|

시장보고서

상품코드

1919587

폴리우레탄 분산액 시장 : 유형별, 화학 구조별, 기능성별, 용도별, 지역별 예측(-2030년)Polyurethane Dispersions Market By Type, By Chemistry, By Functionality (One-Component Systems, Two-Component Systems), By Application, and Region - Global Forecast to 2030 |

||||||

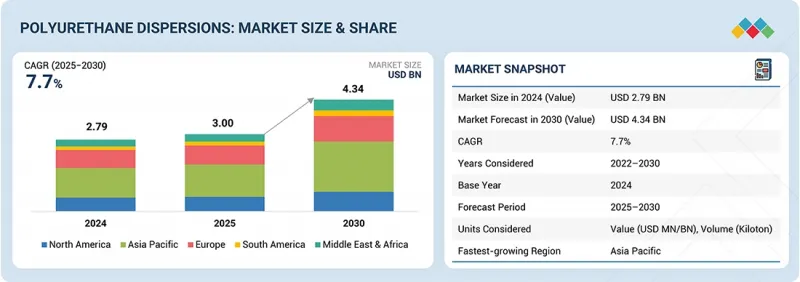

세계의 폴리우레탄 분산액 시장 규모는 2025년 30억 달러에서 2030년까지 43억 4,000만 달러에 이를 것으로 예측되며, 예측 기간 중의 CAGR은 7.7%로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(100만 달러) 및 킬로톤 |

| 부문 | 유형별, 화학 구조별, 기능성별, 용도별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동, 아프리카, 남미 |

폴리우레탄 분산액(PUD)은 자동차, 건설, 섬유, 접착제, 가죽 마감, 목재 코팅 등 다양한 산업에서 채용이 진행되고 있습니다. 이러한 추세를 뒷받침하는 주요 요인 중 하나는 보다 엄격한 환경 규제의 실행과 솔벤트 기반 폴리우레탄 시스템의 급속한 단계적 폐지입니다. 미국 환경보호청(EPA)과 유럽화학물질청(ECHA) 등의 규제기관, REACH 및 EU 도료지령(2004/42/EC) 등 지역의 VOC 지령은 보다 낮은 배출기준을 시행하고 있으며, 제조업체는 수성 PUD 기술로의 전환을 강요받고 있습니다. 현대의 하이브리드형, 음이온형, 양이온형 PUD는 우수한 피막 형성 능력, 물리적 스트레스에 대한 기계적 내구성, 내약품성, 표면에 대한 견고한 밀착성, 낮은 VOC 레벨 등 다양한 이점을 제공함과 동시에 보다 안전한 취급 방법을 보장합니다. 이러한 유형의 PUD를 이용한 고성능 코팅 시스템은 자동차 OEM, 가죽 마감, 방수 섬유, 산업용 목재 코팅, 연포장용 접착제 등 다양한 분야에서 볼 수 있습니다.

솔벤트 프리 폴리우레탄 용액은 낮은 VOC 함량의 친환경 제품에 대한 수요 증가로 인해 폴리우레탄 분산액 시장에서 급속한 성장이 예상됩니다. 유기 용매를 사용하지 않는 이러한 용액은 기존의 선택과 비교하여 우수한 물리적 특성, 내화학성 및 코팅 형성성을 제공합니다. 솔벤트 함량이 0이므로 가죽, 섬유, 포장, 목재 코팅, 자동차 인테리어 등 민감한 용도에 이상적입니다. VOC 배출 감축을 위한 규제 압력의 높아짐에 따라, 폴리카보네이트 폴리올이나 재생 가능 원료의 진보에 의해 무용제 PUD의 내구성과 성능이 향상하고 있습니다. 제조업체가 효율성을 저하시키지 않고 환경 친화적인 대체품으로 전환하는 동안 무용제 폴리우레탄 솔루션은 세계 PUD 시장의 성장을 이끌고 있습니다.

건설, 자동차, 목재 등의 분야에서의 낮은 VOC 및 친환경 도료 수요 증가에 따라 시장은 급속한 성장이 예상됩니다. PUD 도료는 우수한 밀착성, 내약품성, 내습성, 유연성을 갖추고 있으며, 배출 규제의 강화에 따라 용제계 도료를 대체하는 유력한 옵션이 되고 있습니다. 뛰어난 내구성과 미관성의 향상에 의해 건축용 도료, 자동차 보수 도장, 보호 마감 용도로의 채용이 확대되고 있습니다. 게다가 지속 가능한 제조 방법으로의 이행이나 수성 및 무용제 배합의 개발이 진행됨으로써, PUD의 채용은 더욱 촉진될 것입니다. 각 산업이 보다 친환경적인 기술과 뛰어난 성능을 추구하는 가운데, PUD는 차세대 페인트의 발전에 중요한 역할을 하며 시장의 견조한 성장을 확실히할 것입니다.

급속한 산업화, 제조 기회 증가, 친환경 코팅 기술에 대한 수요 증가가 아시아태평양 시장 성장을 이끌고 있습니다. 중국, 인도, 한국, 인도네시아 등의 국가에서는 자동차, 섬유, 건설, 포장 등의 분야에서 현저한 성장이 보이며, 이들은 수성 PUD 기반 코팅, 접착제, 실란트의 주요 소비 분야입니다. 낮은 VOC, 무용제, 지속 가능한 배합으로의 전환은 중국의 VOC 규제와 인도의 정부 주도 그린 케미스트리 구상 등 엄격한 환경 규제에 의해 촉진되고 있습니다. 이러한 요인은 지역 전체에서 PUD 제품 수요를 증가시키고 있습니다. 또한 정부의 인프라 정비 투자, 현지 생산 능력 확대, 경쟁력 있는 제조업체의 존재도 시장 성장에 기여하고 있습니다.

이 보고서는 Covestro AG(독일), BASF(독일), Dow(미국), Wanhua(중국), Lubrizol(미국), Mitsui Chemicals, Inc.(일본), Alberdingk Boley GmbH(독일), Perstorp(스웨덴), Stahl Holdings BV(네덜란드), UBE Corporation(일본) 등의 기업에 대해 조사했습니다.

본 조사는 폴리우레탄 분산제 시장에서 이러한 주요 기업에 대한 기업 프로파일, 최근 동향, 주요 시장 전략 등 상세한 경쟁 분석을 포함하고 있습니다.

조사 범위

본 조사 보고서에서는 폴리우레탄 분산제 시장을 유형별(무용제 폴리우레탄 분산제, 저용제 폴리우레탄 분산제), 화학 구조별(음이온성 폴리우레탄 분산제, 양이온성 폴리우레탄 분산제, 비이온성 폴리우레탄 분산제, 자기 가교형 폴리우레탄 분산제, 하이브리드 폴리우레탄 분산액), 기능성별(1액형(1K) 시스템, 2액형(2K) 시스템), 용도(페인트 및 코팅, 접착제 및 실란트, 피혁 제조 및 마무리, 섬유 가공)별로 분류하고 있습니다. 이 보고서의 범위에는 폴리 우레탄 분산액 시장의 성장에 영향을 미치는 촉진요인, 제약 요인, 과제 및 기회에 대한 자세한 정보가 포함됩니다. 주요 업계 선수의 상세한 분석을 실시하고, 사업 개요, 제공 제품 및 폴리우레탄 분산액 시장과 관련된 인수합병, 제품 발매, 사업 확대 등 주요 전략에 대한 인사이트을 제공합니다. 본 보고서에서는 폴리우레탄 분산액 시장 생태계의 신흥 스타트업 기업의 경쟁 인사이트도 다루고 있습니다.

이 보고서를 구입하는 이유

이 보고서는 시장 리더 및 신규 진출기업에게 전체 폴리 우레탄 분산 시장과 그 하위 부문의 수익 수치에 대한 가장 정확한 추정치를 제공합니다. 이를 통해 이해관계자는 경쟁 구도를 이해하고 자사의 포지셔닝에 대한 인사이트를 높이고 적절한 시장 진출 전략을 수립할 수 있습니다. 이 보고서는 시장 동향을 파악하고 주요 시장 성장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 이해 관계자에게 제공합니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 중요 인사이트

제4장 시장 개요

- 시장 역학

- 미충족 요구와 공백

- 상호접속된 시장과 분야간 기회

- Tier 1/2/3 기업의 전략적 움직임

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제 분석

- 밸류체인 분석

- 생태계 분석

- 무역 분석

- 2025-2026년의 주된 회의와 이벤트

- 고객 사업에 영향을 주는 동향/혼란

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 2025년 미국 관세의 영향 : 폴리우레탄 분산액 시장

제6장 기술, 특허, 디지털, AI의 도입에 의한 전략적 파괴

- 주요 신기술

- 보완적 기술

- 인접 기술

- 기술/제품 로드맵

- 특허 분석

- 미래의 응용

- AI/생성형 AI가 폴리우레탄 분산액 시장에 미치는 영향

- 성공 사례와 실제 세계로의 응용

제7장 지속가능성과 규제 상황

- 지역 규제 및 규정 준수

- 지속가능성에 대한 노력

- 지속가능성에 미치는 영향과 규제 정책의 노력

- 인증, 라벨, 환경 기준

제8장 고객 정세와 구매행동

- 의사결정 프로세스

- 구매자의 이해관계자와 구매평가기준

- 채용 장벽과 내부 과제

- 다양한 최종 이용 산업으로부터의 미충족 수요

- 시장 수익성

제9장 폴리우레탄 분산액 시장(유형별)

- 무용제 폴리우레탄 분산액

- 저용제 폴리우레탄 분산액

제10장 폴리우레탄 분산액 시장(화학 구조별)

- 음이온성 폴리우레탄 분산액

- 양이온성 폴리우레탄 분산액

- 비이온성 폴리우레탄 분산액

- 자기 가교 폴리우레탄 분산액

- 하이브리드 폴리우레탄 분산액

제11장 폴리우레탄 분산액 시장(기능성별)

- 1성분(1) 시스템

- 2성분(2K) 시스템

제12장 폴리우레탄 분산액 시장(용도별)

- 페인트 및 코팅

- 접착제 및 실란트

- 가죽 제조 및 마감

- 섬유 마감

- 기타

제13장 폴리우레탄 분산액 시장(지역별)

- 유럽

- 독일

- 프랑스

- 이탈리아

- 스페인

- 영국

- 기타

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타

- 중동 및 아프리카

- GCC 국가

- 남아프리카

- 기타

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타

제14장 경쟁 구도

- 개요

- 주요 진입기업의 전략/강점

- 수익 분석

- 시장 점유율 분석

- 브랜드 비교

- 기업 평가 매트릭스 : 주요 진입기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 기업 평가와 재무지표

- 경쟁 시나리오

제15장 기업 프로파일

- 주요 진출기업

- COVESTRO AG

- BASF

- DOW

- WANHUA

- LUBRIZOL

- MITSUI CHEMICALS, INC.

- ALBERDINGK BOLEY GMBH

- PERSTORP HOLDING AB(PETRONAS CHEMICALS GROUP)

- STAHL HOLDINGS BV

- UBE CORPORATION

- 기타 기업

- DIC CORPORATION

- ALLNEX GMBH

- LAMBERTI SPA

- POLYNT SPA

- CHASE CORP.

- RUDOLF GMBH

- CL HAUTHAWAY & SONS CORP

- MICHELMAN, INC.

- NANPAO RESINS CHEMICAL GROUP

- INCOREZ

- SNP, INC.

- TAIWAN PU CORPORATION

- SIWOPUD

- VCM POLYURETHANES PVT. LTD

- KAMSONS POLYMERS LIMITED

제16장 조사 방법

제17장 부록

JHS 26.02.09The polyurethane dispersions market is projected to reach USD 4.34 billion by 2030 from USD 3.00 billion in 2025, at a CAGR of 7.7% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Kiloton) |

| Segments | Type, Chemistry, Functionality, Application, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

Polyurethane dispersions (PUDs) are increasingly being adopted across various industries, including automotive, construction, textiles, adhesives, leather finishing, and wood coatings. One major factor driving this trend is the implementation of stricter environmental regulations and the rapid phase-out of solvent-based polyurethane systems. Regulatory agencies, such as the Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA), as well as regional VOC directives like REACH and the EU DECO-PAINT DIRECTIVE (2004/42/EC), are enforcing lower emissions standards, prompting manufacturers to switch to waterborne PUD technologies. Modern hybrid, anionic, and cationic PUDs offer a range of advantages, including excellent film-forming capabilities, mechanical durability against physical stressors, chemical resistance, strong adhesion to surfaces, and low VOC levels, all while ensuring safer handling methods. High-performance coating systems that utilize these types of PUDs are found in various sectors, including automotive OEMs, leather finishing, waterproof textiles, industrial wood coatings, and flexible packaging adhesives.

"Solvent-free polyurethane dispersions are projected to be the fastest-growing type during the forecast period."

Solvent-free polyurethane solutions are projected to grow rapidly in the PUD market due to increasing demand for environmentally friendly products with low VOC content. These solutions, which do not use organic solvents, offer superior physical properties, chemical resistance, and film formation compared to traditional options. Their zero-solvent content makes them ideal for sensitive applications, such as leather, textiles, packaging, wood coatings, and automotive interiors. With rising regulatory pressures to reduce VOC emissions, advancements in polycarbonate polyols and renewable feedstocks are enhancing the durability and performance of solventless PUDs. As manufacturers shift towards greener alternatives without compromising efficiency, solvent-free polyurethane solutions are driving growth in the global PUD market.

"Paints & coatings are projected to be the fastest-growing applications in the market."

The market is expected to grow rapidly due to the rising demand for low-VOC and eco-friendly coatings in sectors such as construction, automotive, and wood. PUD coatings provide excellent adhesion, chemical and moisture resistance, and flexibility, making them a preferred alternative to solvent-based options amid stricter emission regulations. Their superior durability and improved aesthetics enhance their use in architectural coatings, automotive refinishing, and protective finishes. Additionally, the shift toward sustainable manufacturing practices and the development of waterborne and solvent-free formulations will further drive the adoption of PUD. As industries seek greener technologies and better performance, PUDs will play a crucial role in advancing next-generation coatings, ensuring strong market growth.

"Asia Pacific is projected to be the fastest-growing region in the polyurethane dispersions market during the forecast period."

The rapid industrialization, increased manufacturing opportunities, and rising demand for eco-friendly coating technologies are driving market growth in the Asia Pacific. Countries such as China, India, South Korea, and Indonesia have seen significant growth in sectors like automotive, textile, construction, and packaging, which are major consumers of waterborne PUD-based coatings, adhesives, and sealants. The shift toward low-VOC, solvent-free, and sustainable formulations has been fueled by stricter environmental regulations, such as China's VOC limits, and government-supported Green Chemistry initiatives in India. These factors are increasing the demand for PUD products throughout the region. Furthermore, government investments in building infrastructure, the expansion of local production capabilities, and the presence of competitive manufacturers are also contributing to the market's growth.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the PUDs marketplace.

By Company Type: Tier 1: 40%, Tier 2: 30%, and Tier 3: 30%

By Designation: Directors: 30%, Managers: 20%, and Others: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and the Middle East & Africa: 20%

Covestro AG (Germany), BASF (Germany), Dow (US), Wanhua (China), Lubrizol (US), Mitsui Chemicals, Inc. (Japan), Alberdingk Boley GmbH (Germany), Perstorp (Sweden), Stahl Holdings B.V. (Netherlands), and UBE Corporation (Japan) are some companies covered in the report.

The study includes an in-depth competitive analysis of these key players in the polyurethane dispersions market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the polyurethane dispersions market based on by type (solvent-free polyurethane dispersions, low-solvent polyurethane dispersions), by chemistry (anionic polyurethane dispersions, cationic polyurethane dispersions, nonionic polyurethane dispersions, self-crosslinking polyurethane dispersions, hybrid polyurethane dispersions), by functionality (one-component (1k) systems, two-component (2k) systems), by application (paints & coatings, adhesives & sealants, leather manufacturing & finishing, textile finishing). The report's scope encompasses detailed information regarding the drivers, restraints, challenges, and opportunities that influence the growth of the polyurethane dispersions market. A detailed analysis of key industry players has been conducted to provide insights into their business overview, products offered, and key strategies, including mergers, acquisitions, product launches, and expansions, associated with the polyurethane dispersions market. This report covers a competitive analysis of upcoming startups in the polyurethane dispersions market ecosystem.

Reasons to Buy the Report

The report will provide market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall polyurethane dispersions market and its subsegments. It will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points.

- Analysis of key drivers (accelerating adoption of low-VOC and environmentally compliant coatings, growing demand from automotive, construction, and industrial applications, expansion in synthetic leather and functional textile finishing), restraints (higher production costs limiting wider adoption, limited solvent and chemical resistance in certain grades), opportunities (expanding the bio-based & circular polyurethane dispersions market through sustainable innovation, unlocking high-performance industrial & specialty applications with advanced polyurethane dispersions), and challenges (sustaining performance while complying with environmental norms, navigating fierce cost competition from low-cost regional polyurethane dispersions producers).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the polyurethane dispersions market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the polyurethane dispersions market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the polyurethane dispersions market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Covestro AG (Germany), BASF (Germany), Dow (US), Wanhua (China), Lubrizol (US), Mitsui Chemicals, Inc. (Japan), Alberdingk Boley GmbH (Germany), Perstorp (Sweden), Stahl Holdings B.V. (Netherlands), and UBE Corporation (Japan), among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN POLYURETHANE DISPERSIONS MARKET

- 3.2 POLYURETHANE DISPERSIONS MARKET, BY TYPE

- 3.3 POLYURETHANE DISPERSIONS MARKET, BY CHEMISTRY

- 3.4 POLYURETHANE DISPERSIONS MARKET, BY FUNCTIONALITY

- 3.5 POLYURETHANE DISPERSIONS MARKET, BY APPLICATION

- 3.6 POLYURETHANE DISPERSIONS MARKET, BY KEY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Accelerating adoption of low-VOC and environmentally compliant coatings

- 4.2.1.2 Growing demand from automotive, construction, and industrial applications

- 4.2.1.3 Expansion in synthetic leather and functional textile finishing

- 4.2.2 RESTRAINTS

- 4.2.2.1 Higher production costs limiting wider adoption

- 4.2.2.2 Limited solvent and chemical resistance in certain grades

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expanding bio-based & circular polyurethane dispersions market through sustainable innovation

- 4.2.3.2 Unlocking high-performance industrial & specialty applications

- 4.2.4 CHALLENGES

- 4.2.4.1 Sustaining performance while complying with environmental norms

- 4.2.4.2 Navigating fierce cost competition from low-cost regional polyurethane dispersions producers

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN POLYURETHANE DISPERSIONS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 PRICING ANALYSIS

- 5.4.1.1 Pricing analysis based on application

- 5.4.1.2 Pricing analysis based on region

- 5.4.1 PRICING ANALYSIS

- 5.5 TRADE ANALYSIS

- 5.5.1 EXPORT SCENARIO (HS CODE 390950)

- 5.5.2 IMPORT SCENARIO (HS CODE 390950)

- 5.6 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.7.1 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 COVESTRO & JOWAT (FURNITURE LAMINATION USING DISPERCOLL U)

- 5.9.2 BASF (JONCRYL PUD SYSTEMS FOR INDUSTRIAL WOOD COATINGS)

- 5.9.3 PERMUTHANE WATERBORNE POLYURETHANE DISPERSIONS-STAHL (PUDS FOR AUTOMOTIVE SYNTHETIC LEATHER)

- 5.10 IMPACT OF 2025 US TARIFF: POLYURETHANE DISPERSIONS MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 US

- 5.10.4.2 China

- 5.10.4.3 Europe

- 5.10.4.4 Mexico

- 5.10.5 END-USE INDUSTRY IMPACT

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 LOW-SOLVENT AND WATERBORNE POLYURETHANE DISPERSIONS

- 6.1.2 FUNCTIONAL ADDITIVES FOR ENHANCED PERFORMANCE

- 6.1.3 SELF-CROSSLINKING AND HYBRID POLYURETHANE SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 BIO-BASED POLYURETHANE PRECURSORS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 SMART COATINGS AND FUNCTIONAL INTEGRATION

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.4.2 MID-TERM (2027-2030) | EXPANSION & INTEGRATION

- 6.4.3 LONG-TERM (2030-2035+) | MATURITY & ADVANCED SYSTEMS

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 METHODOLOGY

- 6.5.3 POLYURETHANE DISPERSIONS MARKET, PATENT ANALYSIS, 2015-2024

- 6.6 FUTURE APPLICATIONS

- 6.6.1 SMART AND FUNCTIONAL COATINGS FOR INDUSTRY 4.0 APPLICATIONS

- 6.6.2 ECO-FRIENDLY AND BIO-BASED POLYURETHANE DISPERSIONS

- 6.6.3 HIGH-PERFORMANCE COATINGS FOR ADVANCED MATERIALS

- 6.6.4 FUNCTIONAL ADHESIVES AND COATINGS FOR MEDICAL AND PACKAGING APPLICATIONS

- 6.7 IMPACT OF AI/GEN AI ON POLYURETHANE DISPERSIONS MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN POLYURETHANE DISPERSION MANUFACTURING

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN POLYURETHANE DISPERSIONS MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN POLYURETHANE DISPERSIONS MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 AUTOMOTIVE INTERIOR COATINGS & ADHESIVES

- 6.8.2 SUSTAINABLE INTERIOR WALL & FURNITURE COATINGS

- 6.8.3 WOOD AND FURNITURE COATINGS WITH ENHANCED SURFACE FEEL

- 6.8.4 FUNCTIONAL AND ACOUSTIC COATINGS (ACADEMIC/R&D)

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF POLYURETHANE DISPERSIONS

- 7.2.1.1 Carbon Impact Reduction

- 7.2.1.2 Eco-Applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF POLYURETHANE DISPERSIONS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES BY APPLICATION

9 POLYURETHANE DISPERSIONS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 SOLVENT-FREE POLYURETHANE DISPERSIONS

- 9.2.1 LOW IMPACT ON ENVIRONMENT TO DRIVE MARKET

- 9.3 LOW-SOLVENT POLYURETHANE DISPERSIONS

- 9.3.1 VARIOUS ATTRIBUTES LIKELY TO INFLUENCE MARKET

10 POLYURETHANE DISPERSIONS MARKET, BY CHEMISTRY

- 10.1 INTRODUCTION

- 10.2 ANIONIC POLYURETHANE DISPERSIONS

- 10.2.1 WIDESPREAD INDUSTRIAL ADOPTION DRIVEN BY VERSATILITY, COST-EFFICIENCY, AND REGULATORY COMPLIANCE

- 10.3 CATIONIC POLYURETHANE DISPERSIONS

- 10.3.1 GROWING USE IN SPECIALTY APPLICATIONS SUPPORTED BY SUPERIOR SUBSTRATE ADHESION AND ANTIMICROBIAL PERFORMANCE

- 10.4 NONIONIC POLYURETHANE DISPERSIONS

- 10.4.1 INCREASING DEMAND IN HIGH-TEMPERATURE AND SPECIALIZED PLUMBING APPLICATIONS TO PROPEL MARKET

- 10.5 SELF-CROSSLINKING POLYURETHANE DISPERSIONS

- 10.5.1 RISING FOCUS ON HIGH-DURABILITY, LOW-VOC COATINGS ACCELERATES ADOPTION OF SELF-CROSSLINKING SYSTEMS

- 10.6 HYBRID POLYURETHANE DISPERSIONS

- 10.6.1 GROWING PREFERENCE FOR COST-OPTIMIZED, PERFORMANCE-ENHANCED SYSTEMS DRIVES HYBRID PUD ADOPTION

11 POLYURETHANE DISPERSIONS MARKET, BY FUNCTIONALITY

- 11.1 INTRODUCTION

- 11.2 ONE-COMPONENT (1) SYSTEMS

- 11.2.1 GROWING PREFERENCE FOR EASY-TO-APPLY, LOW-VOC COATINGS TO DRIVE EXPANSION OF 1K POLYURETHANE DISPERSIONS TECHNOLOGIES

- 11.3 TWO-COMPONENT (2K) SYSTEMS

- 11.3.1 RISING NEED FOR HIGH-DURABILITY AND CHEMICALLY RESISTANT COATINGS TO DRIVE ADOPTION

12 POLYURETHANE DISPERSIONS MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 PAINTS & COATINGS

- 12.2.1 SHIFT TOWARD LOW-VOC, HIGH-PERFORMANCE FINISHES TO ACCELERATE ADOPTION OF WATERBORNE POLYURETHANE DISPERSION COATINGS

- 12.2.2 AUTOMOTIVE COATING

- 12.2.3 WOOD COATING

- 12.2.4 FLOOR COATING

- 12.2.5 HYGIENE COATING

- 12.3 ADHESIVES & SEALANTS

- 12.3.1 FAVORABLE ATTRIBUTES OF POLYURETHANE DISPERSIONS LIKELY TO DRIVE THEIR USE

- 12.4 LEATHER MANUFACTURING & FINISHING

- 12.4.1 GROWING APPLICATIONS IN LEATHER INDUSTRY TO DRIVE MARKET

- 12.5 TEXTILE FINISHING

- 12.5.1 PHYSICAL AND MECHANICAL PROPERTIES OF POLYURETHANE DISPERSIONS TO INCREASE APPLICATIONS

- 12.6 OTHER APPLICATIONS

- 12.6.1 GLASS FIBER SIZING

- 12.6.2 MEDICAL FILMS & GLOVES

- 12.6.3 COSMETICS

- 12.6.4 GRAPHIC INKS

- 12.6.5 PAPER FINISHING

13 POLYURETHANE DISPERSIONS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 EUROPE

- 13.2.1 GERMANY

- 13.2.1.1 Growing renovation activities to accelerate applications in paints and coatings applications

- 13.2.2 FRANCE

- 13.2.2.1 Expanding construction and foreign investment to drive market

- 13.2.3 ITALY

- 13.2.3.1 Industrial rebound to expand market

- 13.2.4 SPAIN

- 13.2.4.1 Rising industrial investments and strong automotive supply chain to accelerate market growth

- 13.2.5 UK

- 13.2.5.1 Major infrastructure investments and automotive expansion to drive market

- 13.2.6 REST OF EUROPE

- 13.2.1 GERMANY

- 13.3 ASIA PACIFIC

- 13.3.1 CHINA

- 13.3.1.1 Rapid industrialization and infrastructure development to drive market growth

- 13.3.2 JAPAN

- 13.3.2.1 Urban redevelopment and automotive leadership to propel market growth

- 13.3.3 INDIA

- 13.3.3.1 Government initiatives and industrial growth to fuel market expansion

- 13.3.4 SOUTH KOREA

- 13.3.4.1 Strategic infrastructure investments and EV advancements to boost demand

- 13.3.5 REST OF ASIA PACIFIC

- 13.3.1 CHINA

- 13.4 MIDDLE EAST & AFRICA

- 13.4.1 GCC COUNTRIES

- 13.4.1.1 Saudi Arabia

- 13.4.1.1.1 Economic diversification and mega projects propel market

- 13.4.1.2 UAE

- 13.4.1.2.1 Construction activities and automotive initiatives to drive demand

- 13.4.1.3 Rest of GCC countries

- 13.4.1.1 Saudi Arabia

- 13.4.2 SOUTH AFRICA

- 13.4.2.1 Government initiatives and industrial growth to increase consumption

- 13.4.3 REST OF MIDDLE EAST & AFRICA

- 13.4.1 GCC COUNTRIES

- 13.5 NORTH AMERICA

- 13.5.1 US

- 13.5.1.1 Strengthening construction and EV manufacturing to drive market growth

- 13.5.2 CANADA

- 13.5.2.1 Net-Zero push and EV infrastructure investments to increase demand

- 13.5.3 MEXICO

- 13.5.3.1 Growth of construction and water infrastructure sectors to fuel market

- 13.5.1 US

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Rapid industrialization to influence market growth

- 13.6.2 ARGENTINA

- 13.6.2.1 Improving economic conditions to support market growth

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS

- 14.4 MARKET SHARE ANALYSIS

- 14.5 BRAND COMPARISON

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.6.5.1 Company footprint

- 14.6.5.2 Region footprint

- 14.6.5.3 Type footprint

- 14.6.5.4 Chemistry footprint

- 14.6.5.5 Functionality footprint

- 14.6.5.6 Applications footprint

- 14.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.7.5.1 Detailed list of key startups/SMEs

- 14.7.5.2 Competitive benchmarking of key startups/SMEs

- 14.8 COMPANY VALUATION AND FINANCIAL METRICS

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 COVESTRO AG

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 BASF

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.3.2 Expansion

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 DOW

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 WANHUA

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Expansions

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 LUBRIZOL

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 MITSUI CHEMICALS, INC.

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent development

- 15.1.6.3.1 Expansions

- 15.1.6.4 MnM view

- 15.1.7 ALBERDINGK BOLEY GMBH

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.7.4 MnM view

- 15.1.8 PERSTORP HOLDING AB (PETRONAS CHEMICALS GROUP)

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 MnM view

- 15.1.9 STAHL HOLDINGS B.V.

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Expansions

- 15.1.9.4 MnM view

- 15.1.10 UBE CORPORATION

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.4 MnM view

- 15.1.1 COVESTRO AG

- 15.2 OTHER PLAYERS

- 15.2.1 DIC CORPORATION

- 15.2.2 ALLNEX GMBH

- 15.2.3 LAMBERTI S.P.A.

- 15.2.4 POLYNT S.P.A

- 15.2.5 CHASE CORP.

- 15.2.6 RUDOLF GMBH

- 15.2.7 C. L. HAUTHAWAY & SONS CORP

- 15.2.8 MICHELMAN, INC.

- 15.2.9 NANPAO RESINS CHEMICAL GROUP

- 15.2.10 INCOREZ

- 15.2.11 SNP, INC.

- 15.2.12 TAIWAN PU CORPORATION

- 15.2.13 SIWOPUD

- 15.2.14 VCM POLYURETHANES PVT. LTD

- 15.2.15 KAMSONS POLYMERS LIMITED

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key industry insights

- 16.1.2.3 Breakdown of primary interviews

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.3 DATA TRIANGULATION

- 16.4 RESEARCH ASSUMPTIONS

- 16.5 LIMITATIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS