|

시장보고서

상품코드

1877350

동물 상처 치료 시장 : 제품별, 동물 유형별, 유통 채널별, 최종 사용자별, 지역별 예측(-2030년)Animal Wound Care Market by Product (Surgical, Advanced, Traditional ), Animal Type, Distribution Channel, End User - Global Forecast to 2030 |

||||||

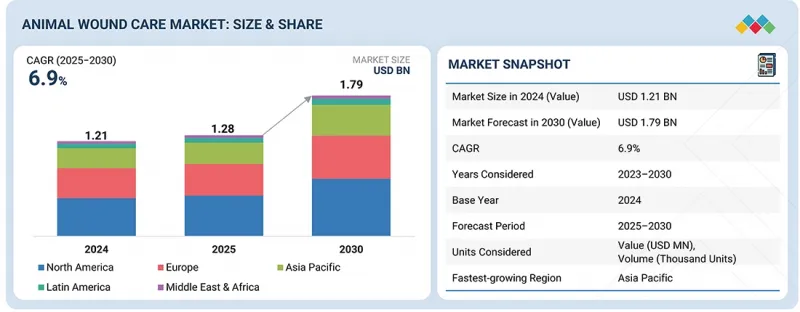

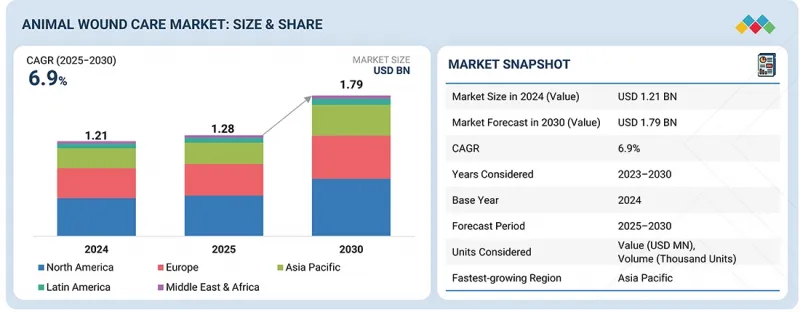

동물 상처 치료 시장 규모는 2025년 12억 8,000만 달러에서 2030년까지 17억 9,000만 달러에 이를 것으로 예측되며, 2025년부터 2030년까지의 CAGR은 6.9%를 나타낼 것으로 전망됩니다.

동물 상처 치료 시장의 주요 동향은 세계적인 반려동물 사육 수 증가와 동물 건강에 대한 관심 증가를 포함합니다. 반려동물 소유자는 자신의 동물의 건강과 복지에 대한 의식을 높이고 더 깊이 관여하게 되었습니다. 이 의식 증가는 반려동물을위한 첨단 상처 치료 및 솔루션을 추구하는 동기가 되었습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(100만 달러) |

| 부문 | 제품별, 동물 유형별, 유통 채널별, 최종 사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양 및 기타 지역 |

개와 고양이와 같은 반려동물이 증가함에 따라 전문 상처 치료 제품 및 서비스에 대한 수요가 증가하고 있습니다. 또한 반려동물 소유자는 동물을위한 고급 수의학 및 개인화된 의료 관리에 투자하는 의지가 있으며, 이는 동물 상처 치료 시장의 확대를 촉진하고 있습니다.

동물 상처 치료 시장은 크게 4개의 부문으로 분류됩니다(수술 상처 치료 제품, 첨단 상처 치료 제품, 전통적인 상처 치료 제품, 치료 장비). 이 중 수술 상처 관리 제품 부문은 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 동물의 만성 질환 치료를 위한 수술과 다양한 의료 개입 증가는 전문적인 수술 상처 관리 제품에 대한 수요 증가에 기여합니다. 봉합사, 스테이플러, 조직 접착제, 실란트, 접착제 등을 포함한 이러한 제품은 동물 수술 후 관리 및 회복에 중요한 역할을 합니다.

또한 동물 상처 치료 분야의 지속적인 혁신으로 획기적인 수술 상처 치료 제품의 개발이 진행되고 있습니다. 이러한 혁신은 효율성 향상, 사용의 간편화 및 전반적인 치료 성과 개선에 초점을 맞추어 수의학 현장에서 해당 제품의 채택을 더욱 촉진하고 있습니다.

또한, 동물 상처 치료 시장에서 수술 상처 치료 제품에 대한 수요 증가는 수의학 수술 증가와 반려동물의 건강에 대한 의식의 향상에 의해 촉진되고 있습니다. 이러한 동향이 결합되어 수술 상처 치료 제품은 동물 상처 치료 시장의 주요 추진력으로 자리매김하고 있습니다.

동물 상처 치료 시장은 동반 동물과 가축의 두 부문으로 나뉩니다. 2024년에는 동반 동물 부문이 세계 시장을 견인했습니다. 이 성장은 주로 반려동물 사육률 증가, 반려동물 관리 지출 확대, 반려동물 보험의 현저한 보급으로 인해 발생합니다.

반려동물 증가와 반려동물의 만성 질환의 만연이 결합되어 상처 치료와 일반적인 건강 관리를 목적으로 한 동물 병원의 진찰이 크게 증가하고 있습니다. 반려동물 소유자는 동물의 건강에 대한 투자 의욕을 높이고 있으며 상처 치료 제품과 치료를 포함한 수의학 서비스에 대한 지출이 증가하고 있습니다. 이러한 요인들이 함께 반려동물의 건강에 대한 투자 전체가 증가하고 동물 상처 치료 제품 수요를 밀어 올리고 있습니다.

아시아태평양은 동물 상처 치료 시장에서 가장 높은 성장률을 기록했으며 인도와 중국이 특히 큰 성장 가능성을 지닌 국가로 부상하고 있습니다. 이 지역에서 반려동물 증가는 시장 확대의 주요 성장 촉진요인이 되었습니다. 게다가 반려동물 사육률 증가, 동물의 건강과 복지에 대한 의식 증가, 특히 인도와 중국에서의 동물 의료비 증가가 동물 상처 치료 제품 수요를 뒷받침하고 있습니다. 그 결과, 이 지역에서는 동물 상처 치료 시장이 현저한 성장을 이루고 있습니다.

본 보고서에서는 세계의 동물 상처 치료 시장에 대해 조사했으며 제품별, 동물 유형별, 유통 채널별, 최종 사용자별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 서론

- 시장 역학

- 업계 동향

- 기술 분석

- Porter's Five Forces 분석

- 규제 분석

- 특허 분석

- 가격 분석

- 무역 분석

- 생태계 분석

- 밸류체인 분석

- 공급망 분석

- 환급 시나리오

- 주요 회의 및 이벤트(2025-2026년)

- AI/생성형 AI가 동물 상처 치료 시장에 미치는 영향

- 미충족 수요(Unmet Needs)와 최종 사용자의 기대

- 주요 이해관계자와 구매 기준

- 사례 연구 분석

- 고객의 비즈니스에 영향을 미치는 동향/혁신

- 투자 및 자금조달 시나리오

- 미국 관세가 동물 상처 치료 시장에 미치는 영향(2025년)

제6장 동물 상처 치료 시장(제품별)

- 서론

- 외과용 상처 치료 제품

- 첨단 상처 치료 제품

- 기존 상처 치료 제품

- 치료 기기

제7장 동물 상처 치료 시장(동물 유형별)

- 서론

- 반려동물

- 가축

제8장 동물 상처 치료 시장(유통 채널별)

- 서론

- 소매 채널

- 전자상거래 플랫폼

- 수의사 클리닉 및 병원(원 내 조제)

- 직접 판매 채널

제9장 동물 상처 치료 시장(최종 사용자별)

- 서론

- 동물병원 및 클리닉

- 재택 케어

- 축산 농장

- 구조 센터 및 NGO

- 기타

제10장 동물 상처 치료 시장(지역별)

- 서론

- 북미

- 북미의 거시경제 전망

- 북미 : 외과용 상처 치료 제품의 수량 분석(유형별, 1,000개, 2023-2030년)

- 미국

- 캐나다

- 유럽

- 유럽의 거시경제 전망

- 유럽 : 외과용 상처 치료 제품의 수량 분석(유형별, 1,000개, 2023-2030년)

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 폴란드

- 네덜란드

- 기타

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 아시아태평양 : 외과용 상처 치료 제품의 수량 분석(유형별, 1,000개, 2023-2030년)

- 일본

- 중국

- 인도

- 호주

- 한국

- 태국

- 인도네시아

- 기타

- 라틴아메리카

- 라틴아메리카의 거시경제 전망

- 라틴아메리카 : 외과용 상처 치료 제품의 수량 분석(유형별, 1,000개, 2023-2030년)

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 중동 및 아프리카의 거시경제 전망

- 중동 및 아프리카 : 외과용 상처 치료 제품의 수량 분석(유형별, 1,000개, 2023-2030년)

- GCC 국가

- 기타 중동 및 아프리카

제11장 경쟁 구도

- 개요

- 주요 진입기업의 전략/강점

- 수익 분석(2022-2024년)

- 시장 점유율 분석(2024년)

- 기업평가 매트릭스 : 주요 진입기업(2024년)

- 기업평가 매트릭스 : 스타트업/중소기업(2024년)

- 주요 기업의 연구 개발비

- 기업평가와 재무지표

- 브랜드/제품 비교

- 경쟁 시나리오

제12장 기업 프로파일

- 주요 진출기업

- B. BRAUN SE

- MEDTRONIC PLC

- 3M COMPANY

- VIRBAC

- DECHRA PHARMACEUTICALS PLC

- NEOGEN CORPORATION

- JORGEN KRUUSE A/S

- SONOMA PHARMACEUTICALS, INC.

- ETHICON, INC.

- ZOETIS INC.

- JAZZ MEDICAL, LLC

- KERICURE INC.

- ADVANCIS MEDICAL

- VERNACARE LTD.

- CREATIVE SCIENCE

- THE WOUND VAC COMPANY, LLC

- DOMES PHARMA, INC.

- 기타 기업

- PRIMAVET INC.

- INNOVACYN, INC.

- SILVERGLIDE

- VETOQUINOL

- MILLPLEDGE LTD.

- OVIK HEALTH

- HYDROFERA

- RIVERPOINT MEDICAL

- INTERNACIONAL FARMACEUTICA SA DE CV

- ORION SUTURES INDIA PVT. LTD.

제13장 부록

KTH 25.11.28The animal wound care market is projected to reach USD 1.79 billion by 2030 from USD 1.28 billion by 2025, at a CAGR of 6.9% from 2025 to 2030. Key trends in the animal wound care market include the increasing global pet ownership and growing concerns for animal health. Pet owners are becoming more aware of and invested in the health and well-being of their animals. This heightened awareness motivates them to seek advanced wound care treatments and solutions for their pets.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD million) |

| Segments | By Product, Animal Type, Distribution Channel, End User, and Region |

| Regions covered | North America, Europe, APAC, RoW |

The rising number of companion animals, such as dogs and cats, is contributing to the growing demand for specialized wound care products and services. Additionally, pet owners are willing to invest in advanced veterinary care and tailored healthcare treatments for their animals, which is driving the expansion of the animal wound care market.

"The surgical wound care segment is projected to witness the highest growth in the animal wound care market, by product, during the forecast period."

The animal wound care market can be broadly categorized into four segments: surgical wound care products, advanced wound care products, traditional wound care products, and therapy devices. Among these, the surgical wound care product segment is expected to experience the highest CAGR during the forecast period. The increasing number of veterinary surgeries and various medical interventions for treating chronic diseases in animals contribute to the growing demand for specialized surgical wound care products. These products, which include sutures, staplers, tissue adhesives, sealants, and glues, play a crucial role in post-operative care and recovery for animals.

Additionally, continuous technological advancements in animal wound care are leading to the development of innovative surgical wound care products. These innovations focus on improving efficacy, ease of application, and overall outcomes, which further drives the adoption of such products in veterinary practices.

Moreover, heightened demand for surgical wound care products in the animal wound care market is fueled by the rise in veterinary surgeries and increased awareness of pet health. Together, these trends position surgical wound care products as a key driver in the animal wound care market.

"The companion animals segment, by animal type, accounted for the largest share of the market in 2024."

The animal wound care market is divided into two segments: companion animals and livestock animals. In 2024, the companion animals segment is expected to dominate the global market. This growth is primarily driven by the increasing adoption of pets, rising spending on pet care, and a notable surge in pet insurance.

The growing population of companion animals, combined with the prevalence of chronic diseases among pets, has resulted in a significant rise in veterinary clinic visits for wound care and general healthcare. Pet owners are increasingly willing to invest in their animals' health, which has led to higher spending on veterinary services, including wound care products and treatments. These factors collectively contribute to an overall increase in investment in companion animal health, thereby boosting the demand for animal wound care products.

"The Asia Pacific market is expected to witness the highest growth during the forecast period."

The Asia Pacific region recorded the highest growth rate in the animal wound care market, with India and China emerging as countries with significant growth potential. The increasing population of pet animals in these areas is a key factor driving the market's expansion. Additionally, the rise in pet adoption, growing awareness of animal health and well-being, and an increase in spending on animal health, especially in India and China, have boosted the demand for animal wound care products. As a result, this region witnessed remarkable growth in the animal wound care market.

A breakdown of the primary participants (supply side) for the animal wound care market referred to in this report is provided below:

- By Company: Tier 1 (45%), Tier 2 (20%), and Tier 3 (35%)

- By Designation: C-level Executives (35%), Directors (25%), and Other Designations (40%)

- By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

The prominent players operating in the animal wound care market are 3M Company (US), Medtronic Plc (Ireland), B. Braun SE (Germany), Virbac (France), Neogen Corporation (US), Jorgen Kruuse A/S (Denmark), Sonoma Pharmaceuticals, Inc. (US), Ethicon, Inc. (US), Dechra Pharmaceuticals (UK), Zoetis Inc. (US), Jazz Medical, LLC (Ireland), KeriCure Inc. (US), Advancis Veterinary (UK), Vernacare Ltd. (UK), Creative Science (US), The Wound VAC Company, LLC (US), and Domes Pharma, Inc. (France).

Research Coverage:

The market study focuses on the animal wound care sector, analyzing various segments. Its goal is to estimate the market size and growth potential across different categories, including product, animal type, distribution channel, end user, and region. Additionally, the study provides a comprehensive competitive analysis of the key players in the market. This includes their company profiles, important insights related to their products and business offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will provide market leaders and new entrants with valuable information about revenue estimates for the overall animal wound care market and its subsegments. It will assist stakeholders in understanding the competitive landscape, allowing them to position their businesses more effectively and develop appropriate go-to-market strategies. Additionally, the report offers insights into market dynamics, including key drivers, restraints, challenges, and opportunities, helping stakeholders stay attuned to the market's pulse.

This report provides insights into the following pointers:

- Analysis of key drivers (expanding companion animal population and pet ownership, increasing adoption of pet insurance and high animal healthcare expenditure, increasing demand for animal-derived food products, and rising prevalence of zoonotic diseases), restraints (high cost of animal wound care products and rising cost of pet care), opportunities (high growth potential of emerging economies and growing number of veterinarians in developed countries), and challenges (lack of animal healthcare awareness in emerging countries and counterfeit or low-quality product circulation).

- Market Penetration: Comprehensive information on product portfolios offered by the top players in the global animal wound care market. The report analyzes this market by product, animal type, distribution channel, end user, and region.

- Product Enhancement/Innovation: Detailed insights on upcoming trends and product launches in the global animal wound care market.

- Market Development: Comprehensive information on the lucrative emerging markets by product, animal type, distribution channel, end user, and region.

- Market Diversification: Exhaustive information about new products, growing geographies, recent developments, and investments in the global animal wound care market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product & service offerings, and capabilities of leading players in the global animal wound care market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.2.3 Breakdown of primary interviews

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 KEY INDUSTRY INSIGHTS

- 2.3 MARKET BREAKDOWN & DATA TRIANGULATION

- 2.4 MARKET RANKING ANALYSIS

- 2.5 STUDY ASSUMPTIONS

- 2.6 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ANIMAL WOUND CARE MARKET OVERVIEW

- 4.2 ASIA PACIFIC: ANIMAL WOUND CARE MARKET, BY PRODUCT AND COUNTRY (2024)

- 4.3 ANIMAL WOUND CARE MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.4 ANIMAL WOUND CARE MARKET, BY REGION (2023-2030)

- 4.5 ANIMAL WOUND CARE MARKET: DEVELOPED VS. DEVELOPING ECONOMIES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Expanding companion animal population and pet ownership

- 5.2.1.2 Increasing adoption of pet insurance and high animal healthcare expenditure

- 5.2.1.3 Increasing demand for animal-derived food products

- 5.2.1.4 Rising prevalence of zoonotic diseases

- 5.2.2 RESTRAINTS

- 5.2.2.1 High cost of animal wound care products

- 5.2.2.2 Rising cost of pet care

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 High growth potential of emerging economies

- 5.2.3.2 Growing number of veterinarians in developed countries

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of animal healthcare awareness in emerging countries

- 5.2.4.2 Counterfeit or low-quality product circulation

- 5.2.1 DRIVERS

- 5.3 INDUSTRY TRENDS

- 5.3.1 POPULARITY OF VACUUM-ASSISTED/NEGATIVE-PRESSURE WOUND THERAPY FOR COMPANION ANIMALS

- 5.3.2 GROWING FUNDING FOR VETERINARY RESEARCH

- 5.4 TECHNOLOGY ANALYSIS

- 5.4.1 KEY TECHNOLOGIES

- 5.4.1.1 Biomaterials

- 5.4.1.2 Animal dermatology therapeutics

- 5.4.2 COMPLEMENTARY TECHNOLOGIES

- 5.4.2.1 Digital wound management

- 5.4.2.2 3D printing for customized wound solutions

- 5.4.3 ADJACENT TECHNOLOGIES

- 5.4.3.1 Wearable sensors for continuous monitoring

- 5.4.1 KEY TECHNOLOGIES

- 5.5 PORTER'S FIVE FORCES ANALYSIS

- 5.5.1 THREAT OF NEW ENTRANTS

- 5.5.2 THREAT OF SUBSTITUTES

- 5.5.3 BARGAINING POWER OF SUPPLIERS

- 5.5.4 BARGAINING POWER OF BUYERS

- 5.5.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.6 REGULATORY ANALYSIS

- 5.6.1 REGULATORY FRAMEWORK

- 5.6.1.1 North America

- 5.6.1.2 Europe

- 5.6.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.6.1 REGULATORY FRAMEWORK

- 5.7 PATENT ANALYSIS

- 5.7.1 INSIGHTS ON PATENT PUBLICATION TRENDS, TOP APPLICANTS, AND JURISDICTION FOR ANIMAL WOUND CARE MARKET

- 5.7.2 LIST OF MAJOR PATENTS, 2023-2024

- 5.8 PRICING ANALYSIS

- 5.8.1 AVERAGE SELLING PRICE TREND OF ANIMAL WOUND CARE PRODUCTS, BY KEY PLAYER, 2022-2024

- 5.8.2 AVERAGE SELLING PRICE TREND OF ANIMAL WOUND CARE PRODUCTS, BY REGION, 2022-2024

- 5.9 TRADE ANALYSIS

- 5.9.1 IMPORT DATA FOR HS CODE 300610, 2020-2024

- 5.9.2 EXPORT DATA FOR HS CODE 300610, 2020-2024

- 5.10 ECOSYSTEM ANALYSIS

- 5.11 VALUE CHAIN ANALYSIS

- 5.12 SUPPLY CHAIN ANALYSIS

- 5.13 REIMBURSEMENT SCENARIO

- 5.14 KEY CONFERENCES & EVENTS, 2025-2026

- 5.15 IMPACT OF AI/GEN AI ON ANIMAL WOUND CARE MARKET

- 5.16 UNMET NEEDS & END-USER EXPECTATIONS

- 5.17 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.17.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.17.2 BUYING CRITERIA

- 5.18 CASE STUDY ANALYSIS

- 5.18.1 CASE STUDY 1: ACELLULAR FISH-SKIN GRAFTS FOR COMPLEX CANINE WOUNDS-AVMA/AJVR CLINICAL SERIES

- 5.18.2 CASE STUDY 2: SILVER-CONTAINING DRESSINGS-SAFETY & ANTIMICROBIAL PERFORMANCE IN ANIMAL MODELS

- 5.18.3 CASE STUDY 3: AMNIOTIC-MEMBRANE AND ECM MATRICES IN VETERINARY WOUND MANAGEMENT (CANINE & EQUINE EVIDENCE)

- 5.19 TRENDS/DISRUPTION INFLUENCING CUSTOMERS' BUSINESSES

- 5.20 INVESTMENT & FUNDING SCENARIO

- 5.21 IMPACT OF 2025 US TARIFFS ON ANIMAL WOUND CARE MARKET

- 5.21.1 INTRODUCTION

- 5.21.2 KEY TARIFF RATES

- 5.21.3 PRICE IMPACT ANALYSIS

- 5.21.4 IMPACT ON COUNTRY/REGION

- 5.21.4.1 North America

- 5.21.4.2 Europe

- 5.21.4.3 Asia Pacific

- 5.21.5 IMPACT ON END-USE INDUSTRIES

- 5.21.5.1 Veterinary hospitals & clinics

- 5.21.5.2 Home care settings

- 5.21.5.3 Livestock farms

- 5.21.5.4 Rescue centers & NGOs

- 5.21.5.5 Livestock farms

- 5.21.5.6 Other end users

6 ANIMAL WOUND CARE MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- 6.2 SURGICAL WOUND CARE PRODUCTS

- 6.2.1 VOLUME ANALYSIS FOR SURGICAL WOUND CARE PRODUCTS, BY TYPE, 2023-2030 (THOUSAND UNITS)

- 6.2.2 SUTURES & STAPLERS

- 6.2.2.1 Growing number of veterinary conditions requiring surgeries to boost demand for sutures & staplers

- 6.2.3 TISSUE ADHESIVES, SEALANTS, AND GLUES

- 6.2.3.1 Effective closure of minor wounds, including simple traumatic lacerations and abrasions, to drive adoption

- 6.3 ADVANCED WOUND CARE PRODUCTS

- 6.3.1 FOAM DRESSINGS

- 6.3.1.1 Easy application and adequate insulation associated with foam dressings to boost growth

- 6.3.2 HYDROCOLLOID DRESSINGS

- 6.3.2.1 Ability of hydrocolloid dressings to promote healing and reduce infection to favor growth

- 6.3.3 FILM DRESSINGS

- 6.3.3.1 Increased ventilation of wounds associated with film dressings to boost growth

- 6.3.4 HYDROGEL DRESSINGS

- 6.3.4.1 Fast absorption of exudates to promote market growth

- 6.3.5 OTHER ADVANCED WOUND DRESSINGS

- 6.3.1 FOAM DRESSINGS

- 6.4 TRADITIONAL WOUND CARE PRODUCTS

- 6.4.1 TAPES

- 6.4.1.1 Tapes to dominate market during forecast period

- 6.4.2 DRESSINGS

- 6.4.2.1 Extensive usage of wound dressings to drive market

- 6.4.3 BANDAGES

- 6.4.3.1 Prevention of infection and faster wound healing to propel market growth

- 6.4.4 ABSORBENTS

- 6.4.4.1 Usage in highly exuding wounds and surgical drains to drive segment

- 6.4.5 OTHER TRADITIONAL WOUND CARE PRODUCTS

- 6.4.1 TAPES

- 6.5 THERAPY DEVICES

- 6.5.1 INCREASED EFFICIENCY AND REDUCED HOSPITALIZATION TO DRIVE MARKET

7 ANIMAL WOUND CARE MARKET, BY ANIMAL TYPE

- 7.1 INTRODUCTION

- 7.2 COMPANION ANIMALS

- 7.2.1 DOGS

- 7.2.1.1 Increasing adoption of dogs to drive market growth

- 7.2.2 CATS

- 7.2.2.1 Emerging trends in feline wound care to boost market growth

- 7.2.3 HORSES

- 7.2.3.1 Higher risk of traumatic injuries in horses to drive demand for animal wound care products

- 7.2.4 OTHER COMPANION ANIMALS

- 7.2.1 DOGS

- 7.3 LIVESTOCK ANIMALS

- 7.3.1 CATTLE

- 7.3.1.1 Economic importance of dairy and beef cattle to drive growth

- 7.3.2 SWINE

- 7.3.2.1 Growing surgical volume for acute conditions in swine to drive market growth

- 7.3.3 POULTRY

- 7.3.3.1 Growing focus on wound prevention and flock health management to boost market

- 7.3.4 OTHER LIVESTOCK ANIMALS

- 7.3.1 CATTLE

8 ANIMAL WOUND CARE MARKET, BY DISTRIBUTION CHANNEL

- 8.1 INTRODUCTION

- 8.2 RETAIL CHANNELS

- 8.2.1 IMPROVED ACCESSIBILITY AND MARKET REACH ASSOCIATED WITH RETAIL CHANNEL TO SUPPORT MARKET GROWTH

- 8.3 E-COMMERCE PLATFORMS

- 8.3.1 BETTER CONVENIENCE AND ACCESSIBILITY WITH E-COMMERCE PLATFORMS TO BOOST GROWTH

- 8.4 VETERINARY CLINICS & HOSPITALS (IN-HOUSE DISPENSING)

- 8.4.1 DELIVERY OF TRUSTED PRODUCTS UNDER PROFESSIONAL SUPERVISION TO DRIVE MARKET

- 8.5 DIRECT SALES CHANNELS

- 8.5.1 ABILITY OF DIRECT SALES TO STRENGTHEN MANUFACTURER-TO-CUSTOMER CONNECTIONS TO FUEL GROWTH

9 ANIMAL WOUND CARE MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.2 VETERINARY HOSPITALS & CLINICS

- 9.2.1 VETERINARY HOSPITALS & CLINICS TO DOMINATE MARKET DURING FORECAST PERIOD

- 9.3 HOME CARE SETTINGS

- 9.3.1 RISING PET EXPENDITURE TO PROPEL MARKET GROWTH

- 9.4 LIVESTOCK FARMS

- 9.4.1 GROWING IMPORTANCE AND OPPORTUNITIES IN ON-FARM WOUND CARE TO BOOST MARKET

- 9.5 RESCUE CENTERS & NGOS

- 9.5.1 GROWING NUMBER OF RESCUE CENTERS & NGOS TO SUPPORT MARKET GROWTH

- 9.6 OTHER END USERS

10 ANIMAL WOUND CARE MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 10.2.2 NORTH AMERICA: VOLUME ANALYSIS FOR SURGICAL WOUND CARE PRODUCTS, BY TYPE, 2023-2030 (THOUSAND UNITS)

- 10.2.3 US

- 10.2.3.1 Surge in animal healthcare expenditure to boost market growth

- 10.2.4 CANADA

- 10.2.4.1 Growing pet population and advanced veterinary services to drive market growth

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 10.3.2 EUROPE: VOLUME ANALYSIS FOR SURGICAL WOUND CARE PRODUCTS, BY TYPE, 2023-2030 (THOUSAND UNITS)

- 10.3.3 GERMANY

- 10.3.3.1 High focus on animal welfare to drive market demand for animal wound care products

- 10.3.4 UK

- 10.3.4.1 Increasing pet ownership to propel market

- 10.3.5 FRANCE

- 10.3.5.1 High standards of veterinary care to provide attractive growth opportunities for market players

- 10.3.6 ITALY

- 10.3.6.1 Growing pet owner awareness and increasing livestock population to drive market

- 10.3.7 SPAIN

- 10.3.7.1 Increasing awareness of animal health to drive market growth

- 10.3.8 POLAND

- 10.3.8.1 Steady market growth driven by expanding pet ownership and livestock sector to fuel growth

- 10.3.9 NETHERLANDS

- 10.3.9.1 Advanced veterinary infrastructure to support steady market expansion

- 10.3.10 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 10.4.2 ASIA PACIFIC: VOLUME ANALYSIS FOR SURGICAL WOUND CARE PRODUCTS, BY TYPE, 2023-2030 (THOUSAND UNITS)

- 10.4.3 JAPAN

- 10.4.3.1 Surge in pet care expenditure and growing adoption of companion animals to drive market

- 10.4.4 CHINA

- 10.4.4.1 China to register highest growth rate during forecast period

- 10.4.5 INDIA

- 10.4.5.1 Increasing livestock population to propel market growth

- 10.4.6 AUSTRALIA

- 10.4.6.1 Growing companion animal ownership and rise in animal health awareness to support market growth

- 10.4.7 SOUTH KOREA

- 10.4.7.1 Growing pet ownership and advancements in veterinary medicine to favor growth

- 10.4.8 THAILAND

- 10.4.8.1 Tourism-linked pet culture and veterinary advancements to fuel market growth

- 10.4.9 INDONESIA

- 10.4.9.1 Government livestock programs and disease control efforts to boost market demand

- 10.4.10 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 10.5.2 LATIN AMERICA: VOLUME ANALYSIS FOR SURGICAL WOUND CARE PRODUCTS, BY TYPE, 2023-2030 (THOUSAND UNITS)

- 10.5.3 BRAZIL

- 10.5.3.1 Brazil to dominate Latin American market

- 10.5.4 MEXICO

- 10.5.4.1 Robust livestock base and growing companion animal care to drive Mexico's animal wound care market

- 10.5.5 ARGENTINA

- 10.5.5.1 Argentina's animal wound care market to face moderate growth amid livestock focus

- 10.5.6 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 10.6.2 MIDDLE EAST & AFRICA: VOLUME ANALYSIS FOR SURGICAL WOUND CARE PRODUCTS, BY TYPE, 2023-2030 (THOUSAND UNITS)

- 10.6.3 GCC COUNTRIES

- 10.6.3.1 Kingdom of Saudi Arabia (KSA)

- 10.6.3.1.1 Vision 2030 investments to drive market growth

- 10.6.3.2 United Arab Emirates (UAE)

- 10.6.3.2.1 Increasing adoption of advanced diagnostic technologies to contribute to market growth

- 10.6.3.3 Rest of GCC Countries

- 10.6.3.1 Kingdom of Saudi Arabia (KSA)

- 10.6.4 REST OF MIDDLE EAST & AFRICA

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.3 REVENUE ANALYSIS, 2022-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.4.1 MARKET SHARE ANALYSIS FOR US, 2024

- 11.4.2 MARKET SHARE ANALYSIS FOR EUROPE, 2024

- 11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- 11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.5.5.1 Company footprint

- 11.5.5.2 Region footprint

- 11.5.5.3 Product footprint

- 11.5.5.4 Animal type footprint

- 11.5.5.5 Distribution channel footprint

- 11.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- 11.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.6.5.1 Detailed list of key startups/SMEs

- 11.6.5.2 Competitive benchmarking of key startups/SMEs

- 11.7 R&D EXPENDITURE OF KEY PLAYERS

- 11.8 COMPANY VALUATION & FINANCIAL METRICS

- 11.8.1 COMPANY VALUATION

- 11.8.2 FINANCIAL METRICS

- 11.9 BRAND/PRODUCT COMPARISON

- 11.10 COMPETITIVE SCENARIO

- 11.10.1 PRODUCT LAUNCHES & APPROVALS

- 11.10.2 DEALS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 B. BRAUN SE

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 MnM view

- 12.1.1.3.1 Right to win

- 12.1.1.3.2 Strategic choices

- 12.1.1.3.3 Weaknesses & competitive threats

- 12.1.2 MEDTRONIC PLC

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 MnM view

- 12.1.2.3.1 Right to win

- 12.1.2.3.2 Strategic choices

- 12.1.2.3.3 Weaknesses & competitive threats

- 12.1.3 3M COMPANY

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 Recent developments

- 12.1.3.4 MnM view

- 12.1.3.4.1 Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses & competitive threats

- 12.1.4 VIRBAC

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 Recent developments

- 12.1.4.4 MnM view

- 12.1.4.4.1 Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses & competitive threats

- 12.1.5 DECHRA PHARMACEUTICALS PLC

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.5.3 MnM view

- 12.1.5.3.1 Right to win

- 12.1.5.3.2 Strategic choices

- 12.1.5.3.3 Weaknesses & competitive threats

- 12.1.6 NEOGEN CORPORATION

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.6.3 Recent developments

- 12.1.7 JORGEN KRUUSE A/S

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.8 SONOMA PHARMACEUTICALS, INC.

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Product launches & approvals

- 12.1.9 ETHICON, INC.

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.10 ZOETIS INC.

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.11 JAZZ MEDICAL, LLC

- 12.1.11.1 Business overview

- 12.1.11.2 Products offered

- 12.1.12 KERICURE INC.

- 12.1.12.1 Business overview

- 12.1.12.2 Products offered

- 12.1.13 ADVANCIS MEDICAL

- 12.1.13.1 Business overview

- 12.1.13.2 Products offered

- 12.1.14 VERNACARE LTD.

- 12.1.14.1 Business overview

- 12.1.14.2 Products offered

- 12.1.15 CREATIVE SCIENCE

- 12.1.15.1 Business overview

- 12.1.15.2 Products offered

- 12.1.15.3 Recent developments

- 12.1.16 THE WOUND VAC COMPANY, LLC

- 12.1.16.1 Business overview

- 12.1.16.2 Products offered

- 12.1.17 DOMES PHARMA, INC.

- 12.1.17.1 Business overview

- 12.1.17.2 Products offered

- 12.1.17.3 Recent developments

- 12.1.1 B. BRAUN SE

- 12.2 OTHER PLAYERS

- 12.2.1 PRIMAVET INC.

- 12.2.2 INNOVACYN, INC.

- 12.2.3 SILVERGLIDE

- 12.2.4 VETOQUINOL

- 12.2.5 MILLPLEDGE LTD.

- 12.2.6 OVIK HEALTH

- 12.2.7 HYDROFERA

- 12.2.8 RIVERPOINT MEDICAL

- 12.2.9 INTERNACIONAL FARMACEUTICA S.A. DE C.V.

- 12.2.10 ORION SUTURES INDIA PVT. LTD.

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.3.1 PRODUCT ANALYSIS

- 13.3.2 GEOGRAPHIC ANALYSIS

- 13.3.3 COMPANY INFORMATION

- 13.3.4 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 13.3.5 COUNTRY-LEVEL VOLUME ANALYSIS, BY PRODUCT

- 13.3.6 MARKET SHARE ANALYSIS, BY PRODUCT (TOP 5 PLAYERS)

- 13.3.7 ANY CONSULTS/CUSTOM REQUIREMENTS AS PER CLIENT REQUEST

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS