|

시장보고서

상품코드

1808965

면역분석 시장 : 제품별, 기술별, 검체별, 용도별, 최종 사용자별, 지역별 예측(-2030년)Immunoassay Market by Product (Reagents & Kits, Analyzers), Technology (ELISA, CLIA, Western Blot), Specimen (Blood, Saliva, Urine), Application (Infectious Diseases, Endocrinology), End User (Hospitals & Clinics, Laboratories) - Global Forecast to 2030 |

||||||

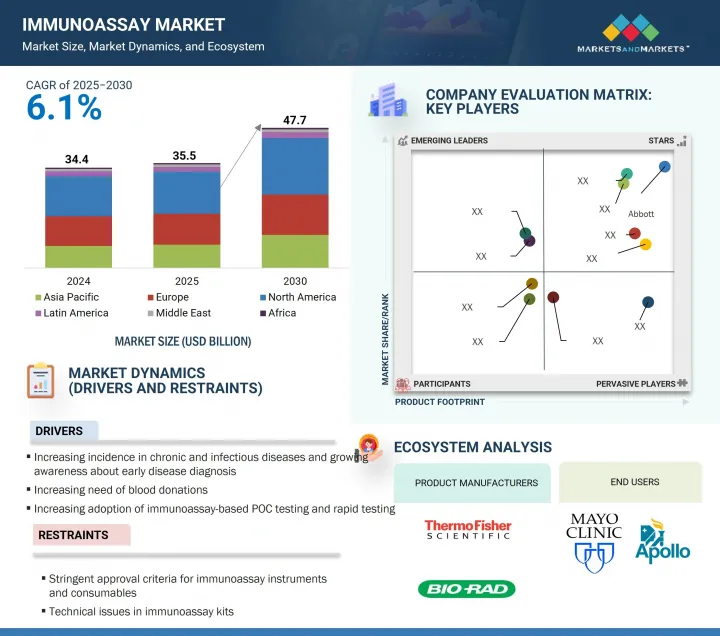

세계의 면역분석 시장 규모는 2025년 355억 달러로 추정되고, 예측 기간 중 CAGR 6.1%로 전망되고 있으며, 2030년에는 477억 달러에 달할 것으로 예측되고 있습니다.

이 성장을 가속하는 주요 요인으로는 만성 질환 및 감염증 증가, 면역분석 시스템의 지속적인 기술 진보, 정부의 지원 정책, 엄격한 규제에 의한 약물 및 알코올 검사의 중의 고조 등이 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(10억 달러) |

| 부문 | 제품별, 기술별, 시료별, 용도별, 최종 사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

제품별로, 세계의 면역분석 시장은 시약 및 키트와 분석 장치로 구분됩니다. 시약 및 키트는 진단 시장에서 가장 중요한 부문이며, 주된 이유는 광범위한 진단 분석에 자주 사용되기 때문입니다. 이러한 소모품에 대한 지속적인 수요는 면역분석법의 세계적인 보급이 배경에 있습니다. 게다가 진단 정확도 및 작업 효율을 향상시키는 고성능 시약 및 키트의 도입은 보다 광범위한 도입을 촉진하고 이 분야의 성장에 박차를 가하고 있습니다.

면역분석 시장은 기술별로 ELISA법, 화학발광 면역분석법(CLIA법), 면역형광측정법(IFA법), 신속검사법, ELISpot법, 웨스턴 블롯법, 기타 방법으로 분류됩니다. CLIA(Chemical Lighting Immunoassay) 분야는 주로 만성 질환과 감염에 모두 적용할 수 있는 진보된 진단 능력으로 인해 상당한 성장이 예상됩니다. ELISA(Enzyme-Linked Immunosorbent Assay) 및 라디오 면역분석과 같은 기존의 방법과 비교할 때 CLIA는 뛰어난 감도, 넓은 동적 범위, 신속한 배달, 백그라운드 간섭 최소화, 특이성 향상을 보여줍니다. 이러한 특성으로 인해 CLIA는 특히 높은 정확도 및 신뢰성이 요구되는 임상 진단에서 선호되는 선택입니다.

세계의 면역분석 시장은 용도별로 감염증, 순환기, 내분비, 종양, 뼈 및 미네랄 질환, 자가면역질환, 혈액 스크리닝, 알레르기 진단, 약물 모니터링 및 검사, 신생아 스크리닝 등으로 분류됩니다. 2022년, 진단 검사 시장은 감염에 크게 영향을 받았습니다. HIV/AIDS, 간염, 말라리아, 인플루엔자 등의 이환율 증가가 주요 원인입니다. 면역분석법의 이용은 이러한 추세에서 중요한 역할을 합니다. 이러한 추세는 신속하고 정확한 진단을 용이하게 하여 세계 감염 유행의 관리를 강화하기 때문입니다.

면역분석 시장은 지역별로 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카로 구분됩니다. 예측 기간 동안 아시아태평양이 가장 큰 성장을 이룰 것으로 예측됩니다. 이 급증은 상호 연관된 여러 요인으로 인해 발생합니다. 즉, 환자 인구의 대폭적인 확대, 만성 질환의 유병률의 상승, 질병의 조기 발견의 중요성에 대한 의식 증가, 중국, 헬스케어, 동남아시아 국가 등에서의 의료 인프라의 지속적인 강화 등입니다.

본 보고서에서는 세계의 면역분석 시장에 대해 조사했으며, 제품별, 기술별, 검체별, 용도별, 최종 사용자별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 서문

- 시장 역학

- 규제 분석

- 기술 분석

- 무역 분석

- 특허 분석

- 밸류체인 분석

- 공급망 분석

- 생태계 분석

- Porter's Five Forces 분석

- 주요 이해관계자 및 구매 기준

- 주된 회의 및 이벤트(2025-2026년)

- 가격 분석

- 고객의 비즈니스에 영향을 미치는 동향 및 혼란

- 사례 연구 분석

- 투자 및 자금조달 시나리오

- AI 및 생성형 AI가 면역분석 시장에 미치는 영향

- 미국 관세가 면역분석 시장에 미치는 영향(2025년)

제6장 면역분석 시장 : 제품별

- 서문

- 시약 및 키트

- 분석기

제7장 면역분석 시장 : 기술별

- 서문

- ELISA

- CLIA

- IFA

- 신속 검사

- 웨스턴 블로팅

- ELISpot

- 기타

제8장 면역분석 시장 : 검체별

- 서문

- 혈액

- 타액

- 소변

- 기타

제9장 면역분석 시장 : 용도별

- 서문

- 감염증

- 내분비학

- 심장병학

- 자가면역질환

- 알레르기 진단

- 종양학

- 뼈 및 미네랄 질환

- 약물 모니터링 및 검사

- 혈액검사

- 신생아 스크리닝

- 기타

제10장 면역분석 시장 : 최종 사용자별

- 서문

- 병원 및 클리닉

- 임상 실험실

- 재택 케어

- 혈액 은행

제11장 면역분석 시장 : 지역별

- 서문

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 거시 경제 전망

- 독일

- 이탈리아

- 프랑스

- 스페인

- 영국

- 러시아

- 기타

- 아시아태평양

- 아시아태평양의 거시 경제 전망

- 일본

- 중국

- 인도

- 호주

- 한국

- 인도네시아

- 기타

- 라틴아메리카

- 라틴아메리카의 거시 경제 전망

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- 숙련된 연구실 직원의 부족 및 불리한 상환 정책이 시장 성장 제한

제12장 경쟁 구도

- 서문

- 주요 진입기업의 전략 및 강점

- 수익 분석(2020-2024년)

- 시장 점유율 분석(2024년)

- 기업 평가 매트릭스 : 주요 진입기업(2024년)

- 기업 평가 매트릭스 : 스타트업 및 중소기업(2024년)

- 기업 평가 및 재무지표

- 브랜드 및 제품 비교

- 경쟁 시나리오

제13장 기업 프로파일

- 주요 진출기업

- ABBOTT

- F. HOFFMANN-LA ROCHE LTD.

- SIEMENS HEALTHINEERS AG

- DANAHER

- THERMO FISHER SCIENTIFIC INC.

- REVVITY

- BECTON, DICKINSON AND COMPANY(BD)

- DIASORIN SPA

- BIO-RAD LABORATORIES, INC.

- QUIDELORTHO CORPORATION

- BIOMERIEUX

- QIAGEN

- SYSMEX CORPORATION

- AGILENT TECHNOLOGIES, INC.

- SHENZHEN MINDRAY BIO-MEDICAL ELECTRONICS CO., LTD.

- 기타 기업

- MERCK KGAA

- MERIDIAN BIOSCIENCE

- BIO-TECHNE

- CELLABS

- ABNOVA CORPORATION

- J. MITRA & CO. PVT. LTD.

- TOSOH CORPORATION(TOSOH BIOSCIENCES)

- CELL SCIENCES

- ENZO BIOCHEM INC.

- CREATIVE DIAGNOSTICS

- BOSTER BIOLOGICAL TECHNOLOGY

- ELABSCIENCE BIONOVATON INC.

- WAK-CHEMIE MEDICAL GMBH

- SERA CARE

- EPITOPE DIAGNOSTICS, INC.

- KAMIYA BIOMEDICAL COMPANY

- GYROS PROTEIN TECHNOLOGIES AB

- TRIVITRON HEALTHCARE

- INBIOS INTERNATIONAL, INC.

- MACCURA BIOTECHNOLOGY CO., LTD.

제14장 부록

AJY 25.09.16The global immunoassay market is valued at an estimated USD 35.5 billion in 2025 and is projected to reach USD 47.7 billion by 2030, at a CAGR of 6.1% during the forecast period. Key factors driving this growth include the increasing rates of chronic and infectious diseases, continuous technological progress in immunoassay systems, supportive government policies, and a growing emphasis on drug and alcohol testing due to strict regulations.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product, Technology, Specimen, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, the Middle East & Africa |

"The reagents & kits accounted for the largest share of the immunoassay products market."

On the basis of products, the global immunoassay market is segmented into reagents & kits and analyzers. Reagents & kits represent the most substantial segment in the diagnostic market, primarily due to their frequent application in a wide array of diagnostic assays. The ongoing demand for these consumables is fueled by the increasing global incidence of immunoassay procedures. Furthermore, the introduction of high-performance reagents and kits, which enhance diagnostic precision and operational efficiency, has facilitated their broader adoption and subsequently spurred growth within this sector.

"The chemiluminescence Immunoassay (CLIA) segment is projected to grow at a considerable rate in the immunoassay technology segment during the forecast period."

The immunoassay market is categorized by technology into ELISA, chemiluminescence immunoassay (CLIA), immunofluorescence assay (IFA), rapid tests, ELISpot, western blotting, and other methods. The CLIA (Chemiluminescent Immunoassays) segment is forecasted to experience substantial growth, largely due to its advanced diagnostic capabilities applicable to both chronic and infectious diseases. When contrasted with conventional methods like ELISA (Enzyme-Linked Immunosorbent Assay) and radioimmunoassays, CLIA demonstrates superior sensitivity, an extended dynamic range, expedited turnaround times, minimized background interference, and enhanced specificity. These attributes make CLIA the preferred choice for clinical diagnostics, particularly in situations demanding high accuracy and reliability.

"Infectious diseases held the largest share of the immunoassay applications market."

The global immunoassay market is categorized by application into infectious diseases, cardiology, endocrinology, oncology, bone & mineral disorders, autoimmune disorders, blood screening, allergy diagnostics, drug monitoring & testing, newborn screening, and other applicatons. In 2022, the market for diagnostic testing was predominantly influenced by infectious diseases, largely due to the increasing incidence of conditions like HIV/AIDS, hepatitis, malaria, and influenza. The utilization of immunoassays has played a critical role in this trend, as these tests facilitate rapid and precise diagnoses, thereby enhancing the management of global infectious disease outbreaks.

"Asia Pacific is expected to be the fastest-growing region in the immunoassay market."

The immunoassay market is regionally segmented into North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. The Asia Pacific region is anticipated to experience the most significant growth during the forecast period. This rapid expansion can be attributed to several interrelated factors: a substantial and expanding patient demographic, an escalating prevalence of chronic diseases, heightened awareness of the importance of early disease detection, and continuous enhancements in healthcare infrastructure in nations such as China, India, and various Southeast Asian countries.

The break-up of the profile of primary participants in the immunoassay market:

- By Respondent: Tier 1-25%, Tier 2-35%, and Tier 3- 40%

- By Designation: CXOs and Directors- 30%, Managers- 45%, and Executives- 25%

- By Region: North America -35%, Europe - 25%, Asia Pacific -15%, Latin America -10%, Middle East- 10%, and Africa- 5%

The key players in this market are Abbott (US), F. Hoffmann-La Roche Ltd. (Switzerland), Siemens Healthineers AG (Germany), Danaher (US), Thermo Fisher Scientific Inc. (US), Revvity (US), Becton, Dickinson and Company (BD) (US), DiaSorin S.p.A (Italy), Bio-Rad Laboratories, Inc. (US), QuidelOrtho Corporation (US), bioMerieux (France), QIAGEN (Germany), Sysmex Corporation (Japan), Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China), Agilent Technologies, Inc. (US), Merck KGaA (Germany), Meridian Bioscience (US), Bio-Techne (US), Cellabs (Australia), Abnova Corporation (Taiwan), J. Mitra & Co. Pvt. Ltd. (India), Tosoh Corporation (Japan), Cell Sciences (US), Enzo Biochem (US), Creative Diagnostics (US), Boster Biological Technology (US), Elabscience (US), WAK-Chemie Medical GmbH (Germany), Sera Care (US), Epitope Diagnostics Inc. (US), Kamiya Biomedical Company (US), Gyros Protein Technologies (Sweden), Trivitron Healthcare (India), InBios International Inc. (India), and Maccura Biotechnology Co., Ltd. (China).

Research Coverage:

This research report categorizes the immunoassay market by product (reagents & kits and analyzers), specimen (blood, urine, saliva, and other specimens), technology (ELISA, CLIA, IFA, rapid tests, ELISpot, western blotting, and other technologies), application (infectious diseases, blood screening, oncology, endocrinology, bone & mineral disorders, autoimmune disorders, cardiology, drug monitoring & testing, allergy diagnostics, newborn screening, and other applications), end user (clinical laboratories, hospitals & clinics, blood banks, and home care settings), and region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The scope of the report covers detailed information regarding the major factors such as drivers, restraints, opportunities, and challenges influencing the growth of the immunoassay market. A detailed analysis of the key industry players has been conducted to provide insights into their business overview, products offered, key strategies, acquisitions, and partnerships. New product launches and approvals, as well as recent developments associated with the immunoassay market, are also included. This report covers the competitive landscape of upcoming startups in the immunoassay market ecosystem.

Key Benefits of Buying the Report:

The report provides market leaders and new entrants with estimates of revenue figures for the overall immunoassay market and its subsegments. It helps stakeholders understand the competitive landscape and gain insights to better position their businesses and develop effective go-to-market strategies. Additionally, the report offers insights into market dynamics, including key drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (increasing incidence of chronic and infectious diseases and growing awareness about early disease diagnosis, growth in biotechnology and biopharmaceutical industries, supportive government policies, increasing adoption of immunoassay-based poc testing and rapid testing, increasing drug and alcohol abuse and stringent laws mandating drug and alcohol testing), restraints (stringent requirements for approval of immunoassay instruments and consumables, technical hurdles of immunoassay kits), opportunities (growth opportunities in emerging economies, importance of companion diagnostics, development of condition-specific biomarkers and tests, integration of microfluidics in immunoassays, improving immunoassay diagnostic technologies), and challenges (design challenges, complexities, and quality of antibodies, dearth of skilled professionals, unfavorable reimbursement scenario, influencing the growth of the immunoassay market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the immunoassay market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the immunoassay market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the immunoassay market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as Abbott (US), F. Hoffmann-La Roche Ltd. (Switzerland), Siemens Healthineers AG (Germany), Danaher (US), and Bio-Rad Laboratories, Inc. (US), among others, in the immunoassay market strategies.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY RESEARCH

- 2.1.1.1 Key secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY RESEARCH

- 2.1.2.1 Key primary sources

- 2.1.2.2 Key objectives of primary research

- 2.1.2.3 Key data from primary sources

- 2.1.2.4 Key industry insights

- 2.1.1 SECONDARY RESEARCH

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 COMPANY PRESENTATIONS & PRIMARY INTERVIEWS

- 2.2.3 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 MARKET SHARE ANALYSIS

- 2.5 STUDY ASSUMPTIONS

- 2.5.1 MARKET ASSUMPTIONS

- 2.5.2 GROWTH RATE ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.6.1 METHODOLOGY-RELATED LIMITATIONS

- 2.6.2 SCOPE-RELATED LIMITATIONS

- 2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 IMMUNOASSAY MARKET OVERVIEW

- 4.2 NORTH AMERICA: IMMUNOASSAY MARKET, BY PRODUCT AND COUNTRY

- 4.3 IMMUNOASSAY MARKET: GEOGRAPHICAL SNAPSHOT

- 4.4 IMMUNOASSAY MARKET: REGIONAL MIX

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing incidence of chronic and infectious diseases

- 5.2.1.1.1 Increased use of immunoassays in oncology

- 5.2.1.1.2 Rising use of immunoassays in diagnostic applications

- 5.2.1.1.3 High geriatric population

- 5.2.1.2 Increased demand for blood donations in healthcare systems and surgical procedures

- 5.2.1.3 Growth in biotechnology & biopharmaceutical industries

- 5.2.1.4 Increasing adoption of immunoassay-based POC and rapid testing

- 5.2.1.5 Supportive government regulatory policies and initiatives

- 5.2.1.6 Increased consumption of drugs, alcohol, and cannabis

- 5.2.1.1 Increasing incidence of chronic and infectious diseases

- 5.2.2 RESTRAINTS

- 5.2.2.1 Stringent requirements for approval of immunoassay instruments and consumables

- 5.2.2.2 Technical hurdles of immunoassay kits

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing growth opportunities in emerging economies

- 5.2.3.2 Focus on importance of companion diagnostics

- 5.2.3.3 Development of condition-specific biomarkers and tests

- 5.2.3.4 Integration of microfluidics in immunoassays

- 5.2.3.5 Improving immunoassay diagnostic technologies

- 5.2.4 CHALLENGES

- 5.2.4.1 Design challenges and low quality of antibodies

- 5.2.4.2 Dearth of skilled professionals

- 5.2.1 DRIVERS

- 5.3 REGULATORY ANALYSIS

- 5.3.1 REGULATORY FRAMEWORK

- 5.3.1.1 North America

- 5.3.1.1.1 US

- 5.3.1.1.2 Canada

- 5.3.1.2 Europe

- 5.3.1.2.1 Russia

- 5.3.1.3 Asia Pacific

- 5.3.1.3.1 Japan

- 5.3.1.3.2 China

- 5.3.1.3.3 India

- 5.3.1.3.4 Indonesia

- 5.3.1.3.5 South Korea

- 5.3.1.4 Middle East

- 5.3.1.4.1 Saudi Arabia

- 5.3.1.5 Latin America

- 5.3.1.5.1 Mexico

- 5.3.1.5.2 Brazil

- 5.3.1.6 Africa

- 5.3.1.1 North America

- 5.3.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.3.1 REGULATORY FRAMEWORK

- 5.4 TECHNOLOGY ANALYSIS

- 5.4.1 KEY TECHNOLOGIES

- 5.4.1.1 ELISA

- 5.4.2 ADJACENT TECHNOLOGIES

- 5.4.2.1 Microfluidics and miniaturized platforms

- 5.4.3 COMPLEMENTARY TECHNOLOGIES

- 5.4.3.1 Lateral flow assays

- 5.4.1 KEY TECHNOLOGIES

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT DATA FOR HS CODE 382200, 2019-2024

- 5.5.2 EXPORT DATA FOR HS CODE 382200, 2019-2024

- 5.6 PATENT ANALYSIS

- 5.7 VALUE CHAIN ANALYSIS

- 5.8 SUPPLY CHAIN ANALYSIS

- 5.9 ECOSYSTEM ANALYSIS

- 5.9.1 ROLE IN ECOSYSTEM

- 5.10 PORTER'S FIVE FORCES ANALYSIS

- 5.10.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.10.2 BARGAINING POWER OF SUPPLIERS

- 5.10.3 BARGAINING POWER OF BUYERS

- 5.10.4 THREAT OF SUBSTITUTES

- 5.10.5 THREAT OF NEW ENTRANTS

- 5.11 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.11.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.11.2 KEY BUYING CRITERIA

- 5.12 KEY CONFERENCES & EVENTS, 2025-2026

- 5.13 PRICING ANALYSIS

- 5.13.1 AVERAGE SELLING PRICE TREND OF IMMUNOASSAY PRODUCTS, BY KEY PLAYER, 2022-2024

- 5.13.2 AVERAGE SELLING PRICE TREND OF IMMUNOASSAY ANAYZERS, BY REGION, 2022-2024

- 5.13.3 AVERAGE SELLING PRICE TREND OF IMMUNOASSAY PRODUCTS, BY TYPE, 2022-2024

- 5.14 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.15 CASE STUDY ANALYSIS

- 5.15.1 PORTABLE MICROFLUIDIC CHEMILUMINESCENT IMMUNOASSAY TO BE USED FOR RAPID COVID 19 IMMUNITY MONITORING

- 5.15.2 MICROFLUIDIC-BASED IMMUNOASSAY TO HELP IN EARLY CANCER DETECTION

- 5.15.3 LUMINEX-BASED MULTIPLEX IMMUNOASSAY TO AID AUTOIMMUNE DISEASE PROFILING

- 5.16 INVESTMENT & FUNDING SCENARIO

- 5.17 IMPACT OF AI/GEN AI ON IMMUNOASSAY MARKET

- 5.17.1 MARKET POTENTIAL FOR IMMUNOASSAY PRODUCTS

- 5.17.2 FUTURE OF AI/GEN AI IN IMMUNOASSAY MARKET

- 5.18 IMPACT OF 2025 US TARIFF ON IMMUNOASSAY MARKET

- 5.18.1 INTRODUCTION

- 5.18.2 KEY TARIFF RATES

- 5.18.3 PRICE IMPACT ANALYSIS

- 5.18.4 IMPACT ON COUNTRY/REGION

- 5.18.4.1 North America

- 5.18.4.1.1 US

- 5.18.4.2 Europe

- 5.18.4.2.1 Germany

- 5.18.4.2.2 UK and France

- 5.18.4.3 Asia Pacific

- 5.18.4.3.1 China

- 5.18.4.3.2 Japan

- 5.18.4.3.3 India

- 5.18.4.1 North America

- 5.18.5 IMPACT ON END-USE INDUSTRIES

- 5.18.5.1 Hospitals & clinics

- 5.18.5.2 Clinical laboratories

- 5.18.5.3 Blood banks

- 5.18.5.4 Home care settings

6 IMMUNOASSAY MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- 6.2 REAGENTS & KITS

- 6.2.1 ELISA REAGENTS & KITS

- 6.2.1.1 Increased use of high-throughput screening in drug discovery programs to drive segment

- 6.2.2 RAPID TEST REAGENTS & KITS

- 6.2.2.1 High demand for preliminary screening tests in remote areas to propel segment growth

- 6.2.3 ELISPOT REAGENTS & KITS

- 6.2.3.1 High sensitivity, functionality, and adaptability of ELISpot technology to aid segment growth

- 6.2.4 CLIA REAGENTS & KITS

- 6.2.4.1 Better diagnosis and higher specificity to augment segment growth

- 6.2.5 IFA REAGENTS & KITS

- 6.2.5.1 Better adaptability in clinical diagnostics to support segment growth

- 6.2.6 WESTERN BLOT REAGENTS & KITS

- 6.2.6.1 Western blot reagents & kits to be considered gold standard for infectious disease test result validation

- 6.2.7 OTHER REAGENTS & KITS

- 6.2.1 ELISA REAGENTS & KITS

- 6.3 ANALYZERS

- 6.3.1 IMMUNOASSAY ANALYZERS MARKET, BY TYPE

- 6.3.1.1 Open-ended systems

- 6.3.1.1.1 Better flexibility and wider availability to drive segment growth

- 6.3.1.2 Closed-ended systems

- 6.3.1.2.1 Higher precision and better automation to fuel segment growth

- 6.3.1.1 Open-ended systems

- 6.3.2 IMMUNOASSAY ANALYZERS MARKET, BY PURCHASE MODE

- 6.3.2.1 Rental purchase

- 6.3.2.1.1 Increased convenience and reduced liability to boost segment growth

- 6.3.2.2 Outright purchase

- 6.3.2.2.1 Inflated cost of immunoassay testing technologies to limit market growth

- 6.3.2.1 Rental purchase

- 6.3.1 IMMUNOASSAY ANALYZERS MARKET, BY TYPE

7 IMMUNOASSAY MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- 7.2 ELISA

- 7.2.1 BETTER SENSITIVITY AND QUICKER RESULTS TO DRIVE MARKET

- 7.3 CLIA

- 7.3.1 GOOD SPECIFICITY, WIDE LINEAR RANGE, AND HIGH SENSITIVITY TO AID MARKET GROWTH

- 7.4 IFA

- 7.4.1 IFA TO DIAGNOSE ANTIBODIES AND ANALYZE SMALL BIOLOGICAL AND NON-BIOLOGICAL MOLECULES

- 7.5 RAPID TESTS

- 7.5.1 FASTER RESULTS AND EASE OF USE TO DRIVE ADOPTION IN POINT-OF-CARE DIAGNOSIS AND EMERGENCY CARE SETTINGS

- 7.6 WESTERN BLOTTING

- 7.6.1 ABILITY TO DETECT AND CONFIRM ANTIBODIES OF RETROVIRUSES TO SPUR MARKET GROWTH

- 7.7 ELISPOT

- 7.7.1 HIGH SENSITIVITY, SPECIFICITY, AND VERSATILITY TO PROPEL MARKET GROWTH

- 7.8 OTHER TECHNOLOGIES

8 IMMUNOASSAY MARKET, BY SPECIMEN

- 8.1 INTRODUCTION

- 8.2 BLOOD

- 8.2.1 HIGH RELIABILITY AND INCREASED NEED DURING SURGICAL PROCEDURES TO AID MARKET GROWTH

- 8.3 SALIVA

- 8.3.1 ADVANCEMENTS IN IMMUNOASSAY-BASED SALIVA TESTS TO AUGMENT MARKET GROWTH

- 8.4 URINE

- 8.4.1 INCREASING USE BY LAW ENFORCEMENT AGENCIES AND RISING PREVALENCE OF KIDNEY DISEASES TO FAVOR MARKET GROWTH

- 8.5 OTHER SPECIMENS

9 IMMUNOASSAY MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 INFECTIOUS DISEASES

- 9.2.1 RISING PREVALENCE OF CHRONIC INFECTIOUS DISEASES TO DRIVE MARKET

- 9.3 ENDOCRINOLOGY

- 9.3.1 RISING INCIDENCE OF DIABETES TO AUGMENT MARKET GROWTH

- 9.4 CARDIOLOGY

- 9.4.1 HIGH BURDEN OF CARDIOVASCULAR DISEASES TO SUPPORT MARKET GROWTH

- 9.5 AUTOIMMUNE DISORDERS

- 9.5.1 HIGH INCIDENCE AND PREVALENCE OF AUTOIMMUNE DISEASES TO AUGMENT MARKET GROWTH

- 9.6 ALLERGY DIAGNOSTICS

- 9.6.1 GROWING PREVALENCE OF ALLERGIES TO AID MARKET GROWTH

- 9.7 ONCOLOGY

- 9.7.1 RISING BURDEN OF CANCER AND GROWING EMPHASIS ON EARLY DETECTION TO PROPEL MARKET GROWTH

- 9.8 BONE & MINERAL DISORDERS

- 9.8.1 INCREASING PREVALENCE OF OSTEOPOROSIS, VITAMIN D DEFICIENCY, AND ARTHRITIS TO AID MARKET GROWTH

- 9.9 DRUG MONITORING & TESTING

- 9.9.1 RISING DRUG ABUSE AND INCREASING ILLICIT DRUG CONSUMPTION TO ACCELERATE MARKET GROWTH

- 9.10 BLOOD SCREENING

- 9.10.1 RISING EMPHASIS ON BLOOD DONATIONS TO FAVOR MARKET GROWTH

- 9.11 NEWBORN SCREENING

- 9.11.1 TECHNOLOGICAL ADVANCEMENTS AND FAVORABLE GOVERNMENT INITIATIVES TO PROPEL MARKET GROWTH

- 9.12 OTHER APPLICATIONS

10 IMMUNOASSAY MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 HOSPITALS & CLINICS

- 10.2.1 GROWING PATIENT POPULATION AND RISING TESTING VOLUME TO DRIVE MARKET

- 10.3 CLINICAL LABORATORIES

- 10.3.1 INCREASING NUMBER OF ACCREDITED LABORATORIES TO DRIVE MARKET

- 10.4 HOME CARE SETTINGS

- 10.4.1 RISING UTILIZATION OF POC DIAGNOSTICS AND AT-HOME ANTIGEN DIAGNOSIS TO PROPEL MARKET GROWTH

- 10.5 BLOOD BANKS

- 10.5.1 INCREASING NUMBER OF ACCIDENTS AND RISING DEMAND FOR BLOOD DURING SURGERIES TO SPUR MARKET GROWTH

11 IMMUNOASSAY MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 11.2.2 US

- 11.2.2.1 US to dominate North American immunoassay market during forecast period

- 11.2.3 CANADA

- 11.2.3.1 Increasing government support and rising incidence of chronic diseases to augment market growth

- 11.3 EUROPE

- 11.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 11.3.2 GERMANY

- 11.3.2.1 High healthcare spending and favorable government initiatives to propel market growth

- 11.3.3 ITALY

- 11.3.3.1 Rising geriatric population and increasing cancer prevalence to spur market growth

- 11.3.4 FRANCE

- 11.3.4.1 Increased use of POC testing and favorable reimbursement policies to boost market growth

- 11.3.5 SPAIN

- 11.3.5.1 Increasing adoption of technologically advanced immunoassay systems to augment market growth

- 11.3.6 UK

- 11.3.6.1 Government support for disease diagnostics and favorable investment scenario to drive market

- 11.3.7 RUSSIA

- 11.3.7.1 Increasing access to quality healthcare and developing pharmaceutical industry to favor market growth

- 11.3.8 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 11.4.2 JAPAN

- 11.4.2.1 Increasing investments in healthcare technologies and research activities to fuel market growth

- 11.4.3 CHINA

- 11.4.3.1 Increasing government investments and rising geriatric population to accelerate maket growth

- 11.4.4 INDIA

- 11.4.4.1 Growing medical tourism and improving healthcare infrastructure to propel market growth

- 11.4.5 AUSTRALIA

- 11.4.5.1 Increasing incidence of cancer and rising focus on blood donations to favor market growth

- 11.4.6 SOUTH KOREA

- 11.4.6.1 Rising healthcare spending and increasing research investments to fuel market growth

- 11.4.7 INDONESIA

- 11.4.7.1 High geriatric population and favorable government healthcare policies to accelerate market growth

- 11.4.8 REST OF ASIA PACIFIC

- 11.5 LATIN AMERICA

- 11.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 11.5.2 BRAZIL

- 11.5.2.1 High incidence of infectious diseases and presence of academic & research institutes to boost market growth

- 11.5.3 MEXICO

- 11.5.3.1 Increasing geriatric population and rising popularity of medical tourism to propel market growth

- 11.5.4 REST OF LATIN AMERICA

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 LACK OF SKILLED LABORATORY PERSONNEL AND UNFAVORABLE REIMBURSEMENT POLICIES TO LIMIT MARKET GROWTH

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.2.1 OVERVIEW OF KEY STRATEGIES ADOPTED BY MAJOR PLAYERS IN IMMUNOASSAY MARKET

- 12.3 REVENUE ANALYSIS, 2020-2024

- 12.4 MARKET SHARE ANALYSIS, 2024

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.5.5.1 Company footprint

- 12.5.5.2 Region footprint

- 12.5.5.3 Product footprint

- 12.5.5.4 Specimen footprint

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- 12.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.6.5.1 List of key startups/SMEs

- 12.6.5.2 Competitive benchmarking of key startups/SMEs

- 12.7 COMPANY VALUATION & FINANCIAL METRICS

- 12.7.1 FINANCIAL METRICS

- 12.7.2 COMPANY VALUATION

- 12.8 BRAND/PRODUCT COMPARISON

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES/APPROVALS/ ENHANCEMENTS

- 12.9.2 DEALS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 ABBOTT

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product approvals

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansions

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses & competitive threats

- 13.1.2 F. HOFFMANN-LA ROCHE LTD.

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches and approvals

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses & competitive threats

- 13.1.3 SIEMENS HEALTHINEERS AG

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches and approvals

- 13.1.3.3.2 Deals

- 13.1.3.3.3 Expansions

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses & competitive threats

- 13.1.4 DANAHER

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches and approvals

- 13.1.4.3.2 Deals

- 13.1.4.3.3 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses & competitive threats

- 13.1.5 THERMO FISHER SCIENTIFIC INC.

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product approvals

- 13.1.5.3.2 Deals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses & competitive threats

- 13.1.6 REVVITY

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product approvals

- 13.1.6.3.2 Other developments

- 13.1.7 BECTON, DICKINSON AND COMPANY (BD)

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Expansions

- 13.1.8 DIASORIN S.P.A.

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product launches and approvals

- 13.1.8.3.2 Deals

- 13.1.9 BIO-RAD LABORATORIES, INC.

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product launches

- 13.1.9.3.2 Deals

- 13.1.10 QUIDELORTHO CORPORATION

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product approvals

- 13.1.10.3.2 Deals

- 13.1.10.3.3 Expansions

- 13.1.11 BIOMERIEUX

- 13.1.11.1 Business overview

- 13.1.11.2 Products offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Product launches and approvals

- 13.1.11.3.2 Deals

- 13.1.12 QIAGEN

- 13.1.12.1 Business overview

- 13.1.12.2 Products offered

- 13.1.12.3 Recent developments

- 13.1.12.3.1 Deals

- 13.1.13 SYSMEX CORPORATION

- 13.1.13.1 Business overview

- 13.1.13.2 Products offered

- 13.1.13.3 Recent developments

- 13.1.13.3.1 Deals

- 13.1.13.3.2 Expansions

- 13.1.14 AGILENT TECHNOLOGIES, INC.

- 13.1.14.1 Business overview

- 13.1.14.2 Products offered

- 13.1.14.3 Recent developments

- 13.1.14.3.1 Product launches and approvals

- 13.1.14.3.2 Deals

- 13.1.14.3.3 Other developments

- 13.1.15 SHENZHEN MINDRAY BIO-MEDICAL ELECTRONICS CO., LTD.

- 13.1.15.1 Business overview

- 13.1.15.2 Products offered

- 13.1.1 ABBOTT

- 13.2 OTHER PLAYERS

- 13.2.1 MERCK KGAA

- 13.2.2 MERIDIAN BIOSCIENCE

- 13.2.3 BIO-TECHNE

- 13.2.4 CELLABS

- 13.2.5 ABNOVA CORPORATION

- 13.2.6 J. MITRA & CO. PVT. LTD.

- 13.2.7 TOSOH CORPORATION (TOSOH BIOSCIENCES)

- 13.2.8 CELL SCIENCES

- 13.2.9 ENZO BIOCHEM INC.

- 13.2.10 CREATIVE DIAGNOSTICS

- 13.2.11 BOSTER BIOLOGICAL TECHNOLOGY

- 13.2.12 ELABSCIENCE BIONOVATON INC.

- 13.2.13 WAK-CHEMIE MEDICAL GMBH

- 13.2.14 SERA CARE

- 13.2.15 EPITOPE DIAGNOSTICS, INC.

- 13.2.16 KAMIYA BIOMEDICAL COMPANY

- 13.2.17 GYROS PROTEIN TECHNOLOGIES AB

- 13.2.18 TRIVITRON HEALTHCARE

- 13.2.19 INBIOS INTERNATIONAL, INC.

- 13.2.20 MACCURA BIOTECHNOLOGY CO., LTD.

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS