|

시장보고서

상품코드

1856922

중기 텔레매틱스 시장 : 서비스별, 커넥티비티별, 판매채널별, 폼팩터별, 하드웨어별, 업계별, 지역별 - 예측(-2032년)Heavy Equipment Telematics Market by Industry, Solution, Hardware, Connectivity, Form Factor and Region - Global Forecast to 2032 |

||||||

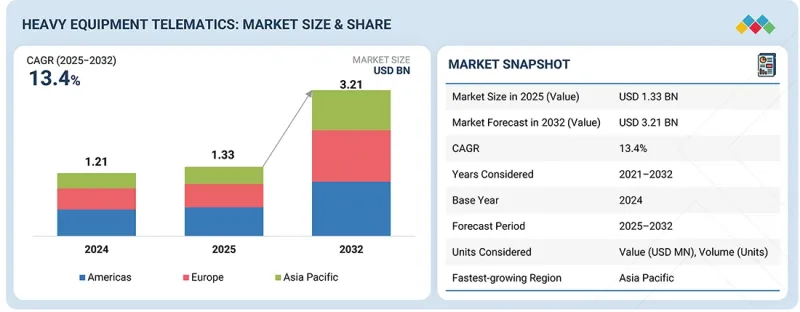

세계의 중기 텔레매틱스 시장 규모는 2025년 13억 3,000만 달러에서 2032년에는 32억 1,000만 달러로 성장하고, 예측 기간 중 연평균 복합 성장률(CAGR)은 13.4%를 보일 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2021-2032년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2032년 |

| 대상 유닛 | Unit 및 금액(100만 달러) |

| 부문별 | 서비스별, 커넥티비티별, 판매채널별, 폼팩터별, 하드웨어별, 업계별, 지역별 |

| 대상 지역 | 아시아태평양, 아메리카, 유럽 |

연료비 상승, 장비 고장, 장비 도난으로 인해 장비 제조업체/운영자는 차량에 텔레매틱스를 장착할 수밖에 없는 상황입니다. 텔레매틱스 서비스는 연비 관리, 유휴 시간 단축, 대형 오프로드 장비의 전반적인 성능 향상에 도움이 되고 있습니다.

건설, 광업 등의 산업에서 다운타임은 큰 재정적 손실과 직결되기 때문에 유지보수 및 진단은 오프하이웨이 장비에서 가장 빠르게 성장하는 텔레매틱스 서비스가 될 것으로 예측됩니다. 자산의 모니터링, 진단 및 유지보수는 연료 효율, 유압, 진동, 오일 품질, 적재량을 실시간으로 추적하는 센서 기반 데이터 입력을 통해 작업자가 고장의 징후를 조기에 파악할 수 있도록 지원합니다. 이 데이터를 텔레매틱스 제어 장치(TCU)를 통해 전송함으로써, 차량은 성능을 최적화하고 예기치 않은 고장을 줄이며, 기계의 수명을 연장할 수 있으며, 궁극적으로 긴급 수리 및 생산성 저하로 인한 비용을 크게 절감할 수 있습니다.

비용 절감뿐만 아니라 OEM은 애프터마켓 부품 및 서비스 수입을 강화하기 위해 진단을 통합하고 있으며, 렌탈업체와 계약업체는 예측적 통찰력이 차량 가동률을 극대화하기 위한 중요한 데이터 포인트라고 보고 있습니다. 텔레매틱스 도입이 확대됨에 따라 예지보전은 단순한 비용 회피 도구에서 효율성, 프로젝트 신뢰성, 장기적인 고객 충성도를 높이는 중요한 원동력으로 발전할 것으로 보입니다.

오프하이웨이 텔레매틱스 시장에는 신규 판매보다 기존 차량의 기여도가 더 클 것으로 예상되지만, 이는 주로 아직 고도의 연결성이 부족한 기계의 방대한 설치 기반에 기인합니다. OEM은 새로운 장비에 텔레매틱스를 통합하고 있지만, 수백만 대의 구형 장비가 여전히 현역으로 사용되고 있습니다. 상장사에 따르면 캐터필라는 약 150만 대, 고마쓰는 약 80만 대, JCB는 약 40만 대의 기계에 텔레매틱스 서비스를 탑재하고 있습니다. 나머지 기존 차량은 지속적인 인프라 및 채굴 프로젝트에 필수적이지만, 자산 추적, 가동률 통찰력, 예지보전 없이 운영되는 경우가 많습니다. 개조 키트 및 플러그 앤 플레이 장치를 포함한 애프터마켓 텔레매틱스 솔루션은 노후 차량에 최신 모니터링 및 분석을 도입하여 이 격차를 해소하고, 운영자가 전체 차량을 교체하지 않고도 자산의 수명을 연장하고, 다운타임을 줄이고, 효율성을 개선할 수 있도록 지원합니다. 효율성을 개선할 수 있도록 돕고 있습니다. 이는 특히 아시아태평양과 같은 고성장 지역에서 기존 차량에 텔레매틱스 도입의 큰 기회로 작용하고 있습니다.

유럽에서 중장비 텔레매틱스의 성장은 볼보건설기계(스웨덴), Liebherr(독일), JCB(영국), CNH Industrial(이탈리아)과 같은 주요 오프하이웨이 OEM의 강력한 존재감에 의해 주도되고 있습니다. 이들 중 상당수는 이미 텔레매틱스를 표준으로 장착하고 있습니다. 또한, Trackunit Corporation(덴마크), Actia Group(프랑스), Trimble(미국) 등 주요 텔레매틱스 업체들은 첨단 차량 모니터링, 예지보전, 안전 솔루션을 제공하기 위해 장비 제조업체와의 제휴를 확대하고 있습니다. 하고 있습니다. 2025년 5월, CNH Industrial은 Starlink(미국)와 자사 브랜드(Case IH, New Holland, Steyr)에 위성 연결을 제공하기로 합의했다고 발표했습니다.

또한, 유럽은 역사적으로 선진적인 디지털 서비스를 가장 먼저 도입해 왔으며, 계약업체와 차량 소유주들은 효율성, 안전성, 지속가능성을 향상시키는 기술을 가장 먼저 도입하고 있습니다. 이 지역의 건설, 광업, 농업 산업이 생산성 향상과 배출량 감소를 추진하면서 중장비에 대한 텔레매틱스 도입은 더욱 가속화될 것으로 예측됩니다. 이는 엄격한 EU 규제, 강력한 커넥티비티 인프라, 데이터 기반 차량 관리를 중시하는 고객 기반에 의해 더욱 강화되고 있습니다.

세계의 중장비 텔레매틱스 시장에 대해 조사했으며, 서비스별, 커넥티비티별, 판매 채널별, 폼팩터별, 하드웨어별, 산업별, 지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

- 서론

- 시장 역학

제6장 업계 동향

- 기술 분석

- 중기 텔레매틱스 시장 AI의 영향

- 사례 연구 분석

- 고객의 비즈니스에 영향을 미치는 동향과 혼란

- 가격 분석

- 생태계 분석

- 공급망 분석

- 특허 분석

- 규제 상황

- 2025-2026년 주요 컨퍼런스 및 이벤트

- 주요 이해관계자와 구입 기준

- 투자 및 자금조달 시나리오

- 텔레매틱스 시장 지역별 점유율과 주요 공급업체

- OEM별 텔레매틱스 제품

- 수익화와 비즈니스 모델

- 오프로드 OEM용 텔레매틱스 서비스 벤더 선정

제7장 중기 텔레매틱스 시장(서비스별)

- 서론

- 내비게이션과 자산 추적

- 기기/차량 유지관리 및 진단

- 연료 관리

- 플릿 퍼포먼스 보고서

- 플릿 안전

- 기타

- 업계 인사이트

제8장 중기 텔레매틱스 시장(커넥티비티별)

- 서론

- 위성

- 셀룰러

- 업계 인사이트

제9장 중기 텔레매틱스 시장(판매채널별)

- 서론

- 신규 판매

- 기존 플릿

- 업계 인사이트

제10장 중기 텔레매틱스 시장(폼팩터별)

- 서론

- 임베디드형

- 통합형

- 업계 인사이트

제11장 중기 텔레매틱스 시장(하드웨어별)

- 서론

- 텔레매틱스 제어 장치

- GPS 수신기

- 센서

- 업계 인사이트

제12장 중기 텔레매틱스 시장(업계별)

- 서론

- 건설

- 광업

- 농업

- 업계 인사이트

제13장 중기 텔레매틱스 시장(지역별)

- 서론

- 아시아태평양

- 거시경제 전망

- 중국

- 인도

- 일본

- 인도네시아

- 유럽

- 거시경제 전망

- 프랑스

- 독일

- 영국

- 이탈리아

- 스페인

- 미국 대륙

- 거시경제 전망

- 미국

- 캐나다

- 멕시코

- 브라질

- 업계 인사이트

제14장 경쟁 구도

- 개요

- 주요 시장 진출기업의 전략/강점, 2021년-2025년

- 시장 점유율 분석, 2024년

- 2020-2024년 주요 5개사의 매출 분석

- 기업 평가 매트릭스:주요 시장 진출기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 기업 평가

- 재무 지표

- 브랜드 및 제품 비교

- 경쟁 시나리오

제15장 기업 개요

- 주요 텔레매틱스 서비스 제공업체

- SAMSARA INC.

- CALAMP CORP.

- TRIMBLE INC.

- TOPCON CORPORATION

- ACTIA

- ORBCOMM

- TELETRAC NAVMAN US LTD

- GEOTAB INC.

- TRACKUNIT CORPORATION

- BRIDGESTONE MOBILITY SOLUTIONS B.V.

- 텔레매틱스 서비스를 제공하는 주요 오프로드 OEM

- CATERPILLAR

- KOMATSU LTD.

- DEERE & COMPANY

- J C BAMFORD EXCAVATORS LTD.

- LIEBHERR

- 스타트업/중소기업

- WENCO INTERNATIONAL MINING SYSTEMS LTD.

- DPL TELEMATICS

- ZONAR SYSTEMS, INC.

- MACHINEMAX

- THE MOREY CORPORATION

- LHP TELEMATICS, LLC.

- WIRELESS LINKS

- HEAVY CONSTRUCTION SYSTEMS SPECIALISTS LLC

- DSA DATEN-UND SYSTEMTECHNIK GMBH

- MIX TELEMATICS

제16장 시장 제안

제17장 부록

LSH 25.11.10The global heavy equipment telematics market is projected to grow from USD 1.33 billion in 2025 to USD 3.21 billion by 2032, at a CAGR of 13.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Volume (Units) and Value (USD Million) |

| Segments | By industry, by hardware, by form factor, by connectivity, by equipment category, by service, and by region |

| Regions covered | Asia Pacific, Americas, Europe |

Rising fuel costs, equipment failures, and equipment thefts are pushing equipment manufacturers/operators to equip their fleets with telematics. Telematics services help manage fuel efficiency, reduce idle time, and improve the overall performance of heavy off-highway equipment.

"Equipment maintenance and diagnostics are expected to be the fastest-growing service during the forecast period."

Maintenance and diagnostics are poised to become the fastest-growing telematics service in off-highway equipment, as downtime in industries such as construction and mining directly translates into significant financial losses. Asset monitoring, diagnostics, and maintenance enable operators to identify early signs of failure through sensor-driven data inputs that track fuel efficiency, hydraulics, vibration, oil quality, and payload in real-time. By transmitting this data through the telematics control unit (TCU), fleets can optimize performance, reduce unexpected breakdowns, and extend machine life, ultimately saving operators substantial costs on emergency repairs and lost productivity.

Beyond cost savings, OEMs are embedding diagnostics to strengthen aftermarket parts and service revenues, while rental firms and contractors see predictive insights as crucial data points to maximize fleet utilization. As telematics adoption grows, predictive maintenance will evolve from a simple cost-avoidance tool into a key driver of efficiency, project reliability, and long-term customer loyalty.

"Telematics service revenues from existing fleets would be the largest equipment category during the forecast period."

Existing fleets are expected to contribute more to the off-highway telematics market than new sales, primarily due to the vast installed base of machines that still lack advanced connectivity. While OEMs are embedding telematics in new equipment, millions of older units are still in active service. According to company publications, Caterpillar has equipped its telematics services in approximately 1.5 million units, while Komatsu has equipped its services in 0.8 million machines, and JCB has equipped its services in 0.4 million machines. The remaining existing fleet remains critical for ongoing infrastructure and mining projects, but often operates without asset tracking, utilization insights, or predictive maintenance. Aftermarket telematics solutions, including retrofit kits and plug-and-play devices, are bridging this gap by bringing modern monitoring and analytics to older fleets, helping operators extend asset life, reduce downtime, and improve efficiency without the need to replace entire fleets. This presents existing fleets as the larger opportunity for telematics adoption, particularly in high-growth regions such as the Asia-Pacific.

"Europe is projected to be one of the major telematics markets for heavy off-highway equipment."

The growth of heavy equipment telematics in Europe is being driven by a strong presence of leading off-highway OEMs such as Volvo Construction Equipment (Sweden), Liebherr (Germany), JCB (UK), and CNH Industrial (Italy), many of which already integrate telematics into their machines as standard. Alongside them, key telematics providers such as Trackunit Corporation (Denmark), Actia Group (France), and Trimble (US) are expanding their partnerships with equipment manufacturers to deliver advanced fleet monitoring, predictive maintenance, and safety solutions. In May 2025, CNH Industrial announced an agreement with Starlink (US) to offer satellite connectivity for its brands (Case IH, New Holland, Steyr), to enhance connectivity in remote rural areas, supporting precision agriculture and connected fleet services.

Moreover, Europe has historically been an early adopter of advanced digital services, with contractors and fleet owners quickly embracing technologies that improve efficiency, safety, and sustainability. As the construction, mining, and agricultural industries in the region push for greater productivity and lower emissions, the adoption of telematics in heavy equipment is expected to continue accelerating. This will be further supported by strict EU regulations, strong connectivity infrastructure, and a customer base that values data-driven fleet management.

The breakdown of the profile of primary participants in the heavy equipment telematics market is as follows:

- By Company Type: OEMs - 60%, Telematics Providers - 40%

- By Designation: C Level - 60%, Director-level - 30%, Others - 10%

- By Region: North America- 20%, Europe - 30%, Asia Pacific - 50%

Prominent companies include Samsara Inc. (US), Trimble Inc. (US), Geotab Inc. (US), ORBCOMM (US), and CalAmp Corp. (US), which are the leading providers of telematics services for heavy off-highway equipment in the global market.

Research Coverage:

The study segments the heavy equipment telematics market. It forecasts the market size based on industry (construction, mining, agriculture), hardware (telematics control unit, GPS receivers, sensors), connectivity (cellular, satellite), form factor (embedded, integrated), service (fuel management, fleet performance reporting, navigation and asset tracking, equipment/fleet maintenance and diagnostics, fleet safety and others), equipment category (new sales, existing fleet), and region (Asia Pacific, Americas, and Europe). This report also covers the competitive analysis of upcoming startups/SMEs in the heavy equipment telematics market ecosystem.

Reasons to buy this report:

The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall telematics market for heavy off-highway equipment and its subsegments. The report includes a comprehensive market share analysis, supply chain analysis, and a competitive landscape. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (enhanced equipment monitoring, technological advancements), restraints (high initial and recurring investments), opportunities (expansion into emerging markets, increase in mechanized farming and mining operations), and challenges (connectivity issues in remote areas) influencing the growth of the heavy equipment telematics market

- Product/service development/innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the heavy equipment telematics market

- Market Development: Comprehensive information about lucrative markets (the report analyzes the heavy equipment telematics market across varied regions and business segments)

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the heavy equipment telematics market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the heavy equipment telematics market, such as Samsara Inc. (US), Trimble Inc. (US), Geotab Inc. (US), ORBCOMM (US), and CalAmp Corp. (US).

The report also helps stakeholders understand the pulse of the heavy equipment telematics market by providing them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key secondary sources for equipment sales

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary participants

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 FACTOR ANALYSIS

- 2.5 RESEARCH ASSUMPTIONS AND RISK ASSESSMENT

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HEAVY EQUIPMENT TELEMATICS MARKET

- 4.2 HEAVY EQUIPMENT TELEMATICS MARKET, BY SERVICE

- 4.3 HEAVY EQUIPMENT TELEMATICS MARKET, BY FORM FACTOR

- 4.4 HEAVY EQUIPMENT TELEMATICS MARKET, BY INDUSTRY

- 4.5 HEAVY EQUIPMENT TELEMATICS MARKET, BY SALES CHANNEL

- 4.6 HEAVY EQUIPMENT TELEMATICS MARKET, BY CONNECTIVITY

- 4.7 HEAVY EQUIPMENT TELEMATICS CELLULAR MARKET, BY TYPE

- 4.8 HEAVY EQUIPMENT TELEMATICS MARKET, BY HARDWARE

- 4.9 HEAVY EQUIPMENT TELEMATICS MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Need for enhanced equipment monitoring

- 5.2.1.1.1 Real-time monitoring

- 5.2.1.1.2 Integration of IoT sensors

- 5.2.1.1.3 Geofencing

- 5.2.1.2 Technological advancements

- 5.2.1.2.1 Integration of 5G connectivity for faster data transmission

- 5.2.1.2.2 Adoption of AI & machine learning for predictive analytics

- 5.2.1.2.3 Development of cloud-based platforms for scalable solutions

- 5.2.1.1 Need for enhanced equipment monitoring

- 5.2.2 RESTRAINTS

- 5.2.2.1 Need for high initial investment

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Expansion into emerging markets

- 5.2.3.2 Increasing adoption of mechanized farming and mining operations

- 5.2.4 CHALLENGES

- 5.2.4.1 Connectivity issues in remote areas

- 5.2.1 DRIVERS

6 INDUSTRY TRENDS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Cloud platforms and APIs

- 6.1.1.2 5G connectivity in off-highway equipment

- 6.1.1.3 Autonomy facilitated by telematics in off-highway equipment

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Fleet analytics for off-highway equipment

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Geofencing for off-highway equipment

- 6.1.3.2 Advanced sensors

- 6.1.1 KEY TECHNOLOGIES

- 6.2 IMPACT OF AI ON HEAVY EQUIPMENT TELEMATICS MARKET

- 6.3 CASE STUDY ANALYSIS

- 6.3.1 TEREX MATERIALS PROCESSING ADOPTED CLOUD-BASED PLATFORM CUSTOMIZED BY ORBCOMM TO PROVIDE REAL-TIME DATA ANALYTICS

- 6.3.2 KUCHERA PARTNERED WITH ORBCOMM TO IMPLEMENT SOLUTION COMBINING SATELLITE AND CELLULAR CONNECTIVITY

- 6.3.3 TELETRAC NAVMAN IMPLEMENTED ADVANCED TELEMATICS SOLUTIONS TO PROVIDE REAL-TIME DATA ON EQUIPMENT LOCATION, USAGE, AND HEALTH

- 6.3.4 CONSTRUCTION FLEET IN NORTH AMERICA INSTALLED TELEMATICS DEVICES TO MONITOR IDLE TIMES AND MACHINE UTILIZATION

- 6.4 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.5 PRICING ANALYSIS

- 6.5.1 AVERAGE SELLING PRICE OF HEAVY EQUIPMENT TELEMATICS, BY PACKAGE TYPE

- 6.5.2 AVERAGE SELLING PRICE, BY REGION

- 6.6 ECOSYSTEM ANALYSIS

- 6.7 SUPPLY CHAIN ANALYSIS

- 6.8 PATENT ANALYSIS

- 6.9 REGULATORY LANDSCAPE

- 6.10 KEY CONFERENCES & EVENTS, 2025-2026

- 6.11 KEY STAKEHOLDERS & BUYING CRITERIA

- 6.11.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.11.2 BUYING CRITERIA

- 6.12 INVESTMENT & FUNDING SCENARIO

- 6.13 REGIONAL SHARE OF TELEMATICS MARKET AND KEY SUPPLIERS

- 6.14 TELEMATICS OFFERINGS BY OEMS

- 6.14.1 TELEMATICS OFFERINGS BY CONSTRUCTION AND MINING EQUIPMENT OEMS

- 6.15 MONETIZATION AND BUSINESS MODELS

- 6.15.1 SUBSCRIPTION MODEL

- 6.15.2 USAGE-BASED CHARGES

- 6.15.3 PREVENTIVE MAINTENANCE UPDATES

- 6.15.4 OEM & DEALER BUNDLING

- 6.15.5 HARDWARE FOR INTEGRATED SYSTEM SALES

- 6.16 VENDOR SHORTLISTING FOR TELEMATICS SERVICES FOR OFF-HIGHWAY OEMS

7 HEAVY EQUIPMENT TELEMATICS MARKET, BY SERVICE

- 7.1 INTRODUCTION

- 7.2 NAVIGATION & ASSET TRACKING

- 7.2.1 NEED FOR REAL-TIME LOCATION SHARING AND EQUIPMENT TRACKING TO DRIVE GROWTH

- 7.3 EQUIPMENT/FLEET MAINTENANCE & DIAGNOSTICS

- 7.3.1 FOCUS ON PREVENTIVE MAINTENANCE AND EQUIPMENT HEALTH MONITORING TO DRIVE GROWTH

- 7.4 FUEL MANAGEMENT

- 7.4.1 INCREASING DEMAND FOR HIGH ACCURACY TO DRIVE GROWTH

- 7.5 FLEET PERFORMANCE REPORTING

- 7.5.1 INCREASING DEMAND FOR HIGH ACCURACY THROUGH PERFORMANCE REPORTING TO DRIVE GROWTH

- 7.6 FLEET SAFETY

- 7.6.1 INCREASING DEMAND FOR SAFETY AT CONSTRUCTION AND MINING SITES TO DRIVE GROWTH

- 7.7 OTHERS

- 7.8 INDUSTRY INSIGHTS

8 HEAVY EQUIPMENT TELEMATICS MARKET, BY CONNECTIVITY

- 8.1 INTRODUCTION

- 8.2 SATELLITE

- 8.2.1 INCREASED ADOPTION OF TELEMATICS IN MINING EQUIPMENT TO DRIVE GROWTH

- 8.3 CELLULAR

- 8.3.1 NEED FOR ADOPTION OF TELEMATICS IN CONSTRUCTION AND AGRICULTURE INDUSTRIES TO DRIVE GROWTH

- 8.3.2 3G/4G

- 8.3.3 5G

- 8.4 INDUSTRY INSIGHTS

9 HEAVY EQUIPMENT TELEMATICS MARKET, BY SALES CHANNEL

- 9.1 INTRODUCTION

- 9.2 NEW SALES

- 9.2.1 GROWTH IN OE-OFFERED FACTORY INSTALLATIONS OF TELEMATICS SYSTEMS TO DRIVE GROWTH

- 9.3 EXISTING FLEET

- 9.3.1 AFTERMARKET POTENTIAL IN LEGACY EQUIPMENT TO FUEL GROWTH

- 9.4 INDUSTRY INSIGHTS

10 HEAVY EQUIPMENT TELEMATICS MARKET, BY FORM FACTOR

- 10.1 INTRODUCTION

- 10.2 EMBEDDED

- 10.2.1 OEMS, INSURANCE PROVIDERS, AND FINANCIAL INSTITUTIONS ARE MAKING TELEMATICS MANDATORY IN HEAVY EQUIPMENT

- 10.3 INTEGRATED

- 10.3.1 OPPORTUNITIES IN AFTERMARKET FOR OLD EQUIPMENT TO DRIVE GROWTH

- 10.4 INDUSTRY INSIGHTS

11 HEAVY EQUIPMENT TELEMATICS MARKET, BY HARDWARE

- 11.1 INTRODUCTION

- 11.2 TELEMATICS CONTROL UNIT

- 11.2.1 UPCOMING DEVELOPMENTS IN CONNECTIVITY AND CYBERSECURITY FEATURES TO DRIVE GROWTH

- 11.3 GPS RECEIVER

- 11.3.1 ADVANCEMENTS IN POSITIONING ACCURACY AND CONNECTIVITY TO DRIVE GROWTH

- 11.4 SENSORS

- 11.4.1 INCREASING DEMAND FOR HIGH ACCURACY TO DRIVE GROWTH

- 11.5 INDUSTRY INSIGHTS

12 HEAVY EQUIPMENT TELEMATICS MARKET, BY INDUSTRY

- 12.1 INTRODUCTION

- 12.2 CONSTRUCTION

- 12.2.1 DEMAND FOR SMART AND CONNECTED ASSETS TO DRIVE GROWTH

- 12.3 MINING

- 12.3.1 DEMAND FOR PRECISION MINING AND FLEET ANALYTICS TO DRIVE GROWTH

- 12.4 AGRICULTURE

- 12.4.1 DEMAND FOR PRECISION FARMING AND IMPROVED YIELDS TO DRIVE GROWTH

- 12.5 INDUSTRY INSIGHTS

13 HEAVY EQUIPMENT TELEMATICS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 MACROECONOMIC OUTLOOK

- 13.2.2 CHINA

- 13.2.2.1 High demand for excavators and earthmoving machines to drive growth

- 13.2.3 INDIA

- 13.2.3.1 Telematics offerings in excavators, backhoe loaders, and tractors to drive growth

- 13.2.4 JAPAN

- 13.2.4.1 Rapid technological advancements in heavy equipment telematics to drive growth

- 13.2.5 INDONESIA

- 13.2.5.1 Increased adoption of telematics in construction equipment to drive growth

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK

- 13.3.2 FRANCE

- 13.3.2.1 Adoption of OE-fitted telematics in construction and mining equipment to drive growth

- 13.3.3 GERMANY

- 13.3.3.1 Increasing demand for fleet/equipment tracking and presence of key OEMs to drive growth

- 13.3.4 UK

- 13.3.4.1 Presence of key OEMs and demand for factory fitment of telematics to drive growth

- 13.3.5 ITALY

- 13.3.5.1 Presence of key OEMs and demand for improving equipment and fleet efficiency to drive growth

- 13.3.6 SPAIN

- 13.3.6.1 Adoption of telematics by construction contractors and farmers to drive growth

- 13.4 AMERICAS

- 13.4.1 MACROECONOMIC OUTLOOK

- 13.4.2 US

- 13.4.2.1 Increasing demand for connected machines to drive growth

- 13.4.3 CANADA

- 13.4.3.1 Adoption of telematics in heavy equipment to drive growth

- 13.4.4 MEXICO

- 13.4.4.1 Increasing adoption of telematics in construction and mining sectors to drive growth

- 13.4.5 BRAZIL

- 13.4.5.1 Adoption of telematics in agricultural equipment for precision farming to drive growth

- 13.5 INDUSTRY INSIGHTS

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 14.3 MARKET SHARE ANALYSIS, 2024

- 14.4 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2020-2024

- 14.5 COMPANY EVALUATION MATRIX, 2024

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.5.5 COMPANY FOOTPRINT: HEAVY EQUIPMENT TELEMATICS PROVIDERS, 2024

- 14.5.5.1 Company footprint

- 14.5.5.2 Region footprint

- 14.5.5.3 Industry footprint

- 14.5.5.4 Connectivity footprint

- 14.5.5.5 Form factor footprint

- 14.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 RESPONSIVE COMPANIES

- 14.6.3 DYNAMIC COMPANIES

- 14.6.4 STARTING BLOCKS

- 14.6.5 COMPETITIVE BENCHMARKING

- 14.6.5.1 List of startups/SMEs

- 14.6.5.2 Competitive benchmarking of startups/SMEs

- 14.7 COMPANY VALUATION

- 14.8 FINANCIAL METRICS

- 14.9 BRAND/PRODUCT COMPARISON

- 14.10 COMPETITIVE SCENARIO

- 14.10.1 PRODUCT LAUNCHES & ENHANCEMENTS

- 14.10.2 DEALS

- 14.10.3 EXPANSION

- 14.10.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY TELEMATICS SERVICE PROVIDERS

- 15.1.1 SAMSARA INC.

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches & enhancements

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 CALAMP CORP.

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches & enhancements

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Expansion

- 15.1.2.3.4 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 TRIMBLE INC.

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches & enhancements

- 15.1.3.3.2 Deals

- 15.1.3.3.3 Expansion

- 15.1.3.3.4 Other developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 TOPCON CORPORATION

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Products launches & enhancements

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansion

- 15.1.4.3.4 Other developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 ACTIA

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Products launches & enhancements

- 15.1.5.3.2 Deals

- 15.1.6 ORBCOMM

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches & enhancements

- 15.1.6.3.2 Deals

- 15.1.6.3.3 Other developments

- 15.1.7 TELETRAC NAVMAN US LTD

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches & enhancements

- 15.1.8 GEOTAB INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches & enhancements

- 15.1.8.3.2 Deals

- 15.1.9 TRACKUNIT CORPORATION

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions offered

- 15.1.10 BRIDGESTONE MOBILITY SOLUTIONS B.V.

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions offered

- 15.1.1 SAMSARA INC.

- 15.2 KEY OFF-HIGHWAY OEMS OFFERING TELEMATICS SERVICES

- 15.2.1 CATERPILLAR

- 15.2.1.1 Business overview

- 15.2.1.2 Products/Solutions offered

- 15.2.1.3 Recent developments

- 15.2.1.3.1 Products launches & enhancements

- 15.2.1.3.2 Deals

- 15.2.1.4 MnM view

- 15.2.1.4.1 Right to win

- 15.2.1.4.2 Strategic choices

- 15.2.1.4.3 Weaknesses & competitive threats

- 15.2.2 KOMATSU LTD.

- 15.2.2.1 Business overview

- 15.2.2.2 Products/Solutions offered

- 15.2.2.3 Recent developments

- 15.2.2.3.1 Product launches & enhancements

- 15.2.2.3.2 Deals

- 15.2.2.4 MnM view

- 15.2.2.4.1 Right to win

- 15.2.2.4.2 Strategic choices

- 15.2.2.4.3 Weaknesses & competitive threats

- 15.2.3 DEERE & COMPANY

- 15.2.3.1 Business overview

- 15.2.3.2 Products/Solutions offered

- 15.2.3.3 Recent developments

- 15.2.3.3.1 Product launches & enhancements

- 15.2.4 J C BAMFORD EXCAVATORS LTD.

- 15.2.4.1 Business overview

- 15.2.4.2 Products/Solutions offered

- 15.2.4.3 Recent developments

- 15.2.4.3.1 Product launches & enhancements

- 15.2.4.3.2 Deals

- 15.2.5 LIEBHERR

- 15.2.5.1 Business overview

- 15.2.5.2 Products/Solutions offered

- 15.2.5.3 Recent developments

- 15.2.5.3.1 Product launches & enhancements

- 15.2.1 CATERPILLAR

- 15.3 STARTUPS/SMES

- 15.3.1 WENCO INTERNATIONAL MINING SYSTEMS LTD.

- 15.3.2 DPL TELEMATICS

- 15.3.3 ZONAR SYSTEMS, INC.

- 15.3.4 MACHINEMAX

- 15.3.5 THE MOREY CORPORATION

- 15.3.6 LHP TELEMATICS, LLC.

- 15.3.7 WIRELESS LINKS

- 15.3.8 HEAVY CONSTRUCTION SYSTEMS SPECIALISTS LLC

- 15.3.9 DSA DATEN- UND SYSTEMTECHNIK GMBH

- 15.3.10 MIX TELEMATICS

16 RECOMMENDATIONS BY MARKETSANDMARKETS

- 16.1 AMERICAS TO BE MAJOR MARKET FOR HEAVY EQUIPMENT TELEMATICS

- 16.2 CONSTRUCTION AND AGRICULTURE EQUIPMENT TO BE KEY FOCUS AREA FOR TELEMATICS SERVICE PROVIDERS

- 16.3 EQUIPMENT/FLEET MAINTENANCE AND DIAGNOSTICS TO BE KEY FOCUS AREAS FOR TELEMATICS SERVICE PROVIDERS AND OFF-HIGHWAY OEMS

- 16.4 CONCLUSION

17 APPENDIX

- 17.1 KEY INDUSTRY INSIGHTS

- 17.2 DISCUSSION GUIDE

- 17.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.4 CUSTOMIZATION OPTIONS

- 17.5 RELATED REPORTS

- 17.6 AUTHOR DETAILS