|

시장보고서

상품코드

1796193

AI 어시스턴트 시장 예측(-2030년) : 서비스, 용도별AI Assistant Market by Offering, Application - Global Forecast to 2030 |

||||||

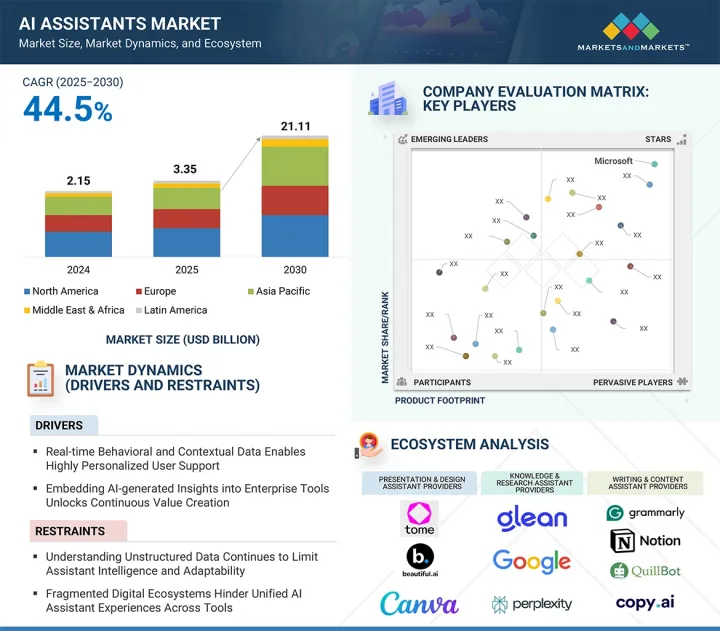

AI 어시스턴트 시장 규모는 2025년 33억 5,000만 달러에서 예측 기간 중 CAGR 44.5%로 추이하며, 2030년에는 211억 1,000만 달러로 성장할 것으로 예측됩니다.

AI 어시스턴트 시장은 플러그인, API, 통합 마켓플레이스의 급증으로 어시스턴트가 CRM, ERP, 수많은 틈새 SaaS 툴와 원활하게 연결될 수 있게 되면서 빠르게 성장하고 있습니다. 이러한 오케스트레이션 기능의 강화는 기업이 파편화된 워크플로우를 통합하고 반복적인 작업을 보다 효율적으로 자동화할 수 있도록 돕습니다.

| 조사 범위 | |

|---|---|

| 조사 대상연도 | 2020-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 달러(달러) |

| 부문 | 제공·용도·최종사용자·지역 |

| 대상 지역 | 북미·유럽·아시아태평양·중동 & 아프리카·라틴아메리카 |

"최종사용자별로는 BFSI 부서가 AI 어시스턴트 도입을 주도하며 컴플라이언스, 효율성, 고객 중심 업무 추진"

BFSI 부문은 방대한 데이터 관리, 복잡한 컴플라이언스 프로세스, 보다 효율적인 고객 대응의 필요성으로 인해 2025년 AI 비서 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 주요 은행과 보험사들은 기존에 수작업으로 진행되던 부정행위 감지, 거래 모니터링, 규제 보고 등의 업무를 자동화하기 위해 지능형 어시스턴트를 빠르게 도입하고 있습니다. 많은 금융기관들은 이미 AI 코파일럿을 도입하여 관계 관리자를 지원하고, 고객 온보딩을 효율화하며, 자산 운용 및 자문 업무를 위한 맞춤형 인사이트를 생성하는 등 다양한 서비스를 제공합니다.

디지털 퍼스트 뱅킹, 모바일 앱, 원격 자문 모델의 성장으로 일상적인 문의 대응, 안전한 거래 지원, 개인화된 제안을 실현하는 대화형 AI에 대한 수요가 더욱 증가하고 있습니다. AI 기반 어시스턴트는 엄격한 프라이버시, 보안 및 규제 요건을 충족하기 위해 감사 추적을 자동화하고 분산된 팀 전체에서 일관된 컴플라이언스를 유지할 수 있도록 돕습니다. BFSI 조직이 디지털 전환과 고객 중심 혁신에 지속적으로 투자하는 가운데, AI 어시스턴트는 서비스 품질 향상, 업무 강인성 및 생산성 향상에 필수적인 요소로 자리 잡으며 전체 기업 AI 어시스턴트 시장에서 가장 큰 도입 분야로 자리매김하고 있습니다. 하고 있습니다.

"용도별로는 API 기반 AI 비서 부문이 유연하고 확장 가능한 기업 워크플로우 통합으로 빠른 성장을 주도한다."

API 기반 AI 어시스턴트는 조직이 다양한 디지털 워크플로우에 인텔리전스를 통합하기 위해 유연하고 모듈화된 통합 프레임워크를 우선시하는 경향이 높아짐에 따라 예측 기간 중 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 임베디드나 독립형 어시스턴트와 달리 API 퍼스트 모델은 기존 용도이나 맞춤형 포털, 자체 플랫폼에 대화형 및 생성형 기능을 직접 통합할 수 있으며, 재설계 비용을 절감할 수 있는 것이 장점입니다.

이 접근 방식은 복잡한 멀티 벤더 기술 기반을 가진 중견 및 대기업에 특히 인기가 높으며, CRM, ERP, 문서 관리 시스템, 산업별 전문 소프트웨어 간의 원활한 상호 운용성을 실현합니다. 주요 기술 프로바이더와 스타트업은 API 마켓플레이스와 개발 툴을 확장하여 컨텍스트 검색, 실시간 요약, 개인화된 작업 자동화 등의 이용 사례에 맞게 어시스턴트를 쉽게 배포하고 확장할 수 있도록 돕고 있습니다.

헤드리스 아키텍처와 마이크로서비스로의 전환은 API 기반 어시스턴트에 대한 수요를 더욱 증가시켜 기업이 인텔리전스를 적용하는 장소와 방법을 세밀하게 제어할 수 있도록 했습니다. 특히 BFSI, 의료, 전문 서비스 등의 분야에서는 컴플라이언스 요구사항을 충족시키면서 사용자 경험을 대규모로 커스터마이징하기 위해 API 기반 AI 도입이 빠르게 진행되고 있습니다.

"아시아태평양은 혁신과 신기술에 힘입어 AI 어시스턴트가 빠르게 성장하고 있으며, 시장 규모는 북미가 주도하고 있습니다. "

아시아태평양은 대규모 디지털 투자, 확대되는 기술 인력, 각국의 국가 AI 전략에 힘입어 예측 기간 중 AI 어시스턴트 시장에서 가장 빠른 성장을 보일 것으로 예측됩니다. 이 지역의 은행, 소매, 의료 등의 기업은 워크플로우 자동화, 다국어 커뮤니케이션 개선, 기존 채널을 넘어선 고객 참여 확대를 위해 AI 어시스턴트 도입을 적극 추진하고 있습니다. 스타트업과 지역 기술 혁신가들의 급격한 성장도 지역 고유의 언어, 규제, 문화적 특성에 대응하는 지역 특화형 AI 비서 개발을 촉진하고 있습니다.

한편, 북미는 기업 클라우드의 높은 성숙도, AI 연구개발 투자 규모, 주요 기술 벤더의 존재에 힘입어 가장 큰 규모를 유지할 것으로 예측됩니다. 북미 기업은 생산성 스위트, CRM 플랫폼, 지식 관리 툴 등에 내장된 산업별 코파일럿을 일찍이 도입하여 복잡한 업무와 의사결정을 최적화하고 있습니다. 또한 책임감 있는 AI와 거버넌스 프레임워크 개선에 중점을 두면서 광범위하게 분산된 팀과 하이브리드 업무 환경에 AI 어시스턴트 배포를 가속화하고 있습니다.

세계의 AI 어시스턴트 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인의 분석, 기술·특허의 동향, 법규제 환경, 사례 연구, 시장 규모 추이·예측, 각종 구분·지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요·업계 동향

- 시장 역학

- 촉진요인

- 억제요인

- 기회

- 과제

- AI 어시스턴트의 진화

- 공급망 분석

- 에코시스템 분석

- 부문 및 직무에서 AI 어시스턴트의 이용 패턴

- 워크플로우 혼란 존 : AI 어시스턴트가 레거시 툴을 대신하는 장소

- AI 어시스턴트의 수익화 모델

- 페르소나 지도제작

- 투자와 자금조달 시나리오

- 사례 연구 분석

- 기술 분석

- 규제 상황

- 특허 분석

- 가격 분석

- 주요 컨퍼런스와 이벤트

- Porter's Five Forces 분석

- 주요 이해관계자 구입 기준

- 고객 사업에 영향을 미치는 동향/혼란

제6장 AI 어시스턴트 시장 : 제공별

- 라이팅 & 컨텐츠 어시스턴트

- 회의 및 협업 어시스턴트

- 지식·조사 어시스턴트

- 스케줄 관리와 캘린더 최적화 어시스턴트

- 영업·잠재 고객 개발 어시스턴트

- 개발자 생산성 어시스턴트

- 프레젠테이션 & 디자인 어시스턴트

- 분석 및 스프레드시트 어시스턴트

제7장 AI 어시스턴트 시장 : 통합 유형별

- 스탠드얼론 어시스턴트

- SaaS 네이티브 어시스턴트

- 브라우저 확장 기능/플러그인

- API 기반 어시스턴트

- 워크스페이스 애드온

제8장 AI 어시스턴트 시장 : 용도별

- AI를 활용한 라이팅과 편집

- 회의 기록과 팔로 업

- 지식 검색과 문서 검색

- 스케줄과 작업 우선순위 결정

- 리드 관여와 메일 시퀀스

- 코드 보완과 리뷰

- 프레젠테이션과 내러티브 디자인

- 데이터 탐색과 스프레드시트 AI

- 기타

제9장 AI 어시스턴트 시장 : 최종사용자별

- 개인 최종사용자

- 기업

- BFSI

- 통신

- 정부·공공 부문

- 의료 & 생명과학

- 제조

- 미디어 & 엔터테인먼트

- 소매·E-Commerce

- 기술 프로바이더

- 전문 서비스 프로바이더

- 교육

- 기타

제10장 AI 어시스턴트 시장 : 지역별

- 북미

- 시장 성장 촉진요인

- 거시경제 전망

- 미국

- 캐나다

- 유럽

- 시장 성장 촉진요인

- 거시경제 전망

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 기타

- 아시아태평양

- 시장 성장 촉진요인

- 거시경제 전망

- 중국

- 인도

- 일본

- 한국

- 싱가포르

- 호주와 뉴질랜드

- 기타

- 중동 및 아프리카

- 시장 성장 촉진요인

- 거시경제 전망

- 사우디아라비아

- 아랍에미리트

- 카타르

- 튀르키예

- 남아프리카공화국

- 기타

- 라틴아메리카

- 시장 성장 촉진요인

- 거시경제 전망

- 브라질

- 멕시코

- 아르헨티나

- 기타

제11장 경쟁 구도

- 개요

- 주요 참여 기업의 전략/강점

- 매출 분석

- 시장 점유율 분석

- 브랜드/제품 비교

- 기업 평가와 재무 지표

- 기업 평가 매트릭스 : 주요 기업

- 기업 평가 매트릭스 : 스타트업/중소기업

- 경쟁 시나리오

제12장 기업 개요

- 주요 기업

- MICROSOFT

- SALESFORCE

- SAP

- ORACLE

- ADOBE

- AWS

- CISCO

- SERVICENOW

- DROPBOX

- ZOOM

- BOX

- ATLASSIAN

- NOTION

- ASANA

- MONDAY.COM

- CLICKUP

- MIRO

- GRAMMARLY

- DOCUSIGN

- LUCID SOFTWARE

- GAMMA

- CANVA

- 스타트업 /SME

- GLEAN

- OTTER.AI

- FIREFLIES.AI

- FATHOM

- SCRIBE AI

- TOME

- JASPER

- COPY.AI

- WRITER.COM

- SYNTHESIA

- BEAUTIFUL.AI

- HIVER

- SUPERNORMAL

- HYPERWRITE

- QUILLBOT

- COPYSMITH

- ABRIDGE

- DESCRIPT

- LUMEN5

- RUNWAY

- PERPLEXITY AI

- REGIE.AI

제13장 인접 시장과 관련 시장

제14장 부록

KSA 25.09.01The AI assistants market is projected to grow from USD 3.35 billion in 2025 to USD 21.11 billion by 2030 at a compound annual growth rate (CAGR) of 44.5% during the forecast period. The AI assistants market is rapidly expanding as the surge in plug-ins, APIs, and integration marketplaces empowers assistants to seamlessly connect with CRMs, ERPs, and countless niche SaaS tools. This growing orchestration capability helps enterprises unify fragmented workflows and automate repetitive tasks more effectively.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | USD (Million) |

| Segments | Offering, Integration Type, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

However, this growth is restrained by the reality of disconnected, legacy tech stacks that make it challenging to deploy AI assistants that operate smoothly across multiple systems without costly custom integrations. Balancing robust plug-in ecosystems with seamless interoperability remains crucial for driving true enterprise-wide adoption.

"BFSI Sector Leads AI Assistant Adoption to Drive Compliance, Efficiency, and Customer-centric Operations"

The Banking, Financial Services, and Insurance (BFSI) sector is expected to capture the largest share of the AI assistants market in 2025, driven by the industry's need to manage vast volumes of data, complex compliance processes, and customer interactions with greater efficiency. Leading banks and insurers are rapidly integrating intelligent assistants to automate tasks such as fraud detection, transaction monitoring, and regulatory reporting, which traditionally demand extensive manual effort. Many financial institutions are now deploying AI co-pilots to support relationship managers, streamline client onboarding, and generate tailored insights for wealth management and advisory services. The growth of digital-first banking, mobile apps, and remote advisory models has further accelerated the demand for conversational AI to handle routine queries, support secure transactions, and deliver personalized recommendations. AI-powered assistants help firms navigate strict privacy, security, and regulatory requirements by automating audit trails and maintaining compliance consistency across distributed teams. As BFSI organizations continue to invest in digital transformation and customer-centric innovations, AI assistants are becoming integral to improving service quality, operational resilience, and productivity, ultimately strengthening the sector's position as the largest adopter within the broader enterprise AI assistants market.

"API-based AI Assistants Drive Rapid Growth with Flexible, Scalable Integration Across Enterprise Workflows"

API-based AI assistants are projected to record the highest compound annual growth rate during the forecast period, as organizations increasingly prioritize flexible, modular integration frameworks to embed intelligence into diverse digital workflows. Unlike embedded or standalone assistants, API-first models allow enterprises to integrate conversational and generative capabilities directly into existing applications, custom portals, or proprietary platforms without costly re-architecture. This approach is especially popular among mid-to-large enterprises operating complex multi-vendor tech stacks, as it ensures seamless interoperability across CRMs, ERPs, document management systems, and industry-specific software. Leading technology providers and startups alike are expanding API marketplaces and developer toolkits that make it easier for IT teams to deploy and scale assistants for use cases such as contextual search, real-time summarization, and personalized task automation. The shift toward headless architecture and microservices has further strengthened the demand for API-based assistants, giving businesses granular control over where and how intelligence is applied. Additionally, sectors like BFSI, healthcare, and professional services are rapidly embracing API-driven AI to meet compliance requirements while customizing user experiences at scale.

"Asia Pacific to witness rapid AI assistants growth fueled by innovation and emerging technologies, while North America leads in market size"

Asia Pacific is poised to witness the fastest growth in the AI assistants market during the forecast period, driven by massive digital investments, growing tech talent pools, and supportive national AI strategies across countries in the region. Organizations across sectors such as banking, retail, and healthcare are actively experimenting with AI assistants to automate workflows, improve multilingual communication, and extend customer engagement beyond traditional channels. The rapid expansion of startups and local tech innovators is also fueling the development of regionally relevant AI assistants that address unique language, compliance, and cultural nuances. In contrast, North America is set to maintain its position as the largest market for AI assistants due to its mature enterprise cloud adoption, high investment in AI R&D, and the presence of leading technology vendors that continue to enhance AI integration in SaaS ecosystems. Companies in North America are also early adopters of industry-specific co-pilots embedded within productivity suites, CRM platforms, and knowledge management tools, helping to optimize complex operations and decision-making. With a strong focus on responsible AI and continuous improvement in governance frameworks, North American enterprises are accelerating the deployment of AI assistants across large, distributed teams and hybrid work environments. Together, these factors reinforce Asia Pacific's role as the fastest-growing market and North America's leadership in large-scale enterprise AI assistant deployment.

Breakdown of primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the AI assistants market.

- By Company: Tier I - 35%, Tier II - 45%, and Tier III - 20%

- By Designation: C Level - 35%, Director Level - 25%, and others - 40%

- By Region: North America - 42%, Europe - 20%, Asia Pacific - 25%, Middle East & Africa - 8%, and Latin America - 5%

The report includes a study of key players offering AI assistant solutions and services. It profiles major vendors in the AI assistants market. The major players in the AI assistants market include Microsoft (US), Google (US), Zoom (US), Salesforce (US), SAP (Germany), Oracle (US), Adobe (US), Dropbox (US), Box (US), Atlassian (Australia), Notion (US), Amazon (US), Cisco (US), ServiceNow (US), Asana (US), Monday.com (Israel), ClickUp (US), Miro (US), Grammarly (US), DocuSign (US), Lucid Software (US), Glean (US), Otter.ai (US), Fireflies.ai (US), Fathom (US), Scribe (US), Regie.ai (US), Tome (US), Gamma (US), Jasper (US), Copy.ai (US), Writer.com (US), Synthesia (UK), Beautiful.ai (US), Canva (Australia), Superhuman AI (US), Hiver (India), Supernormal (Sweden), HyperWrite (US), QuillBot (US), CopySmith (Canada), Abridge (US), Descript (US), Lumen5 (Canada), Runway (US), and Perplexity AI (US).

Research coverage

This research report covers the AI assistants market, which has been segmented based on offering, integration type, application, and end user. The offering segment consists of writing & content assistants, meeting & collaboration assistants, knowledge & research assistants, scheduling & calendar optimization assistants, sales & prospecting assistants, developer productivity assistants, presentation & design assistants, and analytical & spreadsheet assistants. The integration type segment consists of standalone assistants, SaaS-native assistants, browser extensions/plug-ins, API-based assistants, and workspace add-ons. The application segment includes AI-powered writing & editing, transcription & follow-up, knowledge retrieval & document search, scheduling & work prioritization, lead engagement & email sequencing, code completion & review, presentation & narrative design, data exploration & spreadsheet AI, and other applications. The end user segment consists of individual users and enterprises, which consist of BFSI, healthcare & life sciences, retail & ecommerce, technology providers, professional service providers, education, telecommunications, government & public sector, travel & hospitality, and other enterprises. The regional analysis of the AI assistants market covers North America, Europe, Asia Pacific, the Middle East & Africa (MEA), and Latin America.

Key Benefits of Buying the Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall AI assistants market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

Analysis of key drivers (modular deployment of AI assistants within SaaS platforms accelerating enterprise adoption, real-time behavioral and contextual data enables highly personalized user support, embedding AI-generated insights into enterprise tools unlocks continuous value creation, and context-aware assistants meet rising enterprise demand for intelligent task support), restraints (fragmented digital ecosystems hinder unified AI assistant experiences across tools, understanding unstructured data continues to limit assistant intelligence and adaptability), opportunities (low-code customization and multilingual support unlock broader enterprise adoption, proactive assistants that anticipate user needs unlock intelligent work orchestration, federated learning enables AI assistant personalization without compromising enterprise data privacy), and challenges (limits in generalization across roles and workflows restrict long-term scalability of AI assistants, rapid evolution of AI capabilities may outpace employee adaptation and organizational readiness).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the AI assistants market.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the AI assistants market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the AI assistants market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies and offerings of leading players like Microsoft (US), Google (US), Zoom (US), Salesforce (US), SAP (Germany), Oracle (US), Adobe (US), Dropbox (US), Box (US), Atlassian (Australia), Notion (US), Amazon (US), Cisco (US), ServiceNow (US), Asana (US), Monday.com (Israel), ClickUp (US), Miro (US), Grammarly (US), DocuSign (US), Lucid Software (US), Glean (US), Otter.ai (US), Fireflies.ai (US), Fathom (US), Scribe (US), Regie.ai (US), Tome (US), Gamma (US), Jasper (US), Copy.ai (US), Writer.com (US), Synthesia (UK), Beautiful.ai (US), Canva (Australia), Superhuman AI (US), Hiver (India), Supernormal (Sweden), HyperWrite (US), QuillBot (US), CopySmith (Canada), Abridge (US), Descript (US), Lumen5 (Canada), Runway (US), and Perplexity AI (US) among others in the AI assistants market. The report also helps stakeholders understand the pulse of the AI assistants market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 List of primary participants

- 2.1.2.2 Breakdown of primaries

- 2.1.2.3 Key industry insights

- 2.2 MARKET BREAKUP AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES IN AI ASSISTANT MARKET

- 4.2 AI ASSISTANT MARKET: TOP THREE APPLICATIONS

- 4.3 NORTH AMERICA: AI ASSISTANT MARKET, BY OFFERING AND FUNCTIONALITY

- 4.4 AI ASSISTANT MARKET, BY REGION

5 MARKET OVERVIEW AND INDUSTRY TRENDS (STRATEGIC DRIVERS WITH QUANTITATIVE IMPLICATIONS)

Unpacking the Forces Shaping AI Assistant: Adoption & Future Growth Opportunities

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Modular deployment of AI assistants within SaaS platforms accelerating enterprise adoption

- 5.2.1.2 Real-time behavioral and contextual data enables highly personalized user support

- 5.2.1.3 Embedding AI-generated insights into enterprise tools unlocks continuous value creation

- 5.2.1.4 Context-aware assistants meet rising enterprise demand for intelligent task support

- 5.2.2 RESTRAINTS

- 5.2.2.1 Fragmented digital ecosystems hinder unified AI assistant experiences across tools

- 5.2.2.2 Understanding unstructured data continues to limit assistant intelligence and adaptability

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Low-code customization and multilingual support unlock broader enterprise adoption

- 5.2.3.2 Proactive assistants that anticipate user needs unlock intelligent work orchestration

- 5.2.3.3 Federated learning enables AI assistant personalization without compromising enterprise data privacy

- 5.2.4 CHALLENGES

- 5.2.4.1 Limits in generalization across roles and workflows restrict long-term scalability of AI assistants

- 5.2.4.2 Rapid evolution of AI capabilities may outpace employee adaptation and organizational readiness

- 5.2.1 DRIVERS

- 5.3 EVOLUTION OF AI ASSISTANTS

- 5.4 SUPPLY CHAIN ANALYSIS

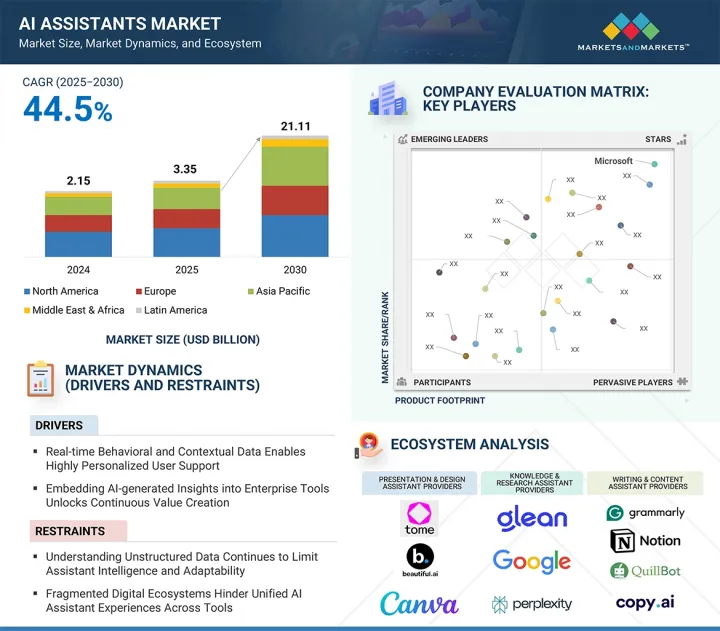

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 WRITING & CONTENT ASSISTANT PROVIDERS

- 5.5.2 MEETING & COLLABORATION ASSISTANT PROVIDERS

- 5.5.3 KNOWLEDGE & RESEARCH ASSISTANT PROVIDERS

- 5.5.4 SALES & PROSPECTING ASSISTANT PROVIDERS

- 5.5.5 DEVELOPER PRODUCTIVITY ASSISTANT PROVIDERS

- 5.5.6 PRESENTATION & DESIGN ASSISTANT PROVIDERS

- 5.5.7 SCHEDULING & CALENDAR OPTIMIZATION ASSISTANTS

- 5.5.8 ANALYTICS & SPREADSHEET ASSISTANTS

- 5.6 AI ASSISTANT USAGE PATTERNS ACROSS DEPARTMENTS AND JOB ROLES

- 5.6.1 ROLE-BASED VALUE CREATION IS OUTPACING DEPARTMENT-CENTRIC ADOPTION

- 5.6.2 ASSISTANT USAGE DENSITY IS HIGHEST IN MID-LEVEL, TASK-SATURATED ROLES

- 5.6.3 AI ASSISTANT USAGE IS STRONGEST IN COMMUNICATION-HEAVY WORKFLOWS

- 5.7 WORKFLOW DISRUPTION ZONES: WHERE AI ASSISTANTS REPLACE LEGACY TOOLS

- 5.7.1 HIGH-ENTROPY WORKFLOWS ARE FIRST TO BE DISRUPTED

- 5.7.2 ASSISTANTS OUTPERFORM LEGACY TOOLS IN LATENCY, ADAPTABILITY, AND MODULARITY

- 5.7.3 VERTICAL-SPECIFIC DISRUPTIONS ARE UNLOCKING DEEPER VALUE

- 5.8 MONETIZATION MODELS OF AI ASSISTANTS

- 5.8.1 SAAS-NATIVE AND PLATFORM-EMBEDDED MONETIZATION

- 5.8.2 VERTICAL SAAS AND ROLE-SPECIFIC MONETIZATION STRATEGIES

- 5.8.3 API CONSUMPTION AND CUSTOM ASSISTANT DEPLOYMENT

- 5.9 PERSONA MAPPING

- 5.9.1 AI ASSISTANT BUYER PROFILE

- 5.9.2 PROCUREMENT TRENDS: EMBEDDED VS. STANDALONE VS. CUSTOM ASSISTANTS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 JASPER EMPOWERED CUSHMAN & WAKEFIELD TO SCALE REAL ESTATE CONTENT CREATION

- 5.11.2 REGIE.AI HELPED CRUNCHBASE BOOST PROSPECTING PERSONALIZATION AND OUTREACH

- 5.11.3 REPLIT ENABLED ZINUS TO ACCELERATE DEVELOPMENT CYCLES AND COLLABORATION

- 5.11.4 SCRIBE TRANSFORMED D300'S PROCESS DOCUMENTATION AND KNOWLEDGE SHARING

- 5.11.5 DESCRIPT SUPPORTS HUBSPOT IN STREAMLINING AUDIO AND VIDEO CONTENT PRODUCTION

- 5.12 TECHNOLOGY ANALYSIS

- 5.12.1 KEY TECHNOLOGIES

- 5.12.1.1 Large Language Models (LLMs)

- 5.12.1.2 Natural Language Processing (NLP)

- 5.12.1.3 Prompt Engineering & Optimization

- 5.12.1.4 Context Management Systems

- 5.12.1.5 Retrieval-augmented Generation (RAG)

- 5.12.1.6 Embedding Models

- 5.12.2 COMPLEMENTARY TECHNOLOGIES

- 5.12.2.1 Vector Databases

- 5.12.2.2 Automated Speech Recognition (ASR)

- 5.12.2.3 Fine-tuning and Adapter Training

- 5.12.2.4 Function Calling Interfaces

- 5.12.3 ADJACENT TECHNOLOGIES

- 5.12.3.1 Human-computer Interaction (HCI)

- 5.12.3.2 Semantic Search Algorithms

- 5.12.3.3 Conversational Memory Architectures

- 5.12.3.4 Latent Attention Mechanisms

- 5.12.1 KEY TECHNOLOGIES

- 5.13 REGULATORY LANDSCAPE

- 5.13.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13.2 REGULATIONS

- 5.13.2.1 North America

- 5.13.2.1.1 California Consumer Privacy Act (CCPA)

- 5.13.2.1.2 California Privacy Rights Act (CPRA)

- 5.13.2.1.3 Children's Online Privacy Protection Act (COPPA)

- 5.13.2.1.4 Artificial Intelligence and Data Act (AIDA) (Canada)

- 5.13.2.1.5 Personal Information Protection and Electronic Documents Act (PIPEDA)

- 5.13.2.1.6 Algorithmic Accountability Act (proposed)

- 5.13.2.2 Europe

- 5.13.2.2.1 General Data Protection Regulation (GDPR)

- 5.13.2.2.2 EU Artificial Intelligence Act

- 5.13.2.2.3 Digital Services Act (DSA)

- 5.13.2.2.4 Digital Markets Act (DMA)

- 5.13.2.2.5 AI Liability Directive (proposed)

- 5.13.2.3 Asia Pacific

- 5.13.2.3.1 Personal Information Protection Law (PIPL)

- 5.13.2.3.2 Administrative Provisions on Deep Synthesis Internet Information Services

- 5.13.2.3.3 Algorithmic Recommendation Regulation

- 5.13.2.3.4 Act on the Protection of Personal Information (APPI)

- 5.13.2.3.5 Personal Data Protection Act (PDPA)

- 5.13.2.3.6 Singapore Model AI Governance Framework

- 5.13.2.3.7 Digital Personal Data Protection Act (DPDP Act, 2023)

- 5.13.2.4 Middle East & Africa

- 5.13.2.4.1 UAE Federal Data Protection Law (2021)

- 5.13.2.4.2 UAE AI Ethics Guidelines

- 5.13.2.4.3 Personal Data Protection Law (PDPL) - Saudi Arabia

- 5.13.2.4.4 Protection of Personal Information Act (POPIA) - South Africa

- 5.13.2.5 Latin America

- 5.13.2.5.1 General Data Protection Law (LGPD)

- 5.13.2.5.2 Federal Law on Protection of Personal Data Held by Private Parties (LFPDPPP)

- 5.13.2.5.3 Personal Data Protection Law (PDPL)

- 5.13.2.1 North America

- 5.14 PATENT ANALYSIS

- 5.14.1 METHODOLOGY

- 5.14.2 PATENTS FILED, BY DOCUMENT TYPE

- 5.14.3 INNOVATION AND PATENT APPLICATIONS

- 5.15 PRICING ANALYSIS

- 5.15.1 AVERAGE SELLING PRICE OF OFFERING, BY KEY PLAYER, 2025

- 5.15.2 AVERAGE SELLING PRICE, BY APPLICATION, 2025

- 5.16 KEY CONFERENCES AND EVENTS

- 5.17 PORTER'S FIVE FORCES ANALYSIS

- 5.17.1 THREAT OF NEW ENTRANTS

- 5.17.2 THREAT OF SUBSTITUTES

- 5.17.3 BARGAINING POWER OF SUPPLIERS

- 5.17.4 BARGAINING POWER OF BUYERS

- 5.17.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.18 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.18.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.18.2 BUYING CRITERIA

- 5.19 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6 AI ASSISTANT MARKET, BY OFFERING (MARKET SIZE & FORECAST TO 2030 - IN VALUE (USD))

Detailed breakdown of market share and growth across AI Assistant Offerings

- 6.1 INTRODUCTION

- 6.1.1 DRIVERS: AI ASSISTANT MARKET, BY OFFERING

- 6.2 WRITING & CONTENT ASSISTANTS

- 6.2.1 EMPOWERING PROFESSIONAL WRITING WITH AI DRIVEN CONTENT ASSISTANTS

- 6.3 MEETING & COLLABORATION ASSISTANTS

- 6.3.1 ACCELERATING TEAM PRODUCTIVITY WITH AI POWERED MEETING ASSISTANTS

- 6.4 KNOWLEDGE & RESEARCH ASSISTANTS

- 6.4.1 UNLOCKING ENTERPRISE KNOWLEDGE WITH CONTEXTUAL AI RESEARCH ASSISTANTS

- 6.5 SCHEDULING & CALENDAR OPTIMIZATION ASSISTANTS

- 6.5.1 REVOLUTIONIZING TIME MANAGEMENT WITH SMART SCHEDULING ASSISTANTS

- 6.6 SALES & PROSPECTING ASSISTANTS

- 6.6.1 DRIVING REVENUE WITH AI ENHANCED SALES AND PROSPECTING ASSISTANTS

- 6.7 DEVELOPER PRODUCTIVITY ASSISTANTS

- 6.7.1 ACCELERATING CODE CREATION WITH AI POWERED DEVELOPER ASSISTANTS

- 6.8 PRESENTATION & DESIGN ASSISTANTS

- 6.8.1 CREATING VISUAL NARRATIVES WITH AI DRIVEN PRESENTATION ASSISTANTS

- 6.9 ANALYTICAL & SPREADSHEET ASSISTANTS

- 6.9.1 UNLOCKING DATA INSIGHTS WITH AI ENHANCED SPREADSHEET ASSISTANTS

7 AI ASSISTANT MARKET, BY INTEGRATION TYPE (MARKET SIZE & FORECAST TO 2030 - IN VALUE (USD))

Detailed breakdown of market share and growth across AI Assistant Integration Types

- 7.1 INTRODUCTION

- 7.1.1 DRIVERS: AI ASSISTANT MARKET, BY INTEGRATION TYPE

- 7.2 STANDALONE ASSISTANTS

- 7.2.1 STANDALONE ASSISTANTS DELIVER INDEPENDENT AI CAPABILITIES

- 7.3 SAAS-NATIVE ASSISTANTS

- 7.3.1 SAAS-NATIVE ASSISTANTS EMBED AI INTO CORE PLATFORMS

- 7.4 BROWSER EXTENSIONS/PLUG-INS

- 7.4.1 BROWSER EXTENSIONS AND PLUG INS ENHANCE IN APP ASSISTANCE

- 7.5 API-BASED ASSISTANTS

- 7.5.1 API BASED ASSISTANTS POWER CUSTOM INTEGRATIONS

- 7.6 WORKSPACE ADD-ONS

- 7.6.1 WORKSPACE ADD ONS UNITE COLLABORATION AND AI ASSISTANCE

8 AI ASSISTANT MARKET, BY APPLICATION (MARKET SIZE & FORECAST TO 2030 - IN VALUE (USD))

Detailed breakdown of market share and growth across AI Assistant Applications

- 8.1 INTRODUCTION

- 8.1.1 DRIVERS: AI ASSISTANT MARKET, BY APPLICATION

- 8.2 AI-POWERED WRITING & EDITING

- 8.2.1 CONTEXT MANAGEMENT TRACKS DOCUMENT HISTORY AND RECENT EDITS, AND HELPS MAINTAIN CONSISTENCY

- 8.3 MEETING TRANSCRIPTION & FOLLOW-UP

- 8.3.1 RETRIEVAL-AUGMENTED GENERATION ENSURES SUMMARIES REFERENCE RELEVANT DOCUMENTS, SLIDE DECKS, OR MEETING NOTES

- 8.4 KNOWLEDGE RETRIEVAL & DOCUMENT SEARCH

- 8.4.1 CONTEXT MANAGEMENT TRACKS INDIVIDUAL USER PROFILES AND PAST QUERIES, TAILORING RESULT RELEVANCE OVER TIME

- 8.5 SCHEDULING & WORK PRIORITIZATION

- 8.5.1 TRANSFORMING PASSIVE SCHEDULES INTO INTELLIGENT, SELF-OPTIMIZING AGENDAS

- 8.6 LEAD ENGAGEMENT & EMAIL SEQUENCING

- 8.6.1 FUNCTION-CALLING APIS AUTOMATE TASKS SUCH AS CREATING CALL ENTRIES, LOGGING MEETING OUTCOMES, OR SENDING CONTRACTS

- 8.7 CODE COMPLETION & REVIEW

- 8.7.1 DEVELOPERS RECEIVE UNIT-TEST SCAFFOLDING, PERFORMANCE OPTIMIZATION SUGGESTIONS, AND SECURITY VULNERABILITY ALERTS

- 8.8 PRESENTATION & NARRATIVE DESIGN

- 8.8.1 GENERATIVE VISION-LANGUAGE MODELS UNDERSTAND DESIGN PRINCIPLES, TYPOGRAPHY, LAYOUT, AND COLOR HARMONY

- 8.9 DATA EXPLORATION & SPREADSHEET AI

- 8.9.1 ASSISTANTS HELP GENERATE FORMULAS, PIVOT TABLES, OR CHARTS AUTOMATICALLY

- 8.10 OTHER APPLICATIONS

9 AI ASSISTANT MARKET, BY END USER (MARKET SIZE & FORECAST TO 2030 - IN VALUE (USD))

End user-specific market sizing, growth, and key trends

- 9.1 INTRODUCTION

- 9.1.1 DRIVERS: AI ASSISTANT MARKET, BY END USER

- 9.2 INDIVIDUAL END USERS

- 9.3 ENTERPRISES

- 9.3.1 BFSI

- 9.3.1.1 AI assistants automate workflows and improve compliance to modernize financial operations and customer engagement

- 9.3.2 TELECOMMUNICATIONS

- 9.3.2.1 AI assistants reduce service friction and enable personalized support across omnichannel telecom environments

- 9.3.3 GOVERNMENT & PUBLIC SECTOR

- 9.3.3.1 AI assistants enhance citizen service delivery and improve operational transparency across public sector functions

- 9.3.4 HEALTHCARE & LIFE SCIENCES

- 9.3.4.1 Intelligent assistants streamline clinical support and administrative tasks while ensuring patient-centric and secure operations

- 9.3.5 MANUFACTURING

- 9.3.5.1 AI assistants optimize frontline operations and decision-making across design, production, and maintenance workflows

- 9.3.6 MEDIA & ENTERTAINMENT

- 9.3.6.1 Content-focused AI assistants streamline creation, curation, and audience engagement across digital media workflows

- 9.3.7 RETAIL & E-COMMERCE

- 9.3.7.1 AI assistants personalize customer journeys and automate backend operations to drive digital retail transformation

- 9.3.8 TECHNOLOGY PROVIDERS

- 9.3.8.1 AI assistants accelerate innovation cycles and enhance product support across engineering and customer success teams

- 9.3.9 PROFESSIONAL SERVICE PROVIDERS

- 9.3.9.1 AI assistants enhance productivity and client service by automating documentation, research, and knowledge retrieval

- 9.3.10 EDUCATION

- 9.3.10.1 AI assistants support personalized learning, administrative automation, and faculty enablement in digital learning environments

- 9.3.11 OTHER ENTERPRISES

- 9.3.1 BFSI

10 AI ASSISTANT MARKET, BY REGION (MARKET SIZE & FORECAST TO 2030 - IN VALUE (USD))

Regional market sizing, forecasts, and regulatory landscapes

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 NORTH AMERICA: AI ASSISTANT MARKET DRIVERS

- 10.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 10.2.3 US

- 10.2.4 CANADA

- 10.3 EUROPE

- 10.3.1 EUROPE: AI ASSISTANT MARKET DRIVERS

- 10.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 10.3.3 UK

- 10.3.4 GERMANY

- 10.3.5 FRANCE

- 10.3.6 ITALY

- 10.3.7 SPAIN

- 10.3.8 NETHERLANDS

- 10.3.9 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 ASIA PACIFIC: AI ASSISTANT MARKET DRIVERS

- 10.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 10.4.3 CHINA

- 10.4.4 INDIA

- 10.4.5 JAPAN

- 10.4.6 SOUTH KOREA

- 10.4.7 SINGAPORE

- 10.4.8 AUSTRALIA & NEW ZEALAND

- 10.4.9 REST OF ASIA PACIFIC

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 MIDDLE EAST & AFRICA: AI ASSISTANT MARKET DRIVERS

- 10.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 10.5.3 SAUDI ARABIA

- 10.5.4 UAE

- 10.5.5 QATAR

- 10.5.6 TURKEY

- 10.5.7 SOUTH AFRICA

- 10.5.8 REST OF MIDDLE EAST & AFRICA

- 10.6 LATIN AMERICA

- 10.6.1 LATIN AMERICA: AI ASSISTANT MARKET DRIVERS

- 10.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 10.6.3 BRAZIL

- 10.6.4 MEXICO

- 10.6.5 ARGENTINA

- 10.6.6 REST OF LATIN AMERICA

11 COMPETITIVE LANDSCAPE

Strategic Profiles of Leading Players & Their Playbooks for Market Dominance

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 11.3 REVENUE ANALYSIS, 2020-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 BRAND/PRODUCT COMPARISON

- 11.5.1 PRODUCT COMPARATIVE ANALYSIS, BY WRITING & CONTENT ASSISTANT PROVIDERS

- 11.5.1.1 Grammarly (GrammarlyGO)

- 11.5.1.2 Notion (Notion AI)

- 11.5.1.3 Jasper (Jasper AI)

- 11.5.1.4 Copy.ai (Copy.ai Assistant)

- 11.5.1.5 QuillBot (QuillBot AI)

- 11.5.2 PRODUCT COMPARATIVE ANALYSIS, BY MEETING & COLLABORATION ASSISTANT PROVIDERS

- 11.5.2.1 Otter.ai (Otter Assistant)

- 11.5.2.2 Fireflies.ai (Fireflies AI Notetaker)

- 11.5.2.3 Zoom (Zoom AI Companion)

- 11.5.2.4 Fathom (Fathom AI Meeting Assistant)

- 11.5.2.5 Supernormal (Supernormal AI Notes)

- 11.5.2.6 Scribe AI (Scribe)

- 11.5.1 PRODUCT COMPARATIVE ANALYSIS, BY WRITING & CONTENT ASSISTANT PROVIDERS

- 11.6 COMPANY VALUATION AND FINANCIAL METRICS

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.7.5.1 Company footprint

- 11.7.5.2 Regional footprint

- 11.7.5.3 Offering footprint

- 11.7.5.4 Application footprint

- 11.7.5.5 End User Footprint

- 11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- 11.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.8.5.1 Detailed list of key startups/SMEs

- 11.8.5.2 Competitive benchmarking of key startups/SMEs

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES

- 11.9.2 DEALS

12 COMPANY PROFILES

In-depth look at their Strengths, Weaknesses, Product Portfolios, Recent Developments, and Strategic Moves

- 12.1 INTRODUCTION

- 12.2 KEY PLAYERS

- 12.2.1 MICROSOFT

- 12.2.1.1 Business overview

- 12.2.1.2 Products/Solutions/Services offered

- 12.2.1.3 Recent developments

- 12.2.1.3.1 Product launches

- 12.2.1.3.2 Deals

- 12.2.1.4 MnM view

- 12.2.1.4.1 Key strengths

- 12.2.1.4.2 Strategic choices

- 12.2.1.4.3 Weaknesses and competitive threats

- 12.2.2 SALESFORCE

- 12.2.2.1 Business overview

- 12.2.2.2 Products/Solutions/Services offered

- 12.2.2.3 Recent developments

- 12.2.2.3.1 Product launches

- 12.2.2.3.2 Deals

- 12.2.2.4 MnM view

- 12.2.2.4.1 Key strengths

- 12.2.2.4.2 Strategic choices

- 12.2.2.4.3 Weaknesses and competitive threats

- 12.2.3 GOOGLE

- 12.2.3.1 Business overview

- 12.2.3.2 Products/Solutions/Services offered

- 12.2.3.3 Recent developments

- 12.2.3.3.1 Product launches

- 12.2.3.3.2 Deals

- 12.2.3.4 MnM view

- 12.2.3.4.1 Key strengths

- 12.2.3.4.2 Strategic choices

- 12.2.3.4.3 Weaknesses and competitive threats

- 12.2.4 SAP

- 12.2.4.1 Business overview

- 12.2.4.2 Products/Solutions/Services offered

- 12.2.4.3 Recent developments

- 12.2.4.3.1 Product launches

- 12.2.4.3.2 Deals

- 12.2.4.4 MnM view

- 12.2.4.4.1 Key strengths

- 12.2.4.4.2 Strategic choices

- 12.2.4.4.3 Weaknesses and competitive threats

- 12.2.5 ORACLE

- 12.2.5.1 Business overview

- 12.2.5.2 Products/Solutions/Services offered

- 12.2.5.3 Recent developments

- 12.2.5.3.1 Product launches

- 12.2.5.3.2 Deals

- 12.2.5.4 MnM view

- 12.2.5.4.1 Key strengths

- 12.2.5.4.2 Strategic choices

- 12.2.5.4.3 Weaknesses and competitive threats

- 12.2.6 ADOBE

- 12.2.6.1 Business overview

- 12.2.6.2 Products/Solutions/Services offered

- 12.2.6.3 Recent developments

- 12.2.6.3.1 Product launches

- 12.2.6.3.2 Deals

- 12.2.7 AWS

- 12.2.7.1 Business overview

- 12.2.7.2 Products/Solutions/Services offered

- 12.2.7.3 Recent developments

- 12.2.7.3.1 Product launches

- 12.2.7.3.2 Deals

- 12.2.8 CISCO

- 12.2.8.1 Business overview

- 12.2.8.2 Products/Solutions/Services offered

- 12.2.8.3 Recent developments

- 12.2.8.3.1 Product launches

- 12.2.8.3.2 Deals

- 12.2.9 SERVICENOW

- 12.2.9.1 Business overview

- 12.2.9.2 Products/Solutions/Services offered

- 12.2.9.3 Recent developments

- 12.2.9.3.1 Product launches

- 12.2.9.3.2 Deals

- 12.2.10 DROPBOX

- 12.2.10.1 Business overview

- 12.2.10.2 Products/Solutions/Services offered

- 12.2.10.3 Recent developments

- 12.2.10.3.1 Product launches

- 12.2.10.3.2 Deals

- 12.2.11 ZOOM

- 12.2.12 BOX

- 12.2.13 ATLASSIAN

- 12.2.14 NOTION

- 12.2.15 ASANA

- 12.2.16 MONDAY.COM

- 12.2.17 CLICKUP

- 12.2.18 MIRO

- 12.2.19 GRAMMARLY

- 12.2.20 DOCUSIGN

- 12.2.21 LUCID SOFTWARE

- 12.2.22 GAMMA

- 12.2.23 CANVA

- 12.2.1 MICROSOFT

- 12.3 STARTUPS/SMES

- 12.3.1 GLEAN

- 12.3.2 OTTER.AI

- 12.3.3 FIREFLIES.AI

- 12.3.4 FATHOM

- 12.3.5 SCRIBE AI

- 12.3.6 TOME

- 12.3.7 JASPER

- 12.3.8 COPY.AI

- 12.3.9 WRITER.COM

- 12.3.10 SYNTHESIA

- 12.3.11 BEAUTIFUL.AI

- 12.3.12 HIVER

- 12.3.13 SUPERNORMAL

- 12.3.14 HYPERWRITE

- 12.3.15 QUILLBOT

- 12.3.16 COPYSMITH

- 12.3.17 ABRIDGE

- 12.3.18 DESCRIPT

- 12.3.19 LUMEN5

- 12.3.20 RUNWAY

- 12.3.21 PERPLEXITY AI

- 12.3.22 REGIE.AI

13 ADJACENT AND RELATED MARKETS

- 13.1 INTRODUCTION

- 13.2 AI AGENTS MARKET - GLOBAL FORECAST TO 2030

- 13.2.1 MARKET DEFINITION

- 13.2.2 MARKET OVERVIEW

- 13.2.2.1 AI agents market, by offering

- 13.2.2.2 AI agents market, by agent system

- 13.2.2.3 AI agents market, by product type

- 13.2.2.4 AI agents market, by agent role

- 13.2.2.5 AI agents market, by end user

- 13.2.2.6 AI agents market, by region

- 13.3 ARTIFICIAL INTELLIGENCE MARKET - GLOBAL FORECAST TO 2032

- 13.3.1 MARKET DEFINITION

- 13.3.2 MARKET OVERVIEW

- 13.3.2.1 Artificial intelligence (AI) market, by business function

- 13.3.2.2 Artificial intelligence (AI) market, by end user

- 13.3.2.3 Artificial intelligence (AI) market, by region

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS