|

시장보고서

상품코드

1931745

미세유체 시장 : 제품별, 용도별, 최종사용자별, 지역별 - 세계 예측(-2030년)Microfluidics Market by Product (Chip, Sensor, Valve, Pump, Needle), Material (Silicon, Polymer), Application, End User - Global forecast to 2030 |

||||||

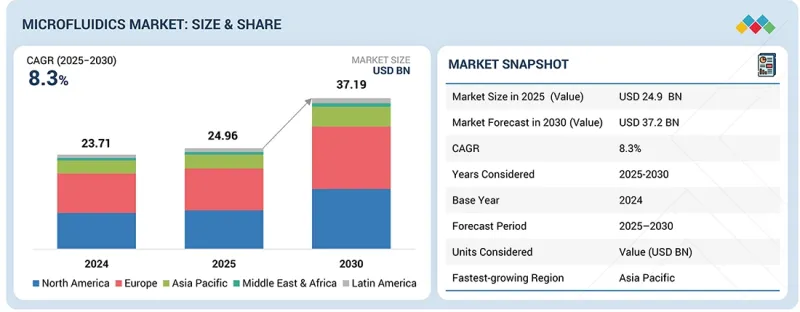

미세유체 시장 규모는 2025년 249억 6,000만 달러에서 2030년까지 372억 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR 8.3%로 성장할 전망입니다. 미세유체 시장은 몇 가지 중요한 요인으로 인해 확대되고 있습니다. 그 중요한 요인 중 하나가 바로 현장진단(POC 진단)에 대한 수요 증가입니다. 암, 당뇨 등 만성질환이 증가함에 따라 신속하고 정확한 진단의 필요성이 높아지고 있으며, 이는 의료 분야에서의 미세유체기술의 적용을 촉진하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

또한, 약물전달, 장기 칩 기술, 맞춤형 의료의 혁신으로 인해 미세유체 장치의 활용이 증가하고 있습니다. 또한, 단백질체학 및 유전체학 관련 연구의 증가가 시장을 주도하고 있습니다.

미세유체 시장은 폴리머의 저비용성, 제조 용이성, 적응성에 의해 주도되고 있습니다. 미세유체 장치의 제조에는 폴리디메틸실록산(PDMS), 폴리메틸메타크릴레이트(PMMA), 고리형 올레핀 공중합체(COC) 등의 폴리머가 자주 필요합니다. 이러한 폴리머는 미세유체 채널 및 구조물 제작에 유용합니다. 또한, 실리콘이나 유리와 같은 기존 소재에 비해 폴리머는 성형이 용이하여 제조비용을 절감할 수 있습니다. 폴리머의 생체적합성은 약물전달, 랩온칩, 진단 등 다양한 의료 용도에 유용합니다. 이러한 장점으로 인해 폴리머는 미세유체 시장에서 가장 큰 점유율을 차지하고 있습니다.

미세유체 산업에서 병원 및 진단 센터의 성장을 촉진하는 여러 가지 중요한 요인이 있습니다. 그 중 하나는 신속한 현장 검사를 통해 환자의 치료 결과를 향상시키는 'Point of Care 진단'에 대한 수요 증가입니다. 미세유체 기술은 보다 빠르고 정확한 결과를 제공하기 때문에 이러한 좋은 결과에 크게 기여하고 있습니다. 또한, COVID-19와 같은 감염병의 증가로 인해 임상 현장에서 효과적인 진단의 필요성이 높아지고 있습니다. 이 장비들은 비용 절감, 검사 방법의 신속성, 진단의 정확성 및 정확성 향상을 실현합니다.

2024년부터 2029년까지 예측 기간 동안 아시아태평양(APAC)에서 가장 높은 CAGR을 기록했습니다. 아시아태평양에는 인도, 중국, 일본, 호주, 한국 및 기타 아시아태평양(RoAPAC)이 포함됩니다. 특히 중국, 인도, 일본에서는 신기술에 대한 수요가 증가하고 있습니다. 일본 정부는 학술기관의 연구개발 활동 촉진에 힘을 쏟고 있으며, 2021년부터 2025년까지 제6차 과학기술기본계획에 642억 6,000만 달러를 배정했습니다. 만성질환 및 감염성 질환의 발생률 증가와 더불어 조기 진단 및 예방의학에 대한 관심이 높아지면서 미세유체 디바이스의 활용이 비약적으로 확대되고 있습니다. 이 지역에서 급성장하고 있는 제약 및 생명과학 분야도 연구개발을 추진하고 있으며, 미세유체 기술에 대한 수요 증가로 이어지고 있습니다.

이 시장의 주요 기업으로는 Abbott laboratories(미국), Agilent Technologies, Inc. Inc(미국),Danaher Corporation(미국),Illumina Inc(미국),Parker Hannifin Corporation(미국),Thermo Fisher Scientific Inc. Idex Corporation(미국),Fortive Corporation(미국),Perkinelmer, Inc.(미국),F.Hoffmann-LA Roche Ltd(스위스),Standard Biotools Inc. Corporation(미국), Hologic Inc.(미국), Dolomite Microfluidics(영국), Elveflow(프랑스) 등이 있습니다.

조사 범위

이 보고서는 최종사용자, 제품, 용도, 지역별로 세분화되어 있습니다. 또한, 미세유체 시장의 성장 궤도에 영향을 미치는 주요 촉진요인, 저해요인, 기회, 도전과제에 대해서도 다루고 있습니다. 주요 플레이어와 경쟁 상황을 중심으로 시장의 잠재력과 과제에 대한 상세한 분석을 이해관계자에게 제공합니다. 또한, 마이크로 시장은 세계 미세유체 부문에 미치는 전반적인 영향, 성장 패턴 및 잠재력을 기반으로 분석됩니다. 본 분석에서는 5개 주요 지역에 초점을 맞추어 시장 세분화 수익 증가를 예측하고 있습니다.

본 보고서 구매의 주요 이점:

본 조사의 목적은 미세유체 시장에 신규 진입하는 기업과 기존 기업 모두 상세하고 전문적인 정보를 통해 투자의 지속가능성을 평가할 수 있도록 돕는 것입니다. 중요한 의사결정을 지원하는 데이터세트를 제공합니다. 본 보고서가 철저한 리스크 평가를 촉진하고 투자 판단의 방향성을 제시할 수 있다는 점은 본 보고서의 주요 장점 중 하나입니다. 이 조사는 최종사용자 및 지리적 영역에 따른 시장 세분화를 통해 정확한 분석과 인사이트를 제공합니다. 또한, 주요 트렌드, 장벽, 기회, 촉진요인을 제시하여 이해관계자들이 장기적인 성장에 도움이 되는 전략적 의사결정을 내리는 데 필요한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다:

미세유체 시장 성장에 영향을 미치는 주요 촉진요인, 제약요인, 기회요인, 과제 분석 - - 혁신적 기술과 만성질환 유병률 증가, 장비 비용 상승 및 엄격한 규제, 진단센터 증가

제품 개발/혁신 : 미세유체 산업의 기술 개요, 연구개발 프로젝트, 혁신적인 제품 및 서비스 도입 현황.

시장 개발 - 수익성 높은 시장에 대한 자세한 정보 - 이 조사는 다양한 지역의 미세유체 사업 동향을 분석합니다.

시장 다각화 : 미세유체 시장의 혁신적인 제품, 미개척 지역, 최근 동향 및 지출에 대한 깊은 이해.

경쟁사 평가 : 시장 점유율, 제공 서비스 및 제품, 그리고 Danaher Corporation(미국), Illumina Inc.(미국), biomerieux(프랑스), Thermo Fisher Scientific Inc.(미국), Abbott laboratories(미국) 등 주요 기업들의 주요 전략에 대한 상세한 분석.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

- 시장 역학

- 성장 촉진요인

- 미세유체 기술의 도입을 촉진하는 e-Health와 디지털 진단

- 성장 억제요인

- 기회

- 과제

- 미충족 수요

- 상호 접속된 시장과 분야 횡단적인 기회

- 티어1/2/3플레이어 전략적 활동

제5장 기술, 특허, AI 도입에 의한 전략적 파괴

- 주요 기술

- 보완적 기술

- 특허 분석

- 향후 응용

- AI/생성형 AI가 미세유체 시장에 미치는 영향

- 성공 사례와 실세계에 대한 응용

- 규제 상황

제6장 고객 상황과 구매 행동

- 구매자 이해관계자와 구입 평가 기준

- 의사결정 프로세스

- 채용 장벽과 내부 과제

- 최종사용자 미충족 수요

제7장 업계 동향

- Porter's Five Forces 분석

- 거시경제 지표

- 밸류체인 분석

- 생태계 분석

- 가격 분석

- 무역 데이터 분석

- 2026-2027년의 주요 회의와 이벤트

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 투자와 자금 조달 시나리오

- 사례 연구 분석

- 2025년 미국 관세가 미세유체 시장에 미치는 영향

제8장 미세유체 시장(제품별)

- 미세유체 기반 디바이스

- 기타 디바이스

- 미세유체 컴포넌트

제9장 미세유체 시장(용도별)

- 체외진단(IVD)

- 치료제

- 의약품 및 생명과학 조사

제10장 미세유체 시장(최종사용자별)

- 병원과 진단 센터

- 제약·바이오테크놀러지 기업

- 학술연구기관

제11장 미세유체 시장(지역별)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타

- 라틴아메리카

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- GCC 국가

- 기타

제12장 경쟁 구도

- 주요 진출 기업의 전략/강점

- 미세유체 시장의 주요 기업이 채용하고 있는 전략 개요

- 매출 분석, 2022-2024년

- 시장 점유율 분석, 2024년

- 주요 시장 진입 기업 순위

- 기업 평가 매트릭스 : 주요 진출 기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 기업 평가와 재무 지표

- 브랜드/제품 비교 분석

- 경쟁 시나리오

제13장 기업 개요

- 주요 진출 기업

- DANAHER CORPORATION

- ILLUMINA, INC.

- BIOMERIEUX

- THERMO FISHER SCIENTIFIC INC.

- ABBOTT LABORATORIES

- PARKER HANNIFIN CORP

- SMC CORPORATION

- IDEX CORPORATION

- FORTIVE

- REVVITY, INC.

- AGILENT TECHNOLOGIES, INC.

- BIO-RAD LABORATORIES, INC.

- BECTON, DICKINSON AND COMPANY

- F. HOFFMANN-LA ROCHE LTD.

- STANDARD BIOTOOLS

- QUIDELORTHO CORPORATION

- AIGNEP S.P.A.

- DOLOMITE MICROFLUIDICS

- ELVEFLOW

- 기타 기업

- NANOSTRING TECHNOLOGIES

- INNOVATIVE BIOCHIPS, LLC

- FLUIDIC ANALYTICS

- HORIBA

- MICRONIT B.V.

- EMULATE, INC.

- SPHERE BIO

- ZEON CORPORATION

- QIAGEN N.V.

제14장 조사 방법

제15장 부록

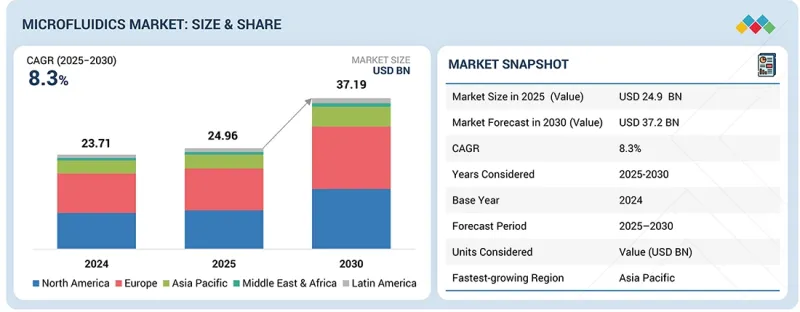

KSM 26.02.25The Microfluidics market is projected to reach USD 37.2 Billion by 2030 from USD 24.96 billion in 2025, growing at a CAGR of 8.3% during the forecast period. The microfluidics market is expanding due to a number of important factors. The growing requirement for point-of-care diagnostics is one of the important factors. The necessity for fast and accurate diagnosis has risen due to the increase in chronic diseases like cancer and diabetes, which is propelling the application of microfluidics in healthcare.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Furthermore, the use of microfluidic devices is increasing due to innovations in drug delivery, organ-on-a-chip technology, and personalized medicine. Additionally, the market is driven by the rise in proteomics and genomics-associated research.

"Polymers to account for the largest market share in 2024."

The microfluidics market is propelled by polymers because of their low costs, ease of production and adaptability. Microfluidic device manufacturing often requires polymers such as polydimethylsiloxane (PDMS), polymethyl methacrylate (PMMA), and cyclic olefin copolymer (COC). These polymers are helpful in the fabrication of microfluidic channels and structures. Moreover, as compared to conventional materials like silicon or glass, polymers are easier to mold and also enable cheaper manufacturing costs. The biocompatible property of polymers makes them useful for a variety of medical applications, including medication delivery, lab-on-a-chip, and diagnostics. Due to such advantages, polymers account for the largest share in the microfluidics market.

"Hospital and Diagnostic Centers to register the highest growth rate in the market during the forecast period."

Various significant factors are propelling the growth of hospitals and diagnostic centers in the microfluidics industry. One important factor is the rising requirement for point-of-care diagnostics, as they provides quick, on-site testing that improves patient outcomes. Microfluidics play a major role in this positive outcome as it offers faster and precise result . Moreover, the requirement for efficacious diagnostics in clinical settings has risen due to the increase in infectious diseases like COVID-19. These equipment decreases cost, expedites testing methods, and improve precision and accuracy of diagnosis.

"Asia Pacific to register highest growth rate in the market during the forecast period."

The highest CAGR was recorded in the APAC region during the forecast period of 2024- 2029. Asia Pacific includes India, China, Japan, Australia, South Korea, and RoAPAC. Demand for novel technologies is also on the rise, particularly in China, India, and Japan. The government is striving hard to develop research activities in academic setups. In this regard, the Japanese government has distributed USD 64.26 billion toward its 6th Science and Technology Basic Plan for 2021-2025. The rising incidence of chronic and infectious diseases, coupled with increased interest in early diagnosis and preventive care, has enhanced the utilization of microfluidic devices by tremendous bounds. The pharmaceutical and life sciences sectors, which are fast growing in the region, are also driving the research and development efforts, hence increasing the demand for microfluidics.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1-30%, Tier 2-42%, and Tier 3- 28%

- By Designation: C-level-- 10%, Director-level-14%, and Others-76%

- By Region: North America-40%, Europe-30%, Asia Pacific-22%, Rest of the World -8%.

Prominent players in this market are Abbott laboratories (US) , Agilent Technologies, Inc. (US), Aignep S.P.A (Italy), biomerieux (France), BD(US), Bio-Rad laboratories, Inc (US), Danaher Corporation (US), Illumina Inc. (US), Parker Hannifin Corporation (US), Thermo Fisher Scientific Inc. (US), SMC Corporation (Japan), Idex Corporation (US), Fortive Corporation (US), Perkinelmer, Inc. (US), F.Hoffmann-LA Roche Ltd (Switzerland), Standard Biotools Inc. (US), Quidelortho Corporation (US), Hologic Inc. (US), Dolomite Microfluidics (UK) and Elveflow (France).

Research Coverage

The report comprise segmentation that covers end users, products, applications, and geographic regions. It also covers the key drivers, restraints, opportunities, and challenges impacting the growth trajectory of the microfluidics market. The research offers stakeholders an in-depth analysis of market potential and challenges, with a focus on major players and competitive landscapes. Moreover, micromarkets are analysed as per their overall impact to the global microfluidics sector, growth patterns, and potential. The analysis forecasts rise in market segment revenues, focusing on five key regions.

Key Benefits of Buying the Report:

The purpose of this research is to assist both new and existing players in the microfluidics market to assess the sustainability of their investments by providing detailed and knowledgeable information. It offers a dataset to assist in making key decisions. This report's potential to facilitate thorough risk evaluation and provide direction for investment decisions is one of its major benefit. Market segmentation according to end-users and geographical areas is provided in the study, that provides precise analysis and insights. It also provide significant trends, obstacles, opportunities, and drivers, giving stakeholders the information they require to make strategic decisions that help in their long-term growth.

The report provides the insights on the following pointers:

Analysis of the key drivers, restraints, opportunities, and challenges affecting the microfluidics market growth: Innovative technology and increase in prevalence of chronic diseases ; increased cost of devices and stringent regulations ; increase in number of diagnostic centers.

Product Development/Innovation: Overview of technologies, research & development ventures and launch of innovative product & service for the microfluidics industry.

Market Development: Details associated with profitable markets: this research studies the microfluidics business in various geographical regions.

Market Diversification: In-depth understanding of innovative products, unexamined regions, recent developments, and expenditures in the microfluidics market.

Competitive Assessment: Detailed analysis of market share, services and products offered and key strategies adopted by prominent players such as Danaher Corporation (US), Illumina Inc. (US), biomerieux (France), Thermo Fisher Scientific Inc. (US) and Abbott laboratories (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKET COVERED

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MICROFLUIDICS MARKET

- 2.4 HIGH GROWTH SEGMENTS

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MICROFLUIDICS MARKET

- 3.2 MICROFLUIDICS MARKET, BY REGION

- 3.3 MICROFLUIDICS MARKET, BY COUNTRY AND END USER

- 3.4 GEOGRAPHIC SNAPSHOT OF MICROFLUIDICS MARKET

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Integration of microfluidics with 3D printing

- 4.2.2 E-HEALTH AND DIGITAL DIAGNOSTICS DRIVING MICROFLUIDICS ADOPTION

- 4.2.2.1 Increasing prevalence of chronic diseases fueling POC testing

- 4.2.2.2 Increasing focus on data precision and accuracy

- 4.2.3 RESTRAINTS

- 4.2.3.1 Regulatory and clinical validation barriers

- 4.2.3.2 Material selection for microfluidic devices

- 4.2.4 OPPORTUNITIES

- 4.2.4.1 Advancing microfluidics for real-time food safety monitoring

- 4.2.4.2 Rising demand for organ-on-a-chip platforms in precision medicine

- 4.2.5 CHALLENGES

- 4.2.5.1 Limited adoption of microfluidic devices

- 4.2.5.2 Technical and operational limitations

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, AND AI ADOPTION

- 5.1 KEY TECHNOLOGIES

- 5.1.1 MICROFABRICATION

- 5.1.2 MATERIAL SCIENCE

- 5.1.3 OPTOFLUIDICS

- 5.2 COMPLEMENTARY TECHNOLOGIES

- 5.2.1 MICRO-ELECTRO-MECHANICAL SYSTEMS (MEMS)

- 5.2.2 WEARABLE & IMPLANTABLE MICROFLUIDICS

- 5.3 PATENT ANALYSIS

- 5.3.1 INNOVATIONS AND PATENT REGISTRATIONS

- 5.4 FUTURE APPLICATIONS

- 5.5 IMPACT OF AI/GENAI ON MICROFLUIDICS MARKET

- 5.5.1 TOP USE CASES AND MARKET POTENTIAL

- 5.5.2 BEST PRACTICES IN MICROFLUIDICS

- 5.5.3 CASE STUDIES OF AI IMPLEMENTATION IN MICROFLUIDICS MARKET

- 5.5.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 5.5.5 CLIENT'S READINESS TO ADOPT GENERATIVE AI IN MICROFLUIDICS MARKET

- 5.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 5.7 REGULATORY LANDSCAPE

- 5.7.1 NORTH AMERICA

- 5.7.1.1 US

- 5.7.1.2 Canada

- 5.7.2 EUROPE

- 5.7.3 ASIA PACIFIC

- 5.7.3.1 Japan

- 5.7.3.2 China

- 5.7.3.3 India

- 5.7.4 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.7.1 NORTH AMERICA

6 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 6.1 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 6.1.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.1.2 BUYING CRITERIA

- 6.2 DECISION-MAKING PROCESS

- 6.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 6.4 UNMET NEEDS FROM END USERS

7 INDUSTRY TRENDS

- 7.1 PORTER'S FIVE FORCES ANALYSIS

- 7.1.1 THREAT OF NEW ENTRANTS

- 7.1.2 THREAT OF SUBSTITUTES

- 7.1.3 BARGAINING POWER OF SUPPLIERS

- 7.1.4 BARGAINING POWER OF BUYERS

- 7.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 7.2 MACROECONOMIC INDICATORS

- 7.2.1 INTRODUCTION

- 7.2.2 HEALTHCARE EXPENDITURE AND INFRASTRUCTURE OUTLOOK

- 7.2.3 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 7.2.4 MACROECONOMIC OUTLOOK FOR EUROPE

- 7.2.5 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 7.2.6 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 7.2.7 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 7.2.8 TRENDS IN GLOBAL MICROFLUIDICS INDUSTRY

- 7.3 VALUE CHAIN ANALYSIS

- 7.3.1 RESEARCH & DEVELOPMENT

- 7.3.2 RAW MATERIAL PROCUREMENT & MANUFACTURING

- 7.3.3 MARKETING & SALES, DISTRIBUTION, AND POST-SALES SERVICES

- 7.4 ECOSYSTEM ANALYSIS

- 7.5 PRICING ANALYSIS

- 7.5.1 AVERAGE SELLING PRICE TREND, BY REGION

- 7.5.2 AVERAGE SELLING PRICE OF MICROFLUIDIC COMPONENTS, BY KEY PLAYERS

- 7.6 TRADE DATA ANALYSIS

- 7.6.1 IMPORT DATA (HS CODE 3822)

- 7.6.2 EXPORT DATA (HS CODE 3822)

- 7.7 KEY CONFERENCES & EVENTS, 2026-2027

- 7.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 7.9 INVESTMENT & FUNDING SCENARIO

- 7.10 CASE STUDY ANALYSIS

- 7.10.1 CASE STUDY 1: MULTIPLEX MICROFLUIDIC CIRCUIT FOR BLOOD VESSEL-ON-A-CHIP PERFUSION USING FLOWEZ

- 7.10.2 CASE STUDY 2: MICROFLUIDIC SYSTEM FOR ROBOTIC HAND PLAYING NINTENDO

- 7.10.3 CASE STUDY 3: 3D-PRINTED MICROFLUIDIC DEVICES USING POLYJET TECHNOLOGY

- 7.11 IMPACT OF 2025 US TARIFFS ON MICROFLUIDICS MARKET

- 7.11.1 INTRODUCTION

- 7.11.2 KEY TARIFF RATES

- 7.11.3 PRICE IMPACT ANALYSIS

- 7.11.4 IMPACT ON COUNTRY/REGION

- 7.11.5 IMPACT ON END-USE INDUSTRIES

8 MICROFLUIDICS MARKET, BY PRODUCT

- 8.1 INTRODUCTION

- 8.2 MICROFLUIDICS-BASED DEVICES

- 8.2.1 HIGH UPTAKE OF POC TESTING AND ORGAN-ON-A-CHIP SYSTEMS TO DRIVE MARKET

- 8.2.2 POLYMERASE CHAIN REACTION (PCR) SYSTEMS

- 8.2.3 MICROFLUIDIC CAPILLARY ELECTROPHORESIS

- 8.2.4 NEXT-GENERATION SEQUENCING (NGS) SYSTEMS

- 8.2.5 DROPLET & PARTICLE PRODUCTION SYSTEMS

- 8.3 OTHER DEVICES

- 8.4 MICROFLUIDIC COMPONENTS

- 8.4.1 CRUCIAL FOR CONTINUOUS HEALTH MONITORING

- 8.4.2 MICROFLUIDIC COMPONENTS, BY TYPE

- 8.4.2.1 Microfluidic chips

- 8.4.2.2 Flow & pressure sensors

- 8.4.2.3 Flow & pressure controllers

- 8.4.2.4 Microfluidic valves

- 8.4.2.5 Micropumps

- 8.4.2.6 Microneedles

- 8.4.2.7 Other microfluidic components

- 8.4.3 MICROFLUIDIC COMPONENTS, BY MATERIAL

- 8.4.3.1 Silicon

- 8.4.3.2 Polymethyl methacrylate (PMMA)

- 8.4.3.3 Polydimethylsiloxane (PDMS)

- 8.4.3.4 Cyclic olefin copolymer (COC)

- 8.4.3.5 Glass

- 8.4.3.6 OTHER MATERIALS

9 MICROFLUIDICS MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 IN VITRO DIAGNOSTICS (IVD)

- 9.2.1 CLINICAL DIAGNOSTICS

- 9.2.1.1 Growing focus on early disease detection to drive market

- 9.2.2 POINT-OF-CARE TESTING (POCT)

- 9.2.2.1 Increasing demand for decentralized infectious disease testing to drive market

- 9.2.3 VETERINARY DIAGNOSTICS

- 9.2.3.1 Rising demand for rapid, field-deployable veterinary diagnostics to drive market

- 9.2.1 CLINICAL DIAGNOSTICS

- 9.3 THERAPEUTICS

- 9.3.1 DRUG DELIVERY

- 9.3.1.1 Ability to enable scalable production of polymer-based drug particles to drive market

- 9.3.2 WEARABLE

- 9.3.2.1 Ability to enable proactive management of hydration, metabolic status, and disease biomarkers to drive market

- 9.3.1 DRUG DELIVERY

- 9.4 PHARMACEUTICAL & LIFE SCIENCE RESEARCH

- 9.4.1 LAB ANALYTICS

- 9.4.1.1 Proteomic analysis

- 9.4.1.1.1 Utilization of proteomes-on-a-chip devices for therapeutic development to drive market

- 9.4.1.2 Genomic analysis

- 9.4.1.2.1 High-throughput, cost-effective genomic analysis enabled by microfluidics

- 9.4.1.3 Cell-based assays

- 9.4.1.3.1 Microfluidic co-cultures enable precise, high-throughput modeling of complex tissues for drug testing and disease research

- 9.4.1.4 Capillary electrophoresis

- 9.4.1.4.1 Enables high-throughput, precise, and cost-efficient protein and nucleic acid analysis

- 9.4.1.1 Proteomic analysis

- 9.4.2 MICRODISPENSING

- 9.4.2.1 Suitability for low-viscosity applications to support market growth

- 9.4.3 MICROREACTORS

- 9.4.3.1 Growing adoption of continuous flow synthesis in research & development to drive market

- 9.4.1 LAB ANALYTICS

10 MICROFLUIDICS MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 HOSPITALS & DIAGNOSTIC CENTERS

- 10.2.1 RISING DEPENDENCE ON RAPID MICROFLUIDIC MOLECULAR DIAGNOSTICS TO DRIVE GROWTH

- 10.3 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 10.3.1 STRONG ADOPTION OF MICROFLUIDIC TECHNOLOGIES FOR PRECISE FORMULATION, NANOPARTICLE PRODUCTION, AND TOXICITY TESTING TO DRIVE GROWTH

- 10.4 ACADEMIC & RESEARCH INSTITUTES

- 10.4.1 INVESTMENTS IN BIOMEDICAL & LIFE SCIENCE RESEARCH TO DRIVE GROWTH

11 MICROFLUIDICS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Expansion of applications beyond traditional diagnostics to drive market

- 11.2.2 CANADA

- 11.2.2.1 Government funding and collaborative ecosystems to support growth

- 11.2.1 US

- 11.3 EUROPE

- 11.3.1 GERMANY

- 11.3.1.1 Ongoing investments in semiconductors and microelectronics to drive market

- 11.3.2 FRANCE

- 11.3.2.1 Rising demand for advanced lab-on-chip and organ-on-chip solutions to drive market

- 11.3.3 UK

- 11.3.3.1 Rising cases of chronic diseases and increasing demand for POC testing to boost demand

- 11.3.4 ITALY

- 11.3.4.1 Shift toward cost-efficient microfluidic platforms for diagnostics, environmental testing, and advanced biomedical research to drive market

- 11.3.5 SPAIN

- 11.3.5.1 Increasing demand for accessible point-of-care and lab-on-chip solutions to drive market

- 11.3.6 REST OF EUROPE

- 11.3.1 GERMANY

- 11.4 ASIA PACIFIC

- 11.4.1 CHINA

- 11.4.1.1 Government support and strategic partnerships to drive market

- 11.4.2 JAPAN

- 11.4.2.1 Government support, innovation, and industry-academia collaboration to drive growth

- 11.4.3 INDIA

- 11.4.3.1 Growing biotech startup ecosystem and research from premier institutions to drive market

- 11.4.4 AUSTRALIA

- 11.4.4.1 Innovation ecosystem, R&D strength, and precision engineering to support growth

- 11.4.5 SOUTH KOREA

- 11.4.5.1 Advanced research, global partnerships, and next-gen technologies to drive market

- 11.4.6 REST OF ASIA PACIFIC

- 11.4.1 CHINA

- 11.5 LATIN AMERICA

- 11.5.1 BRAZIL

- 11.5.1.1 Rising investment in healthtech and emphasis on molecular diagnostics to drive market

- 11.5.2 MEXICO

- 11.5.2.1 Growing demand for advanced diagnostics and biotech innovation to drive market

- 11.5.3 REST OF LATIN AMERICA

- 11.5.1 BRAZIL

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 GCC COUNTRIES

- 11.6.1.1 Disease burden and healthcare modernization to drive market

- 11.6.2 REST OF MIDDLE EAST & AFRICA

- 11.6.1 GCC COUNTRIES

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.3 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN MICROFLUIDICS MARKET

- 12.4 REVENUE ANALYSIS, 2022-2024

- 12.5 MARKET SHARE ANALYSIS, 2024

- 12.6 RANKING OF KEY MARKET PLAYERS

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.5.1 Company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 Product footprint

- 12.7.5.4 Application footprint

- 12.7.5.5 End user footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.8.5.1 List of key startup/SME players

- 12.8.5.2 Competitive benchmarking of key startups/SMEs

- 12.9 COMPANY VALUATION & FINANCIAL METRICS

- 12.9.1 FINANCIAL METRICS

- 12.9.2 COMPANY VALUATION

- 12.10 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 12.11 COMPETITIVE SCENARIO

- 12.11.1 PRODUCT LAUNCHES & APPROVALS

- 12.11.2 DEALS

- 12.11.3 EXPANSIONS

- 12.11.4 OTHER DEVELOPMENTS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 DANAHER CORPORATION

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Deals

- 13.1.1.3.2 Expansions

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses & competitive threats

- 13.1.2 ILLUMINA, INC.

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.3.2 Deals

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses & competitive threats

- 13.1.3 BIOMERIEUX

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches/approvals

- 13.1.3.3.2 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses & competitive threats

- 13.1.4 THERMO FISHER SCIENTIFIC INC.

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches/approvals

- 13.1.4.3.2 Deals

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses & competitive threats

- 13.1.5 ABBOTT LABORATORIES

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 MnM view

- 13.1.5.3.1 Key strengths

- 13.1.5.3.2 Strategic choices

- 13.1.5.3.3 Weaknesses & competitive threats

- 13.1.6 PARKER HANNIFIN CORP

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.7 SMC CORPORATION

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches

- 13.1.8 IDEX CORPORATION

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Deals

- 13.1.9 FORTIVE

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.10 REVVITY, INC.

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Deals

- 13.1.11 AGILENT TECHNOLOGIES, INC.

- 13.1.11.1 Business overview

- 13.1.11.2 Products offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Product approvals/launches

- 13.1.11.3.2 Deals

- 13.1.11.3.3 Expansions

- 13.1.12 BIO-RAD LABORATORIES, INC.

- 13.1.12.1 Business overview

- 13.1.12.2 Products offered

- 13.1.12.3 Recent developments

- 13.1.12.3.1 Product launches

- 13.1.12.3.2 Deals

- 13.1.13 BECTON, DICKINSON AND COMPANY

- 13.1.13.1 Business overview

- 13.1.13.2 Products offered

- 13.1.13.3 Recent developments

- 13.1.13.3.1 Product launches/approvals

- 13.1.13.3.2 Deals

- 13.1.13.3.3 Expansions

- 13.1.14 F. HOFFMANN-LA ROCHE LTD.

- 13.1.14.1 Business overview

- 13.1.14.2 Products offered

- 13.1.14.3 Recent developments

- 13.1.14.3.1 Product launches/approvals

- 13.1.14.3.2 Deals

- 13.1.15 STANDARD BIOTOOLS

- 13.1.15.1 Business overview

- 13.1.15.2 Products offered

- 13.1.15.3 Recent developments

- 13.1.15.3.1 Product launches/approvals

- 13.1.15.3.2 Deals

- 13.1.16 QUIDELORTHO CORPORATION

- 13.1.16.1 Business overview

- 13.1.16.2 Products offered

- 13.1.16.3 Recent developments

- 13.1.16.3.1 Product approvals

- 13.1.16.3.2 Deals

- 13.1.16.3.3 Expansions

- 13.1.17 AIGNEP S.P.A.

- 13.1.17.1 Business overview

- 13.1.17.2 Products offered

- 13.1.17.3 Recent developments

- 13.1.17.3.1 Deals

- 13.1.18 DOLOMITE MICROFLUIDICS

- 13.1.18.1 Business overview

- 13.1.18.2 Products offered

- 13.1.18.3 Recent developments

- 13.1.18.3.1 Product launches

- 13.1.18.3.2 Deals

- 13.1.18.3.3 Other developments

- 13.1.19 ELVEFLOW

- 13.1.19.1 Business overview

- 13.1.19.2 Products offered

- 13.1.1 DANAHER CORPORATION

- 13.2 OTHER PLAYERS

- 13.2.1 NANOSTRING TECHNOLOGIES

- 13.2.2 INNOVATIVE BIOCHIPS, LLC

- 13.2.3 FLUIDIC ANALYTICS

- 13.2.4 HORIBA

- 13.2.5 MICRONIT B.V.

- 13.2.6 EMULATE, INC.

- 13.2.7 SPHERE BIO

- 13.2.8 ZEON CORPORATION

- 13.2.9 QIAGEN N.V.

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.2 RESEARCH DESIGN

- 14.2.1 SECONDARY RESEARCH

- 14.2.1.1 Objectives of secondary research

- 14.2.1.2 Key data from secondary sources

- 14.2.2 PRIMARY RESEARCH

- 14.2.2.1 Objectives of primary research

- 14.2.2.2 Key industry insights

- 14.2.1 SECONDARY RESEARCH

- 14.3 MARKET SIZE ESTIMATION METHODOLOGY

- 14.3.1 BOTTOM-UP APPROACH

- 14.3.1.1 Approach 1: Company revenue estimation approach

- 14.3.1.2 Approach 2: Customer-based market estimation

- 14.3.1.3 Approach 3: Primary interviews

- 14.3.2 TOP-DOWN APPROACH

- 14.3.1 BOTTOM-UP APPROACH

- 14.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 14.5 MARKET SHARE ASSESSMENT

- 14.6 RESEARCH ASSUMPTIONS

- 14.7 RESEARCH LIMITATIONS

- 14.8 RISK ASSESSMENT

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS