|

시장보고서

상품코드

1845349

발포성 내화 코팅 시장 : 유형별, 기재별, 도포 공법별, 최종 이용 산업별, 지역별 - 예측(-2030년)Intumescent Coatings Market by Type, Substrate, Application Technique, End-use Industry, and Region - Global Forecast to 2030 |

||||||

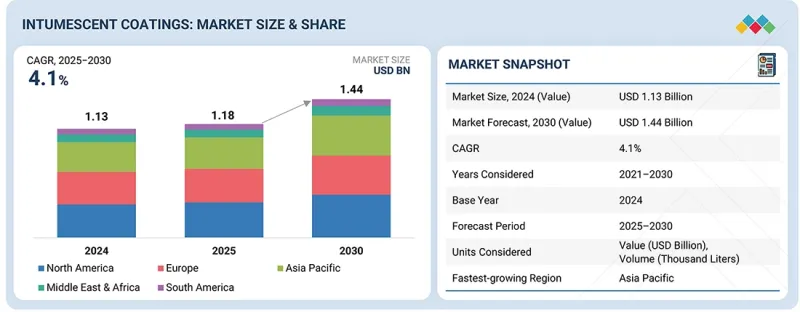

세계의 발포성 내화 코팅 시장 규모는 2024년에 추정 11억 3,000만 달러로 평가되었고, 2030년까지 14억 4,000만 달러에 이를 것으로 예측되어 CAGR 4.1%의 성장이 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 100만 달러, 1,000리터 |

| 부문 | 유형, 기재, 도포 공법, 최종 이용 산업, 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

이 성장의 촉진요인은 화재 안전 규제 강화, 건축법 강화, 건설 투자 증가, 인식 개선 및 보험 혜택, 경량 구조 및 미관에 대한 수요 증가 등입니다. 지속가능성과 낮은 VOC가 특징인 발포성 내화 코팅은 건물 건설, 항공우주, 산업 등 다양한 산업에서 널리 사용되고 있습니다.

"유형별로는 박막 기반 발포성 내화 코팅이 예측 기간 동안 가장 빠른 성장세를 기록할 것으로 예측됩니다. "

박막 발포성 내화 코팅은 미적 완성도, 경량 보호, 현대 건축 및 상업 부문의 구조용 강철에 적용하기 쉽다는 장점으로 인해 세계 시장에서 가장 빠르게 성장하는 분야로 여겨지고 있습니다. 이 코팅은 기본적으로 부피가 크지 않으면서도 내화성을 발휘합니다. 따라서 안전성과 디자인성이 우선시되는 고층빌딩, 공항, 복합상업시설 등 노출된 철골 구조물에 적합합니다. 이러한 코팅에 대한 수요는 화재 안전 법규 증가와 도시 인프라 프로젝트에서의 사용 증가로 인해 증가하고 있습니다.

"기재별로는 구조용 철강 및 주철이 예측 기간 동안 가장 빠른 성장을 기록할 것으로 예측됩니다. "

기재 유형별로는 현대 인프라, 고층 빌딩, 산업 플랜트, 석유 및 가스 시설 등에 광범위하게 사용되어 구조용 강재 및 주철로 만들어진 구조물의 급격한 성장을 보이고 있습니다. 이러한 재료는 고온 조건에 노출되면 강도를 잃기 쉽기 때문에 건물의 구조적 무결성과 안전성을 보장하기 위해 공학적 관점에서 화재 예방 조치가 필요합니다. 녹색 건물과 모듈식 건축을 위한 철강에 힘입어 국제 화재 안전 규정의 강화는 발포성 내화 코팅에 대한 수요 증가에 기여하고 있습니다.

"최종 사용 산업별로는 건축 및 건설 부문이 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예측됩니다. "

주택, 상업시설, 산업시설에서 화재 안전에 대한 중요성이 강조되면서 발포성 내화 코팅 시장 중 건축 및 건설 부문이 가장 빠르게 성장하고 있습니다. 도시화가 진전되고 고층 빌딩과 대형 인프라 프로젝트가 증가함에 따라 고급 수동형 화재 방지 기술의 필요성이 증가하고 있습니다. 건축법, 안전 규정, 보험 요건이 건물 수용을 촉진하는 요인으로 작용하고 있으며, 오래된 건물의 자체 보안 앵글 개조도 이 부문 시장 성장에 박차를 가하고 있습니다.

"도포 공법별로는 스프레이 부문이 가장 큰 비중을 차지했습니다. "

스프레이 도포 공법은 균일한 두께, 매끄러운 마무리, 넓은 표면적을 빠르게 커버할 수 있기 때문에 발포성 내화 코팅의 도포 공법 중 가장 큰 시장 점유율을 차지하는 것으로 추정됩니다. 또한, 구조용 강재 및 산업기기에 적용하는 내화성 코팅으로 중요한 안정된 막의 형성이 가능합니다. 스프레이 도포는 다른 어떤 코팅 방법보다 복잡한 형상에 침투하여 형태를 개선하기 때문에 건설, 석유 및 가스, 항공우주 등의 산업에서 효과적인 도포로 평가받고 있습니다. 그 효율성은 노동 시간과 전체 도포 비용을 절감하고 계약자 및 최종 사용자의 선호도를 높이고 있습니다. 에어리스 스프레이 장비의 개발로 보다 정확한 공법으로서의 스프레이가 더욱 촉진되어 재료의 낭비를 줄이고 점도가 높은 제제의 취급이 용이해졌습니다. 이러한 장점으로 인해 스프레이 도포는 가장 경제적이고 바람직한 선택이 되어 스프레이 도포 공법의 우위에 기여하고 있습니다.

"지역별로는 중동 및 아프리카가 예측 기간 동안 두 번째로 높은 CAGR을 나타낼 것으로 보입니다. "

중동 및 아프리카는 급속한 인프라 개발과 석유 및 가스 부문의 확대로 인해 발포성 내화 코팅 시장에서 두 번째로 빠른 성장세를 보이는 지역 중 하나로 부상하고 있습니다. 사우디아라비아, 아랍에미리트, 카타르 등의 국가들은 고층빌딩, 상업시설, 산업시설 개발에 투자하고 있어 방화 솔루션에 대한 과도한 수요를 창출하고 있습니다. 이 지역에서는 정유공장, 석유화학 플랜트, 해상 플랫폼 건설 등 대규모 에너지 프로젝트와 기타 여러 프로젝트가 진행 중이며, 위험도가 높은 환경에서 구조용 강철을 보호하기 위해 발포성 내화 코팅의 사용이 추진되고 있습니다.

세계의 발포성 내화 코팅 시장에 대해 조사 분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 지견

- 발포성 내화 코팅 시장의 매력적인 기회

- 발포성 내화 코팅 시장 : 유형별

- 발포성 내화 코팅 시장 : 기재별

- 발포성 내화 코팅 시장 : 최종 이용 산업별

- 발포성 내화 코팅 시장 : 도포 공법별

- 북미의 발포성 내화 코팅 시장 : 최종 이용 산업별, 국가별

- 발포성 내화 코팅 시장 : 주요 국가별

제5장 시장 개요

- 서론

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 생태계 분석

- 밸류체인 분석

- 규제 상황

- 규제 상황

- 주요 규제

- 가격 결정 분석

- 무역 분석

- 수출 시나리오(HS코드 3209)

- 수입 시나리오(HS코드 3209)

- 기술 분석

- 주요 기술

- 보완 기술

- 인접 기술

- 특허 분석

- 사례 연구 분석

- 주요 이해관계자와 구입 기준

- 주요 컨퍼런스 및 이벤트(2025년-2026년)

- 투자 및 자금조달 시나리오

- 발포성 내화 코팅 시장에 대한 AI의 영향

- 서론

- 발포성 내화 코팅 시장에 대한 AI의 영향

- Porter의 Five Forces 분석

- 거시경제 분석

- 서론

- GDP 동향과 예측

- 발포성 내화 코팅 시장에 대한 2025년 미국 관세의 영향

- 서론

- 주요 관세율

- 가격 영향 분석

- 국가/지역에 대한 영향

- 최종 이용 산업에 대한 영향

제6장 발포성 내화 코팅 시장 : 도포 공법별

- 서론

- 스프레이

- 브러쉬 및 롤러

제7장 발포성 내화 코팅 시장 : 기재별

- 서론

- 구조용 강철 및 주철

- 목재

- 기타 기재

제8장 발포성 내화 코팅 시장 : 유형별

- 서론

- 박막 발포성 내화 코팅

- 후막 발포성 내화 코팅

제9장 발포성 내화 코팅 시장 : 최종 이용 산업별

- 서론

- 건축 및 건설

- 산업

- 항공우주

- 기타 최종 이용 산업

제10장 발포성 내화 코팅 시장 : 지역별

- 서론

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 이탈리아

- 영국

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC 국가

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 GCC 국가

- 남아프리카공화국

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

제11장 경쟁 구도

- 개요

- 주요 시장 진출기업의 전략/강점

- 매출 분석(2020년-2024년)

- 시장 점유율 분석(2024년)

- 기업 평가와 재무 지표

- 재무 지표

- 브랜드 및 제품 비교

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업 평가 매트릭스 : 스타트업/중소기업(2024년)

- 경쟁 시나리오

제12장 기업 개요

- 주요 기업

- SHERWIN-WILLIAMS

- PPG

- AKZONOBEL

- JOTUN

- HEMPEL A/S

- RPM INTERNATIONAL INC.

- SIKA

- KANSAI PAINT CO., LTD

- ETEX

- TEKNOS

- 기타 기업

- ISOLATEK INTERNATIONAL

- CONTEGO INTERNATIONAL INC.

- ENVIROGRAF

- FIREFREE COATINGS, INC.

- RUDOLF HENSEL GMBH

- NO-BURN, INC.

- HILTI GROUP

- UGAM CHEMICALS

- SUNANDA SPECIALITY COATINGS PVT. LTD.

- AITHON RICERCHE INTERNATIONAL

- IRIS COATINGS

- CHARCOAT PASSIVE FIRE PROTECTION INC.

- CHUGOKU MARINE PAINTS, LTD.

- VITON S.R.O.

- QUANTUM CHEMICAL

제13장 인접 시장과 관련 시장

- 서론

- 내화 코팅 시장

- 시장의 정의

- 시장 개요

- 내화 코팅 시장 : 유형별

- 내화 코팅 시장 : 용도별

- 내화 시장 : 지역별

제14장 부록

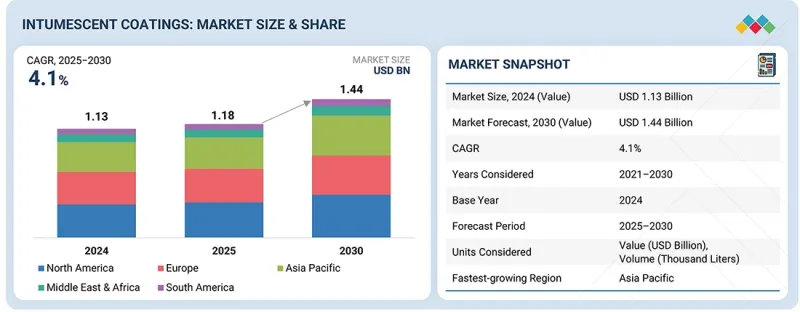

LSH 25.10.28The intumescent coatings market is approximated to be USD 1.13 billion in 2024, and it is projected to reach USD 1.44 billion by 2030, at a CAGR of 4.1%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Thousand Liters) |

| Segments | Type, Substrate, Application Technique, End-use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, and South America |

This growth is driven by tighter fire-safety regulations, stricter building codes, rising construction investments, growing awareness & insurance incentives, and rising demand for lightweight construction and aesthetics. The sustainability and low-VOC of Intumescent Coatings have made it a popular choice in various industries, including building construction, aerospace, industrial, and others.

"By type, thin-film-based intumescent coatings are projected to register the fastest growth during the forecast period."

Thin-film intumescent coatings are considered the fastest-growing segment in the global market because of their super aesthetic finish, lightweight protection, and ease of application on structural steel in the modern architectural and commercial sectors. They essentially provide fire resistance with no added bulk. Hence, they are suitable for exposed steel structures in high-rise buildings, airports, and commercial complexes where safety and design appeal take priority. The demand for these coatings is being augmented by increasing fire safety laws and their growing usage in infrastructure projects across urban areas.

"By substrate, structural steel & cast iron are projected to register the fastest growth during the forecast period."

By the substrate type segments, fast growth rates are observed for structures made out of structural steel and cast iron due to their extensive use in modern infrastructures, high-rise buildings, industrial plants, and oil & gas facilities. These materials are prone to losing their strength when subjected to high-temperature conditions; hence, fire protection is necessary from an engineering point of view to ensure the structural integrity and safety of the buildings. The stricter international implementation of fire safety regulations, aided by steel for green and modular construction, is contributing to increased demand for intumescent coatings.

"By end-use industry, the building & construction segment is projected to register the highest CAGR during the forecast period."

Within the intumescent coatings market, growth continues to be most rapid in the building & construction segment as fire safety gains importance in residential, commercial, and industrial buildings. With growing urbanization and an increasing number of high-rise and big infrastructure projects, the need for high-end passive fire protection technologies has been accentuated. Building codes, safety regulations, and insurance requirements act as driving factors for building acceptance, and renovation and retrofitting of self-security angles of older buildings also added to the market growth in this segment.

"By application techniques, the spray segment accounted for the largest segment."

The spray application method is estimated to account for the largest market share among intumescent coating application methods due to its ability to provide uniform thickness, smooth finish, and faster coverage over large surface areas. It ensures consistent film build, critical for the fire-protective performance of intumescent coatings on structural steel and industrial equipment. Spray application enhances morphology, penetrating even complex shapes better than any other coating method, which is found to be an effective application in construction, oil & gas, aerospace, and other industries. Its efficiency reduces labor time and overall application costs, which drives preference among contractors and end users. The development of airless spray equipment has further facilitated spraying as a more accurate method, resulting in less material wastage and easier handling of higher-viscosity formulations. These collective benefits made spray application the preferred and most economical choice for intumescent coatings, thus contributing to the dominance of the spray application technique.

"By region, the Middle East & Africa is projected to register the second-highest CAGR during the forecast period."

The Middle East & Africa emerges as one of the second-fastest regional segments in the intumescent coatings market, attributed to rapid infrastructure development and expansions of the oil & gas sector. Countries such as Saudi Arabia, UAE, and Qatar are investing in the development of high-rise buildings, commercial complexes, and industrial facilities, which has created excess demand for fire protection solutions. Other large-scale energy projects in the region, such as refineries, petrochemical plants, offshore platform constructions, etc., and many other projects, have propelled the use of intumescent coatings to protect structural steel in high-risk settings. Urban development and housing projects, especially in Africa, push further demand for low-cost fire-resistant building materials. Also, strict building codes and safety regulations, most strongly felt in countries of the GCC, are the ones forcing contractors to apply intumescent coatings to new projects. The market outlook is further enhanced by a rise in foreign direct investments in infrastructure and ongoing megaprojects, such as NEOM in Saudi Arabia and Expo City Dubai.

Profile break-up of primary participants for the report:

- By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

- By Designation: C Level: 20%, Director Level: 30%, and Others: 50%

- By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, Middle East & Africa: 20%, and South America: 10%

Companies Covered

Sherwin-Williams (US), PPG (US), AkzoNobel (Netherlands), Jotun (Norway), Hempel A/S (Denmark), RPM International, Inc. (US), Sika (Switzerland), Kansai Paint Co. Ltd. (Japan), Etex (Belgium), and Teknos (Finland are some of the key players in the intumescent coatings market.

Research Coverage

The market study covers the intumescent coatings market across various segments. It aims to estimate the market size and the growth potential of this market across different segments based on type, substrate, application techniques, end-use industry, and region. The study also includes an in-depth competitive analysis of key players in the market, their company profiles, key observations related to their products and business offerings, recent developments undertaken by them, and key growth strategies adopted by them to improve their position in the intumescent coatings market.

Key Benefits of Buying the Report

The report is expected to help the market leaders/new entrants in this market share the closest approximations of the revenue numbers of the overall intumescent coatings market and its segments and subsegments. This report is projected to help stakeholders understand the competitive landscape of the market, gain insights to improve the position of their businesses, and plan suitable go-to-market strategies. The report also aims to help stakeholders understand the pulse of the market and provide them with information on the key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (tighter fire-safety regulations & building codes), restraints (long, costly certification & testing cycles), opportunities (renovation & retrofitting of old buildings), and challenges (high competition and pricing pressure) influencing the growth of the intumescent coatings market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the intumescent coatings market

- Market Development: Comprehensive information about profitable markets - the report analyses the intumescent coatings market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the intumescent coatings market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of key players like Sherwin-Williams (US), PPG (US), AkzoNobel (Netherlands), Jotun (Norway), Hempel A/S (Denmark), RPM International, Inc. (US), Sika (Switzerland), Kansai Paint Co. Ltd. (Japan), Etex (Belgium), and Teknos (Finland) in the intumescent coatings market; also helps stakeholders understand the pulse of the intumescent coatings market and provides information on key market drivers, restraints, challenges, and opportunities

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.1.2 List of secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key primary participants

- 2.1.2.2 Key data from primary sources

- 2.1.2.3 Breakdown of interviews with experts

- 2.1.2.4 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 TOP-DOWN APPROACH

- 2.2.2 BOTTOM-UP APPROACH

- 2.3 BASE NUMBER CALCULATION

- 2.3.1 SUPPLY-SIDE APPROACH

- 2.4 GROWTH FORECAST

- 2.5 DATA TRIANGULATION

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 FACTOR ANALYSIS

- 2.8 RESEARCH LIMITATIONS

- 2.9 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INTUMESCENT COATINGS MARKET

- 4.2 INTUMESCENT COATINGS MARKET, BY TYPE

- 4.3 INTUMESCENT COATINGS MARKET, BY SUBSTRATE

- 4.4 INTUMESCENT COATINGS MARKET, BY END-USE INDUSTRY

- 4.5 INTUMESCENT COATINGS MARKET, BY APPLICATION TECHNIQUE

- 4.6 NORTH AMERICA: INTUMESCENT COATINGS MARKET, BY END-USE INDUSTRY AND COUNTRY

- 4.7 INTUMESCENT COATINGS MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Stringent fire-safety regulations and building codes

- 5.2.1.2 Rising investments in construction

- 5.2.1.3 Awareness and insurance incentives

- 5.2.1.4 Lightweight construction and esthetics

- 5.2.2 RESTRAINTS

- 5.2.2.1 Long, costly certification and testing cycles

- 5.2.2.2 High upfront costs vs. alternative fire protection solutions

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Renovation and retrofitting of old buildings

- 5.2.3.2 Growth and development in emerging markets

- 5.2.4 CHALLENGES

- 5.2.4.1 High competition and pricing pressure

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 REGULATORY LANDSCAPE

- 5.6.1 REGULATORY LANDSCAPE

- 5.6.1.1 Regulatory bodies, government agencies, and other organizations

- 5.6.2 KEY REGULATIONS

- 5.6.1 REGULATORY LANDSCAPE

- 5.7 PRICING ANALYSIS

- 5.7.1 PRICING ANALYSIS BASED ON REGION, 2021-2024

- 5.8 TRADE ANALYSIS

- 5.8.1 EXPORT SCENARIO (HS CODE 3209)

- 5.8.2 IMPORT SCENARIO (HS CODE 3209)

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Nano-enabled fillers and nanocomposites

- 5.9.1.2 Low-smoke/low-toxicity chemistries

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Abrasive blast cleaning

- 5.9.2.2 Hydroblasting

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 Battery thermal runaway mitigation coatings

- 5.9.1 KEY TECHNOLOGIES

- 5.10 PATENT ANALYSIS

- 5.10.1 INTRODUCTION

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 SASOL CHEMICALS USA -LAKE CHARLES CHEMICAL PROJECT (LCCP)

- 5.11.2 ULTIMATE SOLUTION FOR EXTREME HYDROCARBON FIRE SCENARIOS

- 5.11.3 WEMBLEY NATIONAL STADIUM LIMITED

- 5.12 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.12.2 BUYING CRITERIA

- 5.13 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.14 INVESTMENT AND FUNDING SCENARIO

- 5.15 IMPACT OF AI ON INTUMESCENT COATINGS MARKET

- 5.15.1 INTRODUCTION

- 5.15.2 IMPACT OF AI ON INTUMESCENT COATINGS MARKET

- 5.16 PORTER'S FIVE FORCES ANALYSIS

- 5.16.1 THREAT OF NEW ENTRANTS

- 5.16.2 THREAT OF SUBSTITUTES

- 5.16.3 BARGAINING POWER OF SUPPLIERS

- 5.16.4 BARGAINING POWER OF BUYERS

- 5.16.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.17 MACROECONOMIC ANALYSIS

- 5.17.1 INTRODUCTION

- 5.17.2 GDP TRENDS AND FORECASTS

- 5.18 IMPACT OF 2025 US TARIFF ON INTUMESCENT COATINGS MARKET

- 5.18.1 INTRODUCTION

- 5.18.2 KEY TARIFF RATES

- 5.18.3 PRICE IMPACT ANALYSIS

- 5.18.4 IMPACT ON COUNTRY/REGION

- 5.18.4.1 US

- 5.18.4.2 Asia Pacific

- 5.18.4.3 Europe

- 5.18.5 IMPACT ON END-USE INDUSTRIES

6 INTUMESCENT COATINGS MARKET, BY APPLICATION TECHNIQUE

- 6.1 INTRODUCTION

- 6.2 SPRAY

- 6.2.1 HIGH-BUILD THICKNESS, UNIFORM COVERAGE, AND RAPID PRODUCTIVITY TO DRIVE MARKET

- 6.3 BRUSH & ROLLER

- 6.3.1 MINIMIZING MATERIAL WASTAGE OR COATING DETAILED STRUCTURAL COMPONENTS TO FUEL DEMAND

7 INTUMESCENT COATINGS MARKET, BY SUBSTRATE

- 7.1 INTRODUCTION

- 7.2 STRUCTURAL STEEL & CAST IRON

- 7.2.1 RISING STEEL CONSUMPTION TO FUEL DEMAND

- 7.3 WOOD

- 7.3.1 INCREASING DEMAND FOR WOOD TO ENHANCE FIRE SAFETY AND SUSTAINABILITY

- 7.4 OTHER SUBSTRATES

8 INTUMESCENT COATINGS MARKET, BY TYPE

- 8.1 INTRODUCTION

- 8.2 THIN FILM INTUMESCENT COATINGS

- 8.2.1 RISING ADOPTION FOR EFFECTIVE FIRE PROTECTION AT LOW DRY FILM THICKNESSES TO BOOST MARKET

- 8.3 THICK FILM INTUMESCENT COATINGS

- 8.3.1 HIGH FIRE RESISTANCE FOR SUBSTRATES EXPOSED TO FIRE EXPOSURE TO DRIVE DEMAND

9 INTUMESCENT COATINGS MARKET, BY END-USE INDUSTRY

- 9.1 INTRODUCTION

- 9.2 BUILDING & CONSTRUCTION

- 9.2.1 SAFETY REGULATIONS AND DEMAND FOR RETROFITTING TO BOOST MARKET

- 9.3 INDUSTRIAL

- 9.3.1 DEMAND FOR COATINGS WITHSTANDING HYDROCARBON POOL FIRES AND HIGH-FLUX JET FIRES TO FUEL MARKET

- 9.4 AEROSPACE

- 9.4.1 RISING DEMAND FOR FIRE-RESISTANT AND LIGHTWEIGHT COATINGS TO PROPEL MARKET

- 9.5 OTHER END-USE INDUSTRIES

10 INTUMESCENT COATINGS MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 US

- 10.2.1.1 Growth in housing and aerospace sector to boost market

- 10.2.2 CANADA

- 10.2.2.1 Rising construction and aerospace activity to drive demand

- 10.2.3 MEXICO

- 10.2.3.1 Growth of construction and aerospace sectors to drive market

- 10.2.1 US

- 10.3 EUROPE

- 10.3.1 GERMANY

- 10.3.1.1 Energy-sector investments and renovation initiatives to fuel demand

- 10.3.2 FRANCE

- 10.3.2.1 Expansion of aeronautical sector to provide market opportunities

- 10.3.3 ITALY

- 10.3.3.1 Increasing renovation activities to drive market

- 10.3.4 UK

- 10.3.4.1 New housing development to propel market growth

- 10.3.5 SPAIN

- 10.3.5.1 Boosting affordable and social housing and investments in oil & gas sector to propel growth

- 10.3.6 REST OF EUROPE

- 10.3.1 GERMANY

- 10.4 ASIA PACIFIC

- 10.4.1 CHINA

- 10.4.1.1 Growth of construction, industrial, and aerospace sectors to drive demand

- 10.4.2 INDIA

- 10.4.2.1 Rapid expansion of construction, industrial, and aerospace sectors to accelerate demand

- 10.4.3 JAPAN

- 10.4.3.1 Urban redevelopment initiatives and industrial and aerospace sectors to propel market

- 10.4.4 AUSTRALIA

- 10.4.4.1 Rising demand from infrastructure, energy, and defense sectors to drive demand

- 10.4.5 REST OF ASIA PACIFIC

- 10.4.1 CHINA

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 GCC COUNTRIES

- 10.5.2 SAUDI ARABIA

- 10.5.2.1 Significant industrial expansion, infrastructure development, and growth of end-use industries to drive demand

- 10.5.3 UAE

- 10.5.3.1 Expansion of real estate sector and growth of oil & gas industry to drive demand

- 10.5.4 REST OF GCC COUNTRIES

- 10.5.5 SOUTH AFRICA

- 10.5.5.1 Government investments and energy projects to boost demand

- 10.5.6 REST OF MIDDLE EAST & AFRICA

- 10.6 SOUTH AMERICA

- 10.6.1 BRAZIL

- 10.6.1.1 Expanding automotive, agricultural, chemical, steel, metallurgy, mining, and petrochemical sectors to propel demand

- 10.6.2 ARGENTINA

- 10.6.2.1 Growing large-scale infrastructure investments and oil & gas sector to drive demand

- 10.6.3 REST OF SOUTH AMERICA

- 10.6.1 BRAZIL

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYERS STRATEGIES/RIGHT TO WIN

- 11.3 REVENUE ANALYSIS, 2020-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS

- 11.5.1 COMPANY VALUATION

- 11.6 FINANCIAL METRICS

- 11.7 BRAND/PRODUCT COMPARISON

- 11.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.8.1 STARS

- 11.8.2 EMERGING LEADERS

- 11.8.3 PERVASIVE PLAYERS

- 11.8.4 PARTICIPANTS

- 11.8.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.8.5.1 Company footprint

- 11.8.5.2 Region footprint

- 11.8.5.3 Type footprint

- 11.8.5.4 Substrate footprint

- 11.8.5.5 Application technique footprint

- 11.8.5.6 End-use industry footprint

- 11.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.9.1 PROGRESSIVE COMPANIES

- 11.9.2 RESPONSIVE COMPANIES

- 11.9.3 DYNAMIC COMPANIES

- 11.9.4 STARTING BLOCKS

- 11.9.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.9.5.1 Detailed list of key startups/SMEs

- 11.9.5.2 Competitive benchmarking of key startups/SMEs

- 11.10 COMPETITIVE SCENARIO

- 11.10.1 PRODUCT LAUNCHES

- 11.10.2 DEALS

- 11.10.3 EXPANSIONS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 SHERWIN-WILLIAMS

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Solutions/Services offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches

- 12.1.1.3.2 Deals

- 12.1.1.3.3 Expansions

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 PPG

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Solutions/Services offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches

- 12.1.2.4 MnM view

- 12.1.2.4.1 Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 AKZONOBEL

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Solutions/Services offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches

- 12.1.3.3.2 Deals

- 12.1.3.3.3 Expansions

- 12.1.3.3.4 Other developments

- 12.1.3.4 MnM view

- 12.1.3.4.1 Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 JOTUN

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Solutions/Services offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches

- 12.1.4.3.2 Expansions

- 12.1.4.3.3 Other developments

- 12.1.4.4 MnM view

- 12.1.4.4.1 Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 HEMPEL A/S

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Solutions/Services offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches

- 12.1.5.3.2 Deals

- 12.1.5.3.3 Expansions

- 12.1.5.3.4 Other developments

- 12.1.5.4 MnM view

- 12.1.5.4.1 Right to win

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses and competitive threats

- 12.1.6 RPM INTERNATIONAL INC.

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Solutions/Services offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Expansions

- 12.1.6.4 MnM view

- 12.1.7 SIKA

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Solutions/Services offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Deals

- 12.1.7.4 MnM view

- 12.1.8 KANSAI PAINT CO., LTD

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Solutions/Services offered

- 12.1.8.3 MnM view

- 12.1.9 ETEX

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Solutions/Services offered

- 12.1.9.3 MnM view

- 12.1.10 TEKNOS

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Solutions/Services offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Expansions

- 12.1.10.4 MnM view

- 12.1.1 SHERWIN-WILLIAMS

- 12.2 OTHER PLAYERS

- 12.2.1 ISOLATEK INTERNATIONAL

- 12.2.2 CONTEGO INTERNATIONAL INC.

- 12.2.3 ENVIROGRAF

- 12.2.4 FIREFREE COATINGS, INC.

- 12.2.5 RUDOLF HENSEL GMBH

- 12.2.6 NO-BURN, INC.

- 12.2.7 HILTI GROUP

- 12.2.8 UGAM CHEMICALS

- 12.2.9 SUNANDA SPECIALITY COATINGS PVT. LTD.

- 12.2.10 AITHON RICERCHE INTERNATIONAL

- 12.2.11 IRIS COATINGS

- 12.2.12 CHARCOAT PASSIVE FIRE PROTECTION INC.

- 12.2.13 CHUGOKU MARINE PAINTS, LTD.

- 12.2.14 VITON S.R.O.

- 12.2.15 QUANTUM CHEMICAL

13 ADJACENT & RELATED MARKET

- 13.1 INTRODUCTION

- 13.2 FIRE-RESISTANT COATINGS MARKET

- 13.2.1 MARKET DEFINITION

- 13.2.2 MARKET OVERVIEW

- 13.2.3 FIRE-RESISTANT COATINGS MARKET, BY TYPE

- 13.2.4 FIRE-RESISTANT COATINGS MARKET, BY APPLICATION

- 13.2.5 FIRE-RESISTANT MARKET, BY REGION

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS