|

시장보고서

상품코드

1883941

물류 및 운송 시장 : 수익별, 화물 운송 방식별, 지역별, 비즈니스 시나리오별, 이용 사례별 - 예측(-2035년)Logistics & Transportation Market by Revenue (Transportation, Inventory, Warehousing, Administrative), Freight Transportation by Mode (Road, Rail, Marine, Air), Region (Europe, US, China, India), Business Scenarios & Use Cases- Global Forecast to 2035 |

||||||

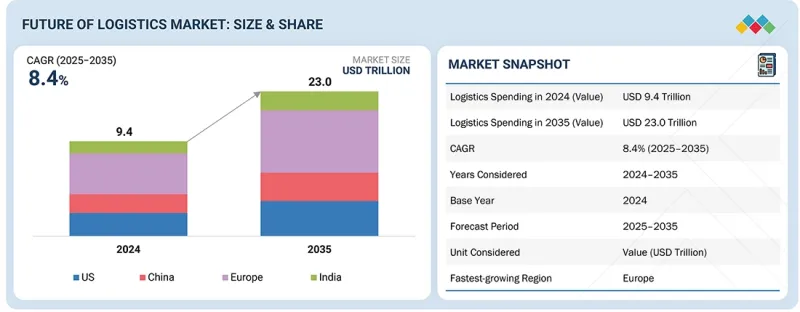

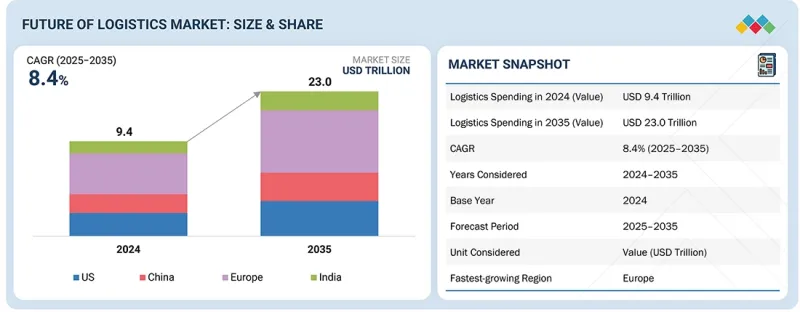

세계의 물류 지출은 2024년 9조 4,000억 달러에서 2035년 23조 달러에 이를 것으로 예측되며, CAGR 8.4%로 성장이 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2035년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2035년 |

| 단위 | 조 달러 |

| 부문 | 수익, 화물 운송 방식, 지역, 비즈니스 시나리오, 이용 사례 |

| 대상 지역 | 북미, 유럽, 중국, 인도 |

물류 및 운송 시장의 성장은 기술 혁신, 세계 무역 확대 및 변화하는 소비자의 기대에 의해 촉진되고 있습니다. AI, IoT, 자동화의 채용이 진행됨에 따라 기업은 경로의 효율화, 재고 절감, 신속하고 확실한 배송 수요에 대응할 수 있습니다. 창고 자동화, 스마트 추적, 고급 분석을 포함한 공급망 업무의 디지털화는 시장의 모든 부문에서 가시성 및 비용 효율성을 향상시킵니다.

2024년 물류 총 지출은 9조 4,000억 달러로 추정되었으며, 그중 도시 물류가 1조 2,000억 달러(전체의 12.5%)를 차지했습니다. 도시 환경 내에서의 효율적인 화물 이동에 특화된 활동인 도시 물류는 기업과 행정이 도시화, 교통 정체, 변화하는 소비자의 기대와 같은 과제를 다루고 있는 가운데 이미 물류 예산의 상당한 비율을 차지하고 있습니다.

디지털 플랫폼, AI, 협동 생태계에 새로운 이용 사례가 등장하고 있으며, 여러 가지 중요한 동향이 업계의 미래를 형성하고 있습니다.

물류 및 운송 시장은 효율성 최적화, 확장성 지원 및 지속가능성 목표 달성을 목표로 한 혁신적인 비즈니스 시나리오에 힘입어 혁신의 최상위에 있습니다. 특히 눈에 띄는 시나리오 중 하나는 5PL 공급자의 상승입니다. 그들은 전체 공급망 네트워크를 관리하고 최적화하며 3PL 및 4PL 서비스의 종합적인 조정 역할을 합니다. 중앙 집중식 관리를 활용한 종합적인 접근 방식은 시장의 획기적인 확대를 이끌 것으로 예측됩니다. 이 시나리오는 세계 물류의 복잡화에 대응하고, 조정과 통합을 경쟁 전략의 최전선에 둡니다.

AI를 활용한 루트 최적화도 중요한 비즈니스 시나리오입니다. 머신러닝과 실시간 데이터를 활용하여 운송 및 배송 경로를 동적으로 최적화하여 자원 이용률을 극대화하고 경영 비용을 절감합니다. AI를 통한 라우팅을 사용하는 조직은 배송 당 최대 30%의 비용 절감이 가능하며, 플릿 관리, 대열 주행, 효율적인 루트 계획에서 AI 기술 투자의 강력한 비즈니스 사례를 명시하고 있습니다. 그 밖의 새로운 동향으로서 탄소 상쇄 물류 플랫폼, 창고 공유 플랫폼, 화물 배달의 우버화, 클라우드 소스 라스트 마일 배송 등이 존재하며, 이들 모두가 업계의 혁신과 성장을 가속하고 있습니다.

중국은 물류 및 운송 시장에서 주도적인 지위를 차지하고 있습니다.

중국 화물 운송 시장의 주요 성장 촉진요인은 디지털 화물 플랫폼 및 AI 기반 경로 최적화의 급속한 발전 등입니다. 이들은 실시간 수용 능력 매칭을 통해 트럭의 가동률을 크게 향상시켜 빈 주행 거리를 줄입니다. 정부 주도의 인프라 개발 사업(도로와 철도의 멀티 모달 통합이나 고속도로망의 확장 등)은 효율적인 장거리 및 월경 트럭 수송을 가능하게 해, 내륙부의 제조업체와 세계적인 현관구를 연결하고 있습니다. 도시 지역의 녹색 회랑에서 경쟁력있는 배터리 전기 트럭과 LNG 트럭의 전개는 지속 가능한 화물 운송을 가속화하고 있습니다. 이것은 신선 식품 및 의약품에 대한 수요 향상에 대응하기 위해 대규모 콜드체인 투자에 의해 지원됩니다. 엄격한 팔레트 표준화 목표와 IoT 기반 추적 시스템은 컨테이너의 보급, 업무 효율성 및 컴플라이언스 추진을 촉진합니다. 전자상거래의 보급은 도시에서의 당일 배송 수요를 더욱 가속화하고 있어 복잡한 재고 관리 및 신속한 풀필먼트의 기대에 부응하기 위해 선진 기술을 이용한 다양한 플릿이 필요합니다.

이 보고서는 세계의 물류 및 운송 시장에 대한 조사 분석을 통해 주요 촉진요인 및 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 물류 산업의 주요 동향

- 전기 트럭이 세계의 화물 수송 독점

- 물류에서 지속 가능한 연료의 상승

- 자율형 화물 네트워크의 혁명

- 분산형 창고가 기세 확장

- 라스트 마일 배송 및 긴급 배송에 있어서 드론의 통합

- 그린 화물로의 전환

- 디지털 화물 중개의 급속한 성장

제4장 물류 산업의 현재 및 미래

- 세계 물류 산업 : 대상 부문

- 세계 물류 지출(GDP비) 및 주요 부문

- 부문 1 : 수송

- 부문 2 : 창고 보관 및 배송

- 부문 3 : 화물 운송

- 부문 4 : 타사 및 포스 파티 물류(3PL/4PL)

- 부문 5 : 디지털 물류

- 부문 6 : 역 물류

- 부문 7 : 특수 물류

- 부문 8 : 부가가치 물류 서비스

- 밸류체인의 진화

제5장 어반 물류의 미래 동향 및 기회

제6장 물류 산업의 주요 촉진요인

- 성장 촉진요인 1 : 로봇 및 자동화

- 성장 촉진요인 2 : 디지털화

- 성장 촉진요인 3 : 니어 쇼어링

- 성장 촉진요인 4 : 탈탄소화

- 성장 촉진요인 5 : 무역 전망 및 관세

- 성장 촉진요인 6 : 기술 혁신

제7장 새로운 비즈니스 시나리오 및 이용 사례

- 피프스파티 로지스틱스(5PL) 프로바이더

- AI에 의한 루트 최적화

- 화물의 우버화

- 창고 공유 플랫폼

- 클라우드 소스 라스트 마일 배송

- 탄소 오프셋 물류 플랫폼

제8장 결론

제9장 부록

AJY 25.12.17The global logistics spending is expected to reach USD 23.0 trillion in 2035, from USD 9.4 trillion in 2024, with a CAGR of 8.4%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2035 |

| Base Year | 2024 |

| Forecast Period | 2025-2035 |

| Units Considered | Value (USD Trillion) |

| Segments | Revenue, Freight Transportation by Mode, Region, Business Scenarios & Use Cases |

| Regions covered | North America, Europe, China, India |

The growth of the logistics and transportation market is being driven by a combination of technological innovation, rising global trade, and evolving consumer expectations. Increasing adoption of AI, IoT, and automation allows companies to streamline routes, reduce inventory, and meet demand for fast, reliable delivery. Digitization of supply chain operations-including warehouse automation, smart tracking, and advanced analytics-is enabling greater visibility and cost efficiency in every segment of the market.

In 2024, total logistics expenditure was estimated at USD 9.4 trillion, with urban logistics accounting for USD 1.2 trillion or 12.5% of this total. Urban logistics, which includes activities dedicated to efficiently moving goods within city environments, is already commanding a considerable share of logistics budgets as businesses and administrations address the challenges posed by urbanization, traffic congestion, and shifting consumer expectations.

Several pivotal trends are shaping the industry's future, with new use cases emerging across digital platforms, AI, and collaborative ecosystems.

The logistics & transportation market is undergoing a transformative shift, fueled by innovative business scenarios designed to optimize efficiency, support scalability, and meet sustainability goals. One prominent scenario is the rise of 5PL providers. They manage and optimize complete supply chain networks, acting as an overarching coordinator for 3PL and 4PL services. Their comprehensive approach, which leverages centralized control, is expected to drive significant market expansion. This scenario addresses the increasing complexity of global logistics, putting orchestration and integration at the forefront of competitive strategy.

AI-powered route optimization is another critical business scenario. Leveraging machine learning and real-time data, these solutions dynamically create optimal transport and delivery routes, maximizing resource utilization and reducing operational expenses. Organizations using AI-driven routing can achieve savings of up to 30% per delivery load, underlining the strong business case for investment in AI technology for fleet management, platooning, and efficient route planning. Several other emerging trends are also present, including carbon offset logistics platforms, warehouse sharing platforms, freight uberization, and crowdsourced last-mile delivery, all of which are driving innovation and growth in the sector.

China holds a leading position in the logistics & transportation market.

Key growth drivers for China's freight transportation market include rapid advancements in digital freight platforms and AI-based route optimization, which significantly increase truck utilization and reduce empty miles through real-time capacity matching. Government-backed infrastructure initiatives, such as road-rail multimodal integration and expressway network expansion, enable efficient long-haul and cross-border trucking, connecting inland manufacturers to global gateways. Competitive battery-electric and LNG truck deployments in urban "green corridors" accelerate sustainable freight, supported by large-scale cold-chain investments to handle rising demand for perishable goods and pharmaceuticals. Stringent pallet standardization targets and IoT-based tracking are driving container penetration, streamlined operations, and compliance. E-commerce proliferation further fuels the demand for same-day urban deliveries, necessitating diversified, technologically advanced fleets to meet complex inventory and quick-fulfillment expectations.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and strategy directors, and executives from various key organizations operating in this market.

- By Company Type: Logistics & Transportation Players - 45%, OEMs - 10%, Logistics Platform Providers - 25%, Reverse & Specialized Players - 20%

- By Designation: C Level - 40%, Directors - 40%, Others - 20%

- By Region: Americas - 20%, Europe - 30%, Asia Pacific (China, India, ASEAN) - 30%

The logistics & transportation market is led by established players such as DHL Group (Germany), FedEx Express (US), Maersk (Denmark), JDL Group (US), ShipBob (US), WebExpress (Russia), Blackbuck (India), Streebo (US), IBM (US), and UPS (US), among others.

Key Benefits of Buying this Report:

The logistics & transportation market report will help market leaders and new entrants with information on business scenarios and use cases for logistics & transportation players. The report also helps stakeholders understand the market's pulse and provides information on key market drivers, trends, and opportunities.

The report provides insights into the following points:

Analysis of Key Drivers (robotics and automation, digitalization across supply chain, nearshoring, decarbonization, and trade prospects and tariffs)

Product Development/Innovation: Detailed insights on development activities, as well as business scenarios for the logistics & transportation market

Market Development: Comprehensive information about lucrative markets; the report analyzes the logistics & transportation market across varied regions.

Market Diversification: Exhaustive information about business opportunities, revenue potential, untapped geographies, and investments in the logistics & transportation market

TABLE OF CONTENTS

1 INTRODUCTION

2 EXECUTIVE SUMMARY

- 2.1 KEY FINDINGS

- 2.2 GLOBAL LOGISTICS SPENDING (AS % OF GDP)

- 2.3 TRENDS LIKELY TO IMPACT LOGISTICS INDUSTRY BY 2035

- 2.4 SEGMENTS COVERED

- 2.5 FUTURE TRENDS AND IMPACT

- 2.6 FACTORS DRIVING LOGISTICS INDUSTRY

- 2.7 URBAN LOGISTICS SPENDING

- 2.8 NEW BUSINESS SCENARIOS AND USE CASES

3 KEY TRENDS IN LOGISTICS INDUSTRY

- 3.1 ELECTRIC TRUCKS TO DOMINATE FREIGHT MOVEMENT GLOBALLY

- 3.2 RISE OF SUSTAINABLE FUELS IN LOGISTICS

- 3.3 REVOLUTION OF AUTONOMOUS FREIGHT NETWORKS

- 3.4 DECENTRALIZED WAREHOUSING TO GAIN MOMENTUM

- 3.5 INTEGRATION OF DRONES IN LAST-MILE AND URGENT DELIVERIES

- 3.6 SHIFT TOWARD GREEN FREIGHT

- 3.7 RAPID GROWTH OF DIGITAL FREIGHT BROKERAGE

4 PRESENT AND FUTURE OF LOGISTICS INDUSTRY

- 4.1 GLOBAL LOGISTICS INDUSTRY: SEGMENTS COVERED

- 4.2 GLOBAL LOGISTICS SPENDING (AS % OF GDP) AND KEY SEGMENTS

- 4.2.1 SEGMENT 1: TRANSPORTATION

- 4.2.2 SEGMENT 2: WAREHOUSING AND DISTRIBUTION

- 4.2.3 SEGMENT 3: FREIGHT FORWARDING

- 4.2.4 SEGMENT 4: THIRD-PARTY AND FOURTH-PARTY LOGISTICS (3PL AND 4PL)

- 4.2.5 SEGMENT 5: DIGITAL LOGISTICS

- 4.2.6 SEGMENT 6: REVERSE LOGISTICS

- 4.2.7 SEGMENT 7: SPECIALIZED LOGISTICS

- 4.2.8 SEGMENT 8: VALUE-ADDED LOGISTICS SERVICES

- 4.3 VALUE CHAIN EVOLUTION

5 FUTURE TRENDS AND OPPORTUNITIES IN URBAN LOGISTICS

6 KEY DRIVERS OF LOGISTICS INDUSTRY

- 6.1 DRIVER 1: ROBOTICS AND AUTOMATION

- 6.2 DRIVER 2: DIGITALIZATION

- 6.3 DRIVER 3: NEARSHORING

- 6.4 DRIVER 4: DECARBONIZATION

- 6.5 DRIVER 5: TRADE PROSPECTS AND TARIFFS

- 6.6 DRIVER 6: TECHNOLOGICAL INNOVATIONS

7 NEW BUSINESS SCENARIOS AND USE CASES

- 7.1 FIFTH-PARTY LOGISTICS (5PL) PROVIDERS

- 7.2 AI-POWERED ROUTE OPTIMIZATION

- 7.3 UBERIZATION OF FREIGHT

- 7.4 WAREHOUSE-SHARING PLATFORMS

- 7.5 CROWD-SOURCED LAST-MILE DELIVERY

- 7.6 CARBON OFFSET LOGISTICS PLATFORMS