|

시장보고서

상품코드

1924863

메타물질 시장 : 용도별, 최종 사용자별, 제품별, 유형별, 지역별 예측(-2032년)Metamaterial Market by Product (Antenna, Reconfigurable Intelligent Surfaces, Lenses & Optical Modules, Sensors & Beam Steering, Anti-Reflective Films), Wave Steering, Electromagnetic, Terahertz, Application, and Region - Global Forecast to 2032 |

||||||

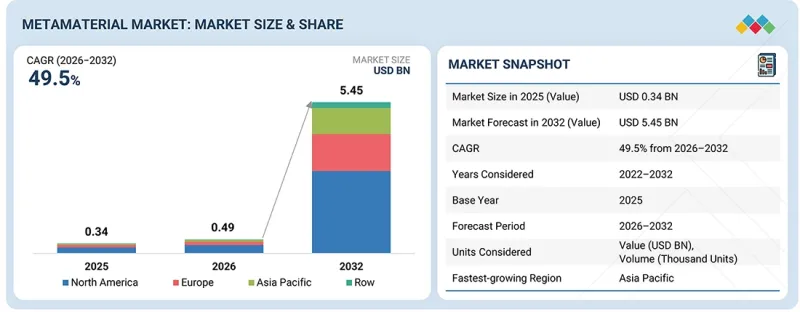

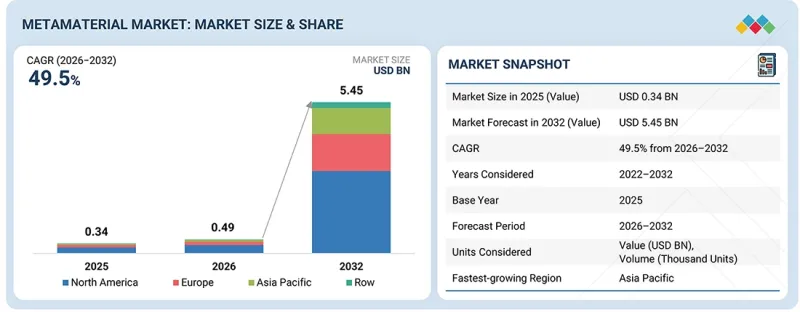

세계의 메타물질 시장 규모는 예측 기간 동안 CAGR 49.5%로 성장할 전망이며, 2026년 4억 9,000만 달러에서 2032년까지 54억 5,000만 달러에 이를 것으로 예측됩니다.

시장 성장은 항공우주 및 방위, 통신, 자동차, 소비자용 전자기기 산업에서의 신호 성능 향상, 소형화, 기능 통합에 대한 수요 증가에 의해 견인되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2026-2032년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 용도별, 최종 사용자별, 제품별, 유형별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양 및 기타 지역 |

고주파 통신, 위성 연결, 레이더 시스템, 자율 플랫폼에 대한 주목이 높아지는 가운데, 메타물질 기반의 안테나, 센서, 빔 스티어링 솔루션의 채용이 더욱 가속화되고 있습니다. 또한, 계산 설계, 나노 패브리케이션, 디지털 제어에 의한 재구성 가능 표면 기술의 진보에 의해 보다 효율적이고 조정 가능하며, 확장성이 높은 메타물질의 실장이 가능해지고 있습니다. 5G 및 차세대 무선 네트워크, 우주 기술, 첨단 센싱 인프라에 대한 투자 확대는 상용화 기회를 더욱 확대하고 메타물질을 차세대 전자 포토닉 시스템의 중요한 기반 기술로 자리매김하고 있습니다.

최종 사용자별로는 다른 최종 사용자 부문이 예측 기간 동안 가장 높은 CAGR을 달성할 것으로 예측됩니다. 이 성장은 신호 제어, 구조 모니터링 및 전자기 간섭 관리 개선을 목표로 스마트 인프라, 산업 자동화 및 에너지 시스템에서 메타 재료 기반 솔루션의 채택 증가로 지원됩니다. 메타물질은 복잡한 환경에서 성능, 신뢰성 및 운영 효율성을 향상시키기 위해 산업용 센서, 무선 통신 모듈 및 차폐 부품에 내장되어 있습니다. 또한 스마트시티, 첨단 도로교통 시스템(ITS), 디지털 접속형 산업시설에 대한 투자 증가가 도입을 가속화하고 있습니다. 확장 가능한 제조 기술과 시스템 레벨 통합의 진전은 대규모 인프라 및 산업 이용 사례에서의 채용을 더욱 촉진하고, 본 부문은 예측 기간 중 주요 성장 요인이 될 전망입니다.

전자기 부문은 예측 기간 동안 다른 유형 부문보다 높은 CAGR로 성장할 것으로 예측됩니다. 이 성장은 고주파 통신, 레이더 및 감지 용도에서 전자기파의 고급 제어에 대한 수요 증가로 인한 것입니다. 위성 통신, 5G 및 미래의 무선 네트워크, 자동차 레이더, 방위 시스템의 강력한 채택이 전개를 가속화하고 있습니다. 이러한 재료는 컴팩트한 안테나 설계, 빔 스티어링 강화, 간섭 감소, 신호 효율 향상을 가능하게 하며 기존 재료의 성능 한계를 해결합니다. 또한 재구성 가능하고 조정 가능한 전자기 메타물질의 발전으로 동적 시스템 및 소프트웨어 정의 시스템의 이용 사례가 확대되고 있습니다. 산업 분야에서 소형화, 성능 최적화, 시스템 수준의 통합이 점점 더 중요해지고 있는 가운데, 전자기 메타물질은 시장 전반에 걸친 주요 촉진요인으로 부상하고 있습니다.

아시아태평양에서는 급속한 디지털 전환, 통신 인프라 확대, 방위 근대화 및 반도체 제조에 대한 투자 증가를 배경으로 메타물질 시장이 강력한 성장을 보이고 있습니다. 중국, 일본, 한국, 인도 등의 국가들은 5G 네트워크, 위성 프로그램, 자동차용 전자기기, 선진 센싱 기술의 대규모 도입을 통해 채용을 주도하고 있습니다. 이 지역의 스마트 인프라, 자율 이동체, 고주파 전자 기기에 대한 주력은 메타물질 기반 안테나, 레이더 부품, 광 모듈에 대한 수요를 가속화하고 있습니다. 또한 경제적인 제조 능력, 견고한 전자 부품 공급망, 첨단 재료 및 차세대 연결 기술에 대한 정부의 지원책이 함께, 아시아태평양은 세계 메타물질 시장에서 가장 급성장하는 지역 중 하나로서의 지위를 확립하고 있습니다.

2차 조사를 통해 수집한 각종 부문 및 하위 부문 시장 규모를 확정 및 검증하기 위해 메타물질 시장 분야의 주요 업계 전문가에게 광범위한 1차 인터뷰를 실시했습니다.

메타물질 시장은 Kymeta Corporation(미국), PIVOTAL COMMWARE(미국), Echodyne Corp.(미국), Lumotive(미국), Radi-Cool, Inc.(미국) 등 세계적으로 확립된 여러 회사의 진출 기업이 주도하고 있습니다. 본 조사에서는 이러한 주요 진출기업에 대해 기업 프로파일, 최근 동향, 주요 시장 전략을 포함한 상세한 경쟁 분석을 실시했습니다.

조사 범위 :

본 보고서에서는 메타물질 시장을 유형별, 용도별, 제품 유형별, 최종 사용자별로 분석했습니다.

이 보고서는 시장 성장 촉진요인, 억제요인, 기회 및 과제에 대해 논의하고 북미, 유럽, 아시아태평양 및 세계 기타 지역에서 시장에 대한 자세한 견해를 제공합니다. 주요 진출기업 공급망 분석 및 메타물질 시장 생태계 분석도 포함되어 있습니다.

이 보고서 구매의 주요 이점 :

- 주요 촉진요인 분석(산업 분야의 인원 및 자산보호 강화, 설비 및 기계 안전기준 의무화), 억제요인(첨단 무선통신 시스템 수요 증가, 광학 메타물질 진보), 기회(신재생 에너지 분야 확대, 열 메타물질 진보), 과제(대중시장용 메타물질 양산화 확대, 자원 가용성)

- 제품 개발 및 이노베이션 : 메타물질 시장에 있어서의 신기술 동향, 연구개발 활동, 제품 투입에 관한 상세한 지견

- 시장 개발 : 다양한 지역의 수익성이 높은 시장에 관한 종합적인 정보

- 시장 다양화 : 신제품, 미개척지역, 최근 동향, 메타물질 시장 투자에 대한 종합적인 정보

- 경쟁 평가 : 메타물질 시장에서 주요 기업(Kymeta Corporation(미국), PIVOTAL COMMWARE(미국), Echodyne Corp.(미국), Lumotive(미국), Radi-Cool, Inc.(미국) 등) 시장 점유율, 성장 전략, 서비스 제공 내용에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 중요 인사이트

제4장 시장 개요

- 시장 역학

- 상호 접속된 시장 및 분야 간 기회

- Tier 1/2/3 참가 기업의 전략적 움직임

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제지표

- 밸류체인 분석

- 생태계 분석

- 가격 분석

- 무역 분석

- 주요 컨퍼런스 및 이벤트(2026년)

- 고객의 비즈니스에 영향을 미치는 동향 및 혼란

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 미국 관세의 영향-개요(2025년)

제6장 규제 상황

- 규제기관, 정부기관, 기타 조직

- 업계 표준

제7장 전략적 파괴, 특허, 디지털, AI 도입

- 주요 신기술

- 보완적 기술

- 기술 및 제품 로드맵

- 특허 분석

- AI 및 생성형 AI가 메타물질 시장에 미치는 영향

제8장 고객 정세 및 구매 행동

- 의사결정 프로세스

- 구매자의 이해관계자 및 구매 평가 기준

- 채용 장벽 및 내부 과제

- 다양한 용도의 미충족 요구

제9장 메타물질의 기능

- 웨이브 스티어링

- 파도 흡수

- 파의 증폭

- 클로킹

- 에너지 집중

- 주파수 필터링

- 빔 성형

- 다기능 행동

제10장 메타물질의 형상인자

- 박막

- 벌크 재료

제11장 메타물질의 주파수 대역

- 테라헤르츠

- 포토닉(근적외선)

- 조정 가능

- 플라즈모닉

제12장 메타물질의 구조 치수

- 2D 메타서피스

- 3D 벌크 메타물질

- 다층 아키텍처

- 구배 굴절률 메타 재료

제13장 메타물질 시장 : 용도별

- 무선 주파수

- 광학

- 기타

제14장 메타물질 시장 : 최종 사용자별

- 가전

- 자동차

- 항공우주 및 방위

- 태양광 발전

- 로봇 공학

- 헬스케어

- 통신

- 기타

제15장 메타물질 시장 : 제품별

- 안테나, 레이더, 재구성 가능한 지능형 서피스(RIS)

- 렌즈 및 광학 모듈

- 센서 및 빔 스티어링 모듈

- 반사 방지 필름

- 기타

제16장 메타물질 시장 : 유형별

- 전자

- 기타

제17장 메타물질 시장 : 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타

- 아시아태평양

- 중국

- 일본

- 인도

- 대만

- 한국

- 기타

- 기타 지역

- 중동

- 아프리카

- 남미

제18장 경쟁 구도

- 개요

- 주요 참가 기업의 전략 및 강점(2021-2025년)

- 시장 점유율 분석(2025년)

- 기업 평가 및 재무 지표(2025년)

- 브랜드 비교

- 기업 평가 매트릭스 : 주요 진입기업(2025년)

- 기업 평가 매트릭스 : 스타트업 및 중소기업(2025년)

- 경쟁 시나리오

제19장 기업 프로파일

- 주요 진출기업

- KYMETA CORPORATION

- PIVOTAL COMMWARE

- ECHODYNE CORP.

- ALCAN SYSTEMS GMBH IL

- METALENZ, INC.

- GREENERWAVE

- EDGEHOG

- METAMAGNETICS INC.

- FRACTAL ANTENNA SYSTEMS, INC.

- LUMOTIVE

- TERAVIEW LIMITED

- 기타 기업

- 2PI INC.

- MOXTEK, INC.

- PLASMONICS INC.

- SINTEC OPTRONICS PTE LTD.

- PHONONIC VIBES SRL

- PHOEBUS OPTOELECTRONICS LLC

- APPLIED METAMATERIALS

- AMG

- RADI-COOL SDN BHD

- METABOARDS

- JEM ENGINEERING

- METASONIXX

- THORLABS, INC.

- HUAWEI TECHNOLOGIES CO., LTD.

- NIL TECHNOLOGY

- ZTE CORPORATION

- METASHIELD LLC

제20장 조사 방법

제21장 부록

AJY 26.02.23The global metamaterial market is projected to reach USD 5.45 billion by 2032, growing from USD 0.49 billion in 2026 at a CAGR of 49.5% during the forecast period. Market growth is fueled by rising demand for enhanced signal performance, miniaturization, and functional integration across the aerospace & defense, telecommunications, automotive, and consumer electronics industries.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Product, Application and Region |

| Regions covered | North America, Europe, APAC, RoW |

The increasing focus on high-frequency communications, satellite connectivity, radar systems, and autonomous platforms is further accelerating the adoption of metamaterial-based antennas, sensors, and beam steering solutions. Additionally, advancements in computational design, nanofabrication, and digitally controlled reconfigurable surfaces are enabling more efficient, tunable, and scalable metamaterial implementations. Growing investments in 5G and future wireless networks, space technologies, and advanced sensing infrastructure are further expanding commercialization opportunities, positioning metamaterials as a key enabler of next-generation electronic and photonic systems.

"The other end users segment is projected to grow at the highest CAGR during the forecast period."

By end user, the other end users segment is projected to achieve the highest CAGR during the forecast period. This growth is supported by increasing adoption of metamaterial-based solutions in smart infrastructure, industrial automation, and energy systems to improve signal control, structural monitoring, and electromagnetic interference management. Metamaterials are being integrated into industrial sensors, wireless communication modules, and shielding components to enhance performance, reliability, and operational efficiency in complex environments. Additionally, rising investments in smart cities, intelligent transportation systems, and digitally connected industrial facilities are accelerating deployment. Advancements in scalable manufacturing and system-level integration are further enabling adoption across large-scale infrastructure and industrial use cases, positioning this segment as a key growth contributor over the forecast period.

"The electromagnetic segment is projected to achieve a higher CAGR than the other types segment during the forecast period."

The electromagnetic segment is projected to grow at a higher CAGR than the other types segment during the forecast period. This growth is driven by increasing demand for advanced control of electromagnetic waves across high-frequency communication, radar, and sensing applications. Strong adoption in satellite communications, 5G and future wireless networks, automotive radar, and defense systems is accelerating deployment. These materials enable compact antenna designs, enhanced beam steering, reduced interference, and improved signal efficiency, addressing performance limitations of conventional materials. Additionally, advancements in reconfigurable and tunable electromagnetic metamaterials are expanding use cases across dynamic and software-defined systems. As industries increasingly prioritize miniaturization, performance optimization, and system-level integration, electromagnetic metamaterials are emerging as a key growth driver in the overall market.

"Asia Pacific is projected to register the highest growth in the metamaterial market between 2026 and 2030."

The Asia Pacific region is witnessing strong growth in the metamaterial market, driven by rapid digital transformation, expanding telecommunications infrastructure, and rising investments in defense modernization and semiconductor manufacturing. Countries such as China, Japan, South Korea, and India are leading adoption through large-scale deployment of 5G networks, satellite programs, automotive electronics, and advanced sensing technologies. The region's focus on smart infrastructure, autonomous mobility, and high-frequency electronics is accelerating demand for metamaterial-based antennas, radar components, and optical modules. Additionally, cost-effective manufacturing capabilities, strong electronics supply chains, and supportive government initiatives for advanced materials and next-generation connectivity are positioning Asia Pacific as one of the fastest-growing regions in the global metamaterial market.

Extensive primary interviews were conducted with key industry experts in the metamaterial market space to determine and verify the market size for various segments and subsegments gathered through secondary research.

The breakdown of primary participants for the report is shown below.

- By Company Type: Tier 1 - 20%, Tier 2 - 45%, Tier 3 - 35%

- By Designation: C-level Executives - 35%, Directors - 25%, Others - 40%

- By Region: Asia Pacific - 45%, Europe - 25%, North America - 20%, RoW - 10%

The metamaterial market is dominated by a few globally established players, such as Kymeta Corporation (US), PIVOTAL COMMWARE (US), Echodyne Corp. (US), Lumotive (US), and Radi-Cool, Inc. (US). The study includes an in-depth competitive analysis of these key players in the metamaterial market, with their company profiles, recent developments, and key market strategies.

Study Coverage:

The report segments the metamaterial market by type (Electromagnetic, other types), application (RF, optical, other applications), product [Antennas, radar, and reconfigurable intelligent surfaces (RIS); lenses & optical modules; sensors and beam steering modules; anti-reflective films; other products], end user (Aerospace & defense, automotive, telecommunication, consumer electronics, robotics, photovoltaics, healthcare, other end users)

The report discusses the market drivers, restraints, opportunities, and challenges, and provides a detailed view of the market across North America, Europe, Asia Pacific, and the Rest of the World. It includes a supply chain analysis of the key players and their competitive analysis in the metamaterial market ecosystem.

Key Benefits of Buying the Report:

- Analysis of key drivers (Rising personnel and asset protection in the industrial sector, mandatory safety standards for equipment and machinery), restraints (Growing demand for enhanced wireless communication systems, advancements in optical metamaterials), opportunities (Expansion of renewable energy sector, advancements in thermal metamaterials), challenges (Scaling up production of metamaterials for mass markets, limited availability of resources)

- Product Development/Innovation: Detailed insights into upcoming technologies, research and development activities, and product launches in the metamaterial market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the metamaterial market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players, such as Kymeta Corporation (US), PIVOTAL COMMWARE (US), Echodyne Corp. (US), Lumotive (US), and Radi-Cool, Inc. (US), in the metamaterial market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN METAMATERIAL MARKET

- 3.2 TYPE: METAMATERIAL MARKET (USD MILLION)

- 3.3 ANTENNA, RADAR, AND RIS: METAMATERIAL MARKET, BY REGION

- 3.4 APPLICATION: METAMATERIAL MARKET

- 3.5 METAMATERIAL MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing demand for enhanced wireless communication systems

- 4.2.1.2 Advancements in optical metamaterials

- 4.2.1.3 Advancements in next-generation aerospace and defense technologies

- 4.2.2 RESTRAINTS

- 4.2.2.1 High production costs

- 4.2.2.2 Complex manufacturing processes

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of renewable energy sector

- 4.2.3.2 Advancements in thermal metamaterials

- 4.2.3.3 Integration of nanotechnology with metamaterials

- 4.2.4 CHALLENGES

- 4.2.4.1 Scaling up production of metamaterials for mass markets

- 4.2.4.2 Limited availability of resources

- 4.2.4.3 Stringent regulatory hurdles

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.2.4 TRENDS IN CONSUMER ELECTRONICS INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING RANGE OF METAMATERIALS PROVIDED BY KEY PLAYERS, BY PRODUCT TYPE

- 5.5.2 AVERAGE SELLING PRICE TREND OF METAMATERIAL-BASED LENSES, BY REGION, 2021-2024

- 5.5.3 AVERAGE SELLING PRICE OF METAMATERIAL-BASED LENSES, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 852910)

- 5.6.2 EXPORT SCENARIO (HS CODE 852910)

- 5.7 KEY CONFERENCES AND EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 KYMETA ENABLES MOBILE SATELLITE CONNECTIVITY USING METAMATERIAL ANTENNAS

- 5.10.2 ECHODYNE ENABLES LOW-SWAP RADAR USING METAMATERIAL ELECTRONIC SCANNING ARRAYS

- 5.10.3 ALCAN SYSTEMS ADDRESSES MMWAVE 5G ROLLOUT CHALLENGES WITH LIQUID CRYSTAL SMART ANTENNAS

- 5.10.4 METALENZ ENABLES COMPACT OPTICAL SYSTEMS USING METASURFACE LENSES

- 5.10.5 PIVOTAL COMMUNICATIONS TRANSFORMS MMWAVE DEPLOYMENT WITH PIVOTAL TURNKEY

- 5.10.6 UNIVERSITY OF EXETER AND VIRGINIA TECH COLLABORATE TO HARNESS ACOUSTIC METAMATERIALS FOR ENHANCED NOISE CONTROL

- 5.11 IMPACT OF 2025 US TARIFF - OVERVIEW

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 REGULATORY LANDSCAPE

- 6.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.2 INDUSTRY STANDARDS

7 STRATEGIC DISRUPTION, PATENT, DIGITAL, AND AI ADOPTION

- 7.1 KEY EMERGING TECHNOLOGIES

- 7.1.1 METASURFACES

- 7.1.2 PHOTONIC CRYSTALS

- 7.2 COMPLEMENTARY TECHNOLOGIES

- 7.2.1 ADVANCED NANOFABRICATION AND LITHOGRAPHY

- 7.2.2 AI-DRIVEN DESIGN AND SIMULATION

- 7.3 TECHNOLOGY/PRODUCT ROADMAP

- 7.4 PATENT ANALYSIS

- 7.5 IMPACT OF AI/GEN AI ON METAMATERIAL MARKET

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS APPLICATIONS

9 FUNCTIONALITIES OF METAMATERIALS

- 9.1 INTRODUCTION

- 9.2 WAVE STEERING

- 9.3 WAVE ABSORPTION

- 9.4 WAVE AMPLIFICATION

- 9.5 CLOAKING

- 9.6 ENERGY FOCUSING

- 9.7 FREQUENCY FILTERING

- 9.8 BEAM SHAPING

- 9.9 MULTI-FUNCTIONAL BEHAVIOR

10 FORM FACTORS OF METAMATERIALS

- 10.1 INTRODUCTION

- 10.2 THIN FILMS

- 10.3 BULK MATERIALS

11 FREQUENCY BAND OF METAMATERIAL

- 11.1 INTRODUCTION

- 11.2 TERAHERTZ

- 11.3 PHOTONIC (NEAR IR)

- 11.4 TUNABLE

- 11.5 PLASMONIC

12 STRUCTURAL DIMENSIONS OF METAMATERIALS

- 12.1 INTRODUCTION

- 12.2 2D METASURFACES

- 12.3 3D BULK METAMATERIALS

- 12.4 MULTI-LAYER ARCHITECTURES

- 12.5 GRADIENT INDEX METAMATERIALS

13 METAMATERIAL MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.2 RF

- 13.2.1 EXPANSION OF 5G, SATELLITE CONNECTIVITY, AND ADVANCED RADAR SYSTEMS TO DRIVE DOMINANCE

- 13.3 OPTICAL

- 13.3.1 GROWING ADOPTION OF COMPACT HIGH-PERFORMANCE IMAGING AND PHOTONIC SYSTEMS ACCELERATING OPTICAL METAMATERIALS USAGE

- 13.4 OTHER APPLICATIONS

14 METAMATERIAL MARKET, BY END USER

- 14.1 INTRODUCTION

- 14.2 CONSUMER ELECTRONICS

- 14.2.1 ADVANCEMENTS TO ENHANCE PERFORMANCE AND ENERGY EFFICIENCY TO BOOST MARKET GROWTH

- 14.2.1.1 Smartphones

- 14.2.1.2 Laptops & tablets

- 14.2.1.3 Head-mounted displays

- 14.2.1 ADVANCEMENTS TO ENHANCE PERFORMANCE AND ENERGY EFFICIENCY TO BOOST MARKET GROWTH

- 14.3 AUTOMOTIVE

- 14.3.1 GROWTH OF AUTONOMOUS, CONNECTED, AND ELECTRIFIED VEHICLES TO FUEL METAMATERIAL ADOPTION

- 14.4 AEROSPACE & DEFENSE

- 14.4.1 INCREASING FOCUS ON STEALTH, ADVANCED SENSING, AND LIGHTWEIGHT PLATFORMS TO BOOST GROWTH

- 14.5 PHOTOVOLTAICS

- 14.5.1 INCREASING EMPHASIS ON SOLAR EFFICIENCY AND ADVANCED LIGHT MANAGEMENT TO FUEL ADOPTION

- 14.6 ROBOTICS

- 14.6.1 EXPANSION OF INTELLIGENT AUTOMATION AND PRECISION ROBOTICS TO DRIVE METAMATERIALS INTEGRATION IN ROBOTIC SYSTEMS

- 14.7 HEALTHCARE

- 14.7.1 HIGH DEMAND FOR ADVANCED IMAGING, DIAGNOSTICS, AND MINIATURIZED MEDICAL DEVICES TO DRIVE ADOPTION

- 14.8 TELECOMMUNICATION

- 14.8.1 RISING DEMAND FOR HIGH-CAPACITY DATA TRANSMISSION TO FUEL MARKET GROWTH

- 14.9 OTHER END USERS

- 14.9.1 GROWING DEMAND FOR ENERGY EFFICIENCY AND NOISE REDUCTION SOLUTIONS TO FUEL GROWTH

15 METAMATERIAL MARKET, BY PRODUCT

- 15.1 INTRODUCTION

- 15.2 ANTENNAS, RADAR, AND RECONFIGURABLE INTELLIGENT SURFACES (RIS)

- 15.2.1 DEMAND FOR ADVANCED WIRELESS CONNECTIVITY AND SMART RADIO ENVIRONMENTS TO DRIVE ADOPTION

- 15.2.2 ACTIVE

- 15.2.3 PASSIVE

- 15.2.4 HYBRID

- 15.3 LENSES & OPTICAL MODULES

- 15.3.1 DEMAND FOR COMPACT, HIGH-RESOLUTION IMAGING AND ADVANCED OPTICAL PERFORMANCE TO DRIVE GROWTH

- 15.4 SENSORS & BEAM STEERING MODULES

- 15.4.1 INCREASING DEMAND IN TELECOMMUNICATIONS TO BOOST MARKET GROWTH

- 15.5 ANTI-REFLECTIVE FILMS

- 15.5.1 ENHANCED OPTICAL EFFICIENCY AND ENERGY SAVINGS TO DRIVE GROWTH

- 15.6 OTHER PRODUCTS

- 15.6.1 RISING DEMAND FOR ADVANCED EMI SHIELDING AND WIRELESS POWER SOLUTIONS TO PROPEL MARKET GROWTH

- 15.6.1.1 Absorbers

- 15.6.1.2 Cloaking devices

- 15.6.1.3 Light and sound filters

- 15.6.1.4 Isolator and circulators

- 15.6.1.5 RF filters

- 15.6.1.6 Transmission lines

- 15.6.1.7 Wireless charging solutions

- 15.6.1 RISING DEMAND FOR ADVANCED EMI SHIELDING AND WIRELESS POWER SOLUTIONS TO PROPEL MARKET GROWTH

16 METAMATERIAL MARKET, BY TYPE

- 16.1 INTRODUCTION

- 16.2 ELECTROMAGNETIC

- 16.2.1 RISING DEMAND FOR 5G, ADVANCED RADAR, AND HIGH-RESOLUTION IMAGING TO DRIVE GROWTH

- 16.2.2 DOUBLE NEGATIVE

- 16.2.3 SINGLE NEGATIVE

- 16.2.4 ELECTRONIC BANDGAP

- 16.2.5 DOUBLE POSITIVE

- 16.2.6 BI-ISOTROPIC

- 16.2.7 CHIRAL

- 16.2.8 FREQUENCY SELECTIVE SURFACE-BASED

- 16.3 OTHER TYPES

- 16.3.1 THERMAL

- 16.3.1.1 Growing demand for advanced thermal control and energy efficiency to drive adoption

- 16.3.2 ELASTIC

- 16.3.2.1 Rising need for vibration control and structural resilience to fuel growth

- 16.3.3 ACOUSTIC

- 16.3.3.1 Increasing focus on noise reduction and advanced sound control to accelerate adoption

- 16.3.1 THERMAL

17 METAMATERIAL MARKET, BY REGION

- 17.1 INTRODUCTION

- 17.2 NORTH AMERICA

- 17.2.1 US

- 17.2.1.1 Defense modernization, advanced wireless infrastructure, and optical innovation driving metamaterials leadership

- 17.2.2 CANADA

- 17.2.2.1 Emphasis on advanced sensing, aerospace research, and wireless innovation to support metamaterials adoption

- 17.2.3 MEXICO

- 17.2.3.1 Electronics manufacturing growth and automotive integration to support gradual metamaterials adoption

- 17.2.1 US

- 17.3 EUROPE

- 17.3.1 GERMANY

- 17.3.1.1 Automotive innovation, industrial digitization, and radar systems to drive metamaterials adoption

- 17.3.2 UK

- 17.3.2.1 Defense research and wireless innovation support metamaterials commercialization

- 17.3.3 FRANCE

- 17.3.3.1 Aerospace leadership and smart connectivity initiatives driving metamaterials adoption

- 17.3.4 ITALY

- 17.3.4.1 Research-driven adoption in aerospace and photonics to support niche market growth

- 17.3.5 REST OF EUROPE

- 17.3.1 GERMANY

- 17.4 ASIA PACIFIC

- 17.4.1 CHINA

- 17.4.1.1 Large-scale 5g deployment and advanced manufacturing to drive market growth

- 17.4.2 JAPAN

- 17.4.2.1 Photonics leadership and precision electronics to drive metamaterials innovation

- 17.4.3 INDIA

- 17.4.3.1 Defense modernization and wireless research to support emerging metamaterials market

- 17.4.4 TAIWAN

- 17.4.4.1 Semiconductor and electronics manufacturing ecosystem enables metamaterials integration

- 17.4.5 SOUTH KOREA

- 17.4.5.1 Next-generation wireless and consumer electronics to drive metamaterials adoption

- 17.4.6 REST OF ASIA PACIFIC

- 17.4.1 CHINA

- 17.5 REST OF THE WORLD

- 17.5.1 MIDDLE EAST

- 17.5.1.1 Defense modernization, satellite communications, and advanced surveillance systems to drive adoption

- 17.5.2 AFRICA

- 17.5.2.1 Selective defense and security applications to support early-stage metamaterials adoption

- 17.5.3 SOUTH AMERICA

- 17.5.3.1 Telecommunications expansion, defense modernization, and infrastructure upgrades to drive market

- 17.5.1 MIDDLE EAST

18 COMPETITIVE LANDSCAPE

- 18.1 OVERVIEW

- 18.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 18.3 MARKET SHARE ANALYSIS, 2025

- 18.4 COMPANY VALUATION AND FINANCIAL METRICS, 2025

- 18.5 BRAND COMPARISON

- 18.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 18.6.1 STARS

- 18.6.2 EMERGING LEADERS

- 18.6.3 PERVASIVE PLAYERS

- 18.6.4 PARTICIPANTS

- 18.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 18.6.5.1 Company footprint

- 18.6.5.2 Region footprint

- 18.6.5.3 Application footprint

- 18.6.5.4 End user footprint

- 18.6.5.5 Product footprint

- 18.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 18.7.1 PROGRESSIVE COMPANIES

- 18.7.2 RESPONSIVE COMPANIES

- 18.7.3 DYNAMIC COMPANIES

- 18.7.4 STARTING BLOCKS

- 18.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 18.7.5.1 Detailed list of startups/SMEs

- 18.7.5.2 Competitive benchmarking of startups/SMEs

- 18.8 COMPETITIVE SCENARIO

- 18.8.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 18.8.2 DEALS

19 COMPANY PROFILES

- 19.1 KEY PLAYERS

- 19.1.1 KYMETA CORPORATION

- 19.1.1.1 Business overview

- 19.1.1.2 Products/Solutions/Services offered

- 19.1.1.3 Recent developments

- 19.1.1.3.1 Product launches

- 19.1.1.3.2 Deals

- 19.1.1.3.3 Other developments

- 19.1.1.4 MnM view

- 19.1.1.4.1 Right to win

- 19.1.1.4.2 Strategic choices

- 19.1.1.4.3 Weaknesses and competitive threats

- 19.1.2 PIVOTAL COMMWARE

- 19.1.2.1 Business overview

- 19.1.2.2 Products/Solutions/Services offered

- 19.1.2.3 Recent developments

- 19.1.2.3.1 Product launches

- 19.1.2.3.2 Deals

- 19.1.2.3.3 Other developments

- 19.1.2.4 MnM view

- 19.1.2.4.1 Right to win

- 19.1.2.4.2 Strategic choices

- 19.1.2.4.3 Weaknesses and competitive threats

- 19.1.3 ECHODYNE CORP.

- 19.1.3.1 Business overview

- 19.1.3.2 Products/Solutions/Services offered

- 19.1.3.3 Recent developments

- 19.1.3.3.1 Product launches

- 19.1.3.3.2 Deals

- 19.1.3.4 MnM view

- 19.1.3.4.1 Right to win

- 19.1.3.4.2 Strategic choices

- 19.1.3.4.3 Weaknesses and competitive threats

- 19.1.4 ALCAN SYSTEMS GMBH I.L.

- 19.1.4.1 Business overview

- 19.1.4.2 Products/Solutions/Services offered

- 19.1.4.3 Recent developments

- 19.1.4.3.1 Product launches

- 19.1.4.3.2 Deals

- 19.1.4.4 MnM view

- 19.1.4.4.1 Right to win

- 19.1.4.4.2 Strategic choices

- 19.1.4.4.3 Weaknesses and competitive threats

- 19.1.5 METALENZ, INC.

- 19.1.5.1 Business overview

- 19.1.5.2 Products/Solutions/Services offered

- 19.1.5.3 Recent developments

- 19.1.5.3.1 Product launches

- 19.1.5.3.2 Deals

- 19.1.5.4 MnM view

- 19.1.5.4.1 Right to win

- 19.1.5.4.2 Strategic choices

- 19.1.5.4.3 Weaknesses and competitive threats

- 19.1.6 GREENERWAVE

- 19.1.6.1 Business overview

- 19.1.6.2 Products/Solutions/Services offered

- 19.1.6.3 Recent developments

- 19.1.6.3.1 Product launches

- 19.1.6.3.2 Deals

- 19.1.7 EDGEHOG

- 19.1.7.1 Business overview

- 19.1.7.2 Products/Solutions/Services offered

- 19.1.8 METAMAGNETICS INC.

- 19.1.8.1 Business overview

- 19.1.8.2 Products/Solutions/Services offered

- 19.1.8.3 Recent developments

- 19.1.8.3.1 Product launches

- 19.1.8.3.2 Other developments

- 19.1.9 FRACTAL ANTENNA SYSTEMS, INC.

- 19.1.9.1 Business overview

- 19.1.9.2 Products/Solutions/Services offered

- 19.1.9.3 Recent developments

- 19.1.9.3.1 Expansions

- 19.1.10 LUMOTIVE

- 19.1.10.1 Business overview

- 19.1.10.2 Products/Solutions/Services offered

- 19.1.10.3 Recent developments

- 19.1.10.3.1 Product launches

- 19.1.10.3.2 Deals

- 19.1.11 TERAVIEW LIMITED

- 19.1.11.1 Business overview

- 19.1.11.2 Products/Solutions/Services offered

- 19.1.11.3 Recent developments

- 19.1.11.3.1 Product launches

- 19.1.1 KYMETA CORPORATION

- 19.2 OTHER PLAYERS

- 19.2.1 2PI INC.

- 19.2.2 MOXTEK, INC.

- 19.2.3 PLASMONICS INC.

- 19.2.4 SINTEC OPTRONICS PTE LTD.

- 19.2.5 PHONONIC VIBES S.R.L.

- 19.2.6 PHOEBUS OPTOELECTRONICS LLC

- 19.2.7 APPLIED METAMATERIALS

- 19.2.8 AMG

- 19.2.9 RADI-COOL SDN BHD

- 19.2.10 METABOARDS

- 19.2.11 JEM ENGINEERING

- 19.2.12 METASONIXX

- 19.2.13 THORLABS, INC.

- 19.2.14 HUAWEI TECHNOLOGIES CO., LTD.

- 19.2.15 NIL TECHNOLOGY

- 19.2.16 ZTE CORPORATION

- 19.2.17 METASHIELD LLC

20 RESEARCH METHODOLOGY

- 20.1 INTRODUCTION

- 20.2 RESEARCH DATA

- 20.2.1 SECONDARY DATA

- 20.2.1.1 List of major secondary sources

- 20.2.1.2 Key data from secondary sources

- 20.2.2 PRIMARY DATA

- 20.2.2.1 List of primary interview participants

- 20.2.2.2 Breakdown of primaries

- 20.2.2.3 Key data from primary sources

- 20.2.2.4 Key industry insights

- 20.2.1 SECONDARY DATA

- 20.3 FACTOR ANALYSIS

- 20.3.1 SUPPLY-SIDE ANALYSIS

- 20.3.2 DEMAND-SIDE ANALYSIS

- 20.4 MARKET SIZE ESTIMATION METHODOLOGY

- 20.4.1 BOTTOM-UP APPROACH

- 20.4.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 20.4.2 TOP-DOWN APPROACH

- 20.4.2.1 Approach to arrive at market size using top-down approach (supply side)

- 20.4.1 BOTTOM-UP APPROACH

- 20.5 MARKET BREAKDOWN AND DATA TRIANGULATION

- 20.6 RESEARCH ASSUMPTIONS

- 20.7 RESEARCH LIMITATIONS

- 20.8 RISK ANALYSIS

21 APPENDIX

- 21.1 INSIGHTS FROM INDUSTRY EXPERTS

- 21.2 DISCUSSION GUIDE

- 21.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 21.4 CUSTOMIZATION OPTIONS

- 21.5 RELATED REPORTS

- 21.6 AUTHOR DETAILS