|

시장보고서

상품코드

1802922

건식 변압기 시장 예측(-2030년) : 기술별, 전압별, 상별, 용도별, 지역별Dry Type Transformer Market by Technology (Cast Resin, Vacuum Pressure Impregnated), Voltage (Low (<1 kV), Medium (1-6 kV), High (Above 36 kV)), Phase (Single, Three), Application (Industrial, Commercial, Utility) and Region - Global Forecast to 2030 |

||||||

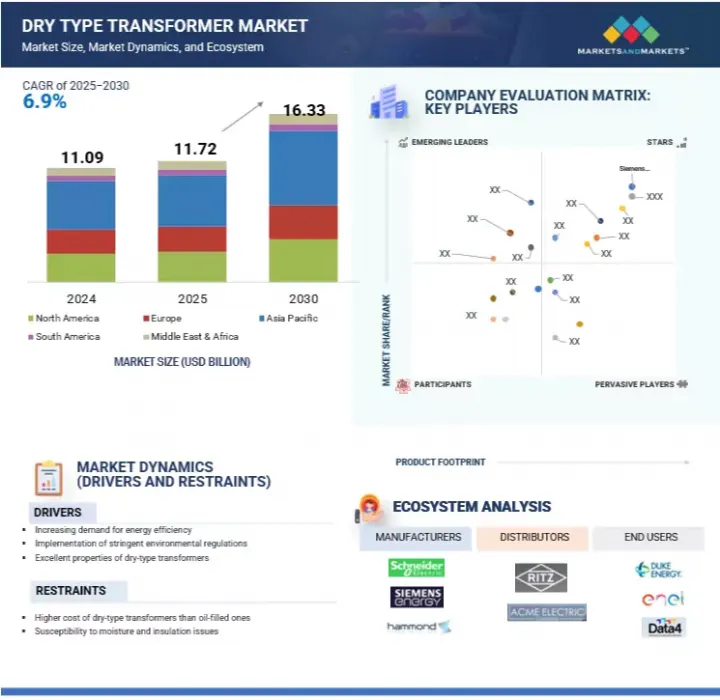

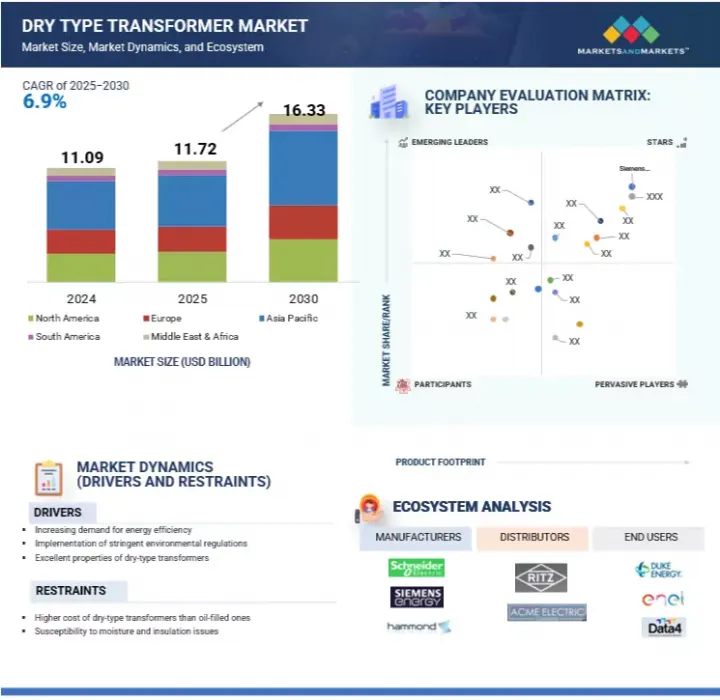

세계의 건식 변압기 시장 규모는 2025년 117억 2,000만 달러에서 2030년에는 163억 3,000만 달러로 성장하며, CAGR은 6.9%에 달할 것으로 예측됩니다.

이러한 성장의 원동력은 스마트 그리드로의 전환과 에너지 시스템의 분산화에 따라 탄력적이고 안전하며 유지보수가 용이한 전기 인프라에 대한 수요가 증가하고 있기 때문입니다. 전력회사가 시스템의 신뢰성과 자산 수명 향상을 목표로 하는 가운데, 건식 변압기에 내장된 예지보전 전략으로 전환이 진행되고 있습니다. 도시 건물, 산업 플랜트, 데이터센터, 재생에너지 시스템, EV 충전 네트워크에서 일반적으로 사용되는 이 변압기에는 현재 실시간 상태 모니터링 및 고장 예측을 가능하게 하는 센서, 통신 모듈, IoT 기반 진단 기능이 탑재되어 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상연도 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 대수 | 금액(100만 달러) 및 수량(대) |

| 부문별 | 기술별, 전압별, 상별, 용도별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미 |

또한 재생에너지의 통합이 증가하고 부하 조건이 변동함에 따라 변압기는 동적 열 및 전기적 스트레스를 관리해야 합니다. 아크 고장 감지, 과부하 보호, 원격 제어 기능을 갖춘 고급 건식 변압기 설계는 그리드 유연성과 신속한 고장 복구를 지원합니다. 그 결과, 유틸리티 및 상업용 사용자들은 그리드 복원력을 높이고, 유지보수 비용을 절감하며, 최신 안전 및 효율성 표준을 충족하기 위해 자동화 지원 센서가 장착된 건식 변압기에 대한 투자를 늘리고 있으며, 예측 유지보수를 건식 변압기 시장 성장의 주요 동력으로 확고히 하고 있습니다. 시장 성장의 주요 촉진요인으로 확고히 하고 있습니다.

예측 기간 중 건식 변압기 시장에서는 산업용, 상업용, 유틸리티 배전망에 널리 사용되는 중전압 부문이 전압별로 가장 큰 비중을 차지할 것으로 예측됩니다. 일반적으로 1kV에서 36kV 사이에서 작동하는 중전압 건식 변압기는 제조 공장, 데이터센터, 병원, 교육 기관, 교통 허브, 재생에너지 시스템 등의 시설에서 고압 송전 전력을 사용 가능한 수준으로 낮추는 데 필수적입니다.

컴팩트한 폼팩터, 화재 안전 특성, 유지보수가 필요 없는 작동은 특히 실내 및 인구 밀집 지역에 적합하며, 오일 기반 대체품의 화재 및 환경 위험이 높은 실내 및 인구 밀집 지역에 적합합니다. 또한 스마트 시티, 전기자동차 충전 인프라, 분산형 재생에너지원의 통합을 향한 전 세계적인 추세는 변동 부하를 관리하고 안정적이고 신뢰할 수 있는 전력 공급을 보장할 수 있는 고성능, 자동화 지원 중전압 변압기에 대한 수요를 가속화하고 있습니다.

예측 기간 중 진공 압력 함침(VPI) 부문은 우수한 기계적 강도, 내습성 및 열 성능으로 인해 건식 변압기 시장에서 가장 높은 CAGR을 나타낼 것으로 예측됩니다. VPI 변압기는 진공 가압 하에서 권선에 특수 배합된 바니시를 함침시켜 제조되어 절연성과 내구성을 높입니다. 이러한 특성으로 인해 화학 플랜트, 광산 작업, 해양 용도, 운송 인프라 등 먼지와 습기, 기계적 스트레스에 자주 노출되는 가혹한 산업 환경에 매우 적합합니다. 특히 중공업의 성장과 전력망 신뢰성에 중점을 둔 지역에서 가혹한 운전 조건에서 견고하고 오래 지속되는 전력 솔루션에 대한 수요가 증가함에 따라 VPI 기술 채택이 가속화되고 있습니다. 또한 VPI 공정은 열 방출을 개선하여 운전 효율과 장비 수명 연장에 기여합니다. 이러한 요소들은 예측 유지보수 및 수명주기 비용 최적화를 중시하는 전력회사의 태도와 일치합니다.

예측 기간 중 아시아태평양은 급속한 도시화, 가속화되는 시장 개발, 인프라 및 재생에너지에 대한 대규모 투자에 힘입어 건식 변압기 시장이 가장 빠르게 성장할 것으로 예측됩니다. 중국, 인도, 일본, 한국, 동남아시아 등의 국가에서는 제조 거점 확대, 인구 증가, 전기자동차 및 스마트 시티 프로젝트 도입 확대로 전력 수요가 급증하고 있습니다. 이 때문에 특히 기존의 오일이 들어있는 유닛이 적합하지 않은 도시 지역이나 환경에 민감한 지역에서는 안전하고 컴팩트한 내화 변압기의 도입이 증가하고 있습니다. 또한 지역 정부는 전력망 현대화, 농촌 전기화, 분산형 에너지 자원의 통합을 추진하고 있으며, 중전압, 저보수 건식 변압기에 대한 수요가 더욱 증가하고 있습니다. 아시아태평양은 또한 강력한 국내 제조거점과 에너지 효율을 개선하고 이산화탄소 배출량을 줄이기 위한 지원 정책의 혜택을 누리고 있습니다. 이 지역은 탄력적이고 지속가능한 에너지 인프라 구축에 지속적으로 집중하고 있으며, IoT 기반 모니터링, 예지보전, 친환경 절연 등의 기능을 갖춘 첨단 건식 변압기에 대한 수요가 크게 확대될 것으로 예측됩니다.

건식 변압기 시장을 독점하고 있는 것은 광범위한 지역적 입지를 가진 소수의 대형 기업입니다. 주요 진출 기업은 Siemens Energy(독일), Schneider Electric(프랑스), Eaton(아일랜드), Toshiba Corporation(일본), General Electric(미국), Hammond Power Solutions(캐나다), Hitachi(일본) 등입니다. 캐나다), Hitachi(일본)입니다.

건식 변압기 시장을 기술별(주조 수지, 진공 가압 함침(VPI)), 전압별(저압(1kV 미만), 중압(1-36kV), 고압(36kV 이상)), 상별(단상, 삼상), 용도별(산업용, 상업용, 유틸리티용, 기타 용도), 지역별로 정의-설명-예측했습니다. 또한 시장의 상세한 질적, 양적 분석을 실시했습니다. 주요 시장 성장 촉진요인, 억제요인, 기회 및 과제를 종합적으로 검토하고 있습니다. 또한 시장의 여러 가지 중요한 측면에 대해서도 다루고 있습니다. 건식 변압기 시장의 주요 업체를 종합적으로 분석합니다. 이 분석을 통해 각 기업의 사업 개요, 솔루션 및 서비스, 주요 전략에 대한 인사이트를 얻을 수 있습니다. 또한 신제품 출시, 합병, 인수, 합병, 인수, 기타 시장의 최근 동향과 함께 관련 계약, 파트너십, 협정 등에 대해서도 다루고 있습니다. 또한 건식 변압기 생태계내 스타트업의 경쟁 분석도 함께 수록되어 있습니다.

이 보고서는 업계 리더와 신규 시장 진출기업을 위한 전략적 자료로, 시장과 그 하위 부문에 대한 종합적인 분석을 제공합니다. 경쟁 구도를 완전히 이해함으로써 이해관계자들은 비즈니스 포지셔닝을 개선하고 효과적인 시장 진출 전략을 수립할 수 있습니다. 또한 이 보고서는 현재 시장 역학에 대한 이해를 돕고, 전략적 의사결정에 도움이 되는 중요한 촉진요인, 억제요인, 과제 및 기회를 파악할 수 있도록 돕습니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

- 서론

- 시장 역학

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 에코시스템 분석

- 공급망 분석

- 기술 분석

- 규제 상황

- 무역 분석

- 2025-2026년의 주요 컨퍼런스와 이벤트

- 특허 분석

- 가격 분석

- 사례 연구 분석

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 건식 변압기 시장에서 GEN AI/AI의 영향

- 2025년 미국 관세가 건식 변압기 시장에 미치는 영향

제6장 건식 변압기 시장(기술별)

- 서론

- 캐스트 레진

- 진공 가압 함침(VPI)

제7장 건식 변압기 시장(전압별)

- 서론

- 저전압

- 중전압

- 고전압

제8장 건식 변압기 시장(상별)

- 서론

- 단상

- 삼상

제9장 건식 변압기 시장(용도별)

- 서론

- 산업

- 상업

- 유틸리티

- 기타

제10장 건식 변압기 시장(지역별)

- 서론

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타

- 북미

- 미국

- 캐나다

- 멕시코

- 중동 및 아프리카

- GCC

- 남아프리카공화국

- 기타

- 남미

- 브라질

- 아르헨티나

- 기타

제11장 경쟁 구도

- 개요

- 주요 참여 기업의 전략/강점, 2020-2024년

- 주요 기업의 업계 집중, 2024년

- 2020-2024년에서 TOP 5사의 매출 분석

- 기업 평가 매트릭스, 주요 참여 기업, 2024년

- 경쟁 시나리오

제12장 기업 개요

- 주요 참여 기업

- SCHNEIDER ELECTRIC

- EATON

- TOSHIBA ENERGY SYSTEMS & SOLUTIONS CORPORATION

- HITACHI ENERGY LTD

- SIEMENS ENERGY

- GE VERNOVA

- FUJI ELECTRIC CO., LTD.

- CG POWER & INDUSTRIAL SOLUTIONS LTD.

- KIRLOSKAR ELECTRIC COMPANY

- HYOSUNG HEAVY INDUSTRIES

- HAMMOND POWER SOLUTIONS

- VOLTAMP TRANSFORMER

- WEG

- TMC TRANSFORMERS S.P.A.

- HANLEY ENERGY

- ALFANAR GROUP

- 기타 기업

- EFACEC

- TBEA CO., LTD.

- JST POWER EQUIPMENT, INC.

- RPT RUHSTRAT POWER TECHNOLOGY GMBH

- RAYCHEM RPG PRIVATE LIMITED

- DELTA STAR POWER MANUFACTURING CORP.

제13장 부록

KSA 25.09.08The global dry-type transformer market is projected to grow from USD 11.72 billion in 2025 to USD 16.33 billion by 2030, at a CAGR of 6.9%. This growth is driven by increasing demand for resilient, safe, and low-maintenance electrical infrastructure, aligned with smart grid transformation and the decentralization of energy systems. As utilities aim to improve system reliability and asset lifespan, there is a growing shift toward predictive maintenance strategies integrated into dry-type transformers. These transformers, commonly used in urban buildings, industrial plants, data centers, renewable energy systems, and EV charging networks, are now fitted with sensors, communication modules, and IoT-based diagnostics to enable real-time condition monitoring and fault prediction.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD million) and Volume (Units) |

| Segments | Dry-type transformer market by application, standard, voltage, type, and region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and South America |

Additionally, with greater integration of renewable energy and fluctuating load conditions, transformers must manage dynamic thermal and electrical stresses. Advanced dry-type transformer designs featuring arc-fault detection, overload protection, and remote-control capabilities support grid flexibility and quick fault recovery. Consequently, utilities and commercial users are increasingly investing in automation-ready, sensor-enabled dry-type transformers to boost grid resilience, lower maintenance costs, and meet modern safety and efficiency standards, solidifying predictive maintenance as a key driver of dry-type transformer market growth.

Medium voltage segment to hold largest market share during forecast period

During the forecast period, the medium voltage segment is projected to be the largest by voltage in the dry-type transformer market, driven by its extensive use across industrial, commercial, and utility-scale power distribution networks. Operating typically between 1 kV and 36 kV, medium-voltage dry-type transformers are vital in reducing high-voltage transmission power to usable levels for facilities such as manufacturing plants, data centers, hospitals, educational institutions, transportation hubs, and renewable energy systems.

Their compact form factor, fire-safe characteristics, and maintenance-free operation make them particularly suitable for indoor and densely populated areas, where oil-filled alternatives present higher fire and environmental risks. Moreover, the global momentum toward smart cities, electric vehicle charging infrastructure, and the integration of distributed renewable energy sources is accelerating demand for high-performance, automation-ready medium-voltage transformers capable of managing variable loads and ensuring stable, reliable power delivery.

Vacuum pressure impregnated segment, by technology, to exhibit highest CAGR during forecast period

During the forecast period, the vacuum pressure impregnated (VPI) segment is projected to exhibit the highest CAGR in the dry-type transformer market, driven by its superior mechanical strength, moisture resistance, and thermal performance. VPI transformers are manufactured by impregnating windings with specially formulated varnishes under vacuum and pressure, enhancing insulation and durability. These attributes make them highly suitable for demanding industrial environments, such as chemical plants, mining operations, marine applications, and transportation infrastructure, where exposure to dust, humidity, and mechanical stress is common. The rising need for robust and long-lasting power solutions in harsh operating conditions is accelerating the adoption of VPI technology, especially in regions focusing on heavy industrial growth and grid reliability. Additionally, the VPI process supports better thermal dissipation, contributing to operational efficiency and prolonged equipment life. These factors align with utilities' growing emphasis on predictive maintenance and lifecycle cost optimization.

Asia Pacific to be fastest-growing market during forecast period

During the forecast period, Asia Pacific is expected to be the fastest-growing market for dry-type transformers, driven by rapid urbanization, accelerating industrial development, and large-scale investments in infrastructure and renewable energy. Countries such as China, India, Japan, South Korea, and those in Southeast Asia are witnessing a surge in electricity demand due to expanding manufacturing bases, rising population, and growing adoption of electric vehicles and smart city projects. This has led to increased deployment of safe, compact, and fire-resistant transformers, particularly in urban and environmentally sensitive areas where traditional oil-filled units are less suitable. Moreover, regional governments are promoting grid modernization initiatives, electrification of rural areas, and integrating decentralized energy resources, further boosting the need for medium-voltage, low-maintenance dry-type transformers. Asia Pacific also benefits from a strong domestic manufacturing base and supportive policies to improve energy efficiency and reduce carbon emissions. As the region continues to focus on building resilient and sustainable energy infrastructure, the demand for advanced dry-type transformers with features like IoT-based monitoring, predictive maintenance, and eco-friendly insulation is expected to grow significantly.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the dry-type transformer market.

By Company Type: Tier 1 - 65%, Tier 2 - 24%, and Tier 3 - 11%

By Designation: C-level Executives - 30%, Directors - 25%, and Others - 45%

By Region: Asia Pacific - 20%, North America - 35%, Europe - 25%, Middle East & Africa - 15%, and South America - 5%

Note: Other designations include engineers and sales & regional managers.

The tiers of the companies are defined based on their total revenue as of 2024: Tier 1: >USD 1 billion, Tier 2: USD 500 million-1 billion, and Tier 3: <USD 500 million.

A few major players with extensive geographic presence dominate the dry-type transformer market. The leading players are Siemens Energy (Germany), Schneider Electric (France), Eaton (Ireland), Toshiba Corporation (Japan), General Electric (US), Hammond Power Solutions (Canada), and Hitachi, Ltd. (Japan).

Research Coverage:

The report defines, describes, and forecasts the dry-type transformer market, by technology (cast resin, vacuum pressure impregnated (VPI)), voltage (low (<1 kV), medium (1-36 kV), high (above 36 kV)), phase (single-phase, three-phase), application (industrial, commercial, utility, other applications), and region. It also offers a detailed qualitative and quantitative analysis of the market. The report comprehensively reviews the major market drivers, restraints, opportunities, and challenges. It also covers various important aspects of the market. A comprehensive analysis of the key players in the dry-type transformer market has been conducted. This analysis provides insights into their business overview, solutions and services, and key strategies. It also covers relevant contracts, partnerships, and agreements, along with new product launches, mergers, acquisitions, and other recent developments in the market. Additionally, the report includes a competitive analysis of emerging startups within the dry-type transformer ecosystem.

Reasons to Buy This Report:

This report is a strategic resource for industry leaders and new entrants, offering a comprehensive analysis of the market and its subsegments. It equips stakeholders with a thorough understanding of the competitive landscape, enabling them to refine their business positioning and devise effective go-to-market strategies. Additionally, the report elucidates the current market dynamics, highlighting critical drivers, constraints, challenges, and opportunities that inform strategic decision-making.

The report provides insights on the following points:

- Analysis of key drivers (increasing demand for energy efficiency, Implementation of stringent environment regulations), restraints (Higher cost of dry-type transformers than oil-filled ones, Susceptibility to moisture and insulation issues), opportunities (Expansion of global electrical infrastructure), and challenges (Limitations in power ratings, Preference for oil-filled transformers) influencing the growth

- Product Development/Innovation: Innovation in the dry-type transformer space is increasingly centered on solid dielectric insulation, cast resin technologies, and dry air or vacuum-based systems that eliminate the need for flammable or environmentally hazardous fluids. Manufacturers integrate smart relays, SCADA compatibility, arc-flash sensors, partial discharge monitors, and wireless communication modules into their products to support condition-based maintenance and predictive diagnostics. New designs feature modular and plug-and-play architectures, touch-safe terminals, enhanced mechanical endurance, and eco-friendly materials with reduced carbon footprints. Enclosures with corrosion resistance, IP-rated sealing, and anti-vandal features are adopted for robust performance in harsh and outdoor environments, particularly in industrial, transit, and renewable energy deployments.

- Market Development: Regions such as Asia Pacific, Africa, and South America are seeing strong market development fueled by smart city initiatives, renewable integration, and government-funded electrification projects. Programs such as India's Revamped Distribution Sector Scheme (RDSS), Brazil's DER integration roadmap, and Africa's Last-mile Connectivity Projects drive the widespread deployment of medium-voltage dry-type transformers. These transformers are critical in secondary distribution, especially where fire safety, reduced footprint, and visual aesthetics are key considerations.

- Market Diversification: Dry-type transformers' application areas are expanding beyond traditional grid utilities to include EV charging stations, solar and wind farms, commercial real estate, underground metro systems, data centers, and healthcare facilities. Each use case demands customized configurations, ranging from compact, low-noise units for hospitals to automation-ready systems for smart infrastructure and renewables. Manufacturers are responding with low-maintenance, arc-resistant, and modular designs that support scalability, reduce installation time, and enhance safety under fluctuating load conditions.

- Competitive Assessment: Key players in the dry-type transformer market include Siemens Energy (Germany), Schneider Electric (France), Eaton (Ireland), Toshiba Corporation (Japan), General Electric (US), Hammond Power Solutions (Canada), and Hitachi, Ltd. (Japan). These companies operate global manufacturing networks and strategically invest in regional partnerships, local assembly units, and R&D hubs to cater to evolving grid needs. Their competitive edge lies in offering digitally enabled, eco-efficient, modular transformer solutions that comply with global efficiency, safety, and environmental regulations. By focusing on smart diagnostics, sustainability, and fast deployment, these firms are well-positioned to meet the demand for resilient, future-ready distribution infrastructure.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.2.1 By technology

- 1.3.2.2 By voltage

- 1.3.2.3 By phase

- 1.3.2.4 By application

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key industry insights

- 2.1.2.2 Breakdown of primaries

- 2.1.1 SECONDARY DATA

- 2.2 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- 2.3.2 TOP-DOWN APPROACH

- 2.3.3 DEMAND-SIDE ANALYSIS

- 2.3.3.1 Assumptions for demand-side analysis

- 2.3.3.2 Assumptions for demand-side analysis

- 2.3.4 SUPPLY-SIDE ANALYSIS

- 2.3.4.1 Assumptions for supply-side analysis

- 2.4 GROWTH FORECAST

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DRY TYPE TRANSFORMER MARKET

- 4.2 DRY TYPE TRANSFORMER MARKET, BY REGION

- 4.3 DRY TYPE TRANSFORMER MARKET, BY TECHNOLOGY

- 4.4 DRY TYPE TRANSFORMER MARKET, BY VOLTAGE

- 4.5 DRY TYPE TRANSFORMER MARKET, BY PHASE

- 4.6 DRY TYPE TRANSFORMER MARKET, BY APPLICATION

- 4.7 ASIA PACIFIC DRY TYPE TRANSFORMER MARKET, BY TECHNOLOGY AND COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising global demand for energy efficiency

- 5.2.1.2 Implementation of stringent environmental regulations

- 5.2.1.3 Superior properties and inherent advantages

- 5.2.1.4 Rising adoption of renewable energy sources

- 5.2.2 RESTRAINTS

- 5.2.2.1 High CAPEX due to usage of advanced materials

- 5.2.2.2 Susceptibility to moisture and insulation

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Expansion of industrial infrastructure

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of liquid-based cooling

- 5.2.4.2 Preference for oil-filled transformers

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 TECHNOLOGY ANALYSIS

- 5.6.1 KEY TECHNOLOGIES

- 5.6.1.1 Cast resin dry type transformers (CRT)

- 5.6.1.2 Vacuum pressure impregnated (VPI)

- 5.6.2 COMPLEMENTARY TECHNOLOGIES

- 5.6.2.1 Temperature and partial discharge sensing systems

- 5.6.2.2 Forced-air or fan-assisted cooling systems

- 5.6.3 ADJACENT TECHNOLOGIES

- 5.6.3.1 Advanced core materials

- 5.6.3.2 Digital twin and real-time monitoring algorithms

- 5.6.1 KEY TECHNOLOGIES

- 5.7 REGULATORY LANDSCAPE

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT DATA (HS CODE 8504)

- 5.8.2 EXPORT DATA (HS CODE 8504)

- 5.9 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.10 PATENT ANALYSIS

- 5.11 PRICING ANALYSIS

- 5.11.1 PRICING RANGE OF DRY TYPE TRANSFORMERS, BY VOLTAGE, 2024

- 5.12 CASE STUDY ANALYSIS

- 5.12.1 BEDC IMPROVES TRANSFORMER RELIABILITY BY OPTIMIZING WIRE SIZING AND ADDRESSING OVERLOADING IN UGHELLI BUSINESS UNIT

- 5.12.2 WIND POWER DEVELOPMENTS TO ADDRESS GRID INTEGRATION ISSUES

- 5.12.3 WIND POWER INTEGRATION STRENGTHENS GRID COLLABORATION AND DRIVES POLICY INNOVATION IN ELETRICITY MARKETS

- 5.13 PORTER'S FIVE FORCES ANALYSIS

- 5.13.1 THREAT OF NEW ENTRANTS

- 5.13.2 BARGAINING POWER OF SUPPLIERS

- 5.13.3 BARGAINING POWER OF BUYERS

- 5.13.4 THREAT OF SUBSTITUTES

- 5.13.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.14 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.14.2 BUYING CRITERIA

- 5.15 IMPACT OF GEN AI/AI ON DRY TYPE TRANSFORMER MARKET

- 5.15.1 ADOPTION OF GEN AI/AI IN DRY TYPE TRANSFORMERS

- 5.15.2 IMPACT OF GEN AI/AI ON DRY TYPE TRANSFORMER MARKET, BY REGION

- 5.16 IMPACT OF 2025 US TARIFF ON DRY-TYPE TRANSFORMER MARKET

- 5.16.1 INTRODUCTION

- 5.16.2 KEY TARIFF RATES

- 5.16.3 PRICE IMPACT ANALYSIS

- 5.16.4 IMPACT ON COUNTRY/REGION

- 5.16.4.1 US

- 5.16.4.2 Europe

- 5.16.4.3 Asia Pacific

- 5.16.5 IMPACT ON APPLICATIONS

6 DRY TYPE TRANSFORMER MARKET, BY TECHNOLOGY

- 6.1 INTRODUCTION

- 6.2 CAST RESIN

- 6.2.1 ENHANCED FIRE SAFETY AND MINIMAL MAINTENANCE NEEDS TO DRIVE SEGMENTAL GROWTH

- 6.3 VACUUM PRESSURE IMPREGNATED (VPI)

- 6.3.1 ABILITY TO IMPROVE PARTIAL DISCHARGE RESISTANCE TO FUEL MARKET GROWTH

7 DRY TYPE TRANSFORMER MARKET, BY VOLTAGE

- 7.1 INTRODUCTION

- 7.2 LOW VOLTAGE

- 7.2.1 COMPATIBILITY WITH SMART GRID TECHNOLOGIES AND RENEWABLE ENERGY SYSTEMS TO FOSTER SEGMENTAL GROWTH

- 7.3 MEDIUM VOLTAGE

- 7.3.1 INTEGRATION WITH SMART MONITORING SYSTEMS TO SUPPORT MARKET GROWTH

- 7.4 HIGH VOLTAGE

- 7.4.1 INNOVATIONS IN COIL DESIGN AND THERMAL MANAGEMENT TO BOOST DEMAND

8 DRY TYPE TRANSFORMER MARKET, BY PHASE

- 8.1 INTRODUCTION

- 8.2 SINGLE PHASE

- 8.2.1 TECHNOLOGICAL ADVANCEMENTS IN THERMAL INSULATION AND ENCAPSULATION TECHNIQUES TO BOOST DEMAND

- 8.3 THREE PHASE

- 8.3.1 ABILITY TO BE CONNECTED ACROSS BROADER ARRAY OF VOLTAGES AND CURRENTS TO FUEL MARKET GROWTH

9 DRY TYPE TRANSFORMER MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 INDUSTRIAL

- 9.2.1 RAPID INDUSTRIALIZATION AND RISING INDUSTRIAL ACTIVITIES TO FOSTER MARKET GROWTH

- 9.3 COMMERCIAL

- 9.3.1 RISING DEMAND FOR TRANSFORMERS FEATURING HIGH SAFETY, ADAPTABILITY, AND ENERGY EFFICIENCY TO SUPPORT MARKET GROWTH

- 9.4 UTILITIES

- 9.4.1 TRANSITION TO CLEANER AND MORE SUSTAINABLE ENERGY SYSTEMS TO DRIVE MARKET

- 9.5 OTHERS

10 DRY TYPE TRANSFORMER MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 ASIA PACIFIC

- 10.2.1 CHINA

- 10.2.1.1 Low labor costs and rising industrialization to support market growth

- 10.2.2 JAPAN

- 10.2.2.1 Growing installations of solar farms, offshore wind facilities, and BESS to drive market

- 10.2.3 INDIA

- 10.2.3.1 Growing investments in renewable energy sector to foster market growth

- 10.2.4 SOUTH KOREA

- 10.2.4.1 Rising emphasis on retrofitting aging grid infrastructure to boost demand

- 10.2.5 REST OF ASIA PACIFIC

- 10.2.1 CHINA

- 10.3 EUROPE

- 10.3.1 GERMANY

- 10.3.1.1 Rapid expansion of EV charging stations, data centers, and industrial automation to support market growth

- 10.3.2 FRANCE

- 10.3.2.1 Growing emphasis on clean energy investments and smart grid expansion to foster market growth

- 10.3.3 UK

- 10.3.3.1 Thriving construction sector to offer lucrative growth opportunities

- 10.3.4 ITALY

- 10.3.4.1 Transition toward smart grids and digital substations to boost demand

- 10.3.5 SPAIN

- 10.3.5.1 Regulatory emphasis on reducing fire hazards and leakage risks in energy systems to drive market

- 10.3.6 REST OF EUROPE

- 10.3.1 GERMANY

- 10.4 NORTH AMERICA

- 10.4.1 US

- 10.4.1.1 Growth of utility-scale solar and wind projects to boost demand

- 10.4.2 CANADA

- 10.4.2.1 Emphasis on upgrading transmission and DERs to foster market growth

- 10.4.3 MEXICO

- 10.4.3.1 Government-led initiatives to enhance grid reliability and resilience to fuel market growth

- 10.4.1 US

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 GCC

- 10.5.1.1 Saudi Arabia

- 10.5.1.1.1 Transition toward renewable energy to foster market growth

- 10.5.1.2 Rest of GCC

- 10.5.1.1 Saudi Arabia

- 10.5.2 SOUTH AFRICA

- 10.5.2.1 Government-backed solar initiatives to drive market

- 10.5.3 REST OF MIDDLE EAST & AFRICA

- 10.5.1 GCC

- 10.6 SOUTH AMERICA

- 10.6.1 BRAZIL

- 10.6.1.1 Commitment to decarbonization and energy transition to drive market

- 10.6.2 ARGENTINA

- 10.6.2.1 Promotion of renewable energy projects to support market growth

- 10.6.3 REST OF SOUTH AMERICA

- 10.6.1 BRAZIL

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020-2024

- 11.3 INDUSTRY CONCENTRATION OF KEY PLAYERS, 2024

- 11.4 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2020-2024

- 11.5 COMPANY EVALUATION MATRIX, KEY PLAYERS, 2024

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- 11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.5.5.1 Region footprint

- 11.5.5.2 Technology footprint

- 11.5.5.3 Application footprint

- 11.5.5.4 Phase footprint

- 11.5.5.5 Voltage footprint

- 11.6 COMPETITIVE SCENARIO

- 11.6.1 DEALS

- 11.6.2 PRODUCT LAUNCHES

- 11.6.3 EXPANSIONS

- 11.6.4 OTHER DEVELOPMENTS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 SCHNEIDER ELECTRIC

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Solutions/Services offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Other developments

- 12.1.1.4 MnM view

- 12.1.1.4.1 Key strengths/Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses/Competitive threats

- 12.1.2 EATON

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Solutions/Services offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Deals

- 12.1.2.3.2 Other developments

- 12.1.2.4 MnM view

- 12.1.2.4.1 Key strengths/Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses/Competitive threats

- 12.1.3 TOSHIBA ENERGY SYSTEMS & SOLUTIONS CORPORATION

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Solutions/Services offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Expansions

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths/Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses/Competitive threats

- 12.1.4 HITACHI ENERGY LTD

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Solutions/Services offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches

- 12.1.4.3.2 Deals

- 12.1.4.3.3 Expansions

- 12.1.4.3.4 Other developments

- 12.1.4.4 MnM view

- 12.1.4.4.1 Key strengths/Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses/Competitive threats

- 12.1.5 SIEMENS ENERGY

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Solutions/Services offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches

- 12.1.5.4 MnM view

- 12.1.5.4.1 Key strengths/Right to win

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses/Competitive threats

- 12.1.6 GE VERNOVA

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Solutions/Services offered

- 12.1.6.3 Recent Developments

- 12.1.6.3.1 Developments

- 12.1.7 FUJI ELECTRIC CO., LTD.

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Solutions/Services offered

- 12.1.8 CG POWER & INDUSTRIAL SOLUTIONS LTD.

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Solutions/Services offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Expansions

- 12.1.9 KIRLOSKAR ELECTRIC COMPANY

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Solutions/Services offered

- 12.1.10 HYOSUNG HEAVY INDUSTRIES

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Solutions/Services offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Developments

- 12.1.11 HAMMOND POWER SOLUTIONS

- 12.1.11.1 Business overview

- 12.1.11.2 Products/Solutions/Services offered

- 12.1.11.3 Recent developments

- 12.1.11.3.1 Product launches

- 12.1.11.3.2 Other developments

- 12.1.12 VOLTAMP TRANSFORMER

- 12.1.12.1 Business overview

- 12.1.12.2 Products/Solutions/Services offered

- 12.1.12.3 Recent Development

- 12.1.12.3.1 Expansions

- 12.1.13 WEG

- 12.1.13.1 Business overview

- 12.1.13.2 Products/Solutions/Services offered

- 12.1.13.3 Recent developments

- 12.1.13.3.1 Developments

- 12.1.14 TMC TRANSFORMERS S.P.A.

- 12.1.14.1 Business overview

- 12.1.14.2 Products/Solutions/Services offered

- 12.1.14.3 Recent developments

- 12.1.14.3.1 Deals

- 12.1.14.3.2 Expansions

- 12.1.15 HANLEY ENERGY

- 12.1.15.1 Business overview

- 12.1.15.2 Products/Solutions/Services offered

- 12.1.16 ALFANAR GROUP

- 12.1.16.1 Business overview

- 12.1.16.2 Products/Solutions/Services offered

- 12.1.1 SCHNEIDER ELECTRIC

- 12.2 OTHER PLAYERS

- 12.2.1 EFACEC

- 12.2.2 TBEA CO., LTD.

- 12.2.3 JST POWER EQUIPMENT, INC.

- 12.2.4 RPT RUHSTRAT POWER TECHNOLOGY GMBH

- 12.2.5 RAYCHEM RPG PRIVATE LIMITED

- 12.2.6 DELTA STAR POWER MANUFACTURING CORP.

13 APPENDIX

- 13.1 INSIGHTS FROM INDUSTRY EXPERTS

- 13.2 DISCUSSION GUIDE

- 13.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.4 CUSTOMIZATION OPTIONS

- 13.5 RELATED REPORTS

- 13.6 AUTHOR DETAILS