|

시장보고서

상품코드

1829990

불소수지 튜브 시장 : 폼팩터별, 재료별, 용도별, 지역별 - 예측(-2030년)Fluoropolymer Tubing Market by Material (PTFE, FEP, PFA, ETFE, PVDF, and Others), Form Factor (Heat Shrink, Single Lumen, Co-extruded, Multi Lumen, Tapered or Bump Tubing, Braided Tubing), Application, and Region - Global Forecast to 2030 |

||||||

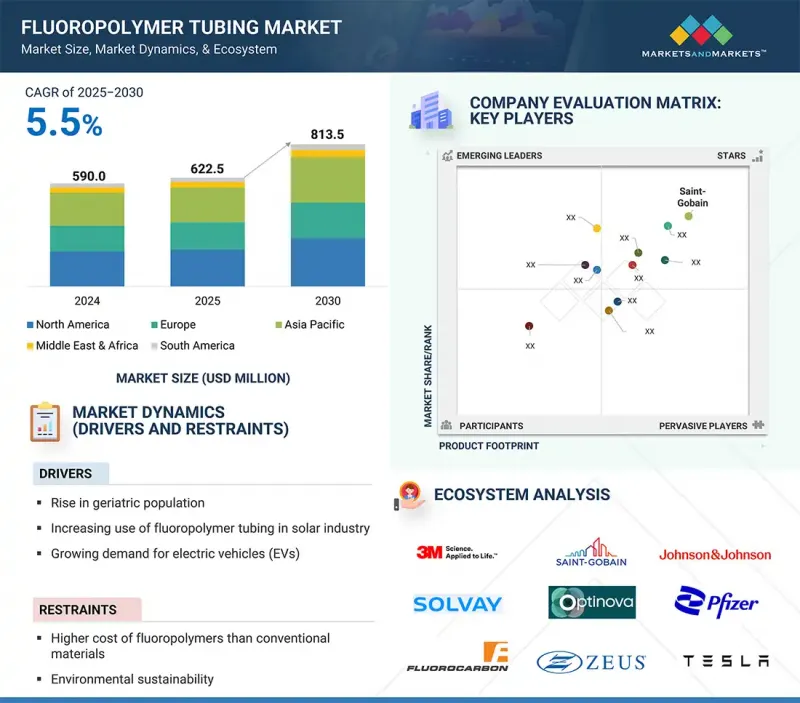

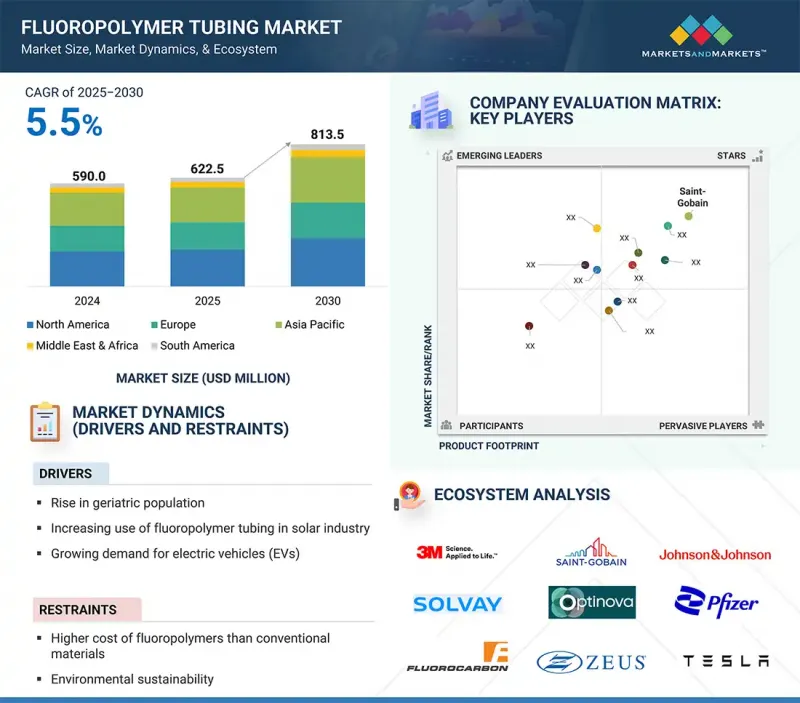

불소수지 튜브 시장 규모는 2025년 6억 2,250만 달러에서 2030년에는 8억 1,350만 달러에 이를 것으로 예측되며, 2025년부터 2030년까지 연평균 복합 성장률(CAGR)은 5.5%로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2022년-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(100만 달러), 킬로톤 |

| 부문 | 폼팩터별, 재료별, 용도별, 지역별 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미 |

불소수지 튜브 시장에서 PFA 소재 부문은 금액 기준으로 세 번째 점유율을 차지하고 있으며, 이는 다양한 산업 분야에서 다재다능하고 고성능인 PFA 소재의 확고한 입지를 반영합니다. PFA 튜브는 PTFE의 뛰어난 내화학성과 열안정성에 더해 유연성과 용융 가공성을 겸비한 독특한 특성 밸런스를 가지고 있어 정밀하고 복잡한 형상을 쉽게 제조할 수 있습니다. 고순도이며 응력 균열이 적기 때문에 웨이퍼 가공 및 클린룸 작업에서 오염이 없는 유체 취급이 중요한 반도체 및 전자기기 용도에 특히 적합합니다. PFA 튜브는 생체적합성, 내멸균성, 강한 자극성 약품 및 반복적인 멸균 사이클에 노출되어도 무결성을 유지하는 능력으로 인해 전자제품 외에도 제약, 생명공학, 의료기기 등의 분야에서 널리 사용되고 있습니다. 화학 처리 산업에서는 가혹한 조건에서 부식성이 높은 액체와 가스를 안전하게 운반하는 데 선호됩니다. 또한, 그 투명성은 육안으로 유량 모니터링이 필요한 응용 분야에서 우위를 발휘합니다. PFA는 다른 불소수지에 비해 고가인 경향이 있지만, 특수 고가용도에서의 성능적 장점과 신뢰성으로 인해 불소수지 튜브 시장에서 금액기준으로 3위를 차지하고 있습니다.

불소수지 튜브 시장에서는 가혹한 사용조건을 견딜 수 있는 고성능 소재에 대한 의존도가 높아짐에 따라 자동차 응용 분야가 예측 기간 동안 금액 기준으로 세 번째 점유율을 차지할 것으로 예측됩니다. 불소수지 튜브는 내열성, 내화학성, 내식성이 우수하여 연료 처리, 브레이크 라인, 변속기, 터보차저 부품, 배기가스 제어 시스템 등 자동차 시스템에 널리 사용되고 있습니다. 전기차와 하이브리드 자동차의 보급에 따라 안전성, 내구성, 효율성이 중요시되는 열관리 시스템, 배터리 냉각, 배선 보호 등을 중심으로 첨단 튜브 솔루션에 대한 수요도 증가하고 있습니다. 주요 자동차 시장에서 배기가스 규제가 강화됨에 따라 불소수지 튜브는 유체 취급 및 배기가스 재순환 시스템의 성능과 신뢰성을 향상시키기 위해 제조업체를 이끌고 있습니다. 또한, 불소수지는 가볍기 때문에 연비 효율과 환경 부하 감소를 중시하는 자동차 산업에 더욱 힘을 실어줄 것입니다. 자동차 제조업체들이 첨단 기술 통합을 추진하고 최소한의 유지보수로 긴 수명을 실현하는 것을 우선시하는 가운데, 불소수지 튜브는 필수적인 부품이 되어 자동차 산업이 전체 시장에 큰 기여를 하고 있습니다.

아시아태평양은 빠르게 성장하는 산업 기반과 다양한 최종 사용 분야에 힘입어 예측 기간 동안 불소수지 튜브 시장에서 두 번째 점유율을 차지할 것으로 예측됩니다. 이 지역은 특히 중국, 일본, 한국, 인도 등의 국가에서 강력한 제조 생태계가 구축되어 있으며, 고성능 소재에 대한 수요가 지속적으로 증가하고 있습니다. 아시아태평양에 집중되어 있는 반도체 및 전자 산업은 칩 제조 및 클린룸 작업에서 초순도 및 무공해 솔루션이 필요하기 때문에 불소수지 튜브의 주요 수요처가 되고 있습니다. 이 지역의 제약 및 의료기기 산업은 의료비 지출 증가와 의료 인프라의 발전에 힘입어 약물 전달, 진단, 저침습 수술 등의 용도로 불소수지 튜브의 채택이 증가하고 있습니다. 아시아태평양의 화학 가공, 자동차, 항공우주 산업은 견조하여 불소수지 튜브에 대한 수요를 더욱 증가시켰습니다. 이러한 산업에서는 우수한 내화학성, 내구성, 가혹한 사용 조건에서의 성능을 갖춘 소재가 요구되기 때문입니다. 이 지역의 급속한 산업화, 첨단 기술에 대한 투자 증가, 제조업과 의료 서비스 확대를 지원하는 정부의 우호적인 정책은 이 지역 시장 지위를 더욱 강화하고 있습니다. 이러한 요인들이 결합되어 아시아태평양은 예측 기간 동안 불소수지 튜브 세계 시장에서 두 번째 점유율을 확보했습니다.

세계의 불소수지 튜브 시장에 대해 조사했으며, 폼팩터별/재료별/용도별/지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

- 서론

- 시장 역학

- Porter의 Five Forces 분석

- 주요 이해관계자와 구입 기준

- 거시경제 지표

- AI/생성형 AI의 영향

- 밸류체인 분석

- 생태계 분석

- 사례 연구 분석

- 규제 상황

- 기술 분석

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 무역 분석

- 2025-2026년 주요 컨퍼런스 및 이벤트

- 가격 분석

- 투자 및 자금조달 시나리오

- 특허 분석

- 2025년 미국 관세가 불소수지 튜브 시장에 미치는 영향

제6장 불소수지 튜브 시장(폼팩터별)

- 서론

- 열수축

- 싱글 루멘

- 공압출

- 멀티 루멘

- TAPERED 또는 BUMP TUBING

- 편조튜브

제7장 불소수지 튜브 시장(재료별)

- 서론

- PTFE

- FEP

- PFA

- ETFE

- PVDF

- 기타

제8장 불소수지 튜브 시장(용도별)

- 서론

- 의료

- 반도체

- 에너지

- 석유 및 가스

- 자동차

- 항공우주

- 체액 관리

- 일반 산업

- 기타

제9장 불소수지 튜브 시장(지역별)

- 서론

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타

- 중동 및 아프리카

- GCC 국가

- 기타

- 남미

- 브라질

- 아르헨티나

- 기타

제10장 경쟁 구도

- 개요

- 주요 시장 진출기업의 전략/강점, 2023년-2025년

- 매출 분석, 2022년-2024년

- 시장 점유율 분석, 2024년

- 기업 평가와 재무 지표

- 브랜드 및 제품 비교

- 기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 경쟁 시나리오

제11장 기업 개요

- 주요 시장 진출기업

- SAINT-GOBAIN

- ZEUS COMPANY LLC

- OPTINOVA

- PARKER HANNIFIN CORP

- TE CONNECTIVITY

- ADTECH POLYMER ENGINEERING LTD.

- AMETEK, INC.

- SWAGELOK COMPANY

- TEF-CAP INDUSTRIES INC.

- TELEFLEX INCORPORATED

- 3M

- 기타 기업

- FLUOROTHERM

- PEXCO

- JUNKOSHA INC.

- NES

- NICHIAS CORPORATION

- POLYFLON TECHNOLOGY LIMITED

- QUALTEK ELECTRONICS CORP.

- ALLIEDSUPRE CORP

- ELRINGKLINGER AG

- ENTEGRIS

- FLUORTUBING

- HABIA

- NEWAGE INDUSTRIES

- XTRAFLEX

제12장 부록

LSH 25.10.15Fluoropolymer tubing market is projected to reach USD 813.5 million by 2030 from USD 622.5 million in 2025, registering a CAGR of 5.5% from 2025 to 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million), Volume (Kilotons) |

| Segments | Form Factor, Material, Application, and Region |

| Regions covered | Europe, North America, Asia Pacific, Middle East & Africa, and South America |

''By material, the PFA segment accounted for the third-largest share of the fluoropolymer tubing market, in terms of value.''

In terms of value, the PFA material segment accounted for the third-largest share of the fluoropolymer tubing market, reflecting its strong position as a versatile and high-performance option across several industries. PFA tubing offers a unique balance of properties, combining the exceptional chemical resistance and thermal stability of PTFE with greater flexibility and melt-processability, which makes it easier to manufacture into precise and complex shapes. Its high purity and resistance to stress cracking make it particularly suitable for semiconductor and electronics applications, where contamination-free fluid handling is critical in wafer processing and cleanroom operations. Beyond electronics, PFA tubing is also widely used in pharmaceuticals, biotechnology, and medical devices due to its biocompatibility, sterilization resistance, and ability to maintain integrity when exposed to aggressive drugs or repeated sterilization cycles. In the chemical processing industry, it is preferred for safely transporting highly corrosive fluids and gases under extreme conditions. Its transparency further provides an advantage in applications requiring visual flow monitoring. Although PFA tends to be costlier compared to other fluoropolymers, its performance advantages and reliability in specialized, high-value applications secure its position as the third-largest material segment in the fluoropolymer tubing market by value.

"By application, the automotive segment is estimated to account for the third-largest market share in terms of value during the forecast period."

The automotive application segment is projected to account for the third-largest share of the fluoropolymer tubing market in terms of value during the forecast period, supported by the sector's growing reliance on high-performance materials that can withstand demanding operating conditions. Fluoropolymer tubing is widely used in automotive systems for fuel handling, brake lines, transmission, turbocharger components, and emission control systems due to its excellent resistance to heat, chemicals, and corrosion. With the increasing adoption of electric and hybrid vehicles, the demand for advanced tubing solutions is also rising, particularly for thermal management systems, battery cooling, and wiring protection, where safety, durability, and efficiency are critical. Stricter emission standards and regulations across major automotive markets are driving manufacturers to adopt fluoropolymer tubing for improved performance and reliability in fluid handling and exhaust gas recirculation systems. Its lightweight nature further supports the automotive industry's focus on fuel efficiency and reduced environmental impact. As automakers continue to integrate advanced technologies and prioritize longer service life with minimal maintenance, fluoropolymer tubing is becoming an essential component, reinforcing the automotive segment's strong contribution to the overall market.

"Asia Pacific is projected to hold the second-largest market share during the forecast period."

The Asia Pacific region is projected to hold the second-largest share of the fluoropolymer tubing market during the forecast period, driven by its rapidly expanding industrial base and diverse end-use sectors. The region is home to a strong manufacturing ecosystem, particularly in countries such as China, Japan, South Korea, and India, where demand for high-performance materials continues to rise. The semiconductor and electronics industry, which is heavily concentrated in the Asia Pacific, is a major consumer of fluoropolymer tubing due to the need for ultra-pure and contamination-free solutions in chip fabrication and cleanroom operations. The region's growing pharmaceutical and medical device industries are increasingly adopting fluoropolymer tubing for applications in drug delivery, diagnostics, and minimally invasive procedures, supported by rising healthcare spending and advancements in medical infrastructure. Asia Pacific's robust chemical processing, automotive, and aerospace sectors are driving further demand for fluoropolymer tubing, as these industries require materials with superior chemical resistance, durability, and performance in extreme operating conditions. The region's rapid industrialization, increasing investments in advanced technologies, and favorable government policies supporting manufacturing and healthcare expansion further reinforce its market position. Together, these factors contribute to Asia Pacific securing the second-largest share in the global fluoropolymer tubing market during the forecast period.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

- By Company Type- Tier 1- 60%, Tier 2- 20%, and Tier 3- 20%

- By Designation- C Level- 33%, Director Level- 33%, and Managers- 34%

- By Region- North America- 20%, Europe- 25%, Asia Pacific- 25%, Middle East & Africa- 15%, and Latin America- 15%

The report provides a comprehensive analysis of company profiles:

Prominent companies include Saint-Gobain (France), Zeus Company LLC (US), Optinova (Finland), Parker Hannifin (US), TE Connectivity (Ireland), Adtech Polymer Engineering Ltd. (UK), AMETEK Inc. (US), Swagelok Company (US), Tef-Cap Industries (US), and Teleflex Incorporated (US).

Research Coverage

This research report categorizes the fluoropolymer tubing market by Material (PTFE, FEP, PFA, ETFE, PVDF and Others), Form Factor (Heat Shrink, Single Lumen, Co-extruded, Multi Lumen, Tapered or Bump Tubing, Braided Tubing), Application (Medical, Semiconductor, Energy, Oil & Gas, Automotive, Aerospace, Fluid Management, General Industrial), and Region (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The scope of the report includes detailed information about the major factors influencing the growth of the fluoropolymer tubing market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted in order to provide insights into their business overview, solutions, services, key strategies, contracts, partnerships, and agreements. Product launches, mergers & acquisitions, and recent developments in the fluoropolymer tubing market are all covered. This report includes a competitive analysis of upcoming startups in the fluoropolymer tubing market ecosystem.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall fluoropolymer tubing market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (rise in geriatric population, increasing use of fluoropolymer tubing in the solar industry, growing demand for electric vehicles (EVs)), restraints (higher cost of fluoropolymers than conventional materials, environmental sustainability), opportunities (increasing healthcare investments in emerging economies, emerging market for melt extrusion), and challenges (stringent and time-consuming regulatory policies, difficulty in processing high-performance fluoropolymers, intense competition from low-cost suppliers in China).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the fluoropolymer tubing market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the fluoropolymer tubing market across varied regions.

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the fluoropolymer tubing market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Saint-Gobain (France), Zeus Company LLC (US), Optinova (Finland), Parker Hannifin (US), TE Connectivity (Ireland), Adtech Polymer Engineering Ltd. (UK), AMETEK Inc. (US), Swagelok Company (US), Tef-Cap Industries (US), and Teleflex Incorporated (US), among others, in the fluoropolymer tubing market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of key secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 List of primary interview participants-demand and supply sides

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of interviews with experts

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 FORECAST NUMBER CALCULATION

- 2.4 DATA TRIANGULATION

- 2.5 FACTOR ANALYSIS

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 RESEARCH LIMITATIONS AND RISKS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FLUOROPOLYMER TUBING MARKET

- 4.2 FLUOROPOLYMER TUBING MARKET, BY MATERIAL

- 4.3 FLUOROPOLYMER TUBING MARKET, BY FORM FACTOR

- 4.4 FLUOROPOLYMER TUBING MARKET, BY APPLICATION

- 4.5 FLUOROPOLYMER TUBING MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rise in geriatric population

- 5.2.1.2 Increasing use of fluoropolymer tubing in solar energy sector

- 5.2.1.3 Surging electric vehicle sales

- 5.2.1.4 Industrialization in Asia Pacific

- 5.2.2 RESTRAINTS

- 5.2.2.1 Higher production cost of fluoropolymers compared to conventional materials

- 5.2.2.2 Environmental sustainability

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing healthcare investments in emerging economies

- 5.2.3.2 Emerging market for melt extrusion

- 5.2.4 CHALLENGES

- 5.2.4.1 Stringent and time-consuming regulatory policies

- 5.2.4.2 Difficulty in processing high-performance fluoropolymers

- 5.2.4.3 Intense competition from China-based low-cost suppliers

- 5.2.1 DRIVERS

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 BARGAINING POWER OF SUPPLIERS

- 5.3.2 BARGAINING POWER OF BUYERS

- 5.3.3 THREAT OF SUBSTITUTES

- 5.3.4 THREAT OF NEW ENTRANTS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.4.2 BUYING CRITERIA

- 5.5 MACROECONOMIC INDICATORS

- 5.5.1 GLOBAL GDP TRENDS

- 5.6 IMPACT OF AI/GEN AI

- 5.7 VALUE CHAIN ANALYSIS

- 5.7.1 RAW MATERIAL SUPPLIERS

- 5.7.2 MANUFACTURERS

- 5.7.3 DISTRIBUTORS

- 5.7.4 END USERS

- 5.8 ECOSYSTEM ANALYSIS

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 OPTIMIZING CENTRIFUGAL FAN PERFORMANCE WITH DURABLE HALAR ECTFE COATING

- 5.9.2 ENHANCING MEDICAL APPLICATIONS WITH PTFE VALVE SOLUTIONS

- 5.9.3 EXTENDING PTFE COMPONENT LIFECYCLE IN FOOD PROCESSING EQUIPMENT

- 5.10 REGULATORY LANDSCAPE

- 5.10.1 REGULATIONS

- 5.10.1.1 Europe

- 5.10.1.2 Asia Pacific

- 5.10.1.3 North America

- 5.10.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.10.1 REGULATIONS

- 5.11 TECHNOLOGY ANALYSIS

- 5.11.1 KEY TECHNOLOGIES

- 5.11.1.1 Expanded polytetrafluoroethylene (ePTFE)

- 5.11.2 COMPLEMENTARY TECHNOLOGIES

- 5.11.2.1 Radiopaque and custom fillers

- 5.11.1 KEY TECHNOLOGIES

- 5.12 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.13 TRADE ANALYSIS

- 5.13.1 EXPORT SCENARIO

- 5.13.2 IMPORT SCENARIO

- 5.14 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.15 PRICING ANALYSIS

- 5.15.1 AVERAGE SELLING PRICE TREND OF FLUOROPOLYMER TUBING, BY REGION (2022-2024)

- 5.15.2 AVERAGE SELLING PRICE TREND OF FLUOROPOLYMER TUBING, BY APPLICATION, 2022-2024

- 5.15.3 AVERAGE SELLING PRICES OF KEY PLAYERS FOR FLUOROPOLYMER TUBING, BY APPLICATION, 2024

- 5.16 INVESTMENT AND FUNDING SCENARIO

- 5.17 PATENT ANALYSIS

- 5.17.1 APPROACH

- 5.17.2 DOCUMENT TYPES

- 5.17.3 PUBLICATION TRENDS

- 5.17.4 INSIGHTS

- 5.17.5 LEGAL STATUS OF PATENTS

- 5.17.6 JURISDICTION ANALYSIS

- 5.17.7 TOP COMPANIES/APPLICANTS

- 5.17.8 TOP 10 PATENT OWNERS (US) 2014-2024

- 5.18 IMPACT OF 2025 US TARIFF ON FLUOROPOLYMER TUBING MARKET

- 5.18.1 INTRODUCTION

- 5.18.2 KEY TARIFF RATES

- 5.18.3 PRICE IMPACT ANALYSIS

- 5.18.4 IMPACT ON KEY COUNTRIES/REGIONS

- 5.18.4.1 North America

- 5.18.4.2 Europe

- 5.18.4.3 Asia Pacific

- 5.18.5 IMPACT ON END-USE INDUSTRIES

6 FLUOROPOLYMER TUBING MARKET, BY FORM FACTOR

- 6.1 INTRODUCTION

- 6.2 HEAT SHRINK

- 6.2.1 SECURING PERFORMANCE WITH HEAT-SHRINK FLUOROPOLYMER TUBING

- 6.3 SINGLE LUMEN

- 6.3.1 ADVANCING PATIENT CARE THROUGH SPECIALIZED FLUOROPOLYMER TUBING

- 6.4 CO-EXTRUDED

- 6.4.1 ADVANCING PATIENT CARE THROUGH SPECIALIZED FLUOROPOLYMER TUBING

- 6.5 MULTI-LUMEN

- 6.5.1 REDEFINING TUBING DESIGN THROUGH ADVANCED MATERIAL INTEGRATION

- 6.6 TAPERED OR BUMP TUBING

- 6.6.1 EXPANDING APPLICATIONS THROUGH PRECISION ENGINEERING

- 6.7 BRAIDED TUBING

- 6.7.1 DRIVING ADOPTION IN CRITICAL INDUSTRIAL AND MEDICAL SYSTEMS

7 FLUOROPOLYMER TUBING MARKET, BY MATERIAL

- 7.1 INTRODUCTION

- 7.2 PTFE

- 7.2.1 EXHIBITS EXCELLENT CHEMICAL AND THERMAL RESISTANCE

- 7.3 FEP

- 7.3.1 CAN BE MELTED AND RE-EXTRUDED

- 7.4 PFA

- 7.4.1 HAS COMBINED PROPERTIES OF PTFE AND FEP

- 7.5 ETFE

- 7.5.1 PROVIDES BALANCE BETWEEN PHYSICAL PROPERTIES AND COST-EFFECTIVENESS

- 7.6 PVDF

- 7.6.1 RESISTANT TO ACIDS, BASES, AND MANY ORGANIC SOLVENTS

- 7.7 OTHERS

8 FLUOROPOLYMER TUBING MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 MEDICAL

- 8.2.1 DEMAND FOR BIOCOMPATIBLE AND NON-REACTIVE MATERIALS IN MEDICAL DEVICE MANUFACTURING TO DRIVE MARKET

- 8.3 SEMICONDUCTOR

- 8.3.1 ABILITY TO ENDURE AND PERFORM UNDER EXTREME CONDITIONS TO DRIVE DEMAND IN SEMICONDUCTOR INDUSTRY

- 8.4 ENERGY

- 8.4.1 DEMAND FOR CHEMICAL RESISTANCE, THERMAL STABILITY, AND ELECTRICAL INSULATION IN ENERGY SECTOR TO DRIVE MARKET

- 8.5 OIL & GAS

- 8.5.1 DEMAND FOR DURABLE AND CHEMICAL-RESISTANT MATERIALS IN OIL & GAS SECTOR TO DRIVE MARKET

- 8.6 AUTOMOTIVE

- 8.6.1 NEED FOR LOW-FRICTION SURFACES IN AUTOMOTIVE TO DRIVE MARKET

- 8.7 AEROSPACE

- 8.7.1 DEMAND FOR MATERIAL RELIABILITY UNDER EXTREME CONDITIONS TO DRIVE MARKET

- 8.8 FLUID MANAGEMENT

- 8.8.1 PTFE, FEP, AND PFA ARE WIDELY USED IN FLUID MANAGEMENT

- 8.9 GENERAL INDUSTRIAL

- 8.9.1 NEED TO INSULATE WIRES & CABLES FOR HIGH-PRESSURE APPLICATIONS TO DRIVE MARKET

- 8.9.2 WIRE COATING

- 8.9.3 OPTICAL FIBER

- 8.9.4 MONOFILAMENT

- 8.10 OTHERS

9 FLUOROPOLYMER TUBING MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 NORTH AMERICA

- 9.2.1 US

- 9.2.1.1 Growth in EV and renewable energy adoption to drive market

- 9.2.2 CANADA

- 9.2.2.1 Industrial diversification to boost tubing applications

- 9.2.3 MEXICO

- 9.2.3.1 Energy transition policies to stimulate tubing demand in renewable projects

- 9.2.1 US

- 9.3 EUROPE

- 9.3.1 GERMANY

- 9.3.1.1 Investments in medical R&D to fuel market

- 9.3.2 FRANCE

- 9.3.2.1 Defense and aerospace leadership to enhance fluoropolymer tubing demand

- 9.3.3 UK

- 9.3.3.1 Increasing aging population and chronic diseases to boost fluoropolymer tubing consumption

- 9.3.4 ITALY

- 9.3.4.1 Integrated industrial growth to create new opportunities for fluoropolymer tubing

- 9.3.5 SPAIN

- 9.3.5.1 Increase in automotive manufacturing and medical technology demand to fuel market

- 9.3.6 REST OF EUROPE

- 9.3.1 GERMANY

- 9.4 ASIA PACIFIC

- 9.4.1 CHINA

- 9.4.1.1 Rising electronics production to support growth of industrial tubing applications

- 9.4.2 JAPAN

- 9.4.2.1 Medical sector modernization to spur demand for high-performance tubing

- 9.4.3 INDIA

- 9.4.3.1 Rise in EV and battery manufacturing to create market growth opportunities

- 9.4.4 SOUTH KOREA

- 9.4.4.1 Vibrant semiconductor and energy sectors to drive market

- 9.4.5 REST OF ASIA PACIFIC

- 9.4.1 CHINA

- 9.5 MIDDLE EAST & AFRICA

- 9.5.1 GCC COUNTRIES

- 9.5.1.1 Saudi Arabia

- 9.5.1.1.1 Petrochemical expansion to elevate tubing requirements

- 9.5.1.2 Rest of GCC countries

- 9.5.1.3 South Africa

- 9.5.1.3.1 Investment in healthcare infrastructure to support market growth

- 9.5.1.1 Saudi Arabia

- 9.5.2 REST OF MIDDLE EAST & AFRICA

- 9.5.1 GCC COUNTRIES

- 9.6 SOUTH AMERICA

- 9.6.1 BRAZIL

- 9.6.1.1 Automotive modernization to support tubing application expansion in EVs

- 9.6.2 ARGENTINA

- 9.6.2.1 Industrial expansion to fuel adoption of fluoropolymer tubing

- 9.6.3 REST OF SOUTH AMERICA

- 9.6.1 BRAZIL

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2025

- 10.3 REVENUE ANALYSIS, 2022-2024

- 10.4 MARKET SHARE ANALYSIS, 2024

- 10.5 COMPANY VALUATION AND FINANCIAL METRICS

- 10.6 BRAND/PRODUCT COMPARISON

- 10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.7.1 STARS

- 10.7.2 EMERGING LEADERS

- 10.7.3 PERVASIVE PLAYERS

- 10.7.4 PARTICIPANTS

- 10.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.7.5.1 Company footprint

- 10.7.5.2 Region footprint

- 10.7.5.3 Form factor footprint

- 10.7.5.4 Application footprint

- 10.7.5.5 Material footprint

- 10.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 10.8.1 PROGRESSIVE COMPANIES

- 10.8.2 RESPONSIVE COMPANIES

- 10.8.3 DYNAMIC COMPANIES

- 10.8.4 STARTING BLOCKS

- 10.8.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2024

- 10.8.5.1 Detailed list of key startups/SMEs

- 10.8.5.2 Competitive benchmarking of key startups/SMEs

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES

- 10.9.2 EXPANSIONS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 SAINT-GOBAIN

- 11.1.1.1 Business overview

- 11.1.1.2 Products/Solutions/Services offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Product launches

- 11.1.1.4 MnM view

- 11.1.1.4.1 Right to win

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses and competitive threats

- 11.1.2 ZEUS COMPANY LLC

- 11.1.2.1 Business overview

- 11.1.2.2 Products/Solutions/Services offered

- 11.1.2.3 MnM view

- 11.1.2.3.1 Right to win

- 11.1.2.3.2 Strategic choices

- 11.1.2.3.3 Weaknesses and competitive threats

- 11.1.3 OPTINOVA

- 11.1.3.1 Business overview

- 11.1.3.2 Products/Solutions/Services offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Expansions

- 11.1.3.4 MnM view

- 11.1.3.4.1 Right to win

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses and competitive threats

- 11.1.4 PARKER HANNIFIN CORP

- 11.1.4.1 Business overview

- 11.1.4.2 Products/Solutions/Services offered

- 11.1.4.3 MnM view

- 11.1.4.3.1 Right to win

- 11.1.4.3.2 Strategic choices

- 11.1.4.3.3 Weaknesses and competitive threats

- 11.1.5 TE CONNECTIVITY

- 11.1.5.1 Business overview

- 11.1.5.2 Products/Solutions/Services offered

- 11.1.5.3 MnM view

- 11.1.5.3.1 Right to win

- 11.1.5.3.2 Strategic choices

- 11.1.5.3.3 Weaknesses and competitive threats

- 11.1.6 ADTECH POLYMER ENGINEERING LTD.

- 11.1.6.1 Business overview

- 11.1.6.2 Products/Solutions/Services offered

- 11.1.6.3 Recent developments

- 11.1.6.3.1 Product launches

- 11.1.6.4 MnM view

- 11.1.7 AMETEK, INC.

- 11.1.7.1 Business overview

- 11.1.7.2 Products/Solutions/Services offered

- 11.1.7.3 MnM view

- 11.1.8 SWAGELOK COMPANY

- 11.1.8.1 Business overview

- 11.1.8.2 Products/Solutions/Services offered

- 11.1.8.3 MnM view

- 11.1.9 TEF-CAP INDUSTRIES INC.

- 11.1.9.1 Business overview

- 11.1.9.2 Products/Solutions/Services offered

- 11.1.9.3 MnM view

- 11.1.10 TELEFLEX INCORPORATED

- 11.1.10.1 Business overview

- 11.1.10.2 Products/Solutions/Services offered

- 11.1.10.3 MnM view

- 11.1.11 3M

- 11.1.11.1 Business overview

- 11.1.11.2 Products/Solutions/Services offered

- 11.1.1 SAINT-GOBAIN

- 11.2 OTHER PLAYERS

- 11.2.1 FLUOROTHERM

- 11.2.2 PEXCO

- 11.2.3 JUNKOSHA INC.

- 11.2.4 NES

- 11.2.5 NICHIAS CORPORATION

- 11.2.6 POLYFLON TECHNOLOGY LIMITED

- 11.2.7 QUALTEK ELECTRONICS CORP.

- 11.2.8 ALLIEDSUPRE CORP

- 11.2.9 ELRINGKLINGER AG

- 11.2.10 ENTEGRIS

- 11.2.11 FLUORTUBING

- 11.2.12 HABIA

- 11.2.13 NEWAGE INDUSTRIES

- 11.2.14 XTRAFLEX

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS