|

시장보고서

상품코드

1873972

인공지능(AI) 로봇 시장 : 구성 요소별, 기술별, 로봇 유형별 예측(-2030년)Artificial Intelligence (AI) Robots Market by Component (Hardware, Software), Technology (Machine learning, Computer Vision, Context Awareness, NLP, Localization & Mapping/SLAM, Motion Planning & Control) and Robot Type - Global Forecast to 2030 |

||||||

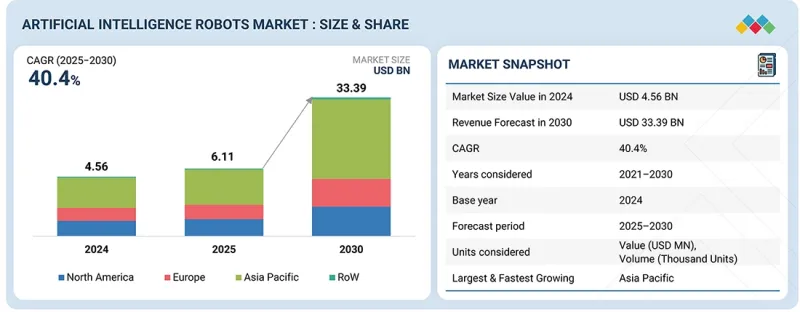

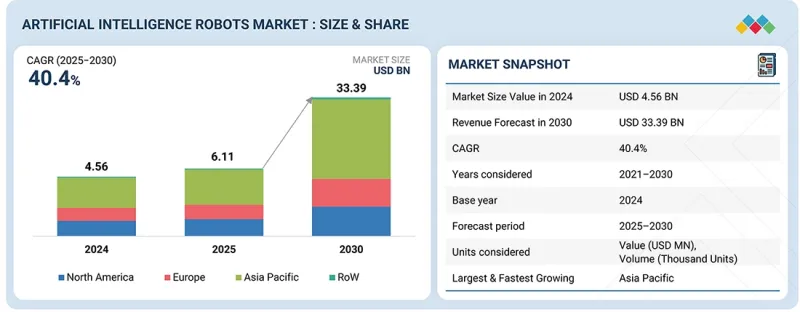

세계의 인공지능(AI) 로봇 시장 규모는 2025년 61억 1,000만 달러에서 2030년까지 333억 9,000만 달러에 달하고, CAGR 40.4%를 나타낼 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 구성 요소별, 기술별, 로봇 유형별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양 및 기타 지역 |

인공지능(AI) 로봇 시장을 견인하는 주요 요인은 산업 자동화에서 지능 로봇의 도입 가속입니다. 공장과 물류 거점이 생산성과 효율성 향상을 목표로 하는 가운데 조립, 검사, 포장, 자재 운반 등의 작업에 AI 탑재 로봇이 도입되고 있습니다. 이러한 로봇은 머신러닝을 활용한 적응형 의사결정을 통해 현대 스마트 공장에 원활하게 통합할 수 있습니다. 제조업 거점의 노동력 부족 심각화와 임금 비용 상승은 운영 비용 절감과 품질 향상을 실현하는 자동화 솔루션 수요를 촉진하고 있습니다. 센서 기술과 컴퓨터 비전의 급속한 진보로 로봇은 복잡한 환경을 탐색하고 정밀한 작업을 수행할 수 있어 경쟁력 있는 확장 가능한 제조에 필수적인 존재가 되고 있습니다.

머신러닝 기술은 로봇이 데이터에서 학습하고 시간이 지남에 따라 성능을 향상시키는 능력으로 인공지능(AI) 로봇 시장에서 큰 점유율을 차지할 것으로 예측됩니다. 이 기술을 통해 로봇은 복잡하고 역동적인 환경에 적응하여 자율성, 정확성 및 의사결정 능력을 향상시킬 수 있습니다. 머신러닝은 물체 인식, 예지 보전, 실시간 조정 등의 고급 기능을 가능하게 하며, 이들은 제조업, 의료, 물류, 서비스 산업에서의 응용에 매우 중요합니다. AI 로봇이 보다 지능적이고 다기능이 됨에 따라, 머신러닝 구동 솔루션에 대한 수요는 급속히 확대될 것으로 예측되고 시장 확대를 견인하는 주요 기술 분야가 될 것입니다.

로봇 기능을 실현하는 데 있어서, 하드웨어 부품은 기초적인 역할을 담당합니다. 센서, 액추에이터, 프로세서, 기계적 프레임워크와 같은 필수 하드웨어 요소는 로봇 시스템의 핵심을 구성하여 정밀한 작동, 이동성 및 환경 인식을 보장합니다. 실시간 데이터 처리와 동작 안정성이 필요한 산업 자동화, 의료 용도, 자율주행차 분야에서 첨단 센서 및 고성능 프로세서에 대한 수요가 높아지고 있습니다.

중국은 2030년까지 아시아태평양의 인공지능(AI) 로봇 시장에서 급속한 산업화와 자동화 기술에 대한 많은 투자를 배경으로 최대 점유율을 차지할 것으로 예측됩니다. 이 나라의 견고한 제조업 기반과 '중국제조 2025' 계획 등 정부 주도의 시책이 함께 자동차, 전자기기, 물류 등 다양한 분야에서 AI 탑재 로봇의 보급을 지원하고 있습니다. 로봇 기술 혁신의 중국 리더십, 거대한 국내 시장, 수직 통합 공급망이 이점을 더욱 강화하고 있습니다. 주요 로봇 기업의 존재와 풍부한 R&D 자금을 통해 중국은 예측 기간 동안 경쟁 우위를 유지하고 시장 리더십을 견지할 수 있습니다.

본 보고서에서는 세계의 인공지능(AI) 로봇 시장에 대해 조사했으며, 구성 요소별, 기술별, 로봇 유형별, 용도별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 중요 인사이트

제4장 시장 개요

- 서론

- 시장 역학

- 연결된 시장과 부문 간 기회

- Tier 1/2/3 기업의 전략적 움직임

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제 전망

- 공급망 분석

- 생태계 분석

- 가격 분석

- 무역 분석

- 주요 컨퍼런스 및 이벤트(2026년)

- 고객사업에 영향을 주는 동향/혼란

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 미국 관세가 인공지능(AI) 로봇 시장에 미치는 영향(2025년)

제6장 기술의 진보, AI별 영향, 특허, 혁신, 향후 용도

- 주요 기술

- 보완적 기술

- 기술/제품 로드맵

- 특허 분석

- 미래의 응용

제7장 규제 상황

- 지역 규제 및 규정 준수

- 규제기관, 정부기관, 기타 조직

- 업계 표준

제8장 고객정세와 구매행동

- 의사결정 프로세스

- 주요 이해관계자와 구매 기준

- 채용 장벽과 내부 과제

- 다양한 용도에서의 미충족 수요(Unmet Needs)

제9장 인공지능(AI) 로봇 시장(구성 요소별)

- 서론

- 하드웨어

- 소프트웨어

제10장 인공지능(AI) 로봇 시장(기술별)

- 서론

- 머신러닝

- 컴퓨터 비전

- 컨텍스트 인식

- 자연언어처리

- 위치 추정 및 매핑/SLAM

- 모션 플래닝 및 제어

제11장 인공지능(AI) 로봇 시장(로봇 유형별)

- 서론

- 산업용 로봇

- 서비스 로봇

제12장 인공지능(AI) 로봇 시장(용도별)

- 서론

- 군사 및 방위

- 개인 지원 및 돌봄 서비스

- 보안 및 모니터링

- 공공 인프라

- 교육 및 엔터테인먼트

- 연구 및 우주 탐사

- 산업

- 농업

- 의료 지원

- 창고 및 물류

- 소매

- 기타

제13장 인공지능(AI) 로봇 시장(지역별)

- 서론

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 멕시코

- 유럽

- 유럽의 거시 경제 전망

- 영국

- 독일

- 이탈리아

- 프랑스

- 스페인

- 기타

- 아시아태평양

- 아시아태평양의 거시 경제 전망

- 중국

- 호주

- 일본

- 한국

- 인도

- 기타

- 기타 지역

- 기타 지역의 거시 경제 전망

- 중동 및 아프리카

- 남미

제14장 경쟁 구도

- 개요

- 주요 참가 기업의 전략/강점(2022-2025년)

- 수익 분석(2020-2024년)

- 시장 점유율 분석(2024년)

- 기업평가와 재무지표

- 브랜드/제품 비교

- 기업평가 매트릭스 : 주요 진입기업(2024년)

- 기업평가 매트릭스 : 스타트업/중소기업(2024년)

- 경쟁 시나리오

제15장 기업 프로파일

- 주요 진출기업

- NABTESCO CORPORATION

- NIDEC CORPORATION

- PANASONIC CORPORATION

- YASKAWA ELECTRIC CORPORATION

- ABB

- NVIDIA CORPORATION

- INTEL CORPORATION

- ADVANCED MICRO DEVICES, INC.

- TEXAS INSTRUMENTS INCORPORATED

- INFINEON TECHNOLOGIES AG

- IBM

- QUALCOMM TECHNOLOGIES, INC.

- SONY GROUP CORPORATION

- BOSCH SENSORTEC GMBH

- STMICROELECTRONICS

- NXP SEMICONDUCTORS

- 기타 기업

- NEURALA, INC.

- STAUBLI INTERNATIONAL AG

- BRAIN CORPORATION

- WIBOTIC

- ELMO MOTION CONTROL LTD.

- ADVANCED MOTION CONTROLS

- ODRIVE

- INTERMODALICS

- ROBOTEQ

- ENERGY ROBOTICS

- SEA MACHINES ROBOTICS, INC.

- PILZ GMBH & CO. KG

- MOTION INDUSTRIES, INC.

- MAXON

- FAULHABER

- LUXONIS

- XELA ROBOTICS

- BENEWAKE(BEIJING) CO., LTD.

제16장 조사 방법

제17장 부록

KTH 25.11.27The global AI robots market is projected to grow from USD 6.11 billion in 2025 to USD 33.39 billion by 2030, at a CAGR of 40.4%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Component, Technology, Robot Type and Region |

| Regions covered | North America, Europe, APAC, RoW |

"Adoption of AI Robots for Industrial Automation to Drive Market"

A primary factor propelling the AI robots market is the accelerated adoption of intelligent robots in industrial automation. As factories and logistics hubs strive for higher productivity and efficiency, AI-powered robots are deployed for tasks such as assembly, inspection, packaging, and material handling. These robots leverage machine learning for adaptive decision-making, allowing seamless integration into modern smart factories. Growing labor shortages and rising wage costs in manufacturing hubs are driving demand for automated solutions that reduce operational expenses and enhance quality. Rapid advancements in sensors and computer vision further enable robots to navigate complex environments and execute precise operations, making them indispensable for competitive and scalable manufacturing.

"Machine Learning Technology to Hold Majority of Market Share in 2030."

Machine learning technology is expected to hold a significant share of the AI robot market due to its ability to enable robots to learn from data and improve their performance over time. This technology allows robots to adapt to complex and dynamic environments, enhancing their autonomy, precision, and decision-making capabilities. Machine learning facilitates advanced functions such as object recognition, predictive maintenance, and real-time adjustments, which are crucial for applications in manufacturing, healthcare, logistics, and service industries. As AI robots become more intelligent and versatile, the demand for machine learning-driven solutions is projected to grow rapidly, making it a key technology segment driving market expansion.

"Hardware Segment to Account for Largest Market Share Throughout Forecast Period"

Hardware components play a fundamental role in enabling robotic functions. Essential hardware elements such as sensors, actuators, processors, and mechanical frameworks form the core of robot systems, ensuring precise operation, mobility, and environmental perception. The demand for advanced sensors and high-performance processors is driven by industrial automation, healthcare applications, and autonomous vehicles, which require reliable hardware for real-time data processing and operational stability.

"China to Account for Prominent Share of Asia Pacific Market for AI Robots in 2030."

China is expected to account for the largest share of the Asia Pacific AI robots market by 2030, driven by rapid industrialization and substantial investments in automation technologies. The country's strong manufacturing base, along with government initiatives such as the "Made in China 2025" plan, supports the widespread adoption of AI-powered robots across various sectors, including automotive, electronics, and logistics. China's leadership in robotics innovation, a vast domestic market, and vertically integrated supply chains further reinforce its dominant position. The presence of major robotics companies and extensive R&D funding enables China to sustain its competitive edge and maintain market leadership throughout the forecast period.

Extensive primary interviews were conducted with key industry experts in the AI robots market to determine and verify the market size for various segments and subsegments, which were gathered through secondary research. The breakup of primary participants for the report is shown below:

The study draws insights from a range of industry experts, including component suppliers, Tier 1 companies, and OEMs. The breakup of the primaries is as follows:

- By Company Type: Tier 1 - 30%, Tier 2 - 50%, and Tier 3 - 20%

- By Designation: C-level Executives - 25%, Directors - 20%, and Others - 55%

- By Region: North America - 40%, Europe - 20%, Asia Pacific - 30%, and RoW - 10%

Notes: The three tiers of companies are based on their total revenue as of 2024: Tier 1, equal to or greater than USD 1,000 million; Tier 2, between USD 500 million and USD 1,000 million; and Tier 3, less than or equal to USD 500 million. Other designations include managers and academicians.

Nabtesco Corporation (Japan), NIDEC CORPORATION (Japan), Panasonic Corporation (Japan), YASKAWA ELECTRIC CORPORATION (Japan), ABB (Switzerland), Texas Instruments Incorporated (US), Infineon Technologies AG (Germany), IBM (US), Qualcomm Technologies, Inc. (US), Sony Corporation (Japan), Bosch Sensortec GmbH (Germany), STMicroelectronics (Switzerland) are some key players in the AI robots market.

The study includes an in-depth competitive analysis of these key players in the AI robots market, with their company profiles, recent developments, and key market strategies.

Study Coverage:

This research report categorizes the AI robots market based on component: hardware & software, by robot type: industrial & service, by technology: machine learning, computer vision, context awareness, natural language, localization & mapping/slam processing, motion planning & control, by application: military & defence, personal assistance and care giving, security and surveillance, public infrastructure, education and entertainment, research and space exploration, industrial, agriculture, healthcare assistance, warehouse & logistics, retail, others and region (North America, Europe, Asia Pacific and Row). The report outlines the key drivers, restraints, challenges, and opportunities influencing the AI robot market and provides forecasts through 2030. The report also includes leadership mapping and analysis of all companies in the AI robot ecosystem.

Key Benefits of Buying the Report

The report will assist market leaders/new entrants in this market by providing information on the closest approximations of the revenue numbers for the overall AI robots market and its subsegments. This report will help stakeholders understand the competitive landscape and gain valuable insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of Key Drivers (High adoption of robots for personal use, Support from governments worldwide to develop modern technologies, Rise in demand for industrial robots ) Restraints (Reluctance to adopt new technologies), Opportunities (Increasing aging population worldwide boosting the demand for AI-based robots for elderly assistance, Increasing investments in AI robotics), and Challenges (Long time to commercialize robots and high maintenance costs), influencing the growth of the AI robots market

- Product Development/Innovation: Detailed insights into upcoming technologies, research and development activities, and the latest product and service launches in the AI robot market

- Market Development: Comprehensive information about lucrative markets by analyzing the AI robots market across varied regions

- Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the AI robots market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Nabtesco Corporation (Japan), NIDEC CORPORATION (Japan), Panasonic Corporation (Japan), YASKAWA ELECTRIC CORPORATION (Japan), ABB (Switzerland), and Texas Instruments Incorporated (US) in the AI robots market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEAR CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIONS SHAPING AI ROBOTS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AI ROBOTS MARKET

- 3.2 AI ROBOTS MARKET, BY ROBOT TYPE

- 3.3 AI ROBOTS MARKET, BY APPLICATION

- 3.4 AI ROBOTS MARKET, BY COMPONENT

- 3.5 AI ROBOTS MARKET IN ASIA PACIFIC, BY APPLICATION AND COUNTRY

- 3.6 AI ROBOTS MARKET, BY GEOGRAPHY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 High adoption of robots for personal use

- 4.2.1.2 Rising government support for robotics and industrial-AI projects

- 4.2.1.3 Growing emphasis on industrial automation

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital investment and shortage of technical expertise

- 4.2.2.2 Lack of standardized regulations to prevent risks associated with networked and autonomous robots

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Mounting demand for AI-based robots for elderly assistance

- 4.2.3.2 Increasing investment in AI robotics

- 4.2.4 CHALLENGES

- 4.2.4.1 Long period of AI robot commercialization

- 4.2.4.2 Complexities associated with integrating AI robots into workflows

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL CONSUMER ROBOTS INDUSTRY

- 5.2.4 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING RANGE AI ROBOT SENSORS OFFERED BY KEY PLAYERS, BY TYPE, 2024

- 5.5.2 AVERAGE SELLING PRICE TREND OF AI ROBOT SENSORS, BY REGION, 2021-2024

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 847950)

- 5.6.2 EXPORT SCENARIO (HS CODE 847950)

- 5.7 KEY CONFERENCES AND EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 PHILIPS ADOPTS SOFTBANK'S AI ROBOT TO TRANSFORM INNOVATION LAB

- 5.10.2 UNIVERSITY OF PISA INSTALLS HANSON ROBOTS TO SUPPORT THERAPY AND RESEARCH FOR AUTISM SPECTRUM DISORDER

- 5.10.3 MOBILE ROBOTS HELP IMPROVE PRODUCTIVITY AND EFFICIENCY OF AUDI ASSEMBLY LINE

- 5.10.4 NEXCOM USES INTEL'S ROBOTICS TO OPTIMIZE MANUFACTURING OPERATIONS

- 5.11 IMPACT OF 2025 US TARIFF ON AI ROBOTS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON APPLICATIONS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 MACHINE LEARNING AND COMPUTER VISION

- 6.1.2 NATURAL LANGUAGE PROCESSING AND HUMAN-ROBOT INTERACTION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 INTERNET OF THINGS (IOT) AND EDGE COMPUTING

- 6.2.2 CLOUD COMPUTING AND DIGITAL TWINS

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FOR VARIOUS APPLICATIONS

9 AI ROBOT MARKET, BY COMPONENT

- 9.1 INTRODUCTION

- 9.2 HARDWARE

- 9.2.1 DRIVE SYSTEMS

- 9.2.1.1 Gearboxes

- 9.2.1.1.1 Ability to handle variable payloads to contribute to segmental growth

- 9.2.1.2 Motors

- 9.2.1.2.1 Adoption of AI-driven predictive control to fuel segmental growth

- 9.2.1.3 Motor controllers

- 9.2.1.3.1 Trend toward AI-enabled control systems to accelerate segmental growth

- 9.2.1.1 Gearboxes

- 9.2.2 SENSORS

- 9.2.2.1 Image sensors

- 9.2.2.1.1 High dynamic range and depth sensing features to boost segmental growth

- 9.2.2.2 LiDAR sensors

- 9.2.2.2.1 Demand for autonomous navigation to accelerate segmental growth

- 9.2.2.3 Temperature sensors

- 9.2.2.3.1 Ability to protect sensitive electronic components from overheating and ensure system reliability to drive market

- 9.2.2.4 Tactile sensors

- 9.2.2.4.1 Focus on enabling touch and force detection in robotics to fuel segmental growth

- 9.2.2.5 Pressure sensors

- 9.2.2.5.1 Use for tactile perception and internal state monitoring to expedite segmental growth

- 9.2.2.6 Encoders

- 9.2.2.6.1 Requirement for precision motion control in advanced robotic applications to augment segmental growth

- 9.2.2.7 IMUs

- 9.2.2.7.1 Increasing application in autonomous vehicles, aerial drones, and humanoid robots to bolster segmental growth

- 9.2.2.8 Ultrasonic sensors

- 9.2.2.8.1 Need for spatial awareness and safe maneuverability in robots to provide market growth opportunities

- 9.2.2.9 Other sensors

- 9.2.2.1 Image sensors

- 9.2.3 CONTROL SYSTEMS

- 9.2.3.1 CPU

- 9.2.3.1.1 Need for high-performance, low-latency processing in AI-driven robotic systems to accelerate segmental growth

- 9.2.3.2 GPU

- 9.2.3.2.1 Growing need for parallel computing and real-time AI processing to foster segmental growth

- 9.2.3.3 ASIC

- 9.2.3.3.1 High demand for miniaturization, low-latency processing, and energy-efficient designs to boost segmental growth

- 9.2.3.4 FPGA

- 9.2.3.4.1 Requirement for low-latency, high-throughput processing in real-time environments to accelerate segmental growth

- 9.2.3.5 DSP

- 9.2.3.5.1 Mounting adoption of intelligent edge devices, AMRs, and cobots to expedite market growth

- 9.2.3.6 Other control systems

- 9.2.3.1 CPU

- 9.2.4 ENERGY SUPPLY SYSTEMS

- 9.2.4.1 Power supply units

- 9.2.4.1.1 Emphasis on reliable and intelligent power management systems to accelerate segmental growth

- 9.2.4.2 Batteries

- 9.2.4.2.1 High demand for high-density, safe, and efficient battery systems to drive market

- 9.2.4.1 Power supply units

- 9.2.1 DRIVE SYSTEMS

- 9.3 SOFTWARE

- 9.3.1 ROBOTIC OS/ROS

- 9.3.1.1 Use to facilitate modularity, scalability, and interoperability to boost segmental growth

- 9.3.2 APPLICATION SOFTWARE

- 9.3.2.1 Ability to support human-robot collaboration to contribute to segmental growth

- 9.3.1 ROBOTIC OS/ROS

10 AI ROBOTS MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 MACHINE LEARNING

- 10.2.1 DEPLOYMENT BY RESEARCHERS TO TEACH HUMANOID ROBOTS TO FUEL SEGMENTAL GROWTH

- 10.3 COMPUTER VISION

- 10.3.1 FOCUS ON HELPING ROBOTS PRECISELY LOCATE AND IDENTIFY IMAGES TO AUGMENT SEGMENTAL GROWTH

- 10.4 CONTEXT AWARENESS

- 10.4.1 DEVELOPMENT OF SOPHISTICATED HARD AND SOFT SENSORS TO CONTRIBUTE TO SEGMENTAL GROWTH

- 10.5 NATURAL LANGUAGE PROCESSING

- 10.5.1 USE TO UNDERSTAND HUMAN SPEECH APPLICATIONS IN ROBOTS FOR ELDERLY ASSISTANCE TO EXPEDITE SEGMENTAL GROWTH

- 10.6 LOCALIZATION & MAPPING/SLAM

- 10.6.1 ABILITY TO HELP ROBOTS CREATE ACCURATE MAPS OF SURROUNDINGS TO FUEL SEGMENTAL GROWTH

- 10.7 MOTION PLANNING & CONTROL

- 10.7.1 EMPHASIS ON PRECISION, SAFETY, AND REAL-TIME AUTONOMOUS OPERATION IN ROBOTICS TO FACILITATE SEGMENTAL GROWTH

11 AI ROBOTS MARKET, BY ROBOT TYPE

- 11.1 INTRODUCTION

- 11.2 INDUSTRIAL ROBOTS

- 11.2.1 TRADITIONAL ROBOTS

- 11.2.1.1 Greater adaptability, predictive maintenance, and intelligent decision-making to foster segmental growth

- 11.2.2 COLLABORATIVE ROBOTS

- 11.2.2.1 Use to enable flexible, low-barrier automation in mixed human-robot workcells to augment segmental growth

- 11.2.1 TRADITIONAL ROBOTS

- 11.3 SERVICE ROBOTS

- 11.3.1 HUMAN-ASSIST ROBOTS

- 11.3.1.1 Growing aging population and shortage of healthcare workers to contribute to segmental growth

- 11.3.2 MOBILE ROBOTS

- 11.3.2.1 High emphasis on automation of transportation and repetitive workflows to boost segmental growth

- 11.3.3 SOCIAL ROBOTS

- 11.3.3.1 Rising need for personalized education tools and focus on automation to expedite segmental growth

- 11.3.1 HUMAN-ASSIST ROBOTS

12 AI ROBOTS MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 MILITARY & DEFENSE

- 12.2.1 INCREASING NEED FOR REAL-TIME DATA COLLECTION AND THREAT DETECTION TO ACCELERATE SEGMENTAL GROWTH

- 12.2.2 SPYING

- 12.2.3 SEARCH & RESCUE OPERATIONS

- 12.2.4 BORDER SECURITY

- 12.2.5 COMBAT OPERATIONS

- 12.3 PERSONAL ASSISTANCE & CAREGIVING

- 12.3.1 GROWING PREFERENCE FOR INDEPENDENT LIVING TO ACCELERATE SEGMENTAL GROWTH

- 12.3.2 ELDERLY ASSISTANCE

- 12.3.3 COMPANIONSHIP

- 12.4 SECURITY & SURVEILLANCE

- 12.4.1 MOUNTING DEMAND FOR REAL-TIME MONITORING AND AUTOMATED SAFETY MANAGEMENT SYSTEMS TO FUEL SEGMENTAL GROWTH

- 12.5 PUBLIC INFRASTRUCTURE

- 12.5.1 INCREASING RELIANCE ON ROBOTS FOR CONSTRUCTION, INSPECTION, AND MONITORING APPLICATIONS TO DRIVE MARKET

- 12.6 EDUCATION & ENTERTAINMENT

- 12.6.1 WIDESPREAD ADOPTION OF DIGITAL TECHNOLOGY TO AUGMENT SEGMENTAL GROWTH

- 12.7 RESEARCH & SPACE EXPLORATION

- 12.7.1 RISING DEPLOYMENT OF ROBOTS FOR COMPUTATIONAL NEUROSCIENCE AND EDUCATIONAL PURPOSES TO SUPPORT MARKET GROWTH

- 12.8 INDUSTRIAL

- 12.8.1 RISE OF SMART FACTORIES AND INDUSTRY 4.0 INITIATIVES TO FACILITATE SEGMENTAL GROWTH

- 12.9 AGRICULTURE

- 12.9.1 GROWING FOCUS ON ANALYZING REAL-TIME DATA OF WEATHER CONDITIONS AND CROP PRICES TO FOSTER SEGMENTAL GROWTH

- 12.10 HEALTHCARE ASSISTANCE

- 12.10.1 ABILITY OF ROBOTS TO HELP PREDICT HIGH-RISK CONDITIONS OF PATIENTS TO ACCELERATE SEGMENTAL GROWTH

- 12.11 WAREHOUSE & LOGISTICS

- 12.11.1 RISING NEED TO OPTIMIZE SUPPLY CHAIN MANAGEMENT TO CONTRIBUTE TO SEGMENTAL GROWTH

- 12.12 RETAIL

- 12.12.1 GROWING EMPHASIS ON OPTIMIZING STORE OPERATIONS AND ENHANCING CUSTOMER EXPERIENCE TO BOOST SEGMENTAL GROWTH

- 12.13 OTHER APPLICATIONS

13 AI ROBOTS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 13.2.2 US

- 13.2.2.1 Increasing investment in advanced technologies by government and private institutions drive market

- 13.2.3 CANADA

- 13.2.3.1 Rising deployment of AI across diverse industries to augment market growth

- 13.2.4 MEXICO

- 13.2.4.1 Emergence as major industrial hub to contribute to market growth

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 13.3.2 UK

- 13.3.2.1 Rapid advances in AI and collaborative robotics to accelerate market growth

- 13.3.3 GERMANY

- 13.3.3.1 Strong industrial base and focus on automation to boost market growth

- 13.3.4 ITALY

- 13.3.4.1 Growing emphasis on improving efficiency and productivity across industries to augment market growth

- 13.3.5 FRANCE

- 13.3.5.1 Mounting adoption of robots to enhance productivity, reduce operational costs, and address labor shortages to drive market

- 13.3.6 SPAIN

- 13.3.6.1 Increasing demand for automation solutions to accelerate market growth

- 13.3.7 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 13.4.2 CHINA

- 13.4.2.1 Escalating adoption of automation solutions in labor-intensive industries to contribute to market growth

- 13.4.3 AUSTRALIA

- 13.4.3.1 Rapid advances in automation solutions for industrial applications to bolster market growth

- 13.4.4 JAPAN

- 13.4.4.1 Strong government support for robots and technological innovation to fuel market growth

- 13.4.5 SOUTH KOREA

- 13.4.5.1 Rapid advances in sensor technologies to accelerate market growth

- 13.4.6 INDIA

- 13.4.6.1 Rapid digital transformation and robust IT infrastructure to boost market growth

- 13.4.7 REST OF ASIA PACIFIC

- 13.5 ROW

- 13.5.1 MACROECONOMIC OUTLOOK FOR ROW

- 13.5.2 MIDDLE EAST & AFRICA

- 13.5.2.1 Increasing government support for automation and manufacturing expansion to foster market growth

- 13.5.3 SOUTH AMERICA

- 13.5.3.1 Escalating adoption of autonomous mobile robots to contribute to market growth

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 14.3 REVENUE ANALYSIS, 2020-2024

- 14.4 MARKET SHARE ANALYSIS, 2024

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 BRAND/PRODUCT COMPARISON

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Component footprint

- 14.7.5.4 Robot type footprint

- 14.7.5.5 Technology footprint

- 14.7.5.6 Application footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 NABTESCO CORPORATION

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths/Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses/Competitive threats

- 15.1.2 NIDEC CORPORATION

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths/Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses/Competitive threats

- 15.1.3 PANASONIC CORPORATION

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths/Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses/Competitive threats

- 15.1.4 YASKAWA ELECTRIC CORPORATION

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths/Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses/Competitive threats

- 15.1.5 ABB

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths/Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses/Competitive threats

- 15.1.6 NVIDIA CORPORATION

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches

- 15.1.7 INTEL CORPORATION

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Deals

- 15.1.8 ADVANCED MICRO DEVICES, INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.8.3.2 Deals

- 15.1.8.3.3 Other developments

- 15.1.9 TEXAS INSTRUMENTS INCORPORATED

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches

- 15.1.9.3.2 Deals

- 15.1.10 INFINEON TECHNOLOGIES AG

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches

- 15.1.11 IBM

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.12 QUALCOMM TECHNOLOGIES, INC.

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.13 SONY GROUP CORPORATION

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product launches

- 15.1.13.3.2 Deals

- 15.1.14 BOSCH SENSORTEC GMBH

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Deals

- 15.1.15 STMICROELECTRONICS

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Product launches

- 15.1.16 NXP SEMICONDUCTORS

- 15.1.16.1 Business overview

- 15.1.16.2 Products/Solutions/Services offered

- 15.1.16.3 Recent developments

- 15.1.16.3.1 Deals

- 15.1.1 NABTESCO CORPORATION

- 15.2 OTHER PLAYERS

- 15.2.1 NEURALA, INC.

- 15.2.2 STAUBLI INTERNATIONAL AG

- 15.2.3 BRAIN CORPORATION

- 15.2.4 WIBOTIC

- 15.2.5 ELMO MOTION CONTROL LTD.

- 15.2.6 ADVANCED MOTION CONTROLS

- 15.2.7 ODRIVE

- 15.2.8 INTERMODALICS

- 15.2.9 ROBOTEQ

- 15.2.10 ENERGY ROBOTICS

- 15.2.11 SEA MACHINES ROBOTICS, INC.

- 15.2.12 PILZ GMBH & CO. KG

- 15.2.13 MOTION INDUSTRIES, INC.

- 15.2.14 MAXON

- 15.2.15 FAULHABER

- 15.2.16 LUXONIS

- 15.2.17 XELA ROBOTICS

- 15.2.18 BENEWAKE (BEIJING) CO., LTD.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY AND PRIMARY RESEARCH

- 16.1.2 SECONDARY DATA

- 16.1.2.1 Key data from secondary sources

- 16.1.2.2 List of key secondary sources

- 16.1.3 PRIMARY DATA

- 16.1.3.1 Key data from primary sources

- 16.1.3.2 Key industry insights

- 16.1.3.3 List of primary interview participants

- 16.1.3.4 Breakdown of primaries

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.1.1 Approach to arrive at market size using bottom-up analysis (supply side)

- 16.2.2 TOP-DOWN APPROACH

- 16.2.2.1 Approach to arrive at market size using top-down analysis (demand side)

- 16.2.1 BOTTOM-UP APPROACH

- 16.3 MARKET FORECAST APPROACH

- 16.3.1 SUPPLY SIDE

- 16.3.2 DEMAND SIDE

- 16.4 DATA TRIANGULATION

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

- 16.7 RISK ANALYSIS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS