|

시장보고서

상품코드

1881234

안과 장비 시장(-2030년) : 기술, 제품 유형(외과용 기기, 진단&모니터링 기기), 최종 사용자별 예측Ophthalmic Equipment Market by Technology, Product Type (Surgical Devices, Diagnostic & Monitoring Devices ), End User - Global Forecast to 2030 |

||||||

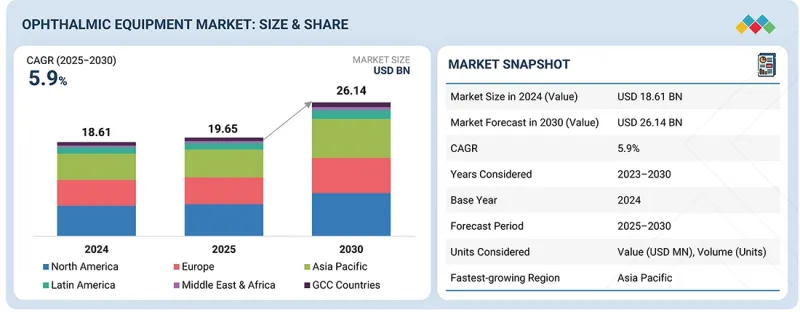

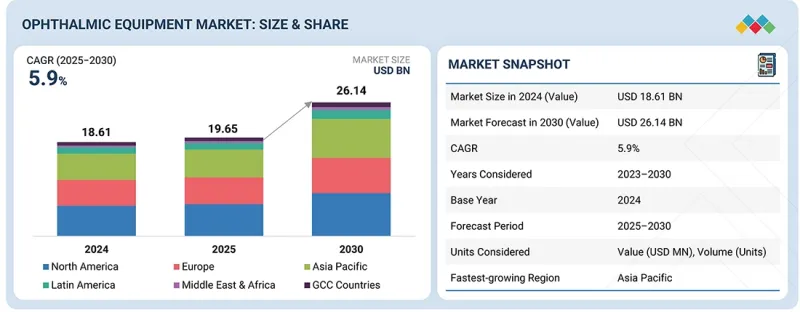

안과 장비 시장 규모는 예측 기간 동안 CAGR 5.9%를 나타내 2025년 196억 5,000만 달러에서 2030년에는 261억 4,000만 달러에 이를 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2033년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러) |

| 부문 | 기술, 제품 유형, 최종 사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

안과 장비 시장은 주로 백내장, 녹내장, 당뇨병성 망막증 등의 안질환의 유병률 증가나 세계적인 고령화에 의해 견인되고 있습니다. OCT와 안저카메라 등의 고급 진단 툴의 사용 증가, 의료비 증가, 개발도상국의 안과 의료 서비스에 대한 액세스 확대도 시장 성장을 가속하고 있습니다.

또한 저침습 및 AI 기반 안과 의료 솔루션을 지원하는 기술 혁신도 그 보급을 촉진하고 있습니다. 그러나 장비의 고비용과 숙련된 전문가의 부족은 시장 확대를 제한하고 있습니다.

제품 유형별로는 백내장 수술, 굴절 교정 수술, 녹내장 수술의 세계적인 실시 건수가 많기 때문에 외과용 기기가 시장을 독점하고 있습니다. 현미 수술 기술, 펨토초 레이저, 초음파 유화 흡입 시스템의 진보로 정밀도와 치료 성적이 향상되어 채용이 증가하고 있습니다. 게다가 노인 인구 증가와 고급 수술센터의 확대는 안과 수술 장비 수요를 더욱 밀어 올리고 있습니다.

최종 사용자별로 병원은 가장 큰 점유율을 차지합니다. 병원은 종합적인 안과 의료를 제공하는 주요 기지로서 진단 서비스와 외과 수술 서비스를 모두 제공합니다. 고급 인프라와 숙련된 안과 의사를 옹호하고 클리닉보다 더 많은 환자를 모으고 있습니다. 또한, 복잡한 치료를 위한 고기능 안과 장비에 대한 투자 능력은 시장 전반에 걸친 병원의 이점을 강화하고 있습니다.

북미는 첨단 의료 인프라, 혁신적인 진단 및 수술 기술의 보급률이 높고 주요 제조업체의 강력한 존재감으로 최대 점유율을 차지합니다. 이 지역은 다량의 의료 지출, 지원적인 상환 정책, 다수의 훈련을 받은 안과 의사의 존재로부터 혜택을 받고 있습니다. 게다가 녹내장과 노인황반변성 등 노화성 안질환의 유병률 증가가 장비 수요를 더욱 밀어 올리고 있으며, 지속적인 기술 혁신과 조기 도입이 시장의 우위성 유지에 기여하고 있습니다.

본 보고서에서는 세계의 안과 장비 시장을 조사했으며, 시장 개요, 시장 성장 영향요인 분석, 기술·특허 동향, 법규제 환경, 사례연구, 시장 규모 추이와 예측, 각종 구분·지역/주요 국가별 상세 분석, 경쟁 구도, 주요기업 프로파일 등을 정리했습니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 고객의 사업에 영향을 주는 동향/혁신

- 가격 분석

- 밸류체인 분석

- 공급망 분석

- 생태계 분석

- 투자 및 자금조달 시나리오

- 기술 분석

- 업계 동향

- 특허 분석

- 무역 분석

- 주요 컨퍼런스 및 이벤트(2025-2026년)

- 사례 연구 분석

- 규제 분석

- Porter's Five Forces 분석

- 주요 이해관계자와 구매 기준

- 언멧 니즈/최종 사용자의 기대

- 미국 관세가 안과 장비 시장에 미치는 영향(2025년)

- AI가 안과 장비 시장에 미치는 영향

- 인접 시장 분석

제6장 안과 장비 시장 : 기술별

- AI 비지원 기기

- AI 지원 기기

제7장 안과 장비 시장 : 제품별

- 수술용 기기

- 백내장 수술용 기기

- 유리체망막 수술 기기

- 굴절 수술 기기

- 녹내장 수술 기기

- 안과용 현미경

- 안과 수술용 액세서리

- 진단 및 모니터링 장비

- 광 간섭 단층 촬영 스캐너

- 안저 카메라

- 시야계/시야 분석 기기

- 자동굴절계 및 각막경

- 안과 초음파 영상 시스템

- 기타 안과용 초음파 영상 시스템

- 안압계

- 세극등

- 프로프터

- 파면계

- 광학 생체측정 시스템

- 안저경

- 렌즈계

- 각막 토포그래피 시스템

- 시력표 투사기

- 반사 현미경

- 망막경

- 기타 진단 및 모니터링 장비

제8장 안과 장비 시장 : 최종 사용자별

- 병원

- 전문 클리닉 및 외래수술센터(ASC)

- 기타

제9장 안과 장비 시장 : 지역별

- 북미

- 거시경제 전망

- 미국

- 캐나다

- 유럽

- 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 거시경제 전망

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타

- 라틴아메리카

- 거시경제 전망

- 브라질

- 멕시코

- 아르헨티나

- 기타

- 중동 및 아프리카

- 거시경제 전망

- GCC 국가

- 거시경제 전망

제10장 경쟁 구도

- 개요

- 주요 기업의 전략/유력 기업

- 수익 분석

- 시장 점유율 분석

- 기업 평가 매트릭스 : 주요 기업

- 기업평가 매트릭스 : 스타트업/중소기업

- 기업평가와 재무지표

- 브랜드/제품 비교

- 경쟁 시나리오

제11장 기업 프로파일

- 주요 기업

- ALCON

- JOHNSON & JOHNSON

- CARL ZEISS MEDITEC AG

- BAUSCH HEALTH COMPANIES INC.

- HOYA CORPORATION

- ESSILORLUXOTTICA

- CANON

- GLAUKOS CORPORATION

- TOPCON CORPORATION

- NIDEK CO., LTD.

- STAAR SURGICAL

- HALMA PLC

- HAAG-STREIT

- SHANGHAI MEDIWORKS PRECISION INSTRUMENTS CO., LTD.

- VISIONIX

- 기타 기업

- VISUNEX MEDICAL SYSTEMS

- COSTRUZIONE STRUMENTI OFTALMICI

- HAI LABORATORIES, INC.

- FORUS HEALTH

- ZIEMER OPHTHALMIC SYSTEMS AG

- CRYSTALVUE MEDICAL CORPORATION

- REMIDIO INNOVATIVE SOLUTIONS PVT. LTD.

- SUZHOU KANGJIE MEDICAL INC.

- LUMENIS

- OPHTEC BV

제12장 부록

KTH 25.12.10The ophthalmic equipment market is projected to reach USD 26.14 billion by 2030 from USD 19.65 billion in 2025, at a CAGR of 5.9% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2033 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Technology, Product Type, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa, and GCC Countries |

The ophthalmic equipment market is mainly propelled by the increasing prevalence of eye conditions such as cataracts, glaucoma, and diabetic retinopathy, along with the aging global population. Rising use of advanced diagnostic tools like OCT and fundus cameras, higher healthcare expenditures, and broader access to eye care services in developing countries also drive market growth.

Additionally, innovations in technology that support minimally invasive and AI-based eye care solutions boost adoption. However, high equipment costs and a shortage of skilled professionals limit market expansion.

By product type, surgical devices dominate the ophthalmic equipment market because of the high volume of cataract, refractive, and glaucoma surgeries worldwide. Advances in microsurgical techniques, femtosecond lasers, and phacoemulsification systems have improved precision and outcomes, increasing their adoption. Additionally, the growing elderly population and the expanding availability of advanced surgical centers further boost demand for ophthalmic surgical devices.

By end user, hospitals hold the largest share in the ophthalmic equipment market because they serve as primary centers for comprehensive eye care, providing both diagnostic and surgical services. They have advanced infrastructure and skilled ophthalmologists, and they attract more patients than clinics. Additionally, hospitals' ability to invest in high-end ophthalmic equipment for complex procedures strengthens their dominance in the overall market.

North America holds the largest share of the ophthalmic equipment market because of its advanced healthcare infrastructure, high adoption of innovative diagnostic and surgical technologies, and a strong presence of leading manufacturers. The region benefits from significant healthcare spending, supportive reimbursement policies, and a large number of trained ophthalmologists. Additionally, the increasing prevalence of age-related eye diseases like glaucoma and macular degeneration further boosts equipment demand, while ongoing innovation and early technology adoption help sustain the market dominance.

A breakdown of the primary participants (supply-side) for the ophthalmic equipment market referred to in this report is provided below:

- By Company Type: Tier 1:34%, Tier 2: 38%, and Tier 3: 28%

- By Designation: C-level: 26%, Director Level: 35%, and Others: 39%

- By Region: North America: 17%, Europe: 39%, Asia Pacific: 28%, Latin America: 8%, Middle East & Africa: 3%, GCC Countries: 5%

Prominent players in the ophthalmic equipment market are Bausch Health Companies, Inc. (Canada), Alcon (US), Carl Zeiss Meditec AG (Germany), Johnson & Johnson Vision Care (US), HOYA Corporation (Japan), EssilorLuxottica (France), Canon Inc. (Japan), Glaukos Corporation (US), Nidek Co., Ltd. (Japan), Topcon Corporation (Japan), Staar Surgical (US), Haag-Streit (Switzerland), Visionix (France), Shanghai Mediworks Precision Instruments Co., Ltd. (China), Halma plc (UK), among others.

Research Coverage

The report assesses the ophthalmic equipment market and estimates its size and future growth potential across various segments, including technology, product type, end user, and region. It also provides a competitive analysis of the major players, featuring company profiles, product offerings, recent developments, and key market dynamics strategies.

Reasons to Buy the Report

The report will help market leaders and new entrants by providing data on approximate revenue figures for the overall market, the ophthalmic equipment sector, and its subsegments. It will assist stakeholders in understanding the competitive landscape and gaining insights to better position their businesses and develop effective go-to-market strategies. Additionally, the report helps stakeholders grasp the market pulse by offering data on key drivers, barriers, obstacles, and opportunities in the market.

This report provides insights into the following points:

- Analysis of key drivers (Increasing geriatric population, Rising prevalence of eye disorders, Technological advancements in ophthalmic devices, and Increased government initiatives to control visual impairment), restraints (High cost of ophthalmology devices, High cost and risk associated with eye surgeries and Rising adoption of refurbished ophthalmic devices), opportunities (Potential growth opportunities in emerging markets and Low adoption of phacoemulsification devices and premium IOLs in emerging markets), and challenges (Low accessibility to eye care in low-income countries, Lack of skilled professionals)

- Product Enhancement/Innovation: Comprehensive details about product launches and anticipated trends in the global ophthalmic equipment market

- Market Development: Thorough knowledge and analysis of the profitable rising markets by technology, product type, end user, and region

- Market Diversification: Comprehensive information about newly launched products, expanding markets, current advancements, and investments in the global ophthalmic equipment market

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings, and capacities of the major competitors in the global ophthalmic equipment market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 SEGMENTS COVERED & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY USED

- 1.5 STAKEHOLDERS

- 1.6 LIMITATIONS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 CAGR PROJECTIONS

- 2.2.2 TOP-DOWN APPROACH

- 2.3 MARKET BREAKDOWN & DATA TRIANGULATION

- 2.4 MARKET SHARE ESTIMATION

- 2.5 STUDY ASSUMPTIONS

- 2.6 LIMITATIONS

- 2.6.1 METHODOLOGY-RELATED LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 OPHTHALMIC EQUIPMENT MARKET OVERVIEW

- 4.2 NORTH AMERICA: OPHTHALMIC EQUIPMENT MARKET, BY COUNTRY AND END USER (2024)

- 4.3 OPHTHALMIC EQUIPMENT MARKET: REGIONAL GROWTH OPPORTUNITIES

- 4.4 OPHTHALMIC EQUIPMENT MARKET, BY REGION (2025-2030)

- 4.5 OPHTHALMIC EQUIPMENT MARKET: DEVELOPED VS. DEVELOPING MARKETS

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing geriatric population

- 5.2.1.2 Rising prevalence of eye disorders

- 5.2.1.2.1 Cataracts

- 5.2.1.2.2 Glaucoma

- 5.2.1.2.3 Obesity and diabetes

- 5.2.1.2.4 Age-related macular degeneration (AMD)

- 5.2.1.3 Technological advancements in ophthalmic devices

- 5.2.1.4 Increased government initiatives to control visual impairment

- 5.2.2 RESTRAINTS

- 5.2.2.1 High cost and risk associated with eye surgeries

- 5.2.2.2 High cost of ophthalmology devices

- 5.2.2.3 Rising adoption of refurbished ophthalmic devices

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Potential growth opportunities in emerging markets

- 5.2.3.2 Low adoption of phacoemulsification devices and premium IOLs in emerging markets

- 5.2.4 CHALLENGES

- 5.2.4.1 Low accessibility to eye care in low-income countries

- 5.2.4.2 Lack of skilled professionals

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE OF OPHTHLAMIC EQUIPMENT PRODUCTS, BY KEY PLAYER, 2024

- 5.4.2 AVERAGE SELLING PRICE TREND OF OPTICAL COHERENCE TOMOGRAPHY SYSTEMS, BY REGION, 2022-2024

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.8 INVESTMENT & FUNDING SCENARIO

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Robotics & image-guided surgical systems

- 5.9.1.2 Wearable and AR/VR-based vision systems

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Teleophthalmology and remote monitoring

- 5.9.2.2 Cloud connectivity and data integration

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 Eye-tracking and motion compensation devices

- 5.9.3.2 Data management & EHR integration tools

- 5.9.1 KEY TECHNOLOGIES

- 5.10 INDUSTRY TRENDS

- 5.10.1 INNOVATIVE APPLICATION OF FEMTOSECOND LASER TECHNOLOGY

- 5.10.2 MINIMALLY INVASIVE GLAUCOMA SURGERY

- 5.11 PATENT ANALYSIS

- 5.12 TRADE ANALYSIS

- 5.12.1 IMPORT DATA (HS CODE 901850)

- 5.12.2 EXPORT DATA (HS CODE 901850)

- 5.13 KEY CONFERENCES & EVENTS, 2025-2026

- 5.14 CASE STUDY ANALYSIS

- 5.14.1 CASE STUDY 1: ZEISS - AI INTEGRATION IN CIRRUS OCT SYSTEMS

- 5.14.2 CASE STUDY 2: INDIAN GOVERNMENT'S NPCB & USE OF FORUS HEALTH'S 3NETHRA

- 5.14.3 CASE STUDY 3: HEIDELBERG ENGINEERING - NHS UK OCT DEPLOYMENT

- 5.15 REGULATORY ANALYSIS

- 5.15.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.15.2 REGULATORY LANDSCAPE

- 5.15.2.1 North America

- 5.15.2.1.1 US

- 5.15.2.1.2 Canada

- 5.15.2.2 Europe

- 5.15.2.2.1 Germany

- 5.15.2.2.2 France

- 5.15.2.2.3 UK

- 5.15.2.3 Asia Pacific

- 5.15.2.3.1 China

- 5.15.2.3.2 Japan

- 5.15.2.3.3 India

- 5.15.2.4 Latin America

- 5.15.2.4.1 Brazil

- 5.15.2.4.2 Mexico

- 5.15.2.5 Middle East & Africa

- 5.15.2.5.1 Saudi Arabia

- 5.15.2.5.2 UAE

- 5.15.2.5.3 South Africa

- 5.15.2.5.4 Nigeria

- 5.15.2.1 North America

- 5.16 PORTER'S FIVE FORCES ANALYSIS

- 5.16.1 THREAT OF NEW ENTRANTS

- 5.16.2 THREAT OF SUBSTITUTES

- 5.16.3 BARGAINING POWER OF BUYERS

- 5.16.4 BARGAINING POWER OF SUPPLIERS

- 5.16.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.17 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.17.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.17.2 BUYING CRITERIA

- 5.18 UNMET NEEDS/END-USER EXPECTATIONS

- 5.19 IMPACT OF 2025 US TARIFFS ON OPHTHALMIC EQUIPMENT MARKET

- 5.19.1 KEY TARIFF RATES

- 5.19.2 PRICE IMPACT ANALYSIS

- 5.19.3 KEY IMPACT ON COUNTRY/REGION

- 5.19.3.1 US

- 5.19.3.2 Europe

- 5.19.3.3 Asia Pacific

- 5.19.4 IMPACT ON END-USER INDUSTRIES

- 5.20 IMPACT OF ARTIFICIAL INTELLIGENCE ON OPHTHALMIC EQUIPMENT MARKET

- 5.21 ADJACENT MARKET ANALYSIS

6 OPHTHALMIC EQUIPMENT MARKET, BY TECHNOLOGY

- 6.1 INTRODUCTION

- 6.2 NON-AI-ENABLED EQUIPMENT

- 6.2.1 RISING SURGICAL VOLUMES AND AFFORDABILITY TO DRIVE NON-AI EQUIPMENT ADOPTION

- 6.3 AI-ENABLED EQUIPMENT

- 6.3.1 RISING DEMAND FOR PRECISION DIAGNOSTICS TO ACCELERATE AI-ENABLED EQUIPMENT ADOPTION

7 OPHTHALMIC EQUIPMENT MARKET, BY PRODUCT

- 7.1 INTRODUCTION

- 7.2 SURGICAL DEVICES

- 7.2.1 CATARACT SURGICAL DEVICES

- 7.2.1.1 Ophthalmic viscoelastic devices

- 7.2.1.1.1 Increasing number of cataract surgeries to support market growth

- 7.2.1.2 Phacoemulsification devices

- 7.2.1.2.1 Advancements in phacoemulsification devices to increase demand during forecast period

- 7.2.1.3 Cataract surgical lasers

- 7.2.1.3.1 Advantages such as high safety and accuracy to drive market growth

- 7.2.1.4 IOL injectors

- 7.2.1.4.1 Rising need for accurate implantation of IOLs to boost market growth

- 7.2.1.5 Intraocular lenses

- 7.2.1.5.1 Rising prevalence of cataracts globally to propel segment

- 7.2.1.1 Ophthalmic viscoelastic devices

- 7.2.2 VITREORETINAL SURGICAL DEVICES

- 7.2.2.1 Vitrectomy machines

- 7.2.2.1.1 Extensive usage of vitrectomy machines to correct retinal errors to boost market

- 7.2.2.2 Vitreoretinal packs

- 7.2.2.2.1 Increasing awareness about vitreoretinal surgery to increase utilization of vitreoretinal packs

- 7.2.2.3 Photocoagulation lasers

- 7.2.2.3.1 Rising prevalence of various eye diseases to drive market growth

- 7.2.2.4 Illumination devices

- 7.2.2.4.1 Growing use of portable, powerful illuminators for greater efficiency to fuel market growth

- 7.2.2.5 Vitrectomy probes

- 7.2.2.5.1 Advancements in vitrectomy probes to result in rapid cutting speed to remove vitreous bodies

- 7.2.2.6 Backflushes

- 7.2.2.6.1 Growing use of backflushes to prevent damage or complications to eye structure to propel growth

- 7.2.2.7 Chandeliers

- 7.2.2.7.1 Growing use of chandeliers for improved visualization of retina to aid growth

- 7.2.2.1 Vitrectomy machines

- 7.2.3 REFRACTIVE SURGICAL DEVICES

- 7.2.3.1 Femtosecond lasers

- 7.2.3.1.1 Rising preference for femtosecond lasers over microkeratomes to support market growth

- 7.2.3.2 Excimer lasers

- 7.2.3.2.1 Rising prevalence of myopia to drive market

- 7.2.3.3 Other refractive surgical devices

- 7.2.3.1 Femtosecond lasers

- 7.2.4 GLAUCOMA SURGICAL DEVICES

- 7.2.4.1 Microinvasive glaucoma surgery devices

- 7.2.4.1.1 Growing preference for microinvasive glaucoma surgery to drive adoption

- 7.2.4.2 Glaucoma drainage devices

- 7.2.4.2.1 Rising prevalence of glaucoma across globe to drives market growth

- 7.2.4.3 Glaucoma laser systems

- 7.2.4.3.1 Increasing prevalence of open-angle glaucoma to boost segment

- 7.2.4.1 Microinvasive glaucoma surgery devices

- 7.2.5 OPHTHALMIC MICROSCOPES

- 7.2.5.1 Increasing prevalence of eye diseases to drive demand

- 7.2.6 OPHTHALMIC SURGICAL ACCESSORIES

- 7.2.6.1 Surgical instruments & kits

- 7.2.6.1.1 Surgical instruments & kits to hold largest share of accessories market

- 7.2.6.2 Ophthalmic tips & handles

- 7.2.6.2.1 Wide range of tips and handles available to meet end-user demand

- 7.2.6.3 Ophthalmic scissors

- 7.2.6.3.1 Growing end-user preference for titanium scissors to boost market

- 7.2.6.4 Ophthalmic forceps

- 7.2.6.4.1 Wide use of forceps in ophthalmological surgeries to drive demand

- 7.2.6.5 Ophthalmic spatulas

- 7.2.6.5.1 China to be fastest-growing market for ophthalmic spatulas

- 7.2.6.6 Macular lenses

- 7.2.6.6.1 Rise in adoption of macular lenses for hands-free operation to support growth

- 7.2.6.7 Ophthalmic cannulas

- 7.2.6.7.1 Rising adoption of single-use cannulas to drive market growth

- 7.2.6.8 Other ophthalmic surgical accessories

- 7.2.6.1 Surgical instruments & kits

- 7.2.1 CATARACT SURGICAL DEVICES

- 7.3 DIAGNOSTIC & MONITORING DEVICES

- 7.3.1 OPTICAL COHERENCE TOMOGRAPHY SCANNERS

- 7.3.1.1 Spectral-domain OCT (SD-OCT)

- 7.3.1.1.1 Growing demand for high-resolution retinal imaging to accelerate spectral-domain OCT adoption

- 7.3.1.2 Swept-source OCT (SS-OCT)

- 7.3.1.2.1 Rising preference for deep tissue imaging and faster scanning to fuel swept-source OCT demand

- 7.3.1.3 Handheld OCT

- 7.3.1.3.1 Surging demand for portability and pediatric imaging to propel handheld OCT system adoption

- 7.3.1.1 Spectral-domain OCT (SD-OCT)

- 7.3.2 FUNDUS CAMERAS

- 7.3.2.1 Rising prevalence of age-related disorders to boost segment

- 7.3.3 PERIMETERS/VISUAL FIELD ANALYZERS

- 7.3.3.1 Increasing incidence of glaucoma and AMD to drive demand for perimeters

- 7.3.4 AUTOREFRACTORS & KERATOMETERS

- 7.3.4.1 Rising patient population with visual impairment to drive utilization

- 7.3.5 OPHTHALMIC ULTRASOUND IMAGING SYSTEMS

- 7.3.5.1 Ophthalmic A-scan ultrasound

- 7.3.5.1.1 Wide usage to measure length of eye in common eye disorders to boost market

- 7.3.5.2 Ophthalmic B-scan ultrasound

- 7.3.5.2.1 Growing use of B-scans to assess eye and orbit to determine eye disorders

- 7.3.5.3 Ophthalmic ultrasound biomicroscopes

- 7.3.5.3.1 Rising volume of refractive surgeries to fuel market growth

- 7.3.5.4 Ophthalmic pachymeters

- 7.3.5.4.1 Growing use of ophthalmic pachymeters to monitor condition of cornea to support growth

- 7.3.5.1 Ophthalmic A-scan ultrasound

- 7.3.6 OTHER OPHTHALMIC ULTRASOUND IMAGING SYSTEMS

- 7.3.7 TONOMETERS

- 7.3.7.1 Rising prevalence of glaucoma to boost demand

- 7.3.8 SLIT LAMPS

- 7.3.8.1 Rising prevalence of ocular conditions to drive market

- 7.3.9 PHOROPTERS

- 7.3.9.1 Phoropters aid in measurement of refractive errors

- 7.3.10 WAVEFRONT ABERROMETERS

- 7.3.10.1 Effectiveness in measuring refractive aberrations to drive demand

- 7.3.11 OPTICAL BIOMETRY SYSTEMS

- 7.3.11.1 Advantages of optical biometry systems to boost adoption in diagnostics

- 7.3.12 OPHTHALMOSCOPES

- 7.3.12.1 Increasing number of patients with glaucoma, diabetic retinopathy, and AMD to fuel market

- 7.3.13 LENSMETERS

- 7.3.13.1 Rising prevalence of myopia & hyperopia to fuel growth

- 7.3.14 CORNEAL TOPOGRAPHY SYSTEMS

- 7.3.14.1 Increasing number of LASIK procedures to drive demand

- 7.3.15 CHART PROJECTORS

- 7.3.15.1 Ability to provide practitioners access to multiple chart types in one device to boost demand

- 7.3.16 SPECULAR MICROSCOPES

- 7.3.16.1 Growing number of patients with diabetes to drive market

- 7.3.17 RETINOSCOPES

- 7.3.17.1 Rising prevalence of myopia across globe to boost market growth

- 7.3.18 OTHER DIAGNOSTIC & MONITORING DEVICES

- 7.3.1 OPTICAL COHERENCE TOMOGRAPHY SCANNERS

8 OPHTHALMIC EQUIPMENT MARKET, BY END USER

- 8.1 INTRODUCTION

- 8.2 HOSPITALS

- 8.2.1 LARGE PATIENT POOL AND HIGH PURCHASING POWER OF HOSPITALS TO DRIVE GROWTH

- 8.3 SPECIALTY CLINICS & AMBULATORY SURGERY CENTERS

- 8.3.1 COST-EFFECTIVENESS OF AMBULATORY CARE TO ENHANCE END-USER INTEREST

- 8.4 OTHER END USERS

9 OPHTHALMIC EQUIPMENT MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 NORTH AMERICA

- 9.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 9.2.2 US

- 9.2.2.1 Rising geriatric population and increasing healthcare expenditure to drive market

- 9.2.3 CANADA

- 9.2.3.1 Rising awareness about eye care and increasing ocular diseases to drive market

- 9.3 EUROPE

- 9.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 9.3.2 GERMANY

- 9.3.2.1 Increasing healthcare expenditure to boost market

- 9.3.3 UK

- 9.3.3.1 Rising prevalence of diabetes-related eye diseases to drive market

- 9.3.4 FRANCE

- 9.3.4.1 Growing number of eye surgeries to drive demand

- 9.3.5 ITALY

- 9.3.5.1 Increasing healthcare spending and growing geriatric population to propel market

- 9.3.6 SPAIN

- 9.3.6.1 Increasing ophthalmic surgical procedures to drive market

- 9.3.7 REST OF EUROPE

- 9.4 ASIA PACIFIC

- 9.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 9.4.2 CHINA

- 9.4.2.1 Rising prevalence of cataracts to drive market

- 9.4.3 JAPAN

- 9.4.3.1 Strong manufacturing capabilities to propel market

- 9.4.4 INDIA

- 9.4.4.1 Increasing geriatric population and prevalence of eye disorders to support market

- 9.4.5 AUSTRALIA

- 9.4.5.1 Increased cataract surgeries to drive market

- 9.4.6 SOUTH KOREA

- 9.4.6.1 Growing focus on medical tourism to boost market

- 9.4.7 REST OF ASIA PACIFIC

- 9.5 LATIN AMERICA

- 9.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 9.5.2 BRAZIL

- 9.5.2.1 Government support and initiatives to boost market

- 9.5.3 MEXICO

- 9.5.3.1 Growing incidence of eye disorders to drive market

- 9.5.4 ARGENTINA

- 9.5.4.1 Increasing healthcare expenditure and well-developed healthcare system to favor market

- 9.5.5 REST OF LATIN AMERICA

- 9.6 MIDDLE EAST & AFRICA

- 9.6.1 IMPROVING HEALTHCARE EXPENDITURE TO DRIVE MARKET

- 9.6.2 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 9.7 GCC COUNTRIES

- 9.7.1 RISING CATARACT PREVALENCE AND ADOPTION OF ADVANCED OPHTHALMIC TECHNOLOGIES TO DRIVE GROWTH

- 9.7.2 MACROECONOMIC OUTLOOK FOR GCC COUNTRIES

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 10.3 REVENUE ANALYSIS, 2020-2024

- 10.4 MARKET SHARE ANALYSIS, 2024

- 10.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.5.1 STARS

- 10.5.2 EMERGING LEADERS

- 10.5.3 PERVASIVE PLAYERS

- 10.5.4 PARTICIPANTS

- 10.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.5.5.1 Company footprint

- 10.5.5.2 Region footprint

- 10.5.5.3 Product footprint

- 10.5.5.4 End-user footprint

- 10.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 10.6.1 PROGRESSIVE COMPANIES

- 10.6.2 RESPONSIVE COMPANIES

- 10.6.3 DYNAMIC COMPANIES

- 10.6.4 STARTING BLOCKS

- 10.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 10.6.5.1 Detailed list of key startups/SMEs

- 10.6.5.2 Competitive benchmarking of key startups/SMEs

- 10.7 COMPANY VALUATION & FINANCIAL METRICS

- 10.7.1 FINANCIAL METRICS

- 10.7.2 COMPANY VALUATION

- 10.8 BRAND/PRODUCT COMPARISON

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES & APPROVALS

- 10.9.2 DEALS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 ALCON

- 11.1.1.1 Business overview

- 11.1.1.2 Products offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Product launches

- 11.1.1.3.2 Deals

- 11.1.1.4 MnM view

- 11.1.1.4.1 Right to win

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses & competitive threats

- 11.1.2 JOHNSON & JOHNSON

- 11.1.2.1 Business overview

- 11.1.2.2 Products offered

- 11.1.2.3 Recent developments

- 11.1.2.3.1 Product launches

- 11.1.2.4 MnM view

- 11.1.2.4.1 Right to win

- 11.1.2.4.2 Strategic choices

- 11.1.2.4.3 Weaknesses & competitive threats

- 11.1.3 CARL ZEISS MEDITEC AG

- 11.1.3.1 Business overview

- 11.1.3.2 Products offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Product launches

- 11.1.3.3.2 Deals

- 11.1.3.4 MnM view

- 11.1.3.4.1 Right to win

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses & competitive threats

- 11.1.4 BAUSCH HEALTH COMPANIES INC.

- 11.1.4.1 Business overview

- 11.1.4.2 Products offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Product launches

- 11.1.4.3.2 Deals

- 11.1.4.4 MnM view

- 11.1.4.4.1 Right to win

- 11.1.4.4.2 Strategic choices

- 11.1.4.4.3 Weaknesses & competitive threats

- 11.1.5 HOYA CORPORATION

- 11.1.5.1 Business overview

- 11.1.5.2 Products offered

- 11.1.5.2.1 Deals

- 11.1.5.3 MnM view

- 11.1.5.3.1 Right to win

- 11.1.5.3.2 Strategic choices

- 11.1.5.3.3 Weaknesses & competitive threats

- 11.1.6 ESSILORLUXOTTICA

- 11.1.6.1 Business overview

- 11.1.6.2 Products offered

- 11.1.6.3 Recent developments

- 11.1.6.3.1 Deals

- 11.1.7 CANON

- 11.1.7.1 Business overview

- 11.1.7.2 Products offered

- 11.1.8 GLAUKOS CORPORATION

- 11.1.8.1 Business overview

- 11.1.8.2 Products offered

- 11.1.8.3 Recent developments

- 11.1.8.3.1 Product approvals

- 11.1.8.3.2 Deals

- 11.1.9 TOPCON CORPORATION

- 11.1.9.1 Business overview

- 11.1.9.2 Products offered

- 11.1.9.3 Recent developments

- 11.1.9.3.1 Product launches

- 11.1.9.3.2 Deals

- 11.1.10 NIDEK CO., LTD.

- 11.1.10.1 Business overview

- 11.1.10.2 Products offered

- 11.1.10.3 Recent developments

- 11.1.10.3.1 Product launches

- 11.1.10.3.2 Deals

- 11.1.11 STAAR SURGICAL

- 11.1.11.1 Business overview

- 11.1.11.2 Products offered

- 11.1.11.3 Recent developments

- 11.1.11.3.1 Product approvals

- 11.1.12 HALMA PLC

- 11.1.12.1 Business overview

- 11.1.12.2 Products offered

- 11.1.13 HAAG-STREIT

- 11.1.13.1 Business overview

- 11.1.13.2 Products offered

- 11.1.13.3 Recent developments

- 11.1.13.3.1 Product launches

- 11.1.13.3.2 Deals

- 11.1.14 SHANGHAI MEDIWORKS PRECISION INSTRUMENTS CO., LTD.

- 11.1.14.1 Business overview

- 11.1.14.2 Products offered

- 11.1.15 VISIONIX

- 11.1.15.1 Business overview

- 11.1.15.2 Products offered

- 11.1.15.3 Recent developments

- 11.1.15.3.1 Deals

- 11.1.1 ALCON

- 11.2 OTHER PLAYERS

- 11.2.1 VISUNEX MEDICAL SYSTEMS

- 11.2.2 COSTRUZIONE STRUMENTI OFTALMICI

- 11.2.3 HAI LABORATORIES, INC.

- 11.2.4 FORUS HEALTH

- 11.2.5 ZIEMER OPHTHALMIC SYSTEMS AG

- 11.2.6 CRYSTALVUE MEDICAL CORPORATION

- 11.2.7 REMIDIO INNOVATIVE SOLUTIONS PVT. LTD.

- 11.2.8 SUZHOU KANGJIE MEDICAL INC.

- 11.2.9 LUMENIS

- 11.2.10 OPHTEC BV

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS