|

시장보고서

상품코드

1823729

그린 데이터센터 시장 예측(-2030년) : 컴포넌트별, 데이터센터 규모와 용량별, 데이터센터 유형별, 기업용 데이터센터별, 지역별Green Data Center Market by Infrastructure, Software - Global Forecast to 2030 |

||||||

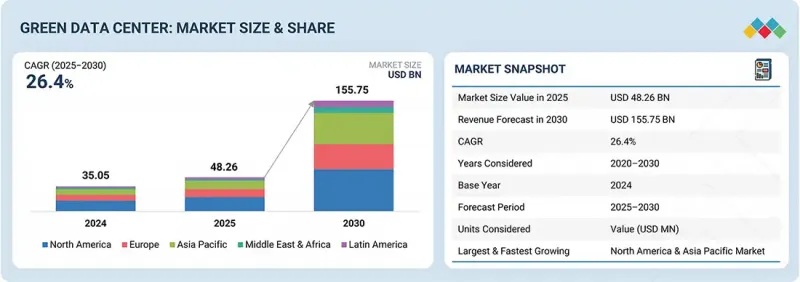

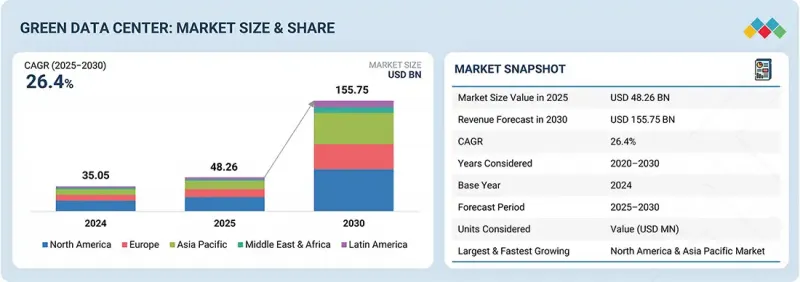

세계의 그린 데이터센터 시장 규모는 급속히 확대하고 있으며, 2025년 약 482억 6,000만 달러에서 2030년에는 1,557억 5,000만 달러로 확대할 것으로 예측되며, CAGR은 26.4%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2020-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 100만 달러 |

| 부문 | 컴포넌트별, 데이터센터 규모와 용량별, 데이터센터 유형별, 기업용 데이터센터별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

이 시장을 주도하는 것은 고밀도 워크로드를 지원하기 위한 에너지 효율적인 인프라에 대한 수요 증가입니다. 또한 기업은 AI, 클라우드 컴퓨팅, 데이터 분석과 같은 리소스 집약적인 용도에 전력을 공급하기 위해 재생에너지원의 채택을 확대하고, 운영 효율성을 최적화하고 기업의 넷제로 목표를 달성하기 위해 첨단 냉각 솔루션과 지능형 에너지 관리 시스템을 요구하고 있습니다. 에너지 관리 시스템을 요구하고 있습니다.

또한 증가하는 디지털 워크로드에 대응하기 위해 신뢰할 수 있는 저탄소 전력과 확장 가능한 모듈형 설계가 필수적이며, 자동 모니터링 및 탄소 보고 기능을 통해 강화되는 세계 규제를 준수할 수 있도록 지원합니다. 한편, 시장에는 재생에너지와의 통합 및 첨단 냉각기술 도입에 따른 막대한 선행투자, 기존 시설 개보수에 따른 운영의 복잡성 등의 억제요인이 있으며, 예산 중심 기업이나 레거시 중심의 기업에서는 도입이 늦어질 수 있습니다.

클라우드 및 하이퍼스케일 데이터센터는 그린 데이터센터 시장의 최전선에 있으며, 대규모 클라우드 플랫폼, AI 워크로드, 세계 용도를 지원하기 위해 재생에너지, 첨단 냉각 기술, 에너지 효율적인 인프라의 채택을 추진하고 있습니다. 추진하고 있습니다. 이 시설들은 환경에 미치는 영향을 최소화하면서 고성능 컴퓨팅을 대규모로 제공할 수 있도록 설계되었으며, 지속가능성을 운영 전략의 핵심 요소로 삼고 있습니다. 전략적 파트너십은 이러한 변화를 가속화하고 신흥 벤더와 솔루션 프로바이더가 혁신적이고 에너지 효율적인 솔루션에 기여할 수 있는 기회를 창출하는 데 중요한 역할을 하고 있습니다. 2024년 11월, 슈나이더 일렉트릭과 버티브는 구글, 마이크로소프트 등 주요 하이테크 기업과 함께 유럽에서 디젤 백업 발전기를 더 깨끗한 대체품으로 대체하기 위한 정보 제공 요청을 시작하며, 이산화탄소 배출량 감소와 저탄소 운전 도입에 대한 업계의 노력을 보여주었습니다. 저탄소 운전 도입에 대한 업계의 의지를 보여주었습니다.

마찬가지로 2023년 화웨이는 Qinghai Yungu 빅데이터 산업개발과 협력하여 칭하이성 하이난현에 100% 청정에너지 데이터센터를 개발하여 신뢰성, 유연성, 높은 에너지 효율을 실현하는 모듈식 설계의 가능성을 밝혔습니다. 이러한 협력 관계는 통합적이고 확장 가능하며 지속가능한 인프라가 환경에 미치는 영향을 최소화하면서 성능 요구 사항을 충족시킬 수 있는 방법을 보여줍니다. 신생 벤더와 솔루션 프로바이더는 이러한 노력에 참여함으로써 혁신적인 기술을 제공하고, 시장에서의 입지를 강화하며, 클라우드 및 하이퍼스케일 데이터센터의 친환경적 전환에 크게 기여할 수 있습니다.

데이터센터 인프라 관리(DCIM)는 지속가능성을 극대화하고 에너지 소비를 줄이기 위해 IT 및 시설 리소스를 종합적으로 모니터링, 제어 및 최적화할 수 있도록 지원하는 그린 데이터센터에서 가장 중요한 소프트웨어 부문으로, 예측 기간 중 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 기간 중 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. DCIM은 지속적인 전력 및 환경 모니터링을 제공하여 시설 전체의 전력 사용량, 전압, 온도, 온도, 습도, 기류 등의 지표를 추적함으로써 운영자는 핫스팟을 식별하고 이상을 감지하여 에너지 낭비를 방지하는 동시에 안정적인 운영을 보장할 수 있습니다. 이 소프트웨어의 에너지 최적화 툴은 소비 패턴을 분석하여 냉각, 조명, IT 워크로드 조정을 제안하거나 자동화하여 성능 저하 없이 이산화탄소 배출량을 줄입니다. DCIM의 용량 계획은 전력, 냉각 및 공간 요구 사항을 정확하게 예측하여 효율적인 리소스 할당을 보장하고 과도한 프로비저닝을 최소화할 수 있도록 합니다.

자산 수명주기관리는 IT 및 인프라 구성 요소의 조달부터 폐기까지 추적하여 최적의 활용, 중복성 감소, 지속가능한 조달 관행을 지원합니다. 경고 및 인시던트 관리 기능은 잠재적 장애, 임계값 위반 또는 비효율성에 대한 실시간 알림을 제공하여 다운타임과 에너지 손실을 최소화하기 위한 신속한 시정 조치를 가능하게 합니다. 신흥 벤더들은 이러한 성장을 활용할 수 있습니다. 예를 들어 2025년 6월 슈나이더 일렉트릭은 NTT 데이터와 협력하여 유럽의 여러 데이터센터에 EcoStruxure IT DCIM 플랫폼을 구축하여 운영 효율성과 에너지 절감을 강화했습니다. 벤더는 분석, 자동화, 모니터링을 통합하여 에너지 효율적이고 지속가능하며 규정을 준수하는 데이터센터 운영을 실현할 수 있습니다.

북미는 에너지 효율이 높은 인프라, 재생에너지 설비, 엄격한 지속가능성 규제 준수에 대한 기업 수요 증가에 힘입어 그린 데이터센터 시장을 주도할 것으로 예측됩니다. 이는 솔루션 프로바이더와 벤더들에게 하이퍼스케일 클라우드, 금융 서비스, AI 기반 분석, 헬스케어 등의 산업을 지원하는 확장 가능한 플랫폼을 제공할 수 있는 큰 기회가 될 것입니다. 이 지역의 성숙한 데이터센터 생태계와 넷제로(Net Zero) 개념의 급속한 채택은 기존의 전력 집약적 시설에서 저배출, 모듈형, 고밀도 설계로의 전환을 가속화하고 있으며, 지속가능하고 규정을 준수하는 인프라에 대한 강력한 수요를 창출하고 있습니다.

재생에너지 공급업체 및 기술 공급업체와의 파트너십을 포함한 전략적 협력 관계는 그린 데이터센터가 어떻게 운영 효율성을 높이고 탄소발자국을 줄일 수 있는지를 입증하고 있습니다. 이러한 발전을 통해 공급자는 기업의 지속가능성 목표를 달성하고, 에너지 및 규제 문제를 해결하며, 환경적 책임과 기술 혁신이 점점 더 중요해지는 업계에서 강력한 시장 입지를 구축할 수 있습니다.

세계의 그린 데이터센터 시장에 대해 조사했으며, 컴포넌트별, 데이터센터 규모와 용량별, 데이터센터 유형별, 기업용 데이터센터별, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요와 업계 동향

- 서론

- 시장 역학

- 사례 연구 분석

- 에코시스템 분석

- 공급망 분석

- 기술 분석

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 가격 분석

- 특허 분석

- 무역 분석

- 규제 상황

- 고객 비즈니스에 영향을 미치는 동향과 혼란

- 2025-2026년의 주요 컨퍼런스와 이벤트

- 생성형 AI의 영향

- 비즈니스 모델

- 투자와 자금조달 시나리오

- 2025년 미국 관세의 영향

제6장 그린 데이터센터 시장(컴포넌트별)

- 서론

- 인프라

- 소프트웨어

- 서비스

제7장 그린 데이터센터 시장(데이터센터 규모와 용량별)

- 서론

- 엣지 & 마이크로 데이터센터(1-5MW)

- 중규모 데이터센터(5-50MW)

- 대규모 및 하이퍼스케일 데이터센터(50MW 이상)

제8장 그린 데이터센터 시장(데이터센터 유형별)

- 서론

- 클라우드 & 하이퍼스케일 데이터센터

- 코로케이션 데이터센터

- 기업 데이터센터

제9장 그린 데이터센터 시장(기업용 데이터센터별)

- 서론

- 제조

- 에너지·유틸리티

- 소매·E-Commerce

- 테크놀러지·소프트웨어

- 통신

- 미디어·엔터테인먼트

- 은행, 금융 서비스, 보험

- 헬스케어·생명과학

- 정부와 방위

- 기타

제10장 그린 데이터센터 시장(지역별)

- 서론

- 북미

- 북미 : 그린 데이터센터 시장 성장 촉진요인

- 북미 : 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽 : 그린 데이터센터 시장 성장 촉진요인

- 유럽 : 거시경제 전망

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타

- 아시아태평양

- 아시아태평양 : 그린 데이터센터 시장 성장 촉진요인

- 아시아태평양 : 거시경제 전망

- 중국

- 일본

- 인도

- 기타

- 중동 및 아프리카

- 중동 및 아프리카 : 그린 데이터센터 시장 성장 촉진요인

- 중동 및 아프리카 : 거시경제 전망

- 걸프협력회의

- 남아프리카공화국

- 기타

- 라틴아메리카

- 라틴아메리카 : 그린 데이터센터 시장 성장 촉진요인

- 라틴아메리카 : 거시경제 전망

- 브라질

- 멕시코

- 기타

제11장 경쟁 구도

- 서론

- 주요 참여 기업의 전략/강점

- 매출 분석, 2020-2024년

- 시장 점유율 분석, 2024년

- 제품/브랜드 비교 분석

- 기업 평가 매트릭스 : 주요 참여 기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 주요 벤더의 기업 평가와 재무 지표

- 경쟁 시나리오

제12장 기업 개요

- 주요 참여 기업

- SCHNEIDER ELECTRIC

- VERTIV

- EATON

- DAIKIN

- ABB

- DELTA ELECTRONICS

- CARRIER

- SIEMENS

- GE VERNOVA

- STULZ GMBH

- 기타 기업

- GREEN REVOLUTION COOLING

- MODINE(AIREDALE)

- JOHNSON CONTROLS

- HUAWEI DIGITAL POWER TECHNOLOGIES CO., LTD.

- HONEYWELL INTERNATIONAL INC.

- HITACHI ENERGY LTD.

- TRANE

- CYBER POWER SYSTEMS, INC.

- LITE-ON TECHNOLOGY CORPORATION.

- RITTAL PVT. LTD.

- ASETEK INC.

- SUNBIRD SOFTWARE, INC.

- PACKET POWER

- DANFOSS

- ZUTACORE, INC.

- SUBMER

- NORTEK DATA CENTER COOLING

- ALFA LAVAL

- TOSHIBA

- MIDAS IMMERSION COOLING

- COOLIT SYSTEMS

- RIELLO UPS

- MITSUBISHI HEAVY INDUSTRIES, LTD.

- LANGLEY HOLDINGS PLC

- FUJI ELECTRIC CO., LTD.

제13장 인접 시장과 관련 시장

제14장 부록

KSA 25.10.02The global green data center market is expanding rapidly, with a projected market size anticipated to rise from about USD 48.26 billion in 2025 to USD 155.75 billion by 2030, featuring a CAGR of 26.4%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | USD Million |

| Segments | Component, Data Center Size & Capacity, Data Center Type, and Enterprise Data Center |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

The market is driven by the increasing demand for energy-efficient infrastructure to support high-density workloads, where minimizing power consumption and emissions is critical for sustainability. Enterprises are also seeking advanced cooling solutions and intelligent energy management systems to optimize operational efficiency and align with corporate net-zero goals, along with the growing adoption of renewable energy sources to power resource-intensive applications such as AI, cloud computing, and data analytics.

Furthermore, the need for reliable, low-carbon power and scalable modular designs is becoming essential to meet expanding digital workloads, while automated monitoring and carbon reporting capabilities enable compliance with tightening global regulations. In contrast, the market faces restraints, including significant upfront capital expenditure for renewable integration and advanced cooling technologies, and operational complexity in retrofitting existing facilities, which can slow adoption among budget-conscious or legacy-focused organizations.

"Cloud & Hyperscale data centers to account for the fastest growth rate during the forecast period"

Cloud & hyperscale data centers are at the forefront of the green data center market, driving the adoption of renewable energy, advanced cooling technologies, and energy-efficient infrastructure to support large-scale cloud platforms, AI workloads, and global applications. These facilities are designed to deliver high-performance computing at scale while minimizing environmental impact, making sustainability a central component of operational strategy. Strategic partnerships are playing a key role in accelerating this transformation and creating opportunities for emerging vendors and solution providers to contribute innovative, energy-efficient solutions. In November 2024, Schneider Electric and Vertiv, in collaboration with major tech companies such as Google and Microsoft, launched a Request for Information in Europe to replace diesel backup generators with cleaner alternatives, demonstrating the industry's commitment to reducing carbon emissions and embracing low-carbon operations.

Similarly, in 2023, Huawei partnered with Qinghai Yungu Big Data Industry Development Co., Ltd. to develop a 100% clean energy data center in Hainan Prefecture, Qinghai, revealing the potential of modular designs to deliver reliability, flexibility, and high energy efficiency. These collaborations highlight how integrated, scalable, and sustainable infrastructure can meet performance demands while reducing environmental impact. For emerging vendors and solution providers, engaging in such initiatives allows them to offer innovative technologies, enhance their market presence, and contribute significantly to the green transformation of cloud and hyperscale data centers.

"Data center infrastructure management software to hold the largest market share during the forecast period"

Data center infrastructure management (DCIM) is the most critical software segment in green data centers, expected to hold the largest market share during the forecast period, as it enables comprehensive monitoring, control, and optimization of IT and facility resources to maximize sustainability and reduce energy consumption. DCIM provides continuous power and environment monitoring, tracking metrics such as power usage, voltage, temperature, humidity, and airflow across the facility, allowing operators to identify hotspots, detect anomalies, and prevent energy waste while ensuring reliable operations. The software's energy optimization tools analyze consumption patterns to suggest or automate adjustments in cooling, lighting, and IT workloads, reducing carbon footprint without compromising performance. Capacity planning within DCIM enables precise forecasting of power, cooling, and space requirements, ensuring efficient resource allocation and minimizing over-provisioning.

Asset lifecycle management tracks IT and infrastructure components from procurement to retirement, supporting optimal utilization, redundancy reduction, and sustainable procurement practices. Alerting and incident management features provide real-time notifications for potential failures, threshold breaches, or inefficiencies, allowing rapid corrective action to minimize downtime and energy loss. Emerging vendors can capitalize on this growth. For instance, in June 2025, Schneider Electric partnered with NTT Data to deploy its EcoStruxure IT DCIM platform across multiple European data centers, enhancing operational efficiency and energy savings. By integrating analytics, automation, and monitoring, vendors can deliver energy-efficient, sustainable, and regulatory-compliant data center operations.

"North America leads the green data center market with advanced energy-efficient facilities, while Asia Pacific is the fastest-growing region driven by rapid digitalization and high-density computing deployments"

North America is expected to dominate the green data center market, driven by rising enterprise demand for energy-efficient infrastructure, renewable-powered facilities, and compliance with stringent sustainability regulations. This presents significant opportunities to deliver scalable platforms that support industries such as hyperscale cloud, financial services, AI-driven analytics, and healthcare for solution providers and vendors. The region's mature data center ecosystem and rapid adoption of net-zero initiatives accelerate the transition from traditional power-intensive facilities to low-emission, modular, and high-density designs, creating strong demand for sustainable, regulation-compliant infrastructure.

Strategic collaborations, including partnerships with renewable energy suppliers and technology vendors, demonstrate how green data centers enhance operational efficiency and reduce carbon footprints. Capitalizing on these developments enables providers to meet evolving enterprise sustainability goals, address energy and regulatory challenges, and establish resilient market positions in an industry increasingly defined by environmental responsibility and technological innovation.

Breakdown of Primaries

In-depth interviews were conducted with chief executive officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the green data center market.

- By Company: Tier I - 30%, Tier II - 45%, and Tier III - 25%

- By Designation: C-Level Executives - 50%, D-Level Executives -35%, and Others - 15%

- By Region: North America - 50%, Europe - 30%, Asia Pacific - 15%, and Rest of the world - 5%

The report includes a study of key players offering green data center products. It profiles major vendors in the green data center market. The major market players include Schneider Electric (France), Vertiv (US), Eaton (US), Daikin (Japan), ABB (Switzerland), Delta Electronics (Taiwan), Carrier (US), Siemens (Germany), GE Vernova (US), Stulz GmbH (Germany), Green Revolution Cooling (US), Johnson Controls (US), Honeywell International Inc. (US), Trane (Ireland), Cyber Power Systems, Inc. (Taiwan), Rittal Pvt. Ltd. (India), Asetek Inc. (Denmark), Sunbird Software, Inc. (US), Packet Power (US), Danfoss (Denmark), Zutacore, Inc. (US), Submer (Spain), Nortek Data Center Cooling (US), Toshiba (Japan), Midas Immersion Cooling (US), Coolit Systems (Canada), and Riello UPS (Italy).

Research Coverage

This research report categorizes the green data center market based on component (infrastructure (energy infrastructure (renewable power generators, power backup & energy storage, energy effective power distribution), cooling infrastructure (green air cooling, green liquid cooling)), software (data center infrastructure management (DCIM), building management, compliance, others), services (strategy consulting & energy audits, eco-friendly integration & deployment, sustainable operation & maintenance services, others)), data center size & capacity (edge & micro centers, medium data centers, large & hyperscale data centers), data center type (cloud & hyperscale data centers, colocation data centers, enterprise data centers), enterprise data center (BFSI, healthcare & life sciences, energy & utilities, manufacturing, technology & software, media & entertainment, government & defense, telecommunications, retail & e-commerce, and other verticals (education, transportation & logistics, and travel & hospitality)) and region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America).

The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the green data center market. A detailed analysis of the key industry players was done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, new product & service launches, and mergers and acquisitions; and recent developments associated with the green data center market. This report also covers the competitive analysis of upcoming startups in the green data center market ecosystem.

Reason to Buy this Report

The report would provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall green data center market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. It also helps stakeholders understand the market's pulse and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the pointers listed below.

- Analysis of key drivers (AI workloads drive the adoption of green data center solutions, Net-zero mandates accelerate renewable-powered facilities, Rising energy tariffs increase demand for efficiency solutions, Carbon pricing drives investment in low-emission operations), restraints (Limited renewable availability restricts large-scale deployments, High upfront CAPEX slows green data center adoption), opportunities (Prefabricated green modules accelerate facility deployment, Circular IT asset management expands service scope, Sustainability certifications improve enterprise client wins, Waste heat recovery creates monetization avenues), and challenges (Regional policy fragmentation complicates vendor compliance, Supply chain gaps limit access to eco-friendly components)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and new product & service launches in the green data center market

- Market Development: Comprehensive information about lucrative markets - analysis of the green data center market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the green data center market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players such as Schneider Electric (France), Vertiv (US), Eaton (US), Daikin (Japan), ABB (Switzerland), Delta Electronics (Taiwan), Carrier (US), Siemens (Germany), GE Vernova (US), Stulz GmbH (Germany), Green Revolution Cooling (US), Johnson Controls (US), Honeywell International Inc. (US), Trane (Ireland), Cyber Power Systems, Inc. (Taiwan), Rittal Pvt. Ltd. (India), Asetek Inc. (Denmark), Sunbird Software, Inc. (US), Packet Power (US), Danfoss (Denmark), Zutacore, Inc. (US), Submer (Spain), Nortek Data Center Cooling (US), Toshiba (Japan), Midas Immersion Cooling (US), Coolit Systems (Canada), and Riello UPS (Italy). The report also helps stakeholders understand the green data center market's pulse and provides information on key market drivers, restraints, challenges, and opportunities

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakup of primary profiles

- 2.1.2.3 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET BREAKUP AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN GREEN DATA CENTER MARKET

- 4.2 GREEN DATA CENTER MARKET, BY COMPONENT

- 4.3 GREEN DATA CENTER MARKET, BY DATA CENTER SIZE & CAPACITY

- 4.4 GREEN DATA CENTER MARKET, BY DATA CENTER TYPE

- 4.5 GREEN DATA CENTER MARKET, BY ENTERPRISE DATA CENTER

- 4.6 GREEN DATA CENTER MARKET, BY REGION

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 AI workloads to drive adoption of green data center solutions

- 5.2.1.2 Net-zero mandates to accelerate renewable-powered facilities

- 5.2.1.3 Rising energy tariffs to increase demand for efficiency solutions

- 5.2.1.4 Carbon pricing to drive investment in low-emission operations

- 5.2.2 RESTRAINTS

- 5.2.2.1 Limited renewable availability to restrict large-scale deployments

- 5.2.2.2 High upfront CAPEX to slow green data center adoption

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Prefabricated green modules to accelerate facility deployment

- 5.2.3.2 Circular IT asset management to expand service scope

- 5.2.3.3 Sustainability certifications to improve enterprise client wins

- 5.2.3.4 Waste heat recovery to create monetization avenues

- 5.2.4 CHALLENGES

- 5.2.4.1 Regional policy fragmentation to complicate vendor compliance

- 5.2.4.2 Supply chain gaps to limit access to eco-friendly components

- 5.2.1 DRIVERS

- 5.3 CASE STUDY ANALYSIS

- 5.3.1 GREENERGY AND A-KAABEL DRIVE GREEN DATA CENTER GROWTH WITH VERTIV RACK PDUS'

- 5.3.2 SIEMENS SUPPORTS BMO FINANCIAL GROUP WITH WHITE SPACE COOLING OPTIMIZATION (WSCO)

- 5.3.3 HITACHI ENERGY POWERS GREEN DATA CENTER ADVANCEMENT AT TURKIYE'S STAR OF BOSPHORUS FACILITY

- 5.3.4 GRC ENABLES GREEN SUPERCOMPUTING AT TACC WITH IMMERSION COOLING

- 5.3.5 RITTAL LOWERS CARBON FOOTPRINT AT SCOTTISH QUALIFICATIONS AUTHORITY (SQA) DATA CENTERS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.5.1 TECHNOLOGY PROVIDERS

- 5.5.2 POWER & COOLING SOLUTION VENDORS

- 5.5.3 INFRASTRUCTURE SPECIALISTS

- 5.5.4 DATA CENTER SERVICE PROVIDERS

- 5.5.5 ENTERPRISE VERTICALS

- 5.6 TECHNOLOGY ANALYSIS

- 5.6.1 KEY TECHNOLOGIES

- 5.6.1.1 Renewable/Clean power integration

- 5.6.1.2 Adiabatic cooling

- 5.6.1.3 Free cooling

- 5.6.1.4 Heat reuse/recovery systems

- 5.6.2 COMPLEMENTARY TECHNOLOGIES

- 5.6.2.1 Immersion cooling

- 5.6.2.2 AI/ML-driven energy optimization

- 5.6.2.3 Grid-interactive demand response systems

- 5.6.2.4 Hydrogen backup systems

- 5.6.3 ADJACENT TECHNOLOGIES

- 5.6.3.1 Smart grid systems

- 5.6.3.2 Carbon capture & storage

- 5.6.3.3 Renewable energy trading platforms

- 5.6.3.4 Smart buildings & energy management systems

- 5.6.1 KEY TECHNOLOGIES

- 5.7 PORTER'S FIVE FORCES ANALYSIS

- 5.7.1 THREAT OF NEW ENTRANTS

- 5.7.2 THREAT OF SUBSTITUTES

- 5.7.3 BARGAINING POWER OF SUPPLIERS

- 5.7.4 BARGAINING POWER OF BUYERS

- 5.7.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.8 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.8.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.8.2 BUYING CRITERIA

- 5.9 PRICING ANALYSIS

- 5.9.1 PRICING RANGE OF DATA CENTER UPS, BY REGION, 2024

- 5.9.2 PRICING RANGE OF DATA-CENTER UPS FOR HYPERSCALE DEPLOYMENTS, BY KEY PLAYER, 2024

- 5.10 PATENT ANALYSIS

- 5.11 TRADE ANALYSIS

- 5.11.1 EXPORT SCENARIO

- 5.11.2 IMPORT SCENARIO

- 5.12 REGULATORY LANDSCAPE

- 5.12.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.12.2 KEY REGULATIONS, BY REGION

- 5.12.2.1 North America

- 5.12.2.2 Europe

- 5.12.2.3 Asia Pacific

- 5.12.2.4 Middle East & South Africa

- 5.12.2.5 Latin America

- 5.13 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.14 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.15 IMPACT OF GENERATIVE AI

- 5.15.1 TOP USE CASES & MARKET POTENTIAL

- 5.15.2 KEY USE CASES

- 5.15.3 CASE STUDY

- 5.15.3.1 Siemens AI-powered Optimization at Greenergy Data Centers, Estonia

- 5.15.4 VENDOR INITIATIVE

- 5.16 BUSINESS MODELS

- 5.17 INVESTMENT AND FUNDING SCENARIO

- 5.18 IMPACT OF 2025 US TARIFF

- 5.18.1 INTRODUCTION

- 5.18.2 KEY TARIFF RATES

- 5.18.3 PRICE IMPACT ANALYSIS

- 5.18.4 IMPACT ON COUNTRY/REGION

- 5.18.4.1 US

- 5.18.4.2 Europe

- 5.18.4.3 Asia Pacific

- 5.18.5 IMPACT ON ENTERPRISE DATA CENTERS

- 5.18.5.1 Manufacturing

- 5.18.5.2 Retail & Ecommerce

- 5.18.5.3 Energy & Utilities

- 5.18.5.4 Technology & Software

- 5.18.5.5 Telecommunications

- 5.18.5.6 Media & Entertainment

- 5.18.5.7 BFSI

- 5.18.5.8 Healthcare & Life Sciences

- 5.18.5.9 Government & Defense

6 GREEN DATA CENTER MARKET, BY COMPONENT

- 6.1 INTRODUCTION

- 6.1.1 COMPONENT: GREEN DATA CENTER MARKET DRIVERS

- 6.2 INFRASTRUCTURE

- 6.2.1 ENERGY INFRASTRUCTURE

- 6.2.1.1 Reducing carbon footprint through clean energy to provide sustainable power

- 6.2.1.2 Renewable power generators

- 6.2.1.2.1 Solar power generators

- 6.2.1.2.2 Wind power generators

- 6.2.1.2.3 Hydrogen-ready turbines/HVO/Biofuel-ready gensets

- 6.2.1.3 Power backup & energy storage

- 6.2.1.3.1 High-efficiency UPS (Modular, Lithium-ion, Eco-mode)

- 6.2.1.3.2 Battery energy storage systems (Li-ion/LFP, Flow)

- 6.2.1.4 Energy-effective power distribution

- 6.2.1.4.1 Intelligent PDUs (Switched/Metered)

- 6.2.1.4.2 Efficient busway systems

- 6.2.1.4.3 Others

- 6.2.2 COOLING INFRASTRUCTURE

- 6.2.2.1 Combining air and liquid cooling to provide optimal efficiency

- 6.2.2.2 Green air cooling

- 6.2.2.2.1 Energy-efficient air handlers (CRAH & CRAC)

- 6.2.2.2.2 Eco-friendly air-cooled chillers

- 6.2.2.2.3 Others

- 6.2.2.3 Green liquid cooling

- 6.2.2.3.1 Optimized thermal transfer coolant distribution units (CDUs)

- 6.2.2.3.2 High-efficiency water-cooled chillers

- 6.2.2.3.3 Energy efficient heat exchangers

- 6.2.2.3.4 Others

- 6.2.1 ENERGY INFRASTRUCTURE

- 6.3 SOFTWARE

- 6.3.1 DATA CENTER INFRASTRUCTURE MANAGEMENT

- 6.3.1.1 Integrating data center infrastructure to maximize sustainability and reduce energy consumption

- 6.3.1.1.1 Power & Environment monitoring

- 6.3.1.1.2 Energy optimization

- 6.3.1.1.3 Capacity planning

- 6.3.1.1.4 Asset lifecycle management

- 6.3.1.1.5 Altering & incident management

- 6.3.1.1 Integrating data center infrastructure to maximize sustainability and reduce energy consumption

- 6.3.2 BUILDING MANAGEMENT

- 6.3.2.1 Monitoring and control of electrical and mechanical systems to minimize energy consumption

- 6.3.2.1.1 Building automation system

- 6.3.2.1.2 Smart lighting systems

- 6.3.2.1.3 HVAC control & optimization platforms

- 6.3.2.1 Monitoring and control of electrical and mechanical systems to minimize energy consumption

- 6.3.3 COMPLIANCE

- 6.3.3.1 Maintaining regulatory and industry standards to track carbon emissions and other sustainability metrics

- 6.3.3.1.1 Sustainability compliance reporting

- 6.3.3.1.2 ESG reporting tools

- 6.3.3.1.3 Green certification management

- 6.3.3.1 Maintaining regulatory and industry standards to track carbon emissions and other sustainability metrics

- 6.3.4 OTHER SOFTWARE

- 6.3.1 DATA CENTER INFRASTRUCTURE MANAGEMENT

- 6.4 SERVICES

- 6.4.1 STRATEGY CONSULTING & ENERGY AUDITS

- 6.4.1.1 Operational risk assessment to ensure sustainability and long-term performance

- 6.4.2 ECO-FRIENDLY INTEGRATION & DEPLOYMENT

- 6.4.2.1 Eco-friendly technology commissioning to reduce energy consumption and environmental impact

- 6.4.3 SUSTAINABLE OPERATION AND MAINTENANCE SERVICES

- 6.4.3.1 Routine inspection and system tuning to ensure optimal efficiency

- 6.4.4 OTHER SERVICES

- 6.4.1 STRATEGY CONSULTING & ENERGY AUDITS

7 GREEN DATA CENTER MARKET, BY DATA CENTER SIZE & CAPACITY

- 7.1 INTRODUCTION

- 7.1.1 DATA CENTER SIZE & CAPACITY: GREEN DATA CENTER MARKET DRIVERS

- 7.2 EDGE & MICRO DATA CENTERS (1-5 MW)

- 7.2.1 POWERING NEXT WAVE OF LOW-CARBON COMPUTING TO SUPPORT 5G, IOT, AND AI APPLICATIONS

- 7.3 MEDIUM DATA CENTERS (5-50 MW)

- 7.3.1 ACCELERATING SUSTAINABLE DIGITAL TRANSFORMATION TO ENHANCE SCALABLE CAPACITY

- 7.4 LARGE & HYPERSCALE DATA CENTERS (50 MW & ABOVE)

- 7.4.1 REDEFINING GLOBAL CONNECTIVITY THROUGH GREEN INNOVATION TO SUPPORT HYPERSCALE CLOUD PLATFORMS

8 GREEN DATA CENTER MARKET, BY DATA CENTER TYPE

- 8.1 INTRODUCTION

- 8.1.1 DATA CENTER TYPE: GREEN DATA CENTER MARKET DRIVERS

- 8.2 CLOUD & HYPERSCALE DATA CENTERS

- 8.2.1 CLOUD AND HYPERSCALE DATA CENTERS TO DRIVE GLOBAL SUSTAINABILITY WITH SCALABLE ENERGY-EFFICIENT INFRASTRUCTURE

- 8.3 COLOCATION DATA CENTERS

- 8.3.1 COLOCATION DATA CENTERS TO TRANSFORM MULTI-TENANT OPERATIONS THROUGH INNOVATIVE GREEN TECHNOLOGIES

- 8.4 ENTERPRISE DATA CENTERS

- 8.4.1 ENTERPRISE DATA CENTERS TO ACCELERATE LOW-CARBON DIGITAL INFRASTRUCTURE VIA STRATEGIC SUSTAINABLE COLLABORATIONS

9 GREEN DATA CENTER MARKET, BY ENTERPRISE DATA CENTER

- 9.1 INTRODUCTION

- 9.1.1 VERTICALS: GREEN DATA CENTER MARKET DRIVERS

- 9.2 MANUFACTURING

- 9.2.1 ENHANCE SUSTAINABLE MANUFACTURING WITH LOW-CARBON, MODULAR, AND ENERGY-EFFICIENT SOLUTIONS

- 9.3 ENERGY & UTILITIES

- 9.3.1 ENABLE SUSTAINABLE GRID INTEGRATION WITH EFFICIENT, RENEWABLE-READY DATA CENTERS

- 9.4 RETAIL & E-COMMERCE

- 9.4.1 POWER SEAMLESS OMNICHANNEL GROWTH THROUGH ENERGY-EFFICIENT, SCALABLE FACILITIES

- 9.5 TECHNOLOGY & SOFTWARE

- 9.5.1 SUPPORT AI AND ANALYTICS WITH LOW-CARBON, HIGH-DENSITY INFRASTRUCTURE

- 9.6 TELECOMMUNICATIONS

- 9.6.1 DRIVE 5G AND EDGE EXPANSION USING RESILIENT GREEN DATA CENTERS

- 9.7 MEDIA & ENTERTAINMENT

- 9.7.1 DELIVER HIGH-PERFORMANCE STREAMING WITH OPTIMIZED COOLING AND POWER SYSTEMS

- 9.8 BANKING, FINANCIAL SERVICES & INSURANCE

- 9.8.1 ENSURE SECURE, COMPLIANT OPERATIONS WITH ENERGY-EFFICIENT, LOW-EMISSION INFRASTRUCTURE

- 9.9 HEALTHCARE & LIFE SCIENCES

- 9.9.1 ENABLE DATA-INTENSIVE RESEARCH WITH SUSTAINABLE, HIGH-AVAILABILITY DATA CENTERS

- 9.10 GOVERNMENT & DEFENSE

- 9.10.1 ACHIEVE RESILIENT DIGITAL INFRASTRUCTURE THROUGH EFFICIENT, POLICY-ALIGNED GREEN FACILITIES

- 9.11 OTHER ENTERPRISE DATA CENTERS

10 GREEN DATA CENTER MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 NORTH AMERICA: GREEN DATA CENTER MARKET DRIVERS

- 10.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 10.2.3 US

- 10.2.3.1 Replacing fossil-based systems with renewable-ready power and efficiency-driven technologies to drive market

- 10.2.4 CANADA

- 10.2.4.1 Innovative cooling initiatives to create favorable conditions for building and scaling sustainable data center infrastructure

- 10.3 EUROPE

- 10.3.1 EUROPE: GREEN DATA CENTER MARKET DRIVERS

- 10.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 10.3.3 UK

- 10.3.3.1 Need for sustainable data center infrastructure to support grid stability and community energy goals

- 10.3.4 GERMANY

- 10.3.4.1 Stringent efficiency laws and emphasis on waste heat reuse to increase demand for utility-integrated solutions

- 10.3.5 FRANCE

- 10.3.5.1 Strong low-carbon grid and stringent energy regulations to drive demand for advanced power and cooling technologies

- 10.3.6 ITALY

- 10.3.6.1 Rising need for AI workloads and growing grid complexity to drive demand for sustainable data center solutions

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 ASIA PACIFIC: GREEN DATA CENTER MARKET DRIVERS

- 10.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 10.4.3 CHINA

- 10.4.3.1 Increasing demand for sustainable data centers to support rising AI and high-performance workloads

- 10.4.4 JAPAN

- 10.4.4.1 Robust policies and strategic industrial partnerships to drive demand for low-carbon and net-zero infrastructure

- 10.4.5 INDIA

- 10.4.5.1 Increasing adoption of green data centers to drive sustainable, low-carbon digital infrastructure

- 10.4.6 REST OF ASIA PACIFIC

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 MIDDLE EAST & AFRICA: GREEN DATA CENTER MARKET DRIVERS

- 10.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 10.5.3 GULF COOPERATION COUNCIL

- 10.5.3.1 Saudi Arabia

- 10.5.3.1.1 Green data center initiatives to offer opportunities for sustainable and energy-efficient solutions

- 10.5.3.2 UAE

- 10.5.3.2.1 Integration of renewable energy and innovative cooling technologies to drive market

- 10.5.3.3 Rest of GCC

- 10.5.3.1 Saudi Arabia

- 10.5.4 SOUTH AFRICA

- 10.5.4.1 Renewable energy integration and energy-efficient operations to boost adoption of sustainable digital infrastructure

- 10.5.5 REST OF MIDDLE EAST & AFRICA

- 10.6 LATIN AMERICA

- 10.6.1 LATIN AMERICA: GREEN DATA CENTER MARKET DRIVERS

- 10.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 10.6.3 BRAZIL

- 10.6.3.1 Aligning renewable energy strength with advanced infrastructure development to drive market

- 10.6.4 MEXICO

- 10.6.4.1 Integration of solar energy and efficient Tier III expansions to boost demand for sustainable digital infrastructure

- 10.6.5 REST OF LATIN AMERICA

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 11.3 REVENUE ANALYSIS, 2020-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 PRODUCT/BRAND COMPARISON ANALYSIS

- 11.5.1 SCHNEIDER ELECTRIC

- 11.5.2 EATON

- 11.5.3 VERTIV

- 11.5.4 DAIKIN

- 11.5.5 ABB

- 11.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.6.1 STARS

- 11.6.2 EMERGING LEADERS

- 11.6.3 PERVASIVE PLAYERS

- 11.6.4 PARTICIPANTS

- 11.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.6.5.1 Company footprint

- 11.6.5.2 Region footprint

- 11.6.5.3 Component footprint

- 11.6.5.4 Data center type footprint

- 11.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.7.1 PROGRESSIVE COMPANIES

- 11.7.2 RESPONSIVE COMPANIES

- 11.7.3 DYNAMIC COMPANIES

- 11.7.4 STARTING BLOCKS

- 11.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.7.5.1 Detailed list of key startups/SMEs

- 11.7.5.2 Competitive benchmarking of startups/SMEs

- 11.8 COMPANY VALUATION AND FINANCIAL METRICS OF KEY VENDORS

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES

- 11.9.2 DEALS

- 11.9.3 EXPANSIONS

12 COMPANY PROFILES

- 12.1 MAJOR PLAYERS

- 12.1.1 SCHNEIDER ELECTRIC

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Solutions/Services offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches

- 12.1.1.3.2 Deals

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 VERTIV

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Solutions/Services offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches

- 12.1.2.3.2 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 EATON

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Solutions/Services offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches

- 12.1.3.3.2 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 DAIKIN

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Solutions/Services offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches

- 12.1.4.3.2 Deals

- 12.1.4.4 MnM view

- 12.1.4.4.1 Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 ABB

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Solutions/Services offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches

- 12.1.5.3.2 Deals

- 12.1.5.4 MnM view

- 12.1.5.4.1 Right to win

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses and competitive threats

- 12.1.6 DELTA ELECTRONICS

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Solutions/Services offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches

- 12.1.6.3.2 Deals

- 12.1.6.4 Expansions

- 12.1.7 CARRIER

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Solutions/Services offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Product launches

- 12.1.7.3.2 Deals

- 12.1.8 SIEMENS

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Solutions/Services offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Product launches

- 12.1.8.3.2 Deals

- 12.1.9 GE VERNOVA

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Solutions/Services offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Product launches

- 12.1.9.3.2 Deals

- 12.1.10 STULZ GMBH

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Solutions/Services offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Product launches

- 12.1.10.3.2 Deals

- 12.1.10.3.3 Expansions

- 12.1.1 SCHNEIDER ELECTRIC

- 12.2 OTHER PLAYERS

- 12.2.1 GREEN REVOLUTION COOLING

- 12.2.2 MODINE (AIREDALE)

- 12.2.3 JOHNSON CONTROLS

- 12.2.4 HUAWEI DIGITAL POWER TECHNOLOGIES CO., LTD.

- 12.2.5 HONEYWELL INTERNATIONAL INC.

- 12.2.6 HITACHI ENERGY LTD.

- 12.2.7 TRANE

- 12.2.8 CYBER POWER SYSTEMS, INC.

- 12.2.9 LITE-ON TECHNOLOGY CORPORATION.

- 12.2.10 RITTAL PVT. LTD.

- 12.2.11 ASETEK INC.

- 12.2.12 SUNBIRD SOFTWARE, INC.

- 12.2.13 PACKET POWER

- 12.2.14 DANFOSS

- 12.2.15 ZUTACORE, INC.

- 12.2.16 SUBMER

- 12.2.17 NORTEK DATA CENTER COOLING

- 12.2.18 ALFA LAVAL

- 12.2.19 TOSHIBA

- 12.2.20 MIDAS IMMERSION COOLING

- 12.2.21 COOLIT SYSTEMS

- 12.2.22 RIELLO UPS

- 12.2.23 MITSUBISHI HEAVY INDUSTRIES, LTD.

- 12.2.24 LANGLEY HOLDINGS PLC

- 12.2.25 FUJI ELECTRIC CO., LTD.

13 ADJACENT AND RELATED MARKETS

- 13.1 INTRODUCTION

- 13.1.1 RELATED MARKETS

- 13.1.2 LIMITATIONS

- 13.2 DATA CENTER COOLING MARKET

- 13.3 DATA CENTER SOLUTIONS MARKET

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS