|

시장보고서

상품코드

1801775

차량 서브스크립션 서비스 시장 예측(-2035년) : 지역별, 향후 동향, 가격 분석, 제품 상황, 소비자 분석, 경쟁 구도Vehicle Subscription Services Market by Region (Europe, Asia Pacific (excl. China), North America, and China), Future Trends, Pricing Analysis, Product Landscape, Consumer Analysis, and Competitive Landscape - Global Forecast to 2035 |

||||||

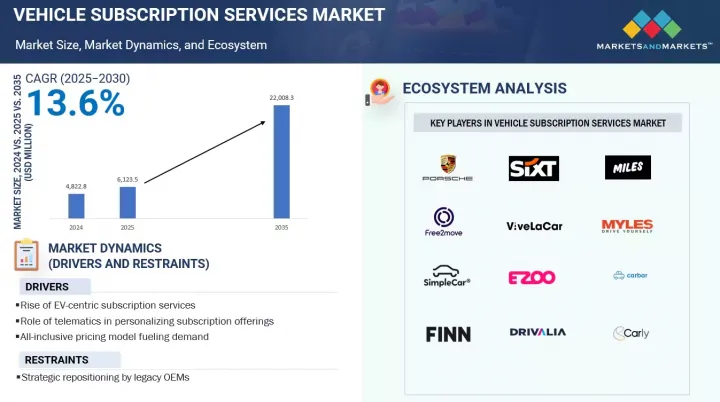

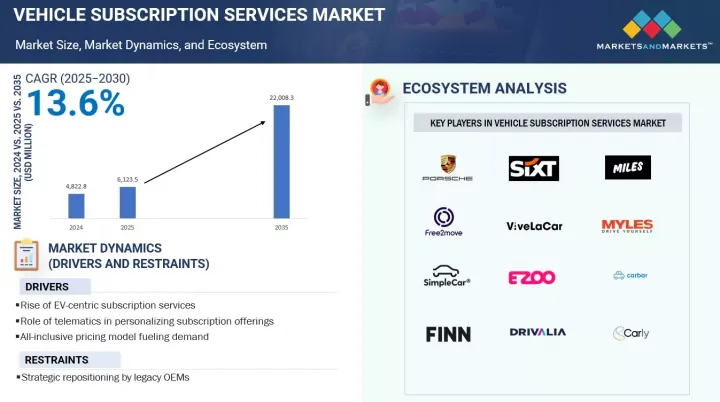

차량 서브스크립션 서비스 시장 규모는 2024년 48억 2,280만 달러에서 2035년에는 220억 830만 달러로 성장하며, CAGR은 13.6%에 달할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상연도 | 2024-2035년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2035년 |

| 검토 단위 | 금액(100만 달러) |

| 부문 | 차량 서브스크립션 서비스 시장(지역별, 북미, 중국), 향후 동향, 가격 분석, 제품 상황, 소비자 분석, 경쟁 구도 - 2035년까지 예측 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중국 |

도시화와 자동차 소유에 대한 규제 압력이 이 시장을 크게 견인하고 있습니다. 세계 각지의 도시에서는 보험, 유지보수, 수리 등의 비용과 연료 자동차에 대한 높은 세금으로 인해 자가용을 소유하고 운행하는 것이 어려워지고 있습니다. 그 결과, 특히 거대 도시에서는 도시 거주자들이 유연한 모빌리티 솔루션으로 이동하고 있습니다.

또한 차량 구독 서비스 증가는 전 세계 출장 증가, 하이브리드 근무 문화, 유연한 근무지 이동이 가속화되고 있습니다. 전문가들이 도시를 오가며 여러 지역에서 근무하는 경우가 많기 때문에 적응력이 뛰어나고 단기간에 높은 품질의 모빌리티 옵션에 대한 수요가 증가하고 있습니다. 유럽, 북미, 동남아시아 일부 지역에서는 현재 많은 회사원과 컨설턴트들이 장기 체류나 도시 간 출퇴근을 위해 렌터카나 택시보다 정액제 차량을 선호하고 있습니다. 개인화 및 차량 유연성이 부족한 렌터카 모델과 달리, 구독 서비스는 특히 월별 스왑 옵션을 통해 경제적 부담 없이 소유의 느낌을 제공합니다. 이러한 수요는 직원 복리후생 패키지의 일환으로 개인 및 업무용 차량을 포함한 차량 구독을 제공하는 기업에 의해 더욱 지원되고 있습니다.

차량 구독 서비스 프로바이더들은 각 사용자의 경험을 독특하게 만들고, 취향에 따라 맞춤화할 수 있는 개인화에 집중 투자하고 있습니다. 이 과정에서 텔레매틱스가 중요한 역할을 하고 있습니다. 운전 습관, 빈도, 주행 거리, 위치 데이터를 분석하여 플랫폼은 맞춤형 패키지, 업그레이드 옵션 또는 사용 기반 가격을 제공하여 소비자의 참여와 만족을 유지할 수 있습니다. 예를 들어 주행거리가 적은 도시 지역 운전자에게는 가끔씩 업그레이드 크레딧을 제공하는 소형 EV 플랜을 제공하고, 주말 여행자에게는 SUV와 할인된 가격으로 교환해주는 식입니다. 이러한 접근 방식은 일반적인 서비스를 판매하는 것이 아니라, 사용자가 이해받고 소중히 여겨지고 있다고 느끼게 함으로써 정서적 충성도를 구축하는 데 도움이 됩니다.

아시아태평양의 급속한 도시화와 메가시티의 성장은 자동차 소유보다 유연한 모빌리티 솔루션을 더욱 매력적으로 만들고 있습니다. 종종 방문 배송, 종합적인 가격 책정, 단기 계약을 포함한 구독 서비스는 바쁜 도시인의 라이프스타일에 적합합니다. 또한 스타트업 생태계의 확장과 벤처 캐피탈의 활동은 이 지역의 모빌리티 혁신에 박차를 가하고 있습니다. 투자자들은 디지털 결제, AI를 활용한 가격 책정, 앱 기반 차량 관리 등을 도입하여 빠르게 확장할 수 있는 에셋 라이트 모델에 자금을 지원하고 있습니다. 정부도 그린 모빌리티 구상의 일환으로 특히 전기자동차에 대한 구독 모델을 지원하기 시작했습니다. 더 많은 EV가 시장에 진입하고 사용자들이 구매 전 체험 옵션을 요구함에 따라 구독은 이상적인 솔루션을 제공합니다. 이러한 기술적 준비, 도시의 압력, 재정적 현실주의가 결합되어 아시아태평양은 자동차 구독 도입의 고성장 지역으로 자리매김하고 있습니다.

세계의 차량 서브스크립션 서비스 시장에 대해 조사했으며, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 개요

제2장 조사의 목적, 범위, 조사 방법

제3장 시장 개요

- 소유권 모델

- 시장의 진화

- 밸류체인 분석

- 서브스크립션 vs.리스 vs.구입

- 전략적 브랜딩

- 고객 분석

- 고객 유지 전략

- SaaS(Software as a Service)로의 이동

제4장 주요 동향

- EV 서브스크립션 서비스의 부상

- 텔레매틱스의 도입

- 파트너십을 통해 비즈니스 범위를 확대

제5장 지역 분석

- 유럽 : 차량 서브스크립션 서비스 상황

- 유럽 : 경쟁 지도제작

- 북미 : 차량 서브스크립션 서비스 상황

- 북미 : 경쟁 지도제작

- 아시아태평양(중국 제외) : 차량 서브스크립션 서비스 상황

- 중국 : 차량 서브스크립션 서비스 상황

- 아시아태평양(중국 제외) 및 중국 : 경쟁 지도제작

제6장 가격 분석

- 지역

- 서브스크립션 vs.리스 vs.구입

- ICE VS. EV 모델

제7장 기업 개요

- FINN

- AUTONOMY

- BIPI

- MYLES

- FREE2MOVE

제8장 과제

제9장 결론

제10장 부록

KSA 25.09.05The vehicle subscription services market is expected to grow from USD 4,822.8 million in 2024 to USD 22,008.3 million by 2035, with a CAGR of 13.6%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2035 |

| Base Year | 2024 |

| Forecast Period | 2025-2035 |

| Units Considered | Value (USD Million) |

| Segments | Vehicle Subscription Services Market by Region, North America, and China), Future Trends, Pricing Analysis, Product Landscape, Consumer Analysis, and Competitive Landscape - Global Forecast to 2035 |

| Regions covered | North America, Europe, Asia Pacific, and China |

Urbanization and regulatory pressures on vehicle ownership significantly drive this market. Cities worldwide are making it difficult to own and operate private vehicles through costs like insurance, maintenance, and repairs, along with high taxes on fuel-based vehicles. As a result, urban residents, especially in megacities, are shifting toward flexible mobility solutions.

Additionally, the rise in vehicle subscription services is fueled by a global increase in business travel, hybrid work culture, and relocation flexibility. With professionals often moving between cities or working from multiple locations, the demand for adaptable, short-term, high-quality mobility options has risen. In regions like Europe, North America, and parts of Southeast Asia, many corporate employees and consultants now prefer subscription vehicles over rentals or taxis for long-term stays or intercity commutes. Unlike car rental models that lack personalization or fleet flexibility, subscription services provide a sense of ownership without the financial burden, especially with monthly swap options. This demand is further supported by companies offering vehicle subscriptions as part of employee benefits packages, including cars for personal and professional use.

Key consumer retention strategies of vehicle subscription service providers

Vehicle subscription providers are heavily investing in personalization, making each user's experience unique and tailored to their preferences. Telematics plays a key role in this process. By analyzing driving habits, frequency, mileage, and location data, platforms can offer customized packages, upgrade options, or usage-based pricing that keeps consumers engaged and satisfied. For instance, a low-mileage urban driver could be offered a compact EV plan with occasional upgrade credits, while a weekend traveler might receive discounted SUV swaps. This approach helps build emotional loyalty by making users feel understood and cared for, rather than selling a generic service.

Asia Pacific witnesses significant growth in vehicle subscription services

Asia Pacific's rapid urbanization and the growth of megacities make flexible mobility solutions more attractive than car ownership. Subscription services, which often include door-to-door delivery, all-inclusive pricing, and short-term contracts, fit with the lifestyles of busy urban professionals. Additionally, the expanding startup ecosystem and venture capital activity in the region have spurred mobility innovation. Investors are funding asset-light models that scale quickly and incorporate digital payments, AI-driven pricing, and app-based fleet management. Governments are also beginning to support subscription models, especially for EVs, as part of their green mobility initiatives. As more EVs enter the market and users look for trial options before buying, subscriptions provide an ideal solution. This combination of technological readiness, urban pressure, and financial pragmatism positions Asia Pacific as a high-growth region for vehicle subscription adoption.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and strategy directors, and executives from various key organizations operating in this market.

- By Company Type: OEMs - 30%, Third-party Providers - 60%, and Vehicle Subscription Platform Providers - 10%

- By Designation: C-level - 40%, Directors - 40%, and Others - 20%

- By Region: North America - 21%, Europe - 50%, Asia Pacific - 10%, and China - 16%

Established players such as Miles Mobility (Germany), FINN (Germany), Autonomy (US), Free2Move (Germany), Myle (India), Drivalia (UK), REVV (India), LeasePlan (Germany), Mocean Subscription (Germany), and Ezoo (UK) lead the vehicle subscription services market.

Key Benefits of Buying this Report:

The report will assist market leaders and new entrants by providing information on the closest estimates. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and develop effective go-to-market strategies. Additionally, the report helps stakeholders grasp the market's pulse and offers information on key market drivers, restraints, and opportunities.

The report provides insights on the following pointers:

Analysis of key drivers (rapid urbanization and shift in lifestyle preferences), restraints (high operational complexity and margins dilution), and opportunities (shift from ownership to usership), influencing market growth

Product Development/Innovation: Detailed insights on upcoming technologies and new vehicle range & services of the vehicle subscription services market

Market Development: Comprehensive information about the lucrative market - the report analyzes the vehicle subscription services market across varied regions

Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the vehicle subscription services market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Miles Mobility, FINN, Autonomy, Free2Move, Myle, Drivalia, REVV, LeasePlan, Mocean Subscription, and Ezoo

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY

2 RESEARCH OBJECTIVES, SCOPE, AND METHODOLOGY

- 2.1 RESEARCH OBJECTIVES AND METHODOLOGY

- 2.2 RESEARCH SCOPE

3 MARKET OVERVIEW

- 3.1 OWNERSHIP MODEL

- 3.2 MARKET EVOLUTION

- 3.3 VALUE CHAIN ANALYSIS

- 3.4 SUBSCRIPTION VS. LEASE VS. PURCHASE

- 3.5 STRATEGIC BRANDING

- 3.6 CUSTOMER ANALYSIS

- 3.7 CUSTOMER RETENTION STRATEGIES

- 3.8 SHIFT TOWARD SOFTWARE-AS-A-SERVICE

4 KEY TRENDS

- 4.1 RISE OF EV SUBSCRIPTION SERVICES

- 4.2 ADOPTION OF TELEMATICS

- 4.3 EXPANDING BUSINESS REACH THROUGH PARTNERSHIPS

5 REGIONAL ANALYSIS

- 5.1 EUROPE: VEHICLE SUBSCRIPTION SERVICES LANDSCAPE

- 5.2 EUROPE: COMPETITIVE MAPPING

- 5.3 NORTH AMERICA: VEHICLE SUBSCRIPTION SERVICES LANDSCAPE

- 5.4 NORTH AMERICA: COMPETITIVE MAPPING

- 5.5 ASIA PACIFIC (EXCL. CHINA): VEHICLE SUBSCRIPTION SERVICES LANDSCAPE

- 5.6 CHINA: VEHICLE SUBSCRIPTION SERVICES LANDSCAPE

- 5.7 ASIA PACIFIC (EXCL. CHINA) AND CHINA: COMPETITIVE MAPPING

6 PRICING ANALYSIS

- 6.1 REGIONAL

- 6.2 SUBSCRIPTION VS. LEASE. VS. PURCHASE

- 6.3 ICE VS. EV MODEL

7 COMPANY PROFILES

- 7.1 FINN

- 7.2 AUTONOMY

- 7.3 BIPI

- 7.4 MYLES

- 7.5 FREE2MOVE