|

시장보고서

상품코드

1804847

XDR(확장형 탐지 및 대응) 시장(-2030년) : 솔루션, 서비스, 공격 대상 영역별Extended Detection and Response (XDR) Market by Solution (Native XDR, Open/Multi-vendor XDR), Service (Managed XDR/XDR as a Service), Attack Surface (Endpoint Detection, Network Detection, Cloud Workload Detection) - Global Forecast to 2030 |

||||||

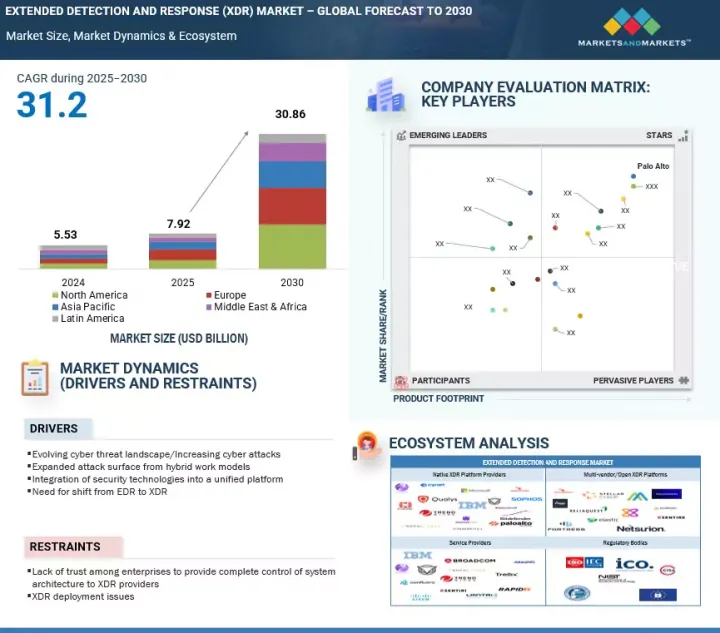

전 세계 XDR(확장형 탐지 및 대응) 시장 규모는 2025년 79억 2,000만 달러에서 예측 기간 동안 CAGR 31.2%로 성장할 것으로 전망되며, 2030년에는 308억 6,000만 달러로 성장할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2019-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러) |

| 부문별 | 제공 구분, 공격 대상 영역, 전개 모드, 조직 규모, 산업, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양 및 기타 지역 |

XDR을 보안 운영에 통합하면 여러 보안 도구를 통합하여 워크플로우를 간소화하고 복잡성을 줄이며 팀 협업을 강화합니다. XDR을 사용하는 조직은 최대 50% 빠른 사고 조사 및 대응을 보고하여 위협 완화 능력을 크게 향상시킵니다. 이러한 운영 효율성 덕분에 SOC 팀은 반복적인 작업보다 우선순위가 높은 위협에 집중할 수 있습니다. 사이버 공격의 규모와 복잡성이 증가함에 따라 SecOps 민첩성 강화에 있어 XDR의 역할이 주요 시장 촉진요인으로 부상하고 있습니다.

"공격 대상 영역별로는 엔드포인트 탐지 부문은 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예상됩니다"

엔드포인트 탐지는 엔드포인트, 클라우드, 네트워크, 신원 신호를 단일 플랫폼으로 통합하여 더 빠르고 정확한 위협 탐지 및 대응을 가능하게 함으로써 장치 수준의 보안을 강화합니다. 이 부문의 솔루션은 복잡하고 진화하는 위협에 대응하기 위해 고급 머신 러닝, 취약점 관리, 공격 표면 축소, 자동화된 조사 기능을 통합합니다.

그 규모와 효율성은 2024년에 있는 플랫폼이 11조건 이상의 IT 이벤트를 처리하고 초당 약 35만 건에 해당하는 이벤트를 처리하면서 심각도가 높은 경보를 자동으로 약 2,000건 봉쇄한 사례에서도 확인할 수 있습니다. PatentPC의 SIEM & XDR Adoption: What the Numbers Say의 조사 결과에 따르면, 보안 전문가의 81%가 엔드포인트 XDR에 의해 감지 속도가 향상되었다고 응답하고, 49%가 툴 통합과 수작업 절감에 의한 비용 절감을 보고하고 있습니다. 통합 가시화, 실시간 분석 및 자동 복구를 제공함으로써 엔드포인트에 특화된 XDR은 조직이 위험을 완화하고 운영을 최적화하며 다양한 장치 환경에서 견고한 보안을 유지할 수 있도록 합니다.

"지역별로는 아시아태평양이 예측 기간 동안 가장 높은 CAGR을 나타낼 전망"

전반에 걸쳐 점점 정교해지는 사이버 위협에 대응하기 위해 기업들이 통합 보안 솔루션을 우선시함에 따라 빠르게 발전하고 있습니다. 싱가포르, 일본, 인도, 호주 등의 국가 정부들은 더 엄격한 사이버 보안 규정과 국가 안보 프레임워크를 도입하며 조직들이 고급 탐지 및 대응 플랫폼을 채택하도록 장려하고 있습니다.

산업용 IoT 구축, 스마트 시티 추진, 5G 네트워크 확산 증가로 새로운 보안 과제가 발생하면서 기업들은 IT, OT, IoT 환경 전반에 실시간 모니터링을 제공하는 XDR 솔루션을 모색하고 있습니다. 최근 발생한 사건들은 이러한 시급성을 강조하는데, 예를 들어 동남아시아에서 " Stately Taurus"와 같은 그룹이 스피어 피싱 및 감염된 USB 장치를 통해 표적 침투를 수행한 사례와 말레이시아 및 싱가포르 기업을 대상으로 한 LockBit의 랜섬웨어 서비스(RaaS) 캠페인이 대표적입니다. 마찬가지로 FatalRAT 피싱 캠페인은 ZIP 첨부 파일, DLL 사이드 로딩, 신뢰할 수 있는 클라우드 서비스를 활용해 방어 체계를 우회하고 민감한 데이터를 탈취하며 대만, 말레이시아, 일본의 여러 산업 분야에 영향을 미쳤습니다. 금융 기관, 의료 서비스 제공자, 통신 사업자들은 특히 XDR을 적극적으로 도입하여 업종별 규정 준수 요건을 충족하고 표적 공격으로부터 핵심 인프라를 보호하고 있습니다.

본 보고서에서는 세계의 XDR(확장형 탐지 및 대응) 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이와 예측, 각종 구분 및 지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요와 업계 동향

- 시장 역학

- 성장 촉진요인

- 억제요인

- 기회

- 과제

- 밸류체인 분석

- 에코시스템

- 특허 분석

- 가격 분석

- 기술 분석

- 사례 연구

- 주요 이해관계자와 구매 기준

- 고객의 사업에 영향을 미치는 동향 및 혼란

- Porter's Five Forces 분석

- 규제 상황

- 주요 회의 및 이벤트(2025-2026년)

- 생성형 AI가 XDR(확장형 탐지 및 대응) 시장에 미치는 영향

- 투자 및 자금조달 시나리오

- 미국 관세 영향(2025년) : 개요

제6장 XDR(확장형 탐지 및 대응) 시장 : 제공 구분별

- 솔루션

- 네이티브 XDR(단일 벤더 XDR)

- 오픈/멀티벤더 XDR

- 서비스

- 전문 서비스

- 관리 서비스

제7장 XDR(확장형 탐지 및 대응) 시장 : 공격 대상 영역별

- 엔드포인트 탐지

- 네트워크 탐지

- 클라우드 워크로드 탐지

- 신원 및 액세스 탐지

- IOT/OT 특유 탐지

제8장 XDR(확장형 탐지 및 대응) 시장 : 전개 모드별

- 클라우드

- 온프레미스

- 하이브리드

제9장 XDR(확장형 탐지 및 대응) 시장 : 조직 규모별

- 대기업

- 중소기업

제10장 XDR(확장형 탐지 및 대응) 시장 : 산업별

- 은행, 금융 서비스, 보험

- 정부

- 제조

- 에너지 및 유틸리티

- 소매 및 전자상거래

- 의료

- IT 및 ITES

- 기타

제11장 XDR(확장형 탐지 및 대응) 시장 : 지역별

- 북미

- 시장 성장 촉진요인

- 거시경제 전망

- 미국

- 캐나다

- 유럽

- 시장 성장 촉진요인

- 거시경제 전망

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타

- 아시아태평양

- 시장 성장 촉진요인

- 거시경제 전망

- 중국

- 일본

- 인도

- 호주

- 기타

- 중동 및 아프리카

- 시장 성장 촉진요인

- 거시경제 전망

- GCC 국가

- 남아프리카

- 기타

- 라틴아메리카

- 시장 성장 촉진요인

- 거시경제 전망

- 브라질

- 멕시코

- 기타

제12장 경쟁 구도

- 개요

- 주요 진입기업의 전략 및 강점

- 수익 분석

- 시장 점유율 분석

- 제품/브랜드 비교

- 기업평가와 재무지표

- 주요 기업용 기업 평가 매트릭스

- 스타스업 및 중소기업용 기업평가 매트릭스

- 경쟁 시나리오

제13장 기업 프로파일

- 주요 기업

- CROWDSTRIKE

- PALO ALTO NETWORKS

- SENTINELONE

- CISCO

- MICROSOFT

- CHECKPOINT

- IBM

- SECUREWORKS

- FORTINET

- BITDEFENDER

- TRELLIX

- TREND MICRO

- QUALYS

- BROADCOM

- SOPHOS

- STELLAR CYBER

- BLUESHIFT CYBERSECURITY

- RAPID7

- EXABEAM

- CYNET SECURITY

- LMNTRIX

- CONFLUERA(XM CYBER)

- NOPALCYBER

- PURPLESEC

- CYBEREASON

- ESENTIRE

- ELASTIC

제14장 인접 시장

제15장 부록

HBR 25.09.12The global Extended Detection and Response (XDR) market size is projected to grow from USD 7.92 billion in 2025 to USD 30.86 billion by 2030 at a Compound Annual Growth Rate (CAGR) of 31.2% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2019-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion) |

| Segments | By Offering, Attack Surface, Deployment Mode, Organization Size, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, and Rest of the World |

Integrating XDR into Security Operations streamlines workflows by unifying multiple security tools, reducing complexity, and enhancing team collaboration. Organizations using XDR report up to 50% faster incident investigation and response, significantly improving threat mitigation. This operational efficiency allows SOC teams to focus on high-priority threats rather than repetitive tasks. As cyberattacks grow in volume and complexity, XDR's role in strengthening SecOps agility is becoming a major market driver.

"By attack surface coverage, the endpoint detection segment accounts for the largest market share during the forecast period."

Endpoint detection enhances device-level security by unifying endpoint, cloud, network, and identity signals into a single platform, enabling faster and more accurate threat detection and response. Solutions in this segment incorporate advanced machine learning, vulnerability management, attack surface reduction, and automated investigation capabilities to address complex and evolving threats. The scale and efficiency of such deployments can be seen in instances where platforms processed over 11 trillion IT events in 2024, equating to roughly 350,000 events per second, while automatically containing nearly 2,000 high-severity alerts. Findings from PatentPC's "SIEM & XDR Adoption: What the Numbers Say" indicate that 81 percent of security professionals experienced faster detection with endpoint XDR, and 49 percent reported cost savings through tool consolidation and reduced manual workloads. By delivering unified visibility, real-time analytics, and automated remediation, endpoint-focused XDR enables organizations to reduce risks, optimize operations, and maintain robust security across diverse device environments.

"By region, Asia Pacific is expected to grow at the highest CAGR during the forecast period."

The Asia Pacific XDR market is advancing rapidly as enterprises prioritize integrated security solutions to counter increasingly sophisticated cyber threats across the region's expanding digital ecosystem. Governments in countries such as Singapore, Japan, India, and Australia are introducing stricter cybersecurity regulations and national security frameworks, encouraging organizations to adopt advanced detection and response platforms. The rise in industrial IoT deployments, smart city initiatives, and 5G network rollouts is creating new security challenges, prompting businesses to seek XDR solutions that can deliver real-time monitoring across IT, OT, and IoT environments. Recent incidents underscore this urgency, such as advanced persistent threat (APT) activity in Southeast Asia by groups like "Stately Taurus," which conducted targeted intrusions via spear-phishing and infected USB devices, and ransomware-as-a-service (RaaS) campaigns by LockBit against organizations in Malaysia and Singapore. Similarly, FatalRAT phishing campaigns have impacted sectors in Taiwan, Malaysia, and Japan, using ZIP attachments, DLL side-loading, and trusted cloud services to bypass defenses and steal sensitive data. Financial institutions, healthcare providers, and telecom operators are particularly active in deploying XDR to meet sector-specific compliance requirements and protect critical infrastructure from targeted attacks.

Breakdown of primaries

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C-level - 40%, Managers & other Levels- 60%

- By Region: North America - 38%, Europe - 26%, Asia Pacific - 21%, Middle East & Africa - 10%, Latin America - 5%

The key players in the Extended Detection and Response (XDR) market include are Palo Alto Networks (US), Microsoft (US), CrowdStrike (US), SentinelOne (US), Trend Micro (Japan), Bitdefender (Romania), IBM (US), Trellix (US), Cisco (US), Sophos (UK), Broadcom (US), Cybereason (US), Elastic (Netherlands), Fortinet (US), eSentire (Canada), Qualys (US), Blueshift (US), Rapid7 (US), Exabeam (US), Cynet Security (US), LMNTRIX (US), Stellar Cyber (US), Confluera (US), NopalCyber (India), PurpleSec (US), and others.

The study includes an in-depth competitive analysis of the key players in the Extended Detection and Response (XDR) market, their company profiles, recent developments, and key market strategies.

Research Coverage

The report segments the Extended Detection and Response (XDR) market and forecasts its size by offering (solutions, services), attack surface (endpoint detection, network detection, cloud workload detection, identity & access detection, IoT/OT-specific detection), deployment mode (on-premises, cloud, hybrid/multi-cloud XDR), organization size (large enterprises, SMEs), vertical (BFSI, government, manufacturing, energy & utilities, retail & e-commerce, healthcare, IT & ITeS, other verticals (education, transport & logistics, and media & entertainment)), and region (North America, Europe, Asia Pacific, RoW).

The study also includes an in-depth competitive analysis of the market's key players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report

The report will help market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall Extended Detection and Response (XDR) market and its subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Evolving cyber threat landscape/Increasing cyber-attacks, Expanded attack surface from hybrid work models, Integration of security technologies into unified platform, Need for shift from EDR to XDR), restraints (Lack of trust among enterprises to provide complete control of system architecture to XDR providers, XDR deployment issues, Privacy and compliance concerns with XDR, High initial deployment costs for full-stack XDR solutions), opportunities (AI and automation integration, Growing XDR needs in small and mid-sized businesses, The integration of XDR into security operations centers, Increasing demand for managed XDR), and challenges (Lack of awareness about XDR and vendor lock-in period, Managing alert fatigue and data overload)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the Extended Detection and Response (XDR) market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the Extended Detection and Response (XDR) market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the Extended Detection and Response (XDR) market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Palo Alto Networks (US), Microsoft (US), CrowdStrike (US), SentinelOne (US), Trend Micro (Japan), Bitdefender (Romania), IBM (US), Trellix (US), Cisco (US), Sophos (UK), Broadcom (US), Cybereason (US), Elastic (Netherlands), Fortinet (US), eSentire (Canada), Qualys (US), Blueshift (US), Rapid7 (US), Exabeam (US), Cynet Security (US), LMNTRIX (US), Stellar Cyber (US), Confluera (US), NopalCyber (India), PurpleSec (US) in the Extended Detection and Response (XDR) market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primary profiles

- 2.1.2.2 Key industry insights

- 2.2 DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.3.3 REVENUE ANALYSIS

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 OVERVIEW OF EXTENDED DETECTION AND RESPONSE MARKET

- 4.2 EXTENDED DETECTION AND RESPONSE MARKET, BY OFFERING

- 4.3 EXTENDED DETECTION AND RESPONSE MARKET, BY ATTACK SURFACE COVERAGE

- 4.4 EXTENDED DETECTION AND RESPONSE MARKET, BY DEPLOYMENT MODE

- 4.5 EXTENDED DETECTION AND RESPONSE MARKET, BY ORGANIZATION SIZE

- 4.6 EXTENDED DETECTION AND RESPONSE MARKET, BY VERTICAL

- 4.7 MARKET INVESTMENT SCENARIO

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Evolving cyber threat landscape/Increasing cyber attacks

- 5.2.1.2 Expanded attack surface from hybrid work models

- 5.2.1.3 Integration of security technologies into unified platforms

- 5.2.1.4 Need for shift from EDR to XDR

- 5.2.1.5 Rising zero-trust adoption

- 5.2.2 RESTRAINTS

- 5.2.2.1 Lack of trust among enterprises to provide complete control of system architecture to XDR providers

- 5.2.2.2 XDR deployment issues

- 5.2.2.3 Privacy and compliance concerns with XDR

- 5.2.2.4 High initial deployment costs for full-stack XDR solutions

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 AI and automation integration

- 5.2.3.2 Growing XDR needs in small and mid-sized businesses

- 5.2.3.3 Integration of XDR into security operations centers

- 5.2.3.4 Increasing demand for managed XDR

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of awareness about XDR and vendor lock-in period

- 5.2.4.2 Managing alert fatigue and data overload

- 5.2.1 DRIVERS

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 PLANNING AND DESIGNING

- 5.3.2 XDR SOLUTION PROVIDERS

- 5.3.3 SYSTEM INTEGRATION

- 5.3.4 CONSULTATION

- 5.3.5 END USERS

- 5.4 ECOSYSTEM

- 5.5 PATENT ANALYSIS

- 5.5.1 LIST OF TOP PATENTS IN EXTENDED DETECTION AND RESPONSE (XDR) MARKET, 2022-2025

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY SOLUTION

- 5.6.2 INDICATIVE PRICING ANALYSIS, BY DEPLOYMENT MODE

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 KEY TECHNOLOGIES

- 5.7.1.1 Endpoint Detection & Response (EDR)

- 5.7.1.2 Network Detection & Response (NDR)

- 5.7.1.3 Cloud Workload Protection Platforms (CWPP)

- 5.7.2 COMPLEMENTARY TECHNOLOGIES

- 5.7.2.1 Security Information and Event Management (SIEM)

- 5.7.2.2 User and Entity Behavior Analytics (UEBA)

- 5.7.2.3 Threat Intelligence Feeds

- 5.7.3 ADJACENT TECHNOLOGIES

- 5.7.3.1 Next-generation Firewalls (NGFW)/Intrusion Detection & Prevention Systems (IDS/IPS)

- 5.7.3.2 Vulnerability Management

- 5.7.3.3 Security Orchestration, Automation, and Response (SOAR)

- 5.7.1 KEY TECHNOLOGIES

- 5.8 CASE STUDIES

- 5.8.1 CISCO ENABLED ELON UNIVERSITY TO STREAMLINE THREAT RESPONSE

- 5.8.2 SABRE'S CYBERSECURITY DEFENSES TAKE OFF, FUELED BY UNIT 42

- 5.8.3 KUWAIT CREDIT BANK BOOSTED THREAT DETECTION AND RESPONSE WITH MICROSOFT DEFENDER XDR

- 5.8.4 XDR ADOPTION ACROSS PRIVATE EQUITY PORTFOLIO FOR STANDARDIZED RISK MANAGEMENT

- 5.9 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.9.2 BUYING CRITERIA

- 5.10 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS

- 5.11 PORTER'S FIVE FORCES ANALYSIS

- 5.11.1 THREAT OF NEW ENTRANTS

- 5.11.2 THREAT OF SUBSTITUTES

- 5.11.3 BARGAINING POWER OF SUPPLIERS

- 5.11.4 BARGAINING POWER OF BUYERS

- 5.11.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.12 REGULATORY LANDSCAPE

- 5.12.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.12.2 KEY REGULATIONS

- 5.12.2.1 Payment Card Industry Data Security Standard (PCI DSS)

- 5.12.2.2 Health Insurance Portability and Accountability Act (HIPAA)

- 5.12.2.3 Federal Information Security Management Act (FISMA)

- 5.12.2.4 Gramm-Leach-Bliley Act (GLBA)

- 5.12.2.5 Sarbanes-Oxley Act (SOX)

- 5.12.2.6 International Organization for Standardization (ISO) Standard 27001

- 5.12.2.7 European Union General Data Protection Regulation (EU GDPR)

- 5.12.2.8 FFIEC Cybersecurity Assessment Tool

- 5.12.2.9 NIST CYBERSECURITY FRAMEWORK

- 5.12.2.10 Defense Federal Acquisition Regulation Supplement (DFARS)

- 5.12.2.11 CSA STAR

- 5.13 KEY CONFERENCES & EVENTS IN 2025-2026

- 5.14 IMPACT OF GENERATIVE AI ON EXTENDED DETECTION AND RESPONSE (XDR) MARKET

- 5.14.1 TOP USE CASES & MARKET POTENTIAL

- 5.14.1.1 Key use cases

- 5.14.2 IMPACT OF GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 5.14.2.1 Security Information and Event Management (SIEM)

- 5.14.2.2 Security Orchestration, Automation, and Response (SOAR)

- 5.14.2.3 Endpoint Detection and Response (EDR)

- 5.14.2.4 Managed Detection and Response (MDR)

- 5.14.1 TOP USE CASES & MARKET POTENTIAL

- 5.15 INVESTMENT AND FUNDING SCENARIO

- 5.16 IMPACT OF 2025 US TARIFF - OVERVIEW

- 5.16.1 INTRODUCTION

- 5.16.2 KEY TARIFF RATES

- 5.16.3 PRICE IMPACT ANALYSIS

- 5.16.4 IMPACT ON COUNTRY/REGION

- 5.16.4.1 North America

- 5.16.4.1.1 United States

- 5.16.4.1.2 Canada

- 5.16.4.1.3 Mexico

- 5.16.4.2 Europe

- 5.16.4.2.1 Germany

- 5.16.4.2.2 France

- 5.16.4.2.3 United Kingdom

- 5.16.4.3 APAC

- 5.16.4.3.1 China

- 5.16.4.3.2 India

- 5.16.4.3.3 Japan

- 5.16.4.1 North America

- 5.16.5 INDUSTRIES

6 EXTENDED DETECTION AND RESPONSE (XDR) MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERING: EXTENDED DETECTION AND RESPONSE MARKET DRIVERS

- 6.2 SOLUTIONS

- 6.2.1 NATIVE XDR (SINGLE VENDOR XDR)

- 6.2.1.1 Rising advanced threats such as targeted attacks, ransomware, and APTs driving market growth

- 6.2.2 OPEN/MULTI-VENDOR XDR

- 6.2.2.1 Open XDR integrates with SIEM, SOAR, and threat intelligence via APIs, giving enterprises customization and vendor-neutral interoperability

- 6.2.1 NATIVE XDR (SINGLE VENDOR XDR)

- 6.3 SERVICES

- 6.3.1 PROFESSIONAL SERVICES

- 6.3.1.1 Rising compliance demands are prompting enterprises to rely on professional services for proper XDR setup and maintenance

- 6.3.1.1.1 Consulting and deployment

- 6.3.1.1.2 Training & education

- 6.3.1.1.3 Integration and support services

- 6.3.1.1 Rising compliance demands are prompting enterprises to rely on professional services for proper XDR setup and maintenance

- 6.3.2 MANAGED SERVICES

- 6.3.2.1 Managed security services and consulting driving adoption of tailored security strategies and continuous risk assessments

- 6.3.1 PROFESSIONAL SERVICES

7 EXTENDED DETECTION AND RESPONSE (XDR) MARKET, BY ATTACK SURFACE COVERAGE

- 7.1 INTRODUCTION

- 7.1.1 ATTACK SURFACE COVERAGE: EXTENDED DETECTION AND RESPONSE (XDR) MARKET DRIVERS

- 7.2 ENDPOINT DETECTION

- 7.2.1 SURGE IN RANSOMWARE TARGETING ENDPOINTS, WITH MOST ATTACKS ORIGINATING FROM COMPROMISED USER DEVICES, ACCELERATING ENDPOINT-FOCUSED XDR ADOPTION

- 7.3 NETWORK DETECTION

- 7.3.1 PROLIFERATION OF IOT AND EDGE DEVICES TO EXPAND EAST-WEST TRAFFIC, DEMANDING NETWORK-CENTRIC DETECTION INTEGRATED INTO XDR

- 7.4 CLOUD WORKLOAD DETECTION

- 7.4.1 GROWTH OF MULTI-CLOUD AND HYBRID DEPLOYMENTS INCREASES COMPLEXITY, DRIVING ADOPTION OF XDR TO UNIFY VISIBILITY ACROSS ENVIRONMENTS

- 7.5 IDENTITY & ACCESS DETECTION

- 7.5.1 CREDENTIAL THEFT TO REMAIN LEADING INITIAL ACCESS VECTOR IN GLOBAL BREACHES, MAKING IDENTITY DETECTION WITHIN XDR CRITICAL

- 7.6 IOT/OT SPECIFIC DETECTION

- 7.6.1 INCREASING ATTACKS ON OT SYSTEMS IN MANUFACTURING, ENERGY, AND UTILITIES DRIVING CROSS-DOMAIN MONITORING NEEDS

8 EXTENDED DETECTION AND RESPONSE (XDR) MARKET, BY DEPLOYMENT MODE

- 8.1 INTRODUCTION

- 8.1.1 DEPLOYMENT MODE: EXTENDED DETECTION AND RESPONSE (XDR) MARKET DRIVERS

- 8.2 CLOUD

- 8.2.1 COST-EFFECTIVENESS AND EASE OF SECURING APPLICATIONS ON CLOUD TO BOOST MARKET

- 8.3 ON-PREMISES

- 8.3.1 COMPLETE CONTROL OVER PLATFORMS, SYSTEMS, AND DATA TO BOOST DEMAND FOR ON-PREMISES SOLUTIONS

- 8.4 HYBRID

- 8.4.1 HYBRID XDR ENABLES PHASED MIGRATION, ENSURING BUSINESS CONTINUITY AND CONSISTENT SECURITY AS ENTERPRISES SHIFT LEGACY WORKLOADS TO CLOUD

9 EXTENDED DETECTION AND RESPONSE (XDR) MARKET, BY ORGANIZATION SIZE

- 9.1 INTRODUCTION

- 9.1.1 ORGANIZATION SIZE: EXTENDED DETECTION AND RESPONSE (XDR) MARKET DRIVERS

- 9.2 LARGE ENTERPRISES

- 9.2.1 SOPHISTICATED ATTACKERS TARGET HIGH-VALUE INTELLECTUAL PROPERTY AND SENSITIVE CUSTOMER DATA, DRIVING LARGE FIRMS TOWARD PROACTIVE, AI-DRIVEN THREAT DETECTION

- 9.3 SMALL & MEDIUM-SIZED ENTERPRISES (SMES)

- 9.3.1 SMES FACE RISING RANSOMWARE AND PHISHING CAMPAIGNS, WITH LIMITED IN-HOUSE SOC EXPERTISE, MAKING XDR'S MANAGED AND AUTOMATED DETECTION HIGHLY ATTRACTIVE

10 EXTENDED DETECTION AND RESPONSE, BY VERTICAL

- 10.1 INTRODUCTION

- 10.1.1 VERTICAL: EXTENDED DETECTION AND RESPONSE (XDR) MARKET DRIVERS

- 10.2 BANKING, FINANCIAL SERVICES, AND INSURANCE

- 10.2.1 RISING FRAUD, PHISHING, AND RANSOMWARE CAMPAIGNS AGAINST FINANCIAL INSTITUTIONS DRIVING ADOPTION OF XDR

- 10.3 GOVERNMENT

- 10.3.1 GOVERNMENTS FACE STATE-SPONSORED CYBERATTACKS AIMED AT CRITICAL INFRASTRUCTURE, DEFENSE, AND CITIZEN DATA, ACCELERATING XDR ADOPTION FOR NATIONAL RESILIENCE

- 10.4 MANUFACTURING

- 10.4.1 SUPPLY CHAIN VULNERABILITIES AND THIRD-PARTY RISKS PUSHING MANUFACTURERS TO DEPLOY ADVANCED DETECTION SOLUTIONS

- 10.5 ENERGY & UTILITIES

- 10.5.1 NATIONAL SECURITY CONCERNS AND CRITICAL INFRASTRUCTURE PROTECTION POLICIES PROMPTING LARGE-SCALE INVESTMENT IN DETECTION SOLUTIONS

- 10.6 RETAIL & E-COMMERCE

- 10.6.1 INCREASING E-COMMERCE GROWTH EXPANDS ATTACK SURFACE WITH CLOUD AND CUSTOMER-FACING PLATFORMS, REQUIRING XDR-LEVEL CORRELATION AND MONITORING

- 10.7 HEALTHCARE

- 10.7.1 ADOPTION OF TELEHEALTH, IOT DEVICES, AND CONNECTED MEDICAL SYSTEMS WIDENS VULNERABILITIES, DRIVING DEMAND FOR XDR'S HOLISTIC VISIBILITY

- 10.8 IT & ITES

- 10.8.1 INCREASING DEMAND FOR MITIGATION OF FRAUDULENT ACTIVITIES AND PROTECTION OF CUSTOMER INTERESTS TO FOSTER MARKET GROWTH

- 10.9 OTHER VERTICALS

11 EXTENDED DETECTION AND RESPONSE MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: MARKET DRIVERS

- 11.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 11.2.3 US

- 11.2.3.1 Presence of several XDR vendors to drive adoption of XDR solutions

- 11.2.4 CANADA

- 11.2.4.1 Government initiatives to drive adoption of XDR for defending against cyberattacks within networks

- 11.3 EUROPE

- 11.3.1 EUROPE: MARKET DRIVERS

- 11.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 11.3.3 UK

- 11.3.3.1 UK being prone to most cybersecurity attacks in Europe to drive XDR market

- 11.3.4 GERMANY

- 11.3.4.1 High cybersecurity maturity and advanced digital infrastructure driving XDR adoption

- 11.3.5 FRANCE

- 11.3.5.1 Rising cyberattacks, including ransomware and data breaches, driving adoption of advanced security solutions

- 11.3.6 ITALY

- 11.3.6.1 Italy's push toward digitalization in public and private sectors increases exposure to cyber threats, driving need for advanced security solutions

- 11.3.7 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: MARKET DRIVERS

- 11.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 11.4.3 CHINA

- 11.4.3.1 Technological advancements in China to drive XDR adoption

- 11.4.4 JAPAN

- 11.4.4.1 Initial adoption of high-end technology, such as XDR, to help cybersecurity developments in Japan

- 11.4.5 INDIA

- 11.4.5.1 Increasing losses due to cyber-attacks to boost demand for XDR solutions

- 11.4.6 AUSTRALIA

- 11.4.6.1 Stringent regulations and mandates initiatives to drive market growth

- 11.4.7 REST OF ASIA PACIFIC

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 MIDDLE EAST & AFRICA: MARKET DRIVERS

- 11.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 11.5.3 GCC COUNTRIES

- 11.5.3.1 KSA

- 11.5.3.2 UAE

- 11.5.3.3 Rest of GCC countries

- 11.5.4 SOUTH AFRICA

- 11.5.4.1 Rising ransomware attacks to drive demand for advanced cybersecurity solutions

- 11.5.5 REST OF MIDDLE EAST & AFRICA

- 11.6 LATIN AMERICA

- 11.6.1 LATIN AMERICA: MARKET DRIVERS

- 11.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 11.6.3 BRAZIL

- 11.6.3.1 Cyber-attacks in Brazil driving cybersecurity demand, which, in turn, will drive demand for XDR solutions

- 11.6.4 MEXICO

- 11.6.4.1 Various global XDR vendors to put efforts to grow in Mexican marketspace

- 11.6.5 REST OF LATIN AMERICA

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS

- 12.4 MARKET SHARE ANALYSIS

- 12.5 PRODUCT/BRAND COMPARISON

- 12.5.1 CROWDSTRIKE

- 12.5.2 PALO ALTO NETWORKS

- 12.5.3 SENTINELONE

- 12.5.4 MICROSOFT

- 12.5.5 CISCO

- 12.6 COMPANY VALUATION AND FINANCIAL METRICS

- 12.6.1 COMPANY VALUATION, 2025

- 12.6.2 FINANCIAL METRICS USING EV/EBIDTA

- 12.7 COMPANY EVALUATION MATRIX FOR KEY PLAYERS, 2024

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.5.1 Company Footprint

- 12.7.5.2 Offering Footprint

- 12.7.5.3 Deployment Mode Footprint

- 12.7.5.4 Region Footprint

- 12.7.5.5 Vertical Footprint

- 12.8 COMPANY EVALUATION MATRIX FOR STARTUPS/SMES, 2024

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.2 Competitive benchmarking of key startups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES AND PRODUCT ENHANCEMENTS

- 12.9.2 DEALS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 CROWDSTRIKE

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches/developments

- 13.1.1.3.2 Deals

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 PALO ALTO NETWORKS

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches/developments

- 13.1.2.3.2 Deals

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 SENTINELONE

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches/developments

- 13.1.3.3.2 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 CISCO

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches/developments

- 13.1.4.3.2 Deals

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 MICROSOFT

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Deals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Key strengths

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 CHECKPOINT

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches/developments

- 13.1.6.3.2 Deals

- 13.1.7 IBM

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches/developments

- 13.1.7.3.2 Deals

- 13.1.8 SECUREWORKS

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product launches/developments

- 13.1.8.3.2 Deals

- 13.1.9 FORTINET

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Deals

- 13.1.10 BITDEFENDER

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product launches/developments

- 13.1.10.3.2 Deals

- 13.1.11 TRELLIX

- 13.1.11.1 Business overview

- 13.1.11.2 Products/Solutions/Services offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Product launches/developments

- 13.1.11.3.2 Deals

- 13.1.12 TREND MICRO

- 13.1.12.1 Business overview

- 13.1.12.2 Products/Solutions/Services offered

- 13.1.12.3 Recent developments

- 13.1.12.3.1 Product launches/developments

- 13.1.13 QUALYS

- 13.1.13.1 Business overview

- 13.1.13.2 Products/Solutions/Services offered

- 13.1.14 BROADCOM

- 13.1.14.1 Business overview

- 13.1.14.2 Products/Solutions/Services offered

- 13.1.14.3 Recent developments

- 13.1.14.3.1 Product launches/developments

- 13.1.14.3.2 Deals

- 13.1.15 SOPHOS

- 13.1.15.1 Business overview

- 13.1.15.2 Products/Solutions/Services offered

- 13.1.15.3 Recent developments

- 13.1.15.3.1 Deals

- 13.1.16 STELLAR CYBER

- 13.1.16.1 Business overview

- 13.1.16.2 Products/Solutions/Services offered

- 13.1.16.3 Recent developments

- 13.1.16.3.1 Product launches/developments

- 13.1.16.3.2 Deals

- 13.1.17 BLUESHIFT CYBERSECURITY

- 13.1.18 RAPID7

- 13.1.19 EXABEAM

- 13.1.20 CYNET SECURITY

- 13.1.21 LMNTRIX

- 13.1.22 CONFLUERA (XM CYBER)

- 13.1.23 NOPALCYBER

- 13.1.24 PURPLESEC

- 13.1.25 CYBEREASON

- 13.1.26 ESENTIRE

- 13.1.27 ELASTIC

- 13.1.1 CROWDSTRIKE

14 ADJACENT MARKETS

- 14.1 LIMITATIONS

- 14.2 MANAGED DETECTION AND RESPONSE MARKET

- 14.3 ENDPOINT SECURITY MARKET

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS