|

시장보고서

상품코드

1808084

휴대용 초음파 시장 : 제품 유형별, 플랫폼별, 최종 사용자별, 용도별, 지역별 예측(-2030년)Portable Ultrasound Market by Product, Platform, Application, End User - Global Forecast to 2030 |

||||||

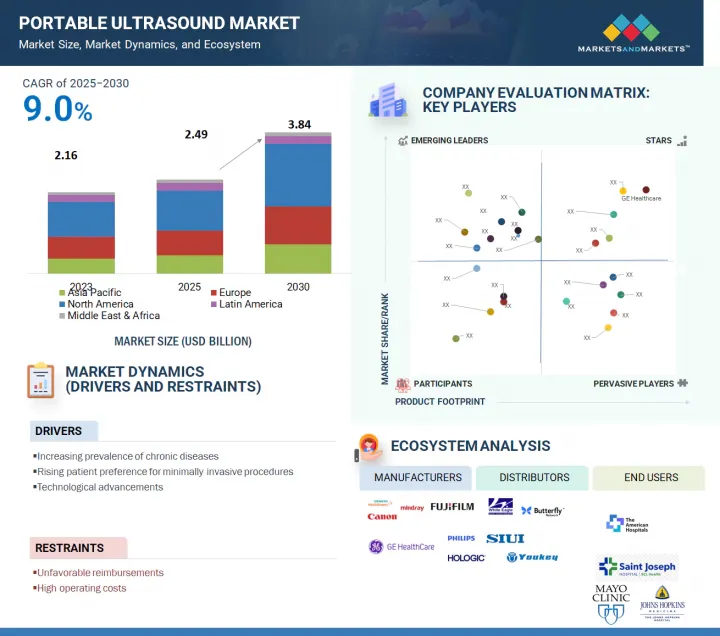

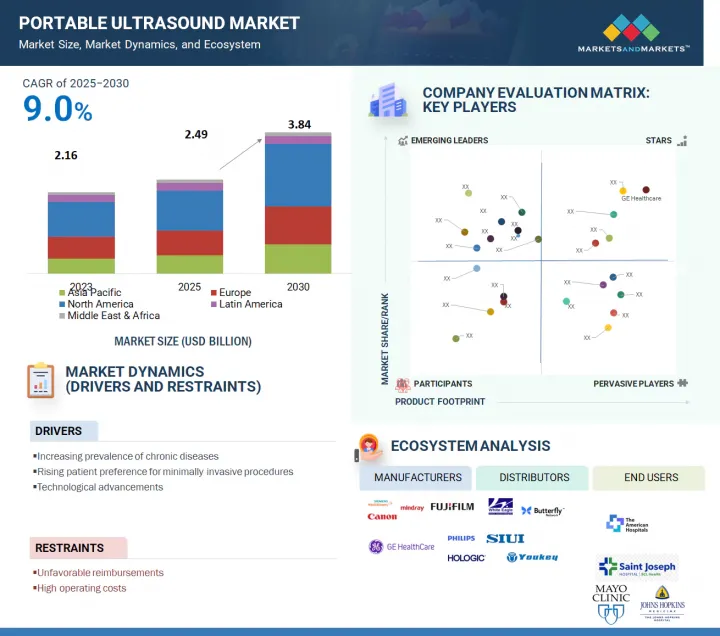

세계의 휴대용 초음파 시장 규모는 2025년 24억 9,000만 달러에서 2030년까지 38억 4,000만 달러에 이르고, 예측 기간 동안 CAGR 9.0%가 될 것으로 예측됩니다.

POC(Point of Care) 진단에 대한 수요가 증가함에 따라 특히 다양한 환경에서 비침습적 이미징 방법을 사용함으로써 휴대용 초음파 기술에 대한 요구가 커지고 있습니다. 이 수요는 만성 질환과 라이프스타일과 관련된 질병의 확산이 확대되고 있는 것이 큰 요인이 되어, 임상 환경에서 신속한 이미징 솔루션의 긴급 요구가 부각되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2023-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(10억 달러) |

| 부문 | 제품 유형별, 플랫폼별, 최종 사용자별, 용도별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

또한 기술의 진보로 이미지 품질이 향상되어 병원, 클리닉 및 원격지의 의료 서비스 제공업체에게 더욱 유익하고 매력적입니다. 임산부의 건강이 보다 중시되게 되어, 응급이나 집중 치료의 현장에서 휴대형 초음파의 사용을 지지하는 근거가 늘어나고 있는 것도 요일인이 되고 있습니다. 가상 헬스케어 솔루션의 탐구가 진행됨에 따라 재택 케어와 원격 의료에 대한 관심이 크게 높아질 것으로 예측됩니다.

트랜스듀서 및 프로브는 이미지 획득에 필수적이고 전문적인 역할을 하기 때문에 휴대용 초음파 시장에서 가장 큰 부분을 차지합니다. 각 트랜스듀서는 특정 해부학적 구조와 깊이를 위해 특별히 설계되었으며, 그 결과 표층 해부학용 리니어 트랜스듀서, 심부 장기용 커빌리니어 트랜스듀서, 심장 응용을 위한 위상 배열 트랜스듀서 등 다양한 유형이 있습니다. 이러한 다양성은 광범위한 임상 응용을 수용하기 위해 필요합니다.

일반적으로 하나의 휴대용 초음파 진단 시스템에서 진단 능력을 최대한 활용하려면 여러 독특한 프로브가 필요합니다. 게다가, 트랜스듀서는 첨단 압전 부품과 첨단 재료를 통합한 고도로 설계된 장치이므로, 1개당 비용이 매우 높습니다. 사용 빈도가 높기 때문에 소모하기 쉽고, 멸균이 필요하기 때문에 교환 빈도도 높습니다.

외상 및 응급 의료는 긴급하고 일각을 다투는 상황에서 신속하고 실시간 진단 이미징에 대한 중요한 요구가 있기 때문에 휴대용 초음파 시장에서 가장 큰 시장 점유율을 차지하고 있습니다. 휴대용 초음파 진단 장치는 응급실, 구급차, 재해 현장과 같은 의료 현장에서 화상 진단 부서로 환자를 운반하지 않고 내상, 출혈, 장기 손상을 즉시 평가할 수 있습니다. 컴팩트한 크기, 사용 편의성, 빠른 시동 시간은 압력이 걸리는 환경에서 신속한 의사 결정에 이상적입니다. 게다가 FAST(Focused Assessment with Sonography in Trauma)와 같은 프로토콜은 외상 치료의 표준 실천 방법이 되어 채용을 더욱 뒷받침하고 있습니다. 응급 서비스가 세계적으로 확대됨에 따라, 특히 신흥국 시장과 원격지에서는 외상 및 응급 현장에서 휴대용 초음파에 대한 수요가 지속적으로 증가하고 있으며 최고 점유율을 강화하고 있습니다.

병원 및 수술 센터는 환자 수가 많고, 다양한 진단 요구, 다양한 영상 진단을 지원하는 수술기 주위 인프라스트럭처를 가지고 있기 때문에 휴대용 초음파 시장의 주요 최종 사용자입니다. 이러한 시설에서는 집중 치료실(ICU)과 수술실을 중심으로 POC(Point of Care) 진단, 긴급 사태, 수술 전 및 수술 후의 평가, 침대 측에서의 화상 진단에 휴대용 초음파 진단 장치가 빈번하게 이용되고 있습니다. 심각한 환자를 침대에서 옮기지 않고도 빠르고 안정적이고 비침습적인 스캔을 수행할 수 있다는 것은 이러한 환경에서 휴대용 초음파의 가치를 두드러지게 합니다. 또한, 순환기과, 산과, 근골격계 영상 진단의 일상적인 워크플로우에서 휴대용 시스템을 사용함으로써 이러한 유형의 시설에서의 채택이 더욱 촉진됩니다.

아시아태평양은 여러 주요 동향으로 견인되었으며 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 중국, 인도, 동남아시아 국가 등의 건강 관리 인프라의 확대가 첨단 의료 기술의 채택을 촉진하고 있습니다. 만성 질환 증가와 고령화도 함께 사용하기 쉽고 저렴한 진단 도구에 대한 수요가 높아지고 있습니다. 휴대용 초음파 진단 장치는 CT 및 MRI 장치, 기존의 초음파 진단 시스템보다 훨씬 저렴하며 다양한 환경에서 사용할 수 있습니다. 게다가 인공지능과 무선기술의 진보로 새로운 장치는 지속적으로 개선되어 휴대용 초음파 장치의 기능과 매력을 모두 높이고 있습니다.

본 보고서에서는 세계의 휴대용 초음파 시장에 대해 조사했으며, 제품 유형별, 플랫폼별, 최종 사용자별, 용도별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 소개

- 시장 역학

- 밸류체인 분석

- 공급망 분석

- Porter's Five Forces 분석

- 주요 이해관계자와 구매 기준

- 특허 분석

- 무역 데이터 분석

- 2025-2026년의 주된 회의와 이벤트

- 미충족 요구와 주요 문제점

- 생태계 분석

- 2025년 미국 관세의 영향

- 생성형 AI가 휴대용 초음파 시장에 미치는 영향

- 고객사업에 영향을 주는 동향/혼란

- 기술 분석

- 사례 연구 분석

- 규제 상황

- 투자 및 자금조달 시나리오

- 가격 분석

- 상환 시나리오

제6장 휴대용 초음파 시장(제품 유형별)

- 소개

- 트랜스듀서 및 프로브

- 시스템 및 콘솔

- 액세서리

- 소프트웨어 및 서비스

제7장 휴대용 초음파 시장(플랫폼별)

- 소개

- 트롤리 및 카트 베이스

- 핸드헬드

- 노트북 베이스

- 태블릿 베이스

제8장 휴대용 초음파 시장(최종사용자별)

- 소개

- 병원 및 수술센터

- 이미지 센터

- 외래 진료 센터

- 기타

제9장 휴대용 초음파 시장(용도별)

- 소개

- 산부인과

- 심장병학

- 혈관

- 소아과

- 비뇨기과

제10장 휴대용 초음파 시장(지역별)

- 소개

- 북미

- 거시경제 전망

- 미국

- 캐나다

- 유럽

- 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 거시경제 전망

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타

- 라틴아메리카

- 거시경제 전망

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- 거시경제 전망

- GCC 국가

- 기타

제11장 경쟁 구도

- 소개

- 주요 진입기업의 전략/강점

- 수익 분석, 2021-2024년

- 시장 점유율 분석, 2024년

- 기업 평가 매트릭스: 주요 진입기업, 2024년

- 기업 평가 매트릭스: 스타트업/중소기업, 2024년

- 기업 평가와 재무지표

- 브랜드/제품 비교

- 경쟁 시나리오

제12장 기업 프로파일

- 주요 진출기업

- GE HEALTHCARE

- PHILIPS HEALTHCARE

- CANON MEDICAL SYSTEMS CORPORATION

- SIEMENS HEALTHINEERS AG

- FUJIFILM CORPORATION

- HOLOGIC, INC.

- SAMSUNG ELECTRONICS CO., LTD.

- MINDRAY MEDICAL INTERNATIONAL LIMITED

- ESAOTE SPA

- CHISON MEDICAL TECHNOLOGIES CO., LTD.

- NEUSOFT CORPORATION

- KONICA MINOLTA, INC.

- CLARIUS

- MEDGYN PRODUCTS, INC.

- PROMED TECHNOLOGY CO., LTD.

- 기타 기업

- WHITE EAGLE SONIC TECHNOLOGIES, INC.

- PERLONG MEDICAL EQUIPMENT CO., LTD.

- YOUKEY MEDICAL

- SIUI

- TELEMED, MEDICAL IMAGING EQUIPMENT DESIGN & MANUFACTURING

- BUTTERFLY NETWORK, INC.

- ALPINION MEDICAL SYSTEMS

- EDAN INSTRUMENTS, INC.

- SHENZHEN LANDWIND INDUSTRY CO., LTD

- ECHONOUS INC.

- MOBISANTE

- SHENZHEN WISONIC MEDICAL TECHNOLOGY CO., LTD

- SHENZHEN BIOCARE BIO-MEDICAL EQUIPMENT CO., LTD

- SONOSCAPE MEDICAL CORP

- CURA HEALTHCARE

제13장 부록

JHS 25.09.16The global portable ultrasound market is projected to reach USD 3.84 billion by 2030 from USD 2.49 billion in 2025, growing at a CAGR of 9.0% during the forecast period. The increasing demand for point-of-care diagnostics has led to a rise in the need for portable ultrasound technology, particularly through the use of non-invasive imaging methods in various settings. This demand is largely driven by the growing prevalence of chronic and lifestyle-related diseases, highlighting the urgent need for prompt imaging solutions in clinical environments.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product, Platform, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Additionally, advancements in technology have enhanced imaging quality, making it more beneficial and appealing to hospitals, clinics, and remote healthcare providers. A greater emphasis on maternal health and a growing body of evidence supporting the use of portable ultrasound in emergency and intensive care settings are also contributing factors. As we continue to explore virtual healthcare solutions, we can anticipate a significant increase in interest in home-based care and telemedicine.

"The transducers/probes segment is expected to register the highest growth rate in the market during the forecast period."

Transducers/probes comprise the largest portion of the portable ultrasound market due to their essential and specialized role in acquiring images. Each transducer is specifically designed for a particular anatomy and depth, resulting in a variety of types, such as linear transducers for superficial anatomy, curvilinear transducers for deeper organs, and phased array transducers for cardiac applications. This variety is necessary to address a wide range of clinical uses.

Typically, a single portable ultrasound system requires multiple unique probes to fully utilize its diagnostic capabilities. Additionally, transducers are highly engineered devices that incorporate sophisticated piezoelectric components and advanced materials, making them quite expensive on a per-unit basis. Their susceptibility to wear and tear from heavy use and the need for sterilization leads to frequent replacement, which further solidifies their dominant presence in the portable ultrasound industry.

"The trauma & emergency care segment commanded the largest market share in 2024."

Trauma & emergency care account for the largest market share in the portable ultrasound market due to the critical need for rapid, real-time diagnostic imaging in urgent and time-sensitive situations. Portable ultrasound devices enable immediate assessment of internal injuries, bleeding, or organ damage at the point of care-whether in emergency rooms, ambulances, or disaster sites-without requiring patient transport to imaging departments. Their compact size, ease of use, and quick boot-up times make them ideal for fast decision-making in high-pressure environments. Additionally, protocols like FAST (Focused Assessment with Sonography in Trauma) have become standard practice in trauma care, further driving adoption. As emergency services expand globally, especially in developing regions and remote areas, the demand for portable ultrasound in trauma and emergency settings continues to grow, reinforcing its leading market share.

"Hospitals & surgical centers held the largest share of the portable ultrasound market in 2024, by end user."

Hospitals & surgical centers are the primary end users in the portable ultrasound market due to their high patient volume, diverse diagnostic needs, and the perioperative infrastructure that supports various imaging procedures. These facilities frequently utilize portable ultrasound devices for point-of-care diagnostics, emergency situations, pre- and post-operative evaluations, and bedside imaging, particularly in intensive care units (ICUs) and operating rooms. The ability to perform rapid, reliable, and non-invasive scans without needing to move critically ill patients from their beds highlights the value of portable ultrasound in these settings. Additionally, the use of portable systems across routine workflows in cardiology, obstetrics, and musculoskeletal imaging further enhances their adoption in these types of facilities.

"Asia Pacific is expected to register the highest growth rate in the market during the forecast period."

The Asia Pacific region is anticipated to register the highest CAGR during the forecast period, driven by several key trends. The expanding healthcare infrastructure in countries like China, India, and those in Southeast Asia is facilitating the adoption of advanced medical technologies. Coupled with the rising prevalence of chronic diseases and an aging population, there is a growing demand for accessible and affordable diagnostic tools. Portable ultrasound devices are significantly less expensive than CT or MRI machines and traditional ultrasound systems, and they can be utilized in various settings. Additionally, newer devices are continually improving through advancements in artificial intelligence and wireless technology, enhancing both the functionality and appeal of portable ultrasound systems.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1 (40%), Tier 2 (30%), and Tier 3 (30%)

- By Designation: C-level Executives (55%), Directors (27%), and Others (18%)

- By Region: North America (35%), Europe (32%), Asia Pacific (25%), Latin America (6%), and the Middle East & Africa (2%)

Prominent players in this market are Philips Healthcare (Netherlands), GE Healthcare (US), Canon Medical Systems Corporation (Japan), Siemens Healthineers (Germany), FUJIFILM Corporation (Japan), Hologic Inc.(US), Samsung Electronics Co., Ltd. (South Korea), Esaote SpA (Italy), Chison Medical Technologies Co., Ltd. (China), MobiSante Inc. (US), Clarius (Canada), MedGyn Products, Inc. (US), Promed Technology (China), and Neusoft Corporation (China), among others.

Research Coverage

The portable ultrasound market is segmented by product, platform, application, end user, and region. Key factors influencing market growth include driving forces, restraints, opportunities, and challenges for stakeholders. The report also reviews the leading companies competing in the portable ultrasound market. A micro-level analysis can be conducted to examine trends, growth opportunities, and contributions to the market. Additionally, it highlights potential revenue growth opportunities across various market segments in five major regions.

Key Benefits of Buying the Report

The report is valuable for new entrants in the portable ultrasound market as it provides comprehensive information about the market. This information is essential for understanding various investment opportunities. The report offers insights into both key and smaller players in the market, which can help in creating a solid basis for risk analysis when making investment decisions. It accurately segments the market by end users and regions, providing focused insights into specific market segments. Additionally, the report highlights key trends, challenges, growth drivers, and opportunities to support strategic decision-making through a thorough analysis.

The report provides insights into the following pointers:

- Key drivers (increasing prevalence of chronic diseases, growing demand for point-of-care diagnostics, technological advancements, and growing public and private investments, funding, and grants), restraints (unfavorable reimbursements and high operating costs), opportunities (integration of AI in portable ultrasound, high growth of emerging markets, and development of wearable and wireless ultrasound devices), and challenges (limited battery life and device durability and shortage of sonographers).

- Product Development/Innovation: Emerging technologies in the space, R&D, recent product & service launches in the portable ultrasound market.

- Market Growth: In-depth insights into the portable ultrasound market across varied geographies.

- Market Diversification: Detailed analysis of new products, unexplored geographies, latest trends, and investments in the portable ultrasound market.

- Competitive Assessment: Detailed assessment of market shares, product offerings, and leading strategies of key players, such as Philips Healthcare (Netherlands), GE Healthcare (US), Canon Medical Systems Corporation (Japan), Siemens Healthineers (Germany), and FUJIFILM Corporation (Japan), among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 PORTABLE ULTRASOUND MARKET SEGMENTATION AND REGIONAL SNAPSHOT

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY RESEARCH

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY RESEARCH

- 2.1.2.1 Key industry insights

- 2.1.1 SECONDARY RESEARCH

- 2.2 MARKET SIZE ESTIMATION APPROACH

- 2.2.1.1 Approach 1: Company revenue estimation approach

- 2.2.1.2 Approach 2: Customer-based market estimation

- 2.3 MARKET FORECASTING APPROACH

- 2.4 DATA TRIANGULATION AND MARKET BREAKDOWN

- 2.5 MARKET SHARE ASSESSMENT

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 RESEARCH LIMITATIONS

- 2.8 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN THE PORTABLE ULTRASOUND MARKET

- 4.2 NORTH AMERICA: PORTABLE ULTRASOUND MARKET, BY COUNTRY AND END USER, 2024

- 4.3 GEOGRAPHIC SNAPSHOT OF PORTABLE ULTRASOUND MARKET

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing prevalence of chronic diseases

- 5.2.1.2 Growing demand for point-of-care diagnostics

- 5.2.1.3 Rising technological advancements in portable ultrasound devices

- 5.2.1.4 Growing public and private investments, funding, and grants

- 5.2.2 RESTRAINTS

- 5.2.2.1 Unfavorable reimbursements

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Integration of AI in portable ultrasound

- 5.2.3.2 High growth potential in emerging economies

- 5.2.3.3 Development of wearable and wireless ultrasound devices

- 5.2.4 CHALLENGES

- 5.2.4.1 Limited battery life and device durability

- 5.2.4.2 Shortage of skilled sonographers

- 5.2.1 DRIVERS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.4.1 PROMINENT COMPANIES

- 5.4.2 SMALL AND MEDIUM-SIZED ENTERPRISES

- 5.4.3 MARKETING & SALES, DISTRIBUTION, AND POST-SALES SERVICES

- 5.4.4 END USERS

- 5.5 PORTER'S FIVE FORCES ANALYSIS

- 5.5.1 THREAT OF NEW ENTRANTS

- 5.5.2 BARGAINING POWER OF SUPPLIERS

- 5.5.3 BARGAINING POWER OF BUYERS

- 5.5.4 THREAT OF SUBSTITUTES

- 5.5.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.6 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.6.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.6.2 BUYING CRITERIA

- 5.7 PATENT ANALYSIS

- 5.8 TRADE DATA ANALYSIS

- 5.8.1 IMPORT DATA

- 5.8.2 EXPORT DATA

- 5.9 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.10 UNMET NEEDS AND KEY PAIN POINTS

- 5.11 ECOSYSTEM ANALYSIS

- 5.12 IMPACT OF 2025 US TARIFFS

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRY/REGION

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.4.4 Impact on end-user facilities

- 5.13 IMPACT OF GEN AI ON PORTABLE ULTRASOUND MARKET

- 5.14 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.15 TECHNOLOGY ANALYSIS

- 5.15.1 KEY TECHNOLOGIES

- 5.15.1.1 Probes

- 5.15.1.2 Contrast-enhanced portable ultrasound

- 5.15.1.3 Portable and handheld ultrasound devices

- 5.15.2 COMPLEMENTARY TECHNOLOGIES

- 5.15.2.1 Elastography

- 5.15.2.2 Transrectal Ultrasound

- 5.15.2.3 Transvaginal Ultrasound

- 5.15.3 ADJACENT TECHNOLOGIES

- 5.15.3.1 Positron emission tomography and computed tomography

- 5.15.1 KEY TECHNOLOGIES

- 5.16 CASE STUDY ANALYSIS

- 5.16.1 EFFICIENT POWER FOR HANDHELD ULTRASOUND UNITS

- 5.16.2 ADVANCEMENTS IN USING PORTABLE ULTRASOUND WITH ARTIFICIAL INTELLIGENCE IN PRE-HOSPITAL EMERGENCIES AND DISASTER RESPONSE SETTINGS

- 5.16.3 EFFECTIVENESS OF HANDHELD PORTABLE ULTRASOUND IN RURAL HOSPITAL IN GUATEMALA

- 5.17 REGULATORY LANDSCAPE

- 5.17.1 NORTH AMERICA

- 5.17.1.1 US

- 5.17.1.2 Canada

- 5.17.2 EUROPE

- 5.17.3 ASIA PACIFIC

- 5.17.3.1 Japan

- 5.17.3.2 China

- 5.17.3.3 India

- 5.17.4 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.17.1 NORTH AMERICA

- 5.18 INVESTMENT AND FUNDING SCENARIO

- 5.19 PRICING ANALYSIS

- 5.19.1 AVERAGE SELLING PRICE TREND, BY REGION

- 5.19.2 AVERAGE SELLING PRICE OF HANDHELD ULTRASOUND BY KEY PLAYERS (USD), 2024

- 5.20 REIMBURSEMENT SCENARIO

6 PORTABLE ULTRASOUND MARKET, BY PRODUCT TYPE

- 6.1 INTRODUCTION

- 6.2 TRANSDUCERS/PROBES

- 6.2.1 CURVILINEAR/CONVEX ARRAY

- 6.2.1.1 Allows for wide-field imaging and better visualization of structures at depth

- 6.2.2 LINEAR ARRAY

- 6.2.2.1 Versatile tool in ultrasound imaging

- 6.2.3 PHASED ARRAY

- 6.2.3.1 Ability to steer and focus the portable ultrasound beam electronically to drive growth

- 6.2.4 OTHER ARRAY TYPES

- 6.2.1 CURVILINEAR/CONVEX ARRAY

- 6.3 SYSTEMS & CONSOLES

- 6.3.1 ADVANCED IMAGING CAPABILITIES AND ROBUST PERFORMANCE TO DRIVE GROWTH

- 6.4 ACCESSORIES

- 6.4.1 CRITICAL TO ENSURING IMAGE QUALITY, USER CONVENIENCE, AND INFECTION CONTROL ACROSS CLINICAL ENVIRONMENTS

- 6.5 SOFTWARE & SERVICES

- 6.5.1 ADVANCED FEATURES LIKE REAL-TIME IMAGE GUIDANCE, CLOUD-BASED IMAGE STORAGE AND SHARING, AND AUTOMATED DIAGNOSTICS TO DRIVE GROWTH

7 PORTABLE ULTRASOUND MARKET, BY PLATFORM

- 7.1 INTRODUCTION

- 7.2 TROLLEY/CART BASED

- 7.2.1 INCREASED USE IN ACUTE CARE SETTINGS AND EMERGENCY CARE IN HOSPITALS TO DRIVE GROWTH

- 7.3 HANDHELD

- 7.3.1 INCREASING NUMBER OF TRAUMA/EMERGENCY CASES TO DRIVE DEMAND

- 7.4 LAPTOP BASED

- 7.4.1 ABILITY TO DELIVER NEAR-CART-LEVEL PERFORMANCE IN A COMPACT FORM TO DRIVE GROWTH

- 7.5 TABLET BASED

- 7.5.1 LIGHTWEIGHT AND USER-FRIENDLY DESIGN TO DRIVE DEMAND

8 PORTABLE ULTRASOUND MARKET, BY END USER

- 8.1 INTRODUCTION

- 8.2 HOSPITALS & SURGICAL CENTERS

- 8.2.1 INCREASING NUMBER OF CANCER CASES TO DRIVE DEMAND

- 8.3 IMAGING CENTERS

- 8.3.1 NEED FOR STREAMLINED WORKFLOWS AND POINT-OF-CARE DIAGNOSTICS TO DRIVE GROWTH

- 8.4 AMBULATORY CARE CENTERS

- 8.4.1 INCREASING DEMAND FOR COMPACT PORTABLE ULTRASOUND DEVICES TO DRIVE GROWTH

- 8.5 OTHER END USERS

9 PORTABLE ULTRASOUND MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 OBSTETRICS/GYNECOLOGY

- 9.2.1 ADOPTION OF AI IN PORTABLE ULTRASOUND TO DRIVE SEGMENTAL GROWTH

- 9.3 OTHER APPLICATIONS

- 9.4 CARDIOLOGY

- 9.4.1 RISING PREVALENCE OF CARDIAC DISEASES TO DRIVE DEMAND

- 9.4.2 ORTHOPEDIC AND MUSCULOSKELETAL

- 9.4.2.1 Rising prevalence of osteoarthritis to drive growth

- 9.5 VASCULAR

- 9.5.1 NEED FOR EARLY DETECTION OF VASCULAR DISEASES TO DRIVE GROWTH

- 9.6 PEDIATRIC

- 9.6.1 LEVERAGING PEDIATRIC PORTABLE ULTRASOUND TO COMBAT NEONATAL MORTALITY

- 9.7 UROLOGY

- 9.7.1 PORTABLE ULTRASOUND WIDELY USED IN DIAGNOSIS AND TREATMENT OF VARIOUS UROLOGICAL DISORDERS

- 9.7.2 PAIN MANAGEMENT

- 9.7.2.1 Increasing adoption of portable ultrasound in outpatient settings to drive growth

10 PORTABLE ULTRASOUND MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK

- 10.2.2 US

- 10.2.2.1 Presence of advanced healthcare infrastructure to drive market

- 10.2.3 CANADA

- 10.2.3.1 New product launch & conference events to drive market

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK

- 10.3.2 GERMANY

- 10.3.2.1 Rapid expansion in applications of portable ultrasound technologies to drive market

- 10.3.3 UK

- 10.3.3.1 Increase in awareness about different diagnostic imaging procedures to drive market

- 10.3.4 FRANCE

- 10.3.4.1 Increasing demand for portable ultrasound devices for routine health check-ups, prenatal care, and diagnostic procedures to drive market

- 10.3.5 ITALY

- 10.3.5.1 Increased availability of reimbursement coverage for diagnostic procedures to drive market

- 10.3.6 SPAIN

- 10.3.6.1 Growing adoption of point-of-care portable ultrasound to drive market

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK

- 10.4.2 CHINA

- 10.4.2.1 Emphasis on modernization and expansion of rural healthcare infrastructure to drive market

- 10.4.3 JAPAN

- 10.4.3.1 Established healthcare infrastructure and research facilities to drive market

- 10.4.4 INDIA

- 10.4.4.1 Rising adoption of advanced diagnostic imaging technologies to drive market

- 10.4.5 AUSTRALIA

- 10.4.5.1 Increasing investments in healthcare infrastructure to drive market

- 10.4.6 SOUTH KOREA

- 10.4.6.1 Rising investments in disease diagnostic system development to drive market

- 10.4.7 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 MACROECONOMIC OUTLOOK

- 10.5.2 BRAZIL

- 10.5.2.1 Growing adoption of healthcare insurance to drive market

- 10.5.3 MEXICO

- 10.5.3.1 Investment in portable ultrasound devices to drive market

- 10.5.4 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 MACROECONOMIC OUTLOOK

- 10.6.2 GCC COUNTRIES

- 10.6.2.1 Government initiatives aimed at digital health and telemedicine to drive market

- 10.6.3 REST OF MIDDLE EAST & AFRICA

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN PORTABLE ULTRASOUND MARKET

- 11.3 REVENUE ANALYSIS, 2021-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.4.1 RANKING OF KEY MARKET PLAYERS

- 11.5 COMPANY EVALUATION MATRIX: PORTABLE ULTRASOUND MARKET, 2024

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- 11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.5.5.1 Company footprint

- 11.5.5.2 Product type footprint

- 11.5.5.3 Platform footprint

- 11.5.5.4 Application footprint

- 11.5.5.5 End user footprint

- 11.5.5.6 Region footprint

- 11.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES (2024)

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- 11.7 COMPANY VALUATION AND FINANCIAL METRICS

- 11.7.1 FINANCIAL METRICS

- 11.7.2 COMPANY VALUATION

- 11.8 BRAND/PRODUCT COMPARISON

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES & APPROVALS

- 11.9.2 DEALS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 GE HEALTHCARE

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches

- 12.1.1.3.2 Deals

- 12.1.1.3.3 Other developments

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses & competitive threats

- 12.1.2 PHILIPS HEALTHCARE

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches

- 12.1.2.3.2 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses & competitive threats

- 12.1.3 CANON MEDICAL SYSTEMS CORPORATION

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches

- 12.1.3.3.2 Deals

- 12.1.3.3.3 Expansions

- 12.1.3.4 MnM view

- 12.1.3.4.1 Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses & competitive threats

- 12.1.4 SIEMENS HEALTHINEERS AG

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches

- 12.1.4.3.2 Deals

- 12.1.4.3.3 Expansions

- 12.1.4.4 MnM view

- 12.1.4.4.1 Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses & competitive threats

- 12.1.5 FUJIFILM CORPORATION

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches

- 12.1.5.3.2 Deals

- 12.1.5.3.3 Expansions

- 12.1.5.4 MnM view

- 12.1.5.4.1 Right to win

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses & competitive threats

- 12.1.6 HOLOGIC, INC.

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches

- 12.1.6.3.2 Deals

- 12.1.6.3.3 Expansions

- 12.1.7 SAMSUNG ELECTRONICS CO., LTD.

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Product launches

- 12.1.7.3.2 Deals

- 12.1.7.3.3 Other developments

- 12.1.8 MINDRAY MEDICAL INTERNATIONAL LIMITED

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Product launches

- 12.1.8.3.2 Deals

- 12.1.9 ESAOTE SPA

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Product launches

- 12.1.9.3.2 Other developments

- 12.1.10 CHISON MEDICAL TECHNOLOGIES CO., LTD.

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Product launches

- 12.1.10.3.2 Deals

- 12.1.11 NEUSOFT CORPORATION

- 12.1.11.1 Business overview

- 12.1.11.2 Products offered

- 12.1.11.3 Recent developments

- 12.1.11.3.1 Product launches

- 12.1.12 KONICA MINOLTA, INC.

- 12.1.12.1 Business overview

- 12.1.12.2 Products offered

- 12.1.12.3 Recent developments

- 12.1.12.3.1 Product launches

- 12.1.12.3.2 Deals

- 12.1.13 CLARIUS

- 12.1.13.1 Business overview

- 12.1.13.2 Products offered

- 12.1.13.3 Recent developments

- 12.1.13.3.1 Product launches and approvals

- 12.1.13.3.2 Deals

- 12.1.14 MEDGYN PRODUCTS, INC.

- 12.1.14.1 Business overview

- 12.1.14.1.1 Products offered

- 12.1.14.1 Business overview

- 12.1.15 PROMED TECHNOLOGY CO., LTD.

- 12.1.15.1 Business overview

- 12.1.15.2 Products offered

- 12.1.1 GE HEALTHCARE

- 12.2 OTHER COMPANIES

- 12.2.1 WHITE EAGLE SONIC TECHNOLOGIES, INC.

- 12.2.2 PERLONG MEDICAL EQUIPMENT CO., LTD.

- 12.2.3 YOUKEY MEDICAL

- 12.2.4 SIUI

- 12.2.5 TELEMED, MEDICAL IMAGING EQUIPMENT DESIGN & MANUFACTURING

- 12.2.6 BUTTERFLY NETWORK, INC.

- 12.2.7 ALPINION MEDICAL SYSTEMS

- 12.2.8 EDAN INSTRUMENTS, INC.

- 12.2.9 SHENZHEN LANDWIND INDUSTRY CO., LTD

- 12.2.10 ECHONOUS INC.

- 12.2.11 MOBISANTE

- 12.2.12 SHENZHEN WISONIC MEDICAL TECHNOLOGY CO., LTD

- 12.2.13 SHENZHEN BIOCARE BIO-MEDICAL EQUIPMENT CO., LTD

- 12.2.14 SONOSCAPE MEDICAL CORP

- 12.2.15 CURA HEALTHCARE

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS