|

시장보고서

상품코드

1881236

BTB(Board-to-board) 커넥터 시장 : 유형별, 커넥터 유형별, 피치별, 마운팅 방식별, 용도별, 최종사용자별, 지역별 - 예측(-2030년)Board-to-Board Connector Market by Type (Male Connectors, Socket), Connector Type (Mezzanine, Backplane), Mounting (Surface-mount Technology, Through-hole Technology, Press-Fit, Hybrid), Pitch (<1 mm, 1 mm to 2 mm, >2 mm) - Global Forecast to 2030 |

||||||

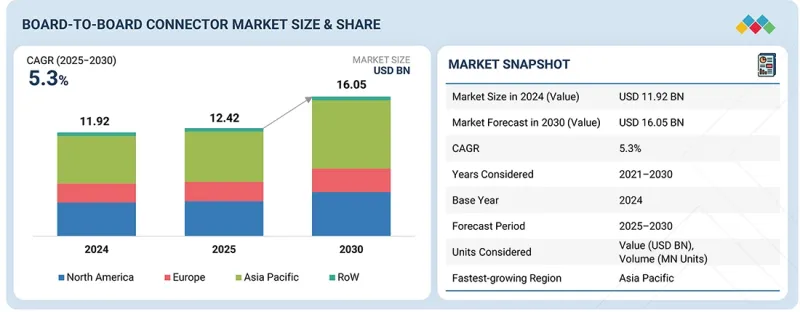

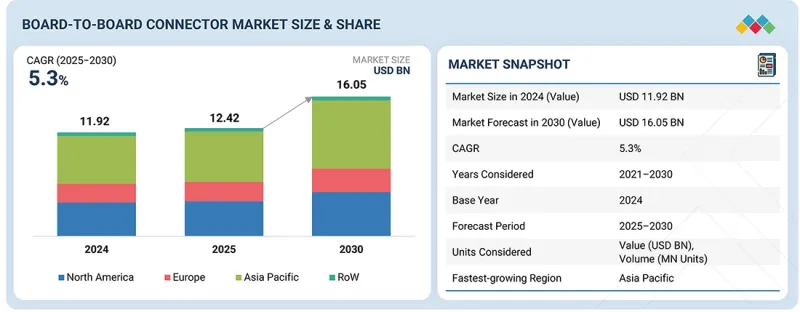

세계의 BTB(Board-to-board) 커넥터 시장 규모는 2025년에 124억 2,000만 달러, 2030년에는 160억 5,000만 달러에 이를 것으로 예측되고 있어 예측 기간 중 CAGR 5.3%를 보일 전망입니다.

산업 자동화 및 로봇 공학에 대한 수요 증가는 시장 성장을 가속하고 있으며, 공장 및 생산 시스템이 보다 혁신적이고 상호 연결된 기술을 채택하는 경향이 증가하고 있습니다. 이러한 커넥터는 제어 유닛, 센서, 로봇 부품 간의 데이터, 전력, 신호의 안정적인 전송을 실현하는 데 매우 중요합니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 유형별, 커넥터 유형별, 피치별, 마운팅 방식별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

산업이 인더스트리 4.0으로 전환하면서 열악한 작동 환경을 견딜 수 있는 소형, 내진동성, 고속 커넥터에 대한 수요가 증가하고 있습니다. 로봇, 프로그래머블 로직 컨트롤러(PLC), 자동화 기계는 정확성과 효율성을 보장하기 위해 이러한 커넥터에 의존하고 있으며, 제조, 물류, 공정 자동화 분야에서 지속적인 채택을 촉진하고 있습니다.

기판 간 커넥터 시장에서 1mm-2mm 피치 부문은 소형화, 신호 무결성, 기계적 신뢰성의 최적의 균형으로 인해 선도적인 위치를 차지할 것으로 예측됩니다. 이 피치 범위는 전기적 성능 저하 없이 컴팩트한 설계가 중요한 가전제품, 산업 자동화, 자동차 용도에 널리 사용되고 있습니다. 1mm 미만의 미세 피치에서는 고전류 처리 및 내구성 확보가 문제인 반면, 2mm 이상의 대형 피치는 공간 점유율이 높아 소자의 소형화를 제한합니다. 1-2mm 피치 범위는 고속 데이터 전송과 안정적인 전력 공급을 지원하므로 IoT 모듈, 웨어러블 기기, 자동차 제어 장치 등 첨단 장치에 적합합니다. 또한, 조립의 용이성, 제조 공정의 단순화, 기존 PCB 레이아웃과의 광범위한 호환성을 제공하기 때문에 제조업체는 이 부문을 선호합니다. 이러한 요소들이 결합되어 1-2mm 부문은 여러 산업 분야에서 성능, 크기, 비용 효율성의 균형을 맞추기 위한 최적의 선택이 되고 있습니다.

전기자동차(EV), 자율주행 기술, 첨단 인포테인먼트 시스템의 급속한 보급으로 자동차 부문은 기판 간 커넥터 시장에서 가장 빠른 성장률을 보일 것으로 예측됩니다. 현대 자동차는 수많은 전자제어장치(ECU), 센서, 배터리 관리 시스템에 의존하고 있으며, 이를 위해서는 소형의 고신뢰성 커넥터가 필수적입니다. 이를 통해 전력과 데이터의 원활한 전송을 보장합니다. 커넥티드카 및 스마트카로의 전환은 열악한 자동차 환경에서도 견딜 수 있는 고속 및 내진동 커넥터에 대한 수요를 더욱 증가시키고 있습니다. 또한, 차량 전동화, 첨단운전자보조시스템(ADAS), 차량용 커넥티비티에 대한 투자 확대는 자동차 산업에서 첨단 기판 간 커넥터 솔루션의 필요성을 지속적으로 견인하고 있습니다.

미국은 자동차, 항공우주, 방위, 전자기기 분야의 주요 제조업체들의 강력한 입지를 바탕으로 북미 기판 간 커넥터 시장을 독점하고 있습니다. 이 나라의 첨단 기술 인프라와 자동화, 5G, IoT 지원 시스템의 높은 도입률은 신뢰할 수 있는 고속 인터커넥트 솔루션에 대한 높은 수요를 견인하고 있습니다. TE Connectivity와 Molex와 같은 주요 기업들은 미국에 광범위한 사업 기반과 연구 개발 시설을 갖추고 혁신과 대규모 생산을 지원하고 있습니다. 또한, 전기자동차, 데이터센터, 산업용 로봇의 보급 확대는 미국 시장 지위를 더욱 강화하여 북미 내 기판 간 커넥터 수요와 개발의 중심지로서의 입지를 확고히 하고 있습니다.

세계의 기판-BTB(Board-to-board) 커넥터(Board-to-Board Connector) 시장을 조사했으며, 유형별/커넥터 유형별/피치별/마운팅 방식별/용도별/최종사용자별/지역별 동향, 시장 진출 기업 프로파일 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

- 서론

- 시장 역학

- 연결된 시장과 분야간 기회

- Tier1/2/3 기업의 전략적 움직임

제5장 업계 동향

- Porter의 Five Forces 분석

- 거시경제 전망

- 밸류체인 분석

- 생태계 분석

- 가격 분석

- 무역 분석

- 2026-2027년 주요 컨퍼런스 및 이벤트

- 관세 분석

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 2025년 미국 관세가 BTB(Board-to-board) 커넥터 시장에 미치는 영향

제6장 기술 진보, AI 별 영향, 특허, 혁신

- 주요 신기술

- 보완 기술

- 인접 기술

- 기술 및 제품 로드맵

- 특허 분석

- 보드간 커넥터 시장에 대한 AI의 영향

제7장 규제 상황

- 지역 규제와 컴플라이언스

- 규제기관, 정부기관 및 기타 조직

- 업계 표준

제8장 고객 상황과 구매 행동

- 의사결정 프로세스

- 주요 이해관계자와 구입 기준

- 채택 장벽과 내부 과제

- 다양한 최종사용자의 미충족 요구

제9장 BTB(Board-to-board) 커넥터 혁신 동향

- 서론

- 하이브리드 커넥터로의 이동

- AI와 엣지 컴퓨팅 하드웨어의 통합

- EMI 차폐 및 고속 커넥터 솔루션 개발

- 소형화와 파인 피치 커넥터 수요

- 제조 공정 자동 테스트와 검사 진보

제10장 BTB(Board-to-board) 커넥터 시장(유형별)

- 서론

- 메일 커넥터

- 소켓

제11장 BTB(Board-to-board) 커넥터 시장(커넥터 유형별)

- 서론

- 메자닌 커넥터

- 백플레인 커넥터

- 기타

제12장 BTB(Board-to-board) 커넥터 시장(피치 별)

- 서론

- 1mm 미만

- 1-2mm

- 2mm 이상

제13장 BTB(Board-to-board) 커넥터 시장(마운팅 유형별)

- 서론

- 표면 마운팅

- 스루홀

- PRESS-FIT

- 하이브리드

제14장 BTB(Board-to-board) 커넥터 시장(용도별)

- 서론

- 신호 전송

- 전력 공급

- 데이터 통신

제15장 BTB(Board-to-board) 커넥터 시장(최종사용자별)

- 서론

- 가전

- 산업 자동화

- 통신

- 자동차

- 건강 관리

- 항공우주 및 방위

- 기타

제16장 BTB(Board-to-board) 커넥터 시장(지역별)

- 서론

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽

- 기타

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 인도네시아

- 말레이시아

- 태국

- 베트남

- 기타

- 기타 지역

- 중동

- 남미

- 아프리카

제17장 경쟁 구도

- 개요

- 주요 시장 진출기업의 전략/강점, 2021년-2025년

- 매출 분석, 2020년-2024년

- 시장 점유율 분석, 2024년

- 기업 평가와 재무 지표

- 브랜드 비교

- 기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 경쟁 시나리오

제18장 기업 개요

- 주요 시장 진출기업

- TE CONNECTIVITY

- AMPHENOL CORPORATION

- HIROSE ELECTRIC CO., LTD.

- MOLEX, LLC

- JAPAN AVIATION ELECTRONICS INDUSTRY, LTD.

- SAMTEC

- CSCONN CORPORATION

- OMRON CORPORATION

- KYOCERA CORPORATION

- FIT HON TENG LIMITED

- HARTING TECHNOLOGY GROUP

- 기타 기업

- 3M

- HARWIN

- EPT GMBH

- KEL CORPORATION

- METZ CONNECT GMBH

- SMK CORPORATION

- ACES ELECTRONICS CO., LTD.

- AUK

- ROSENBERGER

- JST SALES AMERICA, INC.

- IRISO ELECTRONICS CO. LTD.

- YAMAICHI ELECTRONICS CO. LTD

- PHOENIX CONTACT

- DON CONNEX ELECTRONICS CO., LTD.

- WEITRONIC ENTERPRISE CO., LTD.

- AMTEK TECHNOLOGY CO., LTD.

- TAITEK COMPONENTS CO.,LTD.

- GREENCONN CO., LTD

- WCON ELECTRONICS(GUANGDONG) CO., LTD.

- KUNSHAN CONNECTORS ELECTRONICS CO., LTD.

- UNICORN ELECTRONICS COMPONENTS CO., LTD.

- OUPIIN GLOBAL

- CVILUX CORPORATION

- PLASTRON

제19장 조사 방법

제20장 부록

LSH 25.12.10The global board-to-board connector market is anticipated to reach USD 12.42 billion in 2025 and USD 16.05 billion by 2030, exhibiting a CAGR of 5.3% during the forecast period. The increasing demand for industrial automation and robotics fuels the market growth as factories and production systems adopt more innovative, interconnected technologies. These connectors are crucial in enabling the reliable transmission of data, power, and signals between control units, sensors, and robotic components.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Type, Connector Type, End User and Region |

| Regions covered | North America, Europe, APAC, RoW |

As industries transition to Industry 4.0, there is a growing demand for compact, vibration-resistant, and high-speed connectors that can withstand harsh operating environments. Robots, programmable logic controllers (PLCs), and automated machinery rely on these connectors for precision and efficiency, driving continuous adoption across manufacturing, logistics, and process automation sectors.

"1 mm to 2 mm segment is expected to hold the largest market share in 2030."

The 1 mm to 2 mm pitch segment in the board-to-board connector market is expected to dominate due to its optimal balance between miniaturization, signal integrity, and mechanical reliability. This pitch range is widely adopted in consumer electronics, industrial automation, and automotive applications where compact designs are critical without compromising electrical performance. Smaller pitches below 1 mm often face challenges in handling high current and ensuring durability, while larger pitches above 2 mm occupy more space and limit device miniaturization. The 1-2 mm range supports high-speed data transmission and reliable power delivery, making it suitable for advanced devices like IoT modules, wearables, and automotive control units. Additionally, manufacturers prefer this segment because it offers easier assembly, lower manufacturing complexity, and broad compatibility with existing PCB layouts. These factors collectively make the 1-2 mm segment the preferred choice for balancing performance, size, and cost efficiency across multiple industries.

"Automotive segment to grow at the fastest rate during the forecast period. "

The automotive segment is projected to grow the fastest in the board-to-board connector market due to the rapid adoption of electric vehicles (EVs), autonomous driving technologies, and advanced infotainment systems. Modern cars rely on numerous electronic control units (ECUs), sensors, and battery management systems that require compact, high-reliability connectors to ensure seamless power and data transmission. The shift toward connected and smart vehicles further boosts the demand for high-speed, vibration-resistant connectors that can withstand harsh automotive environments. Additionally, the growing investment in vehicle electrification, ADAS, and in-vehicle connectivity continues to drive the need for advanced board-to-board connector solutions in the automotive industry.

"US is expected to hold a significant market share in North America during the forecast period."

The US dominates the board-to-board connector market in North America due to its strong presence of leading manufacturers in the automotive, aerospace, defense, and electronics sectors. The country's advanced technological infrastructure and high adoption of automation, 5G, and IoT-enabled systems drive significant demand for reliable, high-speed interconnect solutions. Major players, such as TE Connectivity and Molex, have extensive operations and R&D facilities in the US, supporting innovation and large-scale production. Additionally, the growing use of electric vehicles, data centers, and industrial robotics further strengthens the US market position, making it the primary hub for board-to-board connector demand and development in North America.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the board-to-board connector marketplace.

- By Company Type: Tier 1 - 40%, Tier 2 - 35%, and Tier 3 - 25%

- By Designation: C-level Executives - 45%, Directors - 35%, and Others - 20%

- By Region: North America - 45%, Europe - 25%, Asia Pacific - 20%, and RoW - 10%

The study includes an in-depth competitive analysis of these key players in the board-to-board connector market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the board-to-board connector market by type, connector type, pitch, mounting type, application, end user, and region (North America, Europe, Asia Pacific, RoW). The report provides detailed information on the significant factors influencing market growth, including drivers, restraints, challenges, and opportunities. A thorough analysis of the key industry players has provided insights into their business overview, solutions and services, key strategies, contracts, partnerships, and agreements. Product and service launches, acquisitions, and recent developments associated with the market. This report covers a competitive analysis of upcoming startups in the board-to-board connector ecosystem.

Reasons to Buy This Report

The report will assist market leaders and new entrants with information on the closest approximations of revenue numbers for the board-to-board connector market and its subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (expansion of 5G networks and high-speed data communication, increasing focus on industrial automation and robotics, rising deployment of Internet of Things devices), restraints (technological complexities associated with developing application-specific board-to-board connectors, environmental and regulatory compliance), opportunities (expansion of electric vehicles, increasing demand for rugged connectors), and challenges (signal integrity and high-speed data transmission, cost optimization and pricing pressure) influencing the growth of the board-to-board connector market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the board-to-board connector market

- Market Development: Comprehensive information about lucrative markets with an analysis of the board-to-board connector market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the board-to-board connector market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the board-to-board connector market, such as TE Connectivity (Ireland), Amphenol Corporation (US), Hirose Electric Co. Ltd. (Japan), Molex (US), and Japan Aviation Electronics Industry, Ltd (Japan)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN BOARD-TO-BOARD CONNECTOR MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN BOARD-TO-BOARD CONNECTOR MARKET

- 3.2 BOARD-TO-BOARD CONNECTOR MARKET, BY TYPE

- 3.3 BOARD-TO-BOARD CONNECTOR MARKET, BY PITCH

- 3.4 BOARD-TO-BOARD CONNECTOR MARKET, BY END USER AND REGION

- 3.5 BOARD-TO-BOARD CONNECTOR MARKET, BY GEOGRAPHY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rapid expansion of 5G networks and escalated demand for high-speed data communication

- 4.2.1.2 Significant demand for industrial automation and robotics

- 4.2.1.3 Elevated adoption of IoT devices

- 4.2.2 RESTRAINTS

- 4.2.2.1 Technological complexities in developing application-specific connectors

- 4.2.2.2 High cost of environmental compliance

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising adoption of electric vehicles

- 4.2.3.2 Increasing demand for rugged, durable, and field-reliable electronics and heavy-duty machinery

- 4.2.4 CHALLENGES

- 4.2.4.1 Signal integrity and high-speed data transmission challenges

- 4.2.4.2 Cost optimization and pricing pressure

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMICS OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL CONSUMER ELECTRONICS INDUSTRY

- 5.2.4 TRENDS IN AUTOMOTIVE INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING RANGE OF BOARD-TO-BOARD CONNECTORS OFFERED BY KEY PLAYERS, BY PITCH, 2024

- 5.5.2 AVERAGE SELLING PRICE TREND OF BOARD-TO-BOARD CONNECTORS, BY PITCH, 2020-2024

- 5.5.3 AVERAGE SELLING PRICE TREND OF BOARD-TO-BOARD CONNECTORS, BY REGION, 2020-2024

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 8536)

- 5.6.2 EXPORT SCENARIO (HS CODE 8536)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TARIFF ANALYSIS

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 AUTOMOBILE MANUFACTURER ACHIEVES RELIABLE HIGH-SPEED COMMUNICATION BETWEEN ECUS USING BOARD-TO-BOARD CONNECTORS FROM JAE

- 5.11.2 GCT DELIVERS GROUND-FIRST CONNECTOR SOLUTION FOR ENHANCED SYSTEM PROTECTION

- 5.11.3 GCT DEVELOPS CUSTOMIZED PIN HEADER INSULATOR TO IMPROVE PCB ASSEMBLY ACCURACY

- 5.12 IMPACT OF 2025 US TARIFF ON BOARD-TO-BOARD CONNECTOR MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END USERS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 HIGH-SPEED DATA TRANSMISSION

- 6.1.2 SURFACE-MOUNT TECHNOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 CONNECTOR LOCKING AND LATCHING MECHANISM

- 6.2.2 ELECTROMAGNETIC INTERFERENCE/RADIO FREQUENCY INTERFERENCE SHIELDING AND FILTERING

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 POWER DELIVERY AND MANAGEMENT

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 MID-TERM EVOLUTION (2027-2030): HIGH-SPEED & HYBRID ARCHITECTURES

- 6.4.2 LONG-TERM OUTLOOK (2025-2035+): INTELLIGENT, ULTRA-MINIATURE & SUSTAINABLE SYSTEMS

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI ON BOARD-TO-BOARD CONNECTOR MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY COMPANIES IN BOARD-TO-BOARD CONNECTOR MARKET

- 6.6.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN BOARD-TO-BOARD CONNECTOR MARKET

- 6.6.4 INTERCONNECTED/ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI IN BOARD-TO-BOARD CONNECTOR MANUFACTURING

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END USERS

9 INNOVATION TRENDS IN BOARD-TO-BOARD TO CONNECTORS

- 9.1 INTRODUCTION

- 9.2 SHIFT TO HYBRID CONNECTORS

- 9.3 INTEGRATION WITH AI AND EDGE COMPUTING HARDWARE

- 9.4 DEVELOPMENT OF EMI-SHIELDED AND HIGH-SPEED CONNECTOR SOLUTIONS

- 9.5 MINIATURIZATION AND DEMAND FOR FINE-PITCH CONNECTORS

- 9.6 ADVANCEMENTS IN AUTOMATED TESTING AND INSPECTION DURING MANUFACTURING

10 BOARD-TO-BOARD CONNECTOR MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 MALE CONNECTORS

- 10.2.1 STACKED HEADERS

- 10.2.1.1 Strong focus on designing compact and high-density devices to spike demand

- 10.2.2 SHROUDED HEADERS

- 10.2.2.1 Pressing need for secure, robust, and error-proof connections between boards and cables to foster segmental growth

- 10.2.1 STACKED HEADERS

- 10.3 SOCKETS

- 10.3.1 INCREASING DEMAND FOR MULTI-BOARD ARCHITECTURES TO CREATE OPPORTUNITIES

11 BOARD-TO-BOARD CONNECTOR MARKET, BY CONNECTOR TYPE

- 11.1 INTRODUCTION

- 11.2 MEZZANINE CONNECTORS

- 11.2.1 INCREASING DEMAND FOR COMPACT CONSUMER ELECTRONICS TO FUEL SEGMENTAL GROWTH

- 11.3 BACKPLANE CONNECTORS

- 11.3.1 SURGING NEED FOR FASTER DATA TRANSMISSION TO STIMULATE SEGMENTAL GROWTH

- 11.4 OTHER CONNECTOR TYPES

12 BOARD-TO-BOARD CONNECTOR MARKET, BY PITCH

- 12.1 INTRODUCTION

- 12.2 LESS THAN 1 MM

- 12.2.1 0.80 MM

- 12.2.1.1 Rising demand for ultra-compact electronics to support segmental growth

- 12.2.2 0.65 MM

- 12.2.2.1 Ongoing requirement for ultra-fine pitch connectors, maintaining signal integrity and mechanical stability to drive market

- 12.2.3 OTHER FINE PITCH CATEGORIES

- 12.2.1 0.80 MM

- 12.3 1 TO 2 MM

- 12.3.1 1.00 MM

- 12.3.1.1 Shrinking size of electronic devices to create growth opportunities

- 12.3.2 1.27 MM

- 12.3.2.1 Growing demand for high mechanical reliability in harsh environments to support segmental growth

- 12.3.3 1.50 MM

- 12.3.3.1 Excellence in balancing high current capacity with efficient space utilization to facilitate market growth

- 12.3.4 2.00 MM

- 12.3.4.1 Wide use in industrial, transportation, and aerospace applications to contribute to market growth

- 12.3.1 1.00 MM

- 12.4 GREATER THAN 2 MM

- 12.4.1 2.54 MM

- 12.4.1.1 Elevating demand for industrial automation, power electronics, and rugged embedded systems to favor segmental growth

- 12.4.2 3.00 MM

- 12.4.2.1 Superior resistance to vibration and thermal stress to stimulate demand

- 12.4.3 OTHER STANDARD PITCH CATEGORIES

- 12.4.1 2.54 MM

13 BOARD-TO-BOARD CONNECTOR MARKET, BY MOUNTING TYPE

- 13.1 INTRODUCTION

- 13.2 SURFACE-MOUNT

- 13.2.1 ABILITY TO SUPPORT HIGH-FREQUENCY SIGNALS AND DENSE CIRCUITRY TO BOOST DEMAND

- 13.3 THROUGH-HOLE

- 13.3.1 RISING USE IN INDUSTRIAL EQUIPMENT, POWER SUPPLIES, AND MILITARY ELECTRONICS TO CONTRIBUTE TO MARKET GROWTH

- 13.4 PRESS-FIT

- 13.4.1 POTENTIAL TO HANDLE HIGH CURRENTS AND FREQUENT MECHANICAL STRESS TO ACCELERATE DEMAND

- 13.5 HYBRID

- 13.5.1 RISING DEMAND FOR HIGH-PERFORMANCE ELECTRONICS IN SPACE-CONSTRAINED ENVIRONMENTS TO PROPEL MARKET

14 BOARD-TO-BOARD CONNECTOR MARKET, BY APPLICATION

- 14.1 INTRODUCTION

- 14.2 SIGNAL TRANSMISSION

- 14.2.1 HIGH-SPEED/HIGH-FREQUENCY

- 14.2.1.1 Escalating demand for high-performance computing to fuel market growth

- 14.2.2 MIXED SIGNAL

- 14.2.2.1 Growing need for compact multifunctional interconnects in industrial automation to fuel market growth

- 14.2.1 HIGH-SPEED/HIGH-FREQUENCY

- 14.3 POWER DELIVERY

- 14.3.1 ABILITY TO ENSURE STABLE POWER FLOW EVEN IN COMPACT ASSEMBLIES TO BOOST DEMAND

- 14.4 DATA COMMUNICATION

- 14.4.1 GROWING INCLINATION TOWARD 5G, IOT, AND EDGE COMPUTING TO SPUR DEMAND

15 BOARD-TO-BOARD CONNECTOR MARKET, BY END USER

- 15.1 INTRODUCTION

- 15.2 CONSUMER ELECTRONICS

- 15.2.1 RISING ADOPTION OF ULTRA-THIN AND COMPACT DEVICE DESIGNS TO SUPPORT MARKET GROWTH

- 15.3 INDUSTRIAL AUTOMATION

- 15.3.1 ROBOTICS

- 15.3.1.1 Rapid integration of smart sensors and AI-based control systems to drive market

- 15.3.2 HUMANOID

- 15.3.2.1 Increasing use of intelligent robots in logistics applications to fuel market growth

- 15.3.3 FACTORY CONTROL SYSTEMS

- 15.3.3.1 Transition toward connected automation to fuel growth

- 15.3.4 INDUSTRIAL IOT DEVICES

- 15.3.4.1 Expansion of smart factories to expedite market growth

- 15.3.1 ROBOTICS

- 15.4 TELECOMMUNICATIONS

- 15.4.1 GLOBAL EXPANSION OF 5G NETWORKS TO SUPPORT MARKET GROWTH

- 15.5 AUTOMOTIVE

- 15.5.1 INTERNAL COMBUSTION ENGINES

- 15.5.1.1 Need for efficient communication and power distribution across complex powertrain architectures to drive market

- 15.5.2 ELECTRIC VEHICLES

- 15.5.2.1 Shift toward integrated electronic architectures to create growth opportunities

- 15.5.3 SELF-DRIVING VEHICLES

- 15.5.3.1 Surging adoption of autonomous driving technologies to boost demand

- 15.5.1 INTERNAL COMBUSTION ENGINES

- 15.6 HEALTHCARE

- 15.6.1 PRESSING NEED FOR PORTABILITY, CONNECTIVITY, AND REAL-TIME DATA HANDLING TO ACCELERATE MARKET GROWTH

- 15.7 AEROSPACE & DEFENSE

- 15.7.1 AIRCRAFT

- 15.7.1.1 Focus on simplifying wiring, reducing aircraft weight, and ensuring high performance to drive demand

- 15.7.2 DRONES

- 15.7.2.1 Increasing demand for autonomous and long-endurance drones to foster market growth

- 15.7.3 WEAPONS & ELECTRONIC WARFARE SYSTEMS

- 15.7.3.1 Surging demand for advanced and mechanically robust electronic warfare systems to stimulate market growth

- 15.7.4 OTHER AEROSPACE & DEFENSE APPLICATIONS

- 15.7.1 AIRCRAFT

- 15.8 OTHER END USERS

16 BOARD-TO-BOARD CONNECTOR MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 NORTH AMERICA

- 16.2.1 US

- 16.2.1.1 Surging demand for cloud services with integration of AI models to accelerate market growth

- 16.2.2 CANADA

- 16.2.2.1 Evolving industrial and electronics landscape to create growth opportunities

- 16.2.3 MEXICO

- 16.2.3.1 Expansion of production facilities to boost demand

- 16.2.1 US

- 16.3 EUROPE

- 16.3.1 GERMANY

- 16.3.1.1 Growing focus of industrial sector on smart manufacturing to support market growth

- 16.3.2 UK

- 16.3.2.1 Increasing investments in data centers to foster market growth

- 16.3.3 FRANCE

- 16.3.3.1 Significant focus on expanding semiconductor packaging and electronic manufacturing capacity to boost demand

- 16.3.4 ITALY

- 16.3.4.1 Modernization of railway networks and industrial electronics to spur demand

- 16.3.5 SPAIN

- 16.3.5.1 Strong focus on strengthening domestic electronics manufacturing base to create opportunities

- 16.3.6 NORDICS

- 16.3.6.1 Rapid expansion of 5G and telecom infrastructure to accelerate demand

- 16.3.7 REST OF EUROPE

- 16.3.1 GERMANY

- 16.4 ASIA PACIFIC

- 16.4.1 CHINA

- 16.4.1.1 Expansion of electronics and electric vehicle manufacturing ecosystem to expedite market growth

- 16.4.2 JAPAN

- 16.4.2.1 Strong focus of electronics manufacturers on miniaturization and precision engineering to support market growth

- 16.4.3 SOUTH KOREA

- 16.4.3.1 Rapid expansion of 5G and semiconductor ecosystem to facilitate demand

- 16.4.4 INDIA

- 16.4.4.1 Booming electronics manufacturing industry to contribute to market growth

- 16.4.5 AUSTRALIA

- 16.4.5.1 Ongoing renewable energy and smart grid infrastructure projects to drive market

- 16.4.6 INDONESIA

- 16.4.6.1 Growing inclination toward industrial automation to surge demand

- 16.4.7 MALAYSIA

- 16.4.7.1 Increasing investments in advanced packaging, automotive electronics, and smart devices to create opportunities

- 16.4.8 THAILAND

- 16.4.8.1 Growing emphasis on smart manufacturing to expedite demand

- 16.4.9 VIETNAM

- 16.4.9.1 Emphasis on expanding consumer electronics and industrial equipment manufacturing base to fuel demand

- 16.4.10 REST OF ASIA PACIFIC

- 16.4.1 CHINA

- 16.5 ROW

- 16.5.1 MIDDLE EAST

- 16.5.1.1 Saudi Arabia

- 16.5.1.1.1 Focus on digital manufacturing and industrial automation to fuel market growth

- 16.5.1.2 UAE

- 16.5.1.2.1 Expansion of data centers, telecommunications networks, and IoT-enabled systems to spike demand

- 16.5.1.3 Qatar

- 16.5.1.3.1 Growth in IT infrastructure to drive demand

- 16.5.1.4 Kuwait

- 16.5.1.4.1 Modernization of energy and industrial infrastructure to favor market growth

- 16.5.1.5 Oman

- 16.5.1.5.1 Digital transformation of industrial sector to boost demand

- 16.5.1.6 Bahrain

- 16.5.1.6.1 Increasing investments in advanced manufacturing to propel market

- 16.5.1.7 Rest of Middle East

- 16.5.1.1 Saudi Arabia

- 16.5.2 SOUTH AMERICA

- 16.5.2.1 Growing renewable energy infrastructure to drive market

- 16.5.3 AFRICA

- 16.5.3.1 South Africa

- 16.5.3.1.1 Growing renewable energy projects and booming power electronics sector to support market growth

- 16.5.3.2 Rest of Africa

- 16.5.3.1 South Africa

- 16.5.1 MIDDLE EAST

17 COMPETITIVE LANDSCAPE

- 17.1 OVERVIEW

- 17.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 17.3 REVENUE ANALYSIS, 2020-2024

- 17.4 MARKET SHARE ANALYSIS, 2024

- 17.5 COMPANY VALUATION AND FINANCIAL METRICS

- 17.6 BRAND COMPARISON

- 17.6.1 TE CONNECTIVITY

- 17.6.2 AMPHENOL CORPORATION

- 17.6.3 HIROSE ELECTRIC CO., LTD.

- 17.6.4 MOLEX

- 17.6.5 JAPAN AVIATION ELECTRONICS INDUSTRY, LTD.

- 17.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 17.7.1 STARS

- 17.7.2 EMERGING LEADERS

- 17.7.3 PERVASIVE PLAYERS

- 17.7.4 PARTICIPANTS

- 17.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 17.7.5.1 Company footprint

- 17.7.5.2 Region footprint

- 17.7.5.3 Type footprint

- 17.7.5.4 Connector type footprint

- 17.7.5.5 Pitch footprint

- 17.7.5.6 End user footprint

- 17.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 17.8.1 PROGRESSIVE COMPANIES

- 17.8.2 RESPONSIVE COMPANIES

- 17.8.3 DYNAMIC COMPANIES

- 17.8.4 STARTING BLOCKS

- 17.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 17.8.5.1 Detailed list of key startups/SMEs

- 17.8.5.2 Competitive benchmarking of key startups/SMEs

- 17.9 COMPETITIVE SCENARIO

- 17.9.1 PRODUCT LAUNCHES & ENHANCEMENTS

- 17.9.2 DEALS

- 17.9.3 EXPANSIONS

18 COMPANY PROFILES

- 18.1 KEY PLAYERS

- 18.1.1 TE CONNECTIVITY

- 18.1.1.1 Business overview

- 18.1.1.2 Products/Solutions/Services offered

- 18.1.1.3 Recent developments

- 18.1.1.3.1 Product launches & enhancements

- 18.1.1.3.2 Expansions

- 18.1.1.4 MnM view

- 18.1.1.4.1 Key strengths/Right to win

- 18.1.1.4.2 Strategic choices

- 18.1.1.4.3 Weaknesses/Competitive threats

- 18.1.2 AMPHENOL CORPORATION

- 18.1.2.1 Business overview

- 18.1.2.2 Products/Solutions/Services offered

- 18.1.2.3 Recent developments

- 18.1.2.3.1 Product launches & enhancements

- 18.1.2.4 MnM view

- 18.1.2.4.1 Key strengths/Right to win

- 18.1.2.4.2 Strategic choices

- 18.1.2.4.3 Weaknesses/Competitive threats

- 18.1.3 HIROSE ELECTRIC CO., LTD.

- 18.1.3.1 Business overview

- 18.1.3.2 Products/Solutions/Services offered

- 18.1.3.3 Recent developments

- 18.1.3.3.1 Product launches & enhancements

- 18.1.3.4 MnM view

- 18.1.3.4.1 Key strengths/Right to win

- 18.1.3.4.2 Strategic choices

- 18.1.3.4.3 Weaknesses/Competitive threats

- 18.1.4 MOLEX, LLC

- 18.1.4.1 Business overview

- 18.1.4.2 Products/Solutions/Services offered

- 18.1.4.3 Recent developments

- 18.1.4.3.1 Product launches & enhancements

- 18.1.4.3.2 Deals

- 18.1.4.3.3 Expansions

- 18.1.4.4 MnM view

- 18.1.4.4.1 Key strengths/Right to win

- 18.1.4.4.2 Strategic choices

- 18.1.4.4.3 Weaknesses/Competitive threats

- 18.1.5 JAPAN AVIATION ELECTRONICS INDUSTRY, LTD.

- 18.1.5.1 Business overview

- 18.1.5.2 Products/Solutions/Services offered

- 18.1.5.3 Recent developments

- 18.1.5.3.1 Product launches & enhancements

- 18.1.5.4 MnM view

- 18.1.5.4.1 Key strengths/Right to win

- 18.1.5.4.2 Strategic choices

- 18.1.5.4.3 Weaknesses/Competitive threats

- 18.1.6 SAMTEC

- 18.1.6.1 Business overview

- 18.1.6.2 Products/Solutions/Services offered

- 18.1.6.3 Recent developments

- 18.1.6.3.1 Product launches & enhancements

- 18.1.6.4 MnM view

- 18.1.6.4.1 Key strengths/Right to win

- 18.1.6.4.2 Strategic choices

- 18.1.6.4.3 Weaknesses/Competitive threats

- 18.1.7 CSCONN CORPORATION

- 18.1.7.1 Business overview

- 18.1.7.2 Products/Solutions/Services offered

- 18.1.7.3 MnM view

- 18.1.7.3.1 Key strengths/Right to win

- 18.1.7.3.2 Strategic choices

- 18.1.7.3.3 Weaknesses/Competitive threats

- 18.1.8 OMRON CORPORATION

- 18.1.8.1 Business overview

- 18.1.8.2 Products/Solutions/Services offered

- 18.1.8.3 MnM view

- 18.1.8.3.1 Key strengths/Right to win

- 18.1.8.3.2 Strategic choices

- 18.1.8.3.3 Weaknesses/Competitive threats

- 18.1.9 KYOCERA CORPORATION

- 18.1.9.1 Business overview

- 18.1.9.2 Products/Solutions/Services offered

- 18.1.9.3 Recent developments

- 18.1.9.3.1 Product launches & enhancements

- 18.1.9.4 MnM view

- 18.1.9.4.1 Key strengths/Right to win

- 18.1.9.4.2 Strategic choices

- 18.1.9.4.3 Weaknesses/Competitive threats

- 18.1.10 FIT HON TENG LIMITED

- 18.1.10.1 Business overview

- 18.1.10.2 Products/Solutions/Services offered

- 18.1.10.3 Recent developments

- 18.1.10.3.1 Expansions

- 18.1.10.4 MnM view

- 18.1.10.4.1 Key strengths/Right to win

- 18.1.10.4.2 Strategic choices

- 18.1.10.4.3 Weaknesses/Competitive threats

- 18.1.11 HARTING TECHNOLOGY GROUP

- 18.1.11.1 Business overview

- 18.1.11.2 Products/Solutions/Services offered

- 18.1.11.3 Recent developments

- 18.1.11.3.1 Product launches & enhancements

- 18.1.11.3.2 Deals

- 18.1.11.3.3 Expansions

- 18.1.11.4 MnM view

- 18.1.11.4.1 Key strengths/Right to win

- 18.1.11.4.2 Strategic choices

- 18.1.11.4.3 Weaknesses/Competitive threats

- 18.1.1 TE CONNECTIVITY

- 18.2 OTHER PLAYERS

- 18.2.1 3M

- 18.2.2 HARWIN

- 18.2.3 EPT GMBH

- 18.2.4 KEL CORPORATION

- 18.2.5 METZ CONNECT GMBH

- 18.2.6 SMK CORPORATION

- 18.2.7 ACES ELECTRONICS CO., LTD.

- 18.2.8 AUK

- 18.2.9 ROSENBERGER

- 18.2.10 JST SALES AMERICA, INC.

- 18.2.11 IRISO ELECTRONICS CO. LTD.

- 18.2.12 YAMAICHI ELECTRONICS CO. LTD

- 18.2.13 PHOENIX CONTACT

- 18.2.14 DON CONNEX ELECTRONICS CO., LTD.

- 18.2.15 WEITRONIC ENTERPRISE CO., LTD.

- 18.2.16 AMTEK TECHNOLOGY CO., LTD.

- 18.2.17 TAITEK COMPONENTS CO.,LTD.

- 18.2.18 GREENCONN CO., LTD

- 18.2.19 WCON ELECTRONICS (GUANGDONG) CO., LTD.

- 18.2.20 KUNSHAN CONNECTORS ELECTRONICS CO., LTD.

- 18.2.21 UNICORN ELECTRONICS COMPONENTS CO., LTD.

- 18.2.22 OUPIIN GLOBAL

- 18.2.23 CVILUX CORPORATION

- 18.2.24 PLASTRON

19 RESEARCH METHODOLOGY

- 19.1 RESEARCH DATA

- 19.1.1 SECONDARY AND PRIMARY RESEARCH

- 19.1.2 SECONDARY DATA

- 19.1.2.1 List of major secondary sources

- 19.1.2.2 Key data from secondary sources

- 19.1.3 PRIMARY DATA

- 19.1.3.1 List of primary interview participants

- 19.1.3.2 Key data from primary sources

- 19.1.3.3 Key industry insights

- 19.1.3.4 Breakdown of primaries

- 19.2 MARKET SIZE ESTIMATION

- 19.2.1 TOP-DOWN APPROACH

- 19.2.2 BOTTOM-UP APPROACH

- 19.2.3 MARKET SIZE ESTIMATION METHODOLOGY

- 19.3 MARKET FORECAST APPROACH

- 19.3.1 SUPPLY SIDE

- 19.3.2 DEMAND SIDE

- 19.4 DATA TRIANGULATION

- 19.5 RESEARCH ASSUMPTIONS

- 19.6 RESEARCH LIMITATIONS

- 19.7 RISK ASSESSMENT

20 APPENDIX

- 20.1 INSIGHTS FROM INDUSTRY EXPERTS

- 20.2 DISCUSSION GUIDE

- 20.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.4 CUSTOMIZATION OPTIONS

- 20.5 RELATED REPORTS

- 20.6 AUTHOR DETAILS