|

시장보고서

상품코드

1811752

웨어러블 주사기 시장 : 제품별, 기술별, 용도별, 전달 방법별, 치료 용도별, 최종 사용자별 예측(-2030년)Wearable Injectors Market by Product, Technology, Usage, Delivery Method, Therapeutic Application, End User - Forecast to 2030 |

||||||

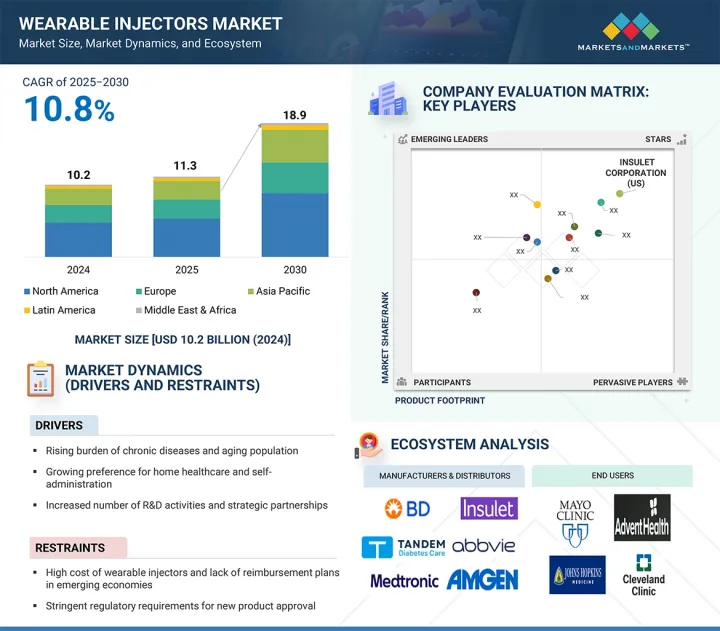

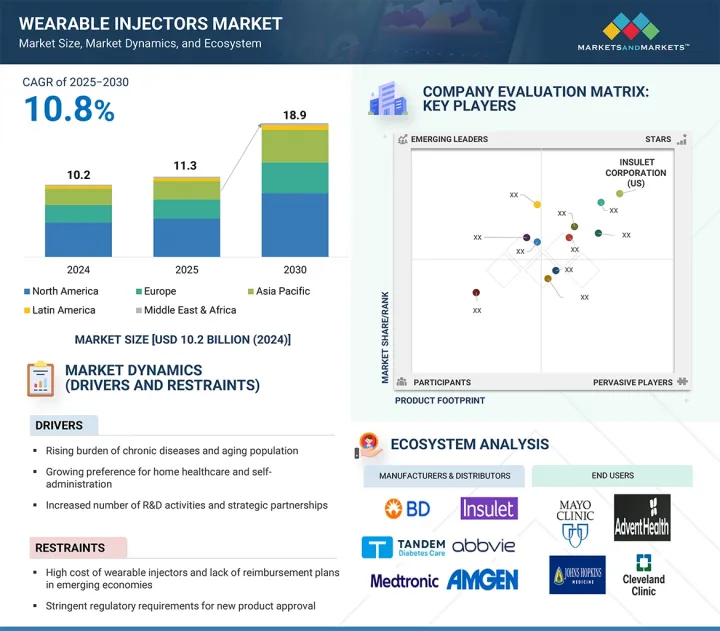

웨어러블 주사기 시장 규모는 예측 기간 동안 10.8%의 연평균 복합 성장률(CAGR)을 나타내고 2025년 113억 3,000만 달러에서 2030년에는 189억 1,000만 달러로 성장할 것으로 예상됩니다.

당뇨병, 암, 심혈관 장애와 같은 만성 질환의 유병률 증가는 약리 요법의 정확하고 통제된 지속적 배포(CD)에 대한 수요를 만들어 웨어러블 주사기 기술의 성장을 현저하게 촉진하고 있습니다. 게다가 디바이스 공학의 진보, 연구개발에 대한 지출 증가, 사물인터넷(IoT)과 원격 모니터링의 통합이 환자의 안전성을 높이고 약물 투여 효율을 향상시키고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(10억 달러) |

| 부문별 | 기술별, 용도별 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동, 아프리카, 남미 |

게다가, 기존의 입원 환경과는 대조적으로, 재택 건강 관리 솔루션으로의 전환은 이러한 고급 전달 시스템에 대한 수요를 더욱 창출하고 있습니다. 게다가, 웨어러블 주사기를 둘러싼 엄격한 규제 프레임워크는 보다 안전하고 신뢰할 수 있는 시스템의 개발을 촉진하고 시장 확대를 추진하고 있습니다.

기술별로 볼 때, 웨어러블 주사기 시장은 스프링 베이스, 모터 구동, 로터리 펌프, 확장 배터리 및 기타 기술로 구분됩니다. 스프링식 웨어러블 주사기는 단순한 설계, 비용 효율성, 신뢰성으로 인해 현재 시장에서 가장 큰 점유율을 차지하고 있습니다. 이 장치는 기계적 스프링 메커니즘을 사용하여 약물을 피하 투여하기 때문에 복잡한 모터나 배터리가 필요하지 않습니다. 제조가 쉽고 기계적 고장의 위험이 적기 때문에 제조업체와 환자 모두에게 선호되는 선택입니다. 또한, 스프링 주사기는 만성 질환의 관리, 특히 빈번한 투여 및 관리가 중요한 종양학 및 당뇨병학에서 널리 사용됩니다. 선진국 시장과 신흥국 시장 모두에서 이러한 주사기가 널리 채택되고 있기 때문에 2030년까지 그 우위가 유지될 것으로 예측됩니다.

웨어러블 주사기 시장은 용도별로 디스포저블형과 재이용형의 2가지로 분류됩니다. 일회용 웨어러블 주사기 부문은 예측 기간 동안 용도별 카테고리에서 우위를 차지할 것으로 예측됩니다. 이 장치는 단일 사용을 위해 설계되었으며 오염 위험을 줄이고 안전성을 높이고 환자 편의성을 향상시킬 수 있습니다. 특히 종양치료나 생물학적 제제의 투여 등 엄격한 무균성이 요구되는 장면에서 선호되고 있습니다. 게다가, 생물제제나 맞춤형 치료제 보급률이 진행되어, 자기 투여가 필요하게 되는 경우가 많기 때문에 사용하기 편리하고, 곧바로 사용할 수 있는 주사기 수요가 높아지고 있습니다. 유지 보수, 교정 및 세척이 필요 없기 때문에 일회용 주사기는 환자와 건강 관리 제공업체 모두에게 매력적이며 시장 리더로서의 입지를 확고하게 하고 있습니다.

북미는 웨어러블 주사기 시장에서 지배적이고 급성장하는 지역입니다. 이 성장의 주요 원인은 견고한 건강 관리 인프라, 높은 의료 비용, 고급 약물전달 기술의 조기 도입입니다. 미국과 캐나다는 당뇨병, 암, 자가면역 질환 등의 만성 질환을 앓고 있는 인구가 많아 정기적이고 정확한 약물 투여가 필요하기 때문에 시장을 선도하고 있습니다. 이 지역은 또한 주요 시장 진출기업의 강한 존재감과 생물 제제 및 맞춤형 의료에서의 끊임없는 기술 혁신의 혜택을 받고 있으며, 모두 웨어러블 주사기와 같은 고급 전달 솔루션이 필요합니다. 게다가 외래치료와 재택치료에 대한 동향 증가, 유리한 상환정책과 강력한 규제당국의 지원이 시장 성장을 더욱 가속화하고 있습니다. 웨어러블 주사기의 디지털 건강 기능과 연결성의 통합을 포함한 기술적 진보는 치료 어드레싱, 환자 모니터링 및 임상 결과를 개선합니다. 이러한 개발은 북미의 밸류 베이스 케어 중시의 자세에 맞추어 세계의 웨어러블 주사기 시장에서 이 지역의 리더십을 더욱 견고하게 하고 있습니다.

본 보고서에서는 세계의 웨어러블 주사기 시장에 대해 조사했으며, 제품별, 전달 방법별, 최종 사용자별, 기술별, 치료 용도별, 사용법별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 서론

- 시장 역학

- 업계 동향

- 기술 분석

- Porter's Five Forces 분석

- 파이프라인 분석

- 규제 상황

- 특허 분석

- 무역 분석

- 가격 분석

- 상환 분석

- 주요 컨퍼런스 및 행사(2025-2026년)

- 주요 이해관계자와 구매 기준

- 언멧 니즈/최종 사용자의 기대

- 웨어러블 주사기 시장에서의 AI의 영향

- 생태계 분석

- 밸류체인 분석

- 투자 및 자금조달 시나리오

- 미국 관세의 영향(2025년)

- 고객사업에 영향을 주는 동향/혼란

제6장 웨어러블 주사기 시장(제품별)

- 서론

- 착용형 웨어러블 주사기

- 비착용형 웨어러블 주사기

제7장 웨어러블 주사기 시장(전달 방법별)

- 서론

- 프로그램/지속적 주입

- 볼루스 전용

제8장 웨어러블 주사기 시장(최종 사용자별)

- 서론

- 웨어러블 주사기 제형 최종 사용자

- 웨어러블 주사기 장치 최종 사용자

제9장 웨어러블 주사기 시장(기술별)

- 서론

- 스프링 기반 기술

- 모터 구동 기술

- 로터리 펌프 기술

- 확장되는 배터리 기술

- 기타

제10장 웨어러블 주사기 시장(치료 용도별)

- 서론

- 자가면역 질환

- 당뇨병

- 종양학

- 심혈관 질환

- 감염성 질환

- 희귀 질환

- 기타

제11장 웨어러블 주사기 시장(사용법별)

- 서론

- 일회용

- 재사용형

제12장 웨어러블 주사기 시장(지역별)

- 서론

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 기타

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 중국

- 일본

- 인도

- 호주

- 태국

- 베트남

- 한국

- 인도네시아

- 기타

- 라틴아메리카

- 라틴아메리카의 거시경제 전망

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- 중동 및 아프리카의 거시경제 전망

- GCC 국가

- 기타

제13장 경쟁 구도

- 개요

- 주요 진입기업의 전략/강점

- 수익 분석(2020-2024년)

- 시장 점유율 분석

- 기업 평가 매트릭스 : 디바이스 주요 진출기업(2024년)

- 기업 평가 매트릭스 : 디바이스 스타트업/중소기업(2024년)

- 기업평가 매트릭스 : 제제 주요 진입기업(2024년)

- 브랜드/제품 비교

- 주요 기업의 연구 개발비

- 기업평가와 재무지표

- 경쟁 시나리오

제14장 기업 프로파일

- 웨어러블 주사기 디바이스 제조업체

- 주요 진출기업

- INSULET CORPORATION

- TANDEM DIABETES CARE, INC.

- MEDTRONIC

- BD

- WEST PHARMACEUTICAL SERVICES, INC.

- GERRESHEIMER AG

- STEVANATO

- LTS LOHMANN THERAPIE-SYSTEME AG

- SONCEBOZ

- NEMERA

- MANNKIND CORPORATION

- ENABLE INJECTIONS, INC.

- ELCAM MEDICAL

- 기타 기업

- DEBIOTECH SA

- MEDTRUM TECHNOLOGIES INC.

- CEQUR SIMPLICITY

- SUBCUJECT APS

- MICROMED CO., LTD

- 웨어러블 주사기 제제 제조업체

- AMGEN INC.

- ABBVIE INC.

- UNITED THERAPEUTICS CORPORATION

- APELLIS PHARMACEUTICALS, INC.

- SUPERNUS PHARMACEUTICALS

- COHERUS BIOSCIENCES, INC.

- SCPHARMACEUTICALS, INC.

제15장 부록

KTH 25.09.19The wearable injectors market is projected to grow from USD 11.33 billion in 2025 to USD 18.91 billion by 2030, at a CAGR of 10.8% during the forecast period. The rising prevalence of chronic diseases such as diabetes, cancer, and cardiovascular disorders has created a demand for the precise, controlled, and continuous delivery of pharmacological therapies, significantly driving the growth of wearable injector technologies. Moreover, advancements in device engineering, increased spending on research and development, and the integration of the Internet of Things (IoT) and remote monitoring are enhancing patient safety and improving the efficiency of drug administration.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | By Technology, Usage, |

| Regions covered | Europe, North America, Asia Pacific, Middle East & Africa, and South America |

Additionally, the shift towards home-based healthcare solutions, as opposed to traditional inpatient settings, is generating further demand for these advanced delivery systems. Furthermore, stringent regulatory frameworks surrounding wearable injectors are promoting the development of safer and more reliable systems, thereby reinforcing market expansion.

"The spring-based technology segment accounted for the largest share of the wearable injectors market, by technology, in 2024."

By technology, the wearable injectors market is segmented into spring-based, motor-driven, rotary pump, expanding battery, and other technologies. Spring-based wearable injectors currently hold the largest share of the market because of their simple design, cost-effectiveness, and reliability. These devices utilize a mechanical spring mechanism to deliver drugs subcutaneously, which eliminates the need for complex motors or batteries. Their ease of manufacturing and reduced risk of mechanical failure make them a preferred choice for both manufacturers and patients. Furthermore, spring-based injectors are widely used in the management of chronic diseases, particularly in oncology and diabetes, where frequent and controlled dosing is crucial. The widespread adoption of these injectors in both developed and developing markets is expected to sustain their dominance through 2030.

"The disposable wearable injectors segment is expected to dominate the market, by usage, during the forecast period."

The wearable injectors market is divided into two categories based on usage: disposable and reusable injectors. The disposable wearable injectors segment is expected to dominate the usage category during the forecast period. These devices are designed for single use, which helps reduce the risk of contamination, improve safety, and enhance patient convenience. They are especially favored in situations that require strict sterility, such as oncology treatments and the administration of biologic drugs. Additionally, the growing prevalence of biologics and personalized therapies, which often necessitate self-administration, has increased the demand for user-friendly, ready-to-use injectors. The absence of the need for maintenance, calibration, or cleaning further makes disposable injectors appealing to both patients and healthcare providers, solidifying their position as market leaders.

"The North American region is expected to capture the largest share during the forecast period."

North America continues to be the dominant and fastest-growing region in the wearable injectors market. This growth is primarily driven by a robust healthcare infrastructure, high healthcare expenditures, and the early adoption of advanced drug delivery technologies. The US and Canada lead the way, with a significant portion of the population suffering from chronic diseases such as diabetes, cancer, and autoimmune disorders-conditions that require regular and precise medication administration. The region also benefits from a strong presence of key market players and continuous innovation in biologics and personalized medicine, both of which demand sophisticated delivery solutions like wearable injectors. Additionally, the increasing trend toward outpatient care and home-based treatment, along with favorable reimbursement policies and strong regulatory support, further accelerates market growth. Technological advancements, including the integration of digital health features and connectivity in wearable injectors, are improving treatment adherence, patient monitoring, and clinical outcomes. These developments align well with North America's focus on value-based care, further solidifying the region's leadership in the global wearable injectors market.

Breakdown of supply-side primary interviews:

- By Company Type: Tier 1 (45%), Tier 2 (20%), and Tier 3 (35%)

- By Designation: C-level Executives (35%), Directors (25%), and Other Designations (40%)

- By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

- By Company Type: Hospitals (45%), Home Care Settings (30%), Ambulatory Surgery Centers/Specialty Infusion Centers (20%), and Other End Users (5%)

- By Designation: Healthcare Professionals (35%), Department Heads (27%), Procurement Heads (22%), and Other Designations (16%)

- By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Research Coverage

This report studies the wearable injectors market based on product, technology, usage, delivery method, therapeutic application, manufacturing type, end user, and region. It also studies factors affecting market growth (drivers, restraints, opportunities, and challenges). It analyzes the market's opportunities and challenges and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micromarkets with respect to their individual growth trends and forecasts the revenue of the market segments with respect to five main regions and respective countries.

Reasons to Buy the Report

The report can help established companies and new or smaller firms understand market trends, which will help them capture a larger market share. Firms that purchase the report can utilize one or more of the five strategies mentioned below.

This report provides insights into the following points:

- Analysis of key drivers (increased shift to home care settings, rising prevalence of chronic diseases, and rising aging population), restraints (high cost of wearable injectors), opportunities (high growth potential in emerging economies), and challenges (lack of training and education for using wearable injectors) influencing the growth of the wearable injectors market.

- Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and product launches in the wearable injectors market.

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of wearable injectors across regions.

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the wearable injectors market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the wearable injectors market.The wearable injectors market is projected to grow from USD 11.33 billion in 2025 to USD 18.91 billion by 2030, at a CAGR of 10.8% during the forecast period. The rising prevalence of chronic diseases such as diabetes, cancer, and cardiovascular disorders has created a demand for the precise, controlled, and continuous delivery of pharmacological therapies, significantly driving the growth of wearable injector technologies. Moreover, advancements in device engineering, increased spending on research and development, and the integration of the Internet of Things (IoT) and remote monitoring are enhancing patient safety and improving the efficiency of drug administration. Additionally, the shift towards home-based healthcare solutions, as opposed to traditional inpatient settings, is generating further demand for these advanced delivery systems. Furthermore, stringent regulatory frameworks surrounding wearable injectors are promoting the development of safer and more reliable systems, thereby reinforcing market expansion.

"The spring-based technology segment accounted for the largest share of the wearable injectors market, by technology, in 2024."

By technology, the wearable injectors market is segmented into spring-based, motor-driven, rotary pump, expanding battery, and other technologies. Spring-based wearable injectors currently hold the largest share of the market because of their simple design, cost-effectiveness, and reliability. These devices utilize a mechanical spring mechanism to deliver drugs subcutaneously, which eliminates the need for complex motors or batteries. Their ease of manufacturing and reduced risk of mechanical failure make them a preferred choice for both manufacturers and patients. Furthermore, spring-based injectors are widely used in the management of chronic diseases, particularly in oncology and diabetes, where frequent and controlled dosing is crucial. The widespread adoption of these injectors in both developed and developing markets is expected to sustain their dominance through 2030.

"The disposable wearable injectors segment is expected to dominate the market, by usage, during the forecast period."

The wearable injectors market is divided into two categories based on usage: disposable and reusable injectors. The disposable wearable injectors segment is expected to dominate the usage category during the forecast period. These devices are designed for single use, which helps reduce the risk of contamination, improve safety, and enhance patient convenience. They are especially favored in situations that require strict sterility, such as oncology treatments and the administration of biologic drugs. Additionally, the growing prevalence of biologics and personalized therapies, which often necessitate self-administration, has increased the demand for user-friendly, ready-to-use injectors. The absence of the need for maintenance, calibration, or cleaning further makes disposable injectors appealing to both patients and healthcare providers, solidifying their position as market leaders.

"The North American region is expected to capture the largest share during the forecast period."

North America continues to be the dominant and fastest-growing region in the wearable injectors market. This growth is primarily driven by a robust healthcare infrastructure, high healthcare expenditures, and the early adoption of advanced drug delivery technologies. The US and Canada lead the way, with a significant portion of the population suffering from chronic diseases such as diabetes, cancer, and autoimmune disorders-conditions that require regular and precise medication administration. The region also benefits from a strong presence of key market players and continuous innovation in biologics and personalized medicine, both of which demand sophisticated delivery solutions like wearable injectors. Additionally, the increasing trend toward outpatient care and home-based treatment, along with favorable reimbursement policies and strong regulatory support, further accelerates market growth. Technological advancements, including the integration of digital health features and connectivity in wearable injectors, are improving treatment adherence, patient monitoring, and clinical outcomes. These developments align well with North America's focus on value-based care, further solidifying the region's leadership in the global wearable injectors market.

Breakdown of supply-side primary interviews:

- By Company Type: Tier 1 (45%), Tier 2 (20%), and Tier 3 (35%)

- By Designation: C-level Executives (35%), Directors (25%), and Other Designations (40%)

- By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

- By Company Type: Hospitals (45%), Home Care Settings (30%), Ambulatory Surgery Centers/Specialty Infusion Centers (20%), and Other End Users (5%)

- By Designation: Healthcare Professionals (35%), Department Heads (27%), Procurement Heads (22%), and Other Designations (16%)

- By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Research Coverage

This report studies the wearable injectors market based on product, technology, usage, delivery method, therapeutic application, manufacturing type, end user, and region. It also studies factors affecting market growth (drivers, restraints, opportunities, and challenges). It analyzes the market's opportunities and challenges and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micromarkets with respect to their individual growth trends and forecasts the revenue of the market segments with respect to five main regions and respective countries.

Reasons to Buy the Report

The report can help established companies and new or smaller firms understand market trends, which will help them capture a larger market share. Firms that purchase the report can utilize one or more of the five strategies mentioned below.

This report provides insights into the following points:

- Analysis of key drivers (increased shift to home care settings, rising prevalence of chronic diseases, and rising aging population), restraints (high cost of wearable injectors), opportunities (high growth potential in emerging economies), and challenges (lack of training and education for using wearable injectors) influencing the growth of the wearable injectors market.

- Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and product launches in the wearable injectors market.

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of wearable injectors across regions.

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the wearable injectors market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the wearable injectors market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 YEARS CONSIDERED

- 1.4 INCLUSIONS AND EXCLUSIONS

- 1.4.1 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 LIMITATIONS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary sources

- 2.1.2.2 Key data from primary sources

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of primary interviews

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 APPROACH 1: SUPPLY-SIDE ANALYSIS (REVENUE SHARE ANALYSIS)

- 2.2.2 APPROACH 2: COMPANY PRESENTATIONS AND PRIMARY INTERVIEWS

- 2.2.3 APPROACH 3: BOTTOM-UP APPROACH

- 2.2.4 APPROACH 4: TOP-DOWN APPROACH

- 2.2.5 APPROACH 5: DEMAND-SIDE APPROACH

- 2.2.6 APPROACH 6: VOLUME DATA ANALYSIS

- 2.2.7 APPROACH 7: ADJACENT MARKET APPROACH

- 2.2.7.1 Injectable drug delivery market

- 2.2.7.2 Pharmaceutical drug delivery market

- 2.3 DATA TRIANGULATION

- 2.4 MARKET SHARE ESTIMATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.5.1 GROWTH RATE ASSUMPTIONS

- 2.6 RISK ASSESSMENT

- 2.7 RESEARCH LIMITATIONS

- 2.7.1 METHODOLOGY-RELATED LIMITATIONS

- 2.7.2 SCOPE-RELATED LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES IN WEARABLE INJECTORS MARKET

- 4.2 ASIA PACIFIC: WEARABLE INJECTORS MARKET, BY APPLICATION AND COUNTRY

- 4.3 WEARABLE INJECTORS MARKET: REGIONAL MIX

- 4.4 WEARABLE INJECTORS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.5 WEARABLE INJECTORS MARKET: DEVELOPED VS. DEVELOPING MARKETS

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising burden of chronic diseases and aging population

- 5.2.1.2 Growing preference for home healthcare and self-administration

- 5.2.1.3 Increased number of R&D activities and strategic partnerships

- 5.2.1.4 Use of artificial intelligence in diabetes management devices

- 5.2.2 RESTRAINTS

- 5.2.2.1 High cost of wearable injectors and lack of reimbursement plans in emerging economies

- 5.2.2.2 Stringent regulatory requirements for new product approval

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Significant growth potential in emerging economies

- 5.2.3.2 Integration with digital health & remote monitoring

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of training and education for using wearable injectors

- 5.2.1 DRIVERS

- 5.3 INDUSTRY TRENDS

- 5.3.1 INTEGRATION OF SMART CONNECTIVITY & DIGITAL HEALTH FEATURES

- 5.3.2 LARGE-VOLUME ON-BODY BIOLOGICS INJECTORS

- 5.4 TECHNOLOGY ANALYSIS

- 5.4.1 KEY TECHNOLOGIES

- 5.4.1.1 Micro-MEMS and Bio-MEMS in wearable injectors

- 5.4.1.2 Electromechanical drive systems (motorized pumps)

- 5.4.1.3 Sensor-integrated closed-loop wearable injector

- 5.4.2 COMPLEMENTARY TECHNOLOGIES

- 5.4.2.1 Smartphone and app interfaces

- 5.4.2.2 IoT and smart analytics in wearable injectors

- 5.4.3 ADJACENT TECHNOLOGIES

- 5.4.3.1 Electrochemical aptamer biosensors

- 5.4.3.2 Telemedicine platforms

- 5.4.1 KEY TECHNOLOGIES

- 5.5 PORTER'S FIVE FORCES ANALYSIS

- 5.5.1 THREAT OF NEW ENTRANTS

- 5.5.2 THREAT OF SUBSTITUTES

- 5.5.3 BARGAINING POWER OF SUPPLIERS

- 5.5.4 BARGAINING POWER OF BUYERS

- 5.5.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.6 PIPELINE ANALYSIS

- 5.7 REGULATORY LANDSCAPE

- 5.7.1 REGULATORY ANALYSIS

- 5.7.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.8 PATENT ANALYSIS

- 5.8.1 PATENT PUBLICATION TRENDS FOR WEARABLE INJECTORS

- 5.8.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 5.9 TRADE ANALYSIS

- 5.9.1 TRADE DATA FOR HS CODE 901890

- 5.9.1.1 Import data for HS Code 901890

- 5.9.1.2 Export data for HS Code 901890

- 5.9.1 TRADE DATA FOR HS CODE 901890

- 5.10 PRICING ANALYSIS

- 5.10.1 AVERAGE SELLING PRICE, BY KEY PLAYER

- 5.10.1.1 Average selling price trend among key players

- 5.10.2 AVERAGE SELLING PRICE, BY REGION

- 5.10.2.1 Average selling price trend of on-body wearable injector, by region

- 5.10.2.2 Average selling price trend of off-body wearable injector, by region

- 5.10.1 AVERAGE SELLING PRICE, BY KEY PLAYER

- 5.11 REIMBURSEMENT ANALYSIS

- 5.12 KEY CONFERENCES & EVENTS, 2025-2026

- 5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS (DEVICES)

- 5.13.2 KEY STAKEHOLDERS IN BUYING PROCESS (FORMULATIONS)

- 5.13.3 BUYING CRITERIA

- 5.14 UNMET NEEDS/END-USER EXPECTATIONS

- 5.15 IMPACT OF AI ON WEARABLE INJECTORS MARKET

- 5.15.1 INTRODUCTION

- 5.15.2 MARKET POTENTIAL IN WEARABLE INJECTORS ECOSYSTEM

- 5.15.3 AI USE CASES

- 5.15.4 KEY COMPANIES IMPLEMENTING AI IN WEARABLE INJECTORS

- 5.15.5 FUTURE OF GEN AI IN WEARABLE INJECTORS ECOSYSTEM

- 5.16 ECOSYSTEM ANALYSIS

- 5.16.1 WEARABLE INJECTOR PROVIDERS

- 5.16.2 END USERS

- 5.16.3 REGULATORY BODIES

- 5.17 VALUE CHAIN ANALYSIS

- 5.18 INVESTMENT AND FUNDING SCENARIO

- 5.19 IMPACT OF 2025 US TARIFF

- 5.19.1 INTRODUCTION

- 5.19.2 KEY TARIFF RATES

- 5.19.3 PRICE IMPACT ANALYSIS

- 5.19.4 IMPACT ON COUNTRY/REGION

- 5.19.5 IMPACT ON END-USE INDUSTRIES

- 5.20 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6 WEARABLE INJECTORS MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- 6.2 ON-BODY WEARABLE INJECTORS

- 6.2.1 LARGE-VOLUME SUBCUTANEOUS DELIVERY AND HOME-BASED CARE TO DRIVE MARKET

- 6.3 OFF-BODY WEARABLE INJECTORS

- 6.3.1 TECHNOLOGICAL VERSATILITY AND PERSONALIZED DRUG DELIVERY TO DRIVE MARKET

7 WEARABLE INJECTORS MARKET, BY DELIVERY METHOD

- 7.1 INTRODUCTION

- 7.2 PROGRAMMED/CONTINUOUS INFUSION

- 7.2.1 NEED FOR PRECISE, CONTROLLED DRUG DELIVERY OVER EXTENDED DURATIONS TO DRIVE SEGMENT

- 7.3 BOLUS-ONLY

- 7.3.1 GROWING DEMAND FOR SELF-ADMINISTERED, SINGLE-DOSE BIOLOGICS TO DRIVE SEGMENT GROWTH

8 WEARABLE INJECTORS MARKET, BY END USER

- 8.1 INTRODUCTION

- 8.2 WEARABLE INJECTOR FORMULATION END USERS

- 8.2.1 HOME CARE SETTINGS

- 8.2.1.1 RISING PREFERENCE FOR SELF-ADMINISTRATION OF MEDICINE TO DRIVE MARKET

- 8.2.2 HOSPITALS & CLINICS

- 8.2.2.1 Increased hospital demand for controlled drug delivery boosting market uptake

- 8.2.3 SPECIALTY INFUSION CENTERS/AMBULATORY SURGERY CENTERS

- 8.2.3.1 Cost-efficiency to drive demand for wearable injectors in specialty centers

- 8.2.4 OTHER FORMULATION END USERS

- 8.2.1 HOME CARE SETTINGS

- 8.3 WEARABLE INJECTOR DEVICE END USERS

- 8.3.1 PHARMACEUTICAL COMPANIES

- 8.3.1.1 Need for efficient subcutaneous delivery of large-volume biologics to drive market

- 8.3.2 BIOTECHNOLOGY COMPANIES

- 8.3.2.1 Improved patient experience, dose accuracy, and at-home administration of complex biologics to drive market

- 8.3.3 CONTRACT DEVELOPMENT & MANUFACTURING ORGANIZATIONS

- 8.3.3.1 Innovation through cost-effective and scalable manufacturing solutions to drive market

- 8.3.1 PHARMACEUTICAL COMPANIES

9 WEARABLE INJECTORS MARKET, BY TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 SPRING-BASED TECHNOLOGY

- 9.2.1 COST-EFFECTIVE ENGINEERING AND MECHANICAL SIMPLICITY TO DRIVE MARKET

- 9.3 MOTOR-DRIVEN TECHNOLOGY

- 9.3.1 PRECISION DOSING AND PROGRAMMABILITY ACCELERATING ADOPTION OF MOTOR-BASED WEARABLE INJECTORS

- 9.4 ROTARY PUMP TECHNOLOGY

- 9.4.1 HIGHER PRECISION AND BETTER CONTROL OVER VISCOUS MEDICINES TO SUPPORT MARKET GROWTH

- 9.5 EXPANDING BATTERY TECHNOLOGY

- 9.5.1 SHIFT TOWARD HIGH-VOLUME DELIVERY OF VISCOUS DRUGS TO BOOST DEMAND

- 9.6 OTHER TECHNOLOGIES

10 WEARABLE INJECTORS MARKET, BY THERAPEUTIC APPLICATION

- 10.1 INTRODUCTION

- 10.2 AUTOIMMUNE DISEASES

- 10.2.1 GROWING PREFERENCE FOR SELF-ADMINISTRATION IN CHRONIC AUTOIMMUNE DISORDERS TO FUEL DEMAND

- 10.3 DIABETES

- 10.3.1 HIGH DISEASE BURDEN AND DAILY INJECTION DEMAND FUEL MARKET DOMINANCE

- 10.4 ONCOLOGY

- 10.4.1 INCREASING NUMBER OF CANCER CASES, SHIFT TOWARD SUBCUTANEOUS CANCER THERAPIES, AND NEED TO REDUCE HOSPITAL BURDEN TO BOOST MARKET

- 10.5 CARDIOVASCULAR DISEASES

- 10.5.1 RISING NEED FOR CONTINUOUS DRUG DELIVERY IN PULMONARY AND CARDIORENAL CONDITIONS TO DRIVE DEMAND

- 10.6 INFECTIOUS DISEASES

- 10.6.1 NEED FOR RAPID AND SELF-ADMINISTERED TREATMENT TO DRIVE ADOPTION

- 10.7 RARE/ORPHAN DISEASES

- 10.7.1 HIGH-COST BIOLOGICS AND PERSONALIZED TREATMENT NEEDS TO DRIVE DEMAND

- 10.8 OTHER THERAPEUTIC APPLICATIONS

11 WEARABLE INJECTORS MARKET, BY USAGE

- 11.1 INTRODUCTION

- 11.2 DISPOSABLE

- 11.2.1 RISING PREFERENCE FOR SIMPLICITY, STERILITY, AND SINGLE-USE SAFETY TO DRIVE DISPOSABLE WEARABLE INJECTORS MARKET

- 11.3 REUSABLE

- 11.3.1 ENABLING LONG-TERM COST EFFICIENCY AND SUSTAINABLE DRUG DELIVERY MODELS TO DRIVE DEMAND

12 WEARABLE INJECTORS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 12.2.2 US

- 12.2.2.1 Growing home healthcare market to drive demand

- 12.2.3 CANADA

- 12.2.3.1 Rising biologic usage and decentralized care pathways to boost demand

- 12.3 EUROPE

- 12.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 12.3.2 GERMANY

- 12.3.2.1 Domestic medtech innovation and government initiatives to fuel growth

- 12.3.3 UK

- 12.3.3.1 NHS digital strategy and homecare shift to accelerate wearable injector adoption

- 12.3.4 FRANCE

- 12.3.4.1 Well-established healthcare system to support market growth

- 12.3.5 ITALY

- 12.3.5.1 Growing demand for cost-effective home care to drive market

- 12.3.6 SPAIN

- 12.3.6.1 Rising prevalence of cancer to drive demand

- 12.3.7 NETHERLANDS

- 12.3.7.1 Strong healthcare infrastructure and aging population to drive market growth

- 12.3.8 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 12.4.2 CHINA

- 12.4.2.1 Growing investments in healthcare infrastructure to drive market

- 12.4.3 JAPAN

- 12.4.3.1 Large geriatric population to drive demand

- 12.4.4 INDIA

- 12.4.4.1 Increasing demand for advanced medical treatment to boost market

- 12.4.5 AUSTRALIA

- 12.4.5.1 Rising prevalence of chronic diseases to fuel market

- 12.4.6 THAILAND

- 12.4.6.1 Expansion of universal healthcare to drive growth of wearable injectors market

- 12.4.7 VIETNAM

- 12.4.7.1 Rapidly aging population to drive demand

- 12.4.8 SOUTH KOREA

- 12.4.8.1 Rise of geriatric population to drive growth

- 12.4.9 INDONESIA

- 12.4.9.1 Growing emphasis on home-based care and universal coverage to drive adoption of wearable injectors

- 12.4.10 REST OF ASIA PACIFIC

- 12.5 LATIN AMERICA

- 12.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 12.5.2 BRAZIL

- 12.5.2.1 Increasing number of chronic conditions to drive market

- 12.5.3 MEXICO

- 12.5.3.1 Government initiatives to boost wearable injectors market

- 12.5.4 REST OF LATIN AMERICA

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 12.6.2 GCC COUNTRIES

- 12.6.2.1 Kingdom of Saudi Arabia (KSA)

- 12.6.2.1.1 Smart healthcare infrastructure and chronic disease burden to propel market expansion

- 12.6.2.2 United Arab Emirates (UAE)

- 12.6.2.2.1 Government support and digital health initiatives to fuel UAE's wearable injectors market

- 12.6.2.3 Rest of GCC Countries

- 12.6.2.1 Kingdom of Saudi Arabia (KSA)

- 12.6.3 REST OF MIDDLE EAST & AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 13.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN WEARABLE INJECTORS MARKET

- 13.3 REVENUE ANALYSIS, 2020-2024

- 13.3.1 WEARABLE INJECTOR DEVICE MANUFACTURERS

- 13.3.2 WEARABLE INJECTOR FORMULATION MANUFACTURERS

- 13.4 MARKET SHARE ANALYSIS

- 13.4.1 WEARABLE INJECTOR DEVICE MANUFACTURERS

- 13.4.2 GLOBAL MARKET SHARE ANALYSIS OF WEARABLE DEVICE MANUFACTURERS, 2024

- 13.4.3 US MARKET SHARE ANALYSIS OF WEARABLE DEVICE MANUFACTURERS, 2024

- 13.4.4 WEARABLE INJECTOR FORMULATION MANUFACTURERS

- 13.4.5 GLOBAL MARKET SHARE ANALYSIS OF WEARABLE FORMULATION MANUFACTURERS, 2024

- 13.4.6 US MARKET SHARE ANALYSIS OF WEARABLE FORMULATION MANUFACTURERS, 2024

- 13.5 COMPANY EVALUATION MATRIX: DEVICE KEY PLAYERS, 2024

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPANY FOOTPRINT: DEVICE KEY PLAYERS, 2024

- 13.5.5.1 Company footprint

- 13.5.5.2 Region footprint

- 13.5.5.3 Product type footprint

- 13.5.5.4 Usage footprint

- 13.5.5.5 Delivery method footprint

- 13.5.5.6 Technology type footprint

- 13.6 COMPANY EVALUATION MATRIX: DEVICE STARTUPS/SMES, 2024

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 DYNAMIC COMPANIES

- 13.6.3 STARTING BLOCKS

- 13.6.4 RESPONSIVE COMPANIES

- 13.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.6.5.1 Detailed list of key device startups/SME players

- 13.6.5.2 Competitive benchmarking of key SMEs/startups

- 13.7 COMPANY EVALUATION MATRIX: FORMULATION KEY PLAYERS, 2024

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: FORMULATION KEY PLAYERS, 2024

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Product type footprint

- 13.7.5.4 Delivery method footprint

- 13.7.5.5 Therapeutic application footprint

- 13.7.5.6 Technology type footprint

- 13.8 BRAND/PRODUCT COMPARISON

- 13.9 R&D EXPENDITURE OF KEY PLAYERS

- 13.10 COMPANY VALUATION AND FINANCIAL METRICS

- 13.10.1 COMPANY VALUATION

- 13.10.2 FINANCIAL METRICS

- 13.11 COMPETITIVE SCENARIO

- 13.11.1 PRODUCT LAUNCHES & APPROVALS

- 13.11.2 DEALS

- 13.11.3 EXPANSIONS

- 13.11.4 OTHER DEVELOPMENTS

14 COMPANY PROFILES

- 14.1 WEARABLE INJECTORS DEVICE MANUFACTURERS

- 14.2 KEY PLAYERS

- 14.2.1 INSULET CORPORATION

- 14.2.1.1 Business overview

- 14.2.1.2 Products/Solutions/Services offered

- 14.2.1.3 Recent developments

- 14.2.1.3.1 Product launches, upgrades, and approvals

- 14.2.1.3.2 Deals

- 14.2.1.3.3 Expansions

- 14.2.1.4 MnM view

- 14.2.1.4.1 Key strengths

- 14.2.1.4.2 Strategic choices

- 14.2.1.4.3 Weaknesses & competitive threats

- 14.2.2 TANDEM DIABETES CARE, INC.

- 14.2.2.1 Business overview

- 14.2.2.2 Products/Solutions/Services offered

- 14.2.2.3 Recent developments

- 14.2.2.3.1 Product launches, upgrades, and approvals

- 14.2.2.3.2 Deals

- 14.2.2.4 MnM view

- 14.2.2.4.1 Key strengths

- 14.2.2.4.2 Strategic choices

- 14.2.2.4.3 Weaknesses & competitive threats

- 14.2.3 MEDTRONIC

- 14.2.3.1 Business overview

- 14.2.3.2 Products/Solutions/Services offered

- 14.2.3.3 Recent developments

- 14.2.3.3.1 Product launches, upgrades, and approvals

- 14.2.3.3.2 Deals

- 14.2.3.4 MnM view

- 14.2.3.4.1 Key strengths

- 14.2.3.4.2 Strategic choices

- 14.2.3.4.3 Weaknesses & competitive threats

- 14.2.4 BD

- 14.2.4.1 Business overview

- 14.2.4.2 Products/Solutions/Services offered

- 14.2.4.3 Recent developments

- 14.2.4.3.1 Deals

- 14.2.4.3.2 Expansions

- 14.2.4.3.3 Other developments

- 14.2.4.4 MnM view

- 14.2.4.4.1 Key strengths

- 14.2.4.4.2 Strategic choices

- 14.2.4.4.3 Weaknesses & competitive threats

- 14.2.5 WEST PHARMACEUTICAL SERVICES, INC.

- 14.2.5.1 Business overview

- 14.2.5.2 Products/Solutions/Services offered

- 14.2.5.3 Recent developments

- 14.2.5.3.1 Expansions

- 14.2.5.4 MnM view

- 14.2.5.4.1 Key strengths

- 14.2.5.4.2 Strategic choices

- 14.2.5.4.3 Weaknesses & competitive threats

- 14.2.6 GERRESHEIMER AG

- 14.2.6.1 Business overview

- 14.2.6.2 Products/Solutions/Services offered

- 14.2.6.3 Recent developments

- 14.2.6.3.1 Expansions

- 14.2.7 STEVANATO

- 14.2.7.1 Business overview

- 14.2.7.2 Products/Solutions/Services offered

- 14.2.7.3 Recent developments

- 14.2.7.3.1 Product launches, upgrades, and approvals

- 14.2.7.3.2 Deals

- 14.2.8 LTS LOHMANN THERAPIE-SYSTEME AG

- 14.2.8.1 Business overview

- 14.2.8.2 Products/Solutions/Services offered

- 14.2.8.3 Recent developments

- 14.2.8.3.1 Product launches, upgrades, and approvals

- 14.2.8.3.2 Deals

- 14.2.8.3.3 Expansions

- 14.2.9 SONCEBOZ

- 14.2.9.1 Business overview

- 14.2.9.2 Products/Solutions/Services offered

- 14.2.10 NEMERA

- 14.2.10.1 Business overview

- 14.2.10.2 Products/Solutions/Services offered

- 14.2.10.3 Recent developments

- 14.2.10.3.1 Deals

- 14.2.10.3.2 Expansions

- 14.2.11 MANNKIND CORPORATION

- 14.2.11.1 Business overview

- 14.2.11.2 Products/Solutions/Services offered

- 14.2.11.3 Recent developments

- 14.2.11.3.1 Deals

- 14.2.12 ENABLE INJECTIONS, INC.

- 14.2.12.1 Business overview

- 14.2.12.2 Products/Solutions/Services offered

- 14.2.12.3 Recent developments

- 14.2.12.3.1 Product launches, upgrades, and approvals

- 14.2.12.3.2 Deals

- 14.2.12.3.3 Expansions

- 14.2.12.3.4 Other developments

- 14.2.13 ELCAM MEDICAL

- 14.2.13.1 Business overview

- 14.2.13.2 Products/Solutions/Services offered

- 14.2.13.3 Recent developments

- 14.2.13.3.1 Expansions

- 14.2.1 INSULET CORPORATION

- 14.3 OTHER PLAYERS

- 14.3.1 DEBIOTECH SA

- 14.3.2 MEDTRUM TECHNOLOGIES INC.

- 14.3.3 CEQUR SIMPLICITY

- 14.3.4 SUBCUJECT APS

- 14.3.5 MICROMED CO., LTD

- 14.4 WEARABLE INJECTORS WITH FORMULATION MANUFACTURERS

- 14.4.1 AMGEN INC.

- 14.4.1.1 Business overview

- 14.4.1.2 Products/Solutions/Services offered

- 14.4.1.3 Recent developments

- 14.4.1.3.1 Deals

- 14.4.1.3.2 Expansions

- 14.4.2 ABBVIE INC.

- 14.4.2.1 Business overview

- 14.4.2.2 Products/Solutions/Services offered

- 14.4.2.3 Recent developments

- 14.4.2.3.1 Product launches, upgrades, and approvals

- 14.4.2.3.2 Expansions

- 14.4.3 UNITED THERAPEUTICS CORPORATION

- 14.4.3.1 Business overview

- 14.4.3.2 Products/Solutions/Services offered

- 14.4.3.3 Recent developments

- 14.4.3.3.1 Expansions

- 14.4.4 APELLIS PHARMACEUTICALS, INC.

- 14.4.4.1 Business overview

- 14.4.4.2 Products/Solutions/Services offered

- 14.4.4.3 Recent developments

- 14.4.4.3.1 Product launches, upgrades, and approvals

- 14.4.5 SUPERNUS PHARMACEUTICALS

- 14.4.5.1 Business overview

- 14.4.5.2 Products/Solutions/Services offered

- 14.4.5.3 Recent developments

- 14.4.5.3.1 Product launches, upgrades, and approvals

- 14.4.6 COHERUS BIOSCIENCES, INC.

- 14.4.6.1 Business overview

- 14.4.6.2 Products/Solutions/Services offered

- 14.4.6.3 Recent developments

- 14.4.6.3.1 Product launches, upgrades, and approvals

- 14.4.6.3.2 Other developments

- 14.4.7 SCPHARMACEUTICALS, INC.

- 14.4.7.1 Business overview

- 14.4.7.2 Products/Solutions/Services offered

- 14.4.7.3 Recent developments

- 14.4.7.3.1 Product launches, upgrades and approvals

- 14.4.1 AMGEN INC.

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS