|

시장보고서

상품코드

1883935

SaaS 관리 시장 : 플랫폼별, 전개 모드별, 업무 기능별, 산업별 - 예측(-2030년)SaaS Management Market by Platform, Deployment Mode, Business Function, Vertical - Global Forecast to 2030 |

||||||

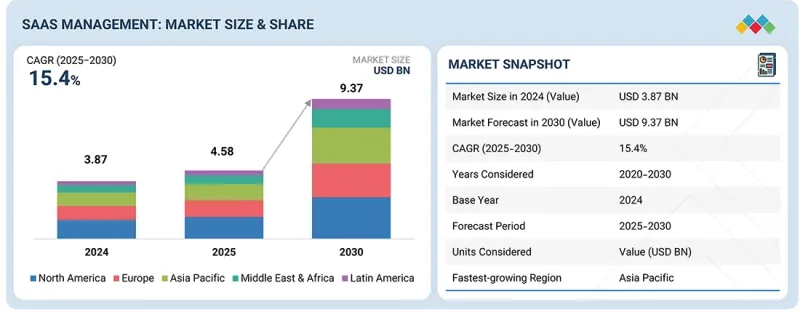

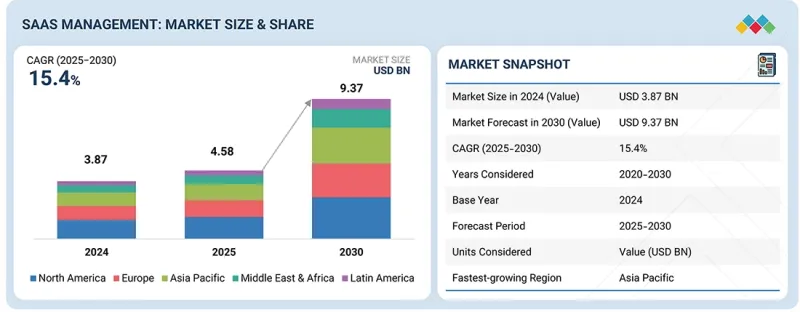

세계의 SaaS 관리 시장 규모는 2025년 45억 8,000만 달러로 추정되고, 2030년까지 93억 7,000만 달러에 이를 것으로 예측되며, CAGR 15.4%로 성장이 전망됩니다.

하이브리드 및 멀티클라우드 아키텍처의 채택이 확대됨에 따라 기업이 AWS, Microsoft Azure, Google Cloud 및 On-Premise 시스템에 걸쳐 애플리케이션을 운영하는 동안 중앙 집중식 SaaS 관리에 대한 요구가 가속화되고 있습니다. 이 분산 환경은 운영 단편화를 만들어 IT, 보안, 조달 팀이 라이선스 소유권 추적, 데이터 흐름 관리, 액세스 제어 구현, 일관된 컴플라이언스 유지를 어렵게 만듭니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 100만/10억 달러 |

| 부문 | 플랫폼, 전개 모드, 업무 기능, 산업, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

클라우드 네이티브 서비스가 대규모 SaaS 포트폴리오와 융합하는 동안 조직은 각 환경에서 사용, 지출, 통합 패턴 및 정책 준수 상황을 중앙에서 시각화해야 합니다. 이러한 상호연결된 에코시스템을 효과적으로 관리하기 위해 클라우드 횡단적인 가관성, 표준화된 거버넌스 워크플로우, 모든 전개 모드에 걸쳐 통합적인 정책 시행을 실현하는 SaaS 관리 플랫폼의 채용이 진행되고 있습니다.

각 공급업체는 멀티클라우드 검색, 자동화된 구성 모니터링, 보안 모니터링, 워크플로 오케스트레이션 및 통합 매핑을 SaaS 관리 솔루션에 통합하여 대응합니다. Torii, Productiv, BetterCloud와 같은 플랫폼은 하이브리드 환경 전반의 사용 현황 분석, 액세스 거버넌스 및 애플리케이션 수명 주기 관리를 통합하는 단일 제어 계층을 조직에 제공합니다. 이러한 도구는 권한이 없는 애플리케이션을 식별하고, 사용자 프로비저닝을 효율화하며, 컴플라이언스 워크플로우를 자동화하고, 업무 일관성을 높이며, 위험을 줄입니다. 하이브리드 및 멀티클라우드 전략이 엔터프라이즈 IT의 기반이 되는 가운데, 애플리케이션 성능 최적화, 데이터 무결성 보호, 복잡한 클라우드 에코시스템 전반에 걸친 소프트웨어 비용 관리를 실현하기 위해서는 중앙 집중식 SaaS 거버넌스 프레임워크가 필수적입니다.

'SaaS 보안 거버넌스는 기업이 보호 및 규정 준수를 우선시하고 있기 때문에 높은 성장이 예상됩니다.'

SaaS 보안 거버넌스 솔루션은 SaaS 관리 시장에서 가장 빠르게 성장하는 부문입니다. 이는 기업이 클라우드 기반 애플리케이션 에코시스템의 보안 강화, 컴플라이언스 철저, 업무 및 액세스 관련 위험 완화에 주력하고 있기 때문입니다. 조직은 분산 SaaS 환경 전반에서 데이터 흐름, 사용자 권한, 구성 설정 및 정책 위반을 실시간으로 시각화하기 위해 이러한 솔루션의 채택을 가속화하고 있습니다. 이러한 플랫폼은 자동 액세스 검토, 보안 설정 기준, 지속적인 모니터링, 위협 감지, 통일된 정책 시행을 지원하며, 기업이 섀도우 IT 위험, 무단 통합 및 개인정보 보호 위험을 해결할 수 있도록 지원합니다. 이 부문의 급속한 성장은 ID 확산, 애플리케이션 간 데이터 마이그레이션, 세계 시장에서의 규제 의무의 복잡성에 의해 더욱 가속화되고 있습니다.

또한 거버넌스 워크플로우의 정확성 및 확장성을 향상시키는 첨단 기술 통합도 성장을 지원합니다. 각 공급업체는 AI에 의한 이상 감지, 자동 컴플라이언스 평가, 행동 분석, 상황 인식 경보를 통합하여 기업의 인력 모니터링을 줄이고 일관된 보안 표준을 시행할 수 있도록 지원합니다. SaaS 포트폴리오가 확대됨에 따라 조직은 다중 테넌트 환경 전반의 통합 제어 액세스, 데이터 보호 프레임워크 준수 및 감사를 위한 보고서 작성을 지원하는 솔루션을 찾고 있습니다. 제로 트러스트 모델의 추진, 보안 액세스 거버넌스, 예방적 위험 완화에 대한 강한 움직임으로 SaaS 보안 거버넌스는 SaaS 관리의 미래를 형성하는 가장 역동적이고 전략적으로 필수적인 부문이 되었습니다.

이 보고서는 세계의 SaaS 관리 시장에 대한 조사 분석을 통해 주요 촉진요인 및 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요한 지견

- SaaS 관리 시장의 기업에게 매력적인 기회

- SaaS 관리 시장 : 주요 플랫폼 유형

- 북미의 SaaS 관리 시장 : 주요 플랫폼 유형별, 업무 기능별

- SaaS 관리 시장 : 지역별

제5장 시장 개요

- 서문서문

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 언멧 요구 및 화이트 스페이스

- SaaS 관리 시장의 미충족 요구

- 화이트 스페이스의 기회

- 상호접속된 시장 및 부문 간 기회

- 상호연결된 시장

- 부문 간 기회

- Tier 1/2/3 기업의 전략적 움직임

제6장 업계 동향

- SaaS 관리의 진화

- Porter's Five Forces 분석

- 공급망 분석

- 생태계 분석

- SaaS 디스커버리 인벤토리 프로바이더

- SaaS 라이선스 관리 제공업체

- SaaS 갱신 및 지출 관리 프로바이더

- SaaS 보안 거버넌스 제공업체

- SaaS 자동화 애널리틱스

- 가격 설정 분석

- SaaS 관리 서비스의 평균 판매 가격 : 주요 기업별(2025년)

- SaaS 관리 플랫폼의 평균 판매 가격 : 업무 기능별(2025년)

- 주요 컨퍼런스 및 이벤트(2025-2026년)

- 고객 사업에 영향을 주는 동향 및 혼란

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 미국 관세의 영향-SaaS 관리 시장(2025년)

- 서문

- 관세 및 무역 정책의 최신 정보(2025년 8월-9월)

- 주요 관세율

- 가격의 영향 분석

- 국가 및 지역에 미치는 영향

- 최종 이용 산업에 대한 영향

제7장 기술의 진보, AI에 의한 영향, 특허, 혁신, 장래 용도

- 주요 신기술

- SaaS 디스커버리 커넥터

- 통합 앱 인벤토리 그래프, 데이터 정규화 레이어

- 사용 상황 텔레메트리 파이프라인, 라이선스 사용률 애널리틱스

- SCIM 및 JIT에 의한 ID 라이프사이클 자동화(JML)

- 액세스 거버넌스(RBAC/ABAC), 정기 액세스 증명

- 계약 인텔리전스

- FINOPS 지출 분석

- 보완 기술

- ID 제공업체, 디렉토리 기술

- ITSM 플랫폼, 변경 워크플로우

- ERP 및 재무, AP 시스템

- 전자 서명 서비스

- IPAAS, 워크플로우 브릿지

- 데이터 파이프라인, 웨어하우징

- SIEM 및 로그 관리

- 비밀 관리, 보관

- 인접 기술

- IGA/IAM 스위트

- 특권 액세스 관리

- 기존 ITAM/SAM 스위트

- 브라우저 보안 플랫폼(BSP), 엔터프라이즈 브라우저 기술

- 디지털 종업원 체험 애널리틱스

- 기술 로드맵

- 단기(2025-2027년) : 기반 구축, 표준화 단계

- 중기(2028-2030년) : 컨버전스, 자동화 단계

- 장기(2031-2035년) : 자율식, 인지 SaaS 관리 단계

- 특허 분석

- 조사 방법

- 특허 출원 건수 : 서류 유형별(2016-2025년)

- 혁신 및 특허출원

- 미래의 용도

- 제로 터치 SaaS 생태계 관리 : 자기 학습 오케스트레이션 엔진

- SaaS 지출 예측, 적응형 예산 편성 : 동적 비용 모델링 알고리즘

- SaaS 상호 운용성, 통합 거버넌스 패브릭 : 크로스 플랫폼 거버넌스 프로토콜

- 동적 컴플라이언스, 지속적인 감사 자동화 : AI에 의한 정책 검증

- SaaS 탄소 회계, 지속 가능한 IT 최적화 : 에너지, 탄소, ESG 데이터 세트를 사용한 SaaS 사용 데이터

- SaaS 관리 시장에 대한 생성형 AI의 영향

- SaaS 디스커버리 애플리케이션 인텔리전스

- 라이선스 최적화 및 지출 인텔리전스

- 계약 수명 주기 및 갱신 관리

- 예측 분석 및 인사이트 생성

- 자동 컴플라이언스 리스크 거버넌스

- 적응형 워크플로우 자동화 및 유저 유효화

제8장 규제 상황

- 지역 규제 및 규정 준수

- 규제 기관, 정부기관, 기타 조직

- 주요 규제

제9장 고객 정세 및 구매 행동

- 의사 결정 프로세스

- 주요 이해관계자 및 구매 평가 기준

- 채용 장벽 및 내부 과제

- 다양한 업계의 미충족 요구

제10장 SaaS 관리 시장 : 제공별

- 서문

- 플랫폼

- SaaS 디스커버리 인벤토리

- SaaS 라이선스 관리

- SaaS 갱신 및 지출 관리

- SaaS 보안 거버넌스

- SaaS 자동화 애널리틱스

- 서비스

- 전문 서비스

- 매니지드 서비스

- 전략적 자문서비스

제11장 SaaS 관리 시장 : 전개 모드별

- 서문

- 클라우드

- 온프레미스

- 하이브리드

제12장 SaaS 관리 시장 : 업무 기능별

- 서문

- IT자산관리

- 재무 및 회계

- 보안, 리스크 및 컴플라이언스

- 법무 및 조달

- 인사

- 마케팅 및 영업 업무

제13장 SaaS 관리 시장 : 산업별

- 서문

- BFSI

- 기술 및 소프트웨어

- 의료 및 생명과학

- 제조 및 산업용 IoT

- 소매 및 전자상거래

- 통신

- 정부 및 공공 부문

- 교육

- 에너지 및 유틸리티

- 미디어 및 엔터테인먼트

- 수송 및 물류

- 기타 산업

제14장 SaaS 관리 시장 : 지역별

- 서문

- 북미

- 북미의 SaaS 관리 시장 성장 촉진요인

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 SaaS 관리 시장 성장 촉진요인

- 유럽의 거시 경제 전망

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 아시아태평양의 SaaS 관리 시장 성장 촉진요인

- 아시아태평양의 거시 경제 전망

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동 및 아프리카의 SaaS 관리 시장 성장 촉진요인

- 중동 및 아프리카의 거시 경제 전망

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 카타르

- 기타 중동 및 아프리카

- 라틴아메리카

- 라틴아메리카의 SaaS 관리 시장 성장 촉진요인

- 라틴아메리카의 거시 경제 전망

- 브라질

- 멕시코

- 기타 라틴아메리카

제15장 경쟁 구도

- 개요

- 주요 참가 기업의 전략(2020-2025년)

- 수익 분석(2020-2024년)

- 시장 점유율 분석(2024년)

- 제품의 비교 분석

- 제품의 비교 분석 : SaaS 디스커버리 및 인벤토리별

- 제품의 비교 분석 : SaaS 갱신 및 지출 관리별

- 제품의 비교 분석 : SaaS 라이선스 관리별

- 기업 평가 매트릭스 : 주요 기업

- 기업 평가 매트릭스 : 스타트업 기업 및 중소기업

- 기업 평가 및 재무 지표

- 경쟁 시나리오

제16장 기업 프로파일

- 서문

- 주요 기업

- IBM

- CHECK POINT SOFTWARE

- AVEPOINT

- FLEXERA

- QUEST SOFTWARE

- SAILPOINT TECHNOLOGIES

- HCLSOFTWARE

- SERVICENOW

- FRESHWORKS

- CALERO

- MANAGEENGINE(ZOHO)

- USU SOLUTIONS

- RAMP

- AXONIUS

- 스타트업 및 중소기업

- APPLOGIE

- BETTERCLOUD

- CLEDARA

- ACTIVTRAK

- ZLURI

- ZYLO

- TORII

- LUMOS

- SUBSTLY

- TRELICA(1PASSWORD)

- JOSYS

- CLOUDEAGLE.AI

- LICENCEONE

- AMPLIPHAE

- PRODUCTIV

- BEAMY.IO

- SPENDFLO

- JUMPCLOUD

- PATRONUM

- VENDR

- SASTRIFY

- SETYL

- CERTERO

- KEEPIT

- GOGENUITY

- AUGMENTT

- TROPIC

- AUVIK

- VIIO

- CLOUDNURO

제17장 인접 시장과 관련 시장

- 서문

- AI 서비스 시장-세계 예측(-2030년)

- 시장 정의

- 시장 개요

제18장 부록

AJY 25.12.17The global SaaS management market size is projected to grow from USD 4.58 billion in 2025 to USD 9.37 billion by 2030, at a CAGR of 15.4%. The growing adoption of hybrid and multi-cloud architectures is accelerating the need for centralized SaaS management as enterprises operate applications across AWS, Microsoft Azure, Google Cloud, and on-premise systems. This distributed environment creates operational fragmentation, making it difficult for IT, security, and procurement teams to track license ownership, manage data flows, enforce access control, and maintain consistent compliance.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | USD Million/Billion |

| Segments | Platform, Deployment Mode, Business Function, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America |

As cloud-native services merge with large SaaS portfolios, organizations require unified visibility into usage, spending, integration patterns, and policy adherence across heterogeneous environments. Managing these interconnected ecosystems effectively is driving the adoption of SaaS management platforms that deliver cross-cloud observability, standardized governance workflows, and consolidated policy enforcement across all deployment models.

Vendors are responding by integrating multi-cloud discovery, automated configuration oversight, security monitoring, workflow orchestration, and integration mapping into SaaS management solutions. Platforms such as Torii, Productiv, and BetterCloud provide organizations with a single control layer that consolidates usage analytics, access governance, and application lifecycle management across hybrid environments. These tools support the identification of unsanctioned applications, streamline user provisioning, and automate compliance workflows, improving operational consistency and reducing risk. With hybrid and multi-cloud strategies becoming foundational to enterprise IT, centralized SaaS governance frameworks are emerging as essential for optimizing application performance, safeguarding data integrity, and managing software costs across increasingly complex cloud ecosystems.

"SaaS security and governance to witness high growth as enterprises prioritize protection and compliance."

SaaS security and governance solutions represent the fastest-growing segment of the SaaS management market as enterprises intensify their focus on securing cloud-based application ecosystems, enforcing compliance, and mitigating operational and access-related risks. Organizations increasingly adopt these solutions to gain real-time visibility into data flows, user permissions, configuration settings, and policy violations across distributed SaaS environments. These platforms support automated access reviews, secure configuration baselines, continuous monitoring, threat detection, and unified policy enforcement, which help enterprises address shadow IT exposure, unauthorized integrations, and privacy risks. The segment's rapid momentum is further strengthened by the rising complexity of identity sprawl, cross-application data movement, and regulatory obligations across global markets.

Growth is also supported by the integration of advanced technologies that improve the precision and scalability of governance workflows. Vendors are embedding AI-driven anomaly detection, automated compliance assessments, behavioral analytics, and context-aware alerts to help enterprises reduce manual oversight and enforce consistent security standards. As SaaS portfolios expand, organizations demand solutions that provide consolidated control across multi-tenant environments, ensure adherence to data protection frameworks, and support audit-ready reporting. The strong push toward zero-trust models, secure access governance, and proactive risk mitigation positions SaaS security and governance as the most dynamic and strategically essential segment shaping the future of SaaS management.

"By business function, IT asset management dominates the SaaS management market as enterprises prioritize visibility, governance, and optimization."

IT asset management holds the largest share of the SaaS management market as enterprises place a stronger emphasis on centralized visibility, lifecycle control, and policy-aligned utilization of cloud applications. Organizations rely on IT asset management platforms to maintain a unified system of record for SaaS usage, entitlements, user activity, and compliance posture across distributed environments. These platforms support automated discovery, continuous inventory enrichment, role-based access control monitoring, and contract alignment, which helps enterprises eliminate unused licenses, prevent unauthorized tool adoption, and maintain consistent governance. The segment's leadership is reinforced by growing demand for accurate entitlement mapping, streamlined renewal workflows, and standardized software provisioning.

The segment continues to expand as global organizations adopt mature operating models for SaaS oversight, focusing on cost optimization, compliance readiness, and operational consistency. Vendors are integrating AI-enabled insights, predictive license intelligence, automated policy enforcement, and granular utilization analytics to help enterprises reduce manual tracking and optimize application portfolios. The increasing complexity in hybrid and multi-SaaS environments, combined with the need for audit-ready documentation and risk-aware decision-making, underscores the strategic importance of IT asset management within digital enterprises. As organizations scale SaaS adoption, this segment remains the backbone for control, efficiency, and long-term application governance.

"North America is expected to account for the largest market share in 2025, and the Asia Pacific is slated to register the highest CAGR during the forecast period."

North America is expected to maintain the largest share of the SaaS management market in 2025, led by the US with significant contributions from Canada. The region's dominance is driven by the enterprise-wide adoption of SaaS management platforms, which enable centralized visibility, automated license optimization, policy-based access governance, and compliance enforcement. Key sectors, including technology, BFSI, healthcare, and government, are driving adoption as organizations seek real-time insights into application usage, shadow-IT discovery, cost rationalization, and multi-cloud portfolio optimization. Leading vendors, including IBM, ServiceNow, Flexera, and SailPoint, are integrating AI-driven spend analytics, automated renewal workflows, and identity governance into their platforms, thereby enhancing operational efficiency and risk management. North America also benefits from advanced cloud infrastructure, mature digital workplace initiatives, and a strong ecosystem of system integrators, managed service providers, and advisory partners. Ongoing investments in AI-enabled automation, multi-tenant orchestration, and FinOps-aligned governance are reinforcing the region's position as the core hub for SaaS management innovation and enterprise-scale deployment.

The Asia Pacific region is emerging as the fastest-growing market for SaaS management, driven by accelerated cloud adoption, the expansion of digital-first enterprises, and an increasing emphasis on software governance and cost efficiency. In China, vendors such as Kingdee are enhancing their SaaS management capabilities to support organizations seeking greater visibility and control over subscription usage within rapidly evolving cloud ecosystems. India is also witnessing strong momentum, supported by platforms like ManageEngine's SaaS Manager Plus, which enables enterprises to streamline application provisioning, optimize license utilization, and strengthen security across distributed environments. In Japan, adoption is rising as businesses prioritize compliance, operational efficiency, and the effective management of multi-vendor SaaS portfolios. Across these markets, growing enterprise technology investments, maturing cloud strategies, and the need to reduce software redundancies are contributing to the Asia Pacific's expanding role in shaping global SaaS management adoption.

Breakdown of Primaries

In-depth interviews were conducted with chief executive officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the SaaS management market.

- By Company: Tier I - 31%, Tier II - 42%, and Tier III - 27%

- By Designation: Directors - 29%, Managers - 44%, and Others - 27%

- By Region: North America - 40%, Europe - 22%, Asia Pacific - 26%, Middle East & Africa - 5%, and Latin America - 7%

The report includes the study and in-depth company profiles of key players offering SaaS management solutions and services. The major players in the SaaS management market IBM (US), Check Point Software (Israel), AvePoint (US), Flexera (US), Quest Software (US), SailPoint Technologies (US), HCLSoftware (India), ServiceNow (US), Freshworks (US), Microsoft (US), Google (US), Calero (US), ManageEngine (US), USU Solutions (Germany), Ramp (US), Axonius (US), Applogie (US), BetterCloud (US), Cledara (UK), ActivTrak (US), Zluri (US), Zylo (US), Torii (US), Lumos (US), Substly (Sweden), Trelica (1Password) (England), Josys (Japan), CloudEagle.ai (US), LicenceOne (France), Ampliphae (Ireland), Productiv (US), Beamy.io (France), Spendflo (US), JumpCloud (US), Patronum (UK), Vendr (US), Sastrify (Germany), Setyl (UK), Certero (UK), Keepit (Denmark), GoGenuity (US), Augmentt (Canada), Tropic (US), Auvik (Canada), Viio (Matrix42) (Denmark), and CloudNuro (US).

Research Coverage

This research report categorizes the SaaS management market by offering, deployment mode, business function, and vertical. The offering segment is split into platform and services. The platform segment is further split into SaaS discovery & inventory, SaaS license management, SaaS renewal & spend management, SaaS security & governance, and SaaS automation & analytics. The services segment comprises professional services, managed services, and strategic advisory services. Professional services are further split into training & advisory, implementation & integration, and support & maintenance. The deployment mode segment is divided into cloud, on-premises, and hybrid. The business function segments include IT asset management, finance & accounting, security, risk, & compliance, legal & procurement, HR, and marketing & sales operations. The vertical segment includes BFSI, technology & software, healthcare & life sciences, manufacturing & industrial IoT, retail & E-commerce, telecommunications, government & public sector, education, energy & utilities, media & entertainment, transportation & logistics, real estate & construction, and other verticals (travel & hospitality, non-profit & NGOs, professional service providers, agriculture & AgTech, automotive (non-manufacturing), and aerospace & defense (non-government)). The regional analysis of the market covers North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

The report's scope encompasses detailed information on the major factors, including drivers, restraints, challenges, and opportunities, that influence the growth of the SaaS management market. A detailed analysis of key industry players has been conducted to provide insights into their business overview, solutions, and services, as well as key strategies, contracts, partnerships, agreements, product & service launches, mergers and acquisitions, and recent developments associated with the SaaS management market. This report provides a competitive analysis of emerging startups in the SaaS management market ecosystem.

Key Benefits of Buying the Report

The report will provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall SaaS management market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (AI-powered telemetry enhances SaaS license optimization and spend efficiency, evolving SaaS pricing models accelerate adoption of intelligent monitoring systems, and cross-cloud complexity accelerates adoption of centralized SaaS management), restraints (fragmented hybrid environments and legacy integration silos hindering unified SaaS lifecycle control and performance bottlenecks in distributed SaaS data streams constrain analytics capabilities), opportunities (leveraging analytics for real-time FinOps dashboarding and cross-tool optimization and no-code workflow automation strengthens enterprise adoption and operational flexibility and predictive AI models advance renewal planning and anomaly detection across SaaS portfolios), and challenges (shadow SaaS usage creates gaps in compliance and lifecycle transparency and Fragmented policies and limited automation scalability undermine governance consistency).

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the SaaS management market.

Market Development: Comprehensive information about lucrative markets - analysis of the SaaS management market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the SaaS management market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of IBM (US), Check Point Software (Israel), AvePoint (US), Flexera (US), Quest Software (US), SailPoint Technologies (US), HCLSoftware (India), ServiceNow (US), Freshworks (US), Microsoft (US), Google (US), Calero (US), ManageEngine (US), USU Solutions (Germany), Ramp (US), Axonius (US), Applogie (US), BetterCloud (US), Cledara (UK), ActivTrak (US), Zluri (US), Zylo (US), Torii (US), Lumos (US), Substly (Sweden), Trelica (1Password) (England), Josys (Japan), CloudEagle.ai (US), LicenceOne (France), Ampliphae (Ireland), Productiv (US), Beamy.io (France), Spendflo (US), JumpCloud (US), Patronum (UK), Vendr (US), Sastrify (Germany), Setyl (UK), Certero (UK), Keepit (Denmark), GoGenuity (US), Augmentt (Canada), Tropic (US), Auvik (Canada), Viio (Matrix42) (Denmark), and CloudNuro (US), among others, in the SaaS management market. The report also helps stakeholders understand the pulse of the SaaS management market, providing them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primary profiles

- 2.1.2.2 Key industry insights

- 2.2 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 STUDY LIMITATIONS

3 EXECUTIVE SUMMARY

- 3.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 3.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 3.3 DISRUPTIVE TRENDS SHAPING SAAS MANAGEMENT MARKET

- 3.4 HIGH-GROWTH SEGMENTS

- 3.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SAAS MANAGEMENT MARKET

- 4.2 SAAS MANAGEMENT MARKET: TOP PLATFORM TYPES

- 4.3 NORTH AMERICA: SAAS MANAGEMENT MARKET, BY TOP PLATFORM TYPES AND BUSINESS FUNCTIONS

- 4.4 SAAS MANAGEMENT MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 AI-powered telemetry enhances SaaS license optimization and spend efficiency

- 5.2.1.2 Evolving SaaS pricing models accelerate adoption of intelligent monitoring systems

- 5.2.1.3 Cross-cloud complexity accelerates adoption of centralized SaaS management

- 5.2.2 RESTRAINTS

- 5.2.2.1 Fragmented hybrid environments and legacy integration silos hindering unified SaaS lifecycle control

- 5.2.2.2 Performance bottlenecks in distributed SaaS data streams constrain analytics capabilities

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Leveraging analytics for real-time FinOps dashboarding and cross-tool optimization

- 5.2.3.2 No-code workflow automation strengthens enterprise adoption and operational flexibility

- 5.2.3.3 Predictive AI models advance renewal planning and anomaly detection across SaaS portfolios

- 5.2.4 CHALLENGES

- 5.2.4.1 Shadow SaaS usage creates gaps in compliance and lifecycle transparency

- 5.2.4.2 Fragmented policies and limited automation scalability undermine governance consistency

- 5.2.1 DRIVERS

- 5.3 UNMET NEEDS AND WHITE SPACES

- 5.3.1 UNMET NEEDS IN SAAS MANAGEMENT MARKET

- 5.3.2 WHITE SPACE OPPORTUNITIES

- 5.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 5.4.1 INTERCONNECTED MARKETS

- 5.4.2 CROSS-SECTOR OPPORTUNITIES

- 5.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 5.5.1 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

6 INDUSTRY TRENDS

- 6.1 EVOLUTION OF SAAS MANAGEMENT

- 6.2 PORTER'S FIVE FORCES ANALYSIS

- 6.2.1 THREAT OF NEW ENTRANTS

- 6.2.2 THREAT OF SUBSTITUTES

- 6.2.3 BARGAINING POWER OF SUPPLIERS

- 6.2.4 BARGAINING POWER OF BUYERS

- 6.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.3 SUPPLY CHAIN ANALYSIS

- 6.4 ECOSYSTEM ANALYSIS

- 6.4.1 SAAS DISCOVERY AND INVENTORY PROVIDERS

- 6.4.2 SAAS LICENSE MANAGEMENT PROVIDERS

- 6.4.3 SAAS RENEWAL AND SPEND MANAGEMENT PROVIDERS

- 6.4.4 SAAS SECURITY AND GOVERNANCE PROVIDERS

- 6.4.5 SAAS AUTOMATION & ANALYTICS

- 6.5 PRICING ANALYSIS

- 6.5.1 AVERAGE SELLING PRICE OF SAAS MANAGEMENT OFFERINGS, BY KEY PLAYER, 2025

- 6.5.2 AVERAGE SELLING PRICE OF SAAS MANAGEMENT PLATFORMS, BY BUSINESS FUNCTION, 2025

- 6.6 KEY CONFERENCES AND EVENTS, 2025-2026

- 6.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.8 INVESTMENT AND FUNDING SCENARIO

- 6.9 CASE STUDY ANALYSIS

- 6.9.1 U, INC. OPTIMIZED SAAS SPEND AND SUBSCRIPTION MANAGEMENT WITH APPLOGIE

- 6.9.2 PIE INSURANCE SIMPLIFIES SAAS OPERATIONS AND ACCESS MANAGEMENT WITH BETTERCLOUD

- 6.9.3 JIMINNY GAINS CENTRALIZED SAAS VISIBILITY AND SPEND CONTROL WITH CLEDARA

- 6.9.4 INSTRUCTURE GAINS COMPLETE SAAS VISIBILITY AND OPERATIONAL EFFICIENCY WITH ZYLO

- 6.9.5 DATASTAX OPTIMIZES SAAS RENEWALS AND PROCUREMENT MANAGEMENT WITH CLOUDEAGLE.AI

- 6.10 IMPACT OF 2025 US TARIFF - SAAS MANAGEMENT MARKET

- 6.10.1 INTRODUCTION

- 6.10.2 TARIFF/TRADE POLICY UPDATES (AUGUST-SEPTEMBER 2025)

- 6.10.3 KEY TARIFF RATES

- 6.10.4 PRICE IMPACT ANALYSIS

- 6.10.4.1 Strategic shifts and emerging trends

- 6.10.5 IMPACT ON COUNTRY/REGION

- 6.10.5.1 US

- 6.10.5.2 China

- 6.10.5.3 Europe

- 6.10.5.4 Asia Pacific (Excluding China)

- 6.10.6 IMPACT ON END-USE INDUSTRIES

- 6.10.6.1 BFSI

- 6.10.6.2 Retail & E-commerce

- 6.10.6.3 Healthcare & life sciences

- 6.10.6.4 Technology & Software

7 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 7.1 KEY EMERGING TECHNOLOGIES

- 7.1.1 SAAS DISCOVERY CONNECTORS

- 7.1.2 UNIFIED APP-INVENTORY GRAPH & DATA NORMALIZATION LAYER

- 7.1.3 USAGE TELEMETRY PIPELINES & LICENSE UTILIZATION ANALYTICS

- 7.1.4 IDENTITY LIFECYCLE AUTOMATION (JML) VIA SCIM/JIT

- 7.1.5 ACCESS GOVERNANCE (RBAC/ABAC) & PERIODIC ACCESS ATTESTATIONS

- 7.1.6 CONTRACT INTELLIGENCE

- 7.1.7 FINOPS SPEND ANALYTICS

- 7.2 COMPLEMENTARY TECHNOLOGIES

- 7.2.1 IDENTITY PROVIDERS & DIRECTORY TECH

- 7.2.2 ITSM PLATFORMS & CHANGE WORKFLOWS

- 7.2.3 ERP/FINANCE & AP SYSTEMS

- 7.2.4 E-SIGNATURE SERVICES

- 7.2.5 IPAAS & WORKFLOW BRIDGES

- 7.2.6 DATA PIPELINES & WAREHOUSING

- 7.2.7 SIEM/LOG MANAGEMENT

- 7.2.8 SECRETS MANAGEMENT & VAULTING

- 7.3 ADJACENT TECHNOLOGIES

- 7.3.1 IGA/IAM SUITES

- 7.3.2 PRIVILEGED ACCESS MANAGEMENT

- 7.3.3 TRADITIONAL ITAM/SAM SUITES

- 7.3.4 BROWSER SECURITY PLATFORMS (BSP) & ENTERPRISE BROWSER TECH

- 7.3.5 DIGITAL EMPLOYEE EXPERIENCE ANALYTICS

- 7.4 TECHNOLOGY ROADMAP

- 7.4.1 SHORT TERM (2025-2027): FOUNDATION AND STANDARDIZATION PHASE

- 7.4.2 MID TERM (2028-2030): CONVERGENCE AND AUTOMATION PHASE

- 7.4.3 LONG TERM (2031-2035): AUTONOMOUS AND COGNITIVE SAAS MANAGEMENT PHASE

- 7.5 PATENT ANALYSIS

- 7.5.1 METHODOLOGY

- 7.5.2 PATENTS FILED, BY DOCUMENT TYPE, 2016-2025

- 7.5.3 INNOVATION AND PATENT APPLICATIONS

- 7.6 FUTURE APPLICATIONS

- 7.6.1 ZERO-TOUCH SAAS ECOSYSTEM MANAGEMENT: SELF-LEARNING ORCHESTRATION ENGINES

- 7.6.2 SAAS SPEND FORECASTING AND ADAPTIVE BUDGETING: DYNAMIC COST-MODELLING ALGORITHMS

- 7.6.3 SAAS INTEROPERABILITY AND UNIFIED GOVERNANCE FABRIC: CROSS-PLATFORM GOVERNANCE PROTOCOLS

- 7.6.4 DYNAMIC COMPLIANCE AND CONTINUOUS AUDIT AUTOMATION: AI-LED POLICY VALIDATION

- 7.6.5 SAAS CARBON ACCOUNTING AND SUSTAINABLE IT OPTIMIZATION: SAAS USAGE DATA WITH ENERGY, CARBON, AND ESG DATASETS

- 7.7 IMPACT OF GENERATIVE AI ON SAAS MANAGEMENT MARKET

- 7.7.1 SAAS DISCOVERY AND APPLICATION INTELLIGENCE

- 7.7.2 LICENSE OPTIMIZATION AND SPEND INTELLIGENCE

- 7.7.3 CONTRACT LIFECYCLE AND RENEWAL MANAGEMENT

- 7.7.4 PREDICTIVE ANALYTICS AND INSIGHT GENERATION

- 7.7.5 AUTOMATED COMPLIANCE AND RISK GOVERNANCE

- 7.7.6 ADAPTIVE WORKFLOW AUTOMATION AND USER ENABLEMENT

8 REGULATORY LANDSCAPE

- 8.1 REGIONAL REGULATIONS AND COMPLIANCE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 KEY REGULATIONS

- 8.1.2.1 North America

- 8.1.2.1.1 Federal Risk and Authorization Management Program (FedRAMP) (US)

- 8.1.2.1.2 Sarbanes-Oxley Act (SOX) (US)

- 8.1.2.1.3 Health Insurance Portability and Accountability Act (HIPAA) (US)

- 8.1.2.1.4 Personal Information Protection and Electronic Documents Act (PIPEDA) - (Canada)

- 8.1.2.2 Europe

- 8.1.2.2.1 General Data Protection Regulation (GDPR) (European Union)

- 8.1.2.2.2 Network and Information Systems Directive 2 (NIS2) (European Union)

- 8.1.2.2.3 Digital Operational Resilience Act (DORA) (European Union)

- 8.1.2.2.4 ePrivacy Directive (Directive 2002/58/EC) (European Union)

- 8.1.2.2.5 Artificial Intelligence Act (AI Act) (European Union)

- 8.1.2.3 Asia Pacific

- 8.1.2.3.1 Personal Information Protection Law (PIPL) (China)

- 8.1.2.3.2 Act on the Protection of Personal Information (APPI) (Japan)

- 8.1.2.3.3 Digital Personal Data Protection/Digital Personal Data Protection Act (DPDP/DPDPA) (India)

- 8.1.2.3.4 Personal Information Protection Act (PIPA) (South Korea)

- 8.1.2.3.5 Privacy Act 1988 and Notifiable Data Breaches (NDB) Scheme; APRA CPS 234 (Australia)

- 8.1.2.3.6 Personal Data Protection Act (PDPA) (Singapore)

- 8.1.2.4 Middle East & Africa

- 8.1.2.4.1 Personal Data Protection Law (PDPL) (Saudi Arabia)

- 8.1.2.4.2 Federal Decree-Law No. 45 of 2021 on Personal Data Protection (UAE)

- 8.1.2.4.3 Protection of Personal Information Act (POPIA) (South Africa)

- 8.1.2.4.4 Law on the Protection of Personal Data (KVKK) (Turkey)

- 8.1.2.4.5 Protection of Privacy Law (Amendment 13) (Israel)

- 8.1.2.5 Latin America

- 8.1.2.5.1 Brazilian General Data Protection Law (LGPD) (Brazil)

- 8.1.2.5.2 Central Bank and Financial Sector Cloud Outsourcing Rules (CMN Resolution No. 4,893 and BCB Resolution No. 85) (Brazil)

- 8.1.2.5.3 Federal Law on the Protection of Personal Data Held by Private Parties (LFPDPPP) (Mexico)

- 8.1.2.5.4 Personal Data Protection Framework (PDPA) (Argentina)

- 8.1.2.1 North America

9 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 9.1 DECISION-MAKING PROCESS

- 9.2 KEY STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 9.2.1 BUYING CRITERIA

- 9.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 9.4 UNMET NEEDS FROM VARIOUS INDUSTRY VERTICALS

10 SAAS MANAGEMENT MARKET, BY OFFERING

- 10.1 INTRODUCTION

- 10.1.1 DRIVERS: SAAS MANAGEMENT MARKET, BY OFFERING

- 10.2 PLATFORMS

- 10.2.1 SAAS DISCOVERY & INVENTORY

- 10.2.1.1 Supports optimization initiatives by highlighting redundant tools, underutilized applications, and overlapping functionalities

- 10.2.1.2 App discovery tools

- 10.2.1.3 App ownership mapping software

- 10.2.1.4 Data normalization engine

- 10.2.1.5 SaaS catalog/directory tools

- 10.2.1.6 Other SaaS discovery & inventory platforms

- 10.2.2 SAAS LICENSE MANAGEMENT

- 10.2.2.1 Critical role in financial optimization and compliance to drive market

- 10.2.2.2 License utilization tracking & entitlement management

- 10.2.2.3 Automated provisioning/deprovisioning

- 10.2.2.4 License optimization engine

- 10.2.2.5 Chargeback/Showback & seat rationalization module

- 10.2.3 SAAS RENEWAL & SPEND MANAGEMENT

- 10.2.3.1 Enhance strategic decision-making by enabling organizations to negotiate from position of strength

- 10.2.3.2 Renewal calendar, alerts, & contract repository

- 10.2.3.3 Vendor performance dashboard

- 10.2.3.4 Spend analytics/FinOps integration & approval workflows

- 10.2.3.5 Benchmarking & pricing intelligence

- 10.2.3.6 Vendor & contract negotiation tools

- 10.2.3.7 Others

- 10.2.4 SAAS SECURITY & GOVERNANCE

- 10.2.4.1 Advancing organizational security with unified policy enforcement

- 10.2.4.2 Access governance, role mapping, & policy compliance engine

- 10.2.4.3 Audit, attestation, & risk scoring reports

- 10.2.4.4 Identity lifecycle integration tools

- 10.2.4.5 Data classification & compliance dashboard

- 10.2.4.6 SaaS security posture management

- 10.2.5 SAAS AUTOMATION & ANALYTICS

- 10.2.5.1 Rising use of Gen AI and LLMs requiring ontology-based contextual tagging for grounding and accuracy to drive market

- 10.2.5.2 Predictive renewal & spend forecasting

- 10.2.5.3 Autonomous workflow automation

- 10.2.5.4 Personalized usage recommendations

- 10.2.5.5 Anomaly detection

- 10.2.1 SAAS DISCOVERY & INVENTORY

- 10.3 SERVICES

- 10.3.1 PROFESSIONAL SERVICES

- 10.3.1.1 Help enterprises successfully deploy, operationalize, and maximize value from SaaS management platforms

- 10.3.1.2 Training & advisory

- 10.3.1.3 Implementation & integration

- 10.3.1.4 Support & maintenance

- 10.3.2 MANAGED SERVICES

- 10.3.2.1 Deliver continuous, outsourced operational support to help enterprises oversee, optimize, and govern SaaS application portfolios

- 10.3.3 STRATEGIC ADVISORY SERVICES

- 10.3.3.1 Help organizations establish structured decision-making models

- 10.3.1 PROFESSIONAL SERVICES

11 SAAS MANAGEMENT MARKET, BY DEPLOYMENT MODE

- 11.1 INTRODUCTION

- 11.1.1 DEPLOYMENT MODE: SAAS MANAGEMENT MARKET DRIVERS

- 11.2 CLOUD

- 11.2.1 DEMAND FOR FLEXIBILITY, SCALABILITY, AND COST EFFICIENCY IN MANAGING SAAS APPLICATIONS TO DRIVE MARKET

- 11.3 ON-PREMISES

- 11.3.1 NEED FOR COMPLETE CONTROL OVER SENSITIVE INFORMATION, SECURE STORAGE, AND INTERNAL POLICY ENFORCEMENT TO DRIVE ADOPTION

- 11.4 HYBRID

- 11.4.1 GROWING NEED FOR ADAPTABLE IT STRATEGIES, MULTI-CLOUD ADOPTION, AND SECURE HANDLING OF SENSITIVE DATA TO SUPPORT MARKET GROWTH

12 SAAS MANAGEMENT MARKET, BY BUSINESS FUNCTION

- 12.1 INTRODUCTION

- 12.1.1 BUSINESS FUNCTION: SAAS MANAGEMENT MARKET DRIVERS

- 12.2 IT ASSET MANAGEMENT

- 12.2.1 ENABLES ENTERPRISES MAINTAIN VISIBILITY, CONTROL, AND ACCOUNTABILITY OVER EXPANDING SAAS ECOSYSTEMS

- 12.3 FINANCE & ACCOUNTING

- 12.3.1 NEED FOR FINANCIAL TRANSPARENCY, COST EFFICIENCY, AND ACCOUNTABILITY TO DRIVE ADOPTION

- 12.4 SECURITY, RISK & COMPLIANCE

- 12.4.1 RISING CYBERSECURITY THREATS AND OPERATIONAL RISKS TO DRIVE MARKET

- 12.5 LEGAL & PROCUREMENT

- 12.5.1 GROWING ADOPTION OF SUBSCRIPTION-BASED AND USAGE-BASED SAAS MODELS TO DRIVE DEMAND

- 12.6 HR

- 12.6.1 OPTIMIZING EMPLOYEE ONBOARDING AND SAAS UTILIZATION FOR OPERATIONAL EFFICIENCY

- 12.7 MARKETING & SALES OPERATIONS

- 12.7.1 GROWING RELIANCE ON DATA-DRIVEN STRATEGIES AND MULTI-CHANNEL CAMPAIGNS TO DRIVE ADOPTION

13 SAAS MANAGEMENT MARKET, BY VERTICAL

- 13.1 INTRODUCTION

- 13.1.1 DRIVERS: SAAS MANAGEMENT MARKET, BY VERTICAL

- 13.2 BFSI

- 13.2.1 TECHNOLOGY MODERNIZATION AND GOVERNANCE ALIGNMENT STRENGTHEN DIGITAL RESILIENCE IN REGULATED INDUSTRIES

- 13.3 TECHNOLOGY & SOFTWARE

- 13.3.1 EVOLVING DEVELOPMENT FRAMEWORKS ACCELERATE NEED FOR CENTRALIZED SAAS VISIBILITY

- 13.4 HEALTHCARE & LIFE SCIENCES

- 13.4.1 DIGITAL HEALTH TRANSFORMATION SPURS DEMAND FOR CENTRALIZED APPLICATION CONTROL

- 13.5 MANUFACTURING & INDUSTRIAL IOT

- 13.5.1 DIGITAL INDUSTRIALIZATION AND SMART FACTORY EXPANSION ACCELERATE SAAS GOVERNANCE ADOPTION

- 13.6 RETAIL & E-COMMERCE

- 13.6.1 EXPANDING DIGITAL COMMERCE ECOSYSTEMS REINFORCE NEED FOR UNIFIED SAAS GOVERNANCE AND EFFICIENCY

- 13.7 TELECOMMUNICATIONS

- 13.7.1 RISING CLOUD INTEGRATION DEMANDS UNIFIED MANAGEMENT AND OPERATIONAL INTELLIGENCE

- 13.8 GOVERNMENT & PUBLIC SECTOR

- 13.8.1 EVOLVING DATA SECURITY PRIORITIES ACCELERATE SHIFT TOWARD CENTRALIZED CLOUD OVERSIGHT

- 13.9 EDUCATION

- 13.9.1 EDUCATION SYSTEMS ADVANCE TOWARD SMARTER, COMPLIANT, AND COST-EFFICIENT SAAS ECOSYSTEMS

- 13.10 ENERGY & UTILITIES

- 13.10.1 RISING ENERGY MODERNIZATION EFFORTS DRIVE DEMAND FOR SECURE AND COMPLIANT SAAS ECOSYSTEMS

- 13.11 MEDIA & ENTERTAINMENT

- 13.11.1 EVOLVING CONTENT ECOSYSTEMS DEMAND GREATER TRANSPARENCY AND EFFICIENCY IN CLOUD WORKFLOWS

- 13.12 TRANSPORTATION & LOGISTICS

- 13.12.1 EVOLVING MOBILITY NETWORKS ACCELERATE DEMAND FOR UNIFIED SAAS OVERSIGHT AND COST OPTIMIZATION

- 13.13 OTHER VERTICALS

14 SAAS MANAGEMENT MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 NORTH AMERICA: SAAS MANAGEMENT MARKET DRIVERS

- 14.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 14.2.3 US

- 14.2.3.1 Rising SaaS subscription spending to drive market

- 14.2.4 CANADA

- 14.2.4.1 Rising adoption of SaaS across business functions to propel market

- 14.3 EUROPE

- 14.3.1 EUROPE: SAAS MANAGEMENT MARKET DRIVERS

- 14.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 14.3.3 UK

- 14.3.3.1 Growing emphasis on automation, integration, and data-driven decision-making to drive market

- 14.3.4 GERMANY

- 14.3.4.1 Emphasis on digital industrialization to drive market

- 14.3.5 FRANCE

- 14.3.5.1 Regulatory compliance and national cloud policies to drive market

- 14.3.6 ITALY

- 14.3.6.1 Accelerating cloud-first adoption through advanced SaaS governance and compliance controls to drive market

- 14.3.7 REST OF EUROPE

- 14.4 ASIA PACIFIC

- 14.4.1 ASIA PACIFIC: SAAS MANAGEMENT MARKET DRIVERS

- 14.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 14.4.3 CHINA

- 14.4.3.1 Large-scale digitalization and cloud-first modernization initiatives to drive market

- 14.4.4 INDIA

- 14.4.4.1 Enterprise modernization and regulatory alignment to drive SaaS optimization efforts

- 14.4.5 JAPAN

- 14.4.5.1 Government initiatives to support market growth

- 14.4.6 SOUTH KOREA

- 14.4.6.1 Strategic investments and consolidation in SaaS ecosystem to drive market

- 14.4.7 AUSTRALIA & NEW ZEALAND

- 14.4.7.1 Increasing regulatory requirements and growing complexity of hybrid IT environments to drive market

- 14.4.8 REST OF ASIA PACIFIC

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 MIDDLE EAST & AFRICA: SAAS MANAGEMENT MARKET DRIVERS

- 14.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 14.5.3 SAUDI ARABIA

- 14.5.3.1 Growing digitalization in both public institutions and private enterprises to propel market

- 14.5.4 UAE

- 14.5.4.1 Government focus on cybersecurity compliance to drive market

- 14.5.5 SOUTH AFRICA

- 14.5.5.1 Rapid cloud migration across sectors to drive demand

- 14.5.6 QATAR

- 14.5.6.1 Rising cloud adoption by enterprises and government institutions to drive market

- 14.5.7 REST OF MIDDLE EAST & AFRICA

- 14.6 LATIN AMERICA

- 14.6.1 LATIN AMERICA: SAAS MANAGEMENT MARKET DRIVERS

- 14.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 14.6.3 BRAZIL

- 14.6.3.1 Increasing adoption of hybrid work models and decentralized software procurement to support market growth

- 14.6.4 MEXICO

- 14.6.4.1 Investments in digital infrastructure to drive market

- 14.6.5 REST OF LATIN AMERICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 STRATEGIES ADOPTED BY KEY PLAYERS, 2020-2025

- 15.3 REVENUE ANALYSIS, 2020-2024

- 15.4 MARKET SHARE ANALYSIS, 2024

- 15.4.1 MARKET RANKING ANALYSIS, 2024

- 15.5 PRODUCT COMPARATIVE ANALYSIS

- 15.5.1 PRODUCT COMPARATIVE ANALYSIS, BY SAAS DISCOVERY & INVENTORY

- 15.5.1.1 Zylo (Zylo Platform)

- 15.5.1.2 Torii (Torii SaaS Management Platform)

- 15.5.1.3 Zluri (Zluri SaaS Management)

- 15.5.1.4 BetterCloud (BetterCloud SaaS Management Platform)

- 15.5.1.5 Axonius (Axonius Asset Cloud)

- 15.5.2 PRODUCT COMPARATIVE ANALYSIS, BY SAAS RENEWAL & SPEND MANAGEMENT

- 15.5.2.1 Flexera (Flexera One)

- 15.5.2.2 CloudEagle.ai (CloudEagle.ai SaaS Management)

- 15.5.2.3 Calero (Calero Platform)

- 15.5.2.4 AvePoint (AvePoint Confidence Platform)

- 15.5.2.5 Lumos (SaaS Management)

- 15.5.3 PRODUCT COMPARATIVE ANALYSIS, BY SAAS LICENSE MANAGEMENT

- 15.5.3.1 ServiceNow (SaaS License Management)

- 15.5.3.2 USU Solutions (USU SaaS Management Platform)

- 15.5.3.3 IBM (IBM MQ SaaS)

- 15.5.3.4 SailPoint Technologies (Identity Security Cloud)

- 15.5.3.5 Auvik (Auvik SaaS Management)

- 15.5.1 PRODUCT COMPARATIVE ANALYSIS, BY SAAS DISCOVERY & INVENTORY

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 15.6.5.1 Company footprint

- 15.6.5.2 Region footprint

- 15.6.5.3 Offering footprint

- 15.6.5.4 Deployment mode footprint

- 15.6.5.5 Business function footprint

- 15.6.5.6 Vertical footprint

- 15.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES

- 15.7.1 PROGRESSIVE COMPANIES

- 15.7.2 RESPONSIVE COMPANIES

- 15.7.3 DYNAMIC COMPANIES

- 15.7.4 STARTING BLOCKS

- 15.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 15.7.5.1 Detailed list of key startups/SMEs

- 15.7.5.2 Competitive benchmarking of key startups/SMEs

- 15.8 COMPANY VALUATION AND FINANCIAL METRICS

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 15.9.2 DEALS

16 COMPANY PROFILES

- 16.1 INTRODUCTION

- 16.2 KEY PLAYERS

- 16.2.1 IBM

- 16.2.1.1 Business overview

- 16.2.1.2 Products/Solutions/Services offered

- 16.2.1.3 Recent developments

- 16.2.1.3.1 Product launches and enhancements

- 16.2.1.3.2 Deals

- 16.2.1.4 MnM view

- 16.2.1.4.1 Key strengths

- 16.2.1.4.2 Strategic choices

- 16.2.1.4.3 Weaknesses and competitive threats

- 16.2.2 CHECK POINT SOFTWARE

- 16.2.2.1 Business overview

- 16.2.2.2 Products/Solutions/Services offered

- 16.2.2.3 Recent developments

- 16.2.2.3.1 Product launches and enhancements

- 16.2.2.3.2 Deals

- 16.2.2.4 MnM view

- 16.2.2.4.1 Key strengths

- 16.2.2.4.2 Strategic choices

- 16.2.2.4.3 Weaknesses and competitive threats

- 16.2.3 AVEPOINT

- 16.2.3.1 Business overview

- 16.2.3.2 Products/Solutions/Services offered

- 16.2.3.3 Recent developments

- 16.2.3.3.1 Product launches and enhancements

- 16.2.3.3.2 Deals

- 16.2.3.4 MnM view

- 16.2.3.4.1 Key strengths

- 16.2.3.4.2 Strategic choices

- 16.2.3.4.3 Weaknesses and competitive threats

- 16.2.4 FLEXERA

- 16.2.4.1 Business overview

- 16.2.4.2 Products/Solutions/Services offered

- 16.2.4.3 Recent developments

- 16.2.4.3.1 Product launches and enhancements

- 16.2.4.3.2 Deals

- 16.2.4.4 MnM view

- 16.2.4.4.1 Key strengths

- 16.2.4.4.2 Strategic choices

- 16.2.4.4.3 Weaknesses and competitive threats

- 16.2.5 QUEST SOFTWARE

- 16.2.5.1 Business overview

- 16.2.5.2 Products/Solutions/Services offered

- 16.2.5.3 Recent developments

- 16.2.5.3.1 Product launches and enhancements

- 16.2.5.4 MnM view

- 16.2.5.4.1 Key strengths

- 16.2.5.4.2 Strategic choices

- 16.2.5.4.3 Weaknesses and competitive threats

- 16.2.6 SAILPOINT TECHNOLOGIES

- 16.2.6.1 Business overview

- 16.2.6.2 Products/Solutions/Services offered

- 16.2.6.3 Recent developments

- 16.2.6.3.1 Product launches and enhancements

- 16.2.6.3.2 Deals

- 16.2.7 HCLSOFTWARE

- 16.2.7.1 Business overview

- 16.2.7.2 Products/Solutions/Services offered

- 16.2.7.3 Recent developments

- 16.2.7.3.1 Product launches and enhancements

- 16.2.7.3.2 Deals

- 16.2.8 SERVICENOW

- 16.2.8.1 Business overview

- 16.2.8.2 Products/Solutions/Services offered

- 16.2.8.3 Recent developments

- 16.2.8.3.1 Deals

- 16.2.9 FRESHWORKS

- 16.2.9.1 Business overview

- 16.2.9.2 Products/Solutions/Services offered

- 16.2.9.3 Recent developments

- 16.2.9.3.1 Product launches and enhancements

- 16.2.9.3.2 Deals

- 16.2.10 CALERO

- 16.2.11 MANAGEENGINE (ZOHO)

- 16.2.12 USU SOLUTIONS

- 16.2.13 RAMP

- 16.2.14 AXONIUS

- 16.2.1 IBM

- 16.3 STARTUPS/SMES

- 16.3.1 APPLOGIE

- 16.3.2 BETTERCLOUD

- 16.3.3 CLEDARA

- 16.3.4 ACTIVTRAK

- 16.3.5 ZLURI

- 16.3.6 ZYLO

- 16.3.7 TORII

- 16.3.8 LUMOS

- 16.3.9 SUBSTLY

- 16.3.10 TRELICA (1PASSWORD)

- 16.3.11 JOSYS

- 16.3.12 CLOUDEAGLE.AI

- 16.3.13 LICENCEONE

- 16.3.14 AMPLIPHAE

- 16.3.15 PRODUCTIV

- 16.3.16 BEAMY.IO

- 16.3.17 SPENDFLO

- 16.3.18 JUMPCLOUD

- 16.3.19 PATRONUM

- 16.3.20 VENDR

- 16.3.21 SASTRIFY

- 16.3.22 SETYL

- 16.3.23 CERTERO

- 16.3.24 KEEPIT

- 16.3.25 GOGENUITY

- 16.3.26 AUGMENTT

- 16.3.27 TROPIC

- 16.3.28 AUVIK

- 16.3.29 VIIO

- 16.3.30 CLOUDNURO

17 ADJACENT AND RELATED MARKETS

- 17.1 INTRODUCTION

- 17.2 AI AS A SERVICE MARKET - GLOBAL FORECAST TO 2030

- 17.2.1 MARKET DEFINITION

- 17.2.2 MARKET OVERVIEW

- 17.2.2.1 AI as a service market, by product type

- 17.2.2.2 AI as a service market, by organization size

- 17.2.2.3 AI as a service market, by end user

- 17.2.2.4 AI as a service market, by region

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS