|

시장보고서

상품코드

1931744

UV 경화 시스템 시장 : 기술별, 시스템 유형별, 압력 유형별, 구성요소별, 용도별, 업계별, 지역별 - 세계 예측(-2032년)UV Curing System Market by System Type, Technology, Application, Vertical and Region - Global Forecast To 2032 |

||||||

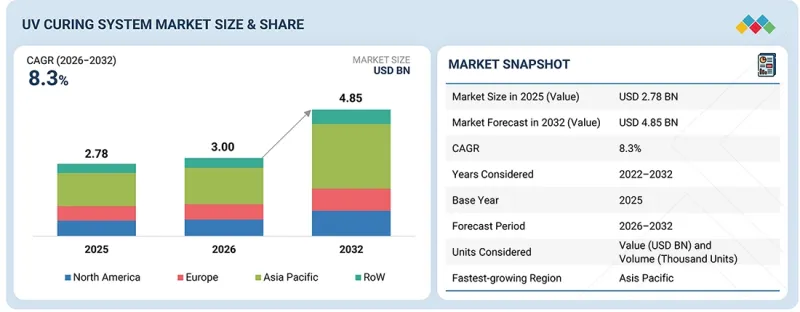

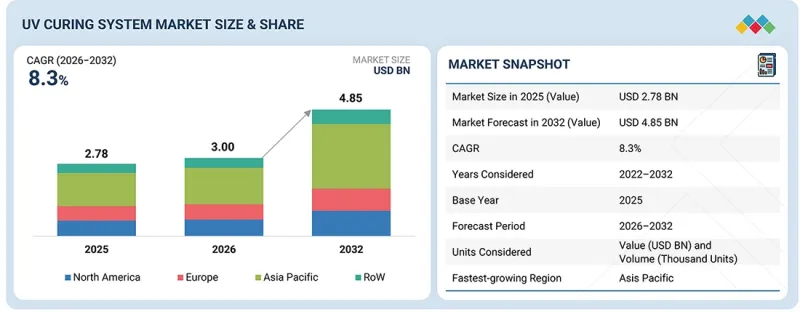

세계의 UV 경화 시스템 시장 규모는 2026년에 30억 달러 규모에 달할 것으로 예측됩니다. 예측 기간 동안 CAGR 8.3%로 성장하여 2032년까지 48억 5,000만 달러 규모에 달할 것으로 예상됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2032년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 기술별, 시스템 유형별, 압력 유형별, 구성요소별, 용도별, 업계별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

저압 UV 경화 시스템은 예측 기간 동안 가장 높은 CAGR을 달성 할 것으로 예상됩니다. 이러한 성장은 우수한 에너지 효율성, 저발열성, 정밀 및 열에 민감한 응용 분야에 대한 적응성에 기인합니다. 제어된 경화 강도와 최소한의 열 영향이 필수적인 전자기기, 의료기기, 특수 코팅 등의 산업 분야에서 이러한 시스템의 활용이 확대되고 있습니다. 에너지 소비 감소와 수은 사용 제한에 대한 규제 압력이 높아지면서 저압 및 UV LED 기반 솔루션으로의 전환이 가속화되고 있습니다. 또한, 램프 효율 향상, 수명 연장, 컴팩트한 시스템 설계, 기술 비용 절감과 함께 소규모, 자동화, 고부가가치 제조 공정에서의 적용 범위가 확대되고 있습니다.

접착제 분야는 전자기기, 의료기기, 자동차 부품, 포장, 산업용 조립 등 다양한 산업에서 광범위하게 사용되어 UV 경화 시스템의 가장 큰 시장을 견인할 것으로 예상됩니다. UV 경화형 접착제는 빠른 접착, 고강도, 정밀한 도포 등의 이점을 제공하며, 빠르고 자동화된 제조 공정을 지원합니다. 저온에서의 경화 능력은 특히 전자 및 의료 응용 분야에서 열에 민감한 부품 및 소형 부품에 특히 적합합니다. 경량 소재, 소형 장치 조립, 제품 내구성 향상에 대한 수요 증가는 UV 경화형 접착제의 채택을 더욱 촉진하고 있습니다. 이러한 접착제는 낮은 VOC 배출, 깨끗한 가공, 안정적인 성능으로 알려져 있으며, 예측 기간 동안 시장에서의 우위를 강화할 것입니다.

아시아태평양은 예측 기간 동안 UV 경화 시스템의 최대 시장을 주도할 것으로 예상됩니다. 이러한 성장은 이 지역의 탄탄한 제조 기반과 인쇄, 포장, 전자, 자동차, 산업 생산 등의 분야에서 시설의 고밀도 집적에 기인합니다. 중국, 일본, 한국, 인도 등의 국가는 전자기기 조립, 포장 가공, 자동차 부품 제조에 크게 기여하고 있으며, 이는 고속 경화 솔루션에 대한 지속적인 수요를 견인하고 있습니다. 또한, 이 지역은 비용 경쟁력 있는 제조, 광범위한 위탁 생산 네트워크, 지속적인 생산능력 확장의 혜택을 누리고 있습니다. 또한, 자동화 보급 확대, 에너지 절약 및 지속가능한 생산 기술에 대한 관심 증가, 수출 지향적 산업의 강력한 수요는 예측 기간 동안 아시아태평양의 시장 주도적 지위를 더욱 강화할 것으로 보입니다.

UV 경화 시스템 시장의 다양한 부문 및 하위 부문의 시장 규모를 확정하고 검증하기 위해 주요 업계 전문가를 대상으로 광범위한 1차 조사를 실시했습니다.

UV 경화 시스템 시장 보고서는 주로 Excelitas Technologies Corp.(미국), Nordson Corporation(미국), IST METZ GmbH & Co. 상세한 기업 개요, 최근 동향, 주요 시장 전략이 포함되어 있습니다. 이 보고서는 UV 경화 시스템 시장의 주요 기업들에 대한 종합적인 경쟁 분석을 제공합니다. 상세한 기업 개요, 최근 동향, 주요 시장 전략이 포함되어 있습니다.

조사 범위:

이 보고서는 UV 경화 시스템 시장을 세분화하여 분석합니다. 시스템 유형별, 압력 유형별, 부품별, 용도별, 산업별 예측을 제공합니다.

본 보고서에서는 산업 성장에 영향을 미치는 주요 시장 촉진요인, 저해요인, 기회, 도전과제를 분석합니다. 또한 북미, 유럽, 아시아태평양 및 기타 지역(ROW)에 대한 상세한 지역별 평가와 함께 주요 시장의 국가별 인사이트도 포함되어 있습니다. 또한, 가치사슬 분석과 세계 UV 경화 시스템 생태계의 주요 진입기업들의 경쟁 상황을 평가한 것이 특징입니다.

본 보고서 구매의 주요 이점:

- 주요 촉진요인 분석(고속 및 친환경 경화에 대한 관심 증가, 전자기기 제조에서 정밀 경화에 대한 수요 증가), 억제요인(초기 투자 규모, 경화 깊이 및 재료 적합성 문제), 기회(제조 자동화 및 스마트 팩토리 통합의 진전), 과제(UV 수은 램프 관련 위험)

- 제품 개발 및 혁신 : UV 경화 시스템 시장의 신기술 동향, 연구개발 활동, 제품 출시에 대한 상세한 정보

- 시장 개발 : 다양한 지역의 수익성 높은 시장에 대한 종합적인 정보를 제공합니다.

- 시장 다각화 : UV 경화 시스템 시장의 신제품, 미개척 지역, 최근 동향, 투자에 대한 종합적인 정보

- 경쟁사 평가 : 주요 기업 - Excelitas Technologies Corp.(미국), Nordson Corporation(미국), IST METZ GmbH & Co. KG(독일), BW Converting(미국), Dymax(미국), Hoenle AG(독일), American Ultraviolet(미국), Hanovia(미국), GEW Limited(영국), Uvitron International, Inc.(미국) 등 주요 기업의 시장 점유율 및 성장 전략에 대한 상세한 평가

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 미충족 수요와 공백

- 상호 접속된 시장과 분야 횡단적인 기회

- 티어1/2/3 참여 기업별 전략적 활동

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제 전망

- 밸류체인 분석

- 생태계 분석

- 가격 분석

- 무역 분석

- 2026년의 주요 회의와 이벤트

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 투자와 자금 조달 시나리오, 2021-2024년

- 사례 연구 분석

- 2025년 미국 관세의 영향 - UV 경화 시스템 시장

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신

- 주요 신기술

- 보완적 기술

- 인접 기술

- 기술/제품 로드맵

- 특허 분석

- UV 경화 시스템 시장에서 AI의 영향

제7장 규제 상황

- 지역 규제와 컴플라이언스

- 규제기관, 정부기관, 기타 조직

- 표준

- 정부 규제

제8장 고객 상황과 구매 행동

- 의사결정 프로세스

- 구매 프로세스에 관여하는 주요 이해관계자와 그 평가 기준

- 채용 장벽과 내부 과제

- 다양한 용도 미충족 수요

제9장 UV 경화 시스템 판매 채널

- 직접 판매

- 판매대리점

- 시스템 통합사업자

- 온라인/E-Commerce

제10장 UV 경화 시스템 분석 - 경화 면적/사이즈

- 소면적 경화

- 중면적 경화

- 대면적 경화

제11장 UV 경화 시스템의 통합 레벨

- 독립형

- 통합형

- 개조

제12장 UV 경화 시스템 시장(기술별)

- 기존 UV/수은 램프 경화

- UV LED 경화

- 하이브리드 경화

제13장 UV 경화 시스템 시장(시스템 유형별)

- 스팟 경화 시스템

- 플러드 경화 시스템

- 휴대용/핸드헬드 경화 시스템

- 컨베이어/인라인 시스템

제14장 UV 경화 시스템 시장(압력 유형별)

- 고

- 중

- 저

제15장 UV 경화 시스템 시장(구성요소별)

- 하드웨어

- 소프트웨어

- 서비스

제16장 UV 경화 시스템 시장(용도별)

- 코팅

- 잉크

- 접착제

- 3D 프린팅

- 전자부품

- 광섬유 코팅

- 기타

제17장 UV 경화 시스템 시장(업계별)

- 산업 제조업

- 자동차

- 일렉트로닉스

- 포장

- 인쇄

- 항공우주 및 방위

- 헬스케어/의료기기

- 목재와 가구

- 기타

제18장 UV 경화 시스템 시장(지역별)

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 멕시코

- 유럽

- 유럽의 거시경제 전망

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 벨기에

- 북유럽

- 기타

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 중국

- 호주

- 일본

- 인도

- 한국

- 동남아시아

- 기타

- 기타 지역

- 기타 지역의 거시경제 전망

- 중동

- 아프리카

- 남미

제19장 경쟁 구도

- 개요

- 주요 진출 기업의 전략/강점, 2021-2025년

- 시장 점유율 분석, 2025년

- 브랜드/제품 비교

- 기업 평가 매트릭스 : 주요 진출 기업, 2025년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2025년

- 경쟁 시나리오

제20장 기업 개요

- 주요 진출 기업

- EXCELITAS TECHNOLOGIES CORP.

- NORDSON CORPORATION

- DYMAX

- IST METZ GMBH & CO. KG

- BW CONVERTING

- AMERICAN ULTRAVIOLET

- HANOVIA

- HOENLE AG

- GEW(EC) LIMITED

- FUJIFILM EUROPE GMBH

- 기타 기업

- UVITRON INTERNATIONAL, INC.

- MILTEC UV

- JENTON GROUP

- ATLANTIC ZEISER GMBH

- UVEXS INC.

- APL MACHINERY PVT. LTD.

- KYOCERA CORPORATION

- SENLIAN AUTOMATIC COATING MACHINERY CO., LTD.

- DOCTORUV

- USHIO INC.

- PROPHOTONIX LIMITED

- BENFORD

- ALPHA-CURE

- SEOUL VIOSYS CO., LTD.

- THORLABS, INC.

- AETEK, INC.

제21장 조사 방법

제22장 부록

KSM 26.02.25The global UV curing system market is estimated to be valued at USD 3.00 billion in 2026. It is projected to reach USD 4.85 billion by 2032 at a CAGR of 8.3% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By System Type, Technology, Component, Application, Vertical and Region |

| Regions covered | North America, Europe, APAC, RoW |

"By pressure type, the low segment is projected to witness the highest CAGR during the forecast period."

Low-pressure UV curing systems are expected to experience the highest compound annual growth rate (CAGR) during the forecast period. This growth can be attributed to their superior energy efficiency, low heat generation, and suitability for precision and heat-sensitive applications. These systems are increasingly used in industries, such as electronics, medical devices, and specialty coatings, where controlled curing intensity and minimal thermal impact are essential. Growing regulatory pressure to reduce energy consumption and limit mercury usage is driving the shift toward low-pressure and UV LED-based solutions. Additionally, advancements in lamp efficiency, longer operational lifetimes, compact system designs, and decreasing technology costs are broadening their applicability in small-scale, automated, and high-value manufacturing processes.

"By application, the adhesives segment is projected to account for the largest market size during the forecast period."

The adhesives segment is projected to lead the largest market for UV curing systems due to their extensive use in various industries, including electronics, medical devices, automotive components, packaging, and industrial assembly. UV-cured adhesives provide advantages, such as rapid bonding, high strength, and precise application, which support fast and automated manufacturing processes. Their ability to cure at low temperatures makes them particularly suitable for heat-sensitive and miniaturized components, especially in electronics and medical applications. The rising demand for lightweight materials, compact device assembly, and enhanced product durability is further driving the adoption of UV-cured adhesives. These adhesives are known for their low VOC emissions, clean processing, and consistent performance, which reinforce their dominant position in the market throughout the forecast period.

"Asia Pacific is projected to account for the largest market during the forecast period."

Asia Pacific is projected to lead the largest market for UV curing systems during the forecast period. This growth can be attributed to the region's robust manufacturing base and high concentration of facilities in sectors, such as printing, packaging, electronics, automotive, and industrial production. Countries like China, Japan, South Korea, and India contribute significantly to electronics assembly, packaging conversion, and automotive component manufacturing, which drive ongoing demand for high-speed curing solutions. Additionally, this region benefits from cost-competitive manufacturing, a vast network of contract manufacturers, and continuous capacity expansions. Also, the growing adoption of automation, increasing awareness of energy-efficient and sustainable production technologies, and strong demand from export-oriented industries further reinforce Asia Pacific's leading market position during the forecast period.

To determine and verify the market size for various segments and sub-segments in the UV curing system market, extensive primary interviews were conducted with key industry experts.

The breakdown of primary participants for the report is detailed below.

- By Company Type: Tier 1 - 55%, Tier 2 - 25%, and Tier 3 - 20%

- By Designation: Directors - 50%, Managers - 30%, and Others - 20%

- By Region: North America - 45%, Europe - 30%, Asia Pacific - 20%, and RoW - 5%

The UV curing system market is primarily dominated by several well-established global players, including Excelitas Technologies Corp. (US), Nordson Corporation (US), IST METZ GmbH & Co. KG (Germany), BW Converting (US), Dymax (US), Hoenle AG (Germany), American Ultraviolet (US), Hanovia (US), GEW Limited (UK), Uvitron International, Inc. (US). This study provides a comprehensive competitive analysis of these key players in the UV curing system market. It includes detailed company profiles, recent developments, and key market strategies.

Study Coverage:

The report segments the UV curing system market. It provides forecasts for segments, by system type (spot curing system, portable/handheld curing system, flood curing system, and conveyor/inline curing system), technology (conventional UV/mercury lamp curing, UV LED curing, and hybrid curing (LED + lamp), pressure type (high, medium, and low)), component (hardware, software, and services), application (coatings, inks, adhesives, 3D printing, electronics, optical fiber coatings, and other applications), vertical (industrial manufacturing, automotive, electronics, packaging, printing, aerospace and defense, healthcare and medical devices, wood and furniture, and other verticals).

The report analyzes key market drivers, restraints, opportunities, and challenges that influence industry growth. Furthermore, the report includes a detailed regional assessment of North America, Europe, Asia Pacific, and the Rest of the World, along with insights at the country level for major markets. Moreover, the study features value chain analysis and a competitive landscape assessment of leading players in the global UV curing system ecosystem.

Key Benefits of Buying the Report:

- Analysis of key drivers (growing emphasis on high-speed, eco-friendly curing; rising demand for precision curing in electronics manufacturing), restraints (requirement for high initial investments, curing depth and material compatibility issues), opportunities (rising manufacturing automation and smart factory integration), challenges (risks associated with UV mercury lamps)

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the UV curing system market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the UV curing system market

- Competitive Assessment: In-depth assessment of market share and growth strategies of leading players, such as Excelitas Technologies Corp. (US), Nordson Corporation (US), IST METZ GmbH & Co. KG (Germany), BW Converting (US), Dymax (US), Hoenle AG (Germany), American Ultraviolet (US), Hanovia (US), GEW Limited (UK), and Uvitron International, Inc. (US)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING UV CURING SYSTEM MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN UV CURING SYSTEM MARKET

- 3.2 UV CURING SYSTEM MARKET, BY SYSTEM TYPE

- 3.3 UV CURING SYSTEM MARKET, BY TECHNOLOGY

- 3.4 UV CURING SYSTEM MARKET, BY COMPONENT

- 3.5 UV CURING SYSTEM MARKET, BY APPLICATION

- 3.6 UV CURING SYSTEM MARKET, BY REGION

- 3.7 UV CURING SYSTEM MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing emphasis on high-speed, eco-friendly curing

- 4.2.1.2 Rising demand for precision curing in electronics manufacturing

- 4.2.2 RESTRAINTS

- 4.2.2.1 Requirement for high initial investments

- 4.2.2.2 Curing depth and material compatibility issues

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising manufacturing automation and smart factory integration

- 4.2.3.2 Mounting adoption of UV curing in high-growth sectors

- 4.2.4 CHALLENGES

- 4.2.4.1 Risks associated with UV mercury lamps

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3/ PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 THREAT OF NEW ENTRANTS

- 5.2.2 THREAT OF SUBSTITUTES

- 5.2.3 BARGAINING POWER OF SUPPLIERS

- 5.2.4 BARGAINING POWER OF BUYERS

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN GLOBAL PRINTING INDUSTRY

- 5.3.4 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF UV CURING SYSTEMS OFFERED BY KEY PLAYERS, BY SYSTEM TYPE, 2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF UV CURING SYSTEMS, BY REGION, 2022-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 8539)

- 5.7.2 EXPORT SCENARIO (HS CODE 8539)

- 5.8 KEY CONFERENCES AND EVENTS, 2026

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO, 2021-2024

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 COMMERCIAL PRINTING AND PACKAGING MANUFACTURER IN ASIA PACIFIC USES INLINE UV LED CURING SYSTEM TO INCREASE PRODUCTION THROUGHPUT

- 5.11.2 ELECTRONICS MANUFACTURING SERVICES PROVIDER IN EAST ASIA DEPLOYS UV CURING SYSTEM TO ENABLE MANUFACTURING FLEXIBILITY

- 5.11.3 MEDICAL DEVICE MANUFACTURER IN NORTH AMERICA ADOPTS UV LED CURING SYSTEM TO ENSURE FAST, REPEATABLE CURING OF MEDICAL-GRADE ADHESIVES

- 5.11.4 AUTOMOTIVE COMPONENT SUPPLIER IN EUROPE IMPLEMENTS INLINE UV CURING SYSTEM TO OPTIMIZE PRODUCTION CYCLES AND IMPROVE COST EFFICIENCY

- 5.12 IMPACT OF 2025 US TARIFF - UV CURING SYSTEM MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON VERTICALS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, AND INNOVATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 DIGITAL AND SMART UV CURING SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 THERMAL AND HYBRID CURING SYSTEMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 CONVENTIONAL THERMAL DRYING AND INFRARED (IR) SYSTEMS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027): SYSTEM OPTIMIZATION AND DIGITAL INTEGRATION

- 6.4.2 MID-TERM (2027-2030): HYBRID CURING & PLATFORM SCALABILITY

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI ON UV CURING SYSTEM MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY OEMS IN UV CURING SYSTEM MARKET

- 6.6.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN UV CURING SYSTEM MARKET

- 6.6.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED UV CURING SYSTEMS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 STANDARDS

- 7.1.3 GOVERNMENT REGULATIONS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.5 UNMET NEEDS OF VARIOUS APPLICATIONS

9 UV CURING SYSTEM SALES CHANNELS

- 9.1 INTRODUCTION

- 9.2 DIRECT SALES

- 9.3 DISTRIBUTORS

- 9.4 SYSTEM INTEGRATORS

- 9.5 ONLINE/E-COMMERCE

10 UV CURING SYSTEM ANALYSIS - CURING AREA/SIZE

- 10.1 INTRODUCTION

- 10.2 SMALL AREA CURING

- 10.3 MEDIUM AREA CURING

- 10.4 LARGE AREA CURING

11 INTEGRATION LEVELS OF UV CURING SYSTEMS

- 11.1 INTRODUCTION

- 11.2 STANDALONE

- 11.3 INTEGRATED

- 11.4 RETROFIT

12 UV CURING SYSTEM MARKET, BY TECHNOLOGY

- 12.1 INTRODUCTION

- 12.2 CONVENTIONAL UV/MERCURY LAMP CURING

- 12.2.1 STRONG RADIANT OUTPUT AND DEEP PENETRATION CAPABILITY TO BOLSTER SEGMENTAL GROWTH

- 12.3 UV LED CURING

- 12.3.1 HIGH DEMAND FOR ENERGY-EFFICIENT MANUFACTURING SOLUTIONS TO FUEL SEGMENTAL GROWTH

- 12.4 HYBRID CURING

- 12.4.1 ENHANCED FLEXIBILITY AND OPTIMIZED OWNERSHIP COST TO AUGMENT SEGMENTAL GROWTH

13 UV CURING SYSTEM MARKET, BY SYSTEM TYPE

- 13.1 INTRODUCTION

- 13.2 SPOT CURING SYSTEM

- 13.2.1 GROWING DEMAND FOR PRECISE AND LOCALIZED CURING TO EXPEDITE SEGMENTAL GROWTH

- 13.3 FLOOD CURING SYSTEM

- 13.3.1 REQUIREMENT FOR UNIFORM, LARGE AREA, AND HIGH-SPEED CURING TO CONTRIBUTE TO SEGMENTAL GROWTH

- 13.4 PORTABLE/HANDHELD CURING SYSTEM

- 13.4.1 COMPACT AND LIGHTWEIGHT DESIGN TO ACCELERATE SEGMENTAL GROWTH

- 13.5 CONVEYOR/INLINE SYSTEM

- 13.5.1 ABILITY TO DELIVER CONSISTENT QUALITY WHILE MAINTAINING UNINTERRUPTED PRODUCTION TO SPUR DEMAND

14 UV CURING SYSTEM MARKET, BY PRESSURE TYPE

- 14.1 INTRODUCTION

- 14.2 HIGH

- 14.2.1 ABILITY TO RAPIDLY CURE THICK, PIGMENTED, AND HIGH-PERFORMANCE MATERIALS TO BOOST SEGMENTAL GROWTH

- 14.3 MEDIUM

- 14.3.1 OPERATIONAL STABILITY, FLEXIBILITY, COMPATIBILITY, AND COST EFFICIENCY TO ACCELERATE SEGMENTAL GROWTH

- 14.4 LOW

- 14.4.1 REQUIREMENT FOR CONTROLLED UV OUTPUT, MINIMAL HEAT GENERATION, AND ENERGY EFFICIENCY TO DRIVE MARKET

15 UV CURING SYSTEM MARKET, BY COMPONENT

- 15.1 INTRODUCTION

- 15.2 HARDWARE

- 15.2.1 SUPPORT FOR FLEXIBLE SYSTEM CONFIGURATIONS TO CONTRIBUTE TO SEGMENTAL GROWTH

- 15.2.2 UV LED MODULES

- 15.2.3 MERCURY LAMPS

- 15.2.4 UV OPTICS AND REFLECTORS

- 15.2.5 CONTROLLERS AND SENSORS

- 15.2.6 OTHER HARDWARE

- 15.3 SOFTWARE

- 15.3.1 INTELLIGENT PROCESS CONTROL, AUTOMATION, AND INTEGRATION CAPABILITIES TO FUEL SEGMENTAL GROWTH

- 15.3.2 UV CURING PROCESS CONTROL

- 15.3.3 IOT-ENABLED SYSTEM MONITORING

- 15.3.4 PRODUCTION LINE INTEGRATION (PLC CONNECTIVITY)

- 15.4 SERVICES

- 15.4.1 ABILITY TO MINIMIZE UNPLANNED DOWNTIME AND EXTEND EQUIPMENT LIFESPAN TO EXPEDITE SEGMENTAL GROWTH

16 UV CURING SYSTEM MARKET, BY APPLICATION

- 16.1 INTRODUCTION

- 16.2 COATINGS

- 16.2.1 RISING NEED FOR HIGH-PERFORMANCE SURFACE FINISHES IN INDUSTRIAL AND COMMERCIAL MANUFACTURING TO SPUR DEMAND

- 16.2.2 WOOD COATING

- 16.2.3 METAL COATING

- 16.2.4 PLASTIC COATING

- 16.3 INKS

- 16.3.1 GROWING EMPHASIS ON PRODUCTIVITY, PRINT DURABILITY, AND REGULATORY COMPLIANCE TO BOLSTER SEGMENTAL GROWTH

- 16.3.2 OFFSET

- 16.3.3 FLEXOGRAPHIC

- 16.3.4 DIGITAL PRINTING

- 16.4 ADHESIVES

- 16.4.1 MOUNTING DEMAND FOR RAPID BONDING, HIGH PRECISION, AND IMPROVED ASSEMBLY EFFICIENCY TO FOSTER SEGMENTAL GROWTH

- 16.5 3D PRINTINGS

- 16.5.1 INCREASING ADOPTION OF PHOTOPOLYMER-BASED ADDITIVE MANUFACTURING TO BOOST SEGMENTAL GROWTH

- 16.6 ELECTRONIC COMPONENTS

- 16.6.1 RISING COMPLEXITY AND MINIATURIZATION TO CONTRIBUTE TO SEGMENTAL GROWTH

- 16.7 OPTICAL FIBER COATINGS

- 16.7.1 MECHANICAL PROTECTION, FLEXIBILITY, AND LONG-TERM DURABILITY TO FUEL SEGMENTAL GROWTH

- 16.8 OTHER APPLICATIONS

17 UV CURING SYSTEM MARKET, BY VERTICAL

- 17.1 INTRODUCTION

- 17.2 INDUSTRIAL MANUFACTURING

- 17.2.1 FOCUS ON HIGH THROUGHPUT PRODUCTION, CONSISTENT PROCESS QUALITY, AND OPERATIONAL EFFICIENCY TO FOSTER SEGMENTAL GROWTH

- 17.3 AUTOMOTIVE

- 17.3.1 NEED FOR DURABLE SURFACE FINISHES AND EFFICIENT ASSEMBLY PROCESSES TO FACILITATE SEGMENTAL GROWTH

- 17.4 ELECTRONICS

- 17.4.1 INCREASING DEVICE MINIATURIZATION, HIGHER COMPONENT DENSITY TO BOLSTER SEGMENTAL GROWTH

- 17.5 PACKAGING

- 17.5.1 STRONG FOCUS ON HIGH-SPEED PRODUCTION, SUPERIOR PRINT QUALITY, AND SUSTAINABLE PACKAGING TO EXPEDITE SEGMENTAL GROWTH

- 17.6 PRINTING

- 17.6.1 RISING EMPHASIS ON CONSISTENT PRINT QUALITY AND FASTER TURNAROUND TIMES TO FUEL SEGMENTAL GROWTH

- 17.7 AEROSPACE & DEFENSE

- 17.7.1 IMPLEMENTATION OF STRINGENT QUALITY STANDARDS AND HIGH RELIABILITY REQUIREMENTS TO BOOST SEGMENTAL GROWTH

- 17.8 HEALTHCARE/MEDICAL DEVICES

- 17.8.1 INCREASING NEED FOR PRECISE MANUFACTURING OF TEMPERATURE SENSITIVE MATERIALS TO AUGMENT SEGMENTAL GROWTH

- 17.9 WOOD & FURNITURE

- 17.9.1 REQUIREMENT FOR QUALITY SURFACE FINISHES, RAPID PRODUCTION CYCLES TO DRIVE MARKET

- 17.10 OTHER VERTICALS

18 UV CURING SYSTEM MARKET, BY REGION

- 18.1 INTRODUCTION

- 18.2 NORTH AMERICA

- 18.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 18.2.2 US

- 18.2.2.1 Increasing investment in advanced manufacturing and sustainable technologies to bolster market growth

- 18.2.3 CANADA

- 18.2.3.1 Growing emphasis on sustainable manufacturing and industrial modernization to augment market growth

- 18.2.4 MEXICO

- 18.2.4.1 Rapid expansion of export-oriented manufacturing in industries to contribute to market growth

- 18.3 EUROPE

- 18.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 18.3.2 GERMANY

- 18.3.2.1 Strong industrial base and advanced manufacturing ecosystem to drive market

- 18.3.3 UK

- 18.3.3.1 Increasing upgrades of production lines with automated systems to boost market growth

- 18.3.4 FRANCE

- 18.3.4.1 Growing emphasis on energy efficiency and high-quality production across industrial sectors to fuel market growth

- 18.3.5 SPAIN

- 18.3.5.1 Rapid modernization of manufacturing base to accelerate market growth

- 18.3.6 ITALY

- 18.3.6.1 Strong focus on compliance with environmental regulations to foster market growth

- 18.3.7 NETHERLANDS

- 18.3.7.1 Growing emphasis on high-value manufacturing, packaging, printing, and industrial processing to drive market

- 18.3.8 BELGIUM

- 18.3.8.1 Strong industrial base and role as key logistics and processing hub to expedite market growth

- 18.3.9 NORDICS

- 18.3.9.1 Increasing deployment of low-emission technologies to accelerate market growth

- 18.3.10 REST OF EUROPE

- 18.4 ASIA PACIFIC

- 18.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 18.4.2 CHINA

- 18.4.2.1 Rise in manufacturing and industrial automation to boost market growth

- 18.4.3 AUSTRALIA

- 18.4.3.1 Implementation of stricter environmental compliance to bolster market growth

- 18.4.4 JAPAN

- 18.4.4.1 Technologically advanced manufacturing ecosystem to contribute to market growth

- 18.4.5 INDIA

- 18.4.5.1 High investment in manufacturing infrastructure to expedite market growth

- 18.4.6 SOUTH KOREA

- 18.4.6.1 Focus on improving throughput, energy efficiency, and process reliability in manufacturing to drive market

- 18.4.7 SOUTHEAST ASIA

- 18.4.7.1 Supportive government policies and industrial park development to fuel market growth

- 18.4.8 REST OF ASIA PACIFIC

- 18.5 ROW

- 18.5.1 MACROECONOMIC OUTLOOK FOR ROW

- 18.5.2 MIDDLE EAST

- 18.5.2.1 Bahrain

- 18.5.2.1.1 Emphasis on industrial diversification and manufacturing optimization to foster market growth

- 18.5.2.2 Kuwait

- 18.5.2.2.1 Rise in packaging, printing, construction materials, coatings, and consumer goods manufacturing to drive market

- 18.5.2.3 Oman

- 18.5.2.3.1 Expansion of industrial facilities and manufacturing modernization to augment market growth

- 18.5.2.4 Qatar

- 18.5.2.4.1 Expansion of packaging, printing, construction, coatings, and specialty manufacturing to boost market growth

- 18.5.2.5 Saudi Arabia

- 18.5.2.5.1 Large-scale industrial diversification initiatives to contribute to market growth

- 18.5.2.6 UAE

- 18.5.2.6.1 Government initiatives promoting advanced manufacturing to foster market growth

- 18.5.2.7 Rest of Middle East

- 18.5.2.1 Bahrain

- 18.5.3 AFRICA

- 18.5.3.1 South Africa

- 18.5.3.1.1 Industrial diversification and packaging sector growth to drive market

- 18.5.3.2 Rest of Africa

- 18.5.3.1 South Africa

- 18.5.4 SOUTH AMERICA

- 18.5.4.1 Brazil

- 18.5.4.1.1 Strong packaging, printing, and industrial manufacturing base to support market growth

- 18.5.4.2 Argentina

- 18.5.4.2.1 Gradual industrial recovery and printing demand to bolster market growth

- 18.5.4.3 Rest of South America

- 18.5.4.1 Brazil

19 COMPETITIVE LANDSCAPE

- 19.1 OVERVIEW

- 19.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 19.3 MARKET SHARE ANALYSIS, 2025

- 19.4 BRAND/PRODUCT COMPARISON

- 19.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 19.5.1 STARS

- 19.5.2 EMERGING LEADERS

- 19.5.3 PERVASIVE PLAYERS

- 19.5.4 PARTICIPANTS

- 19.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 19.5.5.1 Company footprint

- 19.5.5.2 Region footprint

- 19.5.5.3 System type footprint

- 19.5.5.4 Technology footprint

- 19.5.5.5 Pressure type footprint

- 19.5.5.6 Component footprint

- 19.5.5.7 Application footprint

- 19.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 19.6.1 PROGRESSIVE COMPANIES

- 19.6.2 RESPONSIVE COMPANIES

- 19.6.3 DYNAMIC COMPANIES

- 19.6.4 STARTING BLOCKS

- 19.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 19.6.5.1 Detailed list of key startups/SMEs

- 19.6.5.2 Competitive benchmarking of startups/SMEs

- 19.7 COMPETITIVE SCENARIO

- 19.7.1 PRODUCT LAUNCHES

- 19.7.2 DEALS

20 COMPANY PROFILES

- 20.1 INTRODUCTION

- 20.2 KEY PLAYERS

- 20.2.1 EXCELITAS TECHNOLOGIES CORP.

- 20.2.1.1 Business overview

- 20.2.1.2 Products/Solutions/Services offered

- 20.2.1.3 Recent developments

- 20.2.1.3.1 Product launches

- 20.2.1.3.2 Deals

- 20.2.1.4 MnM view

- 20.2.1.4.1 Key strengths/Right to win

- 20.2.1.4.2 Strategic choices

- 20.2.1.4.3 Weaknesses/Competitive threats

- 20.2.2 NORDSON CORPORATION

- 20.2.2.1 Business overview

- 20.2.2.2 Products/Solutions/Services offered

- 20.2.2.3 MnM view

- 20.2.2.3.1 Key strengths/Right to win

- 20.2.2.3.2 Strategic choices

- 20.2.2.3.3 Weaknesses/Competitive threats

- 20.2.3 DYMAX

- 20.2.3.1 Business overview

- 20.2.3.2 Products/Solutions/Services offered

- 20.2.3.3 Recent developments

- 20.2.3.3.1 Product launches

- 20.2.3.3.2 Deals

- 20.2.3.4 MnM view

- 20.2.3.4.1 Key strengths/Right to win

- 20.2.3.4.2 Strategic choices

- 20.2.3.4.3 Weaknesses/Competitive threats

- 20.2.4 IST METZ GMBH & CO. KG

- 20.2.4.1 Business overview

- 20.2.4.2 Products/Solutions/Services offered

- 20.2.4.3 Recent developments

- 20.2.4.3.1 Product launches

- 20.2.4.3.2 Deals

- 20.2.4.4 MnM view

- 20.2.4.4.1 Key strengths/Right to win

- 20.2.4.4.2 Strategic choices

- 20.2.4.4.3 Weaknesses/Competitive threats

- 20.2.5 BW CONVERTING

- 20.2.5.1 Business overview

- 20.2.5.2 Products/Solutions/Services offered

- 20.2.5.3 Recent developments

- 20.2.5.3.1 Deals

- 20.2.5.4 MnM view

- 20.2.5.4.1 Key strengths/Right to win

- 20.2.5.4.2 Strategic choices

- 20.2.5.4.3 Weaknesses/Competitive threats

- 20.2.6 AMERICAN ULTRAVIOLET

- 20.2.6.1 Business overview

- 20.2.6.2 Products/Solutions/Services offered

- 20.2.7 HANOVIA

- 20.2.7.1 Business overview

- 20.2.7.2 Products/Solutions/Services offered

- 20.2.8 HOENLE AG

- 20.2.8.1 Business overview

- 20.2.8.2 Products/Solutions/Services offered

- 20.2.9 GEW (EC) LIMITED

- 20.2.9.1 Business overview

- 20.2.9.2 Products/Solutions/Services offered

- 20.2.9.3 Recent developments

- 20.2.9.3.1 Product launches

- 20.2.10 FUJIFILM EUROPE GMBH

- 20.2.10.1 Business overview

- 20.2.10.2 Products/Solutions/Services offered

- 20.2.10.3 Recent developments

- 20.2.10.3.1 Product launches

- 20.2.1 EXCELITAS TECHNOLOGIES CORP.

- 20.3 OTHER PLAYERS

- 20.3.1 UVITRON INTERNATIONAL, INC.

- 20.3.2 MILTEC UV

- 20.3.3 JENTON GROUP

- 20.3.4 ATLANTIC ZEISER GMBH

- 20.3.5 UVEXS INC.

- 20.3.6 APL MACHINERY PVT. LTD.

- 20.3.7 KYOCERA CORPORATION

- 20.3.8 SENLIAN AUTOMATIC COATING MACHINERY CO., LTD.

- 20.3.9 DOCTORUV

- 20.3.10 USHIO INC.

- 20.3.11 PROPHOTONIX LIMITED

- 20.3.12 BENFORD

- 20.3.13 ALPHA-CURE

- 20.3.14 SEOUL VIOSYS CO., LTD.

- 20.3.15 THORLABS, INC.

- 20.3.16 AETEK, INC.

21 RESEARCH METHODOLOGY

- 21.1 RESEARCH DATA

- 21.1.1 SECONDARY DATA

- 21.1.1.1 List of key secondary sources

- 21.1.1.2 Key data from secondary sources

- 21.1.2 PRIMARY DATA

- 21.1.2.1 List of primary interview participants

- 21.1.2.2 Breakdown of primary interviews

- 21.1.2.3 Key data from primary sources

- 21.1.2.4 Key industry insights

- 21.1.3 SECONDARY AND PRIMARY RESEARCH

- 21.1.1 SECONDARY DATA

- 21.2 MARKET SIZE ESTIMATION

- 21.2.1 BOTTOM-UP APPROACH

- 21.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 21.2.2 TOP-DOWN APPROACH

- 21.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 21.2.1 BOTTOM-UP APPROACH

- 21.3 MARKET FORECAST APPROACH

- 21.3.1 DEMAND SIDE

- 21.3.2 SUPPLY SIDE

- 21.4 DATA TRIANGULATION

- 21.5 RESEARCH ASSUMPTIONS

- 21.6 RESEARCH LIMITATIONS

- 21.7 RISK ANALYSIS

22 APPENDIX

- 22.1 INSIGHTS FROM INDUSTRY EXPERTS

- 22.2 DISCUSSION GUIDE

- 22.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 22.4 CUSTOMIZATION OPTIONS

- 22.5 RELATED REPORTS

- 22.6 AUTHOR DETAILS