|

시장보고서

상품코드

1880373

생체인식 시스템 시장(-2030년) : 인증 방식(지문, 홍채, 얼굴, 음성, 정맥, 장문, 서명, 다요소, 보행, 키스트로크), 제공 구분(센서, 카메라, 리더, 스캐너, 소프트웨어 및 서비스), 유형(접촉형, 비접촉형), 모빌리티별Biometric System Market by Authentication (Fingerprint, Iris, Face, Voice, Vein, Palm, Signature, Multi-factor, Gait, Keystrokes), Offering (Sensor, Camera, Reader, Scanner, Software, Service), Contact, Contactless, Mobility - Global Forecast to 2030 |

||||||

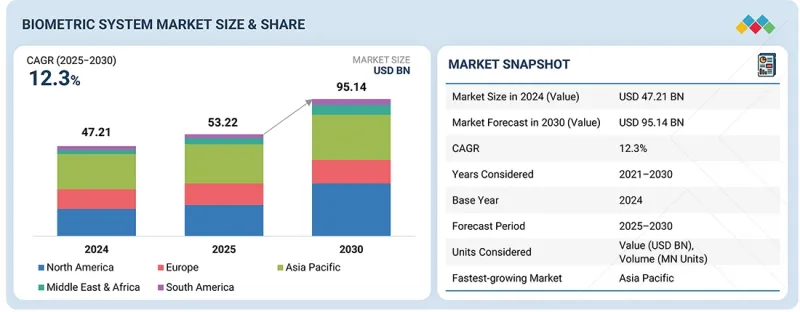

생체인식 시스템 시장 규모는 2025년 532억 2,000만 달러에서 2025-2032년 CAGR 12.3%로 성장하여 2030년에는 951억 4,000만 달러에 이를 것으로 예측됩니다.

스마트폰, 노트북, 태블릿, 웨어러블, 스마트홈 기기에 고도의 생체 인식 기능이 통합되면서 CE 제품의 생체 인식 기술에 대한 수요가 빠르게 증가하고 있습니다. 지문 센서, 얼굴 인식, 홍채 스캔, 음성 인식은 많은 기기에서 표준으로 채택되어 안전하고 편리한 사용자 액세스를 제공하는 동시에 전반적인 사용자 경험을 향상시키고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러) |

| 부문 | 제공 구분, 유형, 산업, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

모바일 결제, 디지털 지갑, 온라인 뱅킹의 성장과 함께 소비자들이 보안과 편의성을 중시하는 가운데, 신뢰할 수 있는 생체 인증의 필요성이 가속화되고 있습니다. 또한, 스마트 워치, 피트니스 트래커와 같은 웨어러블 기기에서는 건강 매개변수 모니터링, 활동 추적, 안전한 기기 액세스를 제공하기 위해 생체 인식 센서를 점점 더 많이 활용하고 있습니다. 보안 시스템, 도어락, 홈 어시스턴트 등 스마트홈 제품도 부정 접근을 방지하기 위해 생체 인식 솔루션을 통합하고 있습니다. 디지털화의 진전, IoT 기기의 보급 확대, 개인화되고 안전한 경험을 원하는 소비자 니즈가 맞물려 괄목할 만한 성장을 견인하고 있습니다. 기술의 발전, 센서의 소형화, AI를 활용한 분석으로 보다 정확하고 원활한 인증이 가능해짐에 따라 CE 제품은 생체 인식 시스템 시장에서 높은 성장 기회로 자리매김하고 있습니다.

"소프트웨어 부문이 2025년과 2030년 시장에서 주요 점유율을 차지할 것으로 예측됩니다."

소프트웨어 부문은 고급 ID 관리, 인증 및 분석 솔루션에 대한 수요 증가로 인해 2025년과 2030년 시장에서 중요한 점유율을 차지할 것으로 예측됩니다. 생체 인식 소프트웨어는 지문, 얼굴, 홍채, 음성 인식 등 다양한 방식으로 정확한 데이터 수집, 처리 및 검증을 가능하게 합니다. 클라우드 기반의 AI 지원 소프트웨어 솔루션은 실시간 분석, 부정행위 감지, 기업 보안 시스템과의 통합을 가능하게 하며, 정부, 은행, 의료, 기업용 대규모 도입에 필수적입니다. 또한, 소프트웨어 플랫폼은 모바일 기기, IoT 네트워크, 출입통제 시스템과의 원활한 통합을 촉진하여 확장성과 운영 효율성을 향상시킵니다. 안전한 디지털 거래, 전자정부 정책, 규제 준수에 대한 강조는 첨단 생체인식 소프트웨어 솔루션의 도입을 더욱 촉진하고 있습니다. AI, 머신러닝, 패턴 인식 기술의 지속적인 발전으로 시스템의 정확성과 신뢰성이 향상되면서 전체 시장에서 소프트웨어의 중요성이 더욱 커지고 있습니다. 그 결과, 견고하고 유연하며 확장성을 갖춘 생체 인식 소프트웨어를 제공하는 벤더가 예측 기간 동안 시장 수익의 상당 부분을 차지할 것으로 예측됩니다.

"모바일 배포 부문은 2025년부터 2030년까지 연평균 성장률(CAGR)이 두드러질 것으로 예측됩니다."

이는 생체인식 기능을 통합한 스마트폰, 태블릿, 웨어러블 기기의 보급에 힘입은 바 큽니다. 지문 센서, 얼굴 인식, 홍채 스캔을 포함한 모바일 생체 인증은 기기 접속, 모바일 결제, 디지털 뱅킹, 본인 확인에 있어 안전하고 편리하며 빠른 인증을 제공합니다. 모바일 지갑, 온라인 뱅킹, 비접촉식 결제 솔루션의 이용 확대는 편리함을 유지하면서도 보안을 강화하고자 하는 사용자들 수요를 더욱 가속화시키고 있습니다. 모바일 생체 인증은 멀티 용도 기능도 지원하여 기업 및 서비스 제공업체가 모바일 앱, 기업 네트워크, 의료 플랫폼에 대한 안전한 액세스를 도입할 수 있도록 지원합니다. 모바일 센서 기술, AI 기반 인식 기술, 클라우드 통합 기술의 발전으로 정확성, 신뢰성, 사용자 경험이 향상되고 있습니다. 또한, 신흥 시장에서의 스마트폰 보급률 증가, 정부 및 기업의 모바일 기반 디지털 ID 프로그램 도입 노력으로 인해 더욱 성장하고 있습니다. 모바일 기기가 일상적인 거래, 통신, 보안 운영의 핵심으로 자리 잡으면서 모바일 부문은 생체인식 시스템 시장에서 가장 빠르게 성장할 것으로 예측됩니다.

"지역별로는 아시아태평양이 2024년 가장 큰 점유율을 차지할 것"

아시아태평양은 빠른 기술 도입, 정부 지원 정책, 보안 및 ID 관리에 대한 높은 투자로 인해 2024년 가장 큰 점유율을 차지했습니다. 중국, 인도, 일본, 한국 등의 국가에서는 대규모 디지털 ID 프로그램, 전자정부 이니셔티브, 스마트시티 프로젝트가 시행되고 있으며, 생체 인식 시스템의 광범위한 도입이 추진되고 있습니다. 방대한 인구, 스마트폰 보급률 증가, 기업 및 공공 부문의 인프라 확대가 수요를 더욱 가속화시키고 있습니다. 주요 응용 분야는 국경 보안, 법 집행 기관, 은행, 의료, 교통 등이며, 생체 인식 기술은 정확한 신원 확인, 출입 통제, 부정 방지를 보장합니다. 현지 기술 제공업체와 스타트업의 존재는 AI 기반, 비접촉식, 클라우드 통합형 생체인증 솔루션의 혁신을 촉진하고 경쟁 구도를 형성하고 있습니다. 또한, 데이터 보안과 프라이버시, 원활한 인증에 대한 소비자의 인식 개선도 도입을 촉진하고 있습니다. 기술 발전, 민관 협력, 지속적인 연구개발을 통해 이 지역 시장 우위는 앞으로도 지속될 것으로 예상되며, 벤더들에게 큰 성장 기회를 제공하는 동시에 전 세계 생체인식 시스템 도입의 주요 거점으로 자리매김할 것으로 전망됩니다.

세계의 생체 인식 시스템(Biometric Systems) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

제5장 업계 동향

- Porter의 Five Forces 분석

- 밸류체인 분석

- 생태계 분석

- 가격 분석

- 무역 분석

- 2025-2026년 주요 컨퍼런스 및 이벤트

- 고객 사업에 영향을 미치는 동향/혼란

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 2025년 미국 관세의 영향

- 주요 기술

- 보완적 기술

- 기술 로드맵

- 특허 분석

- 생성형 AI/AI가 생체인식 시스템 시장에 미치는 영향

제7장 규제 상황

- 지역 규제와 컴플라이언스

제8장 고객 상황과 구매 행동

- 의사결정 프로세스

- 이해관계자와 구입 평가 기준

- 채택 장벽과 내부 과제

- 시장 수익성

제9장 생체인식 시스템 시장 : 용도별

- 액세스 제어 및 인증

- 근태 관리

- 본인 확인

- 감시 및 보안

- 결제 및 거래 처리

- 기타(부정행위 감지)

제10장 생체인식 시스템 시장 : 바이오메트릭 특성별

- 생물학적/생리학적

- DNA/혈액

- 형태학적

- 손 기하학

- 얼굴

- 홍채

- 망막

- 목소리

- 행동적

- GAIT

- 서명

- 키보드 입력

제11장 생체인식 시스템 시장 : 네트워크 접속별

- 오프라인/스탠드얼론

- LAN

- Wi-Fi 대응

- 셀룰러(4G/5G)

- BLUETOOTH/NFC

제12장 생체인식 시스템 시장 : 인증 유형별

- 단요소 인증

- 지문 인식

- 홍채 인식

- 손바닥 인식

- 얼굴 인식

- 정맥 인식

- 서명 인식

- 음성 인식

- 기타

- 다중 인증

- 2요소

- 3요소

- 4요소

- 5요소

제13장 생체인식 시스템 시장 : 모빌리티별

- 고정형

- 휴대형

제14장 생체인식 시스템 시장 : 제공 구분별

- 하드웨어

- 지문 센서

- 리더/스캐너

- 카메라

- 기타

- 소프트웨어

- 생체인식 관리 소프트웨어

- 서비스

제15장 생체인식 시스템 시장 : 유형별

- 접촉형

- 비접촉형

- 하이브리드

제16장 생체인식 시스템 시장 : 전개 구분별

- On-Premise

- 클라우드 기반

제17장 생체인식 시스템 시장 : 산업별

- 정부

- 국민 ID

- 법집행기관

- 국경 관리, 보안

- 군 및 방위

- 국방 기지, 군수 창고 및 제한 구역에 대한 접근 통제

- 군인 및 계약업체 신원 확인

- 무기 접근 권한 부여

- 얼굴 인식 기술을 활용한 감시 및 모니터링

- 보안 통신 인증

- 건강 관리

- 환자 신원 확인을 통한 혼동 방지

- 제한된 실험실/약국 내 의료진 접근 통제

- 전자건강기록(EHR/EMR) 인증

- 처방전 조제 검증

- 의료진 근무 시간 및 출퇴근 기록 관리

- 은행, 금융서비스 및 보험(BFSI)

- 모바일 뱅킹 앱을 위한 생체 인증

- 지문/홍채를 이용한 ATM 접근 및 인출 승인

- 계좌 개설 시 KYC 검증

- 행동 생체 인식 기반 사기 탐지

- POS 또는 온라인 결제 시 생체 인식 결제

- 암호화폐

- CE 제품

- 스마트폰

- 노트북 및 태블릿

- 게임기 및 VR 헤드셋

- 웨어러블

- 음성/얼굴 인식 기능 스마트홈 디바이스

- 여행 및 입국 관리

- 자동화 국경 통제 게이트

- 생체 인식 정보가 내장된 전자 여권

- 항공 여객 체크인 및 탑승 인증

- 상용 고객 프로그램 검증

- 출입국 관리 및 비자 처리

- 자동차

- 차량 액세스/스타트을 위한 운전자 식별(지문/얼굴)

- 차량 접근/시동을 위한 운전자 식별 (지문/얼굴)

- 생체 인식 기반 맞춤형 차량 내 설정 (좌석, 인포테인먼트)

- 생체 인식 시동 인증을 활용한 차량 도난 방지 보안

- 차량 관리 - 운전자 모니터링 및 검증

- 안전을 위한 알코올 감지 및 운전자 생체 인식 결합 감지

- 안전

- 홈 보안

- 상업 보안

- 기타

- 산업

- 유틸리티

- 스포츠

- 엔터테인먼트

제18장 생체인식 시스템 시장 : 지역별

- 아시아태평양

- 거시경제 전망

- 중국

- 일본

- 한국

- 인도

- 호주

- 기타

- 북미

- 거시경제 전망

- 미국

- 캐나다

- 멕시코

- 유럽

- 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타

- 기타 지역

- 거시경제 전망

- 중동

- 아프리카

- 남미

제19장 경쟁 구도

- 개요

- 주요 시장 진출기업의 전략/강점

- 매출 분석

- 시장 점유율 분석

- 브랜드/제품 비교

- 기업 평가 매트릭스 : 주요 기업

- 기업 평가 매트릭스 : 스타트업/중소기업

- 기업 평가와 재무 지표

- 경쟁 시나리오

제20장 기업 개요

- 주요 기업

- THALES

- IDEMIA

- NEC CORPORATION

- ASSA ABLOY

- FUJITSU

- PRECISE BIOMETRICS

- SECUNET SECURITY NETWORKS AG

- AWARE INC.

- COGNITEC SYSTEMS GMBH

- ANVIZ GLOBAL INC.

- 기타 주요 기업

- DAON, INC.

- DERMALOG IDENTIFICATION SYSTEMS GMBH

- NEUROTECHNOLOGY

- INNOVATRICS

- VERIDOS GMBH

- ZETES

- JUMIO

- IPROOV

- FACETEC, INC.

- MITEK SYSTEMS, INC.

- BEIJING KUANGSHI TECHNOLOGY CO., LTD.(MEGVII)

- SENSETIME

- FACEBANX

- BIO-KEY INTERNATIONAL

- SECURIPORT

- M2SYS TECHNOLOGY

- SUPREMA INC.

- FULCRUM BIOMETRICS

- ONESPAN

- QUALCOMM TECHNOLOGIES, INC.

- INTEGRATED BIOMETRICS

- LEIDOS

- PAPILLON

- NUANCE COMMUNICATIONS, INC.

제21장 조사 방법

제22장 부록

LSH 25.12.10The biometric system market is projected to be valued at USD 53.22 billion in 2025 and USD 95.14 billion by 2030, registering a CAGR of 12.3% from 2025 to 2030. The demand for biometric technology in consumer electronics is rapidly increasing as smartphones, laptops, tablets, wearables, and smart home devices integrate advanced biometric authentication features. Fingerprint sensors, facial recognition, iris scanning, and voice recognition are standard in many devices, offering secure and convenient user access while enhancing overall user experience.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Offering, Type, Vertical and Region |

| Regions covered | North America, Europe, APAC, RoW |

The growth of mobile payments, digital wallets, and online banking has accelerated the need for reliable biometric authentication, as consumers prioritize security and convenience. Additionally, wearable devices, such as smartwatches and fitness trackers, increasingly leverage biometric sensors to monitor health parameters, track activities, and provide secure device access. Smart home products, including security systems, door locks, and home assistants, also integrate biometric solutions to prevent unauthorized access. The combination of rising digitalization, growing adoption of IoT devices, and consumer demand for personalized, secure experiences drives significant growth. Technology advancements, miniaturization of sensors, and AI-powered analytics further enable precise and seamless authentication, positioning consumer electronics as a high-growth opportunity within the biometric system market.

"Software segment is likely to contribute a major share of the biometric system market in 2025 and 2030."

The software segment is expected to account for a significant share of the biometric system market in 2025 and 2030, driven by the growing demand for advanced identity management, authentication, and analytics solutions. Biometric software enables accurate data capture, processing, and verification across multiple modalities, including fingerprint, facial, iris, and voice recognition. Cloud-based and AI-enabled software solutions allow real-time analytics, fraud detection, and integration with enterprise security systems, making them essential for large-scale deployments in government, banking, healthcare, and enterprise applications. Additionally, software platforms facilitate seamless integration with mobile devices, IoT networks, and access control systems, enhancing scalability and operational efficiency. The increasing emphasis on secure digital transactions, e-governance initiatives, and regulatory compliance further drives the adoption of sophisticated biometric software solutions. Continuous advancements in AI, machine learning, and pattern recognition enhance system accuracy and reliability, further reinforcing the importance of software in the overall market. Consequently, vendors focusing on robust, flexible, and scalable biometric software are expected to capture a substantial portion of market revenue during the forecast period.

"Mobile deployment mode segment is expected to record a significant CAGR from 2025 to 2030."

The mobile segment is projected to register the highest CAGR in the biometric system market during the forecast period due to the widespread adoption of smartphones, tablets, and wearable devices integrated with biometric authentication features. Mobile biometrics, including fingerprint sensors, facial recognition, and iris scanning, offer secure, convenient, and fast authentication for device access, mobile payments, digital banking, and identity verification. The growing use of mobile wallets, online banking, and contactless payment solutions has further accelerated the demand, as users seek enhanced security without compromising convenience. Mobile biometrics also support multi-application functionality, enabling enterprises and service providers to deploy secure access for mobile apps, corporate networks, and healthcare platforms. Technological advancements in mobile sensors, AI-driven recognition, and cloud integration are improving accuracy, reliability, and user experience. Additionally, the rising penetration of smartphones in emerging markets and government and enterprise initiatives to adopt mobile-based digital identity programs further propel growth. As mobile devices become central to daily transactions, communications, and security operations, the mobile segment is poised to experience the fastest expansion in the biometric system market.

"Asia Pacific accounted for the largest share of the biometric system market in 2024."

Asia Pacific held the largest share of the biometric system market in 2024, fueled by rapid technological adoption, supportive government initiatives, and high investment in security and identity management. Countries such as China, India, Japan, and South Korea are implementing large-scale digital identity programs, e-governance initiatives, and smart city projects, driving widespread deployment of biometric systems. The substantial population, rising smartphone penetration, and expanding enterprise and public sector infrastructure further accelerate demand. Key applications include border security, law enforcement, banking, healthcare, and transportation, where biometrics ensure accurate identification, access control, and fraud prevention. The presence of local technology providers and startups fosters innovation in AI-powered, contactless, and cloud-integrated biometric solutions, creating a competitive market landscape. Additionally, increasing consumer awareness about data security, privacy, and seamless authentication contributes to adoption. With technological advancements, public-private collaborations, and continuous R&D, the regional market dominance is expected to continue, offering significant growth opportunities for vendors and positioning the region as a leading hub for global biometric system deployment.

- By Company Type: Tier 1 - 38%, Tier 2 - 28%, and Tier 3 - 34%

- By Designation: C-level Executives - 40%, Managers - 30%, and Others - 30%

- By Region: North America - 35%, Europe - 35%, Asia Pacific- 20%, and RoW - 10%

Prominent players profiled in this report include Renishaw plc (UK), Keysight Technologies (US), ZEISS Group (Germany), Zygo Corporation (US), and Bruker (US).

Report Coverage

The report defines, describes, and forecasts the biometric system market based on authentication type (single-factor authentication, multi-factor authentication), offering (hardware, software), type (contact-based, contactless, hybrid), mobility (fixed, portable), deployment mode (on-premises, cloud-based), and region (North America, Europe, Asia Pacific, RoW). It provides detailed information regarding drivers, restraints, opportunities, and challenges influencing the market growth. It also analyzes competitive developments such as acquisitions, product launches, expansions, and actions carried out by key players to grow in the market.

Reasons to Buy This Report

The report will help the market leaders/new entrants with information on the closest approximations of the revenue for the overall biometric system market and the subsegments. The report will help stakeholders understand the competitive landscape and gain more insight to position their business better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market's pulse and provides information on key drivers, restraints, opportunities, and challenges.

The report will provide insights into the following points:

- Analysis of key drivers (Surging demand for biometric technology-enabled consumer electronics, Elevating use of biometrics in government projects to enhance security and efficiency, Escalating deployment of biometrics in security and surveillance applications due to increasing terrorism, Rising focus of automakers on enhancing vehicle safety, Pressing need to protect smart infrastructure from cyber threat), restraints (High costs associated with biometric systems, Stringent regulations related to biometric data collection, storage, and processing), opportunities (Development of AI- and ML-based biometric solutions, Collaborative strategies among participants in supply chain, Increasing number of subscribers for BaaS, Transition of businesses toward IoT and cloud technologies), and challenges (Data security concerns and shortage of technical knowledge, Detecting authorized and unauthorized users, System integration-related challenges) in the biometric system market

- Product developments/innovations: Detailed insights into upcoming technologies, research & development activities, and new product launches in the biometric system market

- Market developments: Comprehensive information about lucrative markets; the report analyses the biometric system market across various regions

- Market diversification: Exhaustive information about new products launched, untapped geographies, recent developments, and investments in the biometric system market

- Competitive assessment: In-depth assessment of market share, growth strategies, and offering of leading players, including Thales (France), IDEMIA (France), ASSA ABLOY (Sweden), NEC Corporation (Japan), Fujitsu (Japan), Precise Biometrics (Sweden), secunet Security Networks AG (Germany), Anviz Global Inc. (US), and Aware Inc. (US), in the biometric system market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.3.6 LIMITATIONS

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN BIOMETRIC SYSTEM MARKET

- 3.2 BIOMETRIC SYSTEM MARKET IN NORTH AMERICA, BY COUNTRY AND AUTHENTICATION TYPE

- 3.3 BIOMETRIC SYSTEM MARKET IN ASIA PACIFIC, BY VERTICAL

- 3.4 BIOMETRIC SYSTEM MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Surging demand for biometric technology-enabled consumer electronics

- 4.2.1.2 Use in government projects to enhance security and efficiency

- 4.2.1.3 Deployment of biometrics in security and surveillance applications due to increasing terrorism

- 4.2.1.4 Rising focus of automakers on enhancing vehicle safety

- 4.2.1.5 Pressing need to protect smart infrastructure from cyberthreats

- 4.2.2 RESTRAINTS

- 4.2.2.1 High costs associated with biometric systems

- 4.2.2.2 Stringent regulations related to biometric data collection, storage, and processing

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Development of AI- and ML-based biometric solutions

- 4.2.3.2 Collaborative strategies among participants in supply chain

- 4.2.3.3 Increasing number of subscribers for BaaS

- 4.2.3.4 Transition of businesses toward IoT and cloud technologies

- 4.2.4 CHALLENGES

- 4.2.4.1 Data security concerns and shortage of technical knowledge

- 4.2.4.2 Detecting authorized and unauthorized users

- 4.2.4.3 System integration-related challenges

- 4.2.1 DRIVERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF NEW ENTRANTS

- 5.1.5 THREAT OF SUBSTITUTES

- 5.2 VALUE CHAIN ANALYSIS

- 5.3 ECOSYSTEM ANALYSIS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY FINGERPRINT SENSOR TECHNOLOGY

- 5.4.2 AVERAGE SELLING PRICE TREND OF IRIS SCANNERS, BY KEY PLAYER

- 5.4.3 AVERAGE SELLING PRICE TREND OF FINGERPRINT SENSOR TECHNOLOGIES, BY REGION

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT DATA (HS CODE 847190)

- 5.5.2 EXPORT DATA (HS CODE 847190)

- 5.6 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 EUROPEAN UNION DEPLOYS SBMS TO ENHANCE BORDER SECURITY

- 5.9.2 UAE FACILITATES MULTI-BIOMETRIC ENTRY/EXIT PROGRAMS FOR SMOOTH BORDER CROSSINGS

- 5.9.3 THALES AND GEMALTO IMPLEMENT ADVANCED BIOMETRIC SOLUTIONS TO ENHANCE ELECTORAL INTEGRITY

- 5.9.4 NEC IMPLEMENTS FACIAL RECOGNITION SYSTEM AT HEADQUARTERS TO SECURE ENTRY

- 5.10 IMPACT OF 2025 US TARIFF - BIOMETRIC SYSTEM MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 KEY IMPACTS ON VARIOUS COUNTRY/REGION

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 END-USE INDUSTRY IMPACT

6 STRATEGIC DISRUPTIONS THROUGH TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 CLOUD-BASED BIOMETRIC SYSTEM

- 6.1.2 FINGER-VEIN RECOGNITION

- 6.1.3 3D FACE RECOGNITION

- 6.1.4 FINGERPRINT RECOGNITION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 LIVENESS DETECTION

- 6.2.2 MULTIMODAL BIOMETRICS

- 6.2.3 INTERNET OF THINGS

- 6.2.4 ARTIFICIAL INTELLIGENCE AND MACHINE LEARNING

- 6.3 TECHNOLOGY ROADMAP

- 6.4 PATENT ANALYSIS

- 6.5 IMPACT OF GEN/AI ON BIOMETRIC SYSTEM MARKET

- 6.5.1 INTRODUCTION

- 6.5.2 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2.1 Facial recognition

- 6.5.2.2 Iris recognition

- 6.5.2.3 Palm recognition

- 6.5.2.4 Vein recognition

- 6.5.2.5 Signature recognition

- 6.5.3 BEST PRACTICES

- 6.5.3.1 Case study

- 6.5.4 INTERCONNECT ADJACENT ECOSYSTEM

- 6.5.5 ADOPTION OF AI BY CLIENTS/READINESS TO ADOPT AI

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.1.1 Other regional regulations

- 7.1.2 INDUSTRY STANDARDS

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

8 CUSTOMER LANDSCAPE & BUYING BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 MARKET PROFITABILITY

- 8.4.1 REVENUE POTENTIAL

- 8.4.2 COST DYNAMICS

- 8.4.3 MARGIN OPPORTUNITIES, BY APPLICATION

9 BIOMETRIC SYSTEMS MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 ACCESS CONTROL & AUTHENTICATION

- 9.2.1 SECURING CRITICAL ENTRY POINTS WITH BIOMETRIC AUTHORIZATION

- 9.3 TIME & ATTENDANCE TRACKING

- 9.3.1 STREAMLINING WORKFORCE ADMINISTRATION THROUGH AUTOMATED BIOMETRIC TRACKING

- 9.4 IDENTITY VERIFICATION

- 9.4.1 DRIVING TRUST AND COMPLIANCE IN FINTECH, TELECOM, AND PUBLIC SERVICES

- 9.5 SURVEILLANCE & SECURITY

- 9.5.1 AUTOMATING PASSENGER IDENTITY MANAGEMENT AT BORDERS AND AIRPORTS

- 9.5.2 ENHANCING NATIONAL SECURITY THROUGH BIOMETRIC BORDER MANAGEMENT

- 9.6 PAYMENT & TRANSACTION PROCESSING

- 9.6.1 EMPOWERING CONTACTLESS TRANSACTIONS THROUGH BIOMETRIC WALLETS AND POS SYSTEMS

- 9.7 OTHERS (FRAUD DETECTION)

10 BIOMETRIC TRAITS OF BIOMETRIC SYSTEMS MARKET

- 10.1 INTRODUCTION

- 10.2 BIOLOGICAL/PHYSIOLOGICAL

- 10.2.1 DNA/BLOOD

- 10.2.1.1 Forensic and high security applications

- 10.2.1.2 Processing time and challenges

- 10.2.1 DNA/BLOOD

- 10.3 MORPHOLOGICAL

- 10.3.1 HAND GEOMETRY

- 10.3.1.1 Legacy system transition analysis

- 10.3.1.2 Niche applications

- 10.3.1.3 Palm vein

- 10.3.1.4 Fingerprint

- 10.3.2 FACE

- 10.3.2.1 2D

- 10.3.2.2 3D

- 10.3.2.3 AI-enhanced

- 10.3.3 IRIS

- 10.3.3.1 Near infrared vs. visible light system

- 10.3.3.2 Accuracy and security advantages

- 10.3.3.3 Adoption barriers

- 10.3.4 RETINA

- 10.3.5 VOICE

- 10.3.1 HAND GEOMETRY

- 10.4 BEHAVIORAL

- 10.4.1 GAIT

- 10.4.1.1 Surveillance and security

- 10.4.1.2 Technological limitations

- 10.4.1.3 Healthcare and elderly care

- 10.4.2 SIGNATURES

- 10.4.2.1 Static vs. dynamic

- 10.4.2.2 Digital transformation impact

- 10.4.3 KEYBOARD STROKES

- 10.4.3.1 Enterprise security integration

- 10.4.3.2 Continuous authentication

- 10.4.1 GAIT

11 BIOMETRIC SYSTEMS MARKET, BY NETWORK CONNECTIVITY

- 11.1 INTRODUCTION

- 11.2 OFFLINE/STANDALONE

- 11.3 LAN

- 11.4 WI-FI ENABLED

- 11.5 CELLULAR(4G/5G)

- 11.6 BLUETOOTH/NFC

12 BIOMETRIC SYSTEM MARKET, BY AUTHENTICATION TYPE

- 12.1 INTRODUCTION

- 12.2 SINGLE-FACTOR

- 12.2.1 FINGERPRINT RECOGNITION

- 12.2.1.1 AFIS

- 12.2.1.1.1 High reliance on biometrics for criminal identification and forensic investigations to boost demand

- 12.2.1.2 Non-AFIS

- 12.2.1.2.1 Surging deployment in educational institutions to support market growth

- 12.2.1.1 AFIS

- 12.2.2 IRIS RECOGNITION

- 12.2.2.1 Rising demand from government sector to fuel segmental growth

- 12.2.3 PALM PRINT RECOGNITION

- 12.2.3.1 Growing concerns over security across various sectors to accelerate market growth

- 12.2.4 FACE RECOGNITION

- 12.2.4.1 Increasing use of surveillance and security applications to spur demand

- 12.2.5 VEIN RECOGNITION

- 12.2.5.1 Rising demand for high security in banking and immigration to foster growth

- 12.2.6 SIGNATURE RECOGNITION

- 12.2.6.1 Requirement for convenience in banking & finance to support market growth

- 12.2.7 VOICE RECOGNITION

- 12.2.7.1 Low operational cost, better accuracy, and simplified design to boost demand

- 12.2.8 OTHER SINGLE-FACTOR AUTHENTICATION TYPES

- 12.2.1 FINGERPRINT RECOGNITION

- 12.3 MULTI-FACTOR

- 12.3.1 TWO-FACTOR

- 12.3.1.1 Biometric smart cards

- 12.3.1.1.1 Rising demand for managing access to buildings, secure areas, and IT systems to drive market

- 12.3.1.2 Biometric PIN

- 12.3.1.2.1 Increasing adoption in educational institutions to fuel market

- 12.3.1.3 Two-factor biometric technology

- 12.3.1.3.1 Growing preference for multifaceted authentication to boost demand

- 12.3.1.1 Biometric smart cards

- 12.3.2 THREE-FACTOR

- 12.3.2.1 Biometric smart card with PIN

- 12.3.2.1.1 Surging focus on mitigating cyber threats to foster segmental growth

- 12.3.2.2 Smart card with two-factor biometric technology

- 12.3.2.2.1 Escalating demand for sensitive data handling in healthcare and finance to propel market

- 12.3.2.3 PIN with two-factor biometric technology

- 12.3.2.3.1 Increasing instances of data breaches and identity theft to accelerate demand

- 12.3.2.4 Three-factor biometric technology

- 12.3.2.4.1 Surging deployment in government organizations and forensic labs to drive market

- 12.3.2.1 Biometric smart card with PIN

- 12.3.3 FOUR-FACTOR

- 12.3.3.1 Pressing need to protect sensitive systems from unauthorized access and cyberattacks to boost demand

- 12.3.4 FIVE-FACTOR

- 12.3.4.1 Need for high levels of security in susceptible and regulated sectors to fuel segmental growth

- 12.3.1 TWO-FACTOR

13 BIOMETRIC SYSTEM MARKET, BY MOBILITY

- 13.1 INTRODUCTION

- 13.2 FIXED

- 13.2.1 INCREASING SECURITY CONCERNS TO DRIVE ADOPTION OF FIXED BIOMETRIC SOLUTIONS

- 13.2.1.1 Access control installations

- 13.2.1.2 Border control and immigration systems

- 13.2.1.3 ATMs and kiosks

- 13.2.1.4 Security system blocks

- 13.2.1.5 Others

- 13.2.1 INCREASING SECURITY CONCERNS TO DRIVE ADOPTION OF FIXED BIOMETRIC SOLUTIONS

- 13.3 PORTABLE 159 13.3.1 SURGING DEMAND FROM LAW ENFORCEMENT AGENCIES TO SUPPORT MARKET GROWTH

- 13.3.1.1 Smartphones

- 13.3.1.2 Portable biometrics fitness trackers

- 13.3.1.3 Field authentication

- 13.3.1.4 Wearables

- 13.3.1.4.1 Smart watches

- 13.3.1.4.2 Fitness trackers

- 13.3.1.4.3 Health monitoring

14 BIOMETRIC SYSTEM MARKET, BY OFFERING

- 14.1 INTRODUCTION

- 14.2 HARDWARE

- 14.2.1 FINGERPRINT SENSORS

- 14.2.1.1 Sensor technology

- 14.2.1.1.1 Capacitive

- 14.2.1.1.1.1 Widespread adoption in smartphones, laptops, and other consumer electronics to drive market

- 14.2.1.1.2 Optical

- 14.2.1.1.2.1 Increasing adoption by smartphone manufacturers to boost demand

- 14.2.1.1.3 Thermal

- 14.2.1.1.3.1 Growing use of smart cards for payments and authentication to fuel segmental growth

- 14.2.1.1.4 Ultrasonic

- 14.2.1.1.4.1 Continuous advancements in sensing technology contribute to market growth

- 14.2.1.1.1 Capacitive

- 14.2.1.1 Sensor technology

- 14.2.2 READERS & SCANNERS

- 14.2.3 CAMERAS

- 14.2.3.1 Infrared

- 14.2.3.2 Multispectral

- 14.2.4 OTHER BIOMETRIC HARDWARE

- 14.2.4.1 Microphones

- 14.2.4.2 Speakers

- 14.2.4.3 Connectivity ICs and AI chips

- 14.2.4.4 Iris recognition sensors

- 14.2.4.5 Processing hardware

- 14.2.4.5.1 Edge computing hardware

- 14.2.4.5.2 Cloud processing infrastructure

- 14.2.1 FINGERPRINT SENSORS

- 14.3 SOFTWARE

- 14.3.1 BIOMETRIC MANAGEMENT SOFTWARE

- 14.3.1.1 Machine learning and AI integration

- 14.3.1.2 Identity management software

- 14.3.1.3 Access control software

- 14.3.1.4 Database management software

- 14.3.1.5 Integration middleware and APIs

- 14.3.1.6 Cloud-based management software/platform

- 14.3.1.7 Others (SDKs, biometric algorithms)

- 14.3.2 SERVICES

- 14.3.2.1 Professional

- 14.3.2.1.1 Consulting & advisory

- 14.3.2.1.2 System integration

- 14.3.2.1.3 Installation

- 14.3.2.2 Managed

- 14.3.2.2.1 Cloud biometrics

- 14.3.2.2.2 Biometrics as a service

- 14.3.2.2.3 Maintenance & upgrades

- 14.3.2.2.4 Monitoring & analytics

- 14.3.2.3 Support services

- 14.3.2.1 Professional

- 14.3.1 BIOMETRIC MANAGEMENT SOFTWARE

15 BIOMETRIC SYSTEM MARKET, BY TYPE

- 15.1 INTRODUCTION

- 15.2 CONTACT-BASED

- 15.2.1 HIGH RELIABILITY AND ACCURACY TO CONTRIBUTE TO MARKET GROWTH

- 15.2.1.1 Traditional fingerprint scanners

- 15.2.1.2 Palm print recognition devices

- 15.2.1 HIGH RELIABILITY AND ACCURACY TO CONTRIBUTE TO MARKET GROWTH

- 15.3 CONTACTLESS

- 15.3.1 ADOPTION OF TOUCHLESS TECHNOLOGIES DUE TO HYGIENE CONCERNS TO ACCELERATE DEMAND

- 15.3.1.1 Facial recognition camera systems

- 15.3.1.2 Iris recognition

- 15.3.1.3 Voice recognition

- 15.3.1 ADOPTION OF TOUCHLESS TECHNOLOGIES DUE TO HYGIENE CONCERNS TO ACCELERATE DEMAND

- 15.4 HYBRID

- 15.4.1 FLEXIBILITY AND USER CONVENIENCE TO FOSTER MARKET GROWTH

- 15.4.1.1 Technology integration complexity

- 15.4.1.2 Multi-environment deployment

- 15.4.1 FLEXIBILITY AND USER CONVENIENCE TO FOSTER MARKET GROWTH

16 BIOMETRIC SYSTEM MARKET, BY DEPLOYMENT MODE

- 16.1 INTRODUCTION

- 16.2 ON-PREMISES

- 16.2.1 INCREASING CONCERNS ABOUT DATA SECURITY AND PRIVACY TO FUEL MARKET GROWTH

- 16.3 CLOUD-BASED

- 16.3.1 RISING DEMAND FOR SCALABLE AND COST-EFFECTIVE SOLUTIONS TO DRIVE MARKET

17 BIOMETRIC SYSTEM MARKET, BY VERTICAL

- 17.1 INTRODUCTION

- 17.2 GOVERNMENT

- 17.2.1 INCREASING ADOPTION TO SECURE CRUCIAL DATA TO CONTRIBUTE TO MARKET GROWTH

- 17.2.2 NATIONAL ID

- 17.2.2.1 National ID programs

- 17.2.2.2 Voter registration and authentication in elections

- 17.2.3 LAW ENFORCEMENT

- 17.2.3.1 Criminal identification and forensic investigation

- 17.2.3.2 Evidence management

- 17.2.3.3 Social welfare scheme authentication

- 17.2.4 BORDER CONTROL AND SECURITY

- 17.2.4.1 e-passport & e-visa verification

- 17.3 MILITARY & DEFENSE

- 17.3.1 PRESSING NEED TO COMPLY WITH RIGOROUS SECURITY PROTOCOLS TO BOOST DEMAND

- 17.3.2 ACCESS CONTROL TO DEFENSE BASES, ARSENALS, AND RESTRICTED AREAS

- 17.3.3 IDENTITY VERIFICATION OF MILITARY PERSONNEL AND CONTRACTORS

- 17.3.4 WEAPON ACCESS AUTHORIZATION

- 17.3.5 SURVEILLANCE & MONITORING USING FACIAL RECOGNITION

- 17.3.6 SECURE COMMUNICATIONS AUTHENTICATION

- 17.4 HEALTHCARE

- 17.4.1 NEED FOR RELIABILITY AND ACCURACY IN MEDICAL SETTINGS TO SUPPORT MARKET GROWTH

- 17.4.2 PATIENT IDENTITY VERIFICATION TO AVOID MIX-UPS

- 17.4.3 ACCESS CONTROL FOR MEDICAL STAFF IN RESTRICTED LABS/PHARMACIES

- 17.4.4 AUTHENTICATION FOR ELECTRONIC HEALTH RECORDS (EHR/EMR)

- 17.4.5 PRESCRIPTION DISPENSING VALIDATION

- 17.4.6 TIME & ATTENDANCE TRACKING OF HEALTHCARE STAFF

- 17.5 BFSI

- 17.5.1 INCREASING NEED FOR ROBUST FRAUD PREVENTION SOLUTIONS TO ACCELERATE MARKET GROWTH

- 17.5.2 BIOMETRIC AUTHENTICATION FOR MOBILE BANKING APPS

- 17.5.3 ATM ACCESS AND WITHDRAWAL AUTHORIZATION USING FINGERPRINT/IRIS

- 17.5.4 KYC VERIFICATION DURING ACCOUNT OPENING

- 17.5.5 FRAUD DETECTION VIA BEHAVIORAL BIOMETRICS

- 17.5.6 BIOMETRIC-ENABLED PAYMENTS AT POS OR ONLINE CHECKOUT

- 17.5.7 CRYPTOCURRENCY

- 17.6 CONSUMER ELECTRONICS

- 17.6.1 RISING DEMAND FOR SMARTPHONES WITH IMPROVED SECURITY FEATURES TO SUPPORT MARKET GROWTH

- 17.6.2 SMARTPHONES

- 17.6.3 LAPTOPS & TABLETS

- 17.6.4 GAMING CONSOLES AND VR HEADSETS

- 17.6.5 WEARABLES

- 17.6.6 SMART HOME DEVICES WITH VOICE/FACIAL RECOGNITION

- 17.7 TRAVEL & IMMIGRATION

- 17.7.1 GOVERNMENT-LED INITIATIVES TO PREVENT UNAUTHORIZED ACCESS TO SPUR DEMAND

- 17.7.2 AUTOMATED BORDER CONTROL GATES

- 17.7.3 E-PASSPORTS EMBEDDED WITH BIOMETRIC IDENTIFIERS

- 17.7.4 AIRLINE PASSENGER CHECK-IN AND BOARDING AUTHENTICATION

- 17.7.5 FREQUENT TRAVELER PROGRAM VERIFICATION

- 17.7.6 IMMIGRATION CONTROL AND VISA PROCESSING

- 17.8 AUTOMOTIVE

- 17.8.1 INCREASING EMPHASIS ON ENHANCING VEHICLE SECURITY TO BOOST DEMAND

- 17.8.2 DRIVER IDENTIFICATION FOR VEHICLE ACCESS/START (FINGERPRINT/FACE)

- 17.8.3 PERSONALIZED IN-VEHICLE SETTINGS (SEAT, INFOTAINMENT) BASED ON BIOMETRICS

- 17.8.4 ANTI-THEFT VEHICLE SECURITY USING BIOMETRIC START AUTHORIZATION

- 17.8.5 FLEET MANAGEMENT - MONITORING AND VERIFYING DRIVERS

- 17.8.6 ALCOHOL DETECTION COMBINED WITH DRIVER BIOMETRICS FOR SAFETY

- 17.9 SECURITY

- 17.9.1 HOME SECURITY

- 17.9.1.1 Rising adoption of IoT and wireless technologies in residential settings to drive market

- 17.9.1.2 Smart door locks with fingerprint/face recognition

- 17.9.1.3 Biometrics-enabled home alarm systems

- 17.9.1.4 Surveillance systems with facial recognition for intruder detection

- 17.9.1.5 Voice recognition for smart home assistants controlling security

- 17.9.2 COMMERCIAL SECURITY

- 17.9.2.1 Growing need to replace manual attendance tracking to drive market

- 17.9.2.2 Workplace access control

- 17.9.2.3 Biometrics-enabled visitor management systems

- 17.9.2.4 Multi-factor security for data centers

- 17.9.2.5 Surveillance & anomaly detection in corporate campuses

- 17.9.2.6 Secure storage/vault access

- 17.9.1 HOME SECURITY

- 17.10 OTHER VERTICALS

- 17.10.1 INDUSTRIAL

- 17.10.1.1 Access control to hazardous areas

- 17.10.1.2 Worker attendance and productivity monitoring

- 17.10.1.3 Safety compliance (ensures machines access only for trained workers)

- 17.10.2 UTILITIES

- 17.10.2.1 Biometric authentication for control room operators

- 17.10.2.2 Prevention of unauthorized access to power plants, oil & gas facilities

- 17.10.3 SPORTS

- 17.10.3.1 Stadium access control for ticket holders

- 17.10.3.2 VIP and player identification at events

- 17.10.3.3 Anti-hooliganism surveillance using face recognition

- 17.10.4 ENTERTAINMENT

- 17.10.4.1 Online gaming platforms

- 17.10.4.2 Theme parks (fingerprint passes)

- 17.10.4.3 AR/VR entertainment systems

- 17.10.1 INDUSTRIAL

18 BIOMETRIC SYSTEM MARKET, BY REGION

- 18.1 INTRODUCTION

- 18.2 ASIA PACIFIC

- 18.2.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 18.2.2 CHINA

- 18.2.2.1 Increasing deployment of surveillance cameras to support market growth

- 18.2.3 JAPAN

- 18.2.3.1 Commitment to integrating biometric systems across various applications to propel market

- 18.2.4 SOUTH KOREA

- 18.2.4.1 Development of smart devices based on advanced biometric technologies to boost demand

- 18.2.5 INDIA

- 18.2.5.1 Growing need for more secure, efficient, and convenient transaction methods to spike demand

- 18.2.6 AUSTRALIA

- 18.2.6.1 Increasing use of voice recognition to streamline interactions with public to drive market

- 18.2.7 REST OF ASIA PACIFIC

- 18.3 NORTH AMERICA

- 18.3.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 18.3.2 US

- 18.3.2.1 Increasing focus on modernizing technologies for border surveillance to fuel market growth

- 18.3.3 CANADA

- 18.3.3.1 Rising focus on upgrading immigration biometric identification to accelerate demand

- 18.3.4 MEXICO

- 18.3.4.1 Implementation of city-wide facial recognition system for public safety to spur demand

- 18.4 EUROPE

- 18.4.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 18.4.2 GERMANY

- 18.4.2.1 Integration of biometrics into automotive sector to fuel market growth

- 18.4.3 UK

- 18.4.3.1 Deployment of contactless biometric scanners in high-traffic areas to foster market growth

- 18.4.4 FRANCE

- 18.4.4.1 Implementation of biometrics across finance, healthcare, and transportation sectors to drive market

- 18.4.5 ITALY

- 18.4.5.1 Adoption of advanced biometric technologies in travel & immigration sector to support market growth

- 18.4.6 SPAIN

- 18.4.6.1 Need for security enhancement due to robust tourism sector to stimulate market growth

- 18.4.7 REST OF EUROPE

- 18.5 ROW

- 18.5.1 MACROECONOMIC OUTLOOK FOR ROW

- 18.5.2 MIDDLE EAST

- 18.5.2.1 Advancements and investments in security infrastructure to foster growth

- 18.5.2.2 Bahrain

- 18.5.2.3 Kuwait

- 18.5.2.4 Oman

- 18.5.2.5 Qatar

- 18.5.2.6 Saudi Arabia

- 18.5.2.7 UAE

- 18.5.2.8 Rest of Middle East

- 18.5.3 AFRICA

- 18.5.3.1 Implementation of biometric systems for identity verification and security to boost market

- 18.5.3.2 South Africa

- 18.5.3.3 Other African countries

- 18.5.4 SOUTH AMERICA

- 18.5.4.1 National ID programs, border security, financial services, and public sector digital initiatives - key drivers

19 COMPETITIVE LANDSCAPE

- 19.1 OVERVIEW

- 19.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 19.2.1 COMPETITIVE STRATEGIES INITIATIVES

- 19.2.2 OPERATIONAL STRATEGIC INITIATIVES

- 19.3 REVENUE ANALYSIS, 2020-2024

- 19.4 MARKET SHARE ANALYSIS, 2024

- 19.5 BRAND/PRODUCT COMPARISON

- 19.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 19.6.1 STARS

- 19.6.2 EMERGING LEADERS

- 19.6.3 PERVASIVE PLAYERS

- 19.6.4 PARTICIPANTS

- 19.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 19.6.5.1 Company footprint

- 19.6.5.2 Region footprint

- 19.6.5.3 Authentication footprint

- 19.6.5.4 Mobility footprint

- 19.6.5.5 Offering footprint

- 19.6.5.6 Vertical footprint

- 19.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 19.7.1 PROGRESSIVE COMPANIES

- 19.7.2 RESPONSIVE COMPANIES

- 19.7.3 DYNAMIC COMPANIES

- 19.7.4 STARTING BLOCKS

- 19.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 19.7.5.1 Detailed list of startups/SMEs

- 19.7.5.2 Competitive benchmarking of key startups/SMEs

- 19.8 COMPANY VALUATION AND FINANCIAL METRICS, 2025

- 19.9 COMPETITIVE SCENARIO

- 19.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 19.9.2 DEALS

- 19.9.3 EXPANSIONS

- 19.9.4 OTHER DEVELOPMENTS

20 COMPANY PROFILES

- 20.1 KEY PLAYERS

- 20.1.1 THALES

- 20.1.1.1 Business overview

- 20.1.1.2 Products/Solutions/Services offered

- 20.1.1.3 Recent developments

- 20.1.1.3.1 Product launches/developments

- 20.1.1.3.2 Deals

- 20.1.1.3.3 Expansions

- 20.1.1.3.4 Other developments

- 20.1.1.4 MnM view

- 20.1.1.4.1 Key strengths

- 20.1.1.4.2 Strategic choices

- 20.1.1.4.3 Weaknesses and competitive threats

- 20.1.2 IDEMIA

- 20.1.2.1 Business overview

- 20.1.2.2 Products/Solutions/Services offered

- 20.1.2.3 Recent developments

- 20.1.2.3.1 Product launches/developments

- 20.1.2.3.2 Deals

- 20.1.2.3.3 Other developments

- 20.1.2.4 MnM view

- 20.1.2.4.1 Key strengths

- 20.1.2.4.2 Strategic choices

- 20.1.2.4.3 Weaknesses and competitive threats

- 20.1.3 NEC CORPORATION

- 20.1.3.1 Business overview

- 20.1.3.2 Products/Solutions/Services offered

- 20.1.3.3 Recent developments

- 20.1.3.3.1 Product launches/developments

- 20.1.3.3.2 Deals

- 20.1.3.3.3 Other developments

- 20.1.3.4 MnM view

- 20.1.3.4.1 Key strengths

- 20.1.3.4.2 Strategic choices

- 20.1.3.4.3 Weaknesses and competitive threats

- 20.1.4 ASSA ABLOY

- 20.1.4.1 Business overview

- 20.1.4.2 Products/Solutions/Services offered

- 20.1.4.3 Recent developments

- 20.1.4.3.1 Deals

- 20.1.4.4 MnM view

- 20.1.4.4.1 Key strengths

- 20.1.4.4.2 Strategic choices

- 20.1.4.4.3 Weaknesses and competitive threats

- 20.1.5 FUJITSU

- 20.1.5.1 Business overview

- 20.1.5.2 Products/Solutions/Services offered

- 20.1.5.3 Recent developments

- 20.1.5.3.1 Product launches/developments

- 20.1.5.3.2 Deals

- 20.1.5.4 MnM view

- 20.1.5.4.1 Key strengths

- 20.1.5.4.2 Strategic choices

- 20.1.5.4.3 Weaknesses and competitive threats

- 20.1.6 PRECISE BIOMETRICS

- 20.1.6.1 Business overview

- 20.1.6.2 Products/Solutions/Services offered

- 20.1.6.3 Recent developments

- 20.1.6.3.1 Product launches/developments

- 20.1.6.3.2 Deals

- 20.1.7 SECUNET SECURITY NETWORKS AG

- 20.1.7.1 Business overview

- 20.1.7.2 Products/Solutions/Services offered

- 20.1.7.3 Recent developments

- 20.1.7.3.1 Deals

- 20.1.8 AWARE INC.

- 20.1.8.1 Business overview

- 20.1.8.2 Products/Solutions/Services offered

- 20.1.8.3 Recent developments

- 20.1.8.3.1 Product launches/developments

- 20.1.8.3.2 Deals

- 20.1.9 COGNITEC SYSTEMS GMBH

- 20.1.9.1 Business overview

- 20.1.9.2 Products/Solutions/Services offered

- 20.1.9.3 Recent developments

- 20.1.9.3.1 Product launches/developments

- 20.1.9.3.2 Deals

- 20.1.10 ANVIZ GLOBAL INC.

- 20.1.10.1 Business overview

- 20.1.10.2 Products/Solutions/Services offered

- 20.1.10.3 Recent developments

- 20.1.10.3.1 Product launches/developments

- 20.1.1 THALES

- 20.2 OTHER KEY PLAYERS

- 20.2.1 DAON, INC.

- 20.2.2 DERMALOG IDENTIFICATION SYSTEMS GMBH

- 20.2.3 NEUROTECHNOLOGY

- 20.2.4 INNOVATRICS

- 20.2.5 VERIDOS GMBH

- 20.2.6 ZETES

- 20.2.7 JUMIO

- 20.2.8 IPROOV

- 20.2.9 FACETEC, INC.

- 20.2.10 MITEK SYSTEMS, INC.

- 20.2.11 BEIJING KUANGSHI TECHNOLOGY CO., LTD. (MEGVII)

- 20.2.12 SENSETIME

- 20.2.13 FACEBANX

- 20.2.14 BIO-KEY INTERNATIONAL

- 20.2.15 SECURIPORT

- 20.2.16 M2SYS TECHNOLOGY

- 20.2.17 SUPREMA INC.

- 20.2.18 FULCRUM BIOMETRICS

- 20.2.19 ONESPAN

- 20.2.20 QUALCOMM TECHNOLOGIES, INC.

- 20.2.21 INTEGRATED BIOMETRICS

- 20.2.22 LEIDOS

- 20.2.23 PAPILLON

- 20.2.24 NUANCE COMMUNICATIONS, INC.

21 RESEARCH METHODOLOGY

- 21.1 RESEARCH APPROACH

- 21.1.1 SECONDARY AND PRIMARY RESEARCH

- 21.1.2 SECONDARY DATA

- 21.1.2.1 List of major secondary sources

- 21.1.2.2 Key data from secondary sources

- 21.1.3 PRIMARY DATA

- 21.1.3.1 Intended interview participants

- 21.1.3.2 List of key primary interview participants

- 21.1.3.3 Breakdown of primaries

- 21.1.3.4 Key data from primary sources

- 21.1.3.5 Key industry insights

- 21.2 MARKET SIZE ESTIMATION METHODOLOGY

- 21.2.1 BOTTOM-UP APPROACH

- 21.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 21.2.2 TOP-DOWN APPROACH

- 21.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 21.2.1 BOTTOM-UP APPROACH

- 21.3 DATA TRIANGULATION

- 21.4 RESEARCH ASSUMPTIONS

- 21.5 RESEARCH LIMITATIONS

- 21.6 RISK ASSESSMENT

22 APPENDIX

- 22.1 DISCUSSION GUIDE

- 22.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 22.3 CUSTOMIZATION OPTIONS

- 22.4 RELATED REPORTS

- 22.5 AUTHOR DETAILS