|

시장보고서

상품코드

1800734

반도체용 화학제품 시장(-2030년) : 유형, 용도, 최종사용자, 지역별Semiconductor Chemicals Market by Type, Application, End Use, & Region - Global Forecast to 2030 |

||||||

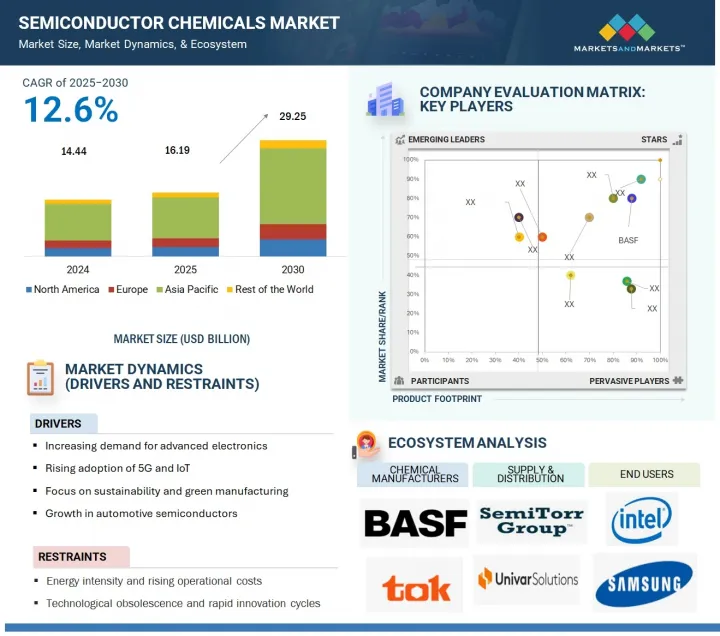

반도체용 화학제품 시장 규모는 2025년 161억 9,000만 달러에서 예측 기간중 CAGR 12.6%로 성장을 지속하여, 2030년에는 292억 5,000만 달러로 성장할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러), 킬로톤(KT) |

| 부문 | 유형, 최종사용자, 용도, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

세계 반도체용 화학물질 시장은 반도체 소자의 복잡성 증가와 고성능 전자제품에 대한 수요 증가에 힘입어 강력한 성장세를 보이고 있습니다. 반도체 약품에는 용매, 산, 염기, 포토레지스트, 도펀트, CMP 슬러리 등이 있으며, 포토리소그래피, 에칭, 증착, 세정 등 많은 제조 공정에서 중요한 역할을 합니다. 5G, AI, IoT, 전기자동차, 고성능 컴퓨팅 등 첨단 기술 및 반도체 관련 용도는 기하급수적으로 성장하고 있으며, 이러한 신기술은 보다 미세한 회로 설계와 고급 아키텍처를 갖춘 첨단 칩을 필요로 합니다. 이에 따라 초순도 및 용도에 특화된 화학 배합물에 대한 수요가 발생하고 있습니다.

CE 제품의 성장, 디지털 전환으로의 세계 전환, 반도체 제조에 대한 대규모 전략적 투자가 이 산업의 주요 원동력이 되고 있습니다. 대만, 한국, 중국, 미국 등 주요 국가들은 막대한 자본 투자와 대규모 공장 증설을 통해 반도체 기술 발전을 추진하고 있습니다. 또한, 극자외선(EUV) 리소그래피와 3D 패키징의 채택은 새롭고 혁신적인 첨단 화학 솔루션과 제품에 대한 수요를 증가시키고 있습니다. 운영비 상승과 원자재 공급의 제약 등의 문제에 직면하고 있지만, 반도체용 화학물질 시장의 세계 전망은 여전히 밝습니다.

"유형별로는 용제 부문이 예측 기간 동안 가장 큰 성장세를 보일 것으로 예측됩니다."

용매는 전체 반도체 제조 공정에서 중요한 역할과 광범위한 응용 분야로 인해 가장 큰 시장 점유율을 차지하고 있습니다. 용매는 반도체 재료의 다양한 하위 카테고리에서 널리 사용되며, 특히 이소프로파일 알코올(IPA), 아세톤, N-메틸-2-피롤리돈(NMP)과 같은 초순수 용매는 포토리소그래피, 웨이퍼 세정, 표면 처리와 같은 많은 반도체 분야에서 필수적인 요소입니다. 이러한 용매는 포토레지스트 및 기타 유기 잔류물, 입자 등의 오염물질을 제거하면서 복잡한 칩 구조를 손상시키거나 다른 화학물질로 인한 결함을 유발하지 않도록 하기 위해 필수적입니다. 반도체 소자가 5nm 이하로 미세화됨에 따라 극도로 깨끗한 표면을 유지하는 것이 점점 더 어려워지고 있으며, 높은 표면 청결도가 요구됨에 따라 용매 사용량이 증가하고 있습니다.

반도체 제조에 사용되는 재료 중 용매 사용량이 많은데, 이는 용매가 전 공정과 후공정 모두에서 재활용되어 사용되기 때문입니다. 용매는 품질 관리에서 중요한 역할을 수행하여 전체 제품이 표준을 충족하도록 보장하고 제조 공정의 운영 효율성을 향상시킵니다. 또한, 다양한 장비와 재료에 적합하다는 점도 용매가 널리 채택되는 요인입니다. 전자제품, 5G 기술, AI, 전기자동차에 대한 수요 증가로 반도체 산업이 지속적으로 확대됨에 따라 용매의 소비도 증가할 것으로 예측됩니다. 따라서, 용매는 반도체용 화학물질 중 가장 중요하고 신뢰할 수 있는 카테고리로 남아 있습니다.

"용도별로는 포토레지스트 부문이 예측 기간 동안 가장 큰 성장을 기록할 것으로 예측됩니다."

포토레지스트는 반도체 웨이퍼에 복잡한 회로 패턴을 전사하는 데 필수적인 포토리소그래피에서 중요한 역할을 하기 때문에 시장에서 가장 빠르게 성장하고 있는 분야입니다. 반도체 산업이 보다 복잡한 칩 아키텍처를 가진 미세 기술 노드로 확장됨에 따라 차세대 포토레지스트에 대한 수요와 요구가 증가하고 있습니다. 극자외선(EUV) 리소그래피와 같은 최근 기술의 발전으로 차세대 포토레지스트 재료에 대한 수요가 크게 증가하고 있습니다. 이러한 재료는 서브나노미터 제작에서 요구되는 정밀도를 달성하기 위해 필수적입니다. 각 웨이퍼는 수 차례의 포토리소그래피 과정을 거치며, 제조 공정에서 자주 사용되는 포토레지스트를 다량으로 소비합니다. 칩 제조업체들이 멀티패터닝 및 3D 집적 기술을 채택함에 따라 웨이퍼 당 포토레지스트 사용량도 비슷한 속도로 증가하고 있습니다. 또한, AI, 5G, 자동차 전장, 데이터센터에 사용되는 고성능 칩에 대한 수요가 증가함에 따라 비용 효율적이고 확장 가능하며 신뢰할 수 있는 포토리소그래피 재료에 대한 요구가 증가하고 있습니다. 새로운 반도체 제조 장비에 대한 투자와 연구개발 노력 증가는 특히 아시아태평양과 미국에서 포토레지스트 시장의 급격한 성장을 가속할 수 있는 좋은 위치에 있습니다.

"지역별로는 아시아태평양이 예측 기간 동안 가장 빠르게 성장할 것으로 예측됩니다."

아시아태평양은 세계 반도체 제조의 지배적 지위와 공급업체, 제조업체, 최종 사용자로 구성된 탄탄한 에코시스템의 존재로 인해 가장 규모가 큰 지역 점유율을 차지하고 있습니다. 대만, 한국, 중국, 중국, 일본 등에는 TSMC, Samsung Electronics, SK하이닉스, Toshiba 등 세계 최대 규모의 반도체 파운드리 및 통합 디바이스 제조업체가 존재합니다. 따라서 리소그래피, 에칭, 도핑, 도핑, 웨이퍼 세정 등 웨이퍼 가공에 사용되는 고순도 화학물질에 대한 수요가 매우 높습니다.

이 지역의 반도체 공급망은 잘 정비된 인프라, 고도로 숙련된 인력, 비용 효율적인 제조 시설, 전자 및 반도체 산업에 대한 정부의 강력한 지원으로 뒷받침되고 있습니다. 또한, 5G, IoT, AI, EV 등의 기술로 인해 반도체 수요가 증가하면서 관련 화학제품의 소비도 증가하고 있습니다. 중국은 반도체 공급망 자급자족을 목표로 하고 있으며, 정책적 지원과 현지 제조 및 재료 공급망에 대한 대규모 투자가 시장 성장을 더욱 가속화하고 있습니다. 한편, 일본과 한국은 소재 및 화학 산업에서 우위를 점하고 있으며, 첨단 혁신과 특수 반도체 등급 화학제품을 제공합니다.

세계의 반도체용 화학제품 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 반도체용 화학제품 시장 생성형 AI의 영향

제6장 업계 동향

- 고객 사업에 영향을 미치는 동향/혼란

- 2025년 미국 관세가 반도체용 화학제품 시장에 미치는 영향

- 공급망 분석

- 투자 및 자금조달 시나리오

- 가격 분석

- 생태계 분석

- 기술 분석

- 특허 분석

- 무역 분석

- 2025-2026년 주요 컨퍼런스 및 이벤트

- 관세 및 규제 상황

- Porter의 Five Forces 분석

- 주요 이해관계자와 구입 기준

- 거시경제 지표

- 사례 연구 분석

제7장 반도체용 화학제품 시장 : 유형별

- 고성능 폴리머

- 폴리이미드

- 불소 폴리머

- 폴리에테르에테르케톤

- LCD 폴리머

- 폴리페닐렌 술피드

- 기타

- 산 및 염기 화학제품

- 불화 수소

- 수산화칼륨

- 수산화나트륨

- 테트라 메틸 암모늄 수산화물

- 접착제

- 에폭시 접착제

- 실리콘 접착제

- UV 접착제

- 폴리이미드 접착제

- 용제

- 프로파일렌 글리콜 사물 메틸 에테르 아세테이트(PGMEA)

- 시클로헥사논

- 프로파일렌 글리콜 사물 메틸 에테르

- 트리크로로에틸렌

- 이소프로파일 알코올

- 황산

- 과산화수소

- 수산화 암모늄

- 염산

- 불화 수소산

- 초산

- 인산

- 기타

- 기타

- 가스

제8장 반도체용 화학제품 시장 : 용도별

- 포토레지스트

- 에칭

- 증착

- 클리닝

- 도핑

- 기타

- 화학적 기계적 평탄화

- 포장

제9장 반도체용 화학제품 시장 : 최종사용자별

- 집적회로(ICS)

- 디스크리트 반도체

- 센서

- 옵토일렉트로닉스

제10장 반도체용 화학제품 시장 : 지역별

- 아시아태평양

- 중국

- 일본

- 대만

- 한국

- 말레이시아

- 베트남

- 기타

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 네덜란드

- 아일랜드

- 영국

- 이스라엘

- 기타

- 기타 지역

- 브라질

- 남아프리카공화국

- 기타

제11장 경쟁 구도

- 주요 시장 진출기업의 전략/강점

- 시장 점유율 분석

- 매출 분석

- 브랜드/제품 비교

- 기업 평가 매트릭스 : 주요 기업

- 기업 평가 매트릭스 : 스타트업/중소기업

- 기업 평가와 재무 지표

- 경쟁 시나리오

제12장 기업 개요

- 주요 기업

- TOKYO OHKA KOGYO CO., LTD.

- JSR CORPORATION

- BASF

- SOLVAY

- DOW

- HONEYWELL INTERNATIONAL INC.

- FUJIFILM HOLDINGS CORPORATION

- EASTMAN CHEMICAL COMPANY

- MERCK KGAA(EMD ELECTRONICS)

- SUMITOMO CHEMICAL CO., LTD.

- SK INC.

- DUPONT

- 기타 기업

- RESONAC HOLDINGS CORPORATION

- MITSUBISHI CHEMICAL CORPORATION

- PARKER HANNIFIN CORP

- AVANTOR, INC.

- AIR PRODUCTS AND CHEMICALS, INC.

- LINDE PLC

- CABOT CORPORATION

- KAO CORPORATION

- KANTO KAGAKU.

- NIPPON KAYAKU CO., LTD.

- FOOSUNG CO., LTD.

- OCI COMPANY LTD.

- TOKUYAMA CORPORATION

제13장 부록

LSH 25.09.05The semiconductor chemicals market is projected to grow from USD 16.19 billion in 2025 to USD 29.25 billion by 2030, registering a CAGR of 12.6% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion) and Volume (Kiloton) |

| Segments | Type, End Use, Application, and Region |

| Regions covered | North America, Europe, Asia Pacific, and the Rest of the World |

The global semiconductor chemicals market is experiencing strong growth, supported by the growing complexity of semiconductor devices and a rising demand for high-performance electronic products. Semiconductor chemicals include solvents, acids, bases, photoresists, dopants, and CMP slurries, which are important in many fabrication processes such as photolithography, etching, deposition, and cleaning. In many advanced technologies and semiconductor-related applications, such as 5G, artificial intelligence (AI), Internet of Things (IoT), electric vehicles (EVs), and high-performance computing continue to grow exponentially, and these new technologies will require advanced chips with smaller geometries and sophisticated architectures, creating a demand for ultra-high-purity and application-specific chemical formulations.

The growth of consumer electronics, the global shift toward digital transformation, and significant strategic investments in semiconductor manufacturing are the key driving forces in the industry. Major players in this field include Taiwan, South Korea, China, and the US, all of which are making advancements in semiconductor technologies through substantial capital investments and extensive factory expansions. The adoption of extreme ultraviolet (EUV) lithography and 3D packaging is also boosting the demand for new, innovative, and advanced chemical solutions and products. Despite facing challenges such as rising operational costs and constraints in raw material supply, the global outlook for the semiconductor chemicals market remains positive.

"Solvents segment to register the fastest growth in the semiconductor chemicals market in terms of value during the forecast period"

Solvents hold the largest market share within the semiconductor chemicals sector, primarily due to their crucial role and extensive application throughout the semiconductor fabrication process. They are prevalent across various subcategories of semiconductor materials. Ultra-high purity solvents, such as isopropyl alcohol (IPA), acetone, and N-methyl-2-pyrrolidone (NMP), are especially vital for the semiconductor industry and its many subsegments, including photolithography, wafer cleaning, and surface preparation. These solvents are essential for removing photoresists and other organic residues, as well as contaminants like particles, while preventing any damage to the intricate chip structures or defects from other chemicals. As semiconductor devices shrink to sizes of 5nm or smaller, achieving and maintaining ultra-clean surfaces has become increasingly challenging. High surface cleanliness is crucial, which drives up the volume of solvent usage. The quantity of solvents employed is significant compared to other types of materials used in semiconductor fabrication because these solvents are typically recycled throughout the fabrication process for both the front-end and back-end stages. They play a vital role in quality control, ensuring the overall product meets standards, and in enhancing the operational efficiency of the manufacturing process. Moreover, the wide range of equipment and materials compatible with solvents contributes to their widespread adoption. As the semiconductor industry continues to expand in response to the growing demand for electronics, 5G technology, artificial intelligence (AI), and electric vehicles (EVs), the consumption of solvents is expected to rise. Therefore, solvents remain the most significant and reliable category within semiconductor chemicals.

"Photoresist segment to register the fastest growth in the semiconductor chemicals market during the forecast period"

Photoresist is the fastest-growing segment in the semiconductor chemicals market because it plays a crucial role in photolithography, the essential process of transferring intricate circuit patterns onto semiconductor wafers. As the semiconductor industry expands into smaller technology nodes (i.e., 5nm, 3nm, and below) with more complex chip architectures, the demand and requirements for next-generation photoresists have increased; specifically, the demand for improved resolution, sensitivity, and etch resistance. Recent advancements in technology, such as extreme ultraviolet (EUV) lithography, have significantly increased the demand for next-generation photoresist materials. These materials are essential for achieving the precision required in sub-nanometer fabrication. Each wafer undergoes several cycles of photolithography, which consume substantial quantities of photoresist used frequently throughout the manufacturing process. As chipmakers adopt multi-patterning and 3D integration technologies, the amount of photoresist used per wafer is rising at a similar pace. Furthermore, the growing demand for high-performance chips used in AI, 5G, automotive electronics, and data centers is intensifying the requirements for photolithographic materials that are cost-effective, scalable, and reliable. Investments in new semiconductor fabrication facilities, coupled with increased research and development efforts-especially in the Asia Pacific region and the US-are well-positioned to drive the rapid growth of the photoresist market.

"Asia Pacific is projected to be the fastest-growing region in the semiconductor chemicals market in terms of value during the forecast period"

The Asia Pacific region holds the largest share of the semiconductor chemicals market, largely due to its dominance in global semiconductor manufacturing and the presence of a well-established ecosystem of suppliers, manufacturers, and end users. Countries such as Taiwan, South Korea, China, and Japan are home to some of the world's largest semiconductor foundries and integrated device manufacturers, including TSMC, Samsung Electronics, SK Hynix, and Toshiba. This results in a high demand for high-purity chemicals used in wafer processing, including lithography, etching, doping, and wafer cleaning. The semiconductor supply chains in this region benefit from a well-developed infrastructure, a skilled labor force, cost-effective fabrication facilities, and strong government support for the electronics and semiconductor industries. Additionally, the increasing demand for semiconductors driven by technologies such as 5G, IoT, AI, and electric vehicles is pressuring end users to consume more associated chemicals. China's push for self-sufficiency in its semiconductor supply chains, supported by policy direction and significant investments in local fabrication and material supply chains, has further fueled market growth. Meanwhile, Japan and South Korea continue to excel in the materials and chemicals industry, offering advanced innovations and specialized semiconductor-grade chemicals.

In-depth interviews were conducted with chief executive officers (CEOs), marketing directors, other innovation and technology directors, and executives from various key organizations operating in the semiconductor chemicals market, and information was gathered from secondary research to determine and verify the market size of several segments.

- By Company Type: Tier 1 - 50%, Tier 2 - 30%, and Tier 3 - 20%

- By Designation: Managers- 15%, Directors - 20%, and Others - 65%

- By Region: North America - 20%, Europe - 30%, Asia Pacific - 40%, Middle East & Africa - 5%, and South America - 5%

The semiconductor chemicals market comprises major players such as Tokyo Ohka Kogyo Co., Ltd. (Japan), JSR Corporation (Japan), BASF (Germany), Solvay (Belgium), Dow (US), Honeywell International Inc. (US), FUJIFILM Holdings Corporation (Japan), Eastman Chemical Company (US), Merck KGaA (Germany), Sumitomo Chemical Co., Ltd. (Japan), SK Inc. (South Korea), and DuPont (US). The study includes an in-depth competitive analysis of these key players in the semiconductor chemicals market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This report segments the semiconductor chemicals market by type, application, end-user, and region and estimates its overall value across various regions. It has also conducted a detailed analysis of key industry players to provide insights into their business overviews, products and services, key strategies, and expansions associated with the Semiconductor chemicals market.

Key benefits of buying this report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape; emerging and high-growth segments of the semiconductor chemicals market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of drivers: (increasing demand for advanced electronics, focus on sustainability and green manufacturing, and rising adoption of IoT and 5G), restraints (energy intensity and rising operational costs), opportunities (development of specialty chemicals for quantum computing), and challenges (complexity of scaling production for emerging materials).

- Market Penetration: Comprehensive information on the semiconductor chemicals offered by top players in the semiconductor chemicals market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, product launches, expansions, investments, collaborations, partnerships, and announcements in the market.

- Market Development: The report provides comprehensive information about lucrative emerging markets and analyzes the semiconductor chemicals market across regions.

- Market Capacity: Wherever possible, the production capacities of companies producing semiconductor chemicals are provided, along with upcoming capacities for the semiconductor chemicals market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the semiconductor chemicals market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 RESEARCH LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Primary data sources

- 2.1.2.3 Key primary participants

- 2.1.2.4 Breakdown of interviews with experts

- 2.1.2.5 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 BASE NUMBER CALCULATION

- 2.2.1 SUPPLY-SIDE APPROACH

- 2.2.2 DEMAND-SIDE APPROACH

- 2.3 FORECAST NUMBER CALCULATION

- 2.3.1 SUPPLY SIDE

- 2.3.2 DEMAND SIDE

- 2.4 MARKET SIZE ESTIMATION

- 2.4.1 BOTTOM-UP APPROACH

- 2.4.2 TOP-DOWN APPROACH

- 2.5 DATA TRIANGULATION

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 GROWTH FORECAST

- 2.8 RISK ASSESSMENT

- 2.9 FACTOR ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SEMICONDUCTOR CHEMICALS MARKET

- 4.2 SEMICONDUCTOR CHEMICALS MARKET, BY TYPE

- 4.3 SEMICONDUCTOR CHEMICALS MARKET, BY APPLICATION

- 4.4 SEMICONDUCTOR CHEMICALS MARKET, BY END USE

- 4.5 SEMICONDUCTOR CHEMICALS MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increased demand for advanced electronics

- 5.2.1.2 Rising adoption of 5G and IoT technologies

- 5.2.1.3 Increasing focus on sustainability and green manufacturing

- 5.2.1.4 Shift toward autonomous driving

- 5.2.2 RESTRAINTS

- 5.2.2.1 Energy-intensive chemical production & fab operations and rising operational costs

- 5.2.2.2 Technological obsolescence and rapid innovation cycles

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Development of specialty chemicals for quantum computing

- 5.2.3.2 Increasing applications in medical and aerospace industries

- 5.2.4 CHALLENGES

- 5.2.4.1 Complexities in scaling production of emerging materials

- 5.2.1 DRIVERS

- 5.3 IMPACT OF GENERATIVE AI ON SEMICONDUCTOR CHEMICALS MARKET

- 5.3.1 INTRODUCTION

- 5.3.2 ACCELERATED R&D AND FORMULATION OF ADVANCED CHEMICALS

- 5.3.3 OPTIMIZATION OF PROCESS CHEMISTRY IN FABRICATION PLANTS

- 5.3.4 DIGITAL TWIN AND PREDICTIVE MAINTENANCE FOR CHEMICAL DELIVERY SYSTEMS

- 5.3.5 STREAMLINING SEMICONDUCTOR SUPPLY CHAIN AND INVENTORY MANAGEMENT

- 5.3.6 ENABLING SUSTAINABILITY AND GREEN CHEMISTRY IN SEMICONDUCTOR PROCESSING

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.3 IMPACT OF 2025 US TARIFFS ON SEMICONDUCTOR CHEMICALS MARKET

- 6.3.1 INTRODUCTION

- 6.3.2 KEY TARIFF RATES

- 6.3.3 PRICE IMPACT ANALYSIS

- 6.3.4 IMPACT ON KEY COUNTRIES/REGIONS

- 6.3.4.1 US

- 6.3.4.2 Europe

- 6.3.4.3 Asia Pacific

- 6.3.5 IMPACT ON END USE SEGMENTS

- 6.4 SUPPLY CHAIN ANALYSIS

- 6.5 INVESTMENT AND FUNDING SCENARIO

- 6.6 PRICING ANALYSIS

- 6.6.1 AVERAGE SELLING PRICE TREND, BY REGION, 2021-2024

- 6.6.2 AVERAGE SELLING PRICE TREND, BY TYPE, 2021-2024

- 6.6.3 AVERAGE SELLING PRICE TREND, BY APPLICATION, 2021-2024

- 6.6.4 AVERAGE SELLING PRICE TREND, BY END USE, 2021-2024

- 6.6.5 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY TYPE, 2024

- 6.7 ECOSYSTEM ANALYSIS

- 6.8 TECHNOLOGY ANALYSIS

- 6.8.1 KEY TECHNOLOGIES

- 6.8.2 COMPLEMENTARY TECHNOLOGIES

- 6.8.3 ADJACENT TECHNOLOGIES

- 6.9 PATENT ANALYSIS

- 6.9.1 METHODOLOGY

- 6.9.2 GRANTED PATENTS, 2015-2024

- 6.9.2.1 Publication trends

- 6.9.3 INSIGHTS

- 6.9.4 LEGAL STATUS

- 6.9.5 JURISDICTION ANALYSIS

- 6.9.6 TOP APPLICANTS

- 6.10 TRADE ANALYSIS

- 6.10.1 IMPORT SCENARIO (HS CODE 381800)

- 6.10.2 EXPORT SCENARIO (HS CODE 381800)

- 6.11 KEY CONFERENCES AND EVENTS, 2025-2026

- 6.12 TARIFF AND REGULATORY LANDSCAPE

- 6.12.1 TARIFF ANALYSIS RELATED TO SEMICONDUCTOR CHEMICALS

- 6.12.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.12.3 REGULATIONS AND STANDARDS RELATED TO SEMICONDUCTOR CHEMICALS

- 6.13 PORTER'S FIVE FORCES ANALYSIS

- 6.13.1 BARGAINING POWER OF SUPPLIERS

- 6.13.2 THREAT OF NEW ENTRANTS

- 6.13.3 THREAT OF SUBSTITUTES

- 6.13.4 BARGAINING POWER OF BUYERS

- 6.13.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.14 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.14.2 BUYING CRITERIA

- 6.15 MACROECONOMIC INDICATORS

- 6.15.1 GDP TRENDS AND FORECAST OF MAJOR ECONOMIES

- 6.16 CASE STUDY ANALYSIS

- 6.16.1 TRANSFORMING SUPPLY CHAIN RESILIENCE AT INFINEON TECHNOLOGIES

- 6.16.2 INNOVATING CHEMICAL EFFICIENCY AT BREWER SCIENCE

- 6.16.3 SCALING SUSTAINABILITY AT SHIN-ETSU CHEMICAL CO., LTD.

7 SEMICONDUCTOR CHEMICALS MARKET, BY TYPE

- 7.1 INTRODUCTION

- 7.2 HIGH-PERFORMANCE POLYMERS

- 7.2.1 POLYIMIDES

- 7.2.1.1 Exceptional dielectric properties and low thermal coefficient to drive market

- 7.2.2 FLUOROPOLYMERS

- 7.2.2.1 Efficient electric insulation to drive market

- 7.2.3 POLYETHER ETHER KETONES

- 7.2.3.1 Enhanced mechanical strength and stiffness to propel demand

- 7.2.4 LIQUID CRYSTAL POLYMERS

- 7.2.4.1 Resistance to temperature and chemicals to boost demand

- 7.2.5 POLYPHENYLENE SULFIDE

- 7.2.5.1 Excellent chemical resistance and thermal stability to drive market

- 7.2.6 OTHER HIGH-PERFORMANCE POLYMER TYPES

- 7.2.6.1 Polyetherimide

- 7.2.6.2 Polyethylene naphthalate

- 7.2.1 POLYIMIDES

- 7.3 ACID & BASE CHEMICALS

- 7.3.1 HYDROGEN FLUORIDE

- 7.3.1.1 High use in etching and cleaning applications to fuel market growth

- 7.3.2 POTASSIUM HYDROXIDE

- 7.3.2.1 Rising use in fabrication of precise patterns and wafer cleaning to drive market

- 7.3.3 SODIUM HYDROXIDE

- 7.3.3.1 Growing adoption in wafer cleaning to boost market

- 7.3.4 TETRAMETHYLAMMONIUM HYDROXIDE

- 7.3.4.1 Use as developer for positive photoresists to drive market

- 7.3.1 HYDROGEN FLUORIDE

- 7.4 ADHESIVES

- 7.4.1 EPOXY ADHESIVES

- 7.4.1.1 Mechanical resilience and adhesive properties to drive market

- 7.4.2 SILICONE ADHESIVES

- 7.4.2.1 Increasing use in sealing and bonding applications to fuel market growth

- 7.4.3 UV ADHESIVES

- 7.4.3.1 Fast curing properties to boost market growth

- 7.4.4 POLYIMIDE ADHESIVES

- 7.4.4.1 High-temperature resistance to boost market growth

- 7.4.1 EPOXY ADHESIVES

- 7.5 SOLVENTS

- 7.5.1 PROPYLENE GLYCOL MONOMETHYL ETHER ACETATE (PGMEA)

- 7.5.1.1 Wide use in manufacturing of cleaning agents to drive market

- 7.5.2 CYCLOHEXANONE

- 7.5.2.1 Fast evaporation rate and aromatic odor to fuel demand

- 7.5.3 PROPYLENE GLYCOL MONOMETHYL ETHER

- 7.5.3.1 Excellent solvency properties and rising application in formulation of photoresists to drive market

- 7.5.4 TRICHLOROETHYLENE

- 7.5.4.1 Light sensitivity and effective dissolving properties to drive market

- 7.5.5 ISOPROPYL ALCOHOL

- 7.5.5.1 Effective disinfectant properties to boost market

- 7.5.6 SULFURIC ACID

- 7.5.6.1 High applications in lead-acid batteries to drive market

- 7.5.7 HYDROGEN PEROXIDE

- 7.5.7.1 Excellent oxidative properties to drive market

- 7.5.8 AMMONIUM HYDROXIDE

- 7.5.8.1 Increased use in laboratories and chemical industries to drive market

- 7.5.9 HYDROCHLORIC ACID

- 7.5.9.1 Rising applications in photolithography to propel market

- 7.5.10 HYDROFLUORIC ACID

- 7.5.10.1 High corrosiveness and etching properties to drive demand

- 7.5.11 NITRIC ACID

- 7.5.11.1 Passivation of silicon wafers and chemical polishing to drive market

- 7.5.12 PHOSPHORIC ACID

- 7.5.12.1 Deoxidizing and etching properties to fuel market growth

- 7.5.13 OTHER SOLVENT TYPES

- 7.5.13.1 Acetone

- 7.5.13.2 Methanol

- 7.5.1 PROPYLENE GLYCOL MONOMETHYL ETHER ACETATE (PGMEA)

- 7.6 OTHER TYPES

- 7.6.1 GASES

- 7.6.1.1 Nitrogen

- 7.6.1.2 Oxygen

- 7.6.1.3 Argon

- 7.6.1.4 Hydrogen

- 7.6.1 GASES

8 SEMICONDUCTOR CHEMICALS MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 PHOTORESIST

- 8.2.1 RISING DEMAND FOR INTRICATE DESIGNS AND PATTERNS TO DRIVE MARKET

- 8.3 ETCHING

- 8.3.1 INCREASING DEMAND FOR PRECISE AND COMPLEX SEMICONDUCTOR DEVICE FABRICATION TO FUEL MARKET GROWTH

- 8.4 DEPOSITION

- 8.4.1 GROWING ADOPTION OF ADVANCED DEPOSITION CHEMICALS FOR THIN FILM FORMATION AND CIRCUIT LAYER DEVELOPMENT TO DRIVE MARKET

- 8.5 CLEANING

- 8.5.1 RISING COMPLEXITY OF SEMICONDUCTOR ARCHITECTURES AND DEMAND FOR ULTRA-PURE CLEANING CHEMICALS TO ENSURE DEFECT-FREE WAFER SURFACES DURING FABRICATION TO DRIVE MARKET

- 8.6 DOPING

- 8.6.1 GROWING NEED FOR ENHANCED ELECTRICAL PERFORMANCE IN SEMICONDUCTOR COMPONENTS TO ACCELERATE DEMAND

- 8.7 OTHER APPLICATIONS

- 8.7.1 CHEMICAL MECHANICAL PLANARIZATION

- 8.7.2 PACKAGING

9 SEMICONDUCTOR CHEMICALS MARKET, BY END USE

- 9.1 INTRODUCTION

- 9.2 INTEGRATED CIRCUITS (ICS)

- 9.2.1 RISING ADOPTION OF ADVANCED INTEGRATED CIRCUITS (ICS) IN CONSUMER ELECTRONICS, AUTOMOTIVE, AND COMMUNICATION DEVICE INDUSTRIES TO DRIVE DEMAND

- 9.2.1.1 Analog

- 9.2.1.2 Micro

- 9.2.1.3 Logic

- 9.2.1.4 Memory

- 9.2.1 RISING ADOPTION OF ADVANCED INTEGRATED CIRCUITS (ICS) IN CONSUMER ELECTRONICS, AUTOMOTIVE, AND COMMUNICATION DEVICE INDUSTRIES TO DRIVE DEMAND

- 9.3 DISCRETE SEMICONDUCTORS

- 9.3.1 GROWING DEMAND FOR SPECIALIZED ELECTRONIC COMPONENTS LIKE DIODES, TRANSISTORS, AND RECTIFIERS FOR PRECISE, SINGLE-FUNCTION APPLICATIONS IN ELECTRONIC SYSTEMS TO FUEL DEMAND

- 9.4 SENSORS

- 9.4.1 HIGH USE IN AUTOMOBILES AND MEDICAL DEVICES TO DRIVE MARKET

- 9.5 OPTOELECTRONICS

- 9.5.1 INCREASING DEMAND FOR OPTOELECTRONIC DEVICES TO DRIVE MARKET

10 SEMICONDUCTOR CHEMICALS MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 ASIA PACIFIC

- 10.2.1 CHINA

- 10.2.1.1 High government-led investments and "Made in China 2025" initiatives to drive production

- 10.2.2 JAPAN

- 10.2.2.1 Strategic government subsidies and focus on high-end materials like photoresists to fuel market growth

- 10.2.3 TAIWAN

- 10.2.3.1 Growth of Taiwan Semiconductor Manufacturing Company (TSMC) and government-led R&D investments to drive market

- 10.2.4 SOUTH KOREA

- 10.2.4.1 "K-Semiconductor Strategy" and surging demand for memory chips to propel market

- 10.2.5 MALAYSIA

- 10.2.5.1 Tax incentives and strategic location as Assembly, Testing, and Packaging (ATP) hub to boost market

- 10.2.6 VIETNAM

- 10.2.6.1 Rising foreign direct investments to drive market

- 10.2.7 REST OF ASIA PACIFIC

- 10.2.1 CHINA

- 10.3 NORTH AMERICA

- 10.3.1 US

- 10.3.1.1 High investment by CHIPS and Science Act and focus on domestic manufacturing to drive market

- 10.3.2 CANADA

- 10.3.2.1 Strategic partnerships and large presence of skilled workforce to propel market

- 10.3.3 MEXICO

- 10.3.3.1 Expanding automotive sector to fuel market growth

- 10.3.1 US

- 10.4 EUROPE

- 10.4.1 GERMANY

- 10.4.1.1 Government-led subsidies and Intel's massive fab investment to drive market

- 10.4.2 NETHERLANDS

- 10.4.2.1 ASML's R&D leadership and EU Chips Act to propel market

- 10.4.3 IRELAND

- 10.4.3.1 Multinational tech investments to drive market

- 10.4.4 UK

- 10.4.4.1 Government-led semiconductor strategy and focus on quantum computing to boost market

- 10.4.5 ISRAEL

- 10.4.5.1 Innovation-driven startups to accelerate demand

- 10.4.6 REST OF EUROPE

- 10.4.1 GERMANY

- 10.5 ROW

- 10.5.1 BRAZIL

- 10.5.1.1 Government-led investments and reopening of Ceitec to drive market

- 10.5.2 SOUTH AFRICA

- 10.5.2.1 Abundant mineral resources and surge in 5G adoption to drive market

- 10.5.3 OTHERS IN ROW

- 10.5.1 BRAZIL

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.3 MARKET SHARE ANALYSIS

- 11.4 REVENUE ANALYSIS

- 11.5 BRAND/PRODUCT COMPARISON

- 11.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.6.1 STARS

- 11.6.2 EMERGING LEADERS

- 11.6.3 PERVASIVE PLAYERS

- 11.6.4 PARTICIPANTS

- 11.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.6.5.1 Company footprint

- 11.6.5.2 Region footprint

- 11.6.5.3 Type footprint

- 11.6.5.4 End use footprint

- 11.6.5.5 Application footprint

- 11.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.7.1 PROGRESSIVE COMPANIES

- 11.7.2 RESPONSIVE COMPANIES

- 11.7.3 DYNAMIC COMPANIES

- 11.7.4 STARTING BLOCKS

- 11.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.7.5.1 Detailed list of key startups/SMEs

- 11.7.5.2 Competitive benchmarking of key startups/SMEs

- 11.8 COMPANY VALUATION AND FINANCIAL METRICS

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 DEALS

- 11.9.2 EXPANSIONS

- 11.9.3 OTHERS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 TOKYO OHKA KOGYO CO., LTD.

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Solutions/Services offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Deals

- 12.1.1.3.2 Expansions

- 12.1.1.4 MnM view

- 12.1.1.4.1 Key strengths/Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses/Competitive threats

- 12.1.2 JSR CORPORATION

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Solutions/Services offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Deals

- 12.1.2.3.2 Expansions

- 12.1.2.3.3 Others

- 12.1.2.4 MnM view

- 12.1.2.4.1 Key strengths/Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses/Competitive threats

- 12.1.3 BASF

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Solutions/Services offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Deals

- 12.1.3.3.2 Expansions

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths/Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses/Competitive threats

- 12.1.4 SOLVAY

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Solutions/Services offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches

- 12.1.4.3.2 Deals

- 12.1.4.3.3 Expansions

- 12.1.4.4 MnM view

- 12.1.4.4.1 Key strengths/Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses/Competitive threats

- 12.1.5 DOW

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Solutions/Services offered

- 12.1.5.3 MnM view

- 12.1.5.3.1 Key strengths/Right to win

- 12.1.5.3.2 Strategic choices

- 12.1.5.3.3 Weaknesses/Competitive threats

- 12.1.6 HONEYWELL INTERNATIONAL INC.

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Solutions/Services offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Deals

- 12.1.6.4 MnM view

- 12.1.6.4.1 Key strengths/Right to win

- 12.1.6.4.2 Strategic choices

- 12.1.6.4.3 Weaknesses/Competitive threats

- 12.1.7 FUJIFILM HOLDINGS CORPORATION

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Solutions/Services offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Deals

- 12.1.7.3.2 Expansions

- 12.1.7.4 MnM view

- 12.1.7.4.1 Key strengths/Right to win

- 12.1.7.4.2 Strategic choices

- 12.1.7.4.3 Weaknesses/Competitive threats

- 12.1.8 EASTMAN CHEMICAL COMPANY

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Solutions/Services offered

- 12.1.8.3 MnM view

- 12.1.8.3.1 Key strengths/Right to win

- 12.1.8.3.2 Strategic choices

- 12.1.8.3.3 Weaknesses/Competitive threats

- 12.1.9 MERCK KGAA (EMD ELECTRONICS)

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Solutions/Services offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Product launches

- 12.1.9.3.2 Deals

- 12.1.9.3.3 Expansions

- 12.1.9.4 MnM view

- 12.1.9.4.1 Key strengths/Right to win

- 12.1.9.4.2 Strategic choices

- 12.1.9.4.3 Weaknesses/Competitive threats

- 12.1.10 SUMITOMO CHEMICAL CO., LTD.

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Solutions/Services offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Deals

- 12.1.10.3.2 Expansions

- 12.1.10.4 MnM view

- 12.1.10.4.1 Key strengths/Right to win

- 12.1.10.4.2 Strategic choices

- 12.1.10.4.3 Weaknesses/Competitive threats

- 12.1.11 SK INC.

- 12.1.11.1 Business overview

- 12.1.11.2 Products/Solutions/Services offered

- 12.1.11.3 Recent developments

- 12.1.11.3.1 Deals

- 12.1.11.3.2 Others

- 12.1.11.4 MnM view

- 12.1.11.4.1 Key strengths/Right to win

- 12.1.11.4.2 Strategic choices

- 12.1.11.4.3 Weaknesses/Competitive threats

- 12.1.12 DUPONT

- 12.1.12.1 Business overview

- 12.1.12.2 Products/Solutions/Services offered

- 12.1.12.3 Recent developments

- 12.1.12.3.1 Deals

- 12.1.12.4 MnM view

- 12.1.12.4.1 Key strengths/Right to win

- 12.1.12.4.2 Strategic choices

- 12.1.12.4.3 Weaknesses/Competitive threats

- 12.1.1 TOKYO OHKA KOGYO CO., LTD.

- 12.2 OTHER PLAYERS

- 12.2.1 RESONAC HOLDINGS CORPORATION

- 12.2.2 MITSUBISHI CHEMICAL CORPORATION

- 12.2.3 PARKER HANNIFIN CORP

- 12.2.4 AVANTOR, INC.

- 12.2.5 AIR PRODUCTS AND CHEMICALS, INC.

- 12.2.6 LINDE PLC

- 12.2.7 CABOT CORPORATION

- 12.2.8 KAO CORPORATION

- 12.2.9 KANTO KAGAKU.

- 12.2.10 NIPPON KAYAKU CO., LTD.

- 12.2.11 FOOSUNG CO., LTD.

- 12.2.12 OCI COMPANY LTD.

- 12.2.13 TOKUYAMA CORPORATION

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS