|

시장보고서

상품코드

1915212

Drug Discovery 기술 시장 : 제품별, 기술별, 프로세스별, 치료 분야별 - 세계 예측(-2030년)Drug Discovery Technologies Market by Product, Technology, Process, Therapeutic Area - Global Forecast to 2030 |

||||||

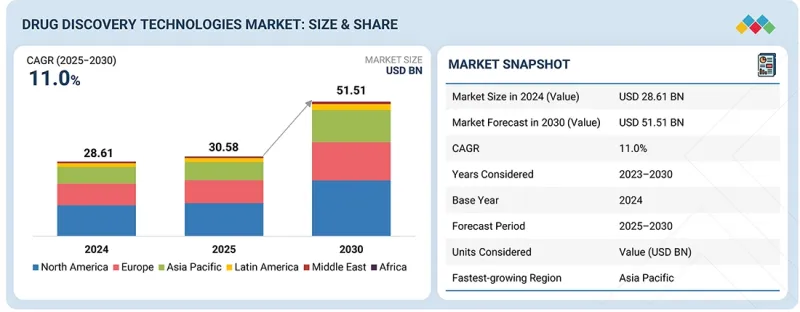

세계의 Drug Discovery 기술 시장 규모는 2025년 305억 8,000만 달러에서 2030년까지 515억 1,000만 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR로 11.0%의 성장이 전망됩니다. 시장 성장은 첨단 스크리닝 플랫폼의 채택 확대와 3차원 세포 배양, 오르가노이드, 장기 온 칩 모델로의 전환에 의해 촉진되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 10억 달러 |

| 부문 | 제품, 기술, 프로세스, 치료 분야, 최종사용자 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

이러한 기술은 질병과의 연관성을 높이고 예측 정확도를 향상시켜 효율적이고 신뢰할 수 있는 신약 개발 프로세스를 지원합니다. 또한, 표적치료와 정밀의료로의 전환은 수요를 더욱 증가시키고 있습니다. 그러나 높은 기술 비용, 복잡한 워크플로우, 숙련된 전문가의 필요성이 시장 성장을 제한하고 있습니다.

인실리콘/AI 기반 Drug Discovery 부문은 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예상됩니다.

인실리코/AI 기반 Drug Discovery 기술 부문은 신약개발 기간 단축, 비용 절감, 성공률 향상으로 인해 Drug Discovery 기술 시장에서 가장 높은 CAGR로 성장하고 있습니다. 이러한 기술은 계산 모델링, 머신러닝, 데이터 분석을 활용하여 신약 후보물질을 신속하게 발굴하고 최적화하는 기술입니다. AI 기반 플랫폼은 대규모 생물학적 및 화학적 데이터세트를 분석하여 초기 단계에서 정확한 표적 식별, 리드 스크리닝, 독성 예측을 가능하게 합니다. 이를 통해 시행착오에 의한 실험실 방식에 대한 의존도를 낮추고, 후기 단계에서의 실패를 최소화할 수 있습니다. 인실리콘/AI 기반 기술은 확장성, 속도, 정밀 의료를 지원하는 능력으로 인해 제약 및 생명공학 기업에게 필수적인 도구가 되어 시장 전반에 걸쳐 강력한 채택을 촉진하고 있습니다.

종양학 부문이 시장에서 가장 큰 점유율을 차지하고 있습니다.

종양학 부문이 가장 큰 시장 점유율을 차지하고 있습니다. 이러한 성장은 전 세계적으로 암 유병률의 증가와 표적 치료 및 맞춤 치료 개발에 대한 관심이 높아짐에 따라 가속화되고 있습니다. 첨단 스크리닝 플랫폼, 하이스루풋 분석, 세포 기반 모델은 잠재적 약물 후보물질 발굴, 표적 검증, 리드 화합물 최적화에 널리 활용되고 있습니다. 암 연구에 대한 적극적인 투자, 임상 파이프라인의 확대, 제약회사와 연구기관의 협력 강화는 이러한 기술의 채택률을 더욱 높이고 있습니다. 의약품 개발의 효율성 향상과 보다 효과적인 암 치료법에 대한 수요는 전 세계적으로 이 부문을 지속적으로 촉진하고 있습니다.

미국은 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예상됩니다.

여러 요인으로 인해 미국이 Drug Discovery 기술 시장에서 가장 높은 성장세를 보이고 있습니다. 주요 제약 및 바이오텍 기업의 강력한 존재감, 선진화된 연구 인프라, 진행 중인 다수의 종양학 프로그램이 주요 촉진요인입니다. 암 연구에서의 하이스루풋 스크리닝, 3D 세포 모델, 장기 칩 플랫폼의 채택 확대가 수요를 촉진하고 있습니다. 지원적인 규제, 생물 의학 연구에 대한 막대한 민관 자금 지원, 정밀 의료에 대한 집중은 시장 확대를 더욱 촉진하고 있습니다. 첨단 Drug Discovery 기술의 폭넓은 활용과 업계와 연구기관의 강력한 협력은 혁신을 촉진하고 고품질 성과를 보장하며, 북미의 선도적 지위를 강화하는 데 기여하고 있습니다.

세계의 Drug Discovery 기술 시장에 대해 조사 분석했으며, 주요 촉진요인과 저해요인, 제품 개발 및 혁신, 경쟁 상황 등에 대해 조사 분석하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

- 북미의 Drug Discovery 기술 시장 : 제품별

- Drug Discovery 기술 시장 : 지리적 성장 기회

- Drug Discovery 기술 시장 : 제품별(2025년·2030년)

제4장 시장 개요

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 미충족 수요와 화이트 스페이스

- 상호 접속된 시장과 부문 횡단적인 기회

- Tier 1/2/3기업 전략적인 활동

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제 전망

- GDP 동향과 예측

- 세계의 의료 업계의 동향

- 세계의 제약 업계의 연구 동향

- 밸류체인 분석

- 생태계 분석

- 가격 책정 분석

- 최종사용자 평균판매가격 : 주요 기업별(2024년)

- 제품 평균판매가격 동향 : 주요 기업별(2022-2024년)

- 평균판매가격 동향 : 기술별(2022-2024년)

- 평균판매가격 동향 : 지역별(2022-2024년)

- 무역 분석

- HS 코드 3822.00 수입 시나리오

- HS 코드 3822.00 수출 시나리오

- HS 코드 9027.00 수입 시나리오

- HS 코드 9027.00 수출 시나리오

- 주요 회의와 이벤트(2025-2026년)

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 투자와 자금 조달 시나리오

- 사례 연구 분석

- Drug Discovery 기술 시장에 대한 2025년 미국 관세의 영향

- 주요 관세율

- 가격의 영향 분석

- 국가/지역에 대한 주요 영향

- 최종 이용 산업에 대한 영향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

- 주요 신기술

- HTS(High Throughput Screening)·자동화

- 자동 액체 처리

- 인접 기술

- AI/ML 대응·인실리코 Drug Discovery 플랫폼

- Drug Discovery 인포매틱스·실험실 디지털화

- 기술/제품 로드맵

- 특허 분석

- 조사 방법

- 출원 특허수

- 주요 특허 리스트

- 향후 용도

- Drug Discovery 기술 시장에 대한 AI/생성형 AI의 영향

- 주요 이용 사례와 시장 전망

- AI를 활용한 Drug Discovery 워크플로우 베스트 프랙티스

- Drug Discovery 기술 시장의 AI 도입 사례 연구

- 상호 접속된 인접 생태계와 시장 기업에 대한 영향

- Drug Discovery 기술 시장의 생성적 분자 설계 채용에 대한 클라이언트 준비 상황

제7장 지속가능성과 규제 상황

- 지역 규제와 컴플라이언스

- 규제기관, 정부기관, 기타 조직

- 업계 표준

- 지속가능성에 대한 대처

- 지속가능성에 대한 영향과 규제 정책의 대처

- 인증, 라벨, 환경기준

제8장 고객 상황과 구매 행동

- 의사결정 프로세스

- 바이어 이해관계자와 구입 평가 기준

- 구매 프로세스의 주요 이해관계자

- 주요 구입 기준 : 최종사용자별

- 채용 장벽과 내부 과제

- 다양한 최종 이용 산업으로부터의 미충족 수요

제9장 Drug Discovery 기술 시장 : 제품별

- 시약·소모품

- 기구

- 바이오인포매틱스 툴·소프트웨어

제10장 Drug Discovery 기술 시장 : 기술별

- HTS(High Throughput Screening) 기술

- 차세대 시퀀싱

- 중합효소 연쇄 반응

- 인실리코/AI 기반 Drug Discovery 기술

- X선 결정구조 분석

- 크로마토그래피

- 질량 분석

- 기타 기술

제11장 Drug Discovery 기술 시장 : 프로세스별

- 타겟 식별

- 타겟 검증

- Hit to Lead 식별

- 리드 최적화

- 후보 검증

제12장 Drug Discovery 기술 시장 : 치료 분야별

- 종양학

- 감염증

- 심혈관질환

- 신경질환

- 내분비·대사질환

- 자가면역질환

- 기타 치료 분야

제13장 Drug Discovery 기술 시장 : 최종사용자별

- 제약 기업·바이오테크놀러지 기업

- 학술연구기관

- 임상시험수탁기관(CRO)

제14장 Drug Discovery 기술 시장 : 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동

- GCC 국가

- 기타 중동

- 아프리카

제15장 경쟁 구도

- 개요

- 주요 기업 경쟁 전략/강점

- 매출 분석

- 시장 점유율 분석

- 브랜드/제품의 비교

- THERMO FISHER SCIENTIFIC INC.

- MERCK KGAA

- AGILENT TECHNOLOGIES, INC.

- REVVITY

- ILLUMINA, INC.

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업 평가 매트릭스 : 스타트업/중소기업(2024년)

- 기업 평가와 재무 지표

- 경쟁 시나리오

제16장 기업 개요

- 주요 기업

- THERMO FISHER SCIENTIFIC INC.

- MERCK KGAA

- AGILENT TECHNOLOGIES, INC.

- REVVITY

- ILLUMINA, INC.

- DANAHER CORPORATION

- F. HOFFMANN-LA ROCHE LTD

- BRUKER

- QIAGEN

- BIO-RAD LABORATORIES, INC.

- TECAN TRADING AG

- TAKARA BIO INC.

- CORNING INCORPORATED

- HAMILTON COMPANY

- PACBIO

- OXFORD NANOPORE TECHNOLOGIES PLC

- PROMEGA CORPORATION

- WATERS CORPORATION

- SARTORIUS AG

- BD

- EPPENDORF SE

- SHIMADZU CORPORATION

- AURORA BIOMED INC.

- STANDARD BIOTOOLS

- JEOL LTD.

- GILSON INCORPORATED

- BIOMERIEUX

- GREINER AG

- BGI GROUP

- PORVAIR

- 기타 기업

- POLARIS GENOMICS

- BICO

- CREATIVE BIOARRAY

- SPHERE BIO

- GENSCRIPT

- SCHRODINGER, INC.

- LECO CORPORATION

- TRANSGEN BIOTECH CO., LTD

- BMG LABTECH

- NANOTEMPER TECHNOLOGIES

- MGI TECH CO., LTD.

- ARACELI BIOSCIENCES

- ANALYTIK JENA GMBH+CO. KG

- BIOSOLVEIT GMBH

- EVOSEP

제17장 조사 방법

제18장 부록

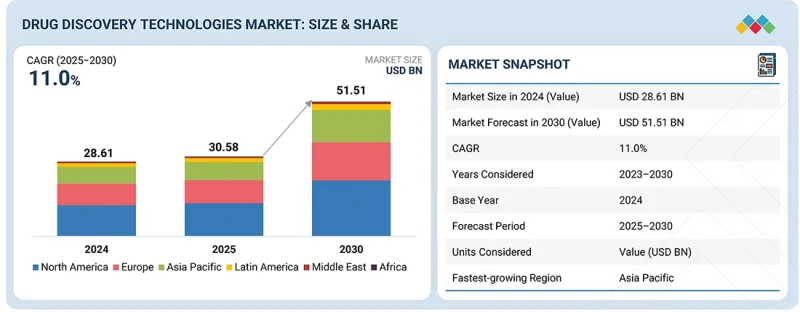

KSM 26.02.05The drug discovery technologies market is expected to reach USD 51.51 billion in 2030 from USD 30.58 billion in 2025, at a CAGR of 11.0% during the forecast period. The market is driven by the increasing adoption of advanced screening platforms and the shift toward 3D cell cultures, organoids, and organ-on-a-chip models.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product, Technology, Process, Therapeutic Area, End User |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, the Middle East, and Africa |

These technologies improve disease relevance, enhance predictive accuracy, and support more efficient and reliable drug discovery processes. Furthermore, the shift towards targeted and precision therapies further boosts demand. However, high technology costs, complex workflows, and the need for skilled professionals continue to limit market growth.

The in-silico/AI-based drug discovery segment is expected to grow at the highest CAGR during the forecast period.

The in silico/AI-based drug discovery technology segment is growing at the highest CAGR in the drug discovery technologies market due to its ability to shorten discovery timelines, reduce costs, and improve success rates. These technologies use computational modeling, machine learning, and data analytics to rapidly identify and optimize drug candidates. By analyzing large biological and chemical datasets, AI-based platforms enable accurate target identification, lead screening, and toxicity prediction at early stages. This reduces reliance on trial-and-error laboratory methods and minimizes late-stage failures. Their scalability, speed, and ability to support precision medicine make in silico and AI-based technologies essential tools for pharmaceutical and biotechnology companies, driving strong adoption across the market.

The oncology segment holds the largest share of the market.

The oncology segment accounts for the largest share of the Drug Discovery Technologies Market. This growth is driven by the increasing prevalence of cancer worldwide and the rising focus on developing targeted and personalized therapies. Advanced screening platforms, high-throughput assays, and cell-based models are widely used to identify potential drug candidates, validate targets, and optimize leads. Strong investments in cancer research, expanding clinical pipelines, and growing collaboration between pharmaceutical companies and research institutes further support the adoption of these technologies. Improved drug development efficiency and the demand for more effective cancer treatments continue to drive growth in this segment globally.

The US is expected to grow at the highest CAGR during the forecast period.

The US is experiencing the highest growth in the drug discovery technologies market due to several factors. A strong presence of leading pharmaceutical and biotech companies, advanced research infrastructure, and a large number of ongoing oncology programs are key drivers. Increasing adoption of high-throughput screening, 3D cell models, and organ-on-a-chip platforms in cancer research is fueling demand. Supportive regulations, substantial public and private funding for biomedical research, and a focus on precision medicine further contribute to market expansion. Widespread use of advanced discovery technologies and robust collaborations between industry and research institutes enhance innovation, ensuring high-quality outputs and reinforcing North America's leading position globally.

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Supply Side - 70% and Demand Side- 30%

- By Designation: Managers - 45%, CXOs and Directors - 30%, and Executives - 25%

- By Region: North America - 40%, Europe - 25%, Asia Pacific - 25%, Latin America - 5%, the Middle East & Africa - 5%

Thermo Fisher Scientific Inc. (US), Danaher Corporation (US), Agilent Technologies, Inc. (US), Illumina, Inc. (US), Revvity (US), F. Hoffmann-La Roche Ltd (Switzerland), Bruker (US), QIAGEN (Germany), Bio-Rad Laboratories, Inc. (US), Tecan Trading AG (Switzerland), Takara Bio Inc. (Japan), Corning Incorporated (US), Hamilton Company (US), PacBio (US), Oxford Nanopore Technologies plc (UK), Promega Corporation (US), Waters Corporation (US), Merck KGAA (Germany), Sartorius AG (Germany), BD (US), Eppendorf SE (Germany), Shimadzu Corporation (Japan), Aurora Biomed Inc. (Canada), Standard BioTools (US), Jeol Ltd. (Japan), Gilson Incorporated (US), BIOMERIEUX (France), Greiner AG (Austria), BGI Group (China), Porvair (UK), Polaris Genomics (US), BICO (Sweden), Creative Bioarray (US), Sphere Bio (UK), GenScript (UK), Schrodinger, Inc. (US), LECO Corporation (US), TransGen Biotech Co., Ltd. (China), BMG LABTECH (Germany), NanoTemper Technologies (Germany), MGI Tech Co., Ltd. (China), Araceli Biosciences (US), Sphere Bio (US), BioSolvelT GmbH (Germany), and Evosep (Denmark) are some of the key companies offering drug discovery technologies products.

Research Coverage

This research report categorizes the drug discovery technologies market by product (reagents & consumables, instruments, bioinformatics tools & software), technology (high-throughput screening technologies, next-generation sequencing, polymerase chain reaction, in-silico/AI-based drug discovery technologies, X-ray crystallography, chromatography, mass spectrometry, other technologies), process (target identification, target validation, hit-to-lead identification, lead optimization, candidate validation), therapeutic area (oncology, infectious diseases, cardiovascular diseases, neurological diseases, endocrine & metabolic diseases, autoimmune disorders, other therapeutic areas), end user (pharmaceutical & biotechnology companies, academic & research institutes, contract research organizations (CROs), other end users), and region (North America, Europe, Asia Pacific, Latin America, Middle East, And Africa).

The report's scope encompasses detailed information about the primary factors, including drivers, restraints, challenges, and opportunities, that influence the growth of the drug discovery technologies market. A comprehensive analysis of key industry players has been performed to provide insights into their business overview, product portfolio, key strategies, new product launches, acquisitions, and recent developments related to the drug discovery technologies market. This report also includes a competitive analysis of emerging startups in the drug discovery technologies industry ecosystem.

Key Benefits of Buying the Report

The report will assist market leaders and new entrants by providing revenue estimates for the overall market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to position their businesses effectively and develop suitable go-to-market strategies. This report will enable stakeholders to grasp the market's pulse and offer information on key market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

- Analysis of key drivers (increasing adoption of advanced screening platforms, shift toward biologics and advanced therapeutic modalities, transition from conventional two-dimensional cultures to three-dimension models, technological innovations in assay miniaturization and automation), restraints (high up-front investment in instruments, automation, and data infrastructure and shortage of skilled personnel), opportunities (growing demand for in-silico based discovery and increasing need for specialized ADME/Toxicology testing), and challenges (assay reproducibility and standardization issues) influencing the market growth

- Product Development/Innovation: Detailed insights into newly launched products and technological assessment of the drug discovery technologies market

- Market Development: Comprehensive information about lucrative markets and analysis of the market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the drug discovery technologies market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players, including Thermo Fisher Scientific Inc. (US), Danaher Corporation (US), Agilent Technologies, Inc. (US), Illumina, Inc. (US), Revvity (US), among others, offering products for the drug discovery technologies market. Other companies include Polaris Genomics (US), BICO (Sweden), Creative Bioarray (US), Sphere Bio (UK), GenScript (UK), Schrodinger, Inc. (US), LECO Corporation (US), among others, for the drug discovery technologies market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN DRUG DISCOVERY TECHNOLOGIES MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 NORTH AMERICA: DRUG DISCOVERY TECHNOLOGIES MARKET, BY PRODUCT

- 3.2 DRUG DISCOVERY TECHNOLOGIES MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.3 DRUG DISCOVERY TECHNOLOGIES MARKET, BY PRODUCT, 2025 VS. 2030 (%)

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing adoption of advanced screening platforms

- 4.2.1.2 Shift toward biologics and advanced therapeutic modalities

- 4.2.1.3 Transition from conventional two-dimensional cultures to three-dimensional models

- 4.2.1.4 Technological innovations in assay miniaturization and automation

- 4.2.2 RESTRAINTS

- 4.2.2.1 High up-front investment in instruments, automation, and data infrastructure

- 4.2.2.2 Shortage of skilled personnel

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing demand for in-silico-based discovery

- 4.2.3.2 Increasing need for specialized ADME/Toxicology testing

- 4.2.4 CHALLENGES

- 4.2.4.1 Assay reproducibility and standardization issues

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVIES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 R&D TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 R&D TRENDS IN GLOBAL PHARMA INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF END USERS, BY KEY PLAYER, 2024

- 5.5.2 AVERAGE SELLING PRICE TREND OF PRODUCTS, BY KEY PLAYER, 2022-2024

- 5.5.2.1 Average selling price of instruments, by key player, 2024

- 5.5.2.2 Average selling price of consumables, by key player, 2024

- 5.5.3 AVERAGE SELLING PRICE TREND, BY TECHNOLOGY, 2022-2024

- 5.5.4 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2024

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO FOR HS CODE 3822.00

- 5.6.2 EXPORT SCENARIO FOR HS CODE 3822.00

- 5.6.3 IMPORT SCENARIO FOR HS CODE 9027.00

- 5.6.4 EXPORT SCENARIO FOR HS CODE 9027.00

- 5.7 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 AI-DESIGNED IPF DRUG CANDIDATE ADVANCES IN CLINICAL DEVELOPMENT

- 5.10.2 INDUSTRY CONSORTIUM POOLS DATA TO IMPROVE AI-DRIVEN SMALL MOLECULE DISCOVERY

- 5.10.3 NEW AI FRAMEWORK FROM IIT MADRAS AND OHIO STATE STREAMLINES MOLECULAR DESIGN

- 5.11 IMPACT OF 2025 US TARIFF ON DRUG DISCOVERY TECHNOLOGIES MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 KEY IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 END-USE INDUSTRY IMPACT

- 5.11.5.1 Pharmaceutical and Biotechnology Companies

- 5.11.5.2 Academic and Research Institutes

- 5.11.5.3 Contract Research Organizations (CROs)

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 HIGH-THROUGHPUT SCREENING (HTS) & AUTOMATION

- 6.1.2 AUTOMATED LIQUID HANDLING

- 6.2 ADJACENT TECHNOLOGIES

- 6.2.1 AI/ML-ENABLED & IN SILICO DISCOVERY PLATFORMS

- 6.2.2 DISCOVERY INFORMATICS & LAB DIGITALIZATION

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.4 PATENT ANALYSIS

- 6.4.1 METHODOLOGY

- 6.4.2 NUMBER OF PATENTS FILED

- 6.4.3 LIST OF KEY PATENTS

- 6.5 FUTURE APPLICATIONS

- 6.6 IMPACT OF AI/GEN AI ON DRUG DISCOVERY TECHNOLOGIES MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN AI-ENABLED DRUG DISCOVERY WORKFLOWS

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN DRUG DISCOVERY TECHNOLOGIES MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE MOLECULAR DESIGN IN DRUG DISCOVERY TECHNOLOGIES MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.2.1 North America

- 7.1.2.1.1 US

- 7.1.2.1.2 Canada

- 7.1.2.2 Europe

- 7.1.2.2.1 UK

- 7.1.2.3 Asia Pacific

- 7.1.2.3.1 China

- 7.1.2.3.2 Japan

- 7.1.2.3.3 India

- 7.1.2.3.4 South Korea

- 7.1.2.3.5 Australia

- 7.1.2.3.6 Rest of Asia Pacific

- 7.1.2.1 North America

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOUR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA, BY END USER

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

9 DRUG DISCOVERY TECHNOLOGIES MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 REAGENTS & CONSUMABLES

- 9.2.1 INNOVATIONS IN ASSAY CHEMISTRY AND SUPPLY CHAIN RESILIENCE TO PROMOTE GROWTH

- 9.3 INSTRUMENTS

- 9.3.1 HIGH-PERFORMANCE ANALYTICAL ATTRIBUTES AND AUTOMATION TO DRIVE MARKET

- 9.4 BIOINFORMATICS TOOLS & SOFTWARE

- 9.4.1 AI RISING ADOPTION OF AI AND MACHINE LEARNING FOR PREDICTIVE MODELING TO FUEL MARKET

10 DRUG DISCOVERY TECHNOLOGIES MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 HIGH-THROUGHPUT SCREENING (HTS) TECHNOLOGIES

- 10.2.1 AUTOMATED LIQUID HANDLING

- 10.2.1.1 Increasing focus on precision, integration, and productivity to drive market

- 10.2.2 MICROPLATE-BASED HTS

- 10.2.2.1 Rising investments in pharmaceutical and biotechnology R&D to fuel market

- 10.2.3 LAB-ON-A CHIP

- 10.2.3.1 Increasing demand for more predictive preclinical models to boost market

- 10.2.4 LABEL-FREE TECHNOLOGY

- 10.2.4.1 Real-time, label-free interaction to accelerate segment growth

- 10.2.1 AUTOMATED LIQUID HANDLING

- 10.3 NEXT-GENERATION SEQUENCING

- 10.3.1 EXPANDED INTEGRATION OF ADVANCED NGS TECHNOLOGIES TO DRIVE MARKET

- 10.4 POLYMERASE CHAIN REACTION

- 10.4.1 ENHANCED POLYMERASE CHAIN REACTION INNOVATION AND AUTOMATION TO DRIVE MARKET

- 10.5 IN-SILICO/ AI-BASED DRUG DISCOVERY TECHNOLOGIES

- 10.5.1 COMPUTATIONAL INTELLIGENCE AND COLLABORATIVE AI INNOVATIONS TO PROPEL MARKET

- 10.6 X-RAY CRYSTALLOGRAPHY

- 10.6.1 ADVANCED INSTRUMENTATION AND INNOVATIVE X-RAY TECHNIQUES TO BOOST MARKET

- 10.7 CHROMATOGRAPHY

- 10.7.1 REGULATORY PRESSURES AND COMPLEX BIOLOGICS R&D TO AID GROWTH

- 10.8 MASS SPECTROMETRY

- 10.8.1 INVESTMENT IN ADVANCED INSTRUMENTATION AND DATA-DRIVEN WORKFLOWS TO DRIVE MARKET

- 10.9 OTHER TECHNOLOGIES

11 DRUG DISCOVERY TECHNOLOGIES MARKET, BY PROCESS

- 11.1 INTRODUCTION

- 11.2 TARGET IDENTIFICATION

- 11.2.1 INCREASING CLINICAL DATA VOLUME TO BOOST MARKET

- 11.3 TARGET VALIDATION

- 11.3.1 INCREASING TECHNOLOGICAL ADVANCEMENTS TO PROMOTE GROWTH

- 11.4 HIT-TO-LEAD IDENTIFICATION

- 11.4.1 GROWING ADOPTION OF MULTI-DISCIPLINARY APPROACHES TO DRIVE MARKET

- 11.5 LEAD OPTIMIZATION

- 11.5.1 INCREASING FOCUS ON REDUCING LATE-STAGE ATTRITION AND INCREASING PROBABILITY OF THERAPEUTIC SUCCESS TO FUEL MARKET

- 11.6 CANDIDATE VALIDATION

- 11.6.1 INCREASING COMPLEXITY OF THERAPEUTIC MODALITIES TO SUSTAIN GROWTH

12 DRUG DISCOVERY TECHNOLOGIES MARKET, BY THERAPEUTIC AREA

- 12.1 INTRODUCTION

- 12.2 ONCOLOGY

- 12.2.1 SHIFT TOWARD PRECISION ONCOLOGY TO PROMOTE GROWTH

- 12.3 INFECTIOUS DISEASES

- 12.3.1 RISING ANTIMICROBIAL RESISTANCE AND AI-DRIVEN INNOVATIONS TO DRIVE MARKET

- 12.4 CARDIOVASCULAR DISEASES

- 12.4.1 INCREASING PREVALENCE OF CARDIOVASCULAR RISK FACTORS TO BOOST MARKET

- 12.5 NEUROLOGICAL DISEASES

- 12.5.1 INTEGRATION OF ADVANCED MODELS AND STRATEGIC INVESTMENTS TO FUEL MARKET

- 12.6 ENDOCRINE & METABOLIC DISORDERS

- 12.6.1 RISING PREVALENCE OF TYPE 2 DIABETES, OBESITY, AND ASSOCIATED METABOLIC SYNDROMES TO DRIVE MARKET

- 12.7 AUTOIMMUNE DISORDERS

- 12.7.1 WIDESPREAD ADOPTION OF BIOLOGICS AND SMALL MOLECULES TO PROPEL MARKET

- 12.8 OTHER THERAPEUTIC AREAS

13 DRUG DISCOVERY TECHNOLOGIES MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 13.2.1 TECHNOLOGY INTEGRATION AND STRATEGIC PARTNERSHIPS TO CONTRBUTE TO GROWTH

- 13.3 ACADEMIC & RESEARCH INSTITUTES

- 13.3.1 RISING PUBLIC AND PRIVATE RESEARCH FUNDING AND STRONGER ACADEMIC-INDUSTRY COLLABORATION FRAMEWORKS TO AUGMENT GROWTH

- 13.4 CONTRACT RESEARCH ORGANIZATIONS (CROS)

- 13.4.1 INCREASING R&D OUTSOURCING TO EXPEDITE GROWTH

14 DRUG DISCOVERY TECHNOLOGIES MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Expanding network of cross-border partnerships and investments to expedite growth

- 14.2.2 CANADA

- 14.2.2.1 Increasing adoption of AI and open-science models to accelerate growth

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Strong network of publicly funded research institutes, contract research organizations, and pharmaceutical developers to boost market

- 14.3.2 UK

- 14.3.2.1 Increasing focus on next-generation computational platforms to promote growth

- 14.3.3 FRANCE

- 14.3.3.1 Robust innovation ecosystem and AI-enabled research to propel market

- 14.3.4 ITALY

- 14.3.4.1 Rising research funding to contribute to growth

- 14.3.5 SPAIN

- 14.3.5.1 Well-established network of research centers and universities to boost market

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Global partnerships to propel market

- 14.4.2 JAPAN

- 14.4.2.1 Rising integration of AI and international partnerships to favor growth

- 14.4.3 INDIA

- 14.4.3.1 Domestic infrastructure enhancements and government initiatives to support growth

- 14.4.4 AUSTRALIA

- 14.4.4.1 Rising adoption of artificial intelligence and advanced computational tools to foster growth

- 14.4.5 SOUTH KOREA

- 14.4.5.1 Favorable public policies to support growth

- 14.4.6 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 LATIN AMERICA

- 14.5.1 BRAZIL

- 14.5.1.1 Public-private collaborations to bolster growth

- 14.5.2 MEXICO

- 14.5.2.1 Rising demand for AI-powered research to support growth

- 14.5.3 REST OF LATIN AMERICA

- 14.5.1 BRAZIL

- 14.6 MIDDLE EAST

- 14.6.1 GCC COUNTRIES

- 14.6.1.1 Saudi Arabia

- 14.6.1.1.1 Increasing focus on regulatory reform, research funding, and international partnerships to boost market

- 14.6.1.2 UAE

- 14.6.1.2.1 Strong government vision and cross-sector partnerships to aid growth

- 14.6.1.3 Rest of GCC countries

- 14.6.1.1 Saudi Arabia

- 14.6.2 REST OF MIDDLE EAST

- 14.6.1 GCC COUNTRIES

- 14.7 AFRICA

- 14.7.1 STRATEGIC PARTNERSHIPS AND CAPACITY BUILDING INITIATIVES TO PROPEL MARKET

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN

- 15.3 REVENUE ANALYSIS

- 15.4 MARKET SHARE ANALYSIS

- 15.5 BRAND/PRODUCT COMPARISON

- 15.5.1 THERMO FISHER SCIENTIFIC INC.

- 15.5.2 MERCK KGAA

- 15.5.3 AGILENT TECHNOLOGIES, INC.

- 15.5.4 REVVITY

- 15.5.5 ILLUMINA, INC.

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 15.6.5.1 Company footprint

- 15.6.5.2 Region footprint

- 15.6.5.3 Product footprint

- 15.6.5.4 Technology footprint

- 15.6.5.5 Process footprint

- 15.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 15.7.1 PROGRESSIVE COMPANIES

- 15.7.2 RESPONSIVE COMPANIES

- 15.7.3 DYNAMIC COMPANIES

- 15.7.4 STARTING BLOCKS

- 15.7.5 COMPETITIVE BENCHMARKING

- 15.7.5.1 Detailed list of key startups/SMEs

- 15.7.5.2 Competitive benchmarking of key startups/SMEs

- 15.8 COMPANY VALUATION AND FINANCIAL METRICS

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

- 15.9.4 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 THERMO FISHER SCIENTIFIC INC.

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches

- 16.1.1.3.2 Deals

- 16.1.1.3.3 Expansions

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths/Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses/Competitive threats

- 16.1.2 MERCK KGAA

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Deals

- 16.1.2.3.2 Expansions

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths/Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses/Competitive threats

- 16.1.3 AGILENT TECHNOLOGIES, INC.

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches

- 16.1.3.3.2 Expansions

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths/Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses/Competitive threats

- 16.1.4 REVVITY

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches

- 16.1.4.3.2 Deals

- 16.1.4.3.3 Expansions

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths/Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses/Competitive threats

- 16.1.5 ILLUMINA, INC.

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product launches

- 16.1.5.3.2 Deals

- 16.1.5.3.3 Expansions

- 16.1.5.3.4 Other developments

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths/Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses/Competitive threats

- 16.1.6 DANAHER CORPORATION

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches

- 16.1.6.3.2 Deals

- 16.1.6.3.3 Expansions

- 16.1.6.4 MnM view

- 16.1.6.4.1 Key strengths/Right to win

- 16.1.6.4.2 Strategic choices

- 16.1.6.4.3 Weaknesses/Competitive threats

- 16.1.7 F. HOFFMANN-LA ROCHE LTD

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Product launches

- 16.1.7.3.2 Deals

- 16.1.7.3.3 Other developments

- 16.1.8 BRUKER

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches

- 16.1.8.3.2 Deals

- 16.1.8.3.3 Expansions

- 16.1.9 QIAGEN

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches

- 16.1.9.3.2 Deals

- 16.1.9.3.3 Expansions

- 16.1.10 BIO-RAD LABORATORIES, INC.

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Product launches

- 16.1.10.3.2 Deals

- 16.1.11 TECAN TRADING AG

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.12 TAKARA BIO INC.

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Product launches

- 16.1.13 CORNING INCORPORATED

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.14 HAMILTON COMPANY

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Product launches

- 16.1.14.3.2 Deals

- 16.1.15 PACBIO

- 16.1.15.1 Business overview

- 16.1.15.2 Products offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Product launches

- 16.1.15.3.2 Expansions

- 16.1.16 OXFORD NANOPORE TECHNOLOGIES PLC

- 16.1.16.1 Business overview

- 16.1.16.2 Products offered

- 16.1.16.3 Recent developments

- 16.1.16.3.1 Product launches

- 16.1.16.3.2 Deals

- 16.1.17 PROMEGA CORPORATION

- 16.1.17.1 Business overview

- 16.1.17.2 Products offered

- 16.1.18 WATERS CORPORATION

- 16.1.18.1 Business overview

- 16.1.18.2 Products offered

- 16.1.18.3 Recent developments

- 16.1.18.3.1 Product launches

- 16.1.18.3.2 Deals

- 16.1.19 SARTORIUS AG

- 16.1.19.1 Business overview

- 16.1.19.2 Products offered

- 16.1.19.3 Recent developments

- 16.1.19.3.1 Deals

- 16.1.20 BD

- 16.1.20.1 Business overview

- 16.1.20.2 Products offered

- 16.1.20.3 Recent developments

- 16.1.20.3.1 Product launches

- 16.1.20.3.2 Deals

- 16.1.21 EPPENDORF SE

- 16.1.21.1 Business overview

- 16.1.21.2 Products offered

- 16.1.21.3 Recent developments

- 16.1.21.3.1 Deals

- 16.1.22 SHIMADZU CORPORATION

- 16.1.22.1 Business overview

- 16.1.22.2 Business overview

- 16.1.22.3 Products offered

- 16.1.23 AURORA BIOMED INC.

- 16.1.23.1 Business overview

- 16.1.23.2 Products offered

- 16.1.24 STANDARD BIOTOOLS

- 16.1.24.1 Business overview

- 16.1.24.2 Products offered

- 16.1.25 JEOL LTD.

- 16.1.25.1 Business overview

- 16.1.25.2 Products offered

- 16.1.26 GILSON INCORPORATED

- 16.1.26.1 Business overview

- 16.1.26.2 Products offered

- 16.1.27 BIOMERIEUX

- 16.1.27.1 Business overview

- 16.1.27.2 Products offered

- 16.1.28 GREINER AG

- 16.1.28.1 Business overview

- 16.1.28.2 Products offered

- 16.1.29 BGI GROUP

- 16.1.29.1 Business overview

- 16.1.29.2 Products offered

- 16.1.30 PORVAIR

- 16.1.30.1 Business overview

- 16.1.30.2 Products offered

- 16.1.1 THERMO FISHER SCIENTIFIC INC.

- 16.2 OTHER PLAYERS

- 16.2.1 POLARIS GENOMICS

- 16.2.2 BICO

- 16.2.3 CREATIVE BIOARRAY

- 16.2.4 SPHERE BIO

- 16.2.5 GENSCRIPT

- 16.2.6 SCHRODINGER, INC.

- 16.2.7 LECO CORPORATION

- 16.2.8 TRANSGEN BIOTECH CO., LTD

- 16.2.9 BMG LABTECH

- 16.2.10 NANOTEMPER TECHNOLOGIES

- 16.2.11 MGI TECH CO., LTD.

- 16.2.12 ARACELI BIOSCIENCES

- 16.2.13 ANALYTIK JENA GMBH+CO. KG

- 16.2.14 BIOSOLVEIT GMBH

- 16.2.15 EVOSEP

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 Key primary participants

- 17.1.2.3 Breakdown of primary interviews

- 17.1.2.4 Key industry insights

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.2.3 BASE NUMBER CALCULATION

- 17.3 GROWTH FORECAST MODEL

- 17.4 DATA TRIANGULATION

- 17.5 FACTOR ANALYSIS

- 17.6 RESEARCH ASSUMPTIONS

- 17.7 RESEARCH LIMITATIONS AND RISK ASSESSMENT

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS