|

시장보고서

상품코드

1802921

의료기기 수탁제조 시장 예측(-2030년) : 기기 유형별, 기기 클래스별, 서비스별Medical Device Contract Manufacturing Market by Device Type (IVD, Cardiovascular, Orthopedic, Dental), Class of Device (Class I, II, III), Service (Device Development & Manufacturing, Packaging & Assembly, Quality Management) - Global Forecast to 2030 |

||||||

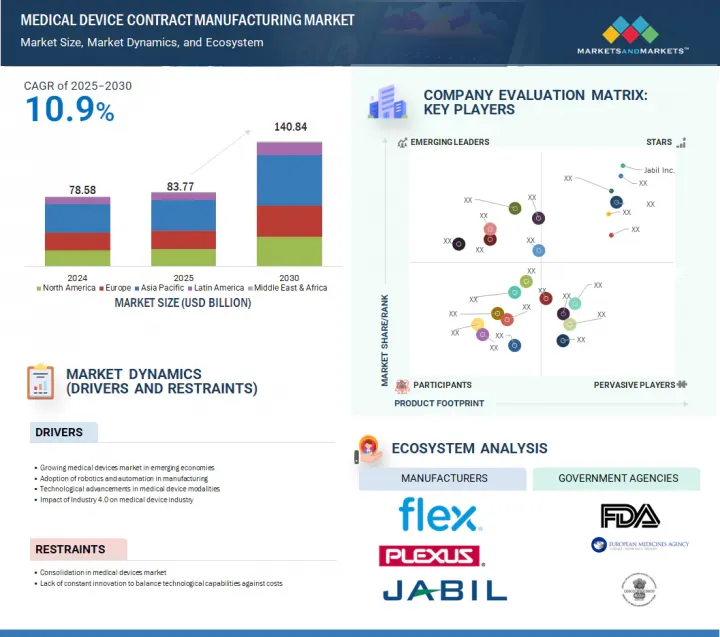

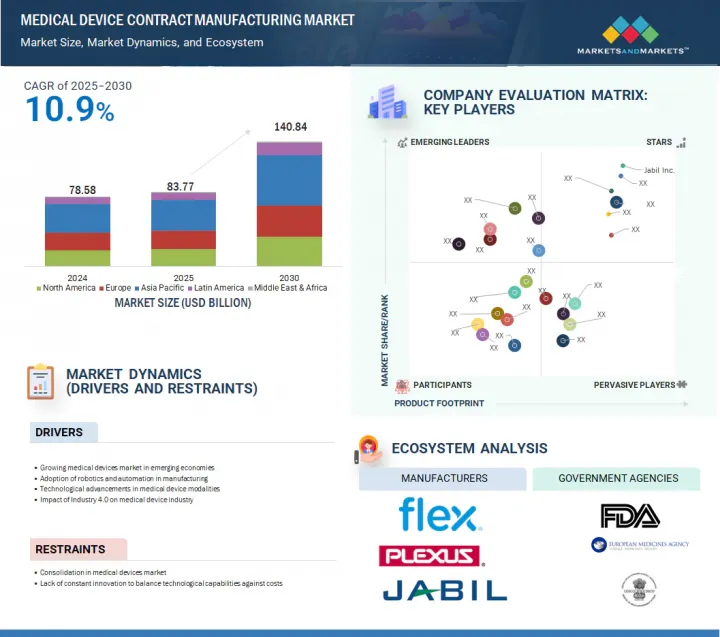

세계의 의료기기 수탁제조 시장 규모는 2025년 837억 7,000만 달러에서 2030년까지 1,408억 4,000만 달러에 달할 것으로 예측되며, 2025-2030년에 CAGR로 10.9%의 성장이 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상연도 | 2024-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 10억 달러 |

| 부문 | 기기 유형, 서비스 유형, 서비스 프로바이더, 계약 유형, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

의료기기 기술 발전과 노령 인구 증가가 시장을 촉진할 것으로 예측됩니다. 로봇공학, 최소침습수술, 의료기기의 AI, 원격의료, 원격 환자 모니터링 등 의료 분야의 지속적인 발전으로 시장 성장이 예상됩니다. 고령화로 인해 의료 진단에 대한 니즈가 증가하면서 시장 성장에 기여하고 있습니다. 그러나 엄격한 규제 준수와 공급망 관리의 복잡성이 시장 성장을 어느 정도 제한할 것으로 예측됩니다.

"기기 유형별로는 약물전달 장치 부문이 의료기기 수탁제조 시장에서 가장 높은 CAGR을 나타낼 것으로 예측됩니다. "

약물전달 장치 부문은 2025-2030년 의료기기 수탁제조 시장에서 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 이러한 성장의 주요 원인은 표적화되고 효율적인 환자 중심의 약물전달 시스템에 대한 수요 증가에 기인합니다. 당뇨병, 암, 호흡기 질환 등 만성질환의 유병률 증가로 인해 흡입기, 인슐린 펜, 자가주사기, 이식형 펌프 등의 기기 이용이 크게 증가하고 있습니다. 제약기업은 이러한 복잡하게 설계된 기기의 제조를 위탁 생산업체에 위탁하여 전문 기술력을 활용하여 생산비용을 최적화하는 경향이 증가하고 있습니다. 또한 생물제제의 발전과 맞춤형 의료로의 전환은 혁신적인 약물전달 메커니즘에 대한 수요를 촉진하여 예측 기간 중 이 부문의 성장을 강화할 것입니다.

"장비 개발 및 제조 서비스 부문이 2024년 서비스별 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. "

의료기기 개발 및 제조 서비스 부문은 주로 컨셉을 실행 가능한 의료기기로 전환하는 데 필수적인 역할을 수행하므로 의료기기 수탁제조 부문 중 가장 큰 시장 점유율을 차지하고 있습니다. 중소기업과 중견기업은 비용을 절감하고, 제품 생산 일정을 단축하고, 전문 지식과 첨단 제조 기술을 활용하기 위해 이러한 서비스를 아웃소싱하는 경우가 많습니다. 이 부문은 초기 설계 및 프로토타이핑부터 대규모 상품화까지 제품 개발의 전체 수명주기을 포괄하므로 스타트업과 기존 기업 모두에게 매우 중요한 부문입니다. 또한 저침습 수술 장비 및 웨어러블 건강 모니터링 기술과 같은 정교하고 정밀한 의료기기에 대한 수요가 증가함에 따라 종합적인 제조 파트너십에 대한 요구가 크게 증가하여 이 부문에서 시장에서의 우위를 확고히 하고 있습니다.

"아시아태평양이 2024년 가장 큰 시장 점유율을 차지했습니다. "

아시아태평양에서는 여러 요인으로 인해 의료기기 수탁제조 서비스에 대한 수요가 급증하고 있습니다. 첫째, 이 지역의 많은 국가에서 인구가 빠르게 증가함에 따라 첨단 의료 솔루션에 대한 수요가 증가하고 있습니다. 또한 최신 의료기기의 장점과 기능에 대한 의료진과 환자들의 인식이 높아지면서 수요를 더욱 촉진하고 있습니다. 또한 아시아태평양 국가들의 중산층이 확대되면서 의료 서비스 및 제품을 이용하는 소비자가 증가함에 따라 이러한 추세에 박차를 가하고 있습니다. 이러한 움직임의 결과, 의료기기 수탁제조 부문의 세계 리더들은 아시아태평양 시장에서 적극적으로 사업을 시작하고 확장하고 있습니다. 이들 기업은 최첨단 의료기기, 혁신적인 소프트웨어 솔루션, 다양한 의료 환경의 요구에 맞는 다양한 생체적합성 소재 등을 도입하고 있습니다. 특히 중국이 아시아태평양 의료기기 수탁제조 시장을 독점하고 있으며, 2024년에는 가장 큰 점유율을 차지할 것으로 예측되고 있습니다. 이러한 성장은 의료기기의 유용성과 효과에 대한 국민과 의료기관의 인식이 높아진 데다 국민들의 만성질환 유병률 증가에 따른 것으로 분석됩니다. 결과적으로 아시아태평양이 전체 시장에서 가장 큰 점유율을 차지하고 있으며, 이러한 상호 연관된 동향과 의료 환경의 지속적인 발전이 이를 촉진하는 요인으로 작용하고 있습니다.

세계의 의료기기 수탁제조 시장에 대해 조사분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 제공하고 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 중요 인사이트

- 의료기기 수탁제조 시장의 개요

- 아시아태평양의 의료기기 수탁제조 시장 : 용도별, 국가별

- 의료기기 수탁제조 시장 : 신규 경제권 시장 vs. 선진국 시장

- 의료기기 수탁제조 시장 : 지역적 성장 기회

- 의료기기 수탁제조 시장 : 지역의 구성

제5장 시장 개요

- 서론

- 시장 역학

- 촉진요인

- 억제요인

- 기회

- 과제

- 산업 동향

- OEM와 수탁제조업체의 통합 진행

- 의료기기 수탁제조에서 사모펀드 기업의 관심 증가

- 의료기기 수탁제조 서비스의 아웃소싱

- 인더스트리 5.0

- 기술 분석

- 주요 기술

- 인접 기술

- 보완 기술

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 규제 상황

- 규제 구조

- 규제기관, 정부기관, 기타 조직

- 가격결정 분석

- 평균 판매 가격 동향 : 주요 기업별(2022-2024년)

- 평균 판매 가격 동향 : 지역별(2022-2024년)

- 밸류체인 분석

- 주요 컨퍼런스와 이벤트(2025-2026년)

- 특허 분석

- 공급망 분석

- 에코시스템 분석

- 무역 분석

- HS 코드 9018의 수입 데이터(2020-2024년)

- HS 코드 9018의 수출 데이터(2020-2024년)

- 의료기기 수탁제조 인접 시장

- 의료기기 수탁제조 시장에서 미충족 요구/최종사용자 기대

- 의료기기 수탁제조 시장에서 생성형 AI의 영향

- 사례 연구 분석

- 사례 연구 1 : JABIL INC.와 HEARTWARE INTERNATIONAL이 제휴하여 첨단 심부전 치료를 개발

- 사례 연구 2 : FLEX LTD.와 MEDTRONIC가 차세대 인슐린 펌프의 개발을 위해 제휴

- 사례 연구 3 : PLEXUS, 스타트업과 제휴하여 혁신적인 인슐린 펌프를 개발

- 투자와 자금조달 시나리오

- 2025년 미국 관세의 영향 - 의료기기 수탁제조 시장

- 서론

- 주요 관세율

- 가격의 영향 분석

- 국가/지역에 대한 영향

- 최종 용도 산업에 대한 영향

제6장 의료기기 수탁제조 시장 : 기기별

- 서론

- 체외진단 기기

- 영상 진단 기기

- 심혈관기기

- 약물전달 디바이스

- 정형외과 기기

- 호흡 케어 기기

- 안과 기기

- 수술 기기

- 당뇨병 케어 기기

- 치과 기기

- 내시경·복강경 기기

- 부인과/비뇨기과 기기

- 퍼스널케어 기기

- 신경학 기기

- 환자 모니터링 기기

- 환자 보조 기기

- 기타 기기

제7장 의료기기 수탁제조 시장 : 기기 클래스별

- 서론

- 클래스 II 의료기기

- 클래스 I 의료기기

- 클래스 III 의료기기

제8장 의료기기 수탁제조 시장 : 서비스별

- 서론

- 기기 개발·제조 서비스

- 품질관리 서비스

- 포장·조립 서비스

- 기타 서비스

제9장 의료기기 수탁제조 시장 : 지역별

- 서론

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 중국

- 인도

- 일본

- 말레이시아

- 태국

- 한국

- 호주

- 필리핀

- 싱가포르

- 뉴질랜드

- 기타 아시아태평양

- 유럽

- 유럽의 거시경제 전망

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 라틴아메리카

- 라틴아메리카의 거시경제 전망

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 중동 및 아프리카의 거시경제 전망

- GCC 국가

- 기타 중동 및 아프리카

제10장 경쟁 구도

- 개요

- 매출 분석(2020-2024년)

- 시장 점유율 분석(2024년)

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업 평가 매트릭스, 스타트업/중소기업(2024년)

- 기업의 평가와 재무 지표

- 브랜드/제품 비교 분석

- 주요 기업의 R&D의 평가

- 경쟁 시나리오

제11장 기업 개요

- 주요 기업

- JABIL INC.

- FLEX LTD.

- PLEXUS CORP.

- SANMINA CORPORATION

- INTEGER HOLDINGS CORPORATION

- TE CONNECTIVITY LTD.

- NIPRO CORPORATION

- CELESTICA INC.

- WEST PHARMACEUTICAL SERVICES, INC.

- BENCHMARK ELECTRONICS INC.

- RECIPHARM AB

- GERRESHEIMER AG

- KIMBALL ELECTRONICS, INC.

- NORTECH SYSTEMS, INC.

- CARCLO PLC

- NOLATO GW, INC.(A PART OF NOLATO AB)

- 기타 기업

- NEMERA

- VIANT MEDICAL HOLDINGS, INC.

- TECOMET, INC.

- SMC LTD.

- PHILLIPS-MEDISIZE CORPORATION

- TESSY PLASTICS CORP.

- MEHOW

- TEKNI-PLEX

- PETER'S TECHNOLOGY

제12장 부록

KSA 25.09.08The global medical device contract manufacturing market is projected to reach USD 140.84 billion in 2030 from USD 83.77 billion in 2025, at a CAGR of 10.9% between 2025 and 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Device Type, Service Type, Service Provider, Contract Type, End User, and Region |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa |

Rising technological advancements in medical devices, along with an increasing geriatric population, are expected to drive the market. The market is anticipated to grow due to continuous developments in medical fields such as robotics and minimally invasive surgery, artificial intelligence (AI) in medical devices, telemedicine, and remote patient monitoring. The aging population with a rising need for medical diagnostics further contributes to market growth. However, strict regulatory compliance and complexities in supply chain management are expected to limit market growth to some extent.

"By device type, the drug delivery devices segment is expected to witness the highest CAGR in the medical device contract manufacturing market."

The drug delivery devices segment is anticipated to experience the highest CAGR in the medical device contract manufacturing market from 2025 to 2030. This growth is primarily driven by the escalating demand for targeted, efficient, and patient-centric drug delivery systems. The rising incidence of chronic conditions such as diabetes, cancer, and respiratory diseases has significantly increased the utilization of devices, including inhalers, insulin pens, auto-injectors, and implantable pumps. Pharmaceutical companies are increasingly outsourcing the manufacturing of these intricately designed devices to contract manufacturers, capitalizing on their specialized technical capabilities and optimizing production costs. Furthermore, the ongoing advancements in biologics and the shift toward personalized medicine are propelling the demand for innovative drug delivery mechanisms, thereby intensifying growth in this sector throughout the projected period.

"The device development & manufacturing services segment has accounted for the largest share in the market in 2024, by services."

The device development and manufacturing services segment commands the largest market share within the medical device contract manufacturing sector, primarily due to its integral role in transforming concepts into viable medical devices. Smaller enterprises and mid-sized firms often outsource these services to mitigate costs, accelerate their product timelines, and leverage specialized knowledge and advanced manufacturing techniques. This segment encompasses the entire lifecycle of product development, from initial design and prototyping to large-scale commercialization, rendering it crucial for both emerging and established companies. Furthermore, the escalating demand for sophisticated, high-precision medical instruments-such as minimally invasive surgical devices and wearable health monitoring technologies-has significantly heightened the need for comprehensive manufacturing partnerships, thereby solidifying the preeminence of this segment in the market.

"The Asia Pacific accounted for the largest market share in 2024."

The Asia Pacific (APAC) region is experiencing a significant surge in demand for medical device contract manufacturing services, driven by several key factors. Firstly, the rapid population growth in many countries within this region is creating an increased need for advanced medical solutions. Additionally, there is a growing awareness among healthcare providers and patients about the benefits and functionalities of modern medical devices, which further fuels this demand. The expanding middle class in various Asia Pacific nations is also contributing to this trend, as more consumers gain access to healthcare services and products. As a result of these dynamics, global leaders in the medical device contract manufacturing sector are actively establishing and expanding their operations in the Asia Pacific market. These companies are introducing a variety of cutting-edge medical devices, innovative software solutions, and a diverse range of biocompatible materials tailored to meet the needs of different healthcare settings. In particular, China is set to dominate the APAC medical device contract manufacturing market, and it is projected to capture the largest share in 2024. This growth can be attributed to the increasing prevalence of chronic diseases within the population, alongside greater public and institutional awareness regarding the availability and efficacy of medical devices. As a result, the overall market in the Asia Pacific region has accounted for the largest share in the market, driven by these interconnected trends and the continued evolution of the healthcare landscape.

A breakdown of the primary participants (supply-side) for the medical device contract manufacturing market referred to in this report is provided below:

- By Company Type: Tier 1-45%, Tier 2-20%, and Tier 3-35%

- By Designation: C-level Executives-35%, Directors-25%, and Others-40%

- By Region: North America-40%, Europe-25%, Asia Pacific-20%, Latin America- 10%, Middle East & Africa-5%.

The prominent players in the medical device contract manufacturing market include include Jabil Inc. (US), Flex Ltd. (Singapore), Plexus Corp. (US), Sanmina Corporation (US), Integer Holdings Corporation (US), TE Connectivity Ltd. (Switzerland), Nipro Corporation (Japan), Celestica Inc. (Canada), West Pharmaceutical Services, Inc. (US), Benchmark Electronics Inc. (US), Recipharm AB (Sweden), Gerresheimer AG (Germany), Kimball Electronics Inc. (US), Nortech Systems, Inc. (US), Carclo Plc (UK), Nolato GW, Inc. (US), and the other players are Nemera. (France), Viant Medical Holdings, Inc. (US), Tecomet, Inc. (US), SMC Ltd. (US), Phillips-Medisize Corporation (US), Tessy Plastics Corp. (US), MeHow (China), Tekni-Plex (US), and Peter's Technology (China).

Research Coverage:

The report examines the medical device contract manufacturing market and aims to estimate the market size and future growth potential across various segments, including device type, device class, service, and region. It also features a competitive analysis of major players in the market, highlighting their company profiles, product and service offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall medical device contract manufacturing market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (growth in medical devices market in developing countries, adoption of robotics and automation in manufacturing, technological advancements in medical device modalities, impact of industry 4.0 on the medical device industry), restraints (consolidation in medical devices market), opportunities (increasing healthcare expenditure, infrastructure, and awareness in developing economies, rising geriatric population and its associated diseases) and challenges (lack of constant innovation to balance technological capabilities against costs)

- Market Penetration: It includes extensive information on product portfolios offered by the major players in the global medical device contract manufacturing market. The report includes various segments in market device type, class of device, service, and region

- Product Enhancement/Innovation: Comprehensive details about new product launches and anticipated trends in the global medical device contract manufacturing market.

- Market Development: Thorough knowledge and analysis of the profitable rising markets by device type, class of device, service, and region

- Market Diversification: Comprehensive information about newly launched products and services, expanding markets, current advancements, and investments in the global medical device contract manufacturing market.

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings of products and services, and capacities of the major competitors in the global medical device contract manufacturing market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- 2.1.1 SECONDARY SOURCES

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY SOURCES

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.1 SECONDARY SOURCES

- 2.2 MARKET SIZE ESTIMATION

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.4 MARKET SHARE ESTIMATION

- 2.5 STUDY ASSUMPTIONS

- 2.6 RISK ASSESSMENT

- 2.7 LIMITATIONS

- 2.7.1 METHODOLOGY-RELATED LIMITATIONS

- 2.7.2 SCOPE-RELATED LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 MEDICAL DEVICE CONTRACT MANUFACTURING MARKET OVERVIEW

- 4.2 ASIA PACIFIC MEDICAL DEVICE CONTRACT MANUFACTURING MARKET, BY APPLICATION AND COUNTRY

- 4.3 MEDICAL DEVICE CONTRACT MANUFACTURING MARKET: EMERGING ECONOMIES VS. DEVELOPED MARKETS

- 4.4 MEDICAL DEVICE CONTRACT MANUFACTURING MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.5 MEDICAL DEVICE CONTRACT MANUFACTURING MARKET: REGIONAL MIX

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growing medical devices market in developing countries

- 5.2.1.2 Adoption of robotics and automation in manufacturing

- 5.2.1.3 Technological advancements in medical device modalities

- 5.2.1.4 Impact of industry 4.0 on medical device industry

- 5.2.2 RESTRAINTS

- 5.2.2.1 Consolidation in medical devices market

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing healthcare expenditure, infrastructure, and awareness in developing economies

- 5.2.3.2 Rising geriatric population and increasing incidence of associated diseases

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of constant innovation to balance technological capabilities against costs

- 5.2.1 DRIVERS

- 5.3 INDUSTRY TRENDS

- 5.3.1 INCREASING CONSOLIDATION OF OEMS AND CONTRACT MANUFACTURERS

- 5.3.2 GROWING INTEREST OF PRIVATE EQUITY FIRMS IN MEDICAL DEVICE CONTRACT MANUFACTURING

- 5.3.3 OUTSOURCING OF MEDICAL DEVICE CONTRACT MANUFACTURING SERVICES

- 5.3.4 INDUSTRY 5.0

- 5.4 TECHNOLOGY ANALYSIS

- 5.4.1 KEY TECHNOLOGIES

- 5.4.1.1 Digital transformation

- 5.4.1.2 Robotics and automation

- 5.4.2 ADJACENT TECHNOLOGIES

- 5.4.2.1 Artificial Intelligence

- 5.4.2.2 Big data

- 5.4.3 COMPLEMENTARY TECHNOLOGIES

- 5.4.3.1 5G

- 5.4.1 KEY TECHNOLOGIES

- 5.5 PORTER'S FIVE FORCES ANALYSIS

- 5.5.1 THREAT OF NEW ENTRANTS

- 5.5.2 THREAT OF SUBSTITUTES

- 5.5.3 BARGAINING POWER OF SUPPLIERS

- 5.5.4 BARGAINING POWER OF BUYERS

- 5.5.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.6 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.6.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.6.2 BUYING CRITERIA

- 5.7 REGULATORY LANDSCAPE

- 5.7.1 REGULATORY FRAMEWORK

- 5.7.1.1 North America

- 5.7.1.1.1 US

- 5.7.1.1.2 Canada

- 5.7.1.2 Europe

- 5.7.1.3 Asia Pacific

- 5.7.1.3.1 Japan

- 5.7.1.3.2 China

- 5.7.1.3.3 India

- 5.7.1.1 North America

- 5.7.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.7.1 REGULATORY FRAMEWORK

- 5.8 PRICING ANALYSIS

- 5.8.1 AVERAGE SELLING PRICE TREND, BY KEY PLAYER, 2022-2024

- 5.8.2 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2024

- 5.9 VALUE CHAIN ANALYSIS

- 5.10 KEY CONFERENCES AND EVENTS IN 2025-2026

- 5.11 PATENT ANALYSIS

- 5.11.1 LIST OF MAJOR PATENTS, 2022-2025

- 5.12 SUPPLY CHAIN ANALYSIS

- 5.13 ECOSYSTEM ANALYSIS

- 5.14 TRADE ANALYSIS

- 5.14.1 IMPORT DATA FOR HS CODE 9018, 2020-2024

- 5.14.2 EXPORT DATA FOR HS CODE 9018, 2020-2024

- 5.15 ADJACENT MARKETS FOR MEDICAL DEVICE CONTRACT MANUFACTURING

- 5.16 UNMET NEEDS/END-USER EXPECTATIONS IN MEDICAL DEVICE CONTRACT MANUFACTURING MARKET

- 5.17 IMPACT OF GEN AI IN MEDICAL DEVICE CONTRACT MANUFACTURING MARKET

- 5.18 CASE STUDY ANALYSIS

- 5.18.1 CASE STUDY 1: JABIL INC. AND HEARTWARE INTERNATIONAL PARTNER TO DEVELOP ADVANCED HEART FAILURE TREATMENT

- 5.18.2 CASE STUDY 2: FLEX LTD. AND MEDTRONIC COLLABORATE TO DEVELOP THE NEXT-GENERATION INSULIN PUMP

- 5.18.3 CASE STUDY 3: PLEXUS PARTNERED WITH A START-UP TO DEVELOP A REVOLUTIONARY INSULIN PUMP

- 5.19 INVESTMENT AND FUNDING SCENARIO

- 5.20 IMPACT OF 2025 US TARIFFS-MEDICAL DEVICE CONTRACT MANUFACTURING MARKET

- 5.20.1 INTRODUCTION

- 5.20.2 KEY TARIFF RATES

- 5.20.3 PRICE IMPACT ANALYSIS

- 5.20.4 IMPACT ON COUNTRIES/REGIONS

- 5.20.4.1 US

- 5.20.4.2 Europe

- 5.20.4.3 APAC

- 5.20.5 IMPACT ON END-USE INDUSTRIES

- 5.20.5.1 Diagnostic & Imaging Equipment

- 5.20.5.2 Surgical Instruments & Implants

- 5.20.5.3 Point-of-Care & Diagnostic Kits

6 MEDICAL DEVICE CONTRACT MANUFACTURING MARKET, BY DEVICE

- 6.1 INTRODUCTION

- 6.2 IVD DEVICES

- 6.2.1 IVD CONSUMABLES

- 6.2.1.1 Increasing demand for reagents & kits to drive market

- 6.2.2 IVD EQUIPMENT

- 6.2.2.1 Advances in life sciences research to support market

- 6.2.1 IVD CONSUMABLES

- 6.3 DIAGNOSTIC IMAGING DEVICES

- 6.3.1 ADOPTION OF NEW AND ADVANCED DIAGNOSTIC IMAGING SYSTEMS IN DEVELOPING COUNTRIES TO AUGMENT MARKET

- 6.4 CARDIOVASCULAR DEVICES

- 6.4.1 RISING PREVALENCE OF CVDS TO PROPEL MARKET

- 6.5 DRUG DELIVERY DEVICES

- 6.5.1 INFUSION DEVICES & ADMINISTRATION SETS

- 6.5.1.1 Rising incidence of chronic diseases and number of surgical procedures to fuel market

- 6.5.2 SYRINGES

- 6.5.2.1 High cost of safety syringes and increasing incidence of needlestick injuries to hinder market

- 6.5.3 INHALERS

- 6.5.3.1 High prevalence of asthma, COPD, and cystic fibrosis to aid market growth

- 6.5.4 AUTOINJECTORS

- 6.5.4.1 Rising number of regulatory approvals for new drug therapies and advancements to drive market

- 6.5.5 PEN INJECTORS

- 6.5.5.1 Rising prevalence of chronic diseases and growing pipeline of biologics and biosimilars to boost market growth

- 6.5.6 OTHER DRUG DELIVERY DEVICES

- 6.5.1 INFUSION DEVICES & ADMINISTRATION SETS

- 6.6 ORTHOPEDIC DEVICES

- 6.6.1 HIGH PREVALENCE OF ORTHOPEDIC CONDITIONS TO DRIVE MARKET

- 6.7 RESPIRATORY CARE DEVICES

- 6.7.1 GROWING PREVALENCE OF RESPIRATORY INFECTIONS TO DRIVE MARKET

- 6.8 OPHTHALMOLOGY DEVICES

- 6.8.1 INCREASING PREVALENCE OF OPHTHALMIC DISEASES TO DRIVE MARKET

- 6.9 SURGICAL DEVICES

- 6.9.1 INCREASE IN SURGICAL PROCEDURES TO FUEL MARKET

- 6.10 DIABETES CARE DEVICES

- 6.10.1 RISING PREVALENCE OF DIABETES TO PROPEL MARKET

- 6.11 DENTAL DEVICES

- 6.11.1 RISING INCIDENCE OF DENTAL DISEASES TO DRIVE MARKET

- 6.12 ENDOSCOPY & LAPAROSCOPY DEVICES

- 6.12.1 RISING PATIENT PREFERENCE FOR MINIMALLY INVASIVE PROCEDURES TO AUGMENT MARKET

- 6.13 GYNECOLOGY/UROLOGY DEVICES

- 6.13.1 GROWING AWARENESS AND PREVENTIVE CHECK-UPS FOR LATE-PHASE DIAGNOSIS OF STDS TO PROPEL MARKET

- 6.14 PERSONAL CARE DEVICES

- 6.14.1 SHIFT IN CONSUMPTION PATTERN TOWARD PREMIUM PERSONAL CARE PRODUCTS TO FUEL MARKET

- 6.15 NEUROLOGY DEVICES

- 6.15.1 RISING GLOBAL BURDEN OF NEUROLOGICAL DISEASES TO DRIVE MARKET

- 6.16 PATIENT MONITORING DEVICES

- 6.16.1 GROWING AVAILABILITY OF INTEGRATED MONITORING TECHNOLOGY TO AID MARKET

- 6.17 PATIENT ASSISTIVE DEVICES

- 6.17.1 RISING GERIATRIC POPULATION TO PROPEL MARKET

- 6.18 OTHER DEVICES

7 MEDICAL DEVICE CONTRACT MANUFACTURING MARKET, BY DEVICE CLASS

- 7.1 INTRODUCTION

- 7.2 CLASS II MEDICAL DEVICES

- 7.2.1 HIGH-VOLUME UTILIZATION OF CLASS II MEDICAL DEVICES TO SUPPORT MARKET

- 7.3 CLASS I MEDICAL DEVICES

- 7.3.1 CLASS I DEVICES HOLD LARGEST SHARE OF ALL APPROVED MEDICAL DEVICES

- 7.4 CLASS III MEDICAL DEVICES

- 7.4.1 HIGHEST LEVEL OF HEALTH RISKS NECESSITATES STRINGENT OVERSIGHT

8 MEDICAL DEVICE CONTRACT MANUFACTURING MARKET, BY SERVICE

- 8.1 INTRODUCTION

- 8.2 DEVICE DEVELOPMENT & MANUFACTURING SERVICES

- 8.2.1 DEVICE & COMPONENT MANUFACTURING SERVICES

- 8.2.1.1 New aspects, such as robotics and personalized medicine, to necessitate specialized device manufacturing capabilities

- 8.2.2 PROCESS DEVELOPMENT SERVICES

- 8.2.2.1 Increased R&D spending and innovation and growing demand for complex products to drive market

- 8.2.3 DEVICE ENGINEERING SERVICES

- 8.2.3.1 Complexity of device engineering services to propel segment

- 8.2.1 DEVICE & COMPONENT MANUFACTURING SERVICES

- 8.3 QUALITY MANAGEMENT SERVICES

- 8.3.1 PACKAGING VALIDATION SERVICES

- 8.3.1.1 Increasing product safety concerns for medical devices to aid market

- 8.3.2 INSPECTION & TESTING SERVICES

- 8.3.2.1 Availability of technological expertise in testing services to eliminate large capital and overhead investments

- 8.3.3 STERILIZATION SERVICES

- 8.3.3.1 Rising complexity of sterility standards to augment market

- 8.3.1 PACKAGING VALIDATION SERVICES

- 8.4 PACKAGING & ASSEMBLY SERVICES

- 8.4.1 PRIMARY & SECONDARY PACKAGING SERVICES

- 8.4.1.1 Growing concerns for patient safety to aid segment

- 8.4.2 LABELING SERVICES

- 8.4.2.1 Export bans and product recalls due to improper labeling to support market

- 8.4.3 OTHER PACKAGING & ASSEMBLY SERVICES

- 8.4.1 PRIMARY & SECONDARY PACKAGING SERVICES

- 8.5 OTHER SERVICES

9 MEDICAL DEVICE CONTRACT MANUFACTURING MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 ASIA PACIFIC

- 9.2.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 9.2.2 CHINA

- 9.2.2.1 Low labor costs and rapidly changing healthcare infrastructure to drive market

- 9.2.3 INDIA

- 9.2.3.1 Rising contract manufacturing capabilities to support market growth

- 9.2.4 JAPAN

- 9.2.4.1 Universal healthcare reimbursement policies to propel market

- 9.2.5 MALAYSIA

- 9.2.5.1 Increasing R&D activities and investments by established players to augment market growth

- 9.2.6 THAILAND

- 9.2.6.1 Government-supported industrial clustering and export competitiveness to propel market

- 9.2.7 SOUTH KOREA

- 9.2.7.1 High-value imports from other countries to offer growth opportunities

- 9.2.8 AUSTRALIA

- 9.2.8.1 Government-backed investment in sovereign capability to drive medtech manufacturing growth

- 9.2.9 PHILIPPINES

- 9.2.9.1 Skilled labor force and IT-enabled support to drive market growth

- 9.2.10 SINGAPORE

- 9.2.10.1 Strong government support and global investments to drive market

- 9.2.11 NEW ZEALAND

- 9.2.11.1 Deregulation of therapeutic products unlocking expedited access and export potential

- 9.2.12 REST OF ASIA PACIFIC

- 9.3 EUROPE

- 9.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 9.3.2 GERMANY

- 9.3.2.1 Presence of major device manufacturers and high healthcare expenditure to support market growth

- 9.3.3 UK

- 9.3.3.1 Rising number of accredited clinical laboratories and hospital laboratories to propel market

- 9.3.4 FRANCE

- 9.3.4.1 Increasing government pressure for healthcare cost reduction and budgetary constraints to support market growth

- 9.3.5 SPAIN

- 9.3.5.1 Increasing adoption of home-based medical devices to drive market

- 9.3.6 ITALY

- 9.3.6.1 Healthcare coverage for all citizens and foreign residents to increase demand for medical devices

- 9.3.7 REST OF EUROPE

- 9.4 NORTH AMERICA

- 9.4.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 9.4.2 US

- 9.4.2.1 Presence of stringent government regulations to drive market

- 9.4.3 CANADA

- 9.4.3.1 Strong presence of key contract manufacturing companies to augment market

- 9.5 LATIN AMERICA

- 9.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 9.5.2 BRAZIL

- 9.5.2.1 Favorable government initiatives and willingness to pay for better healthcare to boost market

- 9.5.3 MEXICO

- 9.5.3.1 Proximity to US and other LATAM countries to strengthen Mexico's relevance as a contract manufacturing hub

- 9.5.4 REST OF LATIN AMERICA

- 9.6 MIDDLE EAST & AFRICA

- 9.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 9.6.2 GCC COUNTRIES

- 9.6.2.1 Increasing healthcare infrastructure development to support market growth

- 9.6.2.2 Kingdom of Saudi Arabia (KSA)

- 9.6.2.2.1 Focus on healthcare localization and Vision 2030 to drive investment

- 9.6.2.3 United Arab Emirates (UAE)

- 9.6.2.3.1 Advanced infrastructure and regulatory efficiency to attract global medtech contract manufacturers

- 9.6.2.4 Rest of GCC Countries

- 9.6.3 REST OF MIDDLE EAST AND AFRICA

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.1.1 KEY STRATEGIES ADOPTED BY PLAYERS IN MEDICAL DEVICE CONTRACT MANUFACTURING MARKET

- 10.2 REVENUE ANALYSIS, 2020-2024

- 10.3 MARKET SHARE ANALYSIS, 2024

- 10.4 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.4.1 STARS

- 10.4.2 EMERGING LEADERS

- 10.4.3 PERVASIVE PLAYERS

- 10.4.4 PARTICIPANTS

- 10.4.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.4.5.1 Company footprint

- 10.4.5.2 Region footprint

- 10.4.5.3 Device footprint

- 10.4.5.4 Device class footprint

- 10.4.5.5 Service footprint

- 10.5 COMPANY EVALUATION MATRIX, STARTUPS/SMES, 2024

- 10.5.1 PROGRESSIVE COMPANIES

- 10.5.2 RESPONSIVE COMPANIES

- 10.5.3 DYNAMIC COMPANIES

- 10.5.4 STARTING BLOCKS

- 10.5.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 10.5.5.1 Detailed list of key startups/SMEs

- 10.5.5.2 Competitive benchmarking of key startups/SMEs

- 10.6 COMPANY VALUATION & FINANCIAL METRICS

- 10.6.1 FINANCIAL METRICS

- 10.6.2 COMPANY VALUATION

- 10.7 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 10.8 R&D ASSESSMENT OF KEY PLAYERS

- 10.9 COMPETITIVE SCENARIO

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 JABIL INC.

- 11.1.1.1 Business overview

- 11.1.1.2 Products/Services/Solutions offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Product approvals

- 11.1.1.3.2 Deals

- 11.1.1.4 MnM view

- 11.1.1.4.1 Right to win

- 11.1.1.4.2 Strategic choices made

- 11.1.1.4.3 Weaknesses and competitive threats

- 11.1.2 FLEX LTD.

- 11.1.2.1 Business overview

- 11.1.2.2 Products/Services/Solutions offered

- 11.1.2.3 Recent developments

- 11.1.2.3.1 Deals

- 11.1.2.4 Expansions

- 11.1.2.5 MnM view

- 11.1.2.5.1 Right to win

- 11.1.2.5.2 Strategic choices made

- 11.1.2.5.3 Weaknesses and competitive threats

- 11.1.3 PLEXUS CORP.

- 11.1.3.1 Business overview

- 11.1.3.2 Products/Services/Solutions offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Expansions

- 11.1.3.4 MnM view

- 11.1.3.4.1 Right to win

- 11.1.3.4.2 Strategic choices made

- 11.1.3.4.3 Weaknesses and competitive threats

- 11.1.4 SANMINA CORPORATION

- 11.1.4.1 Business overview

- 11.1.4.2 Products/Services/Solutions offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Deals

- 11.1.4.4 MnM view

- 11.1.4.4.1 Right to win

- 11.1.4.4.2 Strategic choices made

- 11.1.4.4.3 Weaknesses and competitive threats

- 11.1.5 INTEGER HOLDINGS CORPORATION

- 11.1.5.1 Business overview

- 11.1.5.2 Products/Services/Solutions offered

- 11.1.5.3 Recent developments

- 11.1.5.4 Deals

- 11.1.5.5 MnM view

- 11.1.5.5.1 Right to win

- 11.1.5.5.2 Strategic choices made

- 11.1.5.5.3 Weaknesses and competitive threats

- 11.1.6 TE CONNECTIVITY LTD.

- 11.1.6.1 Business overview

- 11.1.6.2 Products/Services/Solutions offered

- 11.1.6.3 Recent developments

- 11.1.6.3.1 Product launches

- 11.1.6.4 Deals

- 11.1.7 NIPRO CORPORATION

- 11.1.7.1 Business overview

- 11.1.7.2 Products/Services/Solutions offered

- 11.1.7.3 Recent developments

- 11.1.7.3.1 Expansions

- 11.1.8 CELESTICA INC.

- 11.1.8.1 Business overview

- 11.1.8.2 Products/Services/Solutions offered

- 11.1.8.3 Recent developments

- 11.1.8.3.1 Expansions

- 11.1.8.3.2 Other developments

- 11.1.9 WEST PHARMACEUTICAL SERVICES, INC.

- 11.1.9.1 Business overview

- 11.1.9.2 Products/Services/Solutions offered

- 11.1.9.3 Recent developments

- 11.1.9.3.1 Product launches

- 11.1.9.3.2 Deals

- 11.1.10 BENCHMARK ELECTRONICS INC.

- 11.1.10.1 Business overview

- 11.1.10.2 Products/Services/Solutions offered

- 11.1.10.3 Recent developments

- 11.1.10.3.1 Deals

- 11.1.10.3.2 Expansions

- 11.1.11 RECIPHARM AB

- 11.1.11.1 Business overview

- 11.1.11.2 Products/Services/Solutions offered

- 11.1.11.3 Recent developments

- 11.1.11.3.1 Deals

- 11.1.11.4 Other developments

- 11.1.12 GERRESHEIMER AG

- 11.1.12.1 Business overview

- 11.1.12.2 Products/Services/Solutions offered

- 11.1.12.3 Recent developments

- 11.1.12.3.1 Deals

- 11.1.13 KIMBALL ELECTRONICS, INC.

- 11.1.13.1 Business overview

- 11.1.13.2 Products/Services/Solutions offered

- 11.1.14 NORTECH SYSTEMS, INC.

- 11.1.14.1 Business overview

- 11.1.14.2 Products/Services/Solutions offered

- 11.1.14.3 Recent developments

- 11.1.14.3.1 Product approvals

- 11.1.15 CARCLO PLC

- 11.1.15.1 Business overview

- 11.1.15.2 Products/Services/Solutions offered

- 11.1.16 NOLATO GW, INC. (A PART OF NOLATO AB)

- 11.1.16.1 Business overview

- 11.1.16.2 Products/Services/Solutions offered

- 11.1.16.3 Recent developments

- 11.1.16.3.1 Deals

- 11.1.1 JABIL INC.

- 11.2 OTHER PLAYERS

- 11.2.1 NEMERA

- 11.2.2 VIANT MEDICAL HOLDINGS, INC.

- 11.2.3 TECOMET, INC.

- 11.2.4 SMC LTD.

- 11.2.5 PHILLIPS-MEDISIZE CORPORATION

- 11.2.6 TESSY PLASTICS CORP.

- 11.2.7 MEHOW

- 11.2.8 TEKNI-PLEX

- 11.2.9 PETER'S TECHNOLOGY

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS