|

시장보고서

상품코드

1861050

데이터센터용 UPS 시장 : 컨피규레이션 유형별, 디자인 유형별, 단계 유형별, 배터리 유형별, 용량별, 폼팩터별, 데이터센터 유형별, 지역별 - 예측(-2030년)Data Center UPS Market by Capacity, Phase Type, Configuration Type, Design Type - Global Forecast to 2030 |

||||||

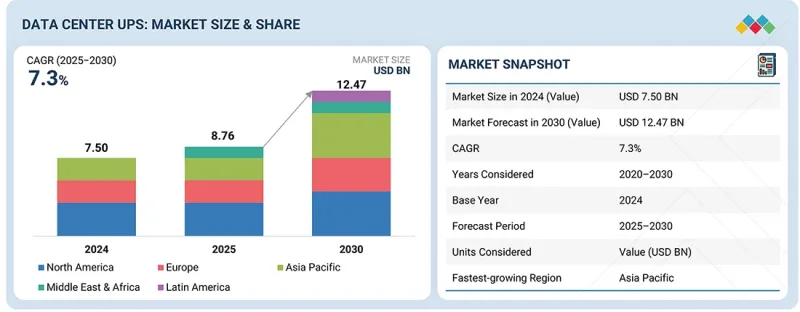

데이터센터용 UPS 시장 규모는 2025년 87억 6,000만 달러에서 2030년에는 124억 7,000만 달러로 성장하여 CAGR은 7.3%를 보일 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2020-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 100만 달러 |

| 부문 | 컨피규레이션 유형별, 디자인 유형별, 단계 유형별, 배터리 유형별, 용량별, 폼팩터별, 데이터센터 유형별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

하이퍼스케일 AI 워크로드의 전력 수요, 랙 전력 밀도 증가, 고부하 환경에서 무중단 운영을 지원할 수 있는 고효율 UPS 시스템에 대한 요구가 증가함에 따라 시장이 빠르게 성장하고 있습니다. AI 및 클라우드 기반 용도가 랙당 전력 소비를 증가시키는 가운데, 운영자는 확장 가능하고 모듈화되며 에너지에 최적화된 UPS 아키텍처를 채택하여 성능을 개선하고 총 소유 비용을 절감하고 있습니다. 리튬 이온 배터리, 그리드 인터랙티브 설계, 통합 배터리 에너지 저장 솔루션으로의 전환은 더 높은 에너지 효율과 우수한 부하 관리를 가능하게 하여 시스템의 신뢰성과 지속가능성을 향상시키고 있습니다. 이러한 발전으로 데이터센터는 기업의 에너지 최적화 목표에 맞추어 운영하면서 전력의 연속성을 유지할 수 있습니다.

그러나 수요가 많은 지역의 데이터센터 확장을 제한하는 계통 전력 이용 제약, 공급망 혼란과 제조 병목현상으로 인한 장비 및 부품 리드타임의 장기화로 인해 시장 성장이 억제되고 있습니다. 이러한 요인으로 인해 구축 일정이 지연되고, 대규모 증설을 관리하는 하이퍼스케일 및 코로케이션 사업자에게는 비용 압박이 가중될 수 있습니다. 이러한 제약에도 불구하고 전력 효율성, 운영 탄력성 및 지속가능성에 대한 지속적인 관심은 세계 데이터센터 네트워크 전반에 걸쳐 안정적이고 확장 가능한 전력 인프라를 보장하는 데 있어 고급 UPS 시스템의 중요한 역할을 강화하고 있습니다.

1,001-2,000kVA의 용량 범위는 방대한 컴퓨팅 포드, 스토리지 팜, AI 워크로드를 보호하기 위해 강력한 대용량 UPS 시스템이 필요한 대규모 및 하이퍼스케일 데이터센터에 적합합니다. 이 UPS 유닛은 중복성을 통합하고 병렬 스트링 수를 최소화하여 바닥 면적을 줄이면서 높은 효율성과 열 성능을 달성합니다. 그 가치는 원활한 확장을 가능하게 하고, 배전의 복잡성을 줄이며, 미션 크리티컬한 환경에서 고밀도 운영을 지원하는 데 있습니다. 2025년 8월, 화웨이는 1,000-2,000kVA 대역의 확장 가능한 구성을 제공하는 SUS2000G 모듈형 UPS 플랫폼을 출시하여 중국의 클라우드 데이터센터와 코로케이션 캠퍼스를 지원합니다. 또한 2024년 3월, ABB는 북유럽 하이퍼스케일 시설의 전력 인프라 업그레이드의 일환으로 여러 개의 1.5MVA(1,500kVA) UPS 시스템을 납품했으며, 전체 전력 모듈에 고도의 병렬화 및 동기화 기능을 통합했습니다. 이러한 도입은 이 대용량 부문 수요 증가를 뒷받침하는 것입니다. 공급업체와 솔루션 제공업체는 모듈성, 고효율 변환, 통합 배터리 관리, 고전압 플랜트 시스템과의 호환성을 우선시해야 합니다. 클라우드 사업자, 하이퍼스케일러, 구축 파트너와 협력하여 사전 구축된 전원 모듈과 성능 보증을 제공함으로써 1,001-2,000kVA 부문에서 조기 보급 및 장기 계약이 가능합니다.

랙마운트 UPS 시스템은 공간 최적화, 높은 전력 밀도, 모듈식 배치가 설계 결정의 원동력이 되는 최신 데이터센터에서 점점 더 중요해지고 있습니다. IT 랙에 직접 설치되는 이 시스템은 일반적으로 최대 50kVA의 부하를 지원하며, 중요한 장비에 효율적이고 국부적인 전원 보호를 제공하도록 설계되었습니다. 컴팩트한 디자인으로 케이블 배선의 복잡성을 줄이고 공기 흐름 관리를 개선하여 제한된 설치 공간에서 운영되는 엣지, 모듈형, 엔터프라이즈형 데이터센터에 적합합니다. 랙마운트 UPS 시스템은 공급업체와 솔루션 제공업체에게 디지털 인프라와 원활하게 통합되고, 원격 관리, 예지보전, 확장 가능한 용량 확장이 가능한 지능적이고 에너지 효율적인 백업 솔루션을 제공할 수 있는 기회를 제공합니다. 이러한 시스템은 분산 복원력과 운영 효율성에 초점을 맞춘 진화하는 데이터센터 아키텍처와 밀접하게 일치합니다. 최근 업계 협업은 이러한 모멘텀을 강조하고 있습니다. 2025년 6월, Eaton은 싱가포르 전역에 단상 랙마운트 UPS 시스템의 유통을 확대하기 위해 Fengsheng Electric과 제휴하여 모듈식 및 엣지 배포에 대한 수요 증가에 대응했습니다. 마찬가지로 Vertiv는 2025년 7월 Great Lakes Data Racks &Cabinets를 인수하여 랙 및 전원 공급 장치 통합 솔루션 포트폴리오를 강화했습니다. 이러한 전략적 움직임은 전원 공급 장치와 인클로저 생태계의 수렴을 강조하는 것입니다. 향후 업체들은 리튬 이온 배터리, 지능형 모니터링, 핫스왑 지원 설계를 갖춘 AI 통합 랙마운트형 UPS 플랫폼 개발에 집중하여 공간 제약이 있는 성능 중심의 데이터센터에서 시장 점유율을 확보해야 합니다.

북미는 대규모 하이퍼스케일 개발, 고급 전원 관리 인프라, 모듈형 고효율 UPS 시스템의 강력한 채택으로 시장을 선도할 것으로 추정됩니다. 아시아태평양은 가속화되는 클라우드 확장, 급속한 산업 디지털화, 신뢰성 있고 에너지에 강한 데이터센터 전원 인프라에 대한 정부 지원 투자로 인해 높은 성장률을 보일 것으로 예측됩니다.

북미는 하이퍼스케일 성장 가속화, AI 기반 워크로드, 고도의 에너지 효율적인 백업 시스템을 요구하는 랙 전력 밀도 증가 등에 힘입어 데이터센터용 UPS 시장을 주도하는 지역으로 부상하고 있습니다. 이 지역의 데이터센터 사업자들은 확장성을 강화하고, 에너지 손실을 줄이고, 배터리 에너지 저장 시스템과 통합하여 더 높은 복원력과 그리드 안정성을 보장하기 위해 모듈형 및 리튬 이온 UPS 아키텍처를 빠르게 채택하고 있습니다. 미국에서는 버지니아 북부, 댈러스, 피닉스 등 주요 거점에서 전력 제약이 증가하고 있으며, AI 및 고밀도 컴퓨팅 클러스터를 지원할 수 있는 차세대 UPS 기술에 대한 대규모 투자를 촉진하고 있습니다. 캐나다의 청정 에너지 정책과 온타리오, 퀘벡 등의 재생에너지를 통한 데이터센터 확대는 탈탄소화 목표에 부합하는 지속 가능한 UPS의 전개에 큰 기회를 제공합니다. 주요 업체들은 리드 타임 단축 압력에 대응하고 새로운 에너지 효율 및 사이버 보안 표준을 충족하기 위해 국내 제조 능력과 공급 네트워크를 강화하고 있습니다. 북미 UPS 인프라는 지역 유틸리티 및 규제 당국이 전력망의 즉각적인 반응성과 탄소 규제 준수를 강화하는 가운데, 전통적인 백업 시스템에서 에너지 사용을 최적화하고 가동 시간을 향상시키는 지능형 고성능 자산으로 진화하고 있으며, 탄력적이고 지속 가능한 데이터센터 전력 관리의 세계 리더로 자리매김하고 있습니다. 데이터센터 전원 관리 분야의 세계 리더로서의 입지를 강화해 나가고 있습니다.

세계의 데이터센터용 UPS 시장에 대해 조사했으며, 구성 유형별, 디자인 유형별, 위상 유형별, 배터리 유형별, 용량별, 폼팩터별, 데이터센터 유형별, 지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

- 서론

- 시장 역학

- 미충족 요구와 공백

- 상호 접속된 시장과 분야 횡단적인 기회

- 새로운 비즈니스 모델과 에코시스템 변화

- Tier1/2/3 기업의 전략적 움직임

제5장 업계 동향

- Porter의 Five Forces 분석

- 거시경제 지표

- 공급망 분석

- 생태계 분석

- 가격 분석

- 무역 분석

- 2025-2026년 주요 컨퍼런스 및 이벤트

- 고객의 비즈니스에 영향을 미치는 동향과 혼란

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 2025년 미국 관세의 영향 - 데이터센터용 UPS 시장

제6장 기술, 특허, 디지털, AI 도입별 전략적 파괴

- 주요 신기술

- 보완 기술

- 인접 기술

- 기술/제품 로드맵

- 특허 분석

- 향후 응용

- AI/생성형 AI가 데이터센터용 UPS 시장에 미치는 영향

- 성공 사례와 실세계에의 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

- 의사결정 프로세스

- 구입자 이해관계자와 구입 평가 기준

- 채택 장벽과 내부 과제

- 다양한 최종사용자 산업의 미충족 요구

- 시장 수익성

제9장 데이터센터용 UPS 시장(컨피규레이션 유형별)

- 서론

- 온라인 더블 전환

- 라인 인터랙티브

- 오프라인/스탠바이/배터리 백업

제10장 데이터센터용 UPS 시장(디자인 유형별)

- 서론

- 모듈러 UPS

- 기존(모놀리식) UPS

제11장 데이터센터용 UPS 시장(단계 유형별)

- 서론

- 단상

- 삼상

제12장 데이터센터용 UPS 시장(배터리 유형별)

- 서론

- 납축전지

- 리튬 이온 배터리

- 니켈 카드뮴 전지

제13장 데이터센터용 UPS 시장(용량별)

- 서론

- 50KVA 이하

- 51-200KVA

- 201-500KVA

- 501-1,000KVA

- 1,001-2,000KVA

- 2,000KVA 이상

제14장 데이터센터용 UPS 시장(폼팩터별)

- 서론

- 랙 마운트형 UPS

- 자립형 UPS

제15장 데이터센터용 UPS 시장(데이터센터 유형별)

- 서론

- 하이퍼스케일러 및 클라우드 데이터센터

- 코로케이션 데이터센터

- 기업 데이터센터

- 은행, 금융서비스 및 보험(BFSI)

- IT 및 통신

- 정부 및 공공 부문

- 헬스케어 및 생명과학

- 제조

- 소매 및 전자상거래

- 운송 및 물류

- 에너지 및 유틸리티

- 기타

제16장 데이터센터용 UPS 시장(지역별)

- 서론

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타

- 아시아태평양

- 중국

- 인도

- 일본

- 기타

- 중동 및 아프리카

- GCC 국가

- 남아프리카공화국

- 기타

- 라틴아메리카

- 브라질

- 멕시코

- 기타

제17장 경쟁 구도

- 개요

- 주요 시장 진출기업의 전략/강점

- 매출 분석

- 시장 점유율 분석

- 제품 비교

- 기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 기업 평가와 재무 지표

- 경쟁 시나리오

제18장 기업 개요

- 주요 시장 진출기업

- SCHNEIDER ELECTRIC

- VERTIV

- EATON

- HUAWEI

- ABB

- DELTA ELECTRONICS

- LEGRAND

- HITACHI

- MITSUBISHI ELECTRIC

- TOSHIBA

- 기타 기업

- FUJI ELECTRIC

- RIELLO UPS

- ROLLS-ROYCE POWER SYSTEMS

- PILLAR POWER SYSTEMS

- KEHUA TECH

- KSTAR

- EAST GROUP

- SICON CHAT UNION ELECTRIC

- AEG POWER SOLUTIONS

- HITEC POWER PROTECTION

- KOHLER UNINTERRUPTIBLE POWER(KUP)

- SALICRU

- MAKELSAN

- TESCOM

- XTREAM POWER CONVERSION

- CYBER POWER

- N1 CRITICAL TECHNOLOGIES

- ZINCFIVE

- NATRON ENERGY

- ATTOM TECHNOLOGY

- ENCONNEX

- INVT POWER

- COOLNET POWER

- CENTIEL

제19장 조사 방법

제20장 부록

LSH 25.11.18The data center UPS market is projected to rise from USD 8.76 billion in 2025 to USD 12.47 billion by 2030, featuring a CAGR of 7.3%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | USD Million |

| Segments | Configuration Type, Design Type, Phase Type, Battery Type, Capacity, Form Factor, Data Center Type |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

The market is expanding rapidly, driven by hyperscale AI workload power demand, rising rack power densities, and the growing requirement for high-efficiency UPS systems capable of supporting uninterrupted operations in high-load environments. As AI and cloud-based applications increase power consumption per rack, operators are adopting scalable, modular, and energy-optimized UPS architectures to enhance performance and reduce the total cost of ownership. The transition toward lithium-ion batteries, grid-interactive designs, and integrated battery energy storage solutions is improving system reliability and sustainability by enabling higher energy efficiency and better load management. These advancements enable data centers to maintain power continuity while aligning their operations with corporate energy optimization goals.

The market's growth, however, is restrained by grid power availability constraints that limit data center expansion in high-demand regions, as well as longer equipment and component lead times resulting from supply chain disruptions and manufacturing bottlenecks. These factors create delays in deployment timelines and add cost pressures for hyperscale and colocation operators managing large build-outs. Despite these restraints, the continued focus on power efficiency, operational resilience, and sustainability is reinforcing the critical role of advanced UPS systems in ensuring stable and scalable power infrastructure across global data center networks.

"By capacity, the 1,001-2,000 kVA segment is projected to exhibit the fastest growth rate during the forecast period."

The 1,001-2,000 kVA capacity range addresses large-scale and hyperscale data centers that require robust, high-capacity UPS systems to protect vast compute pods, storage farms, and AI workloads. These UPS units consolidate redundancy, minimize parallel string count, and reduce floor space while delivering high efficiency and thermal performance. Their value lies in enabling seamless expansion, reducing the complexity of power distribution, and supporting high-density operations in mission-critical environments. In August 2025, Huawei launched its SUS2000G modular UPS platform, offering scalable configurations across the 1,000-2,000 kVA band to support cloud data centers and colocation campuses in China. Additionally, in March 2024, ABB delivered multiple 1.5 MVA (1,500 kVA) UPS systems as part of a power infrastructure upgrade for a hyperscale facility in Northern Europe, integrating advanced paralleling and synchronization capabilities across power modules. These deployments validate the growing demand in this higher-capacity segment. Vendors and solution providers should prioritize modularity, high-efficiency conversion, integrated battery management, and compatibility with high-voltage plant systems. Aligning with cloud providers, hyperscalers, and construction partners to offer prebuilt power modules and performance guarantees will allow early penetration and long-term contracts within the 1,001-2,000 kVA segment.

"By form factor, the rack-mounted segment is estimated to hold the largest market share during the forecast period."

Rack-mounted UPS systems are increasingly vital in modern data centers where space optimization, high power density, and modular deployment drive design decisions. Installed directly within IT racks, these systems typically support loads up to 50 kVA and are engineered to deliver efficient, localized power protection for critical equipment. Their compact design reduces cabling complexity and improves airflow management, making them ideal for edge, modular, and enterprise data centers operating within constrained footprints. For vendors and solution providers, rack-mounted UPS systems offer opportunities to deliver intelligent, energy-efficient backup solutions that integrate seamlessly with digital infrastructure, enabling remote management, predictive maintenance, and scalable capacity expansion. These systems align closely with evolving data center architectures focused on distributed resiliency and operational efficiency. Recent industry collaborations highlight this momentum. In June 2025, Eaton partnered with Fengsheng Electric to expand the distribution of its single-phase rack-mounted UPS systems across Singapore, addressing the growing demand for modular and edge deployments. Similarly, Vertiv's July 2025 acquisition of Great Lakes Data Racks & Cabinets strengthened its portfolio for integrated rack and power solutions. These strategic moves underscore the convergence of power and enclosure ecosystems. Going forward, vendors should focus on developing AI-integrated rack-mounted UPS platforms with lithium-ion batteries, intelligent monitoring, and hot-swappable designs to capture market share in space-constrained and performance-driven data centers.

"North America is estimated to lead the market with large-scale hyperscale developments, advanced power management infrastructure, and strong adoption of modular, high-efficiency UPS systems, while Asia Pacific is expected to exhibit the growth rate, driven by accelerating cloud expansion, rapid industrial digitalization, and government-backed investments in reliable, energy-resilient data center power infrastructure."

North America is emerging as the dominant region in the data center UPS market, fueled by accelerating hyperscale growth, AI-driven workloads, and increasing rack power densities that demand advanced, energy-efficient backup systems. The region's data center operators are rapidly adopting modular and lithium-ion UPS architectures that enhance scalability, reduce energy losses, and integrate with battery energy storage systems to ensure higher resilience and grid stability. In the US, growing power constraints in major hubs such as Northern Virginia, Dallas, and Phoenix are prompting large investments in next-generation UPS technologies capable of supporting AI and high-density computing clusters. Canada's clean energy policies and the expansion of renewable-powered data centers in provinces like Ontario and Quebec are creating strong opportunities for sustainable UPS deployment, aligning with decarbonization goals. Major vendors are strengthening domestic manufacturing capabilities and supply networks to address lead time pressures and meet new energy efficiency and cybersecurity standards. As regional utilities and regulators enforce grid readiness and carbon compliance, North America's UPS infrastructure is evolving from traditional backup systems into intelligent, high-performance assets that optimize energy use, enhance uptime, and reinforce the region's position as the global leader in resilient and sustainable data center power management.

Breakdown of Primaries

In-depth interviews were conducted with chief executive officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the data center UPS market.

- By Company: Tier I - 30%, Tier II - 45%, and Tier III - 25%

- By Designation: C-Level Executives - 50%, D-Level Executives -35%, and others - 15%

- By Region: North America - 50%, Europe - 30%, Asia Pacific - 15%, and Rest of the World - 5%

The report includes a study of key players offering data center UPS products. It profiles major vendors in the data center UPS market. The major market players include Schneider Electric (France), Vertiv (US), Eaton (Ireland), Huawei (China), ABB (Switzerland), Delta Electronics (Taiwan), Legrand (France), Hitachi (Japan), Toshiba (Japan), Mitsubishi Electric (Japan), Fuji Electric (Japan), Riello UPS (Italy), Rolls-Royce Power Systems (Germany), Piller Power Systems (Germany), Kehua Tech (China), Kstar (China), East Group (China), AEG Power Solutions (Netherlands), Hitech Power Protection (Netherlands), Centiel (Switzerland), Kohler Uninterruptible Power (US), Salicru (Spain), Makelsan (Turkey), Tescom (Turkey), Xtream Power Conversion (US), and Cyber Power (US).

Research Coverage

This research report categorizes the data center UPS market based on configuration type (online double conversion, line-interactive, offline/standby/battery backup), design type (modular UPS, conventional (monolithic) UPS), phase type (single-phase, three-phase), battery type (lead-acid batteries, lithium-ion batteries, nickel-cadmium batteries), capacity (up to 50 kVA, 51-200 kVA, 201-500 kVA, 501-1,000 kVA, 1,001-2,000 kVA, above 2,000 kVA), form factor (rack-mounted UPS, freestanding UPS), data center type (hyperscalers & cloud data centers, colocation data centers, enterprise data centers (BFSI, healthcare & life sciences, energy & utilities, manufacturing, IT & telecom, media & entertainment, government & public sector, retail & e-commerce, transportation & logistics, and other enterprise data centers (education and media & entertainment)), and Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the data center UPS market. A detailed analysis of key industry players was conducted to provide insights into their business overview, solutions, and services, as well as key strategies, contracts, partnerships, agreements, new product & service launches, mergers and acquisitions, and recent developments associated with the data center UPS market. This report also includes a competitive analysis of emerging startups in the data center UPS market ecosystem.

Reasons to Buy this Report

The report would provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall data center UPS market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. It also helps stakeholders understand the market's pulse and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Hyperscale AI workload power demand, Rising rack power densities, Demand for high-efficiency UPS systems), restraints (Grid power availability constraints, Longer equipment and component lead times), opportunities (Modular and scalable UPS adoption, Integration of renewables with AI power management, Growth in colocation and hyperscale facilities, Expansion of edge data centers), and challenges (Complex legacy-system integrations, Skilled workforce shortages).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the data center UPS market.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the data center UPS market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the data center UPS market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players such as Schneider Electric (France), Vertiv (US), Eaton (Ireland), Huawei (China), ABB (Switzerland), Delta Electronics (Taiwan), Legrand (France), Hitachi (Japan), Toshiba (Japan), Mitsubishi Electric (Japan), Fuji Electric (Japan), Riello UPS (Italy), Rolls-Royce Power Systems (Germany), Piller Power Systems (Germany), Kehua Tech (China), Kstar (China), East Group (China), AEG Power Solutions (Netherlands), Hitech Power Protection (Netherlands), Centiel (Switzerland), Kohler Uninterruptible Power (US), Salicru (Spain), Makelsan (Turkey), Tescom (Turkey), Xtream Power Conversion (US), and Cyber Power (US). The report also helps stakeholders understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE AND SEGMENTATION

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DATA CENTER UPS MARKET

- 3.2 DATA CENTER UPS MARKET, BY CONFIGURATION TYPE

- 3.3 DATA CENTER UPS MARKET, BY DESIGN TYPE

- 3.4 DATA CENTER UPS MARKET, BY PHASE TYPE

- 3.5 DATA CENTER UPS MARKET, BY BATTERY TYPE

- 3.6 DATA CENTER UPS MARKET, BY CAPACITY

- 3.7 DATA CENTER UPS MARKET, BY FORM FACTOR

- 3.8 DATA CENTER UPS MARKET, BY DATA CENTER TYPE

- 3.9 DATA CENTER UPS MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Hyperscale AI workload power demand

- 4.2.1.2 Rising rack power densities

- 4.2.1.3 Demand for high-efficiency UPS systems

- 4.2.2 RESTRAINTS

- 4.2.2.1 Grid power availability constraints

- 4.2.2.2 Longer equipment and component lead times

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Modular and scalable UPS adoption

- 4.2.3.2 Integration of renewables with AI power management

- 4.2.3.3 Growth in colocation and hyperscale facilities

- 4.2.3.4 Expansion of edge data centers

- 4.2.4 CHALLENGES

- 4.2.4.1 Complex legacy-system integrations

- 4.2.4.2 Skilled workforce shortages

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN DATA CENTER UPS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.1.1 Data center UPS business models

- 4.5.2 ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECASTS

- 5.2.3 TRENDS IN GLOBAL ELECTRONICS INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.3.1 COMPONENT SUPPLIERS

- 5.3.2 UPS MANUFACTURERS (OEMS)

- 5.3.3 SYSTEM INTEGRATORS

- 5.3.4 DATA CENTER SERVICE PROVIDERS

- 5.3.5 ENTERPRISE DATA CENTER

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE (ASP) TREND OF DATA CENTER UPS, BY REGION, 2024-2025

- 5.5.2 AVERAGES SELLING PRICE TREND OF DATA CENTER UPS, BY CAPACITY, 2024-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO

- 5.6.2 IMPORT SCENARIO

- 5.7 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.8 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 EATON DELIVERS COMPACT MODULAR UPS ENCLOSURE FOR NORTHWEST US DATA CENTER CLIENT

- 5.10.2 VERTIV ENHANCES ENERGY EFFICIENCY AND RELIABILITY FOR CONTABO'S DATA CENTERS IN GERMANY

- 5.10.3 SCHNEIDER ELECTRIC POWERS UPS SMART HUB WITH ECOSTRUXURE FOR SCALABLE, ENERGY-EFFICIENT OPERATIONS

- 5.10.4 ABB AND APPLIED DIGITAL PARTNER TO BUILD AI-READY 400 MW DATA CENTER CAMPUS WITH HIPERGUARD MEDIUM VOLTAGE UPS

- 5.10.5 21VIANET CONSTRUCTS FUTURE-ORIENTED DATA CENTER WITH HUAWEI SMARTLI UPS

- 5.11 IMPACT OF 2025 US TARIFF - DATA CENTER UPS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON DATA CENTER TYPES

- 5.11.5.1 Hyperscale & cloud service providers

- 5.11.5.2 Colocation service providers

- 5.11.5.3 Enterprise data centers

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ADVANCED POWER ELECTRONICS (IGBT AND SIC-BASED CONVERTERS)

- 6.1.2 MODULAR UPS ARCHITECTURE

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 BATTERY MANAGEMENT SYSTEMS (BMS)

- 6.2.2 POWER DISTRIBUTION UNITS (PDUS)

- 6.2.3 DCIM (DATA CENTER INFRASTRUCTURE MANAGEMENT) SOFTWARE

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 AI-BASED ENERGY OPTIMIZATION AND LOAD MANAGEMENT

- 6.3.2 DATA CENTER COOLING SYSTEMS

- 6.3.3 RENEWABLE ENERGY INTEGRATION SYSTEMS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | MODULARIZATION & LITHIUM TRANSITION

- 6.4.2 MID-TERM (2027-2030) | GRID-INTERACTIVE & INTELLIGENT UPS ECOSYSTEM

- 6.4.3 LONG-TERM (2030-2035+) | AUTONOMOUS & CARBON SMART POWER INFRASTRUCTURE

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 GRID-INTERACTIVE, BI-DIRECTIONAL UPS (VPP/DR READY)

- 6.6.2 AI-ORCHESTRATED, SOFTWARE-DEFINED UPS FABRIC

- 6.6.3 SOLID-STATE/SIC-FORWARD HIGH-EFFICIENCY UPS (SST-READY)

- 6.6.4 MODULAR EDGE POWER PODS (CONTAINERIZED UPS + BESS)

- 6.6.5 UPS-INTEGRATED MICRO GRIDS & HYBRID BESS (RENEWABLES/EV/H2 READY)

- 6.7 IMPACT OF AI/GENERATIVE AI ON THE DATA CENTER UPS MARKET

- 6.7.1 TOP USE CASES & MARKET POTENTIAL

- 6.7.2 CLIENT READINESS TO ADOPT GENERATIVE AI IN DATA CENTER UPS MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 EATON: 93PM AND 9395XC LITHIUM-ION UPS

- 6.8.2 ZINCFIVE: NIZN BATTERY UPS

7 REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS, BY REGION

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Middle East & South Africa

- 7.1.2.5 Latin America

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USER INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 DATA CENTER UPS MARKET, BY CONFIGURATION TYPE

- 9.1 INTRODUCTION

- 9.1.1 CONFIGURATION TYPE: DATA CENTER UPS MARKET DRIVERS

- 9.2 ONLINE DOUBLE CONVERSION

- 9.2.1 DRIVING DATA CENTER EFFICIENCY WITH ADVANCED DOUBLE CONVERSION UPS

- 9.3 LINE-INTERACTIVE

- 9.3.1 ENHANCING EDGE RELIABILITY THROUGH INTELLIGENT LINE-INTERACTIVE UPS SOLUTIONS

- 9.4 OFFLINE/STANDBY/BATTERY BACKUP

- 9.4.1 TRANSFORMING STANDBY UPS SYSTEMS INTO SMART, EFFICIENT POWER BACKUP

10 DATA CENTER UPS MARKET, BY DESIGN TYPE

- 10.1 INTRODUCTION

- 10.1.1 DESIGN TYPE: DATA CENTER UPS MARKET DRIVERS

- 10.2 MODULAR UPS

- 10.2.1 EMPOWERING SCALABLE AND ENERGY-EFFICIENT DATA CENTER OPERATIONS

- 10.3 CONVENTIONAL (MONOLITHIC) UPS

- 10.3.1 REINFORCING RELIABILITY AND LONGEVITY IN ENTERPRISE DATA CENTERS

11 DATA CENTER UPS MARKET, BY PHASE TYPE

- 11.1 INTRODUCTION

- 11.1.1 PHASE TYPE: DATA CENTER UPS MARKET DRIVERS

- 11.2 SINGLE PHASE

- 11.2.1 DRIVING RELIABILITY IN EDGE AND MICRO DATA CENTERS

- 11.3 THREE-PHASE

- 11.3.1 POWERING HIGH-DENSITY DATA CENTER OPERATIONS

12 DATA CENTER UPS MARKET, BY BATTERY TYPE

- 12.1 INTRODUCTION

- 12.1.1 BATTERY TYPE: DATA CENTER UPS MARKET DRIVERS

- 12.2 LEAD-ACID BATTERIES

- 12.2.1 ADVANCING DATA CENTER RELIABILITY THROUGH NEXT-GENERATION LEAD-ACID UPS TECHNOLOGIES

- 12.3 LITHIUM-ION BATTERIES

- 12.3.1 TRANSFORMING DATA CENTER PERFORMANCE WITH HIGH-EFFICIENCY LITHIUM-ION BATTERY SYSTEMS

- 12.4 NICKEL-CADMIUM BATTERIES

- 12.4.1 EMPOWERING CRITICAL DATA CENTER OPERATIONS WITH ROBUST NICKEL-CADMIUM UPS SOLUTIONS

13 DATA CENTER UPS MARKET, BY CAPACITY

- 13.1 INTRODUCTION

- 13.1.1 CAPACITY: DATA CENTER UPS MARKET DRIVERS

- 13.2 UP TO 50 KVA

- 13.2.1 ACCELERATING LOCALIZED COMPUTE RESILIENCE WITH ADVANCED UP TO 50 KVA UPS INTEGRATION

- 13.3 51-200 KVA

- 13.3.1 ENABLING SCALABLE MID-TIER DATA EXPANSION THROUGH INTELLIGENT 51-200 KVA UPS SYSTEMS

- 13.4 201-500 KVA

- 13.4.1 REINFORCING REGIONAL FACILITY STABILITY USING EFFICIENT 201-500 KVA UPS ARCHITECTURES

- 13.5 501-1,000 KVA

- 13.5.1 ADVANCING MODULAR AND ENTERPRISE UPTIME WITH ROBUST 501-1,000 KVA UPS SOLUTIONS

- 13.6 1,001-2,000 KVA

- 13.6.1 EMPOWERING HIGH-DENSITY INFRASTRUCTURE PERFORMANCE VIA 1,001-2,000 KVA UPS PLATFORMS

- 13.7 ABOVE 2,000 KVA

- 13.7.1 DRIVING HYPERSCALE EFFICIENCY AND AI READINESS WITH ABOVE 2,000 KVA UPS SYSTEMS

14 DATA CENTER UPS MARKET, BY FORM FACTOR

- 14.1 INTRODUCTION

- 14.1.1 FORM FACTOR: DATA CENTER UPS MARKET DRIVERS

- 14.2 RACK-MOUNTED UPS

- 14.2.1 OPTIMIZING POWER DENSITY AND EFFICIENCY THROUGH COMPACT, INTELLIGENT RACK-MOUNTED UPS DEPLOYMENTS

- 14.3 FREE-STANDING UPS

- 14.3.1 ENHANCING CENTRALIZED POWER RELIABILITY WITH HIGH-CAPACITY, SCALABLE FREE-STANDING UPS SOLUTIONS

15 DATA CENTER UPS MARKET, BY DATA CENTER TYPE

- 15.1 INTRODUCTION

- 15.1.1 DATA CENTER TYPE: DATA CENTER UPS MARKET DRIVERS

- 15.2 HYPERSCALERS & CLOUD DATA CENTERS

- 15.2.1 DRIVING ADVANCED, ENERGY-EFFICIENT UPS ADOPTION TO SUPPORT AI AND HIGH-DENSITY CLOUD WORKLOADS

- 15.3 COLOCATION DATA CENTERS

- 15.3.1 ENABLING MODULAR AND SCALABLE UPS ARCHITECTURES FOR MULTI-TENANT EFFICIENCY AND RELIABILITY

- 15.4 ENTERPRISE DATA CENTERS

- 15.4.1 ACCELERATING INTELLIGENT AND MODULAR UPS DEPLOYMENTS TO ENHANCE OPERATIONAL RESILIENCE AND SUSTAINABILITY

- 15.5 BFSI

- 15.5.1 ENHANCING FINANCIAL INFRASTRUCTURE RESILIENCE THROUGH RELIABLE AND ENERGY-EFFICIENT UPS DEPLOYMENTS

- 15.6 IT & TELECOM

- 15.6.1 ENABLING SEAMLESS CONNECTIVITY AND DATA RELIABILITY THROUGH INTELLIGENT UPS INFRASTRUCTURE

- 15.7 GOVERNMENT & PUBLIC SECTOR

- 15.7.1 STRENGTHENING CRITICAL GOVERNMENT DATA OPERATIONS THROUGH SECURE AND SCALABLE UPS SYSTEMS

- 15.8 HEALTHCARE & LIFE SCIENCES

- 15.8.1 SUPPORTING CLINICAL CONTINUITY AND RESEARCH INTEGRITY WITH ADVANCED UPS INFRASTRUCTURE

- 15.9 MANUFACTURING

- 15.9.1 DRIVING INDUSTRIAL EFFICIENCY AND UPTIME THROUGH SMART UPS INTEGRATION IN MANUFACTURING FACILITIES

- 15.10 RETAIL & E-COMMERCE

- 15.10.1 ENSURING CONTINUOUS DIGITAL COMMERCE OPERATIONS THROUGH RELIABLE AND SCALABLE UPS SYSTEMS

- 15.11 TRANSPORTATION & LOGISTICS

- 15.11.1 ENHANCING SUPPLY CHAIN RELIABILITY WITH HIGH-PERFORMANCE UPS INFRASTRUCTURE

- 15.12 ENERGY & UTILITIES

- 15.12.1 OPTIMIZING POWER CONTINUITY AND SMART GRID OPERATIONS THROUGH ADVANCED UPS DEPLOYMENTS

- 15.13 OTHER ENTERPRISE DATA CENTERS

16 DATA CENTER UPS MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 NORTH AMERICA

- 16.2.1 US

- 16.2.1.1 AI and hyperscale expansion to drive UPS demand and power infrastructure growth

- 16.2.2 CANADA

- 16.2.2.1 Rising digital loads and clean energy demand to fuel growth in UPS deployments

- 16.2.1 US

- 16.3 EUROPE

- 16.3.1 UK

- 16.3.1.1 Policy reforms and CNI status to accelerate hyperscale growth, driving UPS deployment across regional data hubs

- 16.3.2 GERMANY

- 16.3.2.1 Renewable integration and industrial digitalization to drive UPS modernization in high-density campuses

- 16.3.3 FRANCE

- 16.3.3.1 Paris metro expansion and national AI initiatives to fuel demand for next-generation UPS

- 16.3.4 ITALY

- 16.3.4.1 AI and cloud buildouts along Milan-Turin corridor to boost UPS investments for regional capacity resilience

- 16.3.5 REST OF EUROPE

- 16.3.1 UK

- 16.4 ASIA PACIFIC

- 16.4.1 CHINA

- 16.4.1.1 Massive AI and cloud investments to propel demand for modular, liquid-cooled UPS systems

- 16.4.2 INDIA

- 16.4.2.1 Hyperscale expansion and government data localization to drive high-efficiency, modular UPS deployments

- 16.4.3 JAPAN

- 16.4.3.1 TEPCO grid expansion and hyperscale AI campuses to reshape UPS architectures for reliability and power stability

- 16.4.4 REST OF ASIA PACIFIC

- 16.4.1 CHINA

- 16.5 MIDDLE EAST & AFRICA

- 16.5.1 GCC COUNTRIES

- 16.5.1.1 Saudi Arabia

- 16.5.1.1.1 National data infrastructure programs and hyperscale development across new economic zones to accelerate large-scale UPS standardization and service growth

- 16.5.1.2 UAE

- 16.5.1.2.1 Expanding hyperscale campuses, AI-focused workloads, and sustainability mandates to drive market

- 16.5.1.3 Other GCC countries

- 16.5.1.1 Saudi Arabia

- 16.5.2 SOUTH AFRICA

- 16.5.2.1 Rapid colocation and cloud expansion, combined with gradual grid stabilization, to drive market

- 16.5.3 REST OF MIDDLE EAST & AFRICA

- 16.5.1 GCC COUNTRIES

- 16.6 LATIN AMERICA

- 16.6.1 BRAZIL

- 16.6.1.1 Widespread hyperscale investments, renewable integration, and domestic manufacturing momentum to drive market

- 16.6.2 MEXICO

- 16.6.2.1 Rise of cloud regions and AI-ready campuses around Queretaro to drive market

- 16.6.3 REST OF LATIN AMERICA

- 16.6.1 BRAZIL

17 COMPETITIVE LANDSCAPE

- 17.1 OVERVIEW

- 17.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 17.2.1 COMPETITIVE STRATEGIES

- 17.3 REVENUE ANALYSIS

- 17.4 MARKET SHARE ANALYSIS

- 17.5 PRODUCT COMPARISON

- 17.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 17.6.1 STARS

- 17.6.2 EMERGING LEADERS

- 17.6.3 PERVASIVE PLAYERS

- 17.6.4 PARTICIPANTS

- 17.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 17.6.5.1 Company footprint

- 17.6.5.2 Region footprint

- 17.6.5.3 Configuration type footprint

- 17.6.5.4 Design type footprint

- 17.6.5.5 Phase type footprint

- 17.6.5.6 Capacity footprint

- 17.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 17.7.1 PROGRESSIVE COMPANIES

- 17.7.2 RESPONSIVE COMPANIES

- 17.7.3 DYNAMIC COMPANIES

- 17.7.4 STARTING BLOCKS

- 17.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 17.7.5.1 Detailed list of key startups/SMEs

- 17.7.5.2 Competitive benchmarking of key startups/SMEs

- 17.8 COMPANY VALUATION AND FINANCIAL METRICS

- 17.9 COMPETITIVE SCENARIO

- 17.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 17.9.2 DEALS

- 17.9.3 EXPANSIONS

18 COMPANY PROFILES

- 18.1 MAJOR PLAYERS

- 18.1.1 SCHNEIDER ELECTRIC

- 18.1.1.1 Business overview

- 18.1.1.2 Products/Solutions/Services offered

- 18.1.1.3 Recent developments

- 18.1.1.3.1 Product launches and enhancements

- 18.1.1.3.2 Deals

- 18.1.1.4 MnM view

- 18.1.1.4.1 Right to win

- 18.1.1.4.2 Strategic choices

- 18.1.1.4.3 Weaknesses and competitive threats

- 18.1.2 VERTIV

- 18.1.2.1 Business overview

- 18.1.2.2 Products/Solutions/Services offered

- 18.1.2.3 Recent developments

- 18.1.2.3.1 Product launches and enhancements

- 18.1.2.3.2 Deals

- 18.1.2.4 MnM view

- 18.1.2.4.1 Right to win

- 18.1.2.4.2 Strategic choices

- 18.1.2.4.3 Weaknesses and competitive threats

- 18.1.3 EATON

- 18.1.3.1 Business overview

- 18.1.3.2 Products/Solutions/Services offered

- 18.1.3.3 Recent developments

- 18.1.3.3.1 Product launches and enhancements

- 18.1.3.3.2 Deals

- 18.1.3.4 MnM view

- 18.1.3.4.1 Right to win

- 18.1.3.4.2 Strategic choices

- 18.1.3.4.3 Weaknesses and competitive threats

- 18.1.4 HUAWEI

- 18.1.4.1 Business overview

- 18.1.4.2 Products/Solutions/Services offered

- 18.1.4.3 Recent developments

- 18.1.4.3.1 Product launches and enhancements

- 18.1.4.3.2 Deals

- 18.1.4.4 MnM view

- 18.1.4.4.1 Right to win

- 18.1.4.4.2 Strategic choices

- 18.1.4.4.3 Weaknesses and competitive threats

- 18.1.5 ABB

- 18.1.5.1 Business overview

- 18.1.5.2 Products/Solutions/Services offered

- 18.1.5.3 Recent developments

- 18.1.5.3.1 Product launches and enhancements

- 18.1.5.3.2 Deals

- 18.1.5.4 MnM view

- 18.1.5.4.1 Right to win

- 18.1.5.4.2 Strategic choices

- 18.1.5.4.3 Weaknesses and competitive threats

- 18.1.6 DELTA ELECTRONICS

- 18.1.6.1 Business overview

- 18.1.6.2 Products/Solutions/Services offered

- 18.1.6.3 Recent developments

- 18.1.6.3.1 Product launches and enhancements

- 18.1.6.3.2 Deals

- 18.1.6.3.3 Expansions

- 18.1.7 LEGRAND

- 18.1.7.1 Business overview

- 18.1.7.2 Products/Solutions/Services offered

- 18.1.7.3 Recent developments

- 18.1.7.3.1 Deals

- 18.1.7.3.2 Expansions

- 18.1.8 HITACHI

- 18.1.8.1 Business overview

- 18.1.8.2 Products/Solutions/Services offered

- 18.1.8.3 Recent developments

- 18.1.8.3.1 Deals

- 18.1.9 MITSUBISHI ELECTRIC

- 18.1.9.1 Business overview

- 18.1.9.2 Products/Solutions/Services offered

- 18.1.9.3 Recent developments

- 18.1.9.3.1 Deals

- 18.1.9.3.2 Expansions

- 18.1.10 TOSHIBA

- 18.1.10.1 Business overview

- 18.1.10.2 Products/Solutions/Services offered

- 18.1.10.3 Recent developments

- 18.1.10.3.1 Product launches and enhancements

- 18.1.10.3.2 Expansions

- 18.1.1 SCHNEIDER ELECTRIC

- 18.2 OTHER PLAYERS

- 18.2.1 FUJI ELECTRIC

- 18.2.2 RIELLO UPS

- 18.2.3 ROLLS-ROYCE POWER SYSTEMS

- 18.2.4 PILLAR POWER SYSTEMS

- 18.2.5 KEHUA TECH

- 18.2.6 KSTAR

- 18.2.7 EAST GROUP

- 18.2.8 SICON CHAT UNION ELECTRIC

- 18.2.9 AEG POWER SOLUTIONS

- 18.2.10 HITEC POWER PROTECTION

- 18.2.11 KOHLER UNINTERRUPTIBLE POWER (KUP)

- 18.2.12 SALICRU

- 18.2.13 MAKELSAN

- 18.2.14 TESCOM

- 18.2.15 XTREAM POWER CONVERSION

- 18.2.16 CYBER POWER

- 18.2.17 N1 CRITICAL TECHNOLOGIES

- 18.2.18 ZINCFIVE

- 18.2.19 NATRON ENERGY

- 18.2.20 ATTOM TECHNOLOGY

- 18.2.21 ENCONNEX

- 18.2.22 INVT POWER

- 18.2.23 COOLNET POWER

- 18.2.24 CENTIEL

19 RESEARCH METHODOLOGY

- 19.1 RESEARCH DATA

- 19.1.1 SECONDARY DATA

- 19.1.1.1 Key data from secondary sources

- 19.1.2 PRIMARY DATA

- 19.1.2.1 Key data from primary sources

- 19.1.2.2 Breakdown of primary interviews

- 19.1.2.3 Key industry insights

- 19.1.3 MARKET SIZE ESTIMATION

- 19.1.1 SECONDARY DATA

- 19.2 DATA TRIANGULATION

- 19.2.1 FACTOR ANALYSIS

- 19.2.2 RESEARCH ASSUMPTIONS

- 19.2.3 RESEARCH LIMITATIONS AND RISK ASSESSMENT

20 APPENDIX

- 20.1 DISCUSSION GUIDE

- 20.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.3 CUSTOMIZATION OPTIONS

- 20.4 RELATED REPORTS

- 20.5 AUTHOR DETAILS