|

시장보고서

상품코드

1919588

그린 수소 시장(-2032년) : 기술(알칼리 전해, PEM 전해), 재생에너지원(풍력, 태양광), 최종 사용 산업(모빌리티, 전력, 화학, 산업, 그리드 주입), 지역별Green Hydrogen Market By Technology (Alkaline, PEM), Renewable Source (Wind, Solar), End-use Industry (Mobility, Power, Chemical, Industrial, Grid Injection), and Region (North America, Europe, APAC, MEA, and Latin America) - Global Forecast to 2032 |

||||||

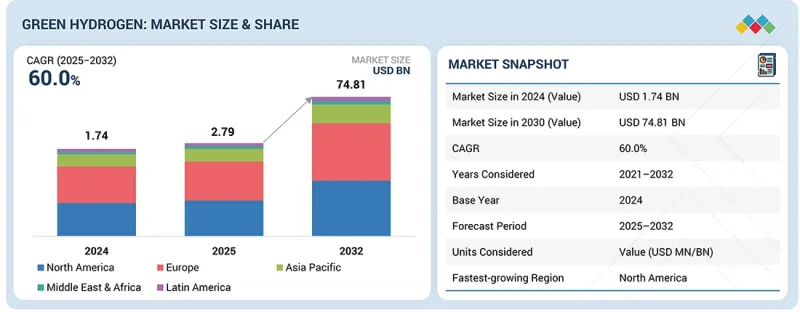

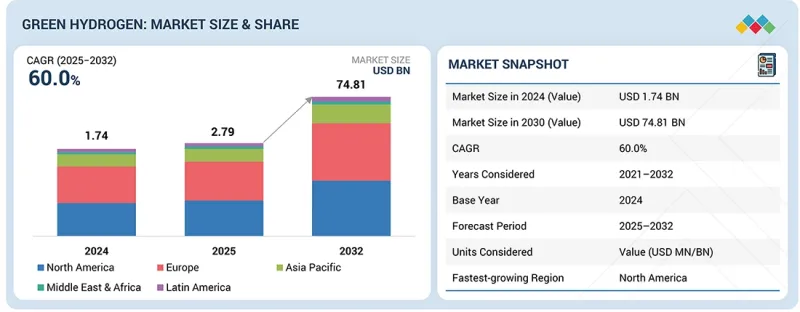

세계의 그린 수소 시장 규모는 2025년 27억 9,000만 달러에서 예측 기간 동안 CAGR 60.0%로 성장하여 2032년에는 748억 1,000만 달러에 이를 것으로 전망됩니다. 시장을 견인하는 주요 요인으로는 모든 신재생 에너지원에서의 제조비용 저하, 전해 기술 진보, 전력업계 및 연료전지 전기자동차에서의 수요 증가 등이 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2032년 |

| 단위 | 금액(달러) |

| 부문 | 재생에너지원, 기술, 최종 사용자 산업, 유통 채널, 제조 규모, 순도 수준, 저장, 지역 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 중동, 아프리카, 남미 |

그린 수소는 화학, 이동성, 계통 연계, 전력 산업 등 다양한 산업 분야에서 응용되고 있습니다. 제로 방출 제조 공정은 기존의 회색 수소, 브라운 수소 및 블루 수소를 대체하는 것으로 점점 더 주목을 받고 있습니다. 기술 진보로 그린 수소의 비용 경쟁력도 향상되었습니다. 이러한 지속가능한 연료원은 다양한 최종사용자 산업에서 화석연료를 대체하는 현실적인 옵션으로 부상하고 있습니다.

"기술별로는 예측 기간 동안 알칼리 전해 기반 부문이 금액 기준으로 최대 점유율을 차지할 전망"

알칼리 전해의 그린 수소 부문은 신뢰성, 확장성 및 저비용성으로 인해 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 이 기술에서는 수산화칼륨 등의 알칼리 전해질을 이용하여 물을 분해하고, 수소 이온이 전해질 중에 천천히 확산하기 때문에 가스 교차가 최소화되어 고순도의 수소를 제조합니다. 배터리 설계와 일반적인 비귀금속 재료의 사용은 새로운 전해법에 비해 설비 투자 비용과 유지 관리 비용을 모두 낮게 유지합니다. 동시에 확립된 제조 공정을 통해 대규모 신속한 배치가 가능합니다. 알칼리 전해 장치는 다양한 전력 조건 하에서 효율적으로 작동하므로 풍력 및 태양광과 같은 재생에너지원과 호환됩니다. 스택의 긴 수명, 운전 안정성, 연속 산업 제조와의 호환성 등의 이점으로 알칼리 전해는 성장하는 그린 수소 시장에서 가장 실용적이고 상업적으로 매력적인 기술 중 하나가 되었습니다.

"최종 사용자 산업별로는 모빌리티 분야가 예측 기간 동안 가장 빠르게 성장할 전망"

철도, 도로, 항공, 선박 등 다양한 운송 모드에서 배터리 기술의 성능 요구 사항을 충족하는 것이 점점 어려워지고 있습니다. 그린 수소는 에너지 밀도가 높기 때문에 항속 거리가 대폭 연장되는 동시에 연료 보급 시간도 단축되고, 연료전지 전기자동차(FCEV)는 대형 트럭, 버스, 열차, 항공기, 선박에 자연스러운 선택이 됩니다. 이를 통해 사업자는 최소한의 다운타임으로 차량을 운영할 수 있어 물류, 대중교통, 산업환경에서 이동성의 우선 옵션이 됩니다. 그린 수소 제조 기술의 급속한 진보, 연료 보급 인프라의 확충, 자동차 제조업체, 에너지 공급자, 플릿 사업자간의 제휴가 다양한 수송 모드에 있어서의 그린 수소 도입을 가속시키고 있습니다. 또한 정부 우대 정책과 국가 탈탄소화 전략이 조기 도입을 뒷받침하고 있습니다.

"유럽 시장이 예측 기간 동안 금액과 수량에서 가장 규모가 큰 지역 시장이 될 전망"

유럽은 세계 최대 지역으로 그린 수소 시장을 선도하고 있습니다. 견고한 산업 기반, 첨단 기술력, 깊은 탈탄소화에 대한 매우 명확한 헌신이 촉진요인입니다. 이 지역에서 설정된 야심적인 기후 목표는 재생에너지 용량과 그린 수소 제조에 대한 대규모 투자를 가속화하고 있습니다. 유럽은 또한 성숙한 제조 에코시스템을 갖고 있으며, 다수의 확립된 전해 장치 제조업체, 엔지니어링 기업, 기술 개발 기업이 확고한 지위를 구축하고 있습니다. 이들은 각각의 밸류체인에서 혁신 추진, 효율성 향상 및 비용 절감 달성에 기여하고 있습니다. 수소 인프라의 확충, 대규모 실증 프로젝트의 개발, 그린 수소의 산업 프로세스, 전력 시스템 및 모빌리티에 통합을 위한 공적, 민간의 다액의 투자가 쏟아지고 있습니다. 이러한 요소들이 함께, 유럽은 그린 수소의 개발 및 보급에 있어 세계의 허브의 중심에 자리잡고 있습니다.

본 보고서에서는 세계의 그린 수소 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이와 예측, 각종 구분, 지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 프로파일 등을 정리했습니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 중요 인사이트

제4장 시장 개요

- 시장 역학

- 성장 촉진요인

- 억제요인

- 기회

- 과제

- 미충족 요구와 화이트 스페이스

- 관련 시장 및 이업종과의 분야 횡단적 기회

- Tier 1/2/3 기업의 전략적 움직임

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제 전망

- 밸류체인 분석

- 그린 수소 시장을 위한 생태계

- 가격 분석

- 무역 분석

- 2025-2026년의 주된 회의와 이벤트

- 동향/혼란의 영향

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 2025년 미국 관세의 영향 - 그린 수소 시장

- 주요 관세율

제6장 기술, 특허, 디지털, AI 도입을 통한 전략적 혁신

- 주요 신기술

- PEM(양성자 교환막) 전해 장치

- 알칼리 전해 장치

- 보완적 기술

- SOEC(고체 산화물형 전해 셀) 전해 장치

- AEM(음이온 교환막) 전해 장치

- 기술/제품 로드맵

- 특허 분석

- 미래의 응용

- 그린 수소 시장에서 AI의 영향

- 성공 사례와 실제 세계로의 응용

제7장 지속가능성과 규제상황

- 지역 규제 및 규정 준수

- 지속가능성에 대한 노력

- 지속가능성에 미치는 영향과 규제 정책의 노력

- 인증, 라벨, 환경 기준

제8장 고객정세와 구매행동

- 의사결정 프로세스

- 주요 이해관계자와 구매 기준

- 채용 장벽과 내부 과제

- 다양한 최종 사용자의 미충족 요구

- 시장 수익성

제9장 그린 수소 시장 : 유통 채널별

- 파이프라인

- 화물

제10장 그린 수소 시장 : 제조 규모별

- 소규모(1MW 미만)

- 중규모(1-10MW)

- 대규모(10MW 초과)

제11장 그린 수소 시장 : 순도별

- 초고순도

- 고순도

- 표준 순도

제12장 그린 수소 시장 : 저장별

- 압축가스 저장

- 액체 수소 저장

- 금속 수소화물 저장

- 기타 저장 옵션(화학 수소화물 저장, 극저온 압축 수소 저장)

제13장 그린 수소 시장 : 재생 에너지원별

- 풍력에너지

- 태양에너지

- 기타

제14장 그린 수소 시장 : 기술별

- 알칼리 전해

- PEM 전해

제15장 그린 수소 시장 : 최종 사용자 산업별

- 이동성

- 화학

- 전력

- 그리드 주입

- 산업

- 기타

제16장 그린 수소 시장 : 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 아시아태평양

- 중국

- 일본

- 호주

- 기타

- 유럽

- 독일

- 오스트리아

- 덴마크

- 영국

- 프랑스

- 기타

- 남미

- 브라질

- 아르헨티나

- 기타

- 중동 및 아프리카

- GCC 국가

- 기타

제17장 경쟁 구도

- 주요 기업의 전략/유력 기업

- 수익 분석

- 시장 점유율 분석

- 브랜드/제품 비교

- SIEMENS ENERGY

- AIR LIQUIDE

- AIR PRODUCTS

- ENGIE

- UNIPER

- 기업 평가와 재무지표

- 기업 평가 매트릭스 : 주요 기업

- 기업 평가 매트릭스 : 스타트업/중소기업

- 경쟁 벤치마킹 : 스타트업/중소기업

- 경쟁 시나리오

제18장 기업 프로파일

- 주요 기업

- AIR LIQUIDE

- LINDE PLC

- AIR PRODUCTS AND CHEMICALS, INC.

- ENGIE

- TOSHIBA ENERGY SYSTEMS & SOLUTIONS CORPORATION

- UNIPER SE

- SIEMENS ENERGY

- LHYFE

- NEL

- ORSTED

- BLOOM ENERGY

- CUMMINS INC.

- H&R GROUP

- W2E TECHNOLOGY, LLC

- SINOSYNERGY

- 기타 기업

- ABO ENERGY KGAA

- GREEN HYDROGEN SYSTEMS

- SALZGITTER AG

- RWE

- ADANI GROUP

- HYDROGENEA GMBH

- WAAREE ENERGIES LTD

- IBERDROLA, SA

- ENEL SPA

- ENVISION GROUP

- HYNAMICS GROUPE(EDF)

- ACWA POWER

- THE STATE ATOMIC ENERGY CORPORATION ROSATOM

- ENEGIX ENERGY

- ACME GROUP

- GEOPURA LTD.

- IWATANI CORPORATION

- IVYS ENERGY SOLUTIONS

- ENAPTER SRL

- ATAWEY

- HIRINGA ENERGY LIMITED

- PLUG POWER, INC.

- ITM POWER PLC.

제19장 조사 방법

제20장 부록

JHS 26.02.09The green hydrogen market is projected to grow from USD 2.79 billion in 2025 to USD 74.81 billion by 2032, at a CAGR of 60.0% during the forecast period. Several key factors are propelling the market for green hydrogen. These include the decreasing cost of renewable energy production from all sources, advancements in electrolysis technologies, and a rising demand from the power industry and fuel cell electric vehicles.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Renewable Source, Technology, End-Use Industry, Distribution Channel, Production Scale, Purity Level, Storage, And Region |

| Regions covered | Asia Pacific, Europe, North America, the Middle East & Africa, and South America |

Green hydrogen has applications across various industries, including chemicals, mobility, grid injection, the power industry, and others. It is increasingly being seen as a replacement for conventional gray, brown, and blue hydrogen due to its zero-emission production process. Technological advancements have also made green hydrogen more cost-competitive. This sustainable fuel source is emerging as a viable alternative to fossil fuels across various end-use industries.

"By technology, the alkaline electrolysis-based green hydrogen segment is estimated to hold the largest share, in terms of value, during the forecast period."

The alkaline electrolysis-based green hydrogen segment is expected to hold the largest market share due to its reliability, scalability, and low cost. In this technology, an alkaline electrolyte, such as potassium hydroxide, is used to split water, producing high-purity hydrogen with minimal gas crossover as hydrogen ions diffuse slowly into the electrolyte. Its cell design and use of common, non-precious materials keep both capital and maintenance costs lower compared to newer electrolysis methods. At the same time, well-established manufacturing processes allow for rapid deployment at scale. Alkalinizers operate efficiently in varying power conditions, making them compatible with renewable sources such as wind and solar. Advantages such as long stack lifetimes, operational stability, and compatibility with continuous industrial production make alkaline electrolysis one of the most practical and commercially attractive technologies in the growing green hydrogen market.

"By end-use industry, the mobility segment is estimated to be the fastest-growing segment of the data green hydrogen market during the forecast period."

The mobility segment is expected to be the fastest-growing segment for green hydrogen during the forecast period. The performance requirements for battery technologies are becoming increasingly challenging to meet across various modes of transportation, including rail, road, aviation, and shipping. Green hydrogen has a higher energy content, which enables much longer ranges coupled with shorter refueling durations, making fuel cell electric vehicles the natural choice for heavy-duty trucks, buses, trains, aircraft, and ships. Operators can thus operate vehicles with minimal downtime, making them a preferred choice for logistics, public transport, and mobility in industrial environments. Rapid improvements in green hydrogen production, the expansion of refueling infrastructure, and cooperation among vehicle manufacturers, energy providers, and fleet operators are accelerating the adoption of green hydrogen across various modes of transportation. Additionally, favorable government policies and national decarbonization strategies are encouraging early deployment.

"The green hydrogen market in Europe is projected to be the largest regional market, in terms of value and volume, during the forecast period."

Europe leads the global green hydrogen market as the largest region. A strong industrial base, advanced technological capabilities, and a very transparent commitment to deep decarbonization are the driving factors. Ambitious climate targets set in the region have accelerated large-scale investments in renewable energy capacity and green hydrogen production. Europe also possesses a mature manufacturing ecosystem, with an established presence of several established electrolyzer producers, engineering firms, and technology developers that contribute to driving innovation, increasing efficiency, and achieving cost reductions within their respective value chains. Significant public and private investments are being directed towards the expansion of hydrogen infrastructure, the development of large demonstration projects, and the integration of green hydrogen into industrial operations, power systems, and mobility. Together, these factors position Europe at the center of all global hubs for the development and deployment of green hydrogen.

Profile break-up of primary participants for the report:

- By Company Type: Tier 1 - 45%, Tier 2 - 22%, and Tier 3 - 33%

- By Designation: C-Level Executives- 50%, Directors- 10%, and Others - 40%

- By Region: North America - 17%, Asia Pacific - 17%, Europe - 33%, Middle East & Africa - 25%, and South America - 8%

Air Liquide Engineering & Construction (Germany), Air Products and Chemicals, Inc. (US), Engie (France), Uniper SE (Germany), Siemens Energy (Germany), Lhyfe (France), Toshiba Energy Systems & Solutions Corporation (Japan), Nel (Norway), Orsted (Denmark), Bloom Energy (US), Linde plc (UK), Cummins Inc. (US), H&R Group (Germany), W2E Technology, LLC (US), SinoSynergy (China), and others are the key players in the green hydrogen market. These players have adopted various strategies, including agreements, joint ventures, and expansions, to increase their market share and business revenue.

Research Coverage:

The report defines segments and projects the size of the green hydrogen market based on renewable source, technology, end-use industry, distribution channel, production scale, purity level, storage, and region. It strategically profiles the key players and comprehensively analyzes their market share and core competencies. It also tracks and analyzes competitive developments, such as expansions, agreements, and acquisitions undertaken by them in the market.

Reasons to Buy the Report:

The report is expected to help the market leaders/new entrants by providing them with the closest approximations of revenue numbers of the green hydrogen market and its segments. This report is also expected to help stakeholders gain a deeper understanding of the market's competitive landscape, acquire valuable insights to enhance their business positions, and develop effective go-to-market strategies. It also enables stakeholders to understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of critical drivers (decarbonization targets and net-zero commitments, rapid growth of renewable energy capacity, rising demand for clean mobility), restraints (high production costs, limited infrastructure and regulatory and standardization issues), opportunities (emergence of hydrogen hubs and industrial clusters, hydrogen in heavy mobility, grid balancing and energy storage) and challenges (hydrogen storage and transport complexity, electrolyzer manufacturing constraints ) influencing the growth of the green hydrogen market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities in the green hydrogen market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the green hydrogen market across varied regions

- Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the green hydrogen market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as Air Liquide Engineering & Construction (Germany), Air Products and Chemicals, Inc. (US), Engie (France), Uniper SE (Germany), Siemens Energy (Germany), Lhyfe (France), Toshiba Energy Systems & Solutions Corporation (Japan), Nel (Norway), Orsted (Denmark), Bloom Energy (US), Linde plc (UK), Cummins Inc. (US), H&R Group (Germany), W2E Technology, LLC (US), and SinoSynergy (China) are the key players in the green hydrogen market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 INCLUSIONS & EXCLUSIONS OF STUDY

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN GREEN HYDROGEN MARKET

- 3.2 GREEN HYDROGEN MARKET, BY TECHNOLOGY AND REGION

- 3.3 GREEN HYDROGEN MARKET, BY RENEWABLE SOURCE

- 3.4 GREEN HYDROGEN MARKET, BY END-USE INDUSTRY

- 3.5 GREEN HYDROGEN MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Decarbonizing targets & net-zero commitments

- 4.2.1.2 Abundant renewable energy resources

- 4.2.1.3 Rising demand for clean mobility

- 4.2.2 RESTRAINTS

- 4.2.2.1 High production costs

- 4.2.2.2 Limited infrastructure

- 4.2.2.3 Regulatory & standardization issues

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Emergence of hydrogen hubs & industrial clusters

- 4.2.3.2 Hydrogen in heavy mobility

- 4.2.3.3 Grid balancing & energy storage

- 4.2.4 CHALLENGES

- 4.2.4.1 Hydrogen storage & transport complexity

- 4.2.4.2 Electrolyzer manufacturing constraints

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN GREEN HYDROGEN MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 THREAT OF SUBSTITUTES

- 5.1.4 THREAT OF NEW ENTRANTS

- 5.1.5 DEGREE OF COMPETITION

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 GDP

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM FOR GREEN HYDROGEN MARKET

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE, BY REGION

- 5.5.2 AVERAGE SELLING PRICE OF GREEN HYDROGEN, BY END-USE INDUSTRY

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO

- 5.6.2 EXPORT SCENARIO

- 5.7 KEY CONFERENCES & EVENTS IN 2025-2026

- 5.8 TRENDS/DISRUPTIONS IMPACT

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 EGYPT GREEN HYDROGEN/SCATEC

- 5.10.1.1 Objective

- 5.10.1.2 Challenge

- 5.10.1.3 Solution statement

- 5.10.1.4 Result

- 5.10.2 INDUSTRIAL USE CASES OF GREEN HYDROGEN: FROM STEEL TO AVIATION

- 5.10.2.1 Objective

- 5.10.2.2 Challenge

- 5.10.2.3 Solution statement

- 5.10.2.4 Result

- 5.10.3 CASE STUDY ON BENEFITS AND RISKS OF GREEN HYDROGEN PRODUCTION CO-LOCATION AT OFFSHORE WIND FARMS

- 5.10.3.1 Objective

- 5.10.3.2 Challenge

- 5.10.3.3 Solution statement

- 5.10.3.4 Result

- 5.10.1 EGYPT GREEN HYDROGEN/SCATEC

- 5.11 IMPACT OF 2025 US TARIFF - GREEN HYDROGEN MARKET

- 5.11.1 KEY TARIFF RATES

- 5.12 KEY TARIFF RATES

- 5.12.1 PRICE IMPACT ANALYSIS

- 5.12.2 IMPACT ON COUNTRY/REGION

- 5.12.2.1 US

- 5.12.2.2 Europe

- 5.12.2.3 Asia Pacific

- 5.12.3 IMPACT ON END-USE INDUSTRY

- 5.12.3.1 Mobility

- 5.12.3.2 Chemical

- 5.12.3.3 Power

- 5.12.3.4 Grid Injection

- 5.12.3.5 Industrial

- 5.12.3.6 Other End-Use Industries

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 PEM (PROTON EXCHANGE MEMBRANE) ELECTROLYZER

- 6.1.2 ALKALINE ELECTROLYZER

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 SOEC (SOLID OXIDE ELECTROLYZER CELL) ELECTROLYZER

- 6.2.2 AEM (ANION EXCHANGE MEMBRANE) ELECTROLYZER

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2030) | EARLY COMMERCIAL DEPLOYMENT

- 6.3.2 MID-TERM (2030-2040) | SCALING & COST REDUCTION

- 6.3.3 LONG-TERM (2040-2050+) | MASS DEPLOYMENT & INTEGRATION

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 METHODOLOGY

- 6.4.3 DOCUMENT TYPE

- 6.4.4 INSIGHTS

- 6.4.5 LEGAL STATUS OF PATENTS

- 6.4.6 JURISDICTION ANALYSIS

- 6.4.7 TOP APPLICANTS

- 6.4.7.1 List of major patents

- 6.5 FUTURE APPLICATIONS

- 6.5.1 POWER & ENERGY SYSTEMS

- 6.5.2 TRANSPORTATION & MOBILITY

- 6.5.3 INDUSTRIAL DECARBONIZATION

- 6.5.4 BUILDINGS & HEATING

- 6.5.5 ENERGY STORAGE & GRID SUPPORT

- 6.6 IMPACT OF ARTIFICIAL INTELLIGENCE (AI) ON GREEN HYDROGEN MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN GREEN HYDROGEN MARKET

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN GREEN HYDROGEN MARKET

- 6.6.3.1 AI-Driven Optimization for Green Hydrogen Production Efficiency

- 6.6.3.1.1 Objective

- 6.6.3.1.2 Challenge

- 6.6.3.1.3 Solution statement

- 6.6.3.1.4 Result

- 6.6.3.1 AI-Driven Optimization for Green Hydrogen Production Efficiency

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN GREEN HYDROGEN MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 YARA INTERNATIONAL

- 6.7.2 ADANI NEW INDUSTRIES LTD.

- 6.7.3 IBERDROLA

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 INTRODUCTION

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF GREEN HYDROGEN

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF GREEN HYDROGEN

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.3.1 KEY SUSTAINABILITY AND REGULATORY DEVELOPMENTS

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FOR VARIOUS END USERS

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY END-USE INDUSTRIES

9 GREEN HYDROGEN MARKET, BY DISTRIBUTION CHANNEL

- 9.1 INTRODUCTION

- 9.2 PIPELINE

- 9.2.1 COST-EFFICIENT BULK TRANSPORT

- 9.3 CARGO

- 9.3.1 LONG-DISTANCE AND INTERCONTINENTAL TRADE

10 GREEN HYDROGEN MARKET, BY PRODUCTION SCALE

- 10.1 INTRODUCTION

- 10.2 SMALL-SCALE (< 1 MW)

- 10.2.1 ON-SITE HYDROGEN GENERATION FOR MOBILITY AND MICRO-APPLICATIONS

- 10.3 MEDIUM-SCALE (1-10 MW)

- 10.3.1 GROWING DEMAND FROM EARLY INDUSTRIAL USERS

- 10.4 LARGE-SCALE (> 10 MW)

- 10.4.1 INTEGRATION WITH LARGE RENEWABLE ENERGY PROJECTS

11 GREEN HYDROGEN MARKET, BY PURITY LEVEL

- 11.1 INTRODUCTION

- 11.2 ULTRA-HIGH PURITY

- 11.2.1 INCREASING REQUIREMENT FOR FUEL CELL PERFORMANCE

- 11.3 HIGH PURITY

- 11.3.1 SHIFT FROM GRAY TO GREEN HYDROGEN IN REFINERIES

- 11.4 STANDARD PURITY

- 11.4.1 GROWING DEMAND FOR POWER GENERATION AND GRID SUPPORT

12 GREEN HYDROGEN MARKET, BY STORAGE

- 12.1 INTRODUCTION

- 12.2 COMPRESSED GAS STORAGE

- 12.2.1 PREFERRED SOLUTION FOR MOBILITY AND REFUELING INFRASTRUCTURE

- 12.3 LIQUID HYDROGEN STORAGE

- 12.3.1 HIGH ENERGY DENSITY FOR SPACE-CONSTRAINED APPLICATIONS

- 12.4 METAL HYDRIDE STORAGE

- 12.4.1 SUPPORT FOR NICHE INDUSTRIAL AND SPECIALTY APPLICATIONS

- 12.5 OTHER STORAGE OPTIONS (CHEMICAL HYDRIDE STORAGE, CRYO-COMPRESSED HYDROGEN STORAGE)

13 GREEN HYDROGEN MARKET, BY RENEWABLE SOURCE

- 13.1 INTRODUCTION

- 13.2 WIND ENERGY

- 13.2.1 RAPID EXPANSION OF OFFSHORE WIND CAPACITY

- 13.3 SOLAR ENERGY

- 13.3.1 HIGH SOLAR RESOURCE AVAILABILITY ACROSS REGIONS

- 13.4 OTHER RENEWABLE SOURCES

14 GREEN HYDROGEN MARKET, BY TECHNOLOGY

- 14.1 INTRODUCTION

- 14.2 ALKALINE ELECTROLYSIS

- 14.2.1 SCALABILITY FOR LARGE-SCALE HYDROGEN PRODUCTION

- 14.3 PEM ELECTROLYSIS

- 14.3.1 HIGH EFFICIENCY AND RAPID DYNAMIC RESPONSE

15 GREEN HYDROGEN MARKET, BY END-USE INDUSTRY

- 15.1 INTRODUCTION

- 15.2 MOBILITY

- 15.2.1 RISING ADOPTION OF FUEL CELL TECHNOLOGY IN TRANSPORTATION SECTOR

- 15.3 CHEMICAL

- 15.3.1 INCREASING DEMAND FOR ECO-FRIENDLY FUELS

- 15.4 POWER

- 15.4.1 NEED FOR SUSTAINABLE OPTIONS TO STORE EXCESS ENERGY

- 15.5 GRID INJECTION

- 15.5.1 INCREASED PENETRATION OF RENEWABLES

- 15.6 INDUSTRIAL

- 15.6.1 GROWING DEMAND FOR CLEAN ENERGY

- 15.7 OTHER END-USE INDUSTRIES

16 GREEN HYDROGEN MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 NORTH AMERICA

- 16.2.1 US

- 16.2.1.1 Growing clean fuel & mobility demand

- 16.2.2 CANADA

- 16.2.2.1 Strong and diversified energy sector

- 16.2.3 MEXICO

- 16.2.3.1 Strategic opportunity to become hydrogen export hub

- 16.2.1 US

- 16.3 ASIA PACIFIC

- 16.3.1 CHINA

- 16.3.1.1 Strong industrial decarbonization push across heavy industries

- 16.3.2 JAPAN

- 16.3.2.1 Advancing fuel cell technology leadership

- 16.3.3 AUSTRALIA

- 16.3.3.1 Abundant renewable energy resources enabling ultra-low-cost hydrogen production

- 16.3.4 REST OF ASIA PACIFIC

- 16.3.1 CHINA

- 16.4 EUROPE

- 16.4.1 GERMANY

- 16.4.1.1 High reliance on mobility and automotive sectors

- 16.4.2 AUSTRIA

- 16.4.2.1 Government focuses on developing green economy

- 16.4.3 DENMARK

- 16.4.3.1 National decarbonization strategy backed by large-scale offshore wind expansion

- 16.4.4 UK

- 16.4.4.1 Strong policy push to scale low-carbon hydrogen

- 16.4.5 FRANCE

- 16.4.5.1 Integration with Europe's hydrogen corridors and cross-border projects

- 16.4.6 REST OF EUROPE

- 16.4.1 GERMANY

- 16.5 SOUTH AMERICA

- 16.5.1 BRAZIL

- 16.5.1.1 Government-supported national hydrogen program (PNH2)

- 16.5.2 ARGENTINA

- 16.5.2.1 Growing economic status and spending on green hydrogen projects

- 16.5.3 REST OF SOUTH AMERICA

- 16.5.1 BRAZIL

- 16.6 MIDDLE EAST & AFRICA

- 16.6.1 GCC COUNTRIES

- 16.6.1.1 UAE

- 16.6.1.1.1 Increasing government spending on infrastructure development

- 16.6.1.2 Saudi Arabia

- 16.6.1.2.1 High economic and mobility industry growth

- 16.6.1.3 Rest of GCC Countries

- 16.6.1.1 UAE

- 16.6.1 GCC COUNTRIES

- 16.7 REST OF MIDDLE EAST & AFRICA

17 COMPETITIVE LANDSCAPE

- 17.1 INTRODUCTION

- 17.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 17.3 REVENUE ANALYSIS, 2024

- 17.3.1 TOP 5 PLAYERS' REVENUE ANALYSIS

- 17.4 MARKET SHARE ANALYSIS, 2024

- 17.4.1 MARKET SHARE ANALYSIS

- 17.4.1.1 Air Liquide (France)

- 17.4.1.2 Linde Plc (Ireland)

- 17.4.1.3 Air Products and Chemicals, Inc. (US)

- 17.4.1.4 ENGIE (France)

- 17.4.1.5 Toshiba Energy Systems & Solutions Corporation (Japan)

- 17.4.1 MARKET SHARE ANALYSIS

- 17.5 BRAND/PRODUCT COMPARISON

- 17.5.1 SIEMENS ENERGY

- 17.5.2 AIR LIQUIDE

- 17.5.3 AIR PRODUCTS

- 17.5.4 ENGIE

- 17.5.5 UNIPER

- 17.6 COMPANY VALUATION AND FINANCIAL METRICS

- 17.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 17.7.1 STARS

- 17.7.2 EMERGING LEADERS

- 17.7.3 PERVASIVE PLAYERS

- 17.7.4 PARTICIPANTS

- 17.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 17.7.5.1 Company footprint

- 17.7.6 REGION FOOTPRINT

- 17.7.7 RENEWABLE SOURCE FOOTPRINT

- 17.7.8 TECHNOLOGY FOOTPRINT

- 17.7.9 END-USE INDUSTRY FOOTPRINT

- 17.7.10 DISTRIBUTION CHANNEL FOOTPRINT

- 17.7.11 PRODUCTION SCALE FOOTPRINT

- 17.7.12 PURITY LEVEL FOOTPRINT

- 17.7.13 STORAGE FOOTPRINT

- 17.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 17.8.1 PROGRESSIVE COMPANIES

- 17.8.2 RESPONSIVE COMPANIES

- 17.8.3 DYNAMIC COMPANIES

- 17.8.4 STARTING BLOCKS

- 17.9 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 17.9.1 DETAILED LIST OF KEY STARTUPS/SMES

- 17.9.2 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 17.10 COMPETITIVE SCENARIO

- 17.10.1 DEALS

- 17.10.2 EXPANSIONS

- 17.10.3 OTHERS

18 COMPANY PROFILES

- 18.1 MAJOR PLAYERS

- 18.1.1 AIR LIQUIDE

- 18.1.1.1 Business overview

- 18.1.1.2 Products/Solutions/Services offered

- 18.1.1.3 Recent developments

- 18.1.1.3.1 Deals

- 18.1.1.3.2 Expansions

- 18.1.1.3.3 Other developments

- 18.1.1.4 MnM view

- 18.1.1.4.1 Right to win

- 18.1.1.4.2 Strategic choices

- 18.1.1.4.3 Weaknesses and competitive threats

- 18.1.2 LINDE PLC

- 18.1.2.1 Business overview

- 18.1.2.2 Products/Solutions/Services offered

- 18.1.2.3 Recent developments

- 18.1.2.3.1 Deals

- 18.1.2.3.2 Expansions

- 18.1.2.4 MnM view

- 18.1.2.4.1 Right to win

- 18.1.2.4.2 Strategic choices

- 18.1.2.4.3 Weaknesses and competitive threats

- 18.1.3 AIR PRODUCTS AND CHEMICALS, INC.

- 18.1.3.1 Business overview

- 18.1.3.2 Products/Solutions/Services offered

- 18.1.3.3 Recent developments

- 18.1.3.3.1 Deals

- 18.1.3.3.2 Expansions

- 18.1.3.3.3 Other developments

- 18.1.3.4 MnM view

- 18.1.3.4.1 Right to win

- 18.1.3.4.2 Strategic choices

- 18.1.3.4.3 Weaknesses and competitive threats

- 18.1.4 ENGIE

- 18.1.4.1 Business overview

- 18.1.4.2 Products/Solutions/Services offered

- 18.1.4.3 Recent developments

- 18.1.4.3.1 Deals

- 18.1.4.3.2 Expansions

- 18.1.4.4 MnM view

- 18.1.4.4.1 Right to win

- 18.1.4.4.2 Strategic choices

- 18.1.4.4.3 Weaknesses and competitive threats

- 18.1.5 TOSHIBA ENERGY SYSTEMS & SOLUTIONS CORPORATION

- 18.1.5.1 Business overview

- 18.1.5.2 Products/Solutions/Services offered

- 18.1.5.3 Recent developments

- 18.1.5.3.1 Deals

- 18.1.5.3.2 Expansions

- 18.1.5.4 MnM view

- 18.1.5.4.1 Right to win

- 18.1.5.4.2 Strategic choices

- 18.1.5.4.3 Weaknesses and competitive threats

- 18.1.6 UNIPER SE

- 18.1.6.1 Business overview

- 18.1.6.2 Products/Solutions/Services offered

- 18.1.6.3 Recent developments

- 18.1.6.3.1 Deals

- 18.1.7 SIEMENS ENERGY

- 18.1.7.1 Business overview

- 18.1.7.2 Products/Solutions/Services offered

- 18.1.7.3 Recent developments

- 18.1.7.3.1 Deals

- 18.1.7.3.2 Expansions

- 18.1.8 LHYFE

- 18.1.8.1 Business overview

- 18.1.8.2 Products/Solutions/Services offered

- 18.1.8.3 Recent developments

- 18.1.8.3.1 Deals

- 18.1.8.3.2 Expansions

- 18.1.8.3.3 Other developments

- 18.1.9 NEL

- 18.1.9.1 Business overview

- 18.1.9.2 Products/Solutions/Services offered

- 18.1.9.3 Recent developments

- 18.1.9.3.1 Deals

- 18.1.9.3.2 Expansions

- 18.1.9.3.3 Other developments

- 18.1.10 ORSTED

- 18.1.10.1 Business overview

- 18.1.10.2 Products/Solutions/Services offered

- 18.1.10.3 Recent developments

- 18.1.10.3.1 Deals

- 18.1.10.3.2 Expansions

- 18.1.10.3.3 Other developments

- 18.1.11 BLOOM ENERGY

- 18.1.11.1 Business overview

- 18.1.11.2 Products/Solutions/Services offered

- 18.1.11.3 Recent developments

- 18.1.11.3.1 Deals

- 18.1.11.3.2 Expansions

- 18.1.12 CUMMINS INC.

- 18.1.12.1 Business overview

- 18.1.12.2 Products/Solutions/Services offered

- 18.1.12.3 Recent developments

- 18.1.12.3.1 Deals

- 18.1.12.3.2 Expansions

- 18.1.12.3.3 Other developments

- 18.1.13 H&R GROUP

- 18.1.13.1 Business overview

- 18.1.13.2 Products/Solutions/Services offered

- 18.1.13.3 Recent developments

- 18.1.13.3.1 Deals

- 18.1.14 W2E TECHNOLOGY, LLC

- 18.1.14.1 Business overview

- 18.1.14.2 Products/Solutions/Services offered

- 18.1.14.3 Recent developments

- 18.1.15 SINOSYNERGY

- 18.1.15.1 Business overview

- 18.1.15.2 Products/Solutions/Services offered

- 18.1.15.3 Recent developments

- 18.1.15.3.1 Product Launches

- 18.1.15.3.2 Deals

- 18.1.1 AIR LIQUIDE

- 18.2 OTHER PLAYERS

- 18.2.1 ABO ENERGY KGAA

- 18.2.1.1 Deals

- 18.2.1.2 Expansions

- 18.2.2 GREEN HYDROGEN SYSTEMS

- 18.2.2.1 Deals

- 18.2.2.2 Expansions

- 18.2.2.3 Other developments

- 18.2.3 SALZGITTER AG

- 18.2.3.1 Deals

- 18.2.3.2 Expansions

- 18.2.4 RWE

- 18.2.4.1 Deals

- 18.2.4.2 Expansions

- 18.2.4.3 Other developments

- 18.2.5 ADANI GROUP

- 18.2.5.1 Other developments

- 18.2.6 HYDROGENEA GMBH

- 18.2.7 WAAREE ENERGIES LTD

- 18.2.8 IBERDROLA, S.A.

- 18.2.8.1 Recent developments

- 18.2.9 ENEL S.P.A

- 18.2.9.1 Recent developments

- 18.2.10 ENVISION GROUP

- 18.2.10.1 Recent developments

- 18.2.11 HYNAMICS GROUPE (EDF)

- 18.2.11.1 Recent developments

- 18.2.12 ACWA POWER

- 18.2.13 THE STATE ATOMIC ENERGY CORPORATION ROSATOM

- 18.2.13.1 Recent developments

- 18.2.14 ENEGIX ENERGY

- 18.2.15 ACME GROUP

- 18.2.15.1 Recent developments

- 18.2.16 GEOPURA LTD.

- 18.2.16.1 Recent developments

- 18.2.17 IWATANI CORPORATION

- 18.2.17.1 Recent developments

- 18.2.18 IVYS ENERGY SOLUTIONS

- 18.2.19 ENAPTER S.R.L

- 18.2.19.1 Recent developments

- 18.2.20 ATAWEY

- 18.2.21 HIRINGA ENERGY LIMITED

- 18.2.21.1 Recent developments

- 18.2.22 PLUG POWER, INC.

- 18.2.22.1 Recent developments

- 18.2.23 ITM POWER PLC.

- 18.2.23.1 Recent developments

- 18.2.1 ABO ENERGY KGAA

19 RESEARCH METHODOLOGY

- 19.1 RESEARCH DATA

- 19.1.1 SECONDARY DATA

- 19.1.1.1 Key data from secondary sources

- 19.1.2 PRIMARY DATA

- 19.1.2.1 Key data from primary sources

- 19.1.2.2 Key industry insights

- 19.1.2.3 List of participating companies for primary research

- 19.1.1 SECONDARY DATA

- 19.2 MARKET SIZE ESTIMATION

- 19.3 BASE NUMBER CALCULATION

- 19.3.1 SUPPLY-SIDE APPROACH

- 19.4 DATA TRIANGULATION

- 19.5 GROWTH RATE ASSUMPTIONS/GROWTH FORECAST

- 19.6 RESEARCH ASSUMPTIONS

- 19.7 RISK ASSESSMENT

- 19.7.1 RESEARCH LIMITATIONS

20 APPENDIX

- 20.1 DISCUSSION GUIDE

- 20.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.3 CUSTOMIZATION OPTIONS

- 20.4 RELATED REPORTS

- 20.5 AUTHOR DETAILS