|

시장보고서

상품코드

1802925

스마트 시티 플랫폼 시장 : 제공별, 전개별, 용도별 - 예측(-2030년)Smart City Platforms Market by Offering (Platforms, Services), Deployment (Cloud, On-premises, Hybrid), Application (Smart Transportation, Public Safety & Emergency Response, Smart Infrastructure, Smart Energy & Utilities) - Global Forecast to 2030 |

||||||

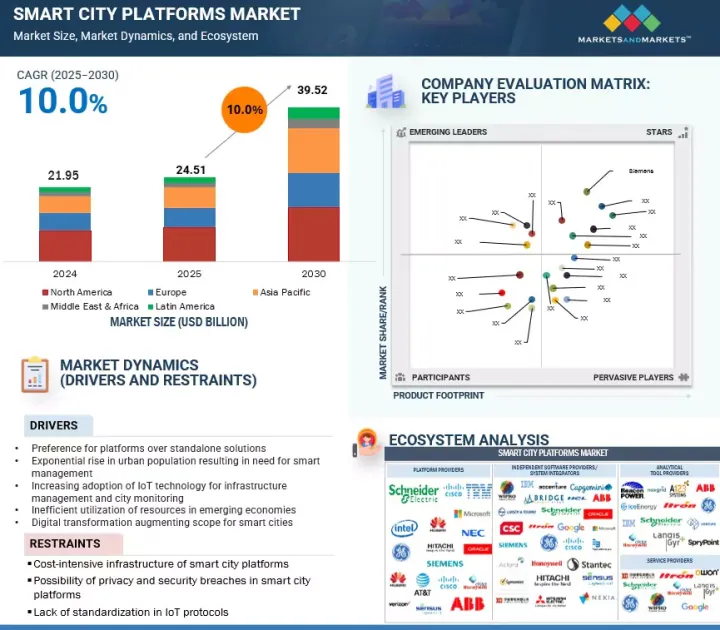

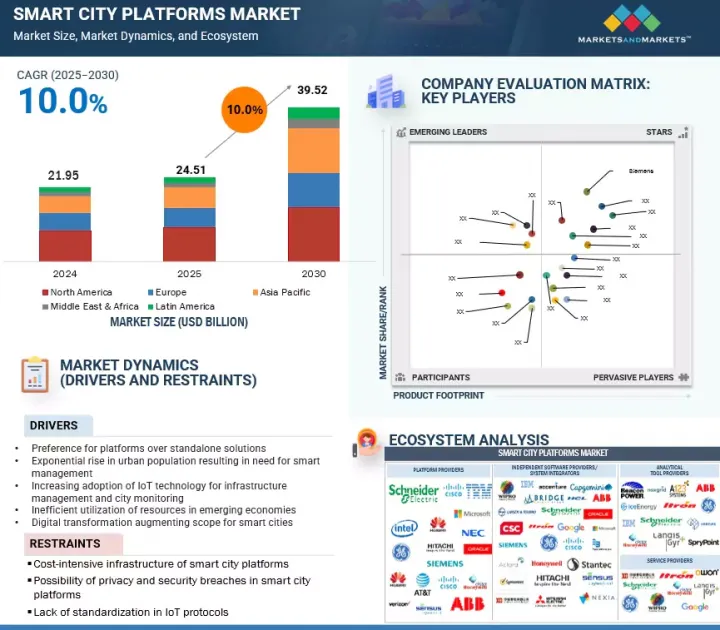

세계의 스마트 시티 플랫폼 시장 규모는 2025년 245억 1,000만 달러에서 2030년까지 395억 2,000만 달러에 달할 것으로 예측되며, 예측 기간에 CAGR로 10.0%의 성장이 전망됩니다.

시장은 주로 급속한 도시화에 의해 주도되고 있으며, 교통, 에너지, 공공안전 등 도시 경영을 관리하기 위해 보다 스마트한 인프라가 필요합니다. 아시아태평양, 유럽, 중동 등의 지역에서는 정부 주도의 스마트 시티 이니셔티브가 플랫폼 채택을 가속화하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2020-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 100만/10억 달러 |

| 부문 | 제공, 전개, 용도, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

IoT, 5G, 엣지 컴퓨팅의 기술 발전과 환경적 지속가능성 목표의 증가로 인해 통합 플랫폼의 필요성이 더욱 커지고 있습니다. 또한, AI와 고급 분석을 활용하여 실시간 의사결정과 업무 효율성을 향상시키고 있습니다. 하지만 높은 초기 투자 및 구축 비용, 데이터 프라이버시 및 사이버 보안에 대한 우려 등 여러 가지 제약요인에 직면해 있습니다. 또한, 레거시 시스템과의 통합 및 상호운용성 문제가 기술적 장벽으로 작용하고, 숙련된 인력 부족과 불투명한 규제 프레임워크가 대규모 채택을 더욱 방해하고 있습니다.

전개별로는 클라우드 부문이 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.

클라우드 전개는 스마트 시티 플랫폼 시장에서 가장 눈에 띄게 빠르게 성장하고 있는 분야입니다. 클라우드 기반 플랫폼은 확장성, 비용 효율성, 실시간 데이터 처리 및 분석을 지원하는 능력으로 인해 도시에서의 채택이 증가하고 있습니다. 이러한 플랫폼은 중앙 집중식 관리, 신속한 서비스 배포, 다양한 도시 시스템 간의 원활한 통합을 용이하게 합니다. 또한, 클라우드 배포는 원격 액세스를 가능하게 하고, 부서 간 협업을 촉진하며, 무거운 IT 인프라의 필요성을 줄여주기 때문에 디지털 전환을 추구하는 도시에 이상적입니다.

용도별로는 공공안전 및 비상 대응 부문이 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예상됩니다.

공공안전 및 긴급 대응 부문은 예방적 기술과 반응적 기술을 통해 시민의 안전을 지키는 데 중점을 두고 있습니다. 스마트 시티 플랫폼은 감시 시스템, 911 콜센터, 소셜 미디어, 드론, 환경 센서의 데이터를 통합하여 보안 업무에 대한 중앙 집중식 뷰를 생성합니다. AI를 활용한 영상 분석, 얼굴 인식, 행동 예측 등의 첨단 도구는 범죄 예방과 신속한 사건 감지에 도움이 됩니다. 긴급 상황 대응은 긴급 차량의 동적 라우팅과 상황 인식 대시보드를 통해 법집행기관, 소방, 의료 서비스 간의 실시간 통신을 통해 강화됩니다. 이러한 시스템은 홍수, 지진, 전염병과 같은 대규모 상황이나 재난을 관리하는 데에도 도움이 되고 있습니다.

아시아태평양은 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예상됩니다.

아시아태평양의 스마트 시티 플랫폼 시장은 급속한 도시화, 정부의 적극적인 노력, IoT, AI, 클라우드, 5G 등 첨단 기술 도입의 가속화로 인해 강력한 성장세를 보이고 있습니다. 중국의 Smart City Development Plan, 인도의 Smart Cities Mission과 같은 전략적 국가 프로그램은 대규모 디지털 인프라의 운영을 촉진하고 있습니다. 스마트 유틸리티, 모빌리티, 거버넌스 등 고성장 부문은 확장성과 비용 효율성을 높이기 위해 클라우드 기반 구축으로 전환하는 추세에 힘입어 높은 성장세를 보이고 있습니다. 화웨이, 알리바바, 마이크로소프트, 시스코, AWS 등 주요 테크 기업들은 정부 및 도시 당국과의 제휴를 통해 이 지역 전체에서 입지를 강화하고 있습니다. 데이터 프라이버시, 인프라 개발 지연 등의 문제가 있지만, 아시아태평양은 스마트 시티 플랫폼에 있어 가장 역동적이고 기회가 풍부한 시장이며, 솔루션 제공업체와 투자자 모두에게 큰 성장 잠재력을 가지고 있습니다.

세계의 스마트 시티 플랫폼 시장에 대해 조사 분석했으며, 주요 촉진요인과 저해요인, 경쟁 구도, 향후 동향 등의 정보를 전해드립니다.

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 중요한 인사이트

- 시장 진입 기업에서 매력적인 기회

- 북미의 스마트 시티 플랫폼 시장 : 제공별, 국가별

- 아시아태평양의 스마트 시티 플랫폼 시장 : 제공별, 상위 3개국

- 스마트 시티 플랫폼 시장 : 용도별

제5장 시장 개요와 산업 동향

- 소개

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 산업 동향

- 스마트 시티 플랫폼 시장의 역사

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 공급망 분석

- 생태계 매핑

- 가격 책정 분석

- 기술 분석

- 특허 분석

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 사례 연구 분석

- 주요 회의와 이벤트(2025-2026년)

- 스마트 시티 플랫폼 시장 기술 로드맵

- 스마트 시티 플랫폼 시장의 구현 베스트 프랙티스

- 현재 비즈니스 모델과 신흥 비즈니스 모델

- AI와 생성형 AI 소개

- 투자와 자금 조달 시나리오

- 2025년 미국 관세의 영향 - 스마트 시티 플랫폼 시장

- 소개

- 주요 관세율

- 가격의 영향 분석

- 국가/지역에 대한 영향

- 최종사용자에 대한 영향

제6장 스마트 시티 플랫폼 시장 : 제공별

- 소개

- 플랫폼

- 연결성 관리 플랫폼

- 통합 플랫폼

- 디바이스 관리 플랫폼

- 데이터 관리 플랫폼

- 보안 플랫폼

- 기타 플랫폼

- 서비스

- 전문 서비스

- 매니지드 서비스

제7장 스마트 시티 플랫폼 시장 : 전개별

- 소개

- 클라우드

- 하이브리드

- 온프레미스

제8장 스마트 시티 플랫폼 시장 : 용도별

- 소개

- 스마트 교통

- 공공안전·긴급 대응

- 스마트 에너지·유틸리티

- 스마트 거버넌스

- 스마트 인프라

- 기타 용도

제9장 스마트 시티 플랫폼 시장 : 지역별

- 소개

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 거시경제 전망

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 북유럽

- 기타 유럽

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 중국

- 일본

- 인도

- 한국

- 호주·뉴질랜드

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동 및 아프리카의 거시경제 전망

- 아랍에미리트

- 사우디아라비아

- 남아프리카공화국

- 이집트

- 나이지리아

- 기타 중동 및 아프리카

- 라틴아메리카

- 라틴아메리카의 거시경제 전망

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

제10장 경쟁 구도

- 소개

- 주요 진출 기업의 전략/강점(2021-2025년)

- 매출 분석(2020-2024년)

- 시장 점유율 분석(2024년)

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업 평가 매트릭스 : 스타트업/중소기업(2024년)

- 브랜드/제품의 비교

- 기업 평가와 재무 지표

- 경쟁 시나리오

제11장 기업 개요

- 주요 기업

- SIEMENS

- CISCO

- HUAWEI

- HITACHI

- MICROSOFT

- IBM

- AWS

- AT&T

- NOKIA

- ATOS

- 기타 기업

- SAP

- NEC

- FUJITSU

- SCHNEIDER ELECTRIC

- ALIBABA CLOUD

- ERICSSON

- BOSCH.IO

- ITRON

- PWC

- SICE

- 스타트업/중소기업

- THETHINGS.IO

- KAAIOT TECHNOLOGIES

- QUANTELA

- UBICQUIA

- IGOR

- 75F

- TELENSA

- ENEVO

- KETOS

- CLEVERCITI

- GAIA SMART CITIES

- GLOBETOM

- TADOOM

- ATHENA SMART CITIES

제12장 인접 시장·부록

- 소개

- 스마트 시티 시장 - 세계의 예측(-2030년)

- 스마트 인프라 시장 - 세계의 예측(-2029년)

제13장 부록

KSM 25.09.09The global smart city platforms market will grow from USD 24.51 billion in 2025 to USD 39.52 billion by 2030 at a compounded annual growth rate (CAGR) of 10.0% during the forecast period. The smart city platforms market is primarily driven by rapid urbanization, which necessitates smarter infrastructure to manage city operations such as transportation, energy, and public safety. Government-led smart city initiatives across regions such as Asia Pacific, Europe, and the Middle East are accelerating platform adoption.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD) Million/Billion |

| Segments | By Offering, Deployment, Application, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

Technological advancements in IoT, 5G, and edge computing, combined with growing environmental sustainability goals, are further fueling the need for integrated platforms. Additionally, the use of AI and advanced analytics is enhancing real-time decision-making and operational efficiency. However, the market faces restraints, including high initial investment and deployment costs, as well as persistent concerns over data privacy and cybersecurity. Integration challenges with legacy systems and interoperability issues pose technical barriers, while a lack of a skilled workforce and unclear regulatory frameworks further hinder large-scale adoption.

Based on deployment, the cloud segment is expected to hold the largest market share during the forecast period.

Cloud deployment is the most prominent and rapidly growing segment in the smart city platforms market. Cities are increasingly adopting cloud-based platforms due to their scalability, cost-effectiveness, and ability to support real-time data processing and analytics. These platforms facilitate centralized management, faster deployment of services, and seamless integration across various urban systems. Additionally, cloud deployment enables remote access, fosters cross-departmental collaboration, and reduces the need for heavy IT infrastructure, making it ideal for cities aiming for digital transformation.

Based on application, the public safety & emergency response segment is expected to grow at the highest CAGR during the forecast period.

Public safety & emergency response is focused on safeguarding citizens through proactive and reactive technologies. Smart city platforms unify data from surveillance systems, 911 call centers, social media, drones, and environmental sensors to create a centralized view of security operations. Advanced tools such as AI-powered video analytics, facial recognition, and behavior prediction help in crime prevention and rapid incident detection. Emergency response is enhanced through real-time communication between law enforcement, fire, and medical services, with dynamic routing for emergency vehicles and situational awareness dashboards. These systems are also instrumental in managing large-scale events and disasters, including floods, earthquakes, or pandemics.

Asia Pacific is expected to grow at the highest CAGR during the forecast period.

The smart city platforms market in Asia Pacific is experiencing robust growth, fueled by rapid urbanization, proactive government initiatives, and accelerated adoption of advanced technologies such as IoT, AI, cloud, and 5G. Strategic national programs, such as China's Smart City Development Plan and India's Smart Cities Mission, are driving large-scale digital infrastructure rollouts. High-growth segments include smart utilities, mobility, and governance, supported by a strong shift toward cloud-based deployments for greater scalability and cost efficiency. Major technology players, including Huawei, Alibaba, Microsoft, Cisco, and AWS, are expanding their presence across the region through partnerships with governments and urban authorities. Despite challenges such as data privacy and uneven infrastructure readiness, Asia-Pacific remains the most dynamic and opportunity-rich market for smart city platforms, offering strong growth potential for solution providers and investors alike.

Breakdown of primaries

We interviewed Chief Executive Officers (CEOs), directors of innovation and technology, system integrators, and executives from several significant companies in the smart city platforms market.

- By Company: Tier I: 35%, Tier II: 40%, and Tier III: 25%

- By Designation: C-Level Executives: 40%, Director Level: 25%, and Others: 35%

- By Region: North America: 25%, Europe: 35%, Asia Pacific: 30%, and Rest of the World: 10%

Some of the major smart city platform vendors are IBM (US), Siemens (Germany), Cisco (US), Hitachi (Japan), Microsoft (US), Huawei (China), AWS (US), AT&T (US), Nokia (Finland), and Atos (France).

Research coverage:

The market report covered the smart city platforms market across segments. We estimated the market size and growth potential for many segments based on offering, deployment, application, and region. It contains a thorough competition analysis of the major market participants, information about their businesses, essential observations about their product offerings, current trends, and critical market strategies.

Reasons to buy this report:

With information on the most accurate revenue estimates for the whole smart city platforms industry and its subsegments, the research will benefit market leaders and recent newcomers. Stakeholders will benefit from this report's increased understanding of the competitive environment, which will help them better position their companies and develop go-to-market strategies. The research offers information on the main market drivers, constraints, opportunities, and challenges, as well as aids players in understanding the pulse of the industry.

The report provides insights on the following pointers:

Analysis of key drivers (Preference for platforms over standalone solutions, exponential rise in urban population resulting in need for smart management, increasing adoption of IoT technology for infrastructure management and city monitoring, inefficient utilization of resources in emerging economies, digital transformation augmenting scope for smart cities), restraints (Cost-intensive infrastructure of smart city platforms, possibility of privacy and security breaches in smart city platforms, lack of standardization in IoT protocols), opportunities (Development of smart infrastructure, industrial and commercial deployment of smart city platforms, rising smart city initiatives worldwide), and challenges (Increasing concern over data privacy and security, growing cybersecurity attacks due to proliferation of IoT devices, disruption in logistics and supply chain of IoT devices).

- Product Development/Innovation: Comprehensive analysis of emerging technologies, R&D initiatives, and new service and product introductions in the smart city platforms market.

- Market Development: In-depth details regarding profitable markets: the paper examines the global smart city platforms market.

- Market Diversification: Comprehensive details regarding recent advancements, investments, unexplored regions, new goods and services, and the smart city platforms market.

- Competitive Assessment: Thorough analysis of the market shares, expansion plans, platforms, and service portfolios of the top competitors in the smart city platforms industry, such as IBM (US), Siemens (Germany), Cisco (US), Hitachi (Japan), Microsoft (US), Huawei (China), AWS (US), AT&T (US), Nokia (Finland), Atos (France), SAP (Germany), NEC (Japan), Fujitsu (Japan), Schneider Electric (France), Alibaba Cloud (China), Ericsson (Sweden), Bosch.io (Germany), Itron (US), PwC (UK), SICE (Spain), thethings.iO (Spain), KaaIoT Technologies (US), Quantela (US), Ubicquia (US), Igor (US), 75F (US), Telensa (UK), Enevo (US), KETOS (US), Cleverciti (Germany), Gaia Smart Cities (India), Globetom (South Africa), Tadoom (Oman), and Athena SmartCities (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primary profiles

- 2.1.2.2 Primary sources

- 2.1.2.3 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET BREAKUP AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- 2.3.2 TOP-DOWN APPROACH

- 2.4 GROWTH FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR MARKET PLAYERS

- 4.2 NORTH AMERICA: SMART CITY PLATFORMS MARKET, BY OFFERING AND COUNTRY

- 4.3 ASIA PACIFIC: SMART CITY PLATFORMS MARKET, BY OFFERING AND TOP 3 COUNTRIES

- 4.4 SMART CITY PLATFORMS MARKET, BY APPLICATION

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Preference for platforms over standalone solutions

- 5.2.1.2 Exponential rise in urban population resulting in need for smart management

- 5.2.1.3 Increasing adoption of IoT technology for infrastructure management and city monitoring

- 5.2.1.4 Inefficient utilization of resources in emerging economies

- 5.2.1.5 Digital transformation augmenting scope for smart cities

- 5.2.2 RESTRAINTS

- 5.2.2.1 Cost-intensive infrastructure of smart city platforms

- 5.2.2.2 Possibility of privacy and security breaches in smart city platforms

- 5.2.2.3 Lack of standardization in IoT protocols

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Development of smart infrastructure

- 5.2.3.2 Industrial and commercial deployment of smart city platforms

- 5.2.3.3 Rising smart city initiatives worldwide

- 5.2.4 CHALLENGES

- 5.2.4.1 Increasing concern over data privacy and security

- 5.2.4.2 Growing cybersecurity attacks due to proliferation of IoT devices

- 5.2.4.3 Disruption in logistics and supply chain of IoT devices

- 5.2.1 DRIVERS

- 5.3 INDUSTRY TRENDS

- 5.3.1 HISTORY OF SMART CITY PLATFORMS MARKET

- 5.3.1.1 1990-2000

- 5.3.1.2 2000-2010

- 5.3.1.3 2010-2020

- 5.3.1.4 2021-present

- 5.3.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.3.3 SUPPLY CHAIN ANALYSIS

- 5.3.4 ECOSYSTEM MAPPING

- 5.3.5 PRICING ANALYSIS

- 5.3.5.1 Average selling price of key players, by application

- 5.3.5.2 Indicative pricing trend of smart city platforms

- 5.3.6 TECHNOLOGY ANALYSIS

- 5.3.6.1 Key Technologies

- 5.3.6.1.1 AI and ML

- 5.3.6.1.2 IoT

- 5.3.6.1.3 Big data analytics

- 5.3.6.2 Adjacent Technologies

- 5.3.6.2.1 AR/VR

- 5.3.6.2.2 Edge computing

- 5.3.6.3 Complementary Technologies

- 5.3.6.3.1 Geospatial information system (GIS)

- 5.3.6.3.2 Smart grids

- 5.3.6.3.3 Cybersecurity solutions

- 5.3.6.1 Key Technologies

- 5.3.7 PATENT ANALYSIS

- 5.3.7.1 METHODOLOGY

- 5.3.8 PORTER'S FIVE FORCES ANALYSIS

- 5.3.9 THREAT OF NEW ENTRANTS

- 5.3.10 THREAT OF SUBSTITUTES

- 5.3.11 BARGAINING POWER OF BUYERS

- 5.3.12 BARGAINING POWER OF SUPPLIERS

- 5.3.13 INTENSITY OF COMPETITIVE RIVALRY

- 5.3.14 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.3.14.1 Key stakeholders in buying process

- 5.3.14.2 Buying criteria

- 5.3.15 CASE STUDY ANALYSIS

- 5.3.15.1 Case study 1: Smart City Ahmedabad Development Limited (SCADL) partnered with NEC to upgrade manually operated bus transit infrastructure

- 5.3.15.2 Case study 2: Sierra Wireless helped Liveable Cities transform streetlights into sensor networks

- 5.3.15.3 Case study 3: Fastned relies on ABB to expand EV fast charge network across Europe

- 5.3.15.4 Case study 4: Honeywell enabled efficient flight routing for Newark Liberty International Airport

- 5.3.15.5 Case study 5: Bane NOR selected Thales to provide next-generation nationwide traffic management system

- 5.3.15.6 Case study 6: Curtin University adopted Hitachi IoT solution to create smart campus

- 5.3.16 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.3.17 TECHNOLOGY ROADMAP FOR SMART CITY PLATFORMS MARKET

- 5.3.17.1 Short-term Roadmap (2025-2026)

- 5.3.17.2 Mid-term Roadmap (2027-2028)

- 5.3.17.3 Long-term Roadmap (2029-2030)

- 5.3.18 BEST PRACTICES TO IMPLEMENT IN SMART CITY PLATFORMS MARKET

- 5.3.19 CURRENT AND EMERGING BUSINESS MODELS

- 5.3.20 INTRODUCTION TO ARTIFICIAL INTELLIGENCE AND GENERATIVE AI

- 5.3.20.1 Impact of Generative AI on Smart City Platforms Market

- 5.3.20.2 Use cases of generative AI in smart city platforms

- 5.3.21 INVESTMENT AND FUNDING SCENARIO

- 5.3.1 HISTORY OF SMART CITY PLATFORMS MARKET

- 5.4 IMPACT OF 2025 US TARIFF - SMART CITY PLATFORMS MARKET

- 5.4.1 INTRODUCTION

- 5.4.2 KEY TARIFF RATES

- 5.4.3 PRICE IMPACT ANALYSIS

- 5.4.3.1 Strategic shifts and emerging trends

- 5.4.4 IMPACT ON COUNTRY/REGION

- 5.4.4.1 US

- 5.4.4.2 China

- 5.4.4.3 Europe

- 5.4.4.4 Asia Pacific (excluding China)

- 5.4.5 IMPACT ON END USERS

- 5.4.5.1 City governments and municipal authorities

- 5.4.5.2 Citizens and residents

- 5.4.5.3 Utility companies and infrastructure providers

6 SMART CITY PLATFORMS MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERING: MARKET DRIVERS

- 6.2 PLATFORMS

- 6.2.1 CONNECTIVITY MANAGEMENT PLATFORMS

- 6.2.1.1 Provide end-to-end connectivity solutions for seamless integration

- 6.2.2 INTEGRATION PLATFORMS

- 6.2.2.1 Need to merge data from different siloed systems to drive adoption

- 6.2.3 DEVICE MANAGEMENT PLATFORMS

- 6.2.3.1 Growing need to manage information across devices to boost adoption

- 6.2.4 DATA MANAGEMENT PLATFORMS

- 6.2.4.1 Ability to ease solution management of various applications to drive demand

- 6.2.5 SECURITY PLATFORMS

- 6.2.5.1 High demand due to rising risk of cyber threats

- 6.2.6 OTHER PLATFORMS

- 6.2.1 CONNECTIVITY MANAGEMENT PLATFORMS

- 6.3 SERVICES

- 6.3.1 PROFESSIONAL SERVICES

- 6.3.1.1 Consulting & architecture designing

- 6.3.1.1.1 Growing demand to ensure cost-optimization

- 6.3.1.2 Infrastructure monitoring & management

- 6.3.1.2.1 Provides high-precision information in real-time

- 6.3.1.3 Deployment & training

- 6.3.1.3.1 Rising demand for services to ensure optimized functioning of platforms

- 6.3.1.1 Consulting & architecture designing

- 6.3.2 MANAGED SERVICES

- 6.3.2.1 Facilitate efficient management of smart city operations

- 6.3.1 PROFESSIONAL SERVICES

7 SMART CITY PLATFORMS MARKET, BY DEPLOYMENT

- 7.1 INTRODUCTION

- 7.1.1 DEPLOYMENT: MARKET DRIVERS

- 7.2 CLOUD

- 7.2.1 GROWING PREFERENCE FOR COST-EFFECTIVE AND FLEXIBLE SOLUTIONS

- 7.3 HYBRID

- 7.3.1 HIGH DEMAND DUE TO NEED FOR SECURE AND SUSTAINABLE TOOLS TO BUILD SMART CITIES

- 7.4 ON-PREMISES

- 7.4.1 REQUIREMENT FOR TIMELY PROBLEM-SOLVING TO INCREASE DEMAND

8 SMART CITY PLATFORMS MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.1.1 APPLICATION: MARKET DRIVERS

- 8.2 SMART TRANSPORTATION

- 8.2.1 OPTIMIZE URBAN MOBILITY WITH REAL-TIME, DATA-DRIVEN TRANSIT SOLUTIONS

- 8.3 PUBLIC SAFETY & EMERGENCY RESPONSE

- 8.3.1 ENHANCE CITIZEN SAFETY THROUGH INTEGRATED, PREDICTIVE EMERGENCY MANAGEMENT

- 8.4 SMART ENERGY & UTILITIES

- 8.4.1 DRIVE EFFICIENCY AND SUSTAINABILITY WITH INTELLIGENT UTILITY INFRASTRUCTURE

- 8.5 SMART GOVERNANCE

- 8.5.1 TRANSFORM PUBLIC SERVICES WITH TRANSPARENT, CITIZEN-CENTRIC DIGITAL PLATFORMS

- 8.6 SMART INFRASTRUCTURE

- 8.6.1 NEED TO BUILD RESILIENT CITIES WITH CONNECTED, SELF-MONITORING URBAN ASSETS TO DRIVE MARKET

- 8.7 OTHER APPLICATIONS

9 SMART CITY PLATFORMS MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 NORTH AMERICA

- 9.2.1 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 9.2.2 US

- 9.2.2.1 Technological advancements and digital readiness to boost market growth

- 9.2.3 CANADA

- 9.2.3.1 Rapid urbanization and use of IoT technology to drive growth of smart cities

- 9.3 EUROPE

- 9.3.1 EUROPE: MACROECONOMIC OUTLOOK

- 9.3.2 UNITED KINGDOM

- 9.3.2.1 Increased adoption of innovative digital technologies to boost market growth

- 9.3.3 GERMANY

- 9.3.3.1 Acceleration of urban digital transformation to drive smart city development

- 9.3.4 FRANCE

- 9.3.4.1 High usage of smart devices to drive market

- 9.3.5 ITALY

- 9.3.5.1 Growing adoption of latest technologies to boost market

- 9.3.6 SPAIN

- 9.3.6.1 Government initiatives to improve quality of life to drive market

- 9.3.7 NORDICS

- 9.3.7.1 Focus on sustainable development to boost demand for smart cities

- 9.3.8 REST OF EUROPE

- 9.4 ASIA PACIFIC

- 9.4.1 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 9.4.2 CHINA

- 9.4.2.1 Government initiatives to promote growth of smart cities

- 9.4.3 JAPAN

- 9.4.3.1 Highly developed telecom sector to boost development of smart cities

- 9.4.4 INDIA

- 9.4.4.1 Growing urban population to drive need for smart cities

- 9.4.5 SOUTH KOREA

- 9.4.6 AUSTRALIA AND NEW ZEALAND

- 9.4.6.1 Knowledge-based Australian economy to offer opportunities for market growth

- 9.4.7 SOUTHEAST ASIA

- 9.4.7.1 Rapid urbanization to drive market

- 9.4.8 REST OF ASIA PACIFIC

- 9.5 MIDDLE EAST & AFRICA

- 9.5.1 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 9.5.2 UAE

- 9.5.2.1 Government focus on sustainable development to drive demand for smart city platforms

- 9.5.3 KSA

- 9.5.3.1 Increasing development of smart cities to boost market

- 9.5.4 SOUTH AFRICA

- 9.5.4.1 Rising urbanization to increase development of smart cities

- 9.5.5 EGYPT

- 9.5.5.1 Introduction of people-centered digital policies to create demand for smart cities

- 9.5.6 NIGERIA

- 9.5.6.1 Rising urbanization to increase demand for smart cities

- 9.5.7 REST OF MIDDLE EAST & AFRICA

- 9.6 LATIN AMERICA

- 9.6.1 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 9.6.2 BRAZIL

- 9.6.2.1 Early adoption of smart city technologies to boost market

- 9.6.3 MEXICO

- 9.6.3.1 Need to create digitally smart urban areas to drive market growth

- 9.6.4 ARGENTINA

- 9.6.4.1 Rising need for smart city management tools to drive market

- 9.6.5 REST OF LATIN AMERICA

10 COMPETITIVE LANDSCAPE

- 10.1 INTRODUCTION

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 10.3 REVENUE ANALYSIS, 2020-2024

- 10.4 MARKET SHARE ANALYSIS, 2024

- 10.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.5.1 STARS

- 10.5.2 EMERGING LEADERS

- 10.5.3 PERVASIVE PLAYERS

- 10.5.4 PARTICIPANTS

- 10.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.5.5.1 Company footprint

- 10.5.5.2 Region footprint

- 10.5.5.3 Application footprint

- 10.5.5.4 Offering footprint

- 10.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 10.6.1 PROGRESSIVE COMPANIES

- 10.6.2 RESPONSIVE COMPANIES

- 10.6.3 DYNAMIC COMPANIES

- 10.6.4 STARTING BLOCKS

- 10.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 10.6.5.1 Detailed list of key startups/SMEs

- 10.6.5.2 Competitive benchmarking of key startups/SMEs

- 10.7 BRAND/PRODUCT COMPARISON

- 10.8 COMPANY VALUATION AND FINANCIAL METRICS

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES

- 10.9.2 DEALS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 SIEMENS

- 11.1.1.1 Business overview

- 11.1.1.2 Products/Solutions/Services offered

- 11.1.1.3 Recent developments

- 11.1.1.4 MnM view

- 11.1.1.4.1 Key strengths/Right to win

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses and competitive threats

- 11.1.2 CISCO

- 11.1.2.1 Business overview

- 11.1.2.2 Products/Solutions/Services offered

- 11.1.2.3 Recent developments

- 11.1.2.4 MnM view

- 11.1.2.4.1 Key strengths/Right to win

- 11.1.2.4.2 Strategic choices

- 11.1.2.4.3 Weaknesses and competitive threats

- 11.1.3 HUAWEI

- 11.1.3.1 Business overview

- 11.1.3.2 Products/Solutions/Services offered

- 11.1.3.3 Recent developments

- 11.1.3.4 MnM view

- 11.1.3.4.1 Key strengths/Right to win

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses and competitive threats

- 11.1.4 HITACHI

- 11.1.4.1 Business overview

- 11.1.4.2 Products/Solutions/Services offered

- 11.1.4.3 Recent developments

- 11.1.4.4 MnM view

- 11.1.4.4.1 Key strengths/Right to win

- 11.1.4.4.2 Strategic choices

- 11.1.4.4.3 Weaknesses and competitive threats

- 11.1.5 MICROSOFT

- 11.1.5.1 Business overview

- 11.1.5.2 Products/Solutions/Services offered

- 11.1.5.3 Recent developments

- 11.1.5.4 MnM view

- 11.1.5.4.1 Key strengths/Right to win

- 11.1.5.4.2 Strategic choices

- 11.1.5.4.3 Weaknesses and competitive threats

- 11.1.6 IBM

- 11.1.6.1 Business overview

- 11.1.6.2 Products/Solutions/Services offered

- 11.1.6.3 Recent developments

- 11.1.7 AWS

- 11.1.7.1 Business overview

- 11.1.7.2 Products/Solutions/Services offered

- 11.1.7.3 Recent developments

- 11.1.8 AT&T

- 11.1.8.1 Business overview

- 11.1.8.2 Products/Solutions/Services offered

- 11.1.9 NOKIA

- 11.1.9.1 Business overview

- 11.1.9.2 Products/Solutions/Services offered

- 11.1.10 ATOS

- 11.1.10.1 Business overview

- 11.1.10.2 Products/Solutions/Services offered

- 11.1.1 SIEMENS

- 11.2 OTHER PLAYERS

- 11.2.1 SAP

- 11.2.2 NEC

- 11.2.3 FUJITSU

- 11.2.4 SCHNEIDER ELECTRIC

- 11.2.5 ALIBABA CLOUD

- 11.2.6 ERICSSON

- 11.2.7 BOSCH.IO

- 11.2.8 ITRON

- 11.2.9 PWC

- 11.2.10 SICE

- 11.3 STARTUPS/SMES

- 11.3.1 THETHINGS.IO

- 11.3.2 KAAIOT TECHNOLOGIES

- 11.3.3 QUANTELA

- 11.3.4 UBICQUIA

- 11.3.5 IGOR

- 11.3.6 75F

- 11.3.7 TELENSA

- 11.3.8 ENEVO

- 11.3.9 KETOS

- 11.3.10 CLEVERCITI

- 11.3.11 GAIA SMART CITIES

- 11.3.12 GLOBETOM

- 11.3.13 TADOOM

- 11.3.14 ATHENA SMART CITIES

12 ADJACENT MARKETS & APPENDIX

- 12.1 INTRODUCTION

- 12.2 SMART CITIES MARKET - GLOBAL FORECAST TO 2030

- 12.2.1 MARKET DEFINITION

- 12.3 SMART INFRASTRUCTURE MARKET - GLOBAL FORECAST TO 2029

- 12.3.1 MARKET DEFINITION

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS