|

시장보고서

상품코드

1804848

진공 증발기 시장 : 기술별, 용도별, 최종 이용 산업별, 지역별 예측(-2030년)Vacuum Evaporators Market by Technology (Heat Pump, Mechanical Vapor Recompression, Thermal), Application (Wastewater Treatment, Product Processing), End-use Industry (Food & Beverage, Pharmaceutical) and Region - Global Forecast to 2030 |

||||||

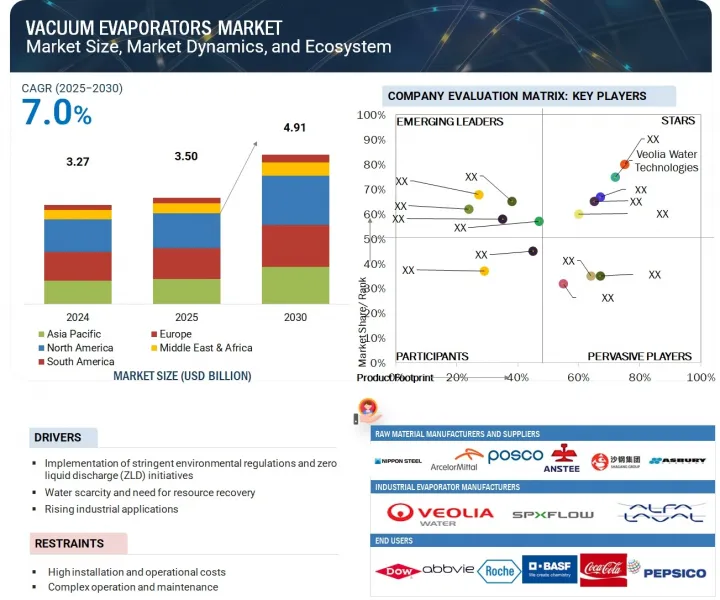

세계의 진공 증발기 시장 규모는 2025년 35억 달러에서 2030년까지 49억 1,000만 달러에 이를 것으로 예측되며, 예측 기간에 CAGR 7.0%로 성장할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2020-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 100만 달러, 톤 |

| 부문 | 기술, 용도, 최종 이용 산업, 용량, 설치 유형, 지역 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 중동, 아프리카, 남미 |

식품 및 음료, 제약, 화학, 폐수 처리 등 다양한 산업 분야에서 효율적인 열 분리 공정에 대한 수요가 증가하고 있습니다. 산업화의 확대와 효과적인 농축, 정제, 용매 회수 솔루션에 대한 필요성이 높아지면서 첨단 증발기 시스템의 도입이 증가하고 있습니다.

"제품 처리 응용 분야가 예측 기간 동안 두 번째로 큰 시장 점유율을 차지할 전망 "

제품 처리 부문은 진공 증발기 시장에서 두 번째로 큰 점유율을 차지할 것으로 예상됩니다. 이는 농축, 정제, 용매 회수가 생산의 핵심 단계인 식품 및 음료, 제약, 화학 산업에서 중요한 역할을 하기 때문입니다. 진공 증발기는 일반적으로 제품 처리 과정에서 민감한 재료에서 물이나 용매를 저온으로 제거하는 데 사용되어 제품 품질, 일관성, 화학적 또는 영양적 무결성을 유지하는 데 도움을 줍니다. 이는 유제품, 과일 농축액, 활성 제약 성분(API), 특수 화학 물질과 같은 열에 민감한 물질에 특히 중요합니다. 또한 진공 증발기는 증발 속도를 정밀하게 제어하고 공정 효율을 개선하며 에너지 소비를 줄여 연속 생산 환경에서 가치가 높습니다. 다양한 산업 전반에 걸친 고순도 및 고농축 제품에 대한 수요 증가와 공정 최적화 및 지속 가능성 분야의 발전은 제품 처리 응용 분야에서 진공 증발기의 광범위한 채택을 촉진하고 있습니다.

"열펌프 기술 부문, 예측 기간 중 두 번째로 큰 시장 점유율 차지할 전망 "

열펌프 진공 증발기는 에너지 효율성, 중소 용량 응용 분야 적합성, 중소규모 산업에서의 광범위한 사용으로 인해 시장에서 두 번째로 큰 점유율을 차지할 것으로 예상됩니다. 이러한 시스템은 열펌프를 활용하여 증발 사이클 내에서 열에너지를 재활용함으로써 기존 열 증발기에 비해 에너지 소비를 크게 낮춥니다. 이로 인해 금속 마감, 전자, 섬유, 소규모 식품 가공 등 중간 수준의 폐수 발생량을 가진 산업에 비용 효율적이고 환경 친화적인 선택지가 됩니다. 열펌프 진공 증발기는 또한 컴팩트한 설계, 낮은 작동 온도, 최소한의 유지보수로 복잡한 폐수 흐름을 처리할 수 있는 능력으로 선호됩니다. 특히 엄격한 폐수 배출 제한과 상승하는 에너지 가격을 가진 지역에서 환경 규제 충족, 처리 비용 절감, 물 재사용 촉진 필요성에 의해 채택이 증가하고 있습니다.

이 보고서는 세계의 진공 증발기 시장에 대한 조사 분석을 통해 주요 촉진요인과 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요한 지견

- 진공 증발기 시장에서의 매력적인 기회

- 진공 증발기 시장 : 지역별

- 북미의 진공 증발기 시장 : 최종 이용 산업별, 국가별

- 진공 증발기 시장 : 주요 국가

제5장 시장 개요

- 소개

- 시장 역학

- 성장 촉진요인

- 억제요인

- 기회

- 과제

- Porter's Five Forces 분석

- 주요 이해관계자와 구매 기준

- 밸류체인 분석

- 진공 증발기 시장의 에코시스템

- 특허 분석

- 조사 방법

- 특허 공보의 동향

- 고찰

- 관할분석

- 사례 연구 분석

- 특수 화학제품 기업용 다중효용 증발기

- ENCON의 열식 증발기를 사용한 매립지 침출수의 최소화

- 무역 분석

- 수입 시나리오

- 수출 시나리오

- 주요 컨퍼런스 및 이벤트(2025-2026년)

- 규제 상황

- 기술 분석

- 인접 기술

- 결정화기

- 건조기(예 : 스프레이 건조기, 드럼 건조기)

- 보완 기술

- 동향 및 파괴적 변화의 영향

- 세계의 거시경제 전망

- 진공 증발기 시장의 미국 관세 영향(2025년)

- 주요 관세율

- 가격의 영향 분석

- 국가 및 지역에 미치는 영향

- 용도에 미치는 영향

- 진공 증발기 시장에서의 AI의 영향

제6장 진공 증발기 시장 : 기술별

- 소개

- 열펌프 진공 증발기

- MVR 진공 증발기

- 열식 진공 증발기

제7장 진공 증발기 시장 : 용도별

- 소개

- 폐수 처리

- 제품 처리

- 기타 용도

제8장 진공 증발기 시장 : 용량별

- 소개

- 소규모(100리터/시 이하)

- 중규모(100-500리터/시)

- 대규모(500리터/시 초과)

제9장 진공 증발기 시장 : 설치별

- 소개

- 신규 설치

- 개조 설치

제10장 진공 증발기 시장 : 최종 이용 산업별

- 소개

- 화학제품 및 석유화학제품

- 전자 및 반도체

- 에너지 및 전력

- 식품 및 음료

- 제약

- 자동차

- 기타 최종 이용 산업

제11장 진공 증발기 시장 : 지역별

- 소개

- 아시아태평양

- 중국

- 한국

- 일본

- 인도

- 말레이시아

- 호주

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 러시아

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 중동 및 아프리카

- GCC 국가

- 이스라엘

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 아르헨티나

- 브라질

- 칠레

- 기타 남미

제12장 경쟁 구도

- 소개

- 주요 참가 기업의 전략 및 강점(2020-2025년)

- 수익 분석

- 수익 분석(2020-2024년)

- 시장 점유율 분석(2024년)

- 브랜드 및 제품 비교

- VEOLIA WATER TECHNOLOGIES(VEOLIA GROUP)

- GEA GROUP AKTIENGESELLSCHAFT

- SPX FLOW INC

- ALFA LAVAL

- CONDORCHEM ENVIRO SOLUTIONS

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업의 평가 매트릭스 : 스타스업 및 중소기업(2024년)

- 기업 평가 및 재무 지표

- 경쟁 시나리오

제13장 기업 프로파일

- 주요 기업

- VEOLIA WATER TECHNOLOGIES(VEOLIA GROUP)

- ALFA LAVAL

- GEA GROUP AKTIENGESELLSCHAFT

- SPX FLOW, INC.

- CONDORCHEM ENVIRO SOLUTIONS

- ECO-TECHNO SRL

- H2O GMBH

- DE DIETRICH

- BUCHER UNIPEKTIN

- SASAKURA ENGINEERING CO, LTD.

- PRAJ INDUSTRIES

- SANSHIN MFG. CO., LTD.

- SALTWORKS TECHNOLOGIES INC.

- ZHEJIANG TAIKANG EVAPORATOR CO., LTD

- BELMAR TECHNOLOGIES

- HEBEI LEHENG ENERGY SAVING EQUIPMENT CO. LTD.

- UNITOP AQUACARE LIMITED

- GMM PFAUDLER

- 기타 기업

- 3V TECH SPA

- VILOKEN RECYCLING TECH

- SAMSCO

- 3R TECHNOLOGY

- KOVOFINIS

- ENCON EVAPORATORS

- SAITA SRL

- KMU LOFT CLEANWATER SE

- TETRA PAK INTERNATIONAL SA

- PROCECO LTD.

- CFT SPA

제14장 인접 시장과 관련 시장

- 소개

- 제한 사항

- 상호연결 시장

- 무배수(ZLD) 시스템 시장 : 시스템별

- 기존식

- 하이브리드

제15장 부록

HBR 25.09.12The global vacuum evaporators market is projected to grow from USD 3.50 billion in 2025 to USD 4.91 billion by 2030, at a CAGR of 7.0% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Ton) |

| Segments | Technology, Application, End-use Industry, Capacity, Installation Type, and Region |

| Regions covered | Asia Pacific, Europe, North America, the Middle East & Africa, and South America |

There is a rising demand for efficient thermal separation processes across industries such as food and beverage, pharmaceuticals, chemicals, and wastewater treatment. Growing industrialization and the need for effective concentration, purification, and solvent recovery solutions are increasing the adoption of advanced evaporator systems.

"Product processing application segment to account for second-largest market share during forecast period"

The product processing segment is projected to hold the second-largest share in the vacuum evaporators market because of its vital role in industries like food & beverage, pharmaceuticals, and chemicals, where concentration, purification, and solvent recovery are key steps in production. Vacuum evaporators are commonly used in product processing to remove water or solvents from sensitive materials at low temperatures, helping to preserve product quality, consistency, and chemical or nutritional integrity. This is especially important for heat-sensitive substances such as dairy products, fruit concentrates, active pharmaceutical ingredients (APIs), and specialty chemicals. Moreover, vacuum evaporators allow for precise control over evaporation rates, improve process efficiency, and reduce energy consumption, making them valuable in continuous production settings. The rising demand for high-purity and concentrated products across different industries and advancements in process optimization and sustainability fuel the widespread adoption of vacuum evaporators in product processing applications.

"Heat pump technology segment to account for second-largest market share during forecast period"

Heat pump vacuum evaporators are estimated to hold the second-largest share in the market because of their energy efficiency, suitability for low- to medium-capacity applications, and widespread use in small and medium-sized industries. These systems utilize a heat pump to recycle thermal energy within the evaporation cycle, significantly lowering energy consumption compared to traditional thermal evaporators. This makes them a cost-effective and environmentally friendly choice for industries with moderate wastewater volumes, such as metal finishing, electronics, textiles, and small-scale food processing. Heat pump vacuum evaporators are also preferred for their compact design, low operating temperatures, and ability to treat complex wastewater streams with minimal maintenance. Their growing adoption is driven by the need to meet environmental regulations, reduce disposal costs, and promote water reuse, especially in regions with strict wastewater discharge limits and rising energy prices.

Profile break-up of primary participants for the report:

- By Company Type: Tier 1 - 40%, Tier 2 - 35%, and Tier 3 - 25%

- By Designation: C-level- 30%, Director Level- 40%, and Others - 30%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 35%, South America - 5%, and Middle East & Africa - 5%

Veolia Water Technologies (France), SPX Flow Inc. (US), Alfa Laval (Sweden), Condorchem Enviro Solutions (Spain), and GEA Group AG (Germany) are some of the major players in the vacuum evaporators market. These players have adopted acquisitions, expansions, partnerships, and agreements to increase their market share and business revenue.

Research Coverage

The report defines, segments, and projects the vacuum evaporators market based on technology, application, end-use industry, capacity, installation type, and region. It provides detailed information about the major factors influencing the market's growth, such as drivers, restraints, opportunities, and challenges. It strategically profiles vacuum evaporator manufacturers, thoroughly analyzes their market shares and core competencies, and tracks and examines competitive developments they undertake in the market, such as expansions, partnerships, and product launches.

Reasons to Buy Report

The report is expected to assist both market leaders and new entrants by providing them with the closest estimates of revenue figures for the vacuum evaporators market and its segments. It also aims to help stakeholders better understand the market's competitive landscape, gather insights to enhance their business position, and develop effective go-to-market strategies. Additionally, it enables stakeholders to understand the market's pulse and provide them with information on key drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (Implementation of stringent environmental regulations and zero liquid discharge (ZLD) initiatives, water scarcity and the need for resource recovery, expanding industrial applications), restraints (High installation and operational costs of vacuum evaporators, complex operation and maintenance), opportunities (Support for green chemistry initiatives, Technological advancements and energy-efficient designs, Increased investment in food safety and quality and increasing urbanization and municipal wastewater treatment), and challenges (Technical complexity and need for skilled labor, competitive from alternative technologies) influencing the growth of the vacuum evaporators market.

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities in the vacuum evaporators market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the vacuum evaporators market across varied regions.

- Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the industrial market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as Veolia Water Technologies (France), SPX Flow, Inc. (US), Condorchem Enviro Solutions (Spain), Eco-Techno Srl (Italy), GEA Group Aktiengesellschaft (Germany), H2O GmbH (Germany), De Dietrich (US), Bucher Unipektin (Switzerland), Alfa Laval (Sweden), Sasakura Engineering Co., Ltd. (Japan), Praj Industries (India), and Sanshin Mfg. Co., Ltd. (Japan), Saltworks Technologies Inc. (Canada), Zhejiang Taikang Evaporator Co., Ltd. (China), Belmar Technologies (England), Hebei Leheng Energy Saving Equipment Co., Ltd. (China), Unitop Aquacare Limited (India), and GMM Pfaudler (India) in the vacuum evaporators market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.3.3 CURRENCY CONSIDERED

- 1.3.4 UNITS CONSIDERED

- 1.3.5 INCLUSIONS & EXCLUSIONS

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.2.3 Breakdown of interviews with experts

- 2.1.2.4 List of participating companies for primary research

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 BASE NUMBER CALCULATION

- 2.3.1 SUPPLY-SIDE APPROACH

- 2.4 DATA TRIANGULATION

- 2.5 GROWTH RATE ASSUMPTIONS/GROWTH FORECAST

- 2.6 ASSUMPTIONS

- 2.7 RISK ASSESSMENT

- 2.8 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES IN VACUUM EVAPORATORS MARKET

- 4.2 VACUUM EVAPORATORS MARKET, BY REGION

- 4.3 NORTH AMERICA VACUUM EVAPORATORS MARKET, BY END-USE INDUSTRY AND COUNTRY

- 4.4 VACUUM EVAPORATORS MARKET: MAJOR COUNTRIES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Implementation of stringent environmental regulations and zero liquid discharge (ZLD) initiatives

- 5.2.1.2 Water scarcity and need for resource recovery

- 5.2.1.3 Expanding industrial applications

- 5.2.2 RESTRAINTS

- 5.2.2.1 High installation and operational costs of vacuum evaporators

- 5.2.2.2 Complex operation and maintenance

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Support for green chemistry initiatives

- 5.2.3.2 Technological advancements and energy-efficient designs

- 5.2.3.3 Increased investment in food safety and quality and increasing urbanization and municipal wastewater treatment

- 5.2.4 CHALLENGES

- 5.2.4.1 Technical complexity and need for skilled labor

- 5.2.4.2 Competition from alternative technologies

- 5.2.1 DRIVERS

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 BARGAINING POWER OF SUPPLIERS

- 5.3.2 BARGAINING POWER OF BUYERS

- 5.3.3 THREAT OF SUBSTITUTES

- 5.3.4 THREAT OF NEW ENTRANTS

- 5.3.5 DEGREE OF COMPETITION

- 5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.4.2 BUYING CRITERIA

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 ECOSYSTEM FOR VACUUM EVAPORATORS MARKET

- 5.7 PATENT ANALYSIS

- 5.7.1 METHODOLOGY

- 5.7.2 PATENT PUBLICATION TRENDS

- 5.7.3 INSIGHTS

- 5.7.4 JURISDICTION ANALYSIS

- 5.7.4.1 LIST OF MAJOR PATENTS

- 5.8 CASE STUDY ANALYSIS

- 5.8.1 MULTIPLE EFFECT EVAPORATOR FOR SPECIALTY CHEMICALS COMPANY

- 5.8.1.1 Objective

- 5.8.1.2 Challenge

- 5.8.1.3 Solution statement

- 5.8.1.4 Result

- 5.8.2 LANDFILL LEACHATE MINIMIZATION USING AN ENCON THERMAL EVAPORATOR

- 5.8.2.1 Objective

- 5.8.2.2 Challenge

- 5.8.2.3 Solution statement

- 5.8.2.4 Result

- 5.8.1 MULTIPLE EFFECT EVAPORATOR FOR SPECIALTY CHEMICALS COMPANY

- 5.9 TRADE ANALYSIS

- 5.9.1 IMPORT SCENARIO

- 5.9.2 EXPORT SCENARIO

- 5.10 KEY CONFERENCES & EVENTS IN 2025-2026

- 5.11 REGULATORY LANDSCAPE

- 5.11.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.12 TECHNOLOGY ANALYSIS

- 5.12.1 KEY TECHNOLOGIES

- 5.12.1.1 Vacuum evaporator technology

- 5.12.1 KEY TECHNOLOGIES

- 5.13 ADJACENT TECHNOLOGIES

- 5.13.1 CRYSTALLIZERS

- 5.13.2 DRYERS (E.G., SPRAY DRYERS, DRUM DRYERS)

- 5.14 COMPLEMENTARY TECHNOLOGIES

- 5.14.1 WASTE HEAT RECOVERY UNITS

- 5.15 TRENDS/DISRUPTION IMPACT

- 5.16 GLOBAL MACROECONOMIC OUTLOOK

- 5.16.1 GDP

- 5.17 IMPACT OF 2025 US TARIFF - VACUUM EVAPORATORS MARKET

- 5.17.1 KEY TARIFF RATES

- 5.17.2 PRICE IMPACT ANALYSIS

- 5.17.3 IMPACT ON COUNTRY/REGION

- 5.17.3.1 Us

- 5.17.3.2 Europe

- 5.17.3.3 Asia Pacific

- 5.17.4 IMPACT ON APPLICATIONS

- 5.17.4.1 Pharmaceutical

- 5.17.4.2 Chemical & petrochemical

- 5.17.4.3 Electronics & semiconductor

- 5.17.4.4 Energy & power

- 5.17.4.5 Food & beverage

- 5.17.4.6 Automotive

- 5.17.4.7 Other applications

- 5.18 IMPACT OF ARTIFICIAL INTELLIGENCE (AI) ON VACUUM EVAPORATOR MARKET

6 VACUUM EVAPORATORS MARKET, BY TYPE OF TECHNOLOGY

- 6.1 INTRODUCTION

- 6.2 HEAT PUMP VACUUM EVAPORATORS

- 6.2.1 STRINGENT ENVIRONMENTAL REGULATIONS TO DRIVE MARKET

- 6.3 MECHANICAL VAPOR RECOMPRESSION VACUUM EVAPORATORS

- 6.3.1 RISING FOCUS ON SUSTAINABLE AND CIRCULAR PROCESSES

- 6.4 THERMAL VACUUM EVAPORATORS

- 6.4.1 EFFECTIVE FOR HIGH-SALINITY AND HIGH-CONTAMINANT WASTEWATER

7 VACUUM EVAPORATORS MARKET, BY APPLICATION

- 7.1 INTRODUCTION

- 7.2 WASTEWATER TREATMENT

- 7.2.1 RISING ADOPTION OF ZERO LIQUID DISCHARGE (ZLD) SYSTEMS

- 7.3 PRODUCT PROCESSING

- 7.3.1 GROWTH IN WATER-INTENSIVE INDUSTRIES

- 7.4 OTHER APPLICATIONS

8 VACUUM EVAPORATORS MARKET, BY CAPACITY

- 8.1 INTRODUCTION

- 8.2 SMALL SCALE (UP TO 100 LITERS/HOUR)

- 8.2.1 GROWING ADOPTION BY SMES AND LABORATORIES TO DRIVE MARKET

- 8.3 MEDIUM SCALE (100-500 LITERS/HOUR)

- 8.3.1 INCREASING DEMAND FROM MID-SIZED MANUFACTURING AND PROCESSING INDUSTRIES

- 8.4 LARGE SCALE (ABOVE 500 LITERS/HOUR)

- 8.4.1 EXPANSION OF INDUSTRIAL INFRASTRUCTURE AND MEGA PROJECTS IN EMERGING ECONOMIES

9 VACUUM EVAPORATORS MARKET, BY INSTALLATION

- 9.1 INTRODUCTION

- 9.2 NEW INSTALLATION

- 9.2.1 FOCUS ON WATER REUSE AND RECYCLING IN GREENFIELD PROJECTS TO DRIVE MARKET

- 9.3 RETROFIT INSTALLATION

- 9.3.1 NEED FOR UPGRADING AGING INFRASTRUCTURE

10 VACUUM EVAPORATORS MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- 10.2 CHEMICAL & PETROCHEMICAL

- 10.2.1 HIGH WATER CONSUMPTION AND COMPLEX WASTEWATER STREAMS TO DRIVE MARKET

- 10.3 ELECTRONICS & SEMICONDUCTOR

- 10.3.1 HIGH DEMAND FOR ULTRAPURE WATER (UPW) TO DRIVE GROWTH

- 10.4 ENERGY & POWER

- 10.4.1 NEED FOR EFFICIENT WASTEWATER TREATMENT

- 10.5 FOOD & BEVERAGE

- 10.5.1 GROWING DEMAND FOR PROCESSED AND SHELF-STABLE PRODUCTS

- 10.6 PHARMACEUTICAL

- 10.6.1 PRODUCT QUALITY AND STABILITY TO DRIVE MARKET

- 10.7 AUTOMOTIVE

- 10.7.1 GENERATION OF COMPLEX EFFLUENTS TO DRIVE MARKET

- 10.8 OTHER END-USE INDUSTRIES

11 VACUUM EVAPORATORS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 ASIA PACIFIC

- 11.2.1 CHINA

- 11.2.1.1 Growing manufacturing hub to drive market

- 11.2.2 SOUTH KOREA

- 11.2.2.1 Growing electronics and automobile sectors to create opportunities

- 11.2.3 JAPAN

- 11.2.3.1 Rising demand driven by sustainability and technological innovation to drive market

- 11.2.4 INDIA

- 11.2.4.1 Initiative in food & beverage industries to generate demand

- 11.2.5 MALAYSIA

- 11.2.5.1 Expanding manufacturing sector to create opportunities

- 11.2.6 AUSTRALIA

- 11.2.6.1 High demand for vacuum evaporators in food & beverage sector to drive market

- 11.2.7 REST OF ASIA PACIFIC

- 11.2.1 CHINA

- 11.3 NORTH AMERICA

- 11.3.1 US

- 11.3.1.1 Regulatory and industrial demand to drive market

- 11.3.2 CANADA

- 11.3.2.1 Industrial expansion to create demand for vacuum evaporators

- 11.3.3 MEXICO

- 11.3.3.1 Economic & policy support to drive market

- 11.3.1 US

- 11.4 EUROPE

- 11.4.1 GERMANY

- 11.4.1.1 Pharmaceutical production and automotive industry to support market growth

- 11.4.2 UK

- 11.4.2.1 Rising demand for vacuum evaporators in electrical & electronics industry

- 11.4.3 RUSSIA

- 11.4.3.1 Growth in food & beverage industry to increase demand

- 11.4.4 FRANCE

- 11.4.4.1 Water treatment infrastructure to drive demand

- 11.4.5 ITALY

- 11.4.5.1 Growth in pharmaceutical and automotive industries to increase demand

- 11.4.6 SPAIN

- 11.4.6.1 Growth in food & beverage industry to support market

- 11.4.7 REST OF EUROPE

- 11.4.1 GERMANY

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.5.1.1 Saudi Arabia

- 11.5.1.1.1 Growth in chemical industry to create demand

- 11.5.1.2 UAE

- 11.5.1.2.1 Manufacturing sector to drive market

- 11.5.1.3 Qatar

- 11.5.1.3.1 Growing petrochemicals sector to drive market

- 11.5.1.4 Rest of GCC Countries

- 11.5.1.1 Saudi Arabia

- 11.5.2 ISRAEL

- 11.5.2.1 National water scarcity & circular economy initiatives to drive market

- 11.5.3 SOUTH AFRICA

- 11.5.3.1 Biggest industrial sectors to create demand for vacuum evaporators

- 11.5.4 REST OF MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.6 SOUTH AMERICA

- 11.6.1 ARGENTINA

- 11.6.1.1 Growing food & beverage and electronics industries to boost market growth

- 11.6.2 BRAZIL

- 11.6.2.1 Automotive industry to drive market

- 11.6.3 CHILE

- 11.6.3.1 Mining sector to create demand for vacuum evaporators

- 11.6.1 ARGENTINA

- 11.7 REST OF SOUTH AMERICA

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020-2025

- 12.3 REVENUE ANALYSIS

- 12.3.1 REVENUE ANALYSIS, 2020-2024

- 12.3.2 MARKET SHARE ANALYSIS, 2024

- 12.3.2.1 Veolia Water Technologies (France)

- 12.3.2.2 Alfa Laval (Sweden)

- 12.3.2.3 SPX Flow, Inc. (US)

- 12.3.2.4 Gea Group Aktiengesellschaft (Germany)

- 12.3.2.5 Condorchem Enviro Solutions (Spain)

- 12.4 BRAND/PRODUCT COMPARISON

- 12.4.1 VEOLIA WATER TECHNOLOGIES ( VEOLIA GROUP)

- 12.4.2 GEA GROUP AKTIENGESELLSCHAFT

- 12.4.3 SPX FLOW INC

- 12.4.4 ALFA LAVAL

- 12.4.5 CONDORCHEM ENVIRO SOLUTIONS

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.5.5.1 Company footprint

- 12.5.6 REGION FOOTPRINT

- 12.5.7 TECHNOLOGY FOOTPRINT '

- 12.5.8 APPLICATION FOOTPRINT '

- 12.5.9 END USE FOOTPRINT

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- 12.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.6.5.1 Detailed list of key startups/SMEs

- 12.6.5.2 Competitive benchmarking of key startups/SMEs

- 12.7 COMPANY VALUATION AND FINANCIAL METRICS

- 12.8 COMPETITIVE SCENARIO

- 12.8.1 PRODUCT LAUNCHES

- 12.8.2 DEALS

- 12.8.3 EXPANSIONS

13 COMPANY PROFILES

- 13.1 MAJOR PLAYERS

- 13.1.1 VEOLIA WATER TECHNOLOGIES (VEOLIA GROUP)

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Deals

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 ALFA LAVAL

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 MnM view

- 13.1.2.3.1 Right to win

- 13.1.2.3.2 Strategic choices

- 13.1.2.3.3 Weaknesses and competitive threats

- 13.1.3 GEA GROUP AKTIENGESELLSCHAFT

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Expansions

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 SPX FLOW, INC.

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 MnM view

- 13.1.4.3.1 Right to win

- 13.1.4.3.2 Strategic choices

- 13.1.4.3.3 Weaknesses and competitive threats

- 13.1.5 CONDORCHEM ENVIRO SOLUTIONS

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 MnM view

- 13.1.5.3.1 Right to win

- 13.1.5.3.2 Strategic choices

- 13.1.5.3.3 Weaknesses and competitive threats

- 13.1.6 ECO-TECHNO SRL

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.7 H2O GMBH

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 Recent developments

- 13.1.8 DE DIETRICH

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.2.1 Product launches

- 13.1.9 BUCHER UNIPEKTIN

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.10 SASAKURA ENGINEERING CO, LTD.

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.11 PRAJ INDUSTRIES

- 13.1.11.1 Business overview

- 13.1.11.2 Products/Solutions/Services offered

- 13.1.12 SANSHIN MFG. CO., LTD.

- 13.1.12.1 Business overview

- 13.1.12.2 Products/Solutions/Services offered

- 13.1.13 SALTWORKS TECHNOLOGIES INC.

- 13.1.13.1 Business overview

- 13.1.13.2 Products/Solutions/Services offered

- 13.1.13.3 Recent developments

- 13.1.13.3.1 Expansions

- 13.1.14 ZHEJIANG TAIKANG EVAPORATOR CO., LTD

- 13.1.14.1 Business overview

- 13.1.14.2 Products/Solutions/Services offered

- 13.1.14.3 Recent developments

- 13.1.15 BELMAR TECHNOLOGIES

- 13.1.15.1 Business overview

- 13.1.15.2 Products/Solutions/Services offered

- 13.1.16 HEBEI LEHENG ENERGY SAVING EQUIPMENT CO. LTD.

- 13.1.16.1 Business overview

- 13.1.16.2 Products/Solutions/Services offered

- 13.1.17 UNITOP AQUACARE LIMITED

- 13.1.17.1 Business overview

- 13.1.17.2 Products/Solutions/Services offered

- 13.1.17.3 Recent developments

- 13.1.17.3.1 Expansions

- 13.1.18 GMM PFAUDLER

- 13.1.18.1 Business overview

- 13.1.18.2 Products/Solutions/Services offered

- 13.1.18.3 Recent developments

- 13.1.18.3.1 Deals

- 13.1.1 VEOLIA WATER TECHNOLOGIES (VEOLIA GROUP)

- 13.2 OTHER PLAYERS

- 13.2.1 3V TECH S.P.A.

- 13.2.2 VILOKEN RECYCLING TECH

- 13.2.3 SAMSCO

- 13.2.4 3R TECHNOLOGY

- 13.2.5 KOVOFINIS

- 13.2.6 ENCON EVAPORATORS

- 13.2.7 S.A.I.T.A SRL

- 13.2.8 KMU LOFT CLEANWATER SE

- 13.2.9 TETRA PAK INTERNATIONAL S.A.

- 13.2.10 PROCECO LTD.

- 13.2.11 CFT S.P.A.

14 ADJACENT AND RELATED MARKETS

- 14.1 INTRODUCTION

- 14.2 LIMITATIONS

- 14.3 INTERCONNECTED MARKETS

- 14.3.1 ZERO LIQUID DISCHARGE (ZLD) SYSTEMS MARKET

- 14.3.1.1 Market definition

- 14.3.1.2 Market overview

- 14.3.1 ZERO LIQUID DISCHARGE (ZLD) SYSTEMS MARKET

- 14.4 ZERO LIQUID DISCHARGE (ZLD) SYSTEMS MARKET, BY SYSTEM

- 14.4.1 CONVENTIONAL

- 14.4.1.1 Requirement in small and medium capacity plants to drive market

- 14.4.2 HYBRID

- 14.4.2.1 High water recovery rate to promote use

- 14.4.1 CONVENTIONAL

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 AVAILABLE CUSTOMIZATIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS