장, 특히 재생에너지 통합에 도입되었습니다. 휴대기기 및 IoT 인프라는 급속 충전, 긴 수명, 안정적인 성능을 제공합니다. 전극 재료, 특히 탄소 기반 및 하이브리드 설계의 기술적 진보는 에너지 밀도를 향상시키고 보다 광범위한 응용 분야에서 그 유용성을 확대하고 있습니다. 산업계가 점점 더 가전화, 효율성, 탄력성을 우선시함에 따라 고성능 슈퍼커패시터 솔루션 수요는 다양한 최종 용도 부문에서 크게 성장할 것입니다.

1,000F 초과 부문은 높은 에너지 버퍼링, 급속한 충방전 사이클, 긴 수명을 요구하는 용도에서의 역할 확대로 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 이러한 고용량 슈퍼커패시터는 그리드 에너지 저장, 철도 운송, 산업 자동화, 백업 파워 시스템 등 종래의 배터리에서는 서지 파워나 수명의 요건을 충족할 수 없는 분야에서 채용이 증가하고 있습니다. 가혹한 사용 조건 하에서도 안정된 성능을 발휘하여 유지 보수의 필요성을 줄일 수 있기 때문에 미션 크리티컬하고 고부하 환경에 최적입니다. 또한 하이브리드 에너지 시스템, 특히 마이크로그리드 및 회생 브레이크 솔루션에 1,000F 이상의 배터리를 통합하는 노력이 진행되고 있으며, 그 채용이 더욱 가속화되고 있습니다. 이 성장은 소형 폼 팩터로 고전압 및 에너지 처리량을 처리하도록 설계된 대형 슈퍼커패시터 모듈에 대한 투자로도 지원됩니다. 산업계가 효율, 가동 시간, 전력 신뢰성을 우선시하는 동안, 이 분야는 가장 강력한 성장 궤도를 나타낼 것으로 보입니다.

자동차 및 운송 분야는 전기자동차와 하이브리드 차량의 효율적인 에너지 저장과 신속한 전력 공급에 대한 수요가 높아지면서 예측 기간 동안 슈퍼커패시터 시장을 선도할 것으로 예측되고 있습니다. 슈퍼커패시터는 회생 브레이크, 스타트-스톱 시스템, 전력 안정화 등의 기능을 위해 차량 시스템에의 통합이 진행되고 있어, 라이프 사이클이 길고, 전력 밀도가 높고, 저온 성능이 우수하다는 점에서 종래의 배터리를 웃도는 이점을 제공합니다. 상용 플릿, 철도, 전기 버스에서 슈퍼커패시터는 신속한 에너지 회수와 짧은 충전 사이클을 가능하게 하고, 배출량 감축과 연비 향상을 목표로 하는 세계의 노력에 부합하고 있습니다. 전기화로의 전환, 지지적인 정부 규정, 지속가능한 이동성 인프라 투자는 슈퍼커패시터 기술에 큰 성장 기회를 창출하고 있습니다. OEM이 가볍고 고효율 에너지 시스템을 선호하기 때문에 이 분야는 시장을 선도할 것으로 예측됩니다.

아시아태평양은 산업 활동 가속화, 에너지 효율 기술에 대한 수요 증가, 전기자동차(EV) 도입 증가에 힘입어 예측 기간 동안 슈퍼커패시터 시장에서 최고의 CAGR을 나타낼 것으로 예측됩니다. 중국, 일본, 한국, 인도 등의 국가들은 운송, 가전, 재생에너지 등 주요 섹터에서 슈퍼커패시터를 전개하는 최전선에 있습니다. 중국은 EV 생산과 배터리 제조의 세계 리더로, 이 지역 수요에 크게 기여하고 있습니다. 동시에 일본과 한국은 고성능 에너지 저장 기술에 대한 투자를 계속하고 있습니다. 한편, 동남아시아에서는 대중교통기기의 전기화와 송전망의 근대화가 진행되고 있어, 이 지역의 전망을 한층 더 높이고 있습니다. 숙련된 제조 거점이 있어 휴대용 전자기기와 자동차 기술의 국내 소비가 확대되고 있기 때문에 아시아태평양은 향후 수년간 슈퍼커패시터 시장 확대의 주요 촉진요인으로 자리매김하고 있습니다.

본 보고서에서는 세계의 슈퍼커패시터 시장에 대해 조사했으며, 유형별, 정전용량 범위별, 최종 용도별, 지역별 동향, 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 소개

- 시장 역학

- 밸류체인 분석

- 가격 분석

- 생태계 분석

- 기술 분석

- 사례 연구 분석

- 무역 분석

- 특허 분석

- AI가 슈퍼커패시터 시장에 미치는 영향

- 2025년 미국 관세가 슈퍼커패시터 시장에 미치는 영향

제6장 슈퍼커패시터용 전극 재료

- 소개

- 탄소

- 복합재료

- 기타 전극 재료

제7장 슈퍼커패시터 시장(유형별)

- 소개

- 전기 이중층 커패시터

- 하이브리드 커패시터

- 슈도 커패시터(정성)

제8장 슈퍼커패시터 시장(정전 용량 범위별)

- 소개

- 100F 미만

- 100-1,000F

- 1,000F 초과

제9장 슈퍼커패시터 시장(최종 용도별)

- 소개

- 자동차 및 운송

- 에너지 및 전력

- 가전

- 공업

- 기타

제10장 슈퍼커패시터 시장(지역별)

- 소개

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 기타

- 기타 지역

- 남미

- 중동

- 아프리카

제11장 경쟁 구도

- 개요

- 주요 참가 기업의 전략/강점, 2021-2025년

- 시장 점유율 분석, 2024년

- 수익 분석, 2020-2024년

- 기업평가 매트릭스 : 주요 진입기업, 2024년

- 기업평가 매트릭스 : 스타트업/중소기업, 2024년

- 경쟁 시나리오

제12장 기업 프로파일

- 주요 진출기업

- MAXWELL TECHNOLOGIES

- LS MATERIALS

- NIPPON CHEMI-CON CORPORATION

- EATON

- CAP-XX

- TECATE GROUP

- CORNELL DUBILIER

- IOXUS

- SKELETON TECHNOLOGIES

- KORCHIP CORPORATION

- NANTONG JIANGHAI CAPACITOR CO., LTD.

- 기타 기업

- KYOCERA AVX COMPONENTS CORPORATION

- KEMET CORPORATION

- SPEL TECHNOLOGIES PRIVATE LTD.

- VINATECH CO., LTD.

- KELTRON COMPONENT COMPLEX LTD

- WUXI CRE NEW ENERGY TECHNOLOGY CO., LTD.

- JINZHOU KAIMEI POWER CO.LTD

- SHENZHEN CHUANGSHIDING ELECTRONICS CO.,LTD

- ELNA CO., LTD.

- AOWEI TECHNOLOGY SHANGHAI

- ZHONGTIAN SUPERCAPACITOR TECHNOLOGY CO., LTD.

- SCHURTER

- SHANGHAI GREEN TECH CO., LTD.

- WURTH ELEKTRONIK EISOS GMBH & CO. KG

제13장 부록

JHS 25.08.28At a CAGR of 16.1%, the global supercapacitor market is projected to grow from USD 1.35 billion in 2025 to USD 2.84 billion by 2030. The automotive sector remains the primary driver, with supercapacitors increasingly adopted in electric vehicles (EVs), hybrid systems, and start-stop applications to support rapid charge-discharge cycles and peak power demands.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Type, Capacitance Range, End User, and Region |

| Regions covered | North America, Europe, APAC, RoW |

Beyond mobility, demand is also rising across consumer electronics, industrial automation, and energy sectors where the need for high-power density, extended cycle life, and fast response times is critical. Supercapacitors are deployed in backup power systems, voltage stabilization, and grid-side energy storage, especially in renewable integrations. In portable devices and IoT infrastructure, they offer quick charging, extended lifespan, and reliable performance. Technological advancements in electrode materials, particularly carbon-based and hybrid designs, improve energy density and expand their utility across broader applications. As industries increasingly prioritize electrification, efficiency, and resilience, the demand for high-performance supercapacitor solutions is set to grow significantly across diverse end-use segments.

">1,000 F segment is projected to exhibit the highest CAGR between 2025 and 2030."

The >1,000 F segment is expected to witness the highest CAGR during the forecast period, driven by its expanding role in applications that demand high energy buffering, rapid charge-discharge cycles, and extended service life. These high-capacitance supercapacitors are increasingly adopted in sectors such as grid energy storage, rail transportation, industrial automation, and backup power systems, where conventional batteries fall short in meeting surge power and longevity requirements. Their ability to deliver stable performance in extreme operating conditions and reduce maintenance needs makes them ideal for mission-critical and high-load environments. Additionally, ongoing efforts to integrate >1,000 F into hybrid energy systems, particularly in microgrids and regenerative braking solutions, further accelerate their adoption. The growth is also supported by investments in large-format supercapacitor modules designed to handle higher voltages and energy throughput in compact form factors. As industries prioritize efficiency, uptime, and power reliability, this segment is set to witness the strongest growth trajectory.

"Automotive & transportation segment to account for the largest share of the supercapacitor market during the forecast period."

The automotive & transportation segment is projected to lead the supercapacitor market during the forecast period, fueled by the rising demand for efficient energy storage and rapid power delivery in electric and hybrid vehicles. Supercapacitors are increasingly integrated into vehicle systems for functions such as regenerative braking, start-stop systems, and power stabilization, offering advantages over traditional batteries in terms of longer lifecycle, higher power density, and superior low-temperature performance. In commercial fleets, railways, and electric buses, supercapacitors enable rapid energy recovery and short charging cycles, aligning with global efforts to reduce emissions and enhance fuel economy. The shift toward electrification, supportive government regulations, and investment in sustainable mobility infrastructure creates substantial growth opportunities for supercapacitor technologies. As OEMs prioritize lightweight, high-efficiency energy systems, the segment is expected to lead the market.

"Asia Pacific is expected to register the highest CAGR in the supercapacitor market from 2025 to 2030."

Asia Pacific is expected to register the highest CAGR in the supercapacitor market during the forecast period, fueled by accelerating industrial activity, growing demand for energy-efficient technologies, and rising adoption of electric vehicles (EVs). Countries such as China, Japan, South Korea, and India are at the forefront of deploying supercapacitors across key sectors, including transportation, consumer electronics, and renewable energy. China, being the global leader in EV production and battery manufacturing, is significantly contributing to the regional demand. At the same time, Japan and South Korea continue to invest in high-performance energy storage technologies. Meanwhile, the electrification of public transport systems and grid modernization efforts in Southeast Asia further enhance the regional outlook. The availability of skilled manufacturing hubs and expanding domestic consumption of portable electronics and automotive technologies position Asia Pacific as a key driver for supercapacitor market expansion over the coming years.

Breakdown of primaries

Various executives from key organizations operating in the Supercapacitor market were interviewed in-depth, including CEOs, marketing directors, and innovation and technology directors.

- By Company Type: Tier 1 -45%, Tier 2 - 35%, and Tier 3 - 20%

- By Designation: Directors - 45%, C-level - 30%, and Others - 25%

- By Region: Asia Pacific - 45%, North America - 25%, Europe - 20%, and RoW - 10%

Note: Other designations include sales and product managers. The three tiers of the companies are defined based on their total revenue in 2024: Tier 1 - revenue greater than or equal to USD 500 million; Tier 2 - revenue between USD 100 million and USD 500 million; and Tier 3 revenue less than or equal to USD 100 million.

Major players profiled in this report are as follows: Maxwell Technologies (US), LS Materials (South Korea), Nippon Chemi-Con Corporation (Japan), Eaton (Ireland), CAP-XX (Australia), Nantong Jianghai capacitor Co., Ltd.(China), KYOCERA AVX Components Corporation (US), KEMET Corporation (US), Tecate Group (US), Cornell Dubilier (US), IOXUS (US), Skeleton Technologies (Estonia), KORCHIP CORPORATION (South Korea), Jinzhou Kaimei Power Co.Ltd (China), ELNA CO., LTD. (Japan), SCHURTER (Switzerland), Zhongtian Supercapacitor Technology Co., Ltd. (China), VINATech Co.,Ltd. (South Korea), Wurth Elektronik eiSos GmbH & Co. KG (Germany), AOWEI TECHNOLOGY Shanghai (China), Wuxi CRE New Energy Technology Co., Ltd. (China), SPEL TECHNOLOGIES PRIVATE LIMITED (India), shenzhen chuangshiding electronics co.,ltd, (China), Shanghai Green Tech Co.,Ltd. (China) and Keltron Component Complex Ltd (India). These leading companies possess a wide portfolio of products, establishing a prominent presence in established as well as emerging markets.

The study provides a detailed competitive analysis of these key players in the supercapacitor market, presenting their company profiles, most recent developments, and key market strategies.

Research Coverage

In this report, the supercapacitor market has been segmented based on type, capacitance range, end user, and region. The type segment includes electric double layer capacitors (EDLCs) and hybrid capacitors. The capacitance range segment is categorized into <100 F, 100-1,000 F, and >1,000 F. Based on end users, the market is segmented into consumer electronics, automotive & transportation, energy & power, industrial, and other end users (aerospace and medical devices). The regional analysis covers North America, Europe, Asia Pacific, and RoW.

Reasons to buy the report

The report will help the leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market and the sub-segments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the supercapacitor market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

Key Benefits of Buying the Report

- Analysis of key drivers (Rising EV Adoption, Rising Demand for Fast-Charging Energy Storage Solutions, Increased Adoption in Renewable Energy Systems, Rising Industrial Automation and Robotics, High Power Density Enabling Instantaneous Energy Delivery), restraints (Limited Suitability for Long-Term Energy Storage, High Initial Cost Compared to Batteries), opportunities (Expanding Integration of Supercapacitors in Next-Generation Aircraft Systems, Rising Use of Supercapacitors as a Sustainable Alternative to Conventional Batteries, Advancements in Materials and Manufacturing Technologies, Emerging Applications in Wearables and IoT Devices), and challenges (Lack of Standardization Across Manufacturers, Temperature Sensitivity and Durability Concerns) influencing the growth of the supercapacitor market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the supercapacitor market.

- Market Development: Comprehensive information about lucrative markets-the report analyses the supercapacitor market across varied regions.

- Market Diversification: Exhaustive information about new products/services, untapped geographies, recent developments, and investments in the supercapacitor market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Maxwell Technologies (US), LS Materials (South Korea), Nippon Chemi-Con Corporation (Japan), Eaton (Ireland), and CAP-XX (Australia).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 LIMITATIONS

- 1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY AND PRIMARY RESEARCH

- 2.1.2 SECONDARY DATA

- 2.1.2.1 List of key secondary sources

- 2.1.2.2 Key data from secondary sources

- 2.1.3 PRIMARY DATA

- 2.1.3.1 Key data from primary sources

- 2.1.3.2 Key industry insights

- 2.1.3.3 List of primary interview participants

- 2.1.3.4 Breakdown of primaries

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RESEARCH LIMITATIONS

- 2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SUPERCAPACITOR MARKET

- 4.2 SUPERCAPACITOR MARKET, BY TYPE

- 4.3 SUPERCAPACITOR MARKET, BY CAPACITANCE RANGE

- 4.4 SUPERCAPACITOR MARKET, BY END USE

- 4.5 SUPERCAPACITOR MARKET, BY GEOGRAPHY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing need for advanced energy storage components for electric vehicles

- 5.2.1.2 Mounting demand for fast-charging energy storage solutions

- 5.2.1.3 Rapid expansion of renewable energy capacity

- 5.2.1.4 Growing focus on automation to optimize industrial operations

- 5.2.1.5 Increasing demand for fast and efficient energy delivery in industries

- 5.2.2 RESTRAINTS

- 5.2.2.1 Limited suitability for long-term energy storage

- 5.2.2.2 High initial costs compared with conventional batteries

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rising integration of supercapacitors into next-generation aircraft systems

- 5.2.3.2 Emergence of supercapacitors as sustainable alternative to smaller conventional batteries

- 5.2.3.3 Continuous innovation in materials science and manufacturing processes

- 5.2.3.4 Mounting deployment of wearables and IoT devices

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of standardized performance benchmarks, testing protocols, and safety certifications

- 5.2.4.2 Temperature sensitivity and durability concerns

- 5.2.1 DRIVERS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 PRICING ANALYSIS

- 5.4.1 PRICING RANGE OF SUPERCAPACITOR CELLS OFFERED BY KEY PLAYERS, 2024

- 5.4.2 AVERAGE SELLING PRICE TREND OF SUPERCAPACITOR CELLS, BY CAPACITANCE RANGE, 2021-2024

- 5.4.3 AVERAGE SELLING PRICE TREND OF <100 F SUPERCAPACITOR CELLS, BY REGION, 2021-2024

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 TECHNOLOGY ANALYSIS

- 5.6.1 KEY TECHNOLOGIES

- 5.6.1.1 Advanced electrode materials

- 5.6.1.2 Solid-state electrolytes

- 5.6.2 COMPLEMENTARY TECHNOLOGIES

- 5.6.2.1 Regenerative braking systems

- 5.6.2.2 Wireless charging systems

- 5.6.3 ADJACENT TECHNOLOGIES

- 5.6.3.1 Lithium-ion batteries

- 5.6.3.2 Power electronics

- 5.6.1 KEY TECHNOLOGIES

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 247 ENERGY AND CE+T POWER HELP INTEGRATE SUPERCAPACITOR-BASED ENERGY STORAGE SYSTEMS IN LOGISTICS COMPANY IN NETHERLANDS

- 5.7.2 NIDEC CONVERSION DESIGNS PROPULSION SYSTEM POWERED BY 128 SUPERCAPACITORS FOR ALL-ELECTRIC PASSENGER FERRY IN FRANCE

- 5.7.3 MATERIAL HANDLING OEM INTEGRATES EATON'S XTM-18 SUPERCAPACITOR MODULES TO OPTIMIZE WAREHOUSE AUTOMATION

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT SCENARIO (HS CODE 853229)

- 5.8.2 EXPORT SCENARIO (HS CODE 853229)

- 5.9 PATENT ANALYSIS

- 5.10 IMPACT OF AI ON SUPERCAPACITOR MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 IMPACT OF AI ON KEY END USES OF SUPERCAPACITORS

- 5.10.2.1 Automotive

- 5.10.2.2 Energy storage

- 5.10.2.3 Industrial

- 5.10.3 AI USE CASES IN SUPERCAPACITOR MARKET

- 5.10.4 FUTURE OF AI IN SUPERCAPACITOR ECOSYSTEM

- 5.11 IMPACT OF 2025 US TARIFF ON SUPERCAPACITOR MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END USES

6 ELECTRODE MATERIALS FOR SUPERCAPACITORS

- 6.1 INTRODUCTION

- 6.2 CARBON

- 6.2.1 ACTIVATED CARBON

- 6.2.2 CARBON NANOTUBES

- 6.2.3 GRAPHENE

- 6.2.4 CARBIDE-DERIVED CARBON

- 6.2.5 CARBON AEROGELS

- 6.3 COMPOSITES

- 6.3.1 CARBON-METAL OXIDE

- 6.3.2 CARBON CONDUCTING POLYMERS

- 6.4 OTHER ELECTRODE MATERIALS

- 6.4.1 METAL OXIDES

- 6.4.1.1 Ruthenium oxide

- 6.4.1.2 Nickel oxide

- 6.4.1.3 Manganese oxide

- 6.4.2 CONDUCTING POLYMERS

- 6.4.2.1 Polyaniline

- 6.4.2.2 Polypyrrole

- 6.4.2.3 Polyacene

- 6.4.2.4 Polyacetylene

- 6.4.1 METAL OXIDES

7 SUPERCAPACITOR MARKET, BY TYPE

- 7.1 INTRODUCTION

- 7.2 ELECTRIC DOUBLE-LAYER CAPACITORS

- 7.2.1 SURGING ADOPTION OF ELECTRIC VEHICLES AND TECHNOLOGICAL ADVANCEMENTS TO FUEL SEGMENTAL GROWTH

- 7.3 HYBRID CAPACITORS

- 7.3.1 INCREASING PRODUCTION FOR COMPACT, HIGH-DEMAND APPLICATIONS TO DRIVE MARKET

- 7.4 PSEUDOCAPACITORS (QUALITATIVE)

8 SUPERCAPACITOR MARKET, BY CAPACITANCE RANGE

- 8.1 INTRODUCTION

- 8.2 <100 F

- 8.2.1 HIGH EFFECTIVENESS IN DEVICES REQUIRING RAPID ENERGY DISCHARGE AND MINIMAL MAINTENANCE TO FUEL SEGMENTAL GROWTH

- 8.3 100-1,000 F

- 8.3.1 IDEAL BALANCE OF ENERGY DENSITY, POWER OUTPUT, AND DESIGN FLEXIBILITY TO CONTRIBUTE TO SEGMENTAL GROWTH

- 8.4 >1,000 F

- 8.4.1 ABILITY TO OFFER RAPID ENERGY BURSTS AND LOAD BALANCING TO BOLSTER SEGMENTAL GROWTH

9 SUPERCAPACITOR MARKET, BY END USE

- 9.1 INTRODUCTION

- 9.2 AUTOMOTIVE & TRANSPORTATION

- 9.2.1 ABILITY TO IMPROVE ACCELERATION, REDUCE STRESS, AND EXTEND LIFE OF BATTERIES TO DRIVE MARKET

- 9.3 ENERGY & POWER

- 9.3.1 INCREASING INVESTMENT IN BATTERY SYSTEMS AND RENEWABLE ENERGY ADOPTION TO DRIVE MARKET

- 9.4 CONSUMER ELECTRONICS

- 9.4.1 RISING ADOPTION OF SUPERCAPACITORS TO ENHANCE POWER EFFICIENCY AND REDUCE BATTERY STRESS TO BOOST SEGMENTAL GROWTH

- 9.5 INDUSTRIAL

- 9.5.1 INCREASING USE OF SUPERCAPACITORS TO ENHANCE RELIABILITY AND BACKUP POWER PERFORMANCE TO AUGMENT SEGMENTAL GROWTH

- 9.6 OTHER END USES

10 SUPERCAPACITOR MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 US

- 10.2.1.1 Rising adoption of plug-in electric vehicles to contribute to market growth

- 10.2.2 CANADA

- 10.2.2.1 Increasing investment in renewable energy and transportation infrastructure to accelerate market growth

- 10.2.3 MEXICO

- 10.2.3.1 Escalating sales of hybrid and fully electric vehicles to bolster market growth

- 10.2.1 US

- 10.3 EUROPE

- 10.3.1 GERMANY

- 10.3.1.1 Rising advanced manufacturing and aerospace innovation to expedite market growth

- 10.3.2 UK

- 10.3.2.1 Supportive medical device regulatory frameworks to contribute to market growth

- 10.3.3 FRANCE

- 10.3.3.1 Increasing investment in next-generation energy storage solutions to boost market growth

- 10.3.4 ITALY

- 10.3.4.1 Growing emphasis on sustainable urban mobility and modernization of public transport systems to drive market

- 10.3.5 REST OF EUROPE

- 10.3.1 GERMANY

- 10.4 ASIA PACIFIC

- 10.4.1 CHINA

- 10.4.1.1 Strong focus on industrialization and digital infrastructure development to augment market growth

- 10.4.2 JAPAN

- 10.4.2.1 Mounting automobile production to contribute to market growth

- 10.4.3 SOUTH KOREA

- 10.4.3.1 Increasing R&D spending to support manufacturing innovation to fuel market growth

- 10.4.4 INDIA

- 10.4.4.1 Ongoing energy transition and infrastructure modernization to drive market

- 10.4.5 REST OF ASIA PACIFIC

- 10.4.1 CHINA

- 10.5 ROW

- 10.5.1 SOUTH AMERICA

- 10.5.1.1 Government support for clean energy to augment market growth

- 10.5.2 MIDDLE EAST

- 10.5.2.1 Increasing investment in renewable energy, electric mobility, and smart infrastructure to drive market

- 10.5.2.2 GCC countries

- 10.5.2.3 Rest of Middle East

- 10.5.3 AFRICA

- 10.5.3.1 Rapid urbanization and thriving automotive sector to bolster market growth

- 10.5.1 SOUTH AMERICA

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 11.3 MARKET SHARE ANALYSIS, 2024

- 11.4 REVENUE ANALYSIS, 2020-2024

- 11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- 11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.5.5.1 Company footprint

- 11.5.5.2 Region footprint

- 11.5.5.3 Type footprint

- 11.5.5.4 Capacitance range footprint

- 11.5.5.5 End use footprint

- 11.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- 11.7 COMPETITIVE SCENARIO

- 11.7.1 PRODUCT LAUNCHES

- 11.7.2 DEALS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 MAXWELL TECHNOLOGIES

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Solutions/Services offered

- 12.1.1.3 MnM view

- 12.1.1.3.1 Key strengths/Right to win

- 12.1.1.3.2 Strategic choices

- 12.1.1.3.3 Weaknesses/Competitive threats

- 12.1.2 LS MATERIALS

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Solutions/Services offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches

- 12.1.2.4 MnM view

- 12.1.2.4.1 Key strengths/Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses/Competitive threats

- 12.1.3 NIPPON CHEMI-CON CORPORATION

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Solutions/Services offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches

- 12.1.3.3.2 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths/Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses/Competitive threats

- 12.1.4 EATON

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Solutions/Services offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Deals

- 12.1.4.4 MnM view

- 12.1.4.4.1 Key strengths/Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses/Competitive threats

- 12.1.5 CAP-XX

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Solutions/Services offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Deals

- 12.1.5.3.2 Other developments

- 12.1.5.4 MnM view

- 12.1.5.4.1 Key strengths/Right to win

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses/Competitive threats

- 12.1.6 TECATE GROUP

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Solutions/Services offered

- 12.1.7 CORNELL DUBILIER

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Solutions/Services offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Deals

- 12.1.8 IOXUS

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Solutions/Services offered

- 12.1.9 SKELETON TECHNOLOGIES

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Solutions/Services offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Product launches

- 12.1.9.3.2 Deals

- 12.1.9.3.3 Expansions

- 12.1.9.3.4 Other developments

- 12.1.10 KORCHIP CORPORATION

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Solutions/Services offered

- 12.1.11 NANTONG JIANGHAI CAPACITOR CO., LTD.

- 12.1.11.1 Business overview

- 12.1.11.2 Products/Solutions/Services offered

- 12.1.1 MAXWELL TECHNOLOGIES

- 12.2 OTHER PLAYERS

- 12.2.1 KYOCERA AVX COMPONENTS CORPORATION

- 12.2.2 KEMET CORPORATION

- 12.2.3 SPEL TECHNOLOGIES PRIVATE LTD.

- 12.2.4 VINATECH CO., LTD.

- 12.2.5 KELTRON COMPONENT COMPLEX LTD

- 12.2.6 WUXI CRE NEW ENERGY TECHNOLOGY CO., LTD.

- 12.2.7 JINZHOU KAIMEI POWER CO.LTD

- 12.2.8 SHENZHEN CHUANGSHIDING ELECTRONICS CO.,LTD

- 12.2.9 ELNA CO., LTD.

- 12.2.10 AOWEI TECHNOLOGY SHANGHAI

- 12.2.11 ZHONGTIAN SUPERCAPACITOR TECHNOLOGY CO., LTD.

- 12.2.12 SCHURTER

- 12.2.13 SHANGHAI GREEN TECH CO., LTD.

- 12.2.14 WURTH ELEKTRONIK EISOS GMBH & CO. KG

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS