|

시장보고서

상품코드

1928851

Midstream 석유 및 가스 여과 시장 : 여과 기술별, 여재별, 용도별, 여과 단계별, 최종사용자별, 지역별 - 예측(-2030년)Midstream Oil & Gas Filtration Market by Filter Technology, Filter Media, Application, Filtration Phase, and Region - Global Forecast to 2030 |

||||||

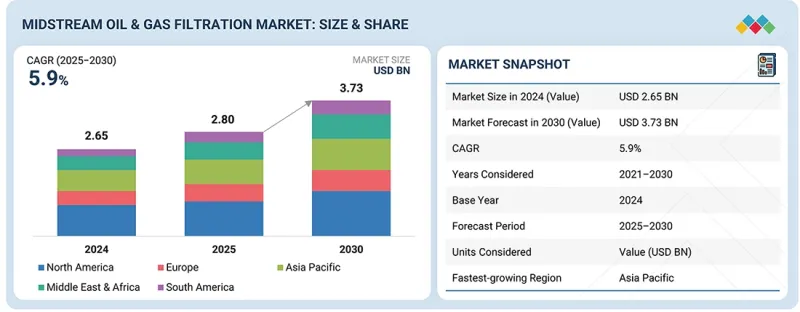

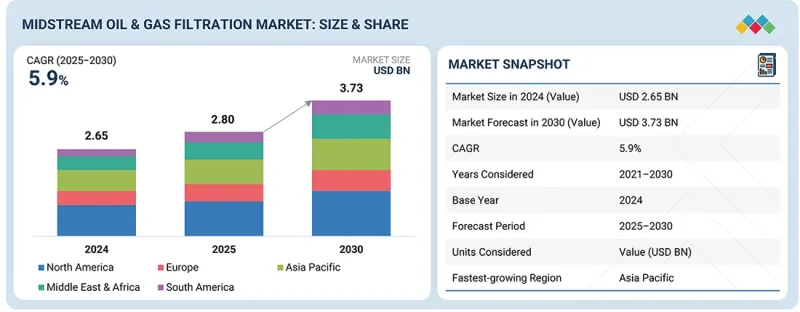

Midstream 석유 및 가스 여과 시장 규모는 예측 기간 중에 CAGR 5.9%로 성장하여 2025년 28억 달러에서 2030년까지 37억 3,000만 달러에 이를 전망입니다.

응집 여과 기술은 가스 및 탄화수소 흐름에서 액체 오염 물질을 효율적으로 분리하는 데 중요한 역할을 하기 때문에 중류 석유 및 가스 여과 시장에서 가장 빠르게 성장하는 유형입니다. 이 필터는 미세한 에어로졸, 물방울, 액체 탄화수소를 효과적으로 제거하여 가스의 품질을 향상시키고, 압축기 및 파이프라인과 같은 다운스트림 설비를 보호합니다. 높은 분리 효율, 낮은 압력 손실, 대 유량 대응 능력으로 인해 코레서 필터는 가스 처리 공장, 파이프라인 네트워크, 저장 터미널 등의 중류 응용 분야에 적합합니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021년-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025년-2030년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 여과 기술별, 여재별, 용도별, 여과 단계별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 남미, 중동 및 아프리카 |

또한, 코어 레서 매체 재료의 발전으로 내구성과 내화학성이 향상되어 유지 보수 요구 사항이 감소하고 운영 비용이 절감되었습니다. 이러한 발전에도 불구하고, 신뢰성, 규제 준수 및 자산 보호에 대한 우려는 계속 증가하고 있으며, 이는 중류 석유 및 가스 인프라에서 코어 레서 필터의 사용을 지속적으로 촉진하고 있습니다.

유리섬유 부문은 중류 석유 및 가스 여과 시장에서 금액 기준으로 두 번째로 높은 성장률을 나타낼 것으로 예측됩니다. 이는 성능, 내구성, 비용 효율성의 탁월한 조합으로 인한 것입니다. 유리 섬유 매체는 높은 오염 유지 능력을 가지고 있으며, 심층 여과를 실현하기 때문에 가스 및 액체 탄화수소 흐름에 일반적으로 존재하는 미립자 및 에어로졸을 포집하는 데 매우 효과적입니다. 그 결과, 유리 섬유 매체를 사용하는 응용 분야에서는 여과 효율이 향상되고 수명이 연장됩니다. 또한, 유리섬유는 우수한 내화학성과 열 안정성을 나타내며, 광범위한 온도 및 압력 범위에서 사용할 수 있습니다. 따라서 중류 파이프라인, 압축기 스테이션, 가스 처리 시설과 같은 가혹한 조건에서 사용하기에 적합합니다. 또한, 고가의 합성 미디어나 특수 미디어에 비해 가성비가 뛰어나며, 동등한 현장 성능을 발휘합니다. 이러한 특성으로 인해 대규모 설비에서 특히 인기가 높습니다. 예측 기간 동안 시장 성장을 뒷받침하는 중요한 요인으로 파이프라인 및 가스 인프라에 대한 투자를 들 수 있습니다.

파이프라인 운송은 중류 석유 및 가스 여과 시장에서 두 번째 점유율을 차지하고 있습니다. 이는 주로 대량의 원유, 천연가스, 정제된 제품을 장거리 운송하는 데 중요한 역할을 하기 때문입니다. 이를 통해 유량 안정화 및 파이프라인의 건전성을 유지합니다. 지속적인 여과는 침식, 막힘, 내부 부식을 유발할 수 있는 고형물, 수분, 부식 부산물, 응축수를 제거하기 위해 필수적입니다. 그 결과, 압축기 스테이션, 펌프 스테이션, 입구 지점에서 필터, 분리기, 코레서에 대한 지속적인 수요가 발생하고 있습니다. 또한, 북미, 중동, 러시아에서 특히 발달한 광범위한 세계 파이프라인 네트워크는 대규모 여과 설비 용량을 창출하는 한편, 지속적인 필터 교체가 필요합니다. 또한, 파이프라인의 무결성, 배출가스 규제, 운영 신뢰성에 대한 엄격한 안전 규정과 표준으로 인해 사업자들은 고품질 여과 시스템에 투자해야 하는 상황에 직면해 있습니다. 이로 인해 파이프라인 운송이 시장에서 차지하는 중요한 지위는 더욱 강화되었습니다.

아시아태평양은 중국, 인도, 동남아시아 국가 등의 산업화, 도시화, 에너지 수요 증가를 배경으로 중류 석유 및 가스 여과 시스템 시장에서 두 번째로 큰 규모를 자랑합니다. 파이프라인, LNG 터미널, 저장시설, 가스처리 플랜트 등을 포함한 중류 인프라는 현재 막대한 투자가 필요한 상황입니다. 이 투자는 효율적이고 신뢰할 수 있는 여과 시스템을 도입하는 데 필수적입니다. 또한, 역내 각국 정부는 청정 연료인 천연가스 사용을 촉진하여 에너지 안보를 강화하는 데 주력하고 있습니다. 그 결과, 파이프라인 네트워크와 LNG 수입 능력이 확대되고 있습니다. 운영 효율성과 환경 규제 준수에 대한 규제 당국의 강력한 강조와 세계 석유 및 가스 기업의 참여 증가가 결합되어 첨단 여과 기술의 빠른 성장을 주도하고 있습니다. 그 결과, 아시아태평양은 이러한 솔루션에 있어 세계에서 가장 빠르게 성장하는 시장이 되었습니다.

이 보고서는 다음과 같은 기업 프로파일에 대한 종합적인 분석을 제공합니다.

주요 기업으로는 Pall Corporation(미국),Jonell Systems(미국),Parker Hannifin(미국),Eaton(아일랜드),Pentair(미국),Graver Technologies(미국),3M(미국),CECO Environmental(미국),FTC Filters(미국),Clark Reliance(미국),Hilliard Corporation(미국),EnerWells(미국),Saifilter(중국),TM Filtration(미국),Brother Filtration(중국), Swift Filter(미국), Fil-Trek(캐나다), Donaldson(미국) 등입니다.

조사 범위

본 보고서는 중류 석유-가스 여과 시장을 막 유형(중공사막, 평판막, 멀티튜브막), 시스템 구성(수중 MBR 시스템, 외부 MBR 시스템), 용량(소용량, 중용량, 대용량), 용도, 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류하여 조사하였습니다. 이 보고서의 조사 범위에는 중류 석유 및 가스 여과 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 저해요인, 과제, 기회 등)에 대한 자세한 정보가 포함되어 있습니다. 주요 업계 진출기업에 대한 철저한 조사를 통해 사업 개요, 솔루션 및 서비스, 주요 전략, 계약, 파트너십, 합의사항에 대한 인사이트를 제공합니다. 제품 출시, 인수합병, 중류 석유 및 가스 여과 시장의 최근 동향도 다루고 있습니다. 본 보고서에는 중류 석유 및 가스 여과 시장 생태계에서 신생 스타트업의 경쟁에 대한 고찰도 포함되어 있습니다.

본 보고서 구매의 장점:

이 보고서는 전체 중류 석유 및 가스 여과 시장과 그 하위 부문의 수익 추정치를 제공함으로써 시장 리더와 신규 시장 진출기업을 지원합니다. 이해관계자들이 경쟁 구도를 이해하고, 더 깊은 인사이트를 얻고, 자사의 포지셔닝을 강화하고, 적절한 시장 진출 전략을 수립하는 데 도움이 될 수 있습니다. 또한, 시장 동향을 파악하고 주요 시장 성장 촉진요인, 억제요인, 과제, 기회에 대한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인 분석(LNG 및 중류 부문 설비 증설 급증, 노후화된 파이프라인 및 저장 인프라, 생산 패턴 변화 및 에너지 안보 대책), 제약 요인(설비 투자 변동성 및 프로젝트 지연에 따른 설비 발주 감소, 높은 초기 비용과 긴 회수 기간으로 개발도상국에서의 도입 저해, 대체 분리 솔루션 및 경쟁 압력, 디지털화, 예지보전, 여과 수명주기 수익성 분석) 대체 분리 기술 및 디지털 솔루션으로 인한 경쟁 압력), 기회(탄화수소 생산량 및 부생가스 증가, 디지털화, 여과 수명주기 수익화를 위한 예지보전 및 분석, 에너지 전환에 따른 신제품 카테고리 및 리노베이션 수요), 과제(공급망 압박, 원자재 가격 상승 및 납품 리드타임, 운영상의 과제-원료 변동성, 오염, 급등하는 O&M 비용)에 대해 분석했습니다.

- 제품 개발/혁신 : 중류 석유 및 가스 여과 시장의 신기술 동향, 연구개발 활동, 서비스 개발에 대한 상세한 분석.

- 시장 개발: 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 중류 석유 및 가스 여과 시장을 분석합니다.

- 시장 다각화 : 중류 석유 및 가스 여과 시장의 서비스, 미개척 지역, 최근 동향, 투자에 대한 종합적인 정보를 제공합니다.

- 경쟁사 평가: 주요 기업(Pall Corporation(미국), Jonell Systems(미국), Parker Hannifin(미국), Eaton(아일랜드), Pentair(미국), Graver Technologies(미국), 3M(미국), CECO) Environmental(미국),FTC Filters(미국),Clark Reliance(미국),Hilliard Corporation(미국),EnerWells(미국),Saifilter(중국),TM Filtration(미국),Brother Filtration(중국), Swift Filter(미국) 등) 시장 점유율, 성장 전략, 서비스 제공 내용에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

- 시장 역학

- 미충족 요구와 공백

- 연결된 시장과 분야간 기회

- 새로운 비즈니스 모델과 에코시스템 변화

- Tier1/2/3참여 기업 전략적 움직임

제5장 업계 동향

- Porter의 Five Forces 분석

- 거시경제 지표

- 밸류체인 분석

- 생태계 분석

- 가격 분석

- 무역 분석

- 2025년-2026년 주요 컨퍼런스 및 이벤트

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 2025년 미국 관세의 영향-개요

제6장 기술 진보, AI 별 영향, 특허, 혁신, 그리고 향후 응용

- 주요 신기술

- 보완적 기술

- 기술/제품 로드맵

- 특허 분석

- 향후 응용

- AI/생성형 AI가 Midstream 석유 및 가스 여과 시장에 미치는 영향

제7장 규제 상황과 지속가능성에 관한 대처

- 지역 규제와 컴플라이언스

- 지속가능성 이니셔티브

- 지속가능성에 대한 영향과 규제 정책 대처

- 인증, 라벨, 환경기준

제8장 고객 상황과 구매 행동

- 의사결정 프로세스

- 주요 이해관계자와 구입 기준

- 채택 장벽과 내부 과제

- 다양한 최종 이용 산업 미충족 요구

제9장 Midstream 석유 및 가스 여과 시장(여과 기술별)

- 코어레서피르타

- 카트리지 필터

- 기계식 필터

- 백 필터

- 미립자 필터

- 활성탄 필터

- 스트레너-

- 기타

제10장 Midstream 석유 및 가스 여과 시장(여재 별)

- 활성탄

- 금속

- 합성 폴리머

- 유리섬유

- 기타

제11장 Midstream 석유 및 가스 여과 시장(용도별)

- 가스 처리 플랜트

- 압축 스테이션

- 보관과 배송

- 파이프라인 운송

- LNG 처리

- 기타

제12장 Midstream 석유 및 가스 여과 시장(여과 단계별)

- 오일 여과

- 가스 여과

제13장 Midstream 석유 및 가스 여과 시장(최종사용자별)

- 정유소

- 석유화학 산업

제14장 Midstream 석유 및 가스 여과 시장(지역별)

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 기타

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트

- 남아프리카공화국

- 기타

- 남미

- 브라질

- 아르헨티나

- 기타

제15장 경쟁 구도

- 개요

- 주요 시장 진출기업의 전략/강점

- 매출 분석, 2022년-2024년

- 시장 점유율 분석, 2024년

- 기업 평가와 재무 지표

- 브랜드/제품 비교 분석

- 기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 경쟁 시나리오

제16장 기업 개요

- 주요 시장 진출기업

- PALL CORPORATION

- JONELL SYSTEMS

- PARKER HANNIFIN

- EATON

- PENTAIR

- GRAVER TECHNOLOGIES

- 3M

- CECO ENVIRONMENTAL

- FTC FILTERS

- CLARK-RELIANCE

- HILLIARD CORPORATION

- ENERWELLS

- SAIFILTER

- TM FILTRATION

- BROTHER FILTRATION

- SWIFT FILTER

- FIL-TREK

- DONALDSON

- 기타 기업

- PS FILTER

- SMITHS GROUP

- CRITICAL PROCESS FILTRATION

- HOFF ENGINEERING

- CLEANOVA

- NORMAN FILTER COMPANY

- COLEMAN FILTER COMPANY

- FILTERS S.P.A

- FILTER SCIENCES

- CHASE FILTERS

- MUELLER ENVIRONMENTAL

- KINGTOOL

- GAS TECH

- ROYAL PRODUCTS

제17장 조사 방법

제18장 부록

LSH 26.02.20The midstream oil & gas filtration market is projected to grow from USD 2.80 billion in 2025 to USD 3.73 billion by 2030, at a CAGR of 5.9% during the forecast period. Coalescer filter technology is the fastest-growing type in the midstream oil and gas filtration market due to its crucial role in efficiently separating liquid contaminants from gas and hydrocarbon streams. These filters effectively remove fine aerosols, water droplets, and liquid hydrocarbons, enhancing the quality of the gas and protecting downstream equipment such as compressors and pipelines. The high separation efficiency, low pressure drop, and ability to handle large flow rates make coalescer filters ideal for midstream applications like gas processing plants, pipeline networks, and storage terminals.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | by Filter Technology, Filter Media, Application, Filtration Phase, and Region |

| Regions covered | North America, Asia Pacific, Europe, South America, Middle East & Africa |

Additionally, advancements in coalescer media materials have increased durability and chemical resistance, reducing maintenance requirements and lowering operating costs. Despite these advancements, there remains a growing concern for reliability, regulatory compliance, and asset protection, which continues to drive the use of coalescer filters in midstream oil and gas infrastructure.

''Based on filter media, fiberglass is projected to register the second-fastest growth rate during the forecast period.''

The fiberglass segment is expected to register the second-fastest growth rate in the midstream oil and gas filtration market, in terms of value. This is due to its impressive combination of performance, durability, and cost-effectiveness. Fiberglass media has a large dirt-holding capacity and provides depth filtration, making it highly effective at capturing fine particles and aerosols commonly found in gas and liquid hydrocarbon streams. As a result, applications using fiberglass media offer increased filtration efficiency and extended service life. Furthermore, fiberglass exhibits excellent chemical resistance and thermal stability, allowing it to be used across a wide range of temperatures and pressures. This makes it suitable for demanding conditions in midstream pipelines, compressor stations, and gas processing facilities. Additionally, fiberglass is more affordable compared to expensive synthetic or specialty media while delivering comparable field performance. This makes it particularly popular for large installations. Investment in pipeline and gas infrastructure is a significant factor that will support market growth during the forecast period.

"Based on application, pipeline transportation accounted for the second-largest market share in terms of value."

Pipeline transportation holds the second-largest share of the midstream oil and gas filtration market, primarily due to its critical role in transporting large volumes of crude oil, natural gas, and refined products over long distances. This ensures flow assurance and maintains pipeline integrity. Continuous filtration is essential to remove solids, water, corrosion by-products, and condensates that can lead to erosion, blockages, and internal corrosion. Consequently, there is a constant demand for filters, separators, and coalescers at compressor stations, pump stations, and inlet points. Moreover, the extensive global pipeline network-particularly well developed in North America, the Middle East, and Russia-creates a large installed filtration capacity while still requiring ongoing filter replacements. Additionally, stringent safety regulations and standards regarding pipeline integrity, emissions control, and operational reliability compel operators to invest in high-quality filtration systems. This further strengthens pipeline transportation's prominent position in the market.

"Based on region, Asia Pacific is the second-largest market for midstream oil & gas filtration in terms of value."

The Asia Pacific region is the second-largest market for midstream oil and gas filtration systems, driven by industrialization, urbanization, and rising energy demand in countries like China, India, and those in Southeast Asia. The midstream infrastructure, which includes pipelines, LNG terminals, storage facilities, and gas processing plants, is currently in need of significant investment. This investment is essential to implementing efficient, reliable filtration systems. Additionally, governments in the region are focused on enhancing energy security by promoting natural gas as a cleaner fuel. As a result, pipeline networks and LNG import capacities are expanding. The strong regulatory emphasis on operational efficiency and environmental compliance, coupled with the growing involvement of global oil and gas companies, is driving the rapid growth of advanced filtration technology. Consequently, the Asia Pacific region has become the fastest-growing market for these solutions worldwide.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

- By Company Type: Tier 1 - 60%, Tier 2 - 20%, and Tier 3 - 20%

- By Designation: C Level - 33%, Director Level - 33%, and Managers - 34%

- By Region: North America - 20%, Europe - 25%, Asia Pacific - 25%, Middle East & Africa - 15%, and South America - 15%

The report provides a comprehensive analysis of company profiles on:

Prominent companies are Pall Corporation (US), Jonell Systems (US), Parker Hannifin (US), Eaton (Ireland), Pentair (US), Graver Technologies (US), 3M (US), CECO Environmental (US), FTC Filters (US), Clark Reliance (US), Hilliard Corporation (US), EnerWells (US), Saifilter (China), TM Filtration (US), Brother Filtration (China), Swift Filter (US), Fil-Trek (Canada), and Donaldson (US).

Research Coverage

This research report categorizes the midstream oil & gas filtration market by membrane type (hollow fiber, flat sheet, multi-tubular), system configuration (submerged MBR system, external MBR system), capacity (small capacity, medium capacity, large capacity), application, and region (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The scope of the report includes detailed information on the major factors influencing the growth of the midstream oil & gas filtration market, including drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted to provide insights into their business overview, solutions and services, key strategies, contracts, partnerships, and agreements. Product launches, mergers and acquisitions, and recent developments in the midstream oil & gas filtration market are all covered. This report includes a competitive analysis of upcoming startups in the midstream oil & gas filtration market ecosystem.

Reasons to buy this report:

The report will help market leaders/new entrants in this market by providing revenue approximations for the overall midstream oil & gas filtration market and its subsegments. This report will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (surge in LNG and midstream capacity buildout, aging pipeline & storage infrastructure, shifting production patterns & energy security moves), restraints (CAPEX volatility & project delays reduce equipment orders, high upfront cost and long payback hinder adoption in developing regions, alternative separation technologies and digital solutions create competitive pressure), opportunities (rising hydrocarbon production & associated gas, digitalization, predictive maintenance & analytics for filtration lifecycle monetization, energy transition-new product classes & retrofit demand), and challenges (supply-chain stress, raw-material inflation and delivery lead times, operational challenges-feed variability, fouling, and higher O&M costs).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the midstream oil & gas filtration market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the midstream oil & gas filtration market across varied regions.

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the midstream oil & gas filtration market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Pall Corporation (US), Jonell Systems (US), Parker Hannifin (US), Eaton (Ireland), Pentair (US), Graver Technologies (US), 3M (US), CECO Environmental (US), FTC Filters (US), Clark Reliance (US), Hilliard Corporation (US), EnerWells (US), Saifilter (China), TM Filtration (US), Brother Filtration (China), Swift Filter (US), Fil-Trek (Canada), and Donaldson (US), among others, in the midstream oil & gas filtration market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MIDSTREAM OIL & GAS FILTRATION MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MIDSTREAM OIL & GAS FILTRATION MARKET

- 3.2 MIDSTREAM OIL & GAS FILTRATION MARKET, BY FILTER TECHNOLOGY AND REGION

- 3.3 MIDSTREAM OIL & GAS FILTRATION MARKET, BY FILTER MEDIA

- 3.4 MIDSTREAM OIL & GAS FILTRATION MARKET, BY APPLICATION

- 3.5 MIDSTREAM OIL & GAS FILTRATION MARKET, BY FILTRATION PHASE

- 3.6 MIDSTREAM OIL & GAS FILTRATION MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Surge in LNG and midstream capacity buildout

- 4.2.1.2 Aging pipeline & storage infrastructure

- 4.2.1.3 Tightening emissions/methane & air-pollution regulations

- 4.2.1.4 Shifting production patterns & energy security moves

- 4.2.2 RESTRAINTS

- 4.2.2.1 Capex volatility & project delays reduce equipment orders

- 4.2.2.2 High upfront cost and long payback hinder adoption in developing regions

- 4.2.2.3 Alternative separation technologies and digital solutions create competitive pressure

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growth in hydrocarbon output and associated gas volumes

- 4.2.3.2 Digitalization, predictive maintenance, and analytics for filtration lifecycle monetization

- 4.2.3.3 Energy transition led product innovation and retrofit demand

- 4.2.4 CHALLENGES

- 4.2.4.1 Supply-chain stress, raw material inflation, and delivery lead times

- 4.2.4.2 Operational challenges such as feed variability, fouling, and higher O&M costs

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN MIDSTREAM OIL & GAS FILTRATION MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL SUPPLIERS

- 5.3.2 MANUFACTURERS

- 5.3.3 DISTRIBUTORS

- 5.3.4 END USERS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING TREND OF MIDSTREAM OIL & GAS FILTRATION SYSTEMS, BY FILTER TECHNOLOGY, 2022-2024

- 5.5.2 PRICING RANGE OF MIDSTREAM OIL & GAS FILTRATION SYSTEMS, BY REGION, 2024

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 842199)

- 5.6.2 EXPORT SCENARIO (HS CODE 842199)

- 5.7 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 NORTH AMERICAN NATURAL GAS PIPELINE OPERATOR IMPROVED OPERATIONAL RELIABILITY AND REDUCED DOWNTIME BY IMPLEMENTING MULTI-STAGE FILTRATION SYSTEM

- 5.10.2 JONELL SYSTEMS: IRON SULFIDE (BLACK POWDER) REMOVAL IN NATURAL-GAS PIPELINE

- 5.11 IMPACT OF 2025 US TARIFF - OVERVIEW

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 US

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ADVANCED FILTER MEDIA: ELECTROSPUN NANOFIBERS, MOF-ENHANCED MEMBRANES, AND HYBRID ADSORPTIVE COATINGS

- 6.1.2 SMART FILTRATION: AI/IOT FOR PREDICTIVE MAINTENANCE, AUTONOMOUS SELF-CLEANING, AND SYSTEMS OPTIMIZATION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ELECTROSTATIC AND ULTRASONIC COALESCENCE

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM ROADMAP: PILOT DEPLOYMENT AND DIGITAL FOUNDATIONS

- 6.3.2 MID-TERM ROADMAP: SCALE-UP, SMART FILTRATION, & AUTOMATION

- 6.3.3 LONG-TERM ROADMAP: FULL AUTOMATION, DIGITAL TWINS, & OUTCOME-BASED MODELS

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 LEGAL STATUS OF PATENTS

- 6.4.3 JURISDICTION ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 HYDROGEN AND LOW-CARBON FUEL TRANSPORTATION FILTRATION

- 6.5.2 LNG AND SMALL-SCALE MODULAR GAS PROCESSING UNITS

- 6.5.3 CARBON CAPTURE, UTILIZATION, & STORAGE (CCUS) TRANSPORT FILTRATION

- 6.5.4 DIGITAL TWIN-DRIVEN AUTONOMOUS COMPRESSOR STATIONS

- 6.5.5 RENEWABLE NATURAL GAS (RNG) AND BIOGAS PIPELINE INJECTION

- 6.6 IMPACT OF AI/GEN AI ON MIDSTREAM OIL & GAS FILTRATION MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN MIDSTREAM OIL & GAS FILTRATION PROCESSING

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN MIDSTREAM OIL & GAS FILTRATION MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN MIDSTREAM OIL & GAS FILTRATION MARKET

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

9 MIDSTREAM OIL & GAS FILTRATION MARKET, BY FILTER TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 COALESCER FILTERS

- 9.2.1 IMPROVED DOWNSTREAM EQUIPMENT RELIABILITY AND COMPLIANCE WITH QUALITY SPECIFICATIONS TO DRIVE MARKET

- 9.3 CARTRIDGE FILTERS

- 9.3.1 STRENGTHENING OPERATIONAL RELIABILITY WITH HIGH-PRECISION FINE PARTICULATE FILTRATION TO PROPEL MARKET

- 9.4 MECHANICAL FILTERS

- 9.4.1 ENSURING PIPELINE INTEGRITY VIA ROBUST BULK SOLID REMOVAL SOLUTIONS TO SUPPORT MARKET GROWTH

- 9.5 BAG FILTERS

- 9.5.1 LOWER FILTRATION COSTS WITH HIGH-FLOW, HIGH-CAPACITY PARTICULATE HANDLING-KEY FACTOR DRIVING MARKET GROWTH

- 9.6 PARTICULATE FILTERS

- 9.6.1 MAXIMIZING EQUIPMENT LIFESPAN THROUGH HIGH-EFFICIENCY PARTICLE CONTROL TO DRIVE MARKET

- 9.7 ACTIVATED CARBON FILTERS

- 9.7.1 IMPROVED PRODUCT PURITY AND EMISSIONS COMPLIANCE THROUGH ADVANCED ADSORPTION TECHNOLOGIES TO PROPEL MARKET

- 9.8 STRAINERS

- 9.8.1 ENHANCING SYSTEM PROTECTION THROUGH FIRST-LINE DEFENSE AGAINST LARGE DEBRIS TO DRIVE MARKET

- 9.9 OTHER FILTER TECHNOLOGIES

10 MIDSTREAM OIL & GAS FILTRATION MARKET, BY FILTER MEDIA

- 10.1 INTRODUCTION

- 10.2 ACTIVATED CARBON

- 10.2.1 STRICTER VOC, H2S, AND EMISSIONS CONTROL REGULATIONS ACROSS MIDSTREAM OPERATIONS TO DRIVE MARKET

- 10.3 METALLIC

- 10.3.1 NEED FOR HIGH-TEMPERATURE, HIGH-PRESSURE, AND CORROSION-RESISTANT FILTRATION SOLUTIONS TO PROPEL MARKET

- 10.4 SYNTHETIC POLYMER

- 10.4.1 MOST WIDELY USED FILTRATION MATERIAL IN MIDSTREAM OIL & GAS OPERATIONS

- 10.5 FIBERGLASS

- 10.5.1 RISING REQUIREMENTS FOR ULTRA-FINE AEROSOL AND SUB-MICRON GAS FILTRATION IN COMPRESSOR PROTECTION TO DRIVE MARKET

- 10.6 OTHER FILTER MEDIA

11 MIDSTREAM OIL & GAS FILTRATION MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 GAS PROCESSING PLANTS

- 11.2.1 NEED FOR HIGH-PERFORMANCE, MULTI-STAGE FILTRATION SYSTEMS TO DRIVE MARKET

- 11.3 COMPRESSION STATIONS

- 11.3.1 NEED TO PROTECT HIGH-VALUE COMPRESSORS FROM CONTAMINATION AND WEAR TO PROPEL MARKET

- 11.4 STORAGE & DISTRIBUTION

- 11.4.1 RISING FUEL QUALITY STANDARDS AND TERMINAL AUTOMATION INITIATIVES TO DRIVE MARKET

- 11.5 PIPELINE TRANSPORTATION

- 11.5.1 NEED FOR CONTINUOUS FLOW ASSURANCE AND PIPELINE ASSET PROTECTION TO DRIVE MARKET

- 11.6 LNG PROCESSING

- 11.6.1 RISE IN GLOBAL LNG TRADE TO DRIVE MARKET

- 11.7 OTHER APPLICATIONS

12 MIDSTREAM OIL & GAS FILTRATION MARKET, BY FILTRATION PHASE

- 12.1 INTRODUCTION

- 12.2 OIL FILTRATION

- 12.2.1 RISING NEED FOR CLEAN CRUDE AND REFINED PRODUCT FLOW IN LONG-DISTANCE PIPELINES TO PROPEL MARKET

- 12.3 GAS FILTRATION

- 12.3.1 EXPANSION OF HIGH-PRESSURE GAS TRANSMISSION AND LNG FEED GAS INFRASTRUCTURE TO DRIVE MARKET

13 MIDSTREAM OIL & GAS FILTRATION MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 REFINERIES

- 13.3 PETROCHEMICAL INDUSTRY

14 MIDSTREAM OIL & GAS FILTRATION MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Surging LNG capacity to drive sustained growth in midstream filtration systems

- 14.2.2 CANADA

- 14.2.2.1 LNG buildout to catalyze demand for high-performance midstream filtration and tertiary water treatment

- 14.2.3 MEXICO

- 14.2.3.1 Pemex deepwater investment and pipeline modernization to drive urgent demand for high-pressure filtration

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Rapid LNG terminal buildout to boost demand for cryogenic and pre-treatment filtration

- 14.3.2 UK

- 14.3.2.1 Gas system reforms and resilience planning to drive upgrades in midstream filtration and monitoring

- 14.3.3 FRANCE

- 14.3.3.1 Growing LNG import mix and storage strategy to increase demand for cryogenic and metering filtration

- 14.3.4 ITALY

- 14.3.4.1 Rapid LNG import growth to drive investment in pre-treatment and cryogenic filtration

- 14.3.5 RUSSIA

- 14.3.5.1 Large domestic pipeline network to sustain strong demand for high-pressure filtration and integrity solutions

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Pipeline density and storage expansion to power China's midstream filtration demand

- 14.4.2 INDIA

- 14.4.2.1 National pipeline interconnectivity and city gas distribution to drive filtration growth

- 14.4.3 JAPAN

- 14.4.3.1 Terminal modernization and carbon-control systems to propel filtration investment

- 14.4.4 AUSTRALIA

- 14.4.4.1 Produced-water management and long-distance pipeline protection to drive filtration demand

- 14.4.5 SOUTH KOREA

- 14.4.5.1 Energy security policies and infrastructure resilience to increase filtration spending

- 14.4.6 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 SAUDI ARABIA

- 14.5.1.1 Jafurah and main-network upgrades to drive demand for high-pressure and cryogenic filtration

- 14.5.2 UAE

- 14.5.2.1 Pipeline extensions and strategic midstream pacts to accelerate filtration capex and aftermarket spend

- 14.5.3 SOUTH AFRICA

- 14.5.3.1 Gas masterplan implementation and onshore industrialization to drive filtration demand

- 14.5.4 REST OF MIDDLE EAST & AFRICA

- 14.5.1 SAUDI ARABIA

- 14.6 SOUTH AMERICA

- 14.6.1 BRAZIL

- 14.6.1.1 Pre-salt ramp-up and offshore maintenance cycles to drive strong demand for high-pressure and cryogenic filtration

- 14.6.2 ARGENTINA

- 14.6.2.1 Vaca Muerta's scale-up and new evacuation pipelines to catalyze midstream filtration investment

- 14.6.3 REST OF SOUTH AMERICA

- 14.6.1 BRAZIL

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 15.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN MIDSTREAM OIL & GAS FILTRATION MARKET BETWEEN JANUARY 2020 AND NOVEMBER 2025

- 15.3 REVENUE ANALYSIS, 2022-2024

- 15.4 MARKET SHARE ANALYSIS, 2024

- 15.4.1 PARKER HANNIFIN

- 15.4.2 EATON

- 15.4.3 PALL CORPORATION

- 15.4.4 3M

- 15.4.5 PENTAIR

- 15.5 COMPANY VALUATION AND FINANCIAL METRICS

- 15.6 BRAND/PRODUCT COMPARISON ANALYSIS

- 15.6.1 PALL CORPORATION

- 15.6.2 PARKER HANNIFIN

- 15.6.3 EATON

- 15.6.4 PENTAIR

- 15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 15.7.1 STARS

- 15.7.2 EMERGING LEADERS

- 15.7.3 PERVASIVE PLAYERS

- 15.7.4 PARTICIPANTS

- 15.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 15.7.5.1 Company footprint

- 15.7.5.2 Region footprint

- 15.7.5.3 Filter technology footprint

- 15.7.5.4 Filter media footprint

- 15.7.5.5 Application footprint

- 15.7.5.6 Filtration phase footprint

- 15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 15.8.1 PROGRESSIVE COMPANIES

- 15.8.2 RESPONSIVE COMPANIES

- 15.8.3 DYNAMIC COMPANIES

- 15.8.4 STARTING BLOCKS

- 15.8.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2024

- 15.8.5.1 Detailed list of key startups/SMEs

- 15.8.5.2 Competitive benchmarking of key startups/SMEs

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

- 15.9.4 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 PALL CORPORATION

- 16.1.1.1 Business overview

- 16.1.1.2 Products/Solutions/Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches

- 16.1.1.3.2 Expansions

- 16.1.1.3.3 Other developments

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 JONELL SYSTEMS

- 16.1.2.1 Business overview

- 16.1.2.2 Products/Solutions/Services offered

- 16.1.2.3 MnM view

- 16.1.2.3.1 Key strengths

- 16.1.2.3.2 Strategic choices

- 16.1.2.3.3 Weaknesses and competitive threats

- 16.1.3 PARKER HANNIFIN

- 16.1.3.1 Business overview

- 16.1.3.2 Products/Solutions/Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 EATON

- 16.1.4.1 Business overview

- 16.1.4.2 Products/Solutions/Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches

- 16.1.4.3.2 Expansions

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 PENTAIR

- 16.1.5.1 Business overview

- 16.1.5.2 Products/Solutions/Services offered

- 16.1.5.3 MnM view

- 16.1.5.3.1 Key strengths

- 16.1.5.3.2 Strategic choices

- 16.1.5.3.3 Weaknesses and competitive threats

- 16.1.6 GRAVER TECHNOLOGIES

- 16.1.6.1 Business overview

- 16.1.6.2 Products/Solutions/Services offered

- 16.1.6.3 MnM view

- 16.1.6.3.1 Key strengths

- 16.1.6.3.2 Strategic choices

- 16.1.6.3.3 Weaknesses and competitive threats

- 16.1.7 3M

- 16.1.7.1 Business overview

- 16.1.7.2 Products/Solutions/Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Deals

- 16.1.7.4 MnM view

- 16.1.7.4.1 Key strengths

- 16.1.7.4.2 Strategic choices

- 16.1.7.4.3 Weaknesses and competitive threats

- 16.1.8 CECO ENVIRONMENTAL

- 16.1.8.1 Business overview

- 16.1.8.2 Products/Solutions/Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Deals

- 16.1.8.4 MnM view

- 16.1.8.4.1 Key strengths

- 16.1.8.4.2 Strategic choices

- 16.1.8.4.3 Weaknesses and competitive threats

- 16.1.9 FTC FILTERS

- 16.1.9.1 Business overview

- 16.1.9.2 Products/Solutions/Services offered

- 16.1.9.3 MnM view

- 16.1.9.3.1 Key strengths

- 16.1.9.3.2 Strategic choices

- 16.1.9.3.3 Weaknesses and competitive threats

- 16.1.10 CLARK-RELIANCE

- 16.1.10.1 Business overview

- 16.1.10.2 Products/Solutions/Services offered

- 16.1.10.3 MnM view

- 16.1.10.3.1 Key strengths

- 16.1.10.3.2 Strategic choices

- 16.1.10.3.3 Weaknesses and competitive threats

- 16.1.11 HILLIARD CORPORATION

- 16.1.11.1 Business overview

- 16.1.11.2 Products/Solutions/Services offered

- 16.1.11.3 MnM view

- 16.1.11.3.1 Key strengths

- 16.1.11.3.2 Strategic choices

- 16.1.11.3.3 Weaknesses and competitive threats

- 16.1.12 ENERWELLS

- 16.1.12.1 Business overview

- 16.1.12.2 Products/Solutions/Services offered

- 16.1.12.3 MnM view

- 16.1.12.3.1 Key strengths

- 16.1.12.3.2 Strategic choices

- 16.1.12.3.3 Weaknesses and competitive threats

- 16.1.13 SAIFILTER

- 16.1.13.1 Business overview

- 16.1.13.2 Products/Solutions/Services offered

- 16.1.13.3 MnM view

- 16.1.13.3.1 Key strengths

- 16.1.13.3.2 Strategic choices

- 16.1.13.3.3 Weaknesses and competitive threats

- 16.1.14 TM FILTRATION

- 16.1.14.1 Business overview

- 16.1.14.2 Products/Solutions/Services offered

- 16.1.14.3 MnM view

- 16.1.14.3.1 Key strengths

- 16.1.14.3.2 Strategic choices

- 16.1.14.3.3 Weaknesses and competitive threats

- 16.1.15 BROTHER FILTRATION

- 16.1.15.1 Business overview

- 16.1.15.2 Products/Solutions/Services offered

- 16.1.15.3 MnM view

- 16.1.15.3.1 Key strengths

- 16.1.15.3.2 Strategic choices

- 16.1.15.3.3 Weaknesses and competitive threats

- 16.1.16 SWIFT FILTER

- 16.1.16.1 Business overview

- 16.1.16.2 Products/Solutions/Services offered

- 16.1.16.3 MnM view

- 16.1.16.3.1 Key strengths

- 16.1.16.3.2 Strategic choices

- 16.1.16.3.3 Weaknesses and competitive threats

- 16.1.17 FIL-TREK

- 16.1.17.1 Business overview

- 16.1.17.2 Products/Solutions/Services offered

- 16.1.17.3 MnM view

- 16.1.18 DONALDSON

- 16.1.18.1 Business overview

- 16.1.18.2 Products/Solutions/Services offered

- 16.1.18.3 MnM view

- 16.1.18.3.1 Key strengths

- 16.1.18.3.2 Strategic choices

- 16.1.18.3.3 Weaknesses and competitive threats

- 16.1.1 PALL CORPORATION

- 16.2 OTHER PLAYERS

- 16.2.1 PS FILTER

- 16.2.2 SMITHS GROUP

- 16.2.3 CRITICAL PROCESS FILTRATION

- 16.2.4 HOFF ENGINEERING

- 16.2.5 CLEANOVA

- 16.2.6 NORMAN FILTER COMPANY

- 16.2.7 COLEMAN FILTER COMPANY

- 16.2.8 FILTERS S.P.A

- 16.2.9 FILTER SCIENCES

- 16.2.10 CHASE FILTERS

- 16.2.11 MUELLER ENVIRONMENTAL

- 16.2.12 KINGTOOL

- 16.2.13 GAS TECH

- 16.2.14 ROYAL PRODUCTS

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 List of key secondary sources

- 17.1.1.2 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 List of primary interview participants-demand and supply sides

- 17.1.2.3 Breakdown of primary interviews

- 17.1.2.4 Key industry insights

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.3 BASE NUMBER CALCULATION

- 17.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 17.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 17.4 MARKET FORECAST APPROACH

- 17.4.1 SUPPLY SIDE

- 17.4.2 DEMAND SIDE

- 17.5 DATA TRIANGULATION

- 17.6 FACTOR ANALYSIS

- 17.7 RESEARCH ASSUMPTIONS

- 17.8 LIMITATIONS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS