|

시장보고서

상품코드

1861053

의료기기 제조 장비 세계 시장 : 유형별, 최종사용자별, 용도별, 지역별 - 예측(-2030년)Medical Device Manufacturing Equipment (by Production) Market by Type (Material Processing, Sterilization & Cleaning Equipment), Application (Consumables & Disposables), End User (OEMs, Contract Manufacturing Organizations) - Global Forecast to 2030 |

||||||

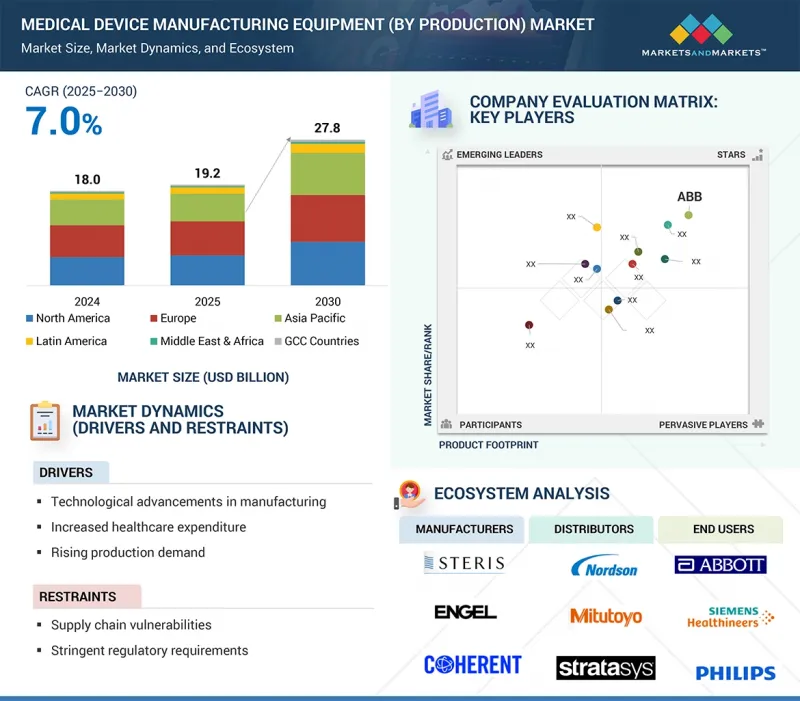

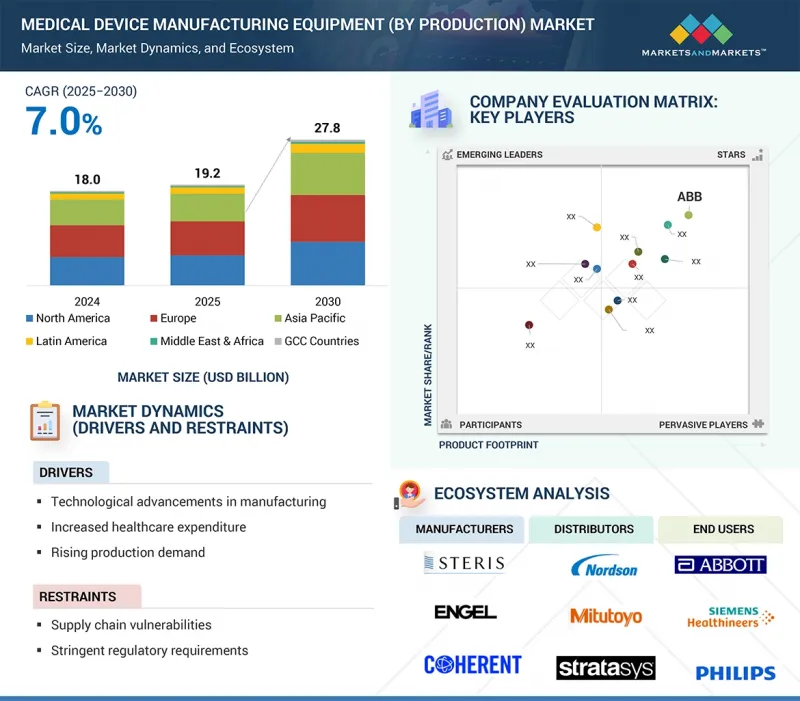

의료기기 제조 장비(생산 별) 시장 규모는 예측 기간 중에 7.6%의 연평균 복합 성장률(CAGR)로 확대되어 2025년 192억 4,000만 달러에서 2030년에는 278억 달러에 이를 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2023-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(100만 달러) |

| 부문 | 유형별, 최종사용자별, 용도별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

의료기기 제조 장비 시장은 자동화, 로봇 공학, 정밀 가공의 기술 발전, 고품질 및 적합성 높은 장비에 대한 수요 증가에 힘입어 성장하고 있습니다. 높은 자본 비용, 복잡한 규제 요건, 공급망 취약성이 성장을 저해하고 있습니다. 비즈니스 기회는 현지 생산에 대한 투자가 증가하고 있는 신흥 시장과 3D 프린팅 및 첨단 소재에 기반한 맞춤형 최소침습적 장치 생산에 존재합니다. IoT 및 AI와 같은 디지털 통합은 생산 효율성과 확장성을 더욱 높여줍니다.

재료 가공 장비 유형별로는 적층 가공/3D 프린팅 시스템이 복잡한 맞춤형 장치를 신속하게 생산하고, 재료 낭비를 줄이며, 생산 주기를 단축하고, 프로토타이핑 및 소량 생산을 지원하는 능력으로 인해 예측 기간 동안 가장 높은 성장률을 보일 것으로 예측됩니다. 유연성, 정밀성, 첨단 소재와의 적합성 등으로 저침습적이고 환자 맞춤형 의료기기에 높은 가치를 발휘하며 전 세계적으로 보급을 주도하고 있습니다.

최종 사용자별로는 제조 위탁 기관이 예측 기간 동안 가장 높은 성장률을 보일 것으로 예측됩니다. 그 배경에는 대규모 설비 투자 없이도 전문적이고 비용 효율적인 제조 솔루션을 제공할 수 있다는 점이 있습니다. 수탁 제조 기관은 확장 가능한 제조, 규제 준수 전문성, 첨단 기술에 대한 접근성을 제공함으로써 의료기기 제조업체가 연구개발과 마케팅에 집중할 수 있도록 하는 한편, 세계 시장에서 효율적이고 고품질의 제품을 생산할 수 있도록 보장합니다.

예측 기간 동안 아시아태평양이 가장 높은 성장률을 보일 것으로 예측됩니다. 빠르게 확대되는 헬스케어 인프라, 정부 투자 증가, 의료기기 생산 증가 등이 그 요인으로 꼽힙니다. 중국, 인도, 일본과 같은 국가들은 자동화 및 3D 프린팅을 포함한 첨단 제조 기술을 채택하고 있습니다. 또한, 낮은 인건비, 유리한 규제 개혁, 환자 전용 기기에 대한 수요 증가가 이 지역의 높은 시장 성장률을 견인하고 있습니다.

세계의 의료기기 제조 장비 시장에 대해 조사했으며, 유형별, 최종사용자별, 용도별, 지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

- 서론

- 시장 역학

- 고객의 비즈니스에 영향을 미치는 동향/파괴적 변화

- 가격 분석

- 밸류체인 분석

- 공급망 분석

- 생태계 분석

- 투자 및 자금조달 시나리오

- 기술 분석

- 업계 동향

- 특허 분석

- 무역 분석

- 2025-2026년 주요 컨퍼런스 및 이벤트

- 사례 연구 분석

- 규제 분석

- Porter의 Five Forces 분석

- 주요 이해관계자와 구입 기준

- AI/생성형 AI가 의료기기 제조 장비 시장에 미치는 영향

- 2025년 미국 관세가 의료기기 제조 장비 시장에 미치는 영향

제6장 의료기기 제조 장비 시장(유형별)

- 서론

- 재료 처리 장비

- 조립 및 자동화 시스템

- 표면 처리 및 코팅 장비

- 시험 및 검사 시스템

- 멸균 및 세정 장비

- 포장 및 라벨링 기기

- 클린룸 및 환경 시스템

제7장 의료기기 제조 장비 시장(최종사용자별)

- 서론

- 의료기기 OEM

- CMO

- 연구 및 학술 프로토타이핑 센터

제8장 의료기기 제조 장비 시장(용도별)

- 서론

- 소모품 및 일회용품

- 외과 기구

- 임플란트

- 진단 및 치료 기기

- 약물전달 기기

- 기타

제9장 의료기기 제조 장비 시장(지역별)

- 서론

- 유럽

- 유럽의 거시경제 전망

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 일본

- 중국

- 인도

- 한국

- 호주

- 기타

- 라틴아메리카

- 라틴아메리카의 거시경제 전망

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- 클린룸, 검사, 라벨링 기술 도입을 촉진하는 헬스케어 산업화 프로그램

- 중동 및 아프리카의 거시경제 전망

- GCC 국가

- 현지 제조능력 향상에 의해 멸균, 성형, 포장 시스템 수요가 증가

- GCC 국가 거시경제 전망

제10장 경쟁 구도

- 개요

- 주요 시장 진출기업의 전략/강점

- 매출 분석, 2020년-2024년

- 시장 점유율 분석, 2024년

- 기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 기업 평가와 재무 지표

- 브랜드/제품 비교

- 경쟁 시나리오

제11장 기업 개요

- 주요 시장 진출기업

- ABB

- STERIS

- ZEISS GROUP

- TRUMPF

- NORDSON CORPORATION

- ENGEL

- HUSKY INJECTION MOLDING SYSTEMS LTD.

- EMERSON

- COHERENT CORP.

- OC OERLIKON MANAGEMENT AG

- NIKON CORPORATION

- DURR GROUP

- MULTIVAC

- MIKRON

- STRATASYS LTD.

- 기타 기업

- BORCHE NORTH AMERICA INC.

- R.P. INJECTION SRL

- LASERAX

- LITHIUM LASERS SRL

- AXIAL3D

- MOLD HOTRUNNER SOLUTIONS LTD.

- ATLAS ENVIRONMENTS, LTD.

- BERKSHIRE CORPORATION

- CLEAN ROOMS INTERNATIONAL, INC.

- CLEAN AIR TECHNOLOGY, INC.

제12장 부록

LSH 25.11.18The medical device manufacturing equipment (by production) market is projected to reach USD 27.80 billion by 2030 from USD 19.24 billion in 2025, at a CAGR of 7.6% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) |

| Segments | Equipment Type, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa, and GCC Countries |

The medical device manufacturing equipment market is driven by technological advancements in automation, robotics, and precision machining, and increasing demand for high-quality, compliant devices. Growth is restrained by high capital costs, complex regulatory requirements, and supply chain vulnerabilities. Opportunities exist in emerging markets, where investments in local manufacturing are rising, and in customized and minimally invasive device production, supported by 3D printing and advanced materials. Digital integration, like IoT and AI, further enhances production efficiency and scalability.

Based on material processing equipment type, the additive manufacturing/3D printing systems are expected to witness the highest growth rate during the forecast period due to their ability to produce complex, customized devices rapidly, reduce material waste, shorten production cycles, and support prototyping and small-batch production. Their flexibility, precision, and compatibility with advanced materials make them highly valuable for minimally invasive and patient-specific medical devices, driving widespread adoption globally.

Based on end user, contract manufacturing organizations are expected to have the highest growth rate during the forecast year. This is driven by the ability to provide specialized, cost-effective production solutions without heavy capital investment. They offer scalable manufacturing, regulatory compliance expertise, and access to advanced technologies, enabling medical device companies to focus on R&D and marketing while ensuring efficient, high-quality device production across global markets.

Asia Pacific is projected to exhibit the highest growth rate during the forecast year. The surge is driven by rapidly expanding healthcare infrastructure, rising government investments, and increasing medical device production. Countries like China, India, and Japan are adopting advanced manufacturing technologies, including automation and 3D printing. Additionally, low labor costs, favorable regulatory reforms, and growing demand for patient-specific devices are driving the region's high market growth rate.

A breakdown of the primary participants (supply-side) for the medical device manufacturing equipment (by production) market referred to in this report is provided below:

- By Company Type: Tier 1: 34%, Tier 2: 38%, and Tier 3: 28%

- By Designation: C-level: 26%, Director Level: 35%, and Others: 39%

- By Region: North America: 17%, Europe: 39%, Asia Pacific: 28%, Latin America: 8%, Middle East & Africa: 3%, GCC Countries: 5%

Prominent players in the medical device manufacturing equipment (by production) market are STERIS (US), Nordson Corporation (US), ENGEL (Austria), Zeiss Group (Germany), Multivac (Germany), Coherent Corp. (US), KUKA AG (Germany), ABB (Switzerland), TRUMPF (Germany), OC Oerlikon Management AG (Switzerland), Arburg (Germany), Stratasys Ltd (US), Plasmatreat (Germany), Nikon Corporation (Japan), and Mitutoyo Corporation (Japan), among others.

Research Coverage

The report evaluates the medical device manufacturing equipment (by production) market and estimates the market size and future growth potential of this market based on various segments including equipment type, application, end user, and region. The report also includes a competitive analysis of the major players in this market, along with company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will assist the market leader/new entrants in the market with data on the nearest approximations of the revenue numbers for the overall, the medical device manufacturing equipment (by production) market and the subsegments. The report will assist stakeholders in understanding the competitive landscape and gain further insights into better positioning their businesses and making appropriate go-to-market strategies. The report assists the stakeholders in understanding the market pulse and gives them data on influential drivers, hindrances, obstacles, and opportunities in the market.

This report provides insights into the following points:

- Analysis of key drivers (technological advancements in manufacturing, increased healthcare expenditure, and rising production demand), restraints (supply chain vulnerabilities and stringent regulatory requirements), opportunities (customization and personalization and adoption of digital health solutions), and challenges (trade tariffs and import restrictions)

- Product Enhancement/Innovation: Comprehensive details about product launches and anticipated trends in the global medical device manufacturing equipment (by production) market

- Market Development: Thorough knowledge and analysis of the profitable rising markets by equipment type, application, end user, and region

- Market Diversification: Comprehensive information about newly launched products and services, expanding markets, current advancements, and investments in the global medical device manufacturing equipment (by production) market

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings, and capacities of the major competitors in the global medical device manufacturing equipment (by production) market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY USED

- 1.5 STAKEHOLDERS

- 1.6 LIMITATIONS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.3 MARKET BREAKDOWN & DATA TRIANGULATION

- 2.4 MARKET SHARE ESTIMATION

- 2.5 STUDY ASSUMPTIONS

- 2.6 METHODOLOGY-RELATED LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 MEDICAL DEVICE MANUFACTURING EQUIPMENT MARKET OVERVIEW

- 4.2 ASIA PACIFIC: MEDICAL DEVICE MANUFACTURING EQUIPMENT MARKET, BY TYPE AND COUNTRY (2024)

- 4.3 MEDICAL DEVICE MANUFACTURING EQUIPMENT MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.4 MEDICAL DEVICE MANUFACTURING EQUIPMENT MARKET, REGIONAL MIX, 2023-2030

- 4.5 MEDICAL DEVICE MANUFACTURING EQUIPMENT MARKET: EMERGING VS. DEVELOPED ECONOMIES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Technological advancements in manufacturing

- 5.2.1.2 Increased healthcare expenditure

- 5.2.1.3 Rising production demand

- 5.2.2 RESTRAINTS

- 5.2.2.1 Supply chain vulnerabilities

- 5.2.2.2 Stringent regulatory requirements

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Customization and personalization

- 5.2.3.2 Adoption of digital health solutions

- 5.2.4 CHALLENGES

- 5.2.4.1 Trade tariffs and import restrictions

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY PRODUCT, 2024

- 5.4.2 AVERAGE SELLING PRICE TREND OF INJECTION MOLDING MACHINES, BY REGION, 2022-2024

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.8 INVESTMENT & FUNDING SCENARIO

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Injection molding systems

- 5.9.1.2 Additive manufacturing (3D printing)

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Metrology & inspection equipment

- 5.9.2.2 Cleanroom & contamination control systems

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 Industrial robotics & automation

- 5.9.3.2 Industrial IoT (IIoT) & AI analytics

- 5.9.1 KEY TECHNOLOGIES

- 5.10 INDUSTRY TRENDS

- 5.10.1 SHIFT TOWARD SMART MANUFACTURING & INDUSTRY 4.0 INTEGRATION

- 5.10.2 RISING DEMAND FOR CUSTOMIZATION AND ADDITIVE MANUFACTURING

- 5.11 PATENT ANALYSIS

- 5.12 TRADE ANALYSIS

- 5.12.1 IMPORT DATA (HS CODE 8477)

- 5.12.2 EXPORT DATA (HS CODE 8477)

- 5.13 KEY CONFERENCES & EVENTS, 2025-2026

- 5.14 CASE STUDY ANALYSIS

- 5.14.1 CASE STUDY 1: MMT/SOMEX AUTOMATION - MANDREL REMOVAL/INSERTION FOR CATHETER SHAFTS

- 5.14.2 CASE STUDY 2: HAHN AUTOMATION GROUP - AUTOMATED COILING FOR VASCULAR DEVICE OEM

- 5.14.3 CASE STUDY 3: AMS MACHINES - ADHESIVE DISPENSE AND UV CURE AUTOMATION FOR WEARABLE INJECTOR OEM

- 5.15 REGULATORY ANALYSIS

- 5.15.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.15.2 REGULATORY FRAMEWORK

- 5.15.2.1 North America

- 5.15.2.1.1 US

- 5.15.2.1.2 Canada

- 5.15.2.2 Europe

- 5.15.2.2.1 Germany

- 5.15.2.2.2 France

- 5.15.2.2.3 UK

- 5.15.2.3 Asia Pacific

- 5.15.2.3.1 India

- 5.15.2.3.2 China

- 5.15.2.3.3 Japan

- 5.15.2.4 Latin America

- 5.15.2.4.1 Brazil

- 5.15.2.4.2 Mexico

- 5.15.2.5 Middle East & Africa

- 5.15.2.5.1 Middle East

- 5.15.2.5.2 Africa

- 5.15.2.1 North America

- 5.16 PORTER'S FIVE FORCES ANALYSIS

- 5.16.1 BARGAINING POWER OF SUPPLIERS

- 5.16.2 BARGAINING POWER OF BUYERS

- 5.16.3 THREAT OF NEW ENTRANTS

- 5.16.4 THREAT OF SUBSTITUTES

- 5.16.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.17 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.17.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.17.2 BUYING CRITERIA

- 5.18 IMPACT OF AI/GENERATIVE AI ON MEDICAL DEVICE MANUFACTURING EQUIPMENT MARKET

- 5.18.1 AI USE CASES

- 5.18.2 KEY COMPANIES IMPLEMENTING AI

- 5.18.3 FUTURE OF AI/GEN AI

- 5.19 IMPACT OF 2025 US TARIFFS ON MEDICAL DEVICE MANUFACTURING EQUIPMENT MARKET

- 5.19.1 KEY TARIFF RATES

- 5.19.2 PRICE IMPACT ANALYSIS

- 5.19.3 KEY IMPACT ON COUNTRY/REGION

- 5.19.3.1 US

- 5.19.3.2 Europe

- 5.19.3.3 Asia Pacific

- 5.19.4 IMPACT ON END-USE INDUSTRIES

6 MEDICAL DEVICE MANUFACTURING EQUIPMENT MARKET, BY TYPE

- 6.1 INTRODUCTION

- 6.2 MATERIAL PROCESSING EQUIPMENT

- 6.2.1 INJECTION MOLDING MACHINES

- 6.2.1.1 Growing need for high-volume disposables and diagnostics to drive precision molding capacity

- 6.2.2 LASER CUTTING & WELDING SYSTEMS

- 6.2.2.1 UDI compliance to accelerates adoption of corrosion-resistant, permanent laser black marking

- 6.2.3 ADDITIVE MANUFACTURING/3D PRINTING SYSTEMS

- 6.2.3.1 Personalization and complexity advantages to shift AM from prototyping to production

- 6.2.4 OTHER MATERIAL PROCESSING EQUIPMENT

- 6.2.1 INJECTION MOLDING MACHINES

- 6.3 ASSEMBLY & AUTOMATION SYSTEMS

- 6.3.1 ROBOTIC ASSEMBLY LINES

- 6.3.1.1 Ability of cobots with AI vision to elevate yield and reduce contamination risk to drive adoption

- 6.3.2 PICK & PLACE ROBOTICS

- 6.3.2.1 Ability of SCARA and delta robots to standardize repeatable handling across ISO cleanrooms to boost demand

- 6.3.3 DISPENSING & GLUING SYSTEMS

- 6.3.3.1 Growing demand for miniaturized devices to drive need for precise, biocompatible bonding with closed-loop control

- 6.3.4 ULTRASONIC WELDING & BONDING SYSTEMS

- 6.3.4.1 ISO 11607 validation to drive demand for ultrasonic sealing across sterile packaging lines

- 6.3.1 ROBOTIC ASSEMBLY LINES

- 6.4 SURFACE TREATMENT & COATING EQUIPMENT

- 6.4.1 PLASMA TREATMENT SYSTEMS

- 6.4.1.1 Solvent-free surface activation to boost adhesion, yield, and sustainability metrics

- 6.4.2 ELECTROPOLISHING & ANODIZING SYSTEMS

- 6.4.2.1 Demand for corrosion-resistant, ultraclean finishes to drive standardized electropolishing investments

- 6.4.3 COATING SYSTEMS

- 6.4.3.1 Infection prevention and performance gains to fuel validated medical coating investments

- 6.4.1 PLASMA TREATMENT SYSTEMS

- 6.5 TESTING & INSPECTION SYSTEMS

- 6.5.1 OPTICAL INSPECTION SYSTEMS

- 6.5.1.1 Growing adoption of AI-driven 2D/3D machine vision to support growth

- 6.5.2 LEAK & PRESSURE TESTERS

- 6.5.2.1 ISO 11607 compliance mandates to drive demand for robust, automated leak and seal testing

- 6.5.3 METROLOGY EQUIPMENT

- 6.5.3.1 ISO 13485 traceability to elevate advanced metrology investments

- 6.5.4 ELECTRICAL & FUNCTIONAL TESTERS

- 6.5.4.1 IEC 60601 compliance requirements to drive demand for automated electrical and functional testing

- 6.5.1 OPTICAL INSPECTION SYSTEMS

- 6.6 STERILIZATION & CLEANING EQUIPMENT

- 6.6.1 STEAM STERILIZERS

- 6.6.1.1 Infection prevention priorities to drive upgrades to networked, efficient autoclaves

- 6.6.2 HYDROGEN PEROXIDE PLASMA SYSTEMS

- 6.6.2.1 EtO emission pressures to accelerate adoption of VHP/H2O2 plasma systems

- 6.6.3 ETHYLENE OXIDE SYSTEMS

- 6.6.3.1 Irreplaceable material compatibility to preserve EtO demand despite tighter regulations

- 6.6.4 ULTRASONIC CLEANING SYSTEMS

- 6.6.4.1 ISO-driven validations to accelerate adoption of automated, aqueous ultrasonic cleaning

- 6.6.1 STEAM STERILIZERS

- 6.7 PACKAGING & LABELING EQUIPMENT

- 6.7.1 BLISTER PACKAGING MACHINES

- 6.7.1.1 Need for unit dose, tamper evident formats to drive blister capacity investments globally

- 6.7.2 FORM-FILL-SEAL (FFS) SYSTEMS

- 6.7.2.1 Inline seal monitoring to accelerate validations and time to market

- 6.7.3 LABELING & CODING SYSTEMS

- 6.7.3.1 UDI deadlines to drive serialization, printing, and vision verified coding investments

- 6.7.4 OTHER PACKAGING & LABELING EQUIPMENT

- 6.7.1 BLISTER PACKAGING MACHINES

- 6.8 CLEANROOM & ENVIRONMENTAL SYSTEMS

- 6.8.1 CLEANROOM INFRASTRUCTURE

- 6.8.1.1 ISO 14644 compliance to drive demand for HVAC, zoning, and continuous environmental monitoring

- 6.8.2 HVAC, HUMIDITY, AND ESD PROTECTION SYSTEMS

- 6.8.2.1 Annex 1 and ISO 14644 to elevate HVAC control and monitoring

- 6.8.3 CONTAMINATION CONTROL SYSTEMS

- 6.8.3.1 Annex 1 mandates to boost contamination control investments

- 6.8.1 CLEANROOM INFRASTRUCTURE

7 MEDICAL DEVICE MANUFACTURING EQUIPMENT MARKET, BY END USER

- 7.1 INTRODUCTION

- 7.2 MEDICAL DEVICE OEMS

- 7.2.1 ABILITY OF OEMS TO DRIVE INNOVATION AND ENSURE REGULATORY COMPLIANCE TO DRIVE MARKET GROWTH

- 7.3 CONTRACT MANUFACTURING ORGANIZATIONS

- 7.3.1 PIVOTAL ROLE PLAYED BY CMOS IN DRIVING EQUIPMENT DEMAND TO SUPPORT MARKET GROWTH

- 7.4 RESEARCH & ACADEMIC PROTOTYPING CENTERS

- 7.4.1 ABILITY TO MITIGATE RISKS AND SPEED UP TRANSFER OF CONCEPTS TO BOOST GROWTH

8 MEDICAL DEVICE MANUFACTURING EQUIPMENT MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 CONSUMABLES & DISPOSABLES

- 8.2.1 RISING SINGLE-USE ADOPTION TO MEET STERILITY, COMPLIANCE, AND THROUGHPUT REQUIREMENTS TO DRIVE MARKET

- 8.3 SURGICAL INSTRUMENTS

- 8.3.1 GROWTH IN MINIMALLY INVASIVE PROCEDURES TO BOOST PRECISION MACHINING INVESTMENTS AND DRIVE MARKET GROWTH

- 8.4 IMPLANTS

- 8.4.1 AGING DEMOGRAPHICS AND EXPANDING ORTHOPEDIC VOLUMES TO DRIVE MARKET

- 8.5 DIAGNOSTIC & THERAPEUTIC DEVICES

- 8.5.1 GROWING DEMAND FOR POINT-OF-CARE TESTING TO DRIVE HIGH-SPEED CARTRIDGE MOLDING AND SEALING CAPACITY

- 8.6 DRUG DELIVERY DEVICES

- 8.6.1 PREFILLED SYRINGE ADOPTION TO ACCELERATE HIGH-SPEED ASSEMBLY AND INSPECTION

- 8.7 OTHER DEVICES

9 MEDICAL DEVICE MANUFACTURING EQUIPMENT MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 EUROPE

- 9.2.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 9.2.2 GERMANY

- 9.2.2.1 Germany's engineering expertise and EU MDR compliance to drive adoption of advanced medical device production equipment

- 9.2.3 FRANCE

- 9.2.3.1 Rising demand for implants and disposables to fuel French investment in molding, coating, and automation systems

- 9.2.4 UK

- 9.2.4.1 Regulatory compliance and export competitiveness to drive adoption of automation, packaging, and inspection equipment

- 9.2.5 ITALY

- 9.2.5.1 Italy's packaging leadership and EU MDR compliance to drive strong adoption of medical device manufacturing equipment

- 9.2.6 SPAIN

- 9.2.6.1 Spain's regulatory compliance and growing CMO base to accelerate adoption of medical device production equipment

- 9.2.7 REST OF EUROPE

- 9.3 NORTH AMERICA

- 9.3.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 9.3.2 US

- 9.3.2.1 FDA compliance and reshoring strategies to accelerate adoption of automation, sterilization, and inspection systems

- 9.3.3 CANADA

- 9.3.3.1 Growing modernization of production facilities with cleanroom equipment to enhance export competitiveness

- 9.4 ASIA PACIFIC

- 9.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 9.4.2 JAPAN

- 9.4.2.1 Japan's robotics and precision engineering strengths to drive accelerated adoption of medical device production equipment

- 9.4.3 CHINA

- 9.4.3.1 Government policies and domestic demand to fuel China's adoption of molding, sterilization, and automation equipment

- 9.4.4 INDIA

- 9.4.4.1 Government incentives and medical device parks to accelerate adoption of molding, sterilization, and automation equipment

- 9.4.5 SOUTH KOREA

- 9.4.5.1 Regulatory rigor and Industry 4.0 integration to drive South Korea's rapid adoption of medical device production equipment

- 9.4.6 AUSTRALIA

- 9.4.6.1 Australia's innovation clusters and strict TGA compliance to drive adoption of advanced medical device production equipment

- 9.4.7 REST OF ASIA PACIFIC

- 9.5 LATIN AMERICA

- 9.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 9.5.2 BRAZIL

- 9.5.2.1 ANVISA compliance and domestic demand to drive Brazil's adoption of advanced medical device production equipment

- 9.5.3 MEXICO

- 9.5.3.1 USMCA integration and FDA compliance to accelerate Mexico's adoption of advanced medical device manufacturing equipment

- 9.5.4 REST OF LATIN AMERICA

- 9.6 MIDDLE EAST & AFRICA

- 9.6.1 HEALTHCARE INDUSTRIALIZATION PROGRAMS TO ACCELERATE ADOPTION OF CLEANROOM, INSPECTION, AND LABELING TECHNOLOGIES

- 9.6.2 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 9.7 GCC COUNTRIES

- 9.7.1 RISING LOCAL MANUFACTURING CAPACITY TO FUEL DEMAND FOR STERILIZATION, MOLDING, AND PACKAGING SYSTEMS

- 9.7.2 MACROECONOMIC OUTLOOK FOR GCC COUNTRIES

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 10.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN MEDICAL DEVICE MANUFACTURING EQUIPMENT MARKET

- 10.3 REVENUE ANALYSIS, 2020-2024

- 10.4 MARKET SHARE ANALYSIS, 2024

- 10.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.5.1 STARS

- 10.5.2 EMERGING LEADERS

- 10.5.3 PERVASIVE PLAYERS

- 10.5.4 PARTICIPANTS

- 10.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.5.5.1 Company footprint

- 10.5.5.2 Region footprint

- 10.5.5.3 Equipment footprint

- 10.5.5.4 Application footprint

- 10.5.5.5 End-user footprint

- 10.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 10.6.1 PROGRESSIVE COMPANIES

- 10.6.2 RESPONSIVE COMPANIES

- 10.6.3 DYNAMIC COMPANIES

- 10.6.4 STARTING BLOCKS

- 10.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 10.6.5.1 Detailed list of key startups/SMEs

- 10.6.5.2 Competitive benchmarking of startups/SMEs

- 10.7 COMPANY VALUATION & FINANCIAL METRICS

- 10.7.1 FINANCIAL METRICS

- 10.7.2 COMPANY VALUATION

- 10.8 BRAND/PRODUCT COMPARISON

- 10.8.1 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES

- 10.9.2 DEALS

- 10.9.3 EXPANSIONS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 ABB

- 11.1.1.1 Business overview

- 11.1.1.2 Products offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Deals

- 11.1.1.3.2 Expansions

- 11.1.1.4 MnM view

- 11.1.1.4.1 Key strengths

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses & competitive threats

- 11.1.2 STERIS

- 11.1.2.1 Business overview

- 11.1.2.2 Products offered

- 11.1.2.3 Recent developments

- 11.1.2.3.1 Product launches

- 11.1.2.4 MnM view

- 11.1.2.4.1 Key strengths

- 11.1.2.4.2 Strategic choices

- 11.1.2.4.3 Weaknesses & competitive threats

- 11.1.3 ZEISS GROUP

- 11.1.3.1 Business overview

- 11.1.3.2 Products offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Deals

- 11.1.3.4 MnM view

- 11.1.3.4.1 Key strengths

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses & competitive threats

- 11.1.4 TRUMPF

- 11.1.4.1 Business overview

- 11.1.4.2 Products offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Product launches

- 11.1.4.3.2 Deals

- 11.1.4.4 MnM view

- 11.1.4.4.1 Key strengths

- 11.1.4.4.2 Strategic choices

- 11.1.4.4.3 Weaknesses & competitive threats

- 11.1.5 NORDSON CORPORATION

- 11.1.5.1 Business overview

- 11.1.5.2 Products offered

- 11.1.5.3 Recent developments

- 11.1.5.3.1 Product launches

- 11.1.5.3.2 Deals

- 11.1.5.3.3 Expansions

- 11.1.5.4 MnM view

- 11.1.5.4.1 Key strengths

- 11.1.5.4.2 Strategic choices

- 11.1.5.4.3 Weaknesses & competitive threats

- 11.1.6 ENGEL

- 11.1.6.1 Business overview

- 11.1.6.2 Products offered

- 11.1.7 HUSKY INJECTION MOLDING SYSTEMS LTD.

- 11.1.7.1 Business overview

- 11.1.7.2 Products offered

- 11.1.8 EMERSON

- 11.1.8.1 Business overview

- 11.1.8.2 Products offered

- 11.1.9 COHERENT CORP.

- 11.1.9.1 Business overview

- 11.1.9.2 Products offered

- 11.1.9.3 Recent developments

- 11.1.9.3.1 Product launches

- 11.1.10 OC OERLIKON MANAGEMENT AG

- 11.1.10.1 Business overview

- 11.1.10.2 Products offered

- 11.1.10.3 Recent developments

- 11.1.10.3.1 Expansions

- 11.1.11 NIKON CORPORATION

- 11.1.11.1 Business overview

- 11.1.11.2 Products offered

- 11.1.11.3 Recent developments

- 11.1.11.3.1 Product launches

- 11.1.11.3.2 Deals

- 11.1.12 DURR GROUP

- 11.1.12.1 Business overview

- 11.1.12.2 Products offered

- 11.1.12.3 Recent developments

- 11.1.12.3.1 Deals

- 11.1.13 MULTIVAC

- 11.1.13.1 Business overview

- 11.1.13.2 Products offered

- 11.1.14 MIKRON

- 11.1.14.1 Business overview

- 11.1.14.2 Products offered

- 11.1.15 STRATASYS LTD.

- 11.1.15.1 Business overview

- 11.1.15.2 Products offered

- 11.1.1 ABB

- 11.2 OTHER PLAYERS

- 11.2.1 BORCHE NORTH AMERICA INC.

- 11.2.2 R.P. INJECTION SRL

- 11.2.3 LASERAX

- 11.2.4 LITHIUM LASERS SRL

- 11.2.5 AXIAL3D

- 11.2.6 MOLD HOTRUNNER SOLUTIONS LTD.

- 11.2.7 ATLAS ENVIRONMENTS, LTD.

- 11.2.8 BERKSHIRE CORPORATION

- 11.2.9 CLEAN ROOMS INTERNATIONAL, INC.

- 11.2.10 CLEAN AIR TECHNOLOGY, INC.

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS