|

시장보고서

상품코드

1808082

염산 전기분해 시장 : 기술별, 용도별, 지역별 예측(-2030년)Hydrochloric Acid Electrolysis Market by Technology, Application (Polyurethane Industry, PVC Production or Chlorination, Fumed Silica Production, Agrochemical, Other Applications), and Region - Global Forecast to 2030 |

||||||

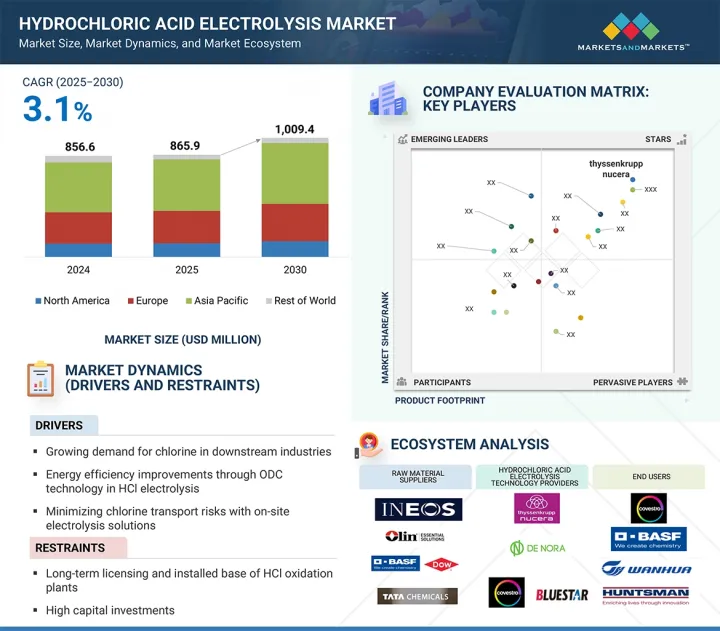

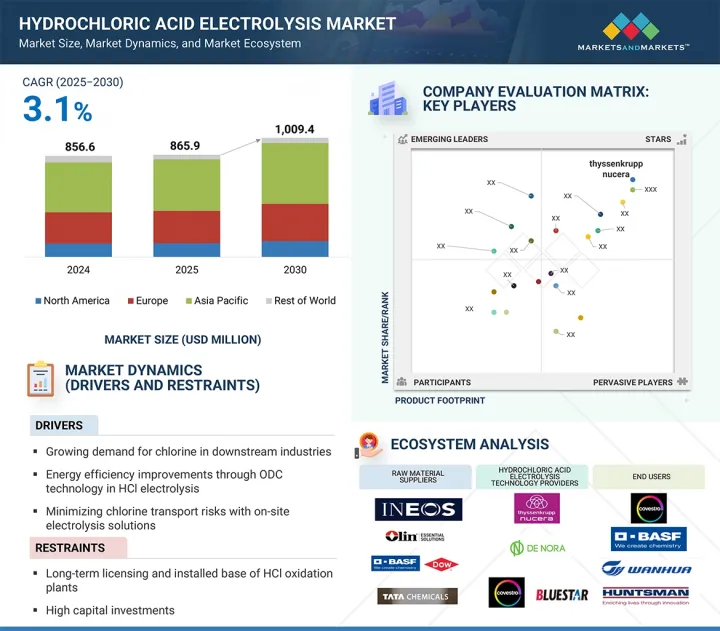

세계의 염산 전기분해 시장 규모는 예측 기간 동안 3.1%의 연평균 복합 성장률(CAGR)로 확대되어 2025년 8억 6,590만 달러에서 2030년까지 10억 940만 달러에 이를 것으로 예측되고 있습니다.

이러한 지속적인 성장은 화학물질의 지속가능한 생산, 염산의 제품별인 염소 및 수소 회수의 재활용 및 재사용에 대한 관심 증가, 그리고 대부분의 국가가 단계적으로 폐지하고 있는 수은계 전기분해와 같은 다른 환경적으로 유해한 공정의 재사용에 기인합니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2023-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(100만 달러), 킬로톤 |

| 부문 | 기술별, 용도별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽 및 기타 지역 |

폴리우레탄(MDI/TDI), PVC, 특수화학 산업은 효율성을 높이고 폐기물을 최소화하며 보다 엄격한 환경 규제에 대응하기 위해 HCL 전기분해 시스템을 공정에 채용하고 있습니다. 기술의 채용조차도 특히 막과 격막을 기반으로 하는 전기분해 시스템에서 보다 경제적이 되고 있으며, 그 적용 범위는 보다 광범위한 용도와 지역을 커버하기까지 확대되고 있습니다.

염산(HCL) 전기분해 시장에서 두 번째로 급성장하는 기술은 격막 기술이며, 성장 요인은 기술이 저렴하고, 업계에서 이용 가능하며, 고액의 설비 투자를 필요로 하지 않는 프로세스를 촉진할 수 있다는 것입니다. 효율이나 환경에 대한 배려라는 점에서는 막 기술이 뛰어나지만, 염소나 수소가 엄밀한 순도를 필요로 하지 않는 경우나, 그 응용이 필요한 분야에서는 다이어프램 셀은 화학 제조업체에 있어서 경제적으로 뛰어난 대체품이 됩니다. 이 기술은 다공성 격막을 사용하여 양극과 음극의 구획을 분리하기 때문에 가스가 섞이지 않지만 이온이 통과 할 수 있습니다. 설계가 간단하고 유지보수 요구가 낮고 기존 인프라에 적합할 수 있기 때문에 막 시스템의 고액의 초기 투자 없이 HCL 중의 염소를 회수하는데 관심이 있는 소규모 및 중규모의 화학 플랜트에 있어서 매력적인 기술입니다. HCL 제품별 재활용에 대한 관심이 높아지고 기업은 예산과 대량 처리 능력 간의 균형을 맞추기 때문에 다이어프램 기술의 사용은 실행 가능하고 비용 효율적인 솔루션으로 성장을 계속할 것으로 보입니다.

염산(HCL) 전기분해 시장에서 두 번째로 급성장하는 응용 분야는 PVC 제조 또는 염소화입니다. 이는 에틸렌 등의 탄화수소가 염소화될 때 제품별로 대량의 HCL을 형성하기 때문입니다. 건축 및 포장 산업의 성장으로 PVC 수요가 세계적으로 증가함에 따라 HCL의 발생량도 증가하고 있으며, 이를 처리하고 재활용하기 위한 적절하고 지속 가능한 솔루션이 필요합니다. 제조업체는 HCL의 전기분해를 통해 고순도 염소와 수소를 생산하고 부산물을 업스트림 염소화 공정에서 재활용함으로써 원료 비용을 줄이고 환경에 영향을 줄 수 있습니다. 이러한 폐쇄 루프는 운영 효율성을 촉진할 뿐만 아니라 산업의 지속가능성 목표와 유해 폐기물을 최소화하는 규제 제약에도 적합합니다. PVC 제조에는 염소를 사용하는 공정이 있으며, 염소의 사용은 순조롭게 진행되고 있기 때문에 HCL 전기분해는 이 용도로 급속히 성장하고 있습니다.

유럽은 지속가능하고 수은을 사용하지 않는 화학 공정을 보장하기 위한 뛰어난 규제 프레임워크과 순환형 경제 접근법에 대한 업계의 노력이 확대되고 있기 때문에 염산(HCL) 전기분해 시장에서 두 번째로 급성장하고 있는 지역입니다. 이 지역에서는 미나마타 조약과 REACH 규정에 명시된 바와 같이 기존의 수은 기반 전기분해를 빠르게 포기하고 막 기반 HCL 전기분해와 같은 더 깨끗한 기술로의 전환을 촉진하고 있습니다. 유럽에 본사를 둔 주요 화학 업체들은 폐기물을 제한하고 배출을 최소화하고 공급망 안전성을 높이기 위해 MDI, TDI, PVC 생산에서 HCL 폐기물에서 염소를 추출하는 전기분해 플랜트를 설치했습니다.

대상 기업 : Thyssenkrupp nucera(독일), Industrie De Nora SpA(이탈리아), Covestro AG(독일), Blueestar(Beijing) Chemical Machinery(중국) 등을 대상으로 합니다.

염산 전기분해 시장에서 이러한 주요 기업의 기업 프로파일, 최근 동향, 주요 시장 전략 등 상세한 경쟁 분석도 포함되어 있습니다.

조사 대상

이 조사 보고서는 염산 전기분해 시장을 기술별, 용도별, 지역별로 분류하고 있습니다. 본 보고서의 조사 범위는 염산 전기분해 시장의 성장에 영향을 주는 촉진요인 및 억제요인과 과제 및 기회에 관한 상세정보를 망라하고 있습니다. 주요 업계 진출 기업을 상세하게 분석하여 사업 개요, 제공 제품, 염산 전기분해 시장과 관련된 제휴 및 확대 등 주요 전략에 대한 통찰력을 제공합니다.

보고서 구매 이유

본 보고서는 염산 전기분해 시장 전체와 하위부문 수익의 가장 가까운 근사치에 대한 정보를 시장 리더/신규 참가자에게 제공합니다. 이 보고서는 이해관계자가 경쟁 구도를 이해하고 자사의 사업을 보다 잘 파악하기 위한 고려사항을 심화하고 적절한 시장 진출 전략을 계획하는 데 도움이 됩니다. 이 보고서는 이해관계자가 시장의 박동을 이해하고 주요 시장 성장 촉진요인 및 억제요인과 과제·기회에 관한 정보를 제공하는 데 도움이 됩니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 소개

- 시장 역학

- 고객사업에 영향을 주는 동향/혼란

- 생태계 분석

- 밸류체인 분석

- 규제 상황

- 가격 분석

- 무역 분석

- 기술 분석

- 특허 분석

- 사례 연구 분석

- 2025-2026년의 주된 회의와 이벤트

- AI/생성형 AI가 염산 전기분해 시장에 미치는 영향

- Porter's Five Forces 분석

- 주요 이해관계자와 구매 기준

- 거시경제 분석

- 2025년 미국 관세의 영향: 염산 전기분해 시장

제6장 염산 전기분해 시장(기술별)

- 소개

- 막 전기분해

- 격막 전기분해

- 수은 전기분해

제7장 염산 전기분해 시장(용도별)

- 소개

- 폴리우레탄 산업(MDI/TDI/HDI)

- PVC 제조 및 염소화

- 흄드 실리카 제조

- 농약

- 기타

제8장 염산 전기분해 시장(지역별)

- 소개

- 아시아태평양

- 중국

- 유럽

- 독일

- 스페인

- 헝가리

- 프랑스

- 포르투갈

- 북미

- 미국

- 기타 지역

- 사우디아라비아

제9장 경쟁 구도

- 소개

- 주요 진입기업의 전략/강점

- 수익 분석

- 시장 랭킹 분석

- 기업 평가와 재무지표

- 브랜드/제품 비교

- 경쟁 시나리오

제10장 기업 프로파일

- 주요 진출기업

- THYSSENKRUPP NUCERA

- COVESTRO AG

- WANHUA

- HUNTSMAN INTERNATIONAL LLC

- BLUESTAR(BEIJING)CHEMICAL MACHINERY CO. LTD.

- BASF

- SADARA

제11장 인접 시장과 관련 시장

제12장 부록

JHS 25.09.16The hydrochloric acid electrolysis market is expected to reach USD 1,009.4 million by 2030 from USD 865.9 million in 2025, at a CAGR of 3.1% during the forecast period. This continuous growth is attributed to the rising interest in sustainable production of chemicals, recycling and reuse of both chlorine and hydrogen recovery as by-products of hydrochloric acid, and the reuse of other environmentally harmful processes, such as mercury-based electrolysis, which most countries are phasing out.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million), Volume (Kiloton) |

| Segments | Type, Filler Type, Application, and Region |

| Regions covered | North America, Asia Pacific, Europe, and Rest of the World |

Polyurethane (MDI/TDI), PVC, and specialty chemicals industries are adopting HCL electrolysis systems in their processes to enhance efficiency, minimize waste, and meet tougher environmental regulations. Even the adoption of technology is becoming more economical, especially in membrane and diaphragm-based electrolysis systems, and its applicability has increased in scope to cover a broader spectrum of applications and geographies.

"Diaphragm technology to be second fastest-growing segment in hydrochloric acid electrolysis market"

The second-fastest growing technology in the hydrochloric acid (HCL) electrolysis market is the diaphragm technology, and its growth is attributed to the inexpensive nature of technology, its availability in the industry, and the ability to facilitate processes that do not require high investments in capital. Although membrane technology is superior in terms of efficiency and environmental concerns, diaphragm cells present a good economic substitute to chemical manufacturers in cases where chlorine and hydrogen do not require the strictest purity and also in those areas where its application is needed. The technology uses the porous diaphragm to separate the anode and the cathode compartments, which do not mix gases, but enables the possibility of ions passing through. Its ease of design, low maintenance demands, and ability to fit on the existing infrastructure make it appealing to small-scale and mid-sized chemical plants that are interested in recovering chlorine in HCL without the high initial investments of the membrane systems. With increased interest in recycling HCL by-products and companies balancing between budget and ability to process large volumes, the use of the diaphragm technology will continue to grow as a viable, cost-effective solution.

"PVC production or chlorination to be second fastest-growing segment in hydrochloric acid electrolysis market"

The second-fastest growing application in the hydrochloric acid (HCL) electrolysis market is PVC production or chlorination, since it forms significant quantities of HCL as a by-product when hydrocarbons, such as ethylene, are chlorinated. With increasing worldwide demand for polyvinyl chloride (PVC) due to the growth in construction and the packaging industry, the generation of HCL is also increasing, which needs adequate, sustainable solutions to deal with and recycle it. Manufacturers can produce high-purity chlorine and hydrogen through HCL electrolysis and recycle the by-product in the upstream chlorination processes, decreasing the cost of raw materials and impacting the environment. Such a closed loop can not only promote operational efficiency but also fit the industry sustainability objectives and regulatory constraints to minimize hazardous waste. As PVC manufacture involves chlorinated processes, and the use of chlorine is holding up well, HCL electrolysis is rapidly growing in this application.

"Europe to be second fastest-growing regional market for hydrochloric acid electrolysis"

Europe is the second fastest-growing region of the hydrochloric acid (HCL) electrolysis market owing to a good regulatory framework to ensure sustainable and mercury-free chemical processes, and growing industry commitments to circular economy approaches. The region is rapidly abandoning conventional mercury-based electrolysis as stated at the Minamata Convention and the REACH regulation, which is encouraging a transition toward more cleaner technologies such as membrane-based HCL electrolysis. Major European-based chemical manufacturers are installing electrolysis plants to extract chlorine from HCL waste products, in MDI, TDI, and PVC production, to limit waste, minimize emissions, and boost supply chain security.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Note: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 billion; Tier 2: USD 500 million-1 billion; and Tier 3: <USD 500 million

Companies Covered: thyssenkrupp nucera (Germany), Industrie De Nora S.p.A. (Italy), Covestro AG (Germany), and Bluestar (Beijing) Chemical Machinery Co., Ltd. (China), among others, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the hydrochloric acid electrolysis market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the hydrochloric acid electrolysis market based on technology (membrane technology and diaphragm technology), application (polyurethane Industry (MDI/TDI), PVC production or chlorination, fumed silica production, agrochemical, and other applications), and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the hydrochloric acid electrolysis market. A detailed analysis of the key industry players has been done to provide insights into their business overviews, products offered, and key strategies, such as partnerships and expansions, associated with the hydrochloric acid electrolysis market.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall hydrochloric acid electrolysis market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Growing demand for chlorine in downstream industries), restraints (High capital investments), opportunities (Sustainability and circular economy practices), and challenges (Market fragmentation and knowledge gaps).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product/technology & service launches in the hydrochloric acid electrolysis market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the hydrochloric acid electrolysis market across varied regions.

Market Diversification: Exhaustive information about new products/technologies & services, untapped geographies, recent developments, and investments in the hydrochloric acid electrolysis market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as thyssenkrupp nucera (Germany), Industrie De Nora S.p.A. (Italy), Covestro AG (Germany), and Bluestar (Beijing) Chemical Machinery Co., Ltd. (China).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.1.2 List of secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key primary participants

- 2.1.2.2 Key data from primary sources

- 2.1.2.3 Breakdown of interviews with experts

- 2.1.2.4 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 TOP-DOWN APPROACH

- 2.2.2 BOTTOM-UP APPROACH

- 2.3 GROWTH FORECAST

- 2.4 DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 FACTOR ANALYSIS

- 2.7 RESEARCH LIMITATIONS

- 2.8 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HYDROCHLORIC ACID ELECTROLYSIS MARKET

- 4.2 HYDROCHLORIC ACID ELECTROLYSIS MARKET, BY TECHNOLOGY

- 4.3 HYDROCHLORIC ACID ELECTROLYSIS MARKET, BY APPLICATION

- 4.4 ASIA PACIFIC: HYDROCHLORIC ACID ELECTROLYSIS MARKET, BY APPLICATION & COUNTRY

- 4.5 HYDROCHLORIC ACID ELECTROLYSIS MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growing demand for chlorine in downstream industries

- 5.2.1.2 Energy efficiency improvements through ODC technology in hydrochloric acid electrolysis

- 5.2.1.3 Minimizing chlorine transport risks with on-site electrolysis solutions

- 5.2.2 RESTRAINTS

- 5.2.2.1 Long-term licensing and installed base of hydrogen chloride oxidation plants

- 5.2.2.2 High capital investment

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Sustainability and circular economy practices

- 5.2.4 CHALLENGES

- 5.2.4.1 Volatility in energy prices

- 5.2.4.2 Market fragmentation and knowledge gaps

- 5.2.4.3 Regulatory and safety compliance

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 REGULATORY LANDSCAPE

- 5.6.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.7 PRICING ANALYSIS

- 5.7.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY TECHNOLOGY, 2024

- 5.7.2 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2030

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT DATA (HS CODE 280110)

- 5.8.2 EXPORT DATA (HS CODE 280110)

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Diaphragm (Porous) Electrolysis

- 5.9.1.2 Membrane Cell Electrolysis

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Gas Treatment Technologies

- 5.9.2.2 Gas Separation Technologies

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 Hydrochloric Acid Recovery & Regeneration Systems

- 5.9.3.2 Electrodialysis (ED) and Ion Exchange Technologies

- 5.9.1 KEY TECHNOLOGIES

- 5.10 PATENT ANALYSIS

- 5.10.1 INTRODUCTION

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 ADVANCES IN HYDROCHLORIC ACID GAS-PHASE ELECTROLYSIS EMPLOYING OXYGEN-DEPOLARIZED CATHODE

- 5.12 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.13 IMPACT OF AI/GEN AI ON HYDROCHLORIC ACID ELECTROLYSIS MARKET

- 5.13.1 INTRODUCTION

- 5.14 PORTER'S FIVE FORCES ANALYSIS

- 5.14.1 THREAT OF NEW ENTRANTS

- 5.14.2 THREAT OF SUBSTITUTES

- 5.14.3 BARGAINING POWER OF SUPPLIERS

- 5.14.4 BARGAINING POWER OF BUYERS

- 5.14.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.15.2 BUYING CRITERIA

- 5.16 MACROECONOMIC ANALYSIS

- 5.16.1 INTRODUCTION

- 5.16.2 GDP TRENDS AND FORECASTS

- 5.17 IMPACT OF 2025 US TARIFF: HYDROCHLORIC ACID ELECTROLYSIS MARKET

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 IMPACT ON COUNTRY/REGION

- 5.17.4.1 US

- 5.17.4.2 Europe

- 5.17.4.3 Asia Pacific

- 5.17.5 IMPACT ON APPLICATIONS

6 HYDROCHLORIC ACID ELECTROLYSIS MARKET, BY TECHNOLOGY

- 6.1 INTRODUCTION

- 6.2 MEMBRANE ELECTROLYSIS

- 6.2.1 RAPID ADOPTION OF MEMBRANE ELECTROLYSIS DRIVEN BY EFFICIENCY AND SUSTAINABILITY

- 6.2.2 ODC (OXYGEN-DEPOLARIZED CATHODE) TECHNOLOGY

- 6.3 DIAPHRAGM ELECTROLYSIS

- 6.3.1 MERCURY-FREE CHEMICAL PRODUCTION TO DRIVE DEMAND FOR DIAPHRAGM ELECTROLYSIS

- 6.4 MERCURY ELECTROLYSIS

- 6.4.1 PHASE-OUT OF MERCURY TECHNOLOGY DUE TO ENVIRONMENTAL CONCERNS AND REGULATORY ACTION

7 HYDROCHLORIC ACID ELECTROLYSIS MARKET, BY APPLICATION

- 7.1 INTRODUCTION

- 7.2 POLYURETHANE INDUSTRY (MDI/TDI/HDI)

- 7.2.1 ENVIRONMENTAL PRESSURES AND CIRCULAR MANUFACTURING TO DRIVE MARKET

- 7.3 PVC PRODUCTION & CHLORINATION

- 7.3.1 HIGH CHLORINE DEMAND IN PVC PRODUCTION TO PROPEL MARKET

- 7.4 FUMED SILICA PRODUCTION

- 7.4.1 SUSTAINABILITY AND CIRCULAR CHLORINE UTILIZATION TO DRIVE MARKET

- 7.5 AGROCHEMICAL

- 7.5.1 SUSTAINABILITY AND REGULATORY COMPLIANCE TO DRIVE DEMAND

- 7.6 OTHER APPLICATIONS

8 HYDROCHLORIC ACID ELECTROLYSIS MARKET, BY REGION

- 8.1 INTRODUCTION

- 8.2 ASIA PACIFIC

- 8.2.1 CHINA

- 8.2.1.1 Strong demand for chlorine in key industrial segments to drive market

- 8.2.1 CHINA

- 8.3 EUROPE

- 8.3.1 GERMANY

- 8.3.1.1 Stringent environmental regulations to drive market

- 8.3.2 SPAIN

- 8.3.2.1 Strategic geographic advantage to drive market

- 8.3.3 HUNGARY

- 8.3.3.1 Industry leadership and strategic investments to drive the market

- 8.3.4 FRANCE

- 8.3.4.1 Circular economy goals to drive market

- 8.3.5 PORTUGAL

- 8.3.5.1 EU funding support to drive market

- 8.3.1 GERMANY

- 8.4 NORTH AMERICA

- 8.4.1 US

- 8.4.1.1 Government-backed sustainability initiatives to drive market

- 8.4.1 US

- 8.5 REST OF THE WORLD

- 8.5.1 SAUDI ARABIA

- 8.5.1.1 Petrochemical industry expansion to drive market

- 8.5.1 SAUDI ARABIA

9 COMPETITIVE LANDSCAPE

- 9.1 INTRODUCTION

- 9.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 9.3 REVENUE ANALYSIS

- 9.4 MARKET RANKING ANALYSIS

- 9.5 COMPANY VALUATION AND FINANCIAL METRICS

- 9.6 BRAND/PRODUCT COMPARISON

- 9.6.1 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 9.6.1.1 Company footprint

- 9.6.1.2 Region footprint

- 9.6.1.3 Technology footprint

- 9.6.1.4 Application footprint

- 9.6.1 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 9.7 COMPETITIVE SCENARIO

- 9.7.1 DEALS

- 9.7.2 EXPANSIONS

10 COMPANY PROFILES

- 10.1 KEY PLAYERS

- 10.1.1 THYSSENKRUPP NUCERA

- 10.1.1.1 Business overview

- 10.1.1.2 Products/Solutions/Services offered

- 10.1.1.3 Recent developments

- 10.1.1.3.1 Expansions

- 10.1.1.4 MnM view

- 10.1.1.4.1 Right to win

- 10.1.1.4.2 Strategic choices

- 10.1.1.4.3 Weaknesses and competitive threats

- 10.1.2 COVESTRO AG

- 10.1.2.1 Business overview

- 10.1.2.2 Products/Solutions/Services offered

- 10.1.2.3 Recent developments

- 10.1.2.3.1 Deals

- 10.1.2.3.2 Expansions

- 10.1.2.4 MnM view

- 10.1.2.4.1 Right to win

- 10.1.2.4.2 Strategic choices

- 10.1.2.4.3 Weaknesses and competitive threats

- 10.1.3 WANHUA

- 10.1.3.1 Business overview

- 10.1.3.2 Products/Solutions/Services offered

- 10.1.3.3 MnM view

- 10.1.3.3.1 Right to win

- 10.1.3.3.2 Strategic choices

- 10.1.3.3.3 Weaknesses and competitive threats

- 10.1.4 HUNTSMAN INTERNATIONAL LLC

- 10.1.4.1 Business overview

- 10.1.4.2 Products/Solutions/Services offered

- 10.1.4.3 MnM view

- 10.1.4.3.1 Right to win

- 10.1.4.3.2 Strategic choices

- 10.1.4.3.3 Weaknesses and competitive threats

- 10.1.5 BLUESTAR (BEIJING) CHEMICAL MACHINERY CO. LTD.

- 10.1.5.1 Business overview

- 10.1.5.2 Products/Solutions/Services offered

- 10.1.5.3 MnM view

- 10.1.6 BASF

- 10.1.6.1 Business overview

- 10.1.6.2 Products/Solutions/Services offered

- 10.1.6.3 MnM view

- 10.1.7 SADARA

- 10.1.7.1 Business overview

- 10.1.7.2 Products/Solutions/Services offered

- 10.1.7.3 MnM view

- 10.1.1 THYSSENKRUPP NUCERA

11 ADJACENT & RELATED MARKET

- 11.1 INTRODUCTION

- 11.2 LIMITATIONS

- 11.3 HYDROCHLORIC ACID MARKET

- 11.3.1 MARKET DEFINITION

- 11.3.2 HYDROCHLORIC ACID MARKET, BY GRADE

- 11.3.3 HYDROCHLORIC ACID MARKET, BY APPLICATION

- 11.3.4 HYDROCHLORIC ACID MARKET, BY END-USE INDUSTRY

- 11.3.5 HYDROCHLORIC ACID MARKET, BY REGION

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS