|

시장보고서

상품코드

1869550

보안 솔루션 시장 예측(-2030년) : 시스템별, 서비스별, 업계별, 지역별Security Solutions Market by System (Fire Protection, Video Surveillance, Multi-technology Reader, Biometric Reader, Electronic Lock, Entrance Control, Intruder Alarm, Thermal Imaging), Service (Remote Monitoring, VSaaS, ACaaS) - Global Forecast to 2030 |

||||||

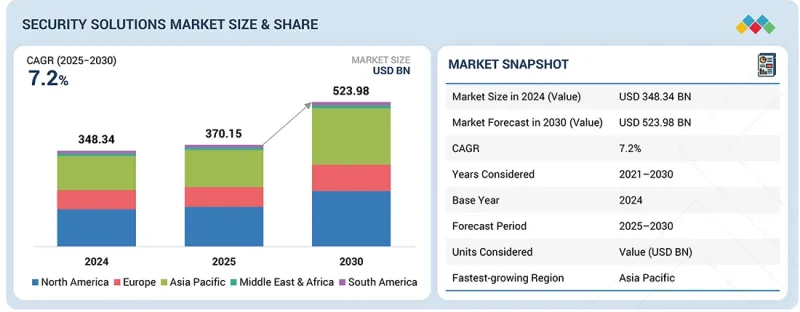

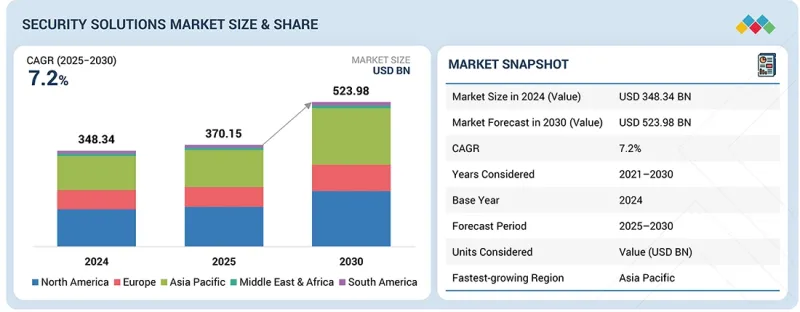

세계의 보안 솔루션 시장 규모는 2025년 3,701억 5,000만 달러에서 2030년까지 5,239억 8,000만 달러로, CAGR 7.2%로 성장할 것으로 예측됩니다.

AI를 활용한 감시 시스템 및 생체인식 출입통제의 급속한 보급이 보안 시스템의 정확성, 효율성, 신뢰성을 크게 향상시키며 성장을 촉진하고 있습니다. AI는 실시간 영상 분석, 얼굴 인식, 행동 감지를 통해 위협을 신속하게 식별하고 대응하는 동시에 오경보를 줄일 수 있습니다. 지문, 홍채, 얼굴 스캔을 이용한 생체인식 출입 통제는 위조나 회피가 어려운 높은 보안성과 편의성을 갖춘 인증 방법을 제공합니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 시스템별, 서비스별, 업계별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

이러한 기술들이 결합되어 상업용 및 주거용 시설의 고도화된 보호 요구사항을 충족하는 보다 스마트하고 자동화된 보안 솔루션을 제공함으로써 광범위한 도입을 촉진하고 전체 시장을 확대할 수 있습니다.

영상 감시 서비스는 다양한 분야에서 지속적인 실시간 모니터링과 강화된 보안을 제공할 수 있다는 점에서 가장 빠르게 성장하고 있습니다. 클라우드 기반 플랫폼은 원격 액세스, 쉬운 확장성, 초기 비용 절감을 통해 기업과 일반 가정 모두 이러한 서비스를 이용할 수 있도록 하고 있습니다. AI 기반 분석, 얼굴 인식, 자동 경고 등의 첨단 기술은 위협 감지의 정확도를 높이고 오보를 줄여 보다 신속한 대응을 가능하게 합니다. 강화된 규제 요건과 수사 과정에서 신뢰할 수 있는 증거의 필요성도 이러한 서비스에 대한 수요를 촉진하고 있습니다. 또한 구독형 및 관리형 비디오 감시 모델의 등장은 최소한의 초기 투자로 비용 효율적인 솔루션을 제공함으로써 모든 규모의 조직에 매력적으로 작용합니다. 안전과 자산 보호에 대한 관심이 높아지는 가운데, 비디오 감시 서비스는 유연하고 효율적이며 확장 가능한 자산 감시 및 보호 수단을 제공함으로써 보안 시장의 빠른 성장에 기여하고 있습니다.

직원, 기밀 데이터 및 귀중한 자산 보호에 대한 관심이 높아짐에 따라 상업 부문은 보안 솔루션에서 가장 빠른 성장세를 보이고 있습니다. 사무실에서는 부정한 접근을 방지하고 안전한 업무 환경을 유지하기 위해 출입통제, 영상감시, 침입감지 등 첨단 보안 대책이 요구됩니다. 강화된 규제 요건과 업계 컴플라이언스 기준도 기업이 종합적인 보안 시스템에 투자하도록 압박하는 요인으로 작용하고 있습니다. 스마트 빌딩의 보급과 IoT 통합으로 원격 모니터링이 가능한 효율적이고 자동화된 보안 솔루션의 도입이 진행되어 여러 거점에서의 운영을 지원하고 있습니다. 또한 소매, 의료, 금융, 물류 등 사무실 공간이 중요한 부문의 성장이 확장성과 사용자 정의가 가능한 보안 기술에 대한 수요를 견인하고 있습니다. 조직이 리스크 관리와 비즈니스 연속성을 우선시하는 가운데, 상업 부문에서는 혁신적이고 통합적인 보안 솔루션의 채택이 지속되고 있으며, 이는 전체 보안 시장의 급속한 확장을 촉진하고 있습니다.

미국은 첨단 기술 인프라, 높은 보안 의식, 다양한 분야의 막대한 투자로 북미 보안 솔루션 시장을 독점하고 있습니다. 이 국가에는 출입 통제, 영상 감시, 통합 보안 시스템 분야의 혁신을 주도하는 많은 주요 보안 기업이 있습니다. 금융, 의료, 정부 등 각 산업 분야의 엄격한 규제 프레임워크와 컴플라이언스 요건도 조직이 강력한 보안 조치를 도입하는 요인으로 작용하고 있습니다. 또한 도시화의 진전, 대규모 상업용 부동산 부문, 직장 및 주거 안전에 대한 관심 증가가 수요 증가에 기여하고 있습니다. 미국 시장에서는 AI, 클라우드 기반 솔루션, 생체인식 등 새로운 기술을 조기에 도입하여 이 지역 보안 솔루션 시장에서의 선도적 입지를 더욱 강화하고 있습니다.

세계의 보안 솔루션 시장에 대해 조사했으며, 시스템별, 서비스별, 업계별, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

- 서론

- 시장 역학

- 밸류체인 분석

- 에코시스템 분석

- 투자와 자금조달 시나리오

- 가격 분석

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 기술 분석

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 구매 프로세스에서 주요 이해관계자

- 구입 기준

- 사례 연구 분석

- 무역 분석

- 특허 분석

- 2025-2027년의 주요 컨퍼런스와 이벤트

- 관세 분석

- 기준과 규제 상황

- AI/생성형 AI가 보안 솔루션 시장에 미치는 영향

- 2025년 미국 관세가 보안 솔루션 시장에 미치는 영향

제6장 물리적 보안의 미래

- 서론

- 차세대 보안에서 AI, 드론, 로봇의 역할

- 스마트 시티의 출현

- 물리 보안과 사이버 보안의 융합

- 위협 방지를 위한 예측 분석의 동향

제7장 보안 솔루션 시장(시스템별)

- 서론

- 방화 시스템

- 비디오 감시 시스템

- 액세스 제어 시스템

- 입장 제어 시스템

- 침입자 경보 시스템

- 열 영상 시스템

제8장 보안 솔루션 시장(서비스별)

- 서론

- 방화 서비스

- 비디오 감시 서비스

- 액세스 제어 서비스

- 보안 시스템 통합 서비스

- 리모트 모니터링 서비스

제9장 보안 솔루션 시장(업계별)

- 서론

- 주택

- 상업

- 정부

- 운송

- 소매

- 은행·금융

- 교육

- 산업용

- 에너지·유틸리티

- 스포츠와 레저

- 헬스케어

- 군·방위

제10장 보안 솔루션 시장(지역별)

- 서론

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 멕시코

- 유럽

- 유럽의 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽

- 기타

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 중국

- 일본

- 한국

- 인도

- 호주

- 인도네시아

- 말레이시아

- 태국

- 베트남

- 기타

- 기타 지역

- 기타 지역의 거시경제 전망

- 중동

- 남미

- 아프리카

- 남아프리카공화국

- 기타

제11장 경쟁 구도

- 개요

- 주요 참여 기업의 전략/강점, 2021-2025년

- 매출 분석, 2020-2024년

- 시장 점유율 분석, 2024년

- 기업 평가와 재무 지표

- 브랜드 비교

- 기업 평가 매트릭스 : 주요 참여 기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 경쟁 시나리오

제12장 기업 개요

- 주요 참여 기업

- JOHNSON CONTROLS

- HONEYWELL INTERNATIONAL INC.

- ROBERT BOSCH GMBH

- ADT SECURITY SERVICES

- HANGZHOU HIKVISION DIGITAL TECHNOLOGY CO., LTD

- AXIS COMMUNICATIONS AB

- DAHUA TECHNOLOGY CO., LTD

- SECOM CO., LTD

- SIEMENS

- ASSA ABLOY

- KEENFINITY

- 기타 기업

- HALMA PLC

- HOCHIKI CORPORATION

- DORMAKABA GROUP

- TELEDYNE FLIR LLC

- ALLEGION PLC

- NICE S.P.A.

- GODREJ GROUP

- ALARM.COM

- MOTOROLA SOLUTIONS, INC.

- DALLMEIER ELECTRONIC GMBH & CO KG

- SECURITAS TECHNOLOGY

- GUNNEBO AB

- BRIVO SYSTEMS, LLC

- BRINKS HOME

- VERKADA INC.

제13장 부록

KSA 25.11.25The global security solutions market is projected to grow from USD 370.15 billion in 2025 to USD 523.98 billion by 2030, at a CAGR of 7.2%. The rapid adoption of AI-powered surveillance and biometric access control is fueling growth by significantly enhancing the accuracy, efficiency, and reliability of security systems. AI enables real-time video analytics, facial recognition, and behavior detection, allowing for quicker threat identification and response while reducing false alarms. Biometric access control, using fingerprint, iris, or facial scans, offers highly secure and convenient authentication methods that are difficult to forge or bypass.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By System, Services, Vertical and Region |

| Regions covered | North America, Europe, APAC, RoW |

Together, these technologies provide smarter, automated security solutions that meet the growing demand for advanced protection in both commercial and residential settings, driving widespread adoption and expanding the overall market.

"Video Surveillance service to grow at the fastest rate during the forecasted period"

Video surveillance services are growing fastest due to their ability to provide continuous, real-time monitoring and enhanced security across various sectors. Cloud-based platforms enable remote access, easy scalability, and lower upfront costs, making these services accessible to both businesses and homeowners. Advanced technologies, such as AI-driven analytics, facial recognition, and automated alerts, improve the accuracy of threat detection and reduce false alarms, leading to faster responses. Increasing regulatory requirements and the need for reliable evidence in investigations also drive demand for these services. Moreover, the rise of subscription-based and managed video surveillance models offers cost-effective solutions that require minimal initial investment, appealing to organizations of all sizes. As concerns about safety and asset protection continue to rise, video surveillance services offer a flexible, efficient, and scalable way to monitor and secure properties, contributing to their rapid growth in the security market.

"Commercial segment to grow at the fastest rate during the forecasted period. "

The commercial segment is experiencing the fastest growth in security solutions due to heightened concerns about safeguarding employees, sensitive data, and valuable assets. Offices require advanced security measures such as access control, video surveillance, and intrusion detection to prevent unauthorized access and maintain a safe working environment. Increasing regulatory requirements and industry compliance standards further compel businesses to invest in comprehensive security systems. The rise of smart buildings and IoT integration allows offices to implement more efficient, automated security solutions that can be monitored remotely, supporting multi-location operations. Additionally, the growth of sectors like retail, healthcare, finance, and logistics-where office spaces are critical-drives demand for scalable and customizable security technologies. As organizations prioritize risk management and business continuity, the commercial segment continues to adopt innovative and integrated security solutions, fueling its rapid expansion within the overall security market.

"US is expected to hold the most prominent market share in North America during the forecast period."

The US dominates the North American security solutions market due to its advanced technological infrastructure, high security awareness, and substantial investments across various sectors. The country hosts many leading security companies that drive innovation in access control, video surveillance, and integrated security systems. Strict regulatory frameworks and compliance requirements in industries like finance, healthcare, and government also push organizations to adopt robust security measures. Additionally, widespread urbanization, a large commercial real estate sector, and the increasing focus on workplace and residential safety contribute to strong demand. The US market's early adoption of emerging technologies such as AI, cloud-based solutions, and biometrics further strengthens its leadership position in the region's security solutions landscape.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the security solutions marketplace.

- By Company Type: Tier 1 - 40%, Tier 2 - 35%, and Tier 3 - 25%

- By Designation: C-level Executives - 45%, Directors - 35%, and Others - 20%

- By Region: North America - 45%, Europe - 25%, Asia Pacific - 20%, and RoW - 10%

The study includes an in-depth competitive analysis of these key players in the security solutions market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the security solutions market by system, services, vertical, and region (North America, Europe, Asia Pacific, RoW). The report covers detailed information regarding major factors influencing market growth, such as drivers, restraints, challenges, and opportunities. A thorough analysis of the key industry players has provided insights into their business overview, solutions and services, key strategies, contracts, partnerships, and agreements. Product and service launches, acquisitions, and recent developments associated with the security solutions market. This report covers a competitive analysis of upcoming startups in the security solutions market ecosystem.

Reasons to Buy This Report

The report will help market leaders and new entrants with information on the closest approximations of the revenue numbers for the security solutions market and subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Increasing concerns regarding public safety and infrastructure protection, rapid adoption of AI-powered surveillance and biometric access control is redefining global security standards, rising incidents of theft, vandalism, and unauthorized access, expansion of smart infrastructure and smart city projects globally, modernization of physical security and access control systems), restraints (Concerns over privacy and data protection regulations, risk of system vulnerabilities and exploits, complexity in integration with existing infrastructure), opportunities (Increasing demand for remote monitoring and surveillance solutions, growing adoption of cloud-based security solutions, requirement for robust security in retail and commercial sectors, expansion in emerging markets), and challenges (Risk of rapid technological changes and obsolescence, complex regulatory landscape and compliance challenges, high initial costs) influencing the growth of the security solutions market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the security solutions market

- Market Development: Comprehensive information about lucrative markets with an analysis of the security solutions market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the security solutions market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the security solutions market, such as Johnson Controls (Ireland), Honeywell International Inc (US), Robert Bosch GmbH (Germany), ADT Security Services (US), and Hangzhou Hikvision Digital Technology Co., Ltd (China).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY AND PRIMARY RESEARCH

- 2.1.2 SECONDARY DATA

- 2.1.2.1 List of key secondary sources

- 2.1.2.2 Key data from secondary sources

- 2.1.3 PRIMARY DATA

- 2.1.3.1 List of primary interview participants

- 2.1.3.2 Key data from primary sources

- 2.1.3.3 Key industry insights

- 2.1.3.4 Breakdown of primaries

- 2.2 FACTOR ANALYSIS

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- 2.3.1.1 Approach to estimate market size using bottom-up analysis (demand side)

- 2.3.2 TOP-DOWN APPROACH

- 2.3.2.1 Approach to estimate market size using top-down analysis (supply side)

- 2.3.1 BOTTOM-UP APPROACH

- 2.4 DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SECURITY SOLUTIONS MARKET

- 4.2 SECURITY SOLUTIONS MARKET, BY SYSTEM

- 4.3 SECURITY SOLUTIONS MARKET, BY SERVICE

- 4.4 SECURITY SOLUTIONS MARKET, BY VERTICAL AND REGION

- 4.5 SECURITY SOLUTIONS MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing concerns regarding public safety and infrastructure protection

- 5.2.1.2 Adoption of AI-powered surveillance and biometric access control

- 5.2.1.3 Rising incidents of theft, vandalism, and unauthorized access

- 5.2.1.4 Expansion of smart infrastructure and smart city projects

- 5.2.1.5 Modernization of physical security and access control systems

- 5.2.2 RESTRAINTS

- 5.2.2.1 Concerns regarding privacy and data protection regulations

- 5.2.2.2 Risks associated with unauthorized access

- 5.2.2.3 Complexity of integrating modern security solutions with existing infrastructure

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing adoption of remote monitoring

- 5.2.3.2 Deployment of cloud-based security solutions

- 5.2.3.3 Expansion of security requirements in retail and commercial sectors

- 5.2.3.4 Rapid urbanization in developed countries

- 5.2.4 CHALLENGES

- 5.2.4.1 Competitive pressure for technological updates

- 5.2.4.2 Complex regulatory landscape and compliance challenges

- 5.2.4.3 High initial costs

- 5.2.1 DRIVERS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 INVESTMENT AND FUNDING SCENARIO

- 5.6 PRICING ANALYSIS

- 5.6.1 PRICING RANGE OF SECURITY SOLUTIONS OFFERED BY KEY PLAYERS, BY SYSTEM, 2024

- 5.6.2 AVERAGE SELLING PRICE TREND OF SECURITY SOLUTIONS, BY SYSTEM, 2020-2024

- 5.6.3 AVERAGE SELLING PRICE TREND OF SECURITY SOLUTIONS, BY REGION, 2020-2024

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 Video surveillance

- 5.8.1.2 Biometrics

- 5.8.1.3 AI and ML

- 5.8.1.4 Wireless technologies

- 5.8.2 COMPLEMENTARY TECHNOLOGIES

- 5.8.2.1 Integrated security management systems

- 5.8.2.2 Physical and cyber convergence

- 5.8.2.3 GIS integration

- 5.8.2.4 Incident response platforms

- 5.8.3 ADJACENT TECHNOLOGIES

- 5.8.3.1 IoT security

- 5.8.3.2 Edge computing security

- 5.8.3.3 Behavioral analytics

- 5.8.1 KEY TECHNOLOGIES

- 5.9 PORTER'S FIVE FORCES ANALYSIS

- 5.10 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.11 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.12 BUYING CRITERIA

- 5.13 CASE STUDY ANALYSIS

- 5.13.1 AUTOMATED SURVEILLANCE SYSTEM ENHANCES THREAT DETECTION AND RESPONSE FOR FPSO OPERATIONS

- 5.13.2 HONEYWELL DELIVERS ADVANCED FIRE AND SECURITY ECOSYSTEM FOR DUBAI MALL

- 5.13.3 BOSCH DEPLOYS INTELLIGENT VIDEO SURVEILLANCE SYSTEM FOR STADIUM-WIDE SECURITY

- 5.13.4 AXIS COMMUNICATIONS DELIVERS INTEGRATED VIDEO SURVEILLANCE ACROSS THE SHARD

- 5.13.5 AVIGILON ALTA SOLUTION UNIFIES AND STRENGTHENS VIDEO SURVEILLANCE FOR SUPERDRY

- 5.14 TRADE ANALYSIS

- 5.14.1 IMPORT SCENARIO (HS CODE 854231)

- 5.14.2 EXPORT SCENARIO (HS CODE 854231)

- 5.15 PATENT ANALYSIS

- 5.16 KEY CONFERENCES AND EVENTS, 2025-2027

- 5.17 TARIFF ANALYSIS

- 5.18 STANDARDS AND REGULATORY LANDSCAPE

- 5.18.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.18.2 STANDARDS AND REGULATIONS RELATED TO SECURITY SOLUTIONS MARKET

- 5.18.2.1 ISO 27001 - Information Security Management

- 5.18.2.2 UL 2900 - Standard for Software Cybersecurity for Network-Connectable Products

- 5.18.2.3 EN 50130 Series - Alarm Systems

- 5.18.2.4 BS EN 50131 Series - Alarm Systems

- 5.18.2.5 IEC 62676

- 5.18.3 GOVERNMENT REGULATIONS

- 5.18.3.1 US

- 5.18.3.2 Canada

- 5.18.3.3 Europe

- 5.18.3.4 UK

- 5.18.3.5 Japan

- 5.18.3.6 India

- 5.19 IMPACT OF AI/GEN AI ON SECURITY SOLUTIONS MARKET

- 5.19.1 INTRODUCTION

- 5.20 IMPACT OF 2025 US TARIFF ON SECURITY SOLUTIONS MARKET

- 5.20.1 INTRODUCTION

- 5.20.2 KEY TARIFF RATES

- 5.20.3 PRICE IMPACT ANALYSIS

- 5.20.4 IMPACT ON COUNTRIES/REGIONS

- 5.20.4.1 US

- 5.20.4.2 Europe

- 5.20.4.3 Asia Pacific

- 5.20.5 IMPACT ON VERTICALS

6 FUTURE OF PHYSICAL SECURITY

- 6.1 INTRODUCTION

- 6.2 ROLE OF AI, DRONES, AND ROBOTICS IN NEXT-GEN SECURITY

- 6.3 EMERGENCE OF SMART CITIES

- 6.4 CONVERGENCE OF PHYSICAL AND CYBERSECURITY

- 6.5 TRENDS IN PREDICTIVE ANALYTICS FOR THREAT PREVENTION

7 SECURITY SOLUTIONS MARKET, BY SYSTEM

- 7.1 INTRODUCTION

- 7.2 FIRE PROTECTION SYSTEMS

- 7.2.1 FIRE SUPPRESSION SYSTEMS

- 7.2.1.1 Growing trend of modular and adaptable fire suppression solutions to drive market

- 7.2.2 FIRE SPRINKLERS

- 7.2.2.1 Rising demand for environmentally conscious fire suppression solutions to fuel market growth

- 7.2.3 FIRE DETECTION SYSTEMS

- 7.2.3.1 Increasing awareness of fire hazards to drive market

- 7.2.4 FIRE ANALYTICS SYSTEMS

- 7.2.4.1 Integration of IoT and cloud-based platforms to support market growth

- 7.2.5 FIRE RESPONSE SYSTEMS

- 7.2.5.1 Adoption of integrated and data-driven fire response solutions to fuel market growth

- 7.2.1 FIRE SUPPRESSION SYSTEMS

- 7.3 VIDEO SURVEILLANCE SYSTEMS

- 7.3.1 CAMERAS

- 7.3.1.1 Increasing adoption of AI-enabled IP cameras to boost demand

- 7.3.1.2 IP cameras and analytics

- 7.3.1.3 PTZ and fixed cameras

- 7.3.2 MONITORS

- 7.3.2.1 Growing demand for touchscreen and interactive monitors to support market growth

- 7.3.3 STORAGE DEVICES

- 7.3.3.1 Rising use of high-resolution 4K and 8K cameras to drive market

- 7.3.4 ACCESSORIES

- 7.3.4.1 Increasing deployment of weather-resistant mounts and enclosures to boost demand

- 7.3.5 SOFTWARE

- 7.3.5.1 Deployment of AI-powered video management software to offer growth opportunities

- 7.3.1 CAMERAS

- 7.4 ACCESS CONTROL SYSTEMS

- 7.4.1 CARD-BASED READERS

- 7.4.1.1 Increasing deployment in corporate offices, educational institutions, and government facilities to drive market growth

- 7.4.2 BIOMETRIC READERS

- 7.4.2.1 Growing adoption of fingerprint recognition to fuel market growth

- 7.4.3 MULTI-TECHNOLOGY READERS

- 7.4.3.1 Flexibility for visitor management and access across multiple sites to offer growth opportunities

- 7.4.4 ELECTRONIC LOCKS

- 7.4.4.1 Growth in smart lock installations for offices and residences to fuel market growth

- 7.4.5 ACCESS CONTROLLERS

- 7.4.5.1 Need for enhanced security across diverse security environments to boost demand

- 7.4.6 SOFTWARE SOLUTIONS

- 7.4.6.1 Rising use of AI and predictive analytics for threat detection to support market growth

- 7.4.7 OTHERS

- 7.4.1 CARD-BASED READERS

- 7.5 ENTRANCE CONTROL SYSTEMS

- 7.5.1 INTEGRATION WITH VIDEO SURVEILLANCE AND SECURITY PLATFORMS TO OFFER LUCRATIVE GROWTH OPPORTUNITIES

- 7.6 INTRUDER ALARM SYSTEMS

- 7.6.1 RISING CONCERNS OVER THEFT, VANDALISM, AND UNAUTHORIZED ACCESS TO FUEL SEGMENTAL GROWTH

- 7.7 THERMAL IMAGING SYSTEMS

- 7.7.1 THERMAL CAMERAS

- 7.7.1.1 Growing application in border security and critical infrastructure protection to boost demand

- 7.7.2 THERMAL MODULES

- 7.7.2.1 Enhanced detection, tracking, and analysis with thermal imaging into existing infrastructure to drive market

- 7.7.1 THERMAL CAMERAS

8 SECURITY SOLUTIONS MARKET, BY SERVICE

- 8.1 INTRODUCTION

- 8.2 FIRE PROTECTION SERVICES

- 8.2.1 MAINTENANCE SERVICES

- 8.2.1.1 Growing application in residential complexes, public venues, and transportation hubs to fuel market growth

- 8.2.2 MANAGED SERVICES

- 8.2.2.1 Optimized fire protection performance to drive market

- 8.2.3 INSTALLATION AND DESIGN SERVICES

- 8.2.3.1 Growing importance of customized fire protection solutions to foster market growth

- 8.2.4 ENGINEERING SERVICES

- 8.2.4.1 Rising demand for integrated and adaptive fire safety approaches to support market growth

- 8.2.5 OTHER SERVICES

- 8.2.1 MAINTENANCE SERVICES

- 8.3 VIDEO SURVEILLANCE SERVICES

- 8.3.1 VSAAS

- 8.3.1.1 Rising demand for cloud-based surveillance solutions to offer growth opportunities

- 8.3.2 INSTALLATION AND MAINTENANCE

- 8.3.2.1 Reduced risk of failures during critical events to augment market growth

- 8.3.1 VSAAS

- 8.4 ACCESS CONTROL SERVICES

- 8.4.1 INSTALLATION AND INTEGRATION

- 8.4.1.1 Enhanced protection for assets, personnel, and sensitive information to fuel market growth

- 8.4.2 SUPPORT AND MAINTENANCE

- 8.4.2.1 Growing improvement-related initiatives to boost demand

- 8.4.1 INSTALLATION AND INTEGRATION

- 8.5 SECURITY SYSTEM INTEGRATION SERVICES

- 8.5.1 ENHANCED REAL-TIME MONITORING, INCIDENT DETECTION, AND COORDINATED RESPONSES TO FUEL MARKET GROWTH

- 8.6 REMOTE MONITORING SERVICES

- 8.6.1 INCREASING DEMAND FOR REAL-TIME SURVEILLANCE TO SUPPORT MARKET GROWTH

9 SECURITY SOLUTIONS MARKET, BY VERTICAL

- 9.1 INTRODUCTION

- 9.2 RESIDENTIAL

- 9.2.1 INCREASING DEMAND FOR CONVENIENCE AND AUTOMATION TO BENEFIT MARKET

- 9.2.1.1 Smart home security

- 9.2.1.2 Gated community solutions

- 9.2.1 INCREASING DEMAND FOR CONVENIENCE AND AUTOMATION TO BENEFIT MARKET

- 9.3 COMMERCIAL

- 9.3.1 ADOPTION OF AI, CLOUD PLATFORMS, AND BIOMETRIC SOLUTIONS TO OFFER GROWTH OPPORTUNITIES

- 9.3.2 CORPORATE OFFICES AND FACILITIES

- 9.3.2.1 Employee access management

- 9.3.2.2 Visitor management system

- 9.3.2.3 Asset protection

- 9.3.2.4 Compliance management

- 9.3.3 MALLS

- 9.4 GOVERNMENT

- 9.4.1 INCREASING THREATS OF TERRORISM AND CYBER-PHYSICAL ATTACKS IN PUBLIC SPACES TO BOOST DEMAND

- 9.4.2 CITY SURVEILLANCE

- 9.4.3 COURTS AND PRISONS

- 9.5 TRANSPORTATION

- 9.5.1 NEED FOR INTEGRATED, INTELLIGENT, AND SCALABLE SECURITY SYSTEMS TO FOSTER MARKET GROWTH

- 9.5.2 AIRPORTS

- 9.5.3 RAILWAYS

- 9.5.4 MARITIME

- 9.5.5 CARGO AND WAREHOUSE SECURITY

- 9.6 RETAIL

- 9.6.1 ADOPTION OF AI-POWERED VIDEO ANALYTICS TO ENABLE REAL-TIME MONITORING TO FUEL MARKET GROWTH

- 9.6.2 LOSS PREVENTION SYSTEM

- 9.6.3 POS SECURITY

- 9.6.4 INVENTORY PROTECTION

- 9.7 BANKING AND FINANCE

- 9.7.1 NEED TO SAFEGUARD PHYSICAL BRANCHES AND ONLINE ASSETS TO DRIVE MARKET

- 9.7.2 BRANCH SECURITY SOLUTIONS

- 9.7.3 ATM SECURITY SOLUTIONS

- 9.7.4 DATA CENTER PROTECTION

- 9.8 EDUCATION

- 9.8.1 SMART CAMPUS INITIATIVES TO OFFER GROWTH OPPORTUNITIES

- 9.8.2 CAMPUS SECURITY

- 9.8.3 RESEARCH AND FACILITY

- 9.9 INDUSTRIAL

- 9.9.1 GROWING INCIDENTS OF THEFT, SABOTAGE, AND WORKPLACE ACCIDENTS TO DRIVE MARKET

- 9.9.2 MANUFACTURING PLANTS

- 9.9.3 WAREHOUSES

- 9.10 ENERGY & UTILITIES

- 9.10.1 RISING RENEWABLE ENERGY INFRASTRUCTURE TO FUEL MARKET GROWTH

- 9.11 SPORTS & LEISURE

- 9.11.1 EMPHASIS ON SAFEGUARDING STADIUMS, ARENAS, AND RECREATION CENTERS TO FOSTER MARKET GROWTH

- 9.12 HEALTHCARE

- 9.12.1 ADOPTION OF INTELLIGENT SECURITY SOLUTIONS TO SUPPORT MARKET GROWTH

- 9.12.2 HOSPITALITY SECURITY SYSTEMS

- 9.12.3 PHARMACEUTICAL SECURITY

- 9.13 MILITARY & DEFENSE

- 9.13.1 EVOLVING SECURITY THREATS TO BOOST DEMAND

- 9.13.2 BORDER SECURITY

- 9.13.3 LAW ENFORCEMENT SOLUTIONS

10 SECURITY SOLUTIONS MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 10.2.2 US

- 10.2.2.1 Growing urban crime to boost demand

- 10.2.3 CANADA

- 10.2.3.1 Shift toward integrated and cloud-enabled solutions to foster market growth

- 10.2.4 MEXICO

- 10.2.4.1 Government-led initiatives and investments in public safety to drive market

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 10.3.2 GERMANY

- 10.3.2.1 Emphasis on Industry 4.0 to offer growth opportunities

- 10.3.3 UK

- 10.3.3.1 Increasing emphasis on secure infrastructure to drive market

- 10.3.4 FRANCE

- 10.3.4.1 Rising adoption of AI-powered security solutions for industrial and commercial sectors to propel market growth

- 10.3.5 ITALY

- 10.3.5.1 Adoption of smart building technologies to fuel market growth

- 10.3.6 SPAIN

- 10.3.6.1 Push toward digital transformation to foster market growth

- 10.3.7 NORDICS

- 10.3.7.1 Convergence of technological innovation to offer growth opportunities

- 10.3.8 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 10.4.2 CHINA

- 10.4.2.1 Expansion of smart city initiatives to support market growth

- 10.4.3 JAPAN

- 10.4.3.1 Emphasis on upgrading safety in transportation networks to drive market

- 10.4.4 SOUTH KOREA

- 10.4.4.1 Increasing focus on smart infrastructure to fuel market growth

- 10.4.5 INDIA

- 10.4.5.1 Rapid urbanization to offer growth opportunities

- 10.4.6 AUSTRALIA

- 10.4.6.1 Increasing safety standards across industrial facilities to fuel market growth

- 10.4.7 INDONESIA

- 10.4.7.1 Rising demand for modern video surveillance and access control systems to foster market growth

- 10.4.8 MALAYSIA

- 10.4.8.1 Increasing adoption of AI-based monitoring and robotic security to boost demand

- 10.4.9 THAILAND

- 10.4.9.1 Growing tourism to boost demand

- 10.4.10 VIETNAM

- 10.4.10.1 Increasing investment in infrastructure projects to drive market

- 10.4.11 REST OF ASIA PACIFIC

- 10.5 ROW

- 10.5.1 MACROECONOMIC OUTLOOK FOR ROW

- 10.5.2 MIDDLE EAST

- 10.5.2.1 Saudi Arabia

- 10.5.2.1.1 Growing focus on life safety and risk management to boost demand

- 10.5.2.2 UAE

- 10.5.2.2.1 Increasing investments in commercial properties to drive market

- 10.5.2.3 Qatar

- 10.5.2.3.1 Investment in large infrastructure and airport expansions fuel market growth

- 10.5.2.4 Kuwait

- 10.5.2.4.1 Increasing demand in oil & gas facilities and public institutions to drive market

- 10.5.2.5 Oman

- 10.5.2.5.1 Importance of improved safety standards to support market growth

- 10.5.2.6 Bahrain

- 10.5.2.6.1 Emphasis on infrastructure modernization to fuel market growth

- 10.5.2.7 Rest of Middle East

- 10.5.2.1 Saudi Arabia

- 10.5.3 SOUTH AMERICA

- 10.5.3.1 Rising technological innovation to foster market growth

- 10.5.4 AFRICA

- 10.5.5 SOUTH AFRICA

- 10.5.5.1 Need to protect critical infrastructure to boost demand

- 10.5.6 REST OF AFRICA

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 11.3 REVENUE ANALYSIS, 2020-2024

- 11.4 MARKET SHARE ANALYSIS, 2O24

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS

- 11.6 BRAND COMPARISON

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.7.5.1 Company footprint

- 11.7.5.2 Region footprint

- 11.7.5.3 System footprint

- 11.7.5.4 Service footprint

- 11.7.5.5 Vertical footprint

- 11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- 11.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.8.5.1 Detailed list of key startups/SMEs

- 11.8.5.2 Competitive benchmarking of key startups/SMEs

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES

- 11.9.2 DEALS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 JOHNSON CONTROLS

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Solutions/Services offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches

- 12.1.1.3.2 Deals

- 12.1.1.4 MnM view

- 12.1.1.4.1 Key strengths/Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses/Competitive threats

- 12.1.2 HONEYWELL INTERNATIONAL INC.

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Solutions/Services offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches

- 12.1.2.3.2 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Key strengths/Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses/Competitive threats

- 12.1.3 ROBERT BOSCH GMBH

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Solutions/Services offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches

- 12.1.3.3.2 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths/Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses/Competitive threats

- 12.1.4 ADT SECURITY SERVICES

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Solutions/Services offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches

- 12.1.4.3.2 Deals

- 12.1.4.4 MnM view

- 12.1.4.4.1 Key strengths/Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses/Competitive threats

- 12.1.5 HANGZHOU HIKVISION DIGITAL TECHNOLOGY CO., LTD

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Solutions/Services offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches

- 12.1.5.3.2 Deals

- 12.1.5.4 MnM view

- 12.1.5.4.1 Key strengths/Right to win

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses/Competitive threats

- 12.1.6 AXIS COMMUNICATIONS AB

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Solutions/Services offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches

- 12.1.6.3.2 Deals

- 12.1.7 DAHUA TECHNOLOGY CO., LTD

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Solutions/Services offered

- 12.1.7.2.1 Product launches

- 12.1.8 SECOM CO., LTD

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Solutions/Services offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Product launches

- 12.1.9 SIEMENS

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Solutions/Services offered

- 12.1.10 ASSA ABLOY

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Solutions/Services offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Deals

- 12.1.11 KEENFINITY

- 12.1.11.1 Business overview

- 12.1.11.2 Products/Solutions/Services offered

- 12.1.1 JOHNSON CONTROLS

- 12.2 OTHER PLAYERS

- 12.2.1 HALMA PLC

- 12.2.2 HOCHIKI CORPORATION

- 12.2.3 DORMAKABA GROUP

- 12.2.4 TELEDYNE FLIR LLC

- 12.2.5 ALLEGION PLC

- 12.2.6 NICE S.P.A.

- 12.2.7 GODREJ GROUP

- 12.2.8 ALARM.COM

- 12.2.9 MOTOROLA SOLUTIONS, INC.

- 12.2.10 DALLMEIER ELECTRONIC GMBH & CO KG

- 12.2.11 SECURITAS TECHNOLOGY

- 12.2.12 GUNNEBO AB

- 12.2.13 BRIVO SYSTEMS, LLC

- 12.2.14 BRINKS HOME

- 12.2.15 VERKADA INC.

13 APPENDIX

- 13.1 INSIGHTS FROM INDUSTRY EXPERTS

- 13.2 DISCUSSION GUIDE

- 13.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.4 AVAILABLE CUSTOMIZATIONS

- 13.5 RELATED REPORTS

- 13.6 AUTHOR DETAILS