|

시장보고서

상품코드

1863604

채혈 디바이스 시장 예측(-2030년) : 제품별, 방법별, 용도별, 최종사용자별, 지역별Blood Collection Devices Market By Product (Tubes (Plasma, Serum), Needles & Syringes, Blood Bags, Monitors), Method, Application, End User - Global Forecast to 2030 |

||||||

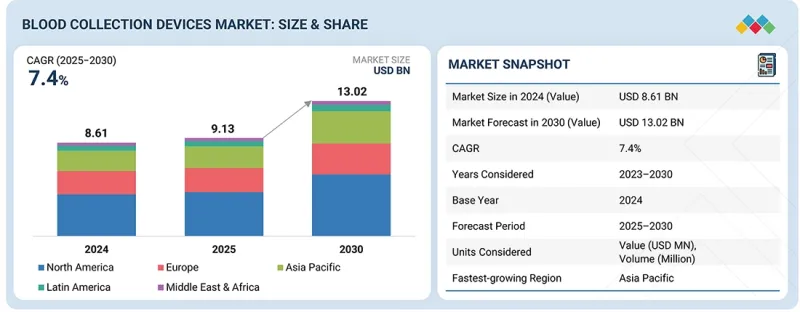

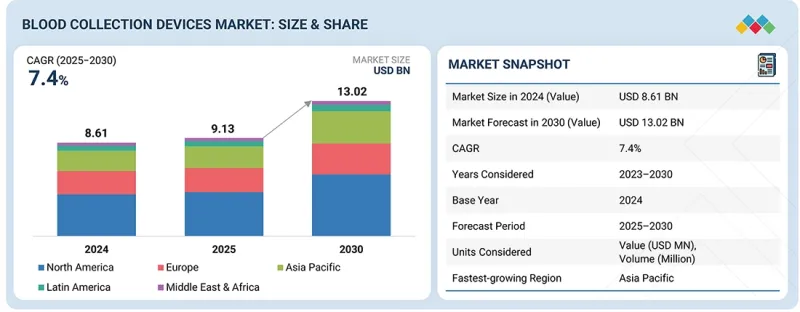

세계의 채혈 디바이스 시장 규모는 예측 기간 중 CAGR 7.4%로 성장하며, 2025년 91억 3,000만 달러에서 2030년에는 130억 2,000만 달러에 달할 것으로 전망되고 있습니다.

채혈 장치 시장의 성장은 몇 가지 주요 요인에 의해 주도되고 있습니다. 감염성 질환 증가 추세와 더불어 만성질환 및 생활습관병의 확산으로 인해 빈번하고 신뢰할 수 있는 혈액검사의 필요성이 높아지고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2033년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품별, 방법별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

동시에 전 세계에서 병원과 수술센터가 증가함에 따라 의료 인프라가 확대되고 효율적인 채혈 솔루션에 대한 수요가 증가하고 있습니다. 사고 및 외상 사례 증가로 인해 응급의료 및 수혈을 위한 신속하고 안전한 채혈의 필요성이 더욱 커지고 있습니다. 또한 혈액 샘플을 이용한 조기 암 감지 및 모니터링을 위한 액체생검 검사의 출현으로 샘플의 품질과 정확성을 보장하는 첨단 채혈 장비에 대한 수요가 증가하고 있습니다. 헌혈과 혈액 성분에 대한 인식과 수요 증가도 특히 신흥 지역에서 시장의 전반적인 확대에 기여하고 있습니다.

시중에서 판매되는 채혈 장비는 수동식 및 자동식 두 가지 주요 방법을 기반으로 합니다. 자동 채혈 부문은 예측 기간 중 높은 CAGR을 나타낼 것으로 예측됩니다. 자동 채혈 부문의 성장은 보다 안전한 시술에 대한 수요 증가와 첨단 채혈 제품의 보급에 기인하는 것으로 보입니다. 그러나 채혈 장치 시장에서 가장 널리 사용되는 방법은 수동 채혈입니다. 이 부문은 2024년 시장에서 가장 큰 점유율을 차지했습니다.

2024년 기준, 병원, 외래수술센터(ASC), 요양 시설 부문이 채혈 장비 시장에서 가장 큰 점유율을 차지했습니다.

2024년 병원, 수술센터, 요양시설 부문이 채혈 장치 시장에서 가장 큰 점유율을 차지했습니다. 감염 발생률 증가, 외상 환자 수 증가, 제왕절개 및 장기 이식 증가로 인해 병원 시설에서 채혈 장치 및 장비에 대한 수요가 확보되고 있습니다. 이 외에도 기능 확장이 시장 성장을 주도하고 있습니다.

2024년, 북미가 채혈 장치 시장을 장악했습니다.

미국과 캐나다로 구성된 북미는 2024년 세계 채혈 장치 시장에서 가장 큰 점유율을 차지할 것으로 예상되며, 유럽이 그 뒤를 이을 것으로 예측됩니다. 생활습관병 증가, 혈액질환의 발생률 증가, 의료시설의 확충, 주요 제조업체의 지역 진출 등의 요인이 북미 혈액채혈기기 시장의 성장을 가속하고 있습니다. 그러나 예측 기간 중 아시아태평양 시장이 가장 높은 CAGR로 성장할 것으로 예측됩니다.

세계의 채혈 디바이스 시장에 대해 조사했으며, 제품별, 방법별, 용도별, 최종사용자별, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

- 서론

- 시장 역학

- 고객 비즈니스에 영향을 미치는 동향/파괴적 변화

- 가격 분석

- 밸류체인 분석

- 공급망 분석

- 에코시스템 분석

- 투자와 자금조달 시나리오

- 기술 분석

- 특허 분석

- 무역 분석

- 2025-2026년의 주요 컨퍼런스와 이벤트

- 사례 연구 분석

- 규제 분석

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 생성형 AI가 채혈 디바이스 시장에 미치는 영향

- 2025년 미국 관세가 채혈 기기 시장에 미치는 영향

제6장 채혈 디바이스 시장(제품별)

- 서론

- 채혈관

- 바늘과 주사기

- 혈액 백

- 채혈 시스템/모니터

- 랜싯

제7장 채혈 디바이스 시장(방법별)

- 서론

- 수동 채혈

- 자동 채혈

제8장 채혈 디바이스 시장(용도별)

- 서론

- 진단

- 치료

제9장 채혈 디바이스 시장(최종사용자별)

- 서론

- 병원, 외래 수술 센터, 요양시설

- 진단 및 병리학 검사실

- 혈액은행

- 기타

제10장 채혈 디바이스 시장(지역별)

- 서론

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 거시경제 전망

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 일본

- 중국

- 인도

- 호주

- 기타

- 라틴아메리카

- 라틴아메리카의 거시경제 전망

- 중동 및 아프리카

- 감염증의 만연과 헬스케어 인프라의 확대가 시장의 성장을 지원한다.

- 중동 및 아프리카의 거시경제 전망

제11장 경쟁 구도

- 개요

- 주요 참여 기업의 전략/강점

- 매출 분석, 2022-2024년

- 시장 점유율 분석, 2024년

- 기업 평가와 재무 지표

- 브랜드/제품 비교

- 기업 평가 매트릭스 : 주요 참여 기업, 2024년

- 기업 평가 매트릭스(스타트업/중소기업), 2024년

- 경쟁 시나리오

제12장 기업 개요

- 주요 참여 기업

- BECTON, DICKINSON AND COMPANY(BD)

- TERUMO BCT, INC.

- FRESENIUS KABI AG

- GRIFOLS, S.A.

- NIPRO CORPORATION

- SARSTEDT AG & CO. KG

- MACOPHARMA

- HAEMONETICS CORPORATION

- ICU MEDICAL, INC.

- CARDINAL HEALTH

- RETRACTABLE TECHNOLOGIES, INC.

- GREINER HOLDING AG

- 기타 기업

- LIUYANG SANLI MEDICAL TECHNOLOGY DEVELOPMENT CO., LTD.

- FL MEDICAL S.R.L.

- AB MEDICAL CO., LTD.

- APTACA SPA

- JIANGSU MICSAFE MEDICAL TECHNOLOGY CO., LTD.

- DISERA TIBBI MALZEME LOJISTIK SANAYI VE TICARET A.S

- AJOSHA BIO TEKNIK PVT. LTD.

- PREQ SYSTEMS

- CML BIOTECH LTD

- LMB TECHNOLOGIE GMBH

- MITRA INDUSTRIES PRIVATE LIMITED

- NEOMEDIC LIMITED

- MHC MEDICAL PRODUCTS, LLC

제13장 부록

KSA 25.11.20The global blood collection devices market is projected to reach USD 13.02 billion by 2030 from USD 9.13 billion in 2025, at a CAGR of 7.4% during the forecast period. The blood collection devices market is driven by several key factors. The rising prevalence of infectious diseases, along with chronic and lifestyle-related conditions, has increased the need for frequent and reliable blood testing.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2033 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product, Method, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

At the same time, the growing number of hospitals and surgical centers worldwide is expanding healthcare infrastructure, creating greater demand for efficient blood collection solutions. The rise in accidents and trauma cases has further heightened the need for rapid and safe blood collection for emergency care and transfusions. Additionally, the emergence of liquid biopsy tests, which use blood samples for early cancer detection and monitoring, is driving the demand for advanced collection devices that ensure sample quality and accuracy. Growing awareness and the demand for blood donations and blood components are also contributing to the overall expansion of the market, particularly in emerging regions.

The automated blood collection segment is expected to grow at the highest rate during the forecast period.

The blood collection devices available in the market are based on two major methods: manual and automated blood collection methods. The automated blood collection segment is projected to register a higher CAGR during the forecast period. The growth of the automated blood collection segment can be attributed to the increasing demand for safer procedures and the availability of advanced blood collection products. However, the most widely used method in the blood collection devices market is manual blood collection. This segment accounted for the largest share of the market in 2024.

The hospitals, ASCs, and nursing homes segment accounted for the largest share of the blood collection devices market in 2024.

The hospitals, ASCs, and nursing homes segment accounted for the largest share of the blood collection devices market in 2024. The increasing incidence of infectious diseases and the rise in the number of trauma cases, as well as C-sections and organ transplants, have ensured the demand for blood collection equipment and devices in hospital facilities. This, along with expanded capabilities, is driving the growth of this market.

North America dominated the blood collection devices market in 2024.

North America, comprising the US and Canada, accounted for the largest share of the global blood collection devices market in 2024, followed by Europe. Factors such as the increasing prevalence of lifestyle diseases and the rising incidence of blood disorders, better healthcare facilities, and the presence of major manufacturers in the region are stimulating the growth of the blood collection devices market in North America. However, the Asia Pacific market is expected to grow at the highest CAGR during the forecast period.

Breakdown of supply-side primary interviews, by company type, designation, and region:

- By Company Type: Tier 1 (40%), Tier 2 (30%), and Tier 3 (30%)

- By Designation: C-level Executives (27%), Director-level Executives (18%), and Others (55%)

- By Region: North America (51%), Europe (21%), Asia Pacific (18%), Latin America (6%), and the Middle East & Africa (4%)

List of Companies Profiled in the Report

- Fresenius Kabi AG (Germany)

- Becton, Dickinson and Company (US)

- Terumo BCT, Inc. (Japan)

- Greiner Holding (Austria)

- Cardinal Health (US)

- Haemonetics Corporation (US)

- Grifols, S.A (Spain)

- Nipro Medical Corporation (Japan)

- SARSTEDT AG & Co. (Germany)

- Macopharma (France)

- ICU Medical, Inc. (US)

- Retractable Technologies, Inc. (US)

- Liuyang Sanli Medical Technology Development (China)

- F.L. Medical s.r.l. (Italy)

- AB Medical Co., Ltd. (South Korea)

- Aptaca SPA (Italy)

- Jiangsu Micsafe Medical Technology Co., Ltd. (China)

- Disera Tibbi Malzeme Lojistik Sanayi Ve Ticaret A.S (Turkey)

- Ajosha Bio Teknik Pvt. Ltd. (India)

- Preq Systems (India)

- CML Biotech (India)

- Lmb Technologie GmbH (Germany)

- Mitra Industries Private Limited (India)

- Neomedic Limited (UK)

Research Coverage

This research report categorizes the blood collection devices market by product (blood collection tubes, needles & syringes, blood bags, blood collection systems/monitors, and lancets), method (manual blood collection and automated blood collection), application (diagnostic applications and therapeutic applications), end user (hospitals, ASCs, and nursing homes; blood banks; diagnostic & pathology laboratories; and other end users), and region (North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, opportunities, and challenges, influencing the growth of the blood collection devices market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, key strategies, acquisitions, and partnerships. This report covers the competitive analysis of upcoming startups in the blood collection devices market ecosystem.

Key Benefits of Buying the Report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall blood collection devices market and subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (rising prevalence of infectious diseases and chronic & lifestyle diseases, increasing number of hospitals and surgical centers, rise in accidents and trauma cases, emergence of liquid biopsy tests, and growing demand for and awareness of blood donations and blood components), restraints (high cost of automated blood collection devices), opportunities (increasing demand for apheresis, lucrative opportunities in emerging economies, and advancements in blood collection procedures and products), and challenges (complex storage and shipping and lack of skilled professionals) influencing the growth of the blood collection devices market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the blood collection devices market.

- Market Development: Comprehensive information about lucrative markets; the report analyzes the blood collection devices market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the blood collection devices market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players, such as Fresenius Kabi AG (Germany), Becton, Dickinson and Company (ND) (US), Terumo BCT, Inc. (Japan), Greiner Holding AG (Austria), Cardinal Health (US), Haemonetics Corporation (US), Grifols, S.A. (Spain), Nipro Medical Corporation (Japan), SARSTEDT AG & Co. KG (Germany), Macopharma (France), ICU Medical, Inc. (US), and Retractable Technologies, Inc. (US), among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY RESEARCH

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY RESEARCH

- 2.1.2.1 Primary sources

- 2.1.2.2 Key objectives of primary research

- 2.1.2.3 Key data from primary sources

- 2.1.2.4 Key industry insights

- 2.1.1 SECONDARY RESEARCH

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach 2: Presentations of companies and primary interviews

- 2.2.1.2 Growth forecast

- 2.2.2 TOP-DOWN APPROACH

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.4 MARKET SHARE ESTIMATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.5.1 PARAMETRIC ASSUMPTIONS

- 2.5.2 GROWTH RATE ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 BLOOD COLLECTION DEVICES MARKET OVERVIEW

- 4.2 BLOOD COLLECTION DEVICES MARKET, BY PRODUCT, 2025 VS. 2030

- 4.3 BLOOD COLLECTION DEVICES MARKET, BY METHOD, 2025 VS. 2030

- 4.4 BLOOD COLLECTION DEVICES MARKET, BY APPLICATION, 2025 VS. 2030

- 4.5 BLOOD COLLECTION DEVICES MARKET, BY END USER, 2025 VS. 2030

- 4.6 BLOOD COLLECTION DEVICES MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising prevalence of infectious diseases and chronic & lifestyle diseases

- 5.2.1.2 Increasing number of hospitals and surgical centers

- 5.2.1.3 Rise in accidents and trauma cases

- 5.2.1.4 Emergence of liquid biopsy tests

- 5.2.1.5 Growing demand for and awareness of blood donations and blood components

- 5.2.2 RESTRAINTS

- 5.2.2.1 Rising costs of automated blood collection devices

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing demand for apheresis

- 5.2.3.2 Lucrative opportunities in emerging economies

- 5.2.3.3 Advancements in blood collection

- 5.2.4 CHALLENGES

- 5.2.4.1 Complex storage and shipping

- 5.2.4.2 Lack of skilled professionals

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND, BY PRODUCT

- 5.4.2 AVERAGE SELLING PRICE TREND OF BLOOD COLLECTION DEVICES, BY KEY PLAYER

- 5.4.3 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Core blood collection devices

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Sampling and collection kits

- 5.9.1 KEY TECHNOLOGIES

- 5.10 PATENT ANALYSIS

- 5.11 TRADE ANALYSIS

- 5.11.1 IMPORT DATA

- 5.11.2 EXPORT DATA

- 5.12 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.13 CASE STUDY ANALYSIS

- 5.13.1 CASE STUDY 1: REDUCING HOSPITAL-ONSET BACTEREMIA USING PIVO NEEDLELESS BLOOD COLLECTION

- 5.13.2 CASE STUDY 2: ADOPTION OF PIVO NEEDLE-FREE BLOOD COLLECTION DEVICE AT VIRGINIA MASON MEDICAL CENTER

- 5.13.3 CASE STUDY 3: AUTONOMOUS BLOOD COLLECTION ENHANCES EFFICIENCY AND PATIENT EXPERIENCE AT ST. ANTONIUS HOSPITAL

- 5.14 REGULATORY ANALYSIS

- 5.14.1 REGULATORY LANDSCAPE

- 5.14.1.1 North America

- 5.14.1.1.1 US

- 5.14.1.1.2 Canada

- 5.14.1.2 Europe

- 5.14.1.2.1 Germany

- 5.14.1.2.2 UK

- 5.14.1.2.3 France

- 5.14.1.2.4 Italy

- 5.14.1.2.5 Spain

- 5.14.1.3 Asia Pacific

- 5.14.1.3.1 China

- 5.14.1.3.2 Japan

- 5.14.1.3.3 India

- 5.14.1.4 Latin America

- 5.14.1.4.1 Brazil

- 5.14.1.4.2 Mexico

- 5.14.1.5 Middle East

- 5.14.1.6 Africa

- 5.14.1.1 North America

- 5.14.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14.1 REGULATORY LANDSCAPE

- 5.15 PORTER'S FIVE FORCES ANALYSIS

- 5.15.1 BARGAINING POWER OF SUPPLIERS

- 5.15.2 BARGAINING POWER OF BUYERS

- 5.15.3 THREAT OF NEW ENTRANTS

- 5.15.4 THREAT OF SUBSTITUTES

- 5.15.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.16 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.16.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.16.2 BUYING CRITERIA

- 5.17 IMPACT OF GENERATIVE AI ON BLOOD COLLECTION DEVICES MARKET

- 5.17.1 INTRODUCTION

- 5.17.2 MARKET POTENTIAL FOR BLOOD COLLECTION DEVICES

- 5.17.3 AI USE CASES

- 5.17.4 KEY COMPANIES IMPLEMENTING AI

- 5.17.5 FUTURE OF GENERATIVE AI IN BLOOD COLLECTION DEVICES MARKET

- 5.18 IMPACT OF 2025 US TARIFFS ON BLOOD COLLECTION DEVICES MARKET

- 5.18.1 INTRODUCTION

- 5.18.2 KEY TARIFF RATES

- 5.18.3 PRICE IMPACT ANALYSIS

- 5.18.4 IMPACT ON COUNTRY/REGION

- 5.18.4.1 North America

- 5.18.4.2 Europe

- 5.18.4.3 Asia Pacific

- 5.18.5 IMPACT ON END-USE INDUSTRIES

- 5.18.5.1 Hospitals, ambulatory surgical centers, and nursing homes

- 5.18.5.2 Diagnostic & pathology labs

- 5.18.5.3 Blood banks

6 BLOOD COLLECTION DEVICES MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- 6.2 BLOOD COLLECTION TUBES

- 6.2.1 BLOOD COLLECTION TUBES MARKET, BY TYPE

- 6.2.1.1 Plasma/Whole-blood tubes

- 6.2.1.1.1 EDTA tubes

- 6.2.1.1.2 Heparin tubes

- 6.2.1.1.3 Coagulation tubes

- 6.2.1.1.4 Glucose tubes

- 6.2.1.1.5 ESR tubes

- 6.2.1.2 Serum tubes

- 6.2.1.2.1 Need for high-quality serum specimens to fuel market

- 6.2.1.1 Plasma/Whole-blood tubes

- 6.2.2 BLOOD COLLECTION TUBES, BY SYSTEM TYPE

- 6.2.2.1 Vacuum tubes

- 6.2.2.1.1 Need to minimize blood exposure to promote growth

- 6.2.2.2 Non-vacuum tubes

- 6.2.2.2.1 Cost constraints to contribute to growth

- 6.2.2.1 Vacuum tubes

- 6.2.1 BLOOD COLLECTION TUBES MARKET, BY TYPE

- 6.3 NEEDLES & SYRINGES

- 6.3.1 RISING ADOPTION OF SAFETY BLOOD COLLECTION SETS TO BOLSTER GROWTH

- 6.4 BLOOD BAGS

- 6.4.1 INCREASING BLOOD DONATIONS WORLDWIDE TO AUGMENT GROWTH

- 6.5 BLOOD COLLECTION SYSTEMS/MONITORS

- 6.5.1 GROWING CONCERNS REGARDING BLOOD SAFETY AND BLOOD SHORTAGE TO PROPEL MARKET

- 6.6 LANCETS

- 6.6.1 HIGH CONVENIENCE AND MINIMAL PAIN TO CONTRIBUTE TO GROWTH

7 BLOOD COLLECTION DEVICES MARKET, BY METHOD

- 7.1 INTRODUCTION

- 7.2 MANUAL BLOOD COLLECTION

- 7.2.1 RISING INCLINATION TOWARD SELF-CARE AND INCREASING NUMBER OF DIAGNOSTIC CENTERS TO DRIVE MARKET

- 7.3 AUTOMATED BLOOD COLLECTION

- 7.3.1 INCREASING DEMAND FOR SAFER COLLECTION PROCEDURES AND AVAILABILITY OF ADVANCED BLOOD-COLLECTING PRODUCTS TO AID GROWTH

8 BLOOD COLLECTION DEVICES MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 DIAGNOSTIC APPLICATIONS

- 8.2.1 RISING INCIDENCE OF INFECTIOUS DISEASES TO SPUR GROWTH

- 8.3 THERAPEUTIC APPLICATIONS

- 8.3.1 RISING PREVALENCE OF HEMATOLOGICAL DISORDERS TO SUPPORT GROWTH

9 BLOOD COLLECTION DEVICES MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.2 HOSPITALS, AMBULATORY SURGICAL CENTERS, AND NURSING HOMES

- 9.2.1 INCREASING NUMBER OF SURGICAL PROCEDURES AND HOSPITALS TO FOSTER GROWTH

- 9.3 DIAGNOSTIC & PATHOLOGY LABORATORIES

- 9.3.1 RISING NUMBER OF TEST VOLUMES TO CONTRIBUTE TO GROWTH

- 9.4 BLOOD BANKS

- 9.4.1 INCREASING AWARENESS ABOUT BLOOD DONATION AND USE OF BLOOD FOR TREATING CLINICAL CONDITIONS TO BOOST MARKET

- 9.5 OTHER END USERS

10 BLOOD COLLECTION DEVICES MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 10.2.2 US

- 10.2.2.1 High healthcare expenditure and increasing prevalence of cancer to expedite growth

- 10.2.3 CANADA

- 10.2.3.1 Growing volume of surgical procedures to support growth

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 10.3.2 GERMANY

- 10.3.2.1 Increasing healthcare expenditure and new blood tests to aid growth

- 10.3.3 FRANCE

- 10.3.3.1 Growing number of new diagnostic tests and prevalence of cardiovascular diseases to drive market

- 10.3.4 UK

- 10.3.4.1 Increasing prevalence of lifestyle diseases and HIV to spur growth

- 10.3.5 ITALY

- 10.3.5.1 Rising blood donation to contribute to growth

- 10.3.6 SPAIN

- 10.3.6.1 Rise in organ transplants to aid growth

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 10.4.2 JAPAN

- 10.4.2.1 Rapid increase in aging population to accelerate growth

- 10.4.3 CHINA

- 10.4.3.1 Growing demand for blood components to facilitate growth

- 10.4.4 INDIA

- 10.4.4.1 Rise in government initiatives for healthcare infrastructure to accelerate growth

- 10.4.5 AUSTRALIA

- 10.4.5.1 Growing emphasis on improving access to diagnostic and preventive healthcare to fuel market

- 10.4.6 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 PREVALENCE OF INFECTIOUS DISEASES AND GROWING HEALTHCARE INFRASTRUCTURE TO SUPPORT MARKET GROWTH

- 10.6.2 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.2.1 OVERVIEW OF KEY STRATEGIES DEPLOYED BY MAJOR PLAYERS

- 11.3 REVENUE ANALYSIS, 2022-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS

- 11.6 BRAND/PRODUCT COMPARISON

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.7.5.1 Company footprint

- 11.7.5.2 Region footprint

- 11.7.5.3 Product footprint

- 11.7.5.4 Application footprint

- 11.7.5.5 Method footprint

- 11.8 COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- 11.8.5 COMPETITIVE BENCHMARKING

- 11.8.5.1 Detailed list of key startups/SMEs

- 11.8.5.2 Competitive benchmarking of key startups/SMEs

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES AND APPROVALS

- 11.9.2 DEALS

- 11.9.3 EXPANSIONS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 BECTON, DICKINSON AND COMPANY (BD)

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches and approvals

- 12.1.1.3.2 Expansions

- 12.1.1.3.3 Deals

- 12.1.1.4 MnM view

- 12.1.1.4.1 Key strengths

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 TERUMO BCT, INC.

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Key strengths

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 FRESENIUS KABI AG

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches and approvals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 GRIFOLS, S.A.

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.5 NIPRO CORPORATION

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.6 SARSTEDT AG & CO. KG

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.7 MACOPHARMA

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.8 HAEMONETICS CORPORATION

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Deals

- 12.1.8.3.2 Product launches and approvals

- 12.1.8.3.3 Expansions

- 12.1.9 ICU MEDICAL, INC.

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.10 CARDINAL HEALTH

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.11 RETRACTABLE TECHNOLOGIES, INC.

- 12.1.11.1 Business overview

- 12.1.11.2 Products offered

- 12.1.12 GREINER HOLDING AG

- 12.1.12.1 Business overview

- 12.1.12.2 Products offered

- 12.1.1 BECTON, DICKINSON AND COMPANY (BD)

- 12.2 OTHER PLAYERS

- 12.2.1 LIUYANG SANLI MEDICAL TECHNOLOGY DEVELOPMENT CO., LTD.

- 12.2.2 FL MEDICAL S.R.L.

- 12.2.3 AB MEDICAL CO., LTD.

- 12.2.4 APTACA SPA

- 12.2.5 JIANGSU MICSAFE MEDICAL TECHNOLOGY CO., LTD.

- 12.2.6 DISERA TIBBI MALZEME LOJISTIK SANAYI VE TICARET A.S

- 12.2.7 AJOSHA BIO TEKNIK PVT. LTD.

- 12.2.8 PREQ SYSTEMS

- 12.2.9 CML BIOTECH LTD

- 12.2.10 LMB TECHNOLOGIE GMBH

- 12.2.11 MITRA INDUSTRIES PRIVATE LIMITED

- 12.2.12 NEOMEDIC LIMITED

- 12.2.13 MHC MEDICAL PRODUCTS, LLC

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS