|

시장보고서

상품코드

1936009

원심 펌프 시장 : 유형별, 단수별, 운전 방식별, 최종사용자별, 지역별 - 세계 예측(-2030년)Centrifugal Pump Market by Type, Operation Type, Stage, End User, and Region - Global Forecast to 2030 |

||||||

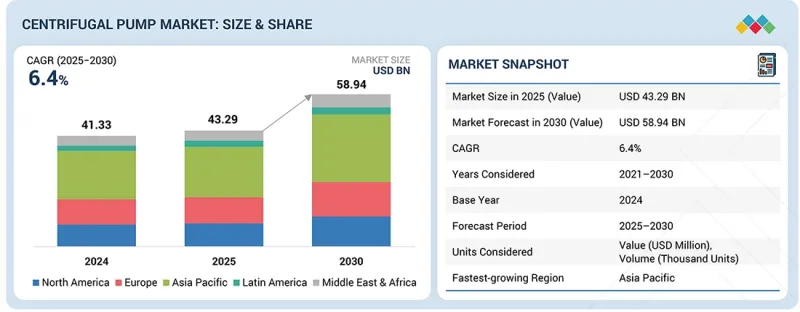

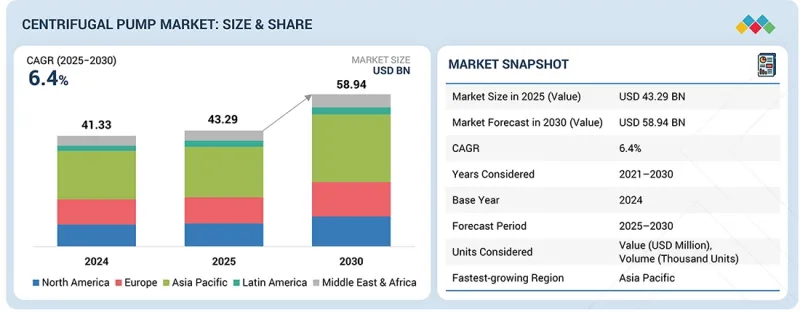

세계의 원심 펌프 시장 규모는 예측 기간 동안 CAGR 6.4%로 성장하여 2025년 432억 9,000만 달러에서 2030년까지 589억 4,000만 달러에 달할 것으로 추정됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 가치(100만/10억 달러) |

| 부문 | 유형별, 단수별, 운전 방식별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

발전 용량의 증가, 폐수처리의 필요성, 해수 담수화에 대한 요구가 증가함에 따라 원심 펌프 시장은 좋은 성장 전망을 가지고 있습니다.

유형별로 원심 펌프 시장은 오버행 임펠러, 수직형, 양손잡이 유형으로 분류됩니다. 오버행 임펠러식 원심 펌프는 상하수도 처리, 석유 및 가스, 화학, 제조 등 다양한 산업 분야에서 폭넓게 활용되고 있습니다. 산업 분야에서 신뢰할 수 있고 에너지 효율적인 펌프 솔루션에 대한 수요가 증가하고 있습니다. 이 펌프는 고성능과 높은 가동 효율을 실현하여 최종사용자의 에너지 소비를 줄이고 운영 비용을 절감하는 데 기여합니다. 효율적인 운영은 에너지 자원을 보존하고 탄소발자국을 줄이는 데 기여하며, 이는 업계의 지속가능한 실천이라는 목표에 부합하는 것입니다.

최종사용자별로는 물 및 폐수 부문이 예측 기간 동안 가장 큰 부문이 될 것으로 예상됩니다. 원심 펌프는 폐수처리 공정에서 약품 주입 응용 분야에서 중요한 역할을 합니다. 전체적으로 원심 펌프는 폐수처리 공정의 다양한 측면에서 중요한 역할을 수행하여 견고한 이물질 처리 능력을 제공하고 여과, 투약, 이송 및 기타 기능에 기여합니다. 경기 침체기에는 상수도 사업자가 상하수도 분야의 인프라 및 운영 효율성 향상에 집중하기 때문에 수요가 증가할 수 있습니다.

예측 기간 동안 북미는 아시아태평양에 이어 원심 펌프 시장에서 두 번째로 높은 성장률을 보일 것으로 예상됩니다. 아시아태평양의 원심 펌프 시장의 성장은 이 지역의 급성장하는 경제권의 수요 증가에 기인합니다. 한편, 북미 원심 펌프 시장은 상하수도 처리 시설의 원심 펌프 수요 증가에 힘입어 성장세를 보이고 있습니다. 또한, 미국의 노후화된 전력 및 수도 인프라, 캐나다의 화학 부문 확대, 멕시코만의 육상 및 해상 유전 증가, 새로운 상하수도 인프라 개발 등의 요인으로 인해 이 지역의 원심 펌프 수요는 더욱 증가할 것으로 예상됩니다.

원심 펌프 시장의 주요 기업으로는 Xylem(미국), Grundfos Holding A/S(덴마크), Flowserve Corporation(미국), KSB SE & Co. KGaA(독일), Wilo SE(독일) 등을 들 수 있습니다. 본 조사에서는 이들 주요 기업들에 대해 기업 프로파일, 최근 동향, 주요 시장 전략을 포함한 상세한 경쟁 분석을 실시하였습니다.

조사 범위:

이 보고서는 유형별, 작동 방식별, 단계별, 최종사용자별, 지역별로 세계 클린 파워 VFD 시장을 정의, 설명 및 예측합니다. 또한, 시장의 상세한 정성적, 정량적 분석을 제공합니다. 주요 시장 촉진요인, 억제요인, 기회, 도전과제에 대해 종합적으로 살펴봅니다. 또한, 시장의 다양한 중요한 측면을 다룹니다. 여기에는 경쟁 상황 분석, 시장 역학, 가치 기반 시장 추정, 원심 펌프 시장의 미래 동향이 포함됩니다.

본 보고서 구매의 주요 이점

- 본 보고서에서는 원심 펌프 시장의 성장에 영향을 미치는 주요 촉진요인(탐사 활동 및 산업 공정의 증가, 농업 분야의 수요 증가, 신규 주거 및 상업 시설의 증가), 제약요인(원심 펌프의 캐비테이션 효과 및 공회전 고장, 원심 펌프 시스템의 관리, 운영 및 유지보수에 필요한 기술력, 자금, 기회, 정부 주도의 첨단 펌프 파이프라인 인프라 투자), 도전과제(비조직적 세제 혜택), 기회(태양광 워터 펌프 보급 증가) 기술력, 자금, 인프라 부족), 기회(태양광 워터 펌프의 보급 확대, 첨단 펌프 및 파이프라인 인프라에 대한 정부 주도 투자), 도전 과제(비조직 부문의 치열한 경쟁) 등 원심 펌프 시장의 성장에 영향을 미치는 요인을 분석하고 있습니다.

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 원심 펌프 시장을 분석합니다.

- 시장 다각화 : 신제품 및 서비스, 미개척 지역, 최근 동향, 원심 펌프 시장 투자에 대한 자세한 정보를 수록하고 있습니다.

- 경쟁사 평가 : 주요 기업 - Xylem(미국), Grundfos Holding A/S(덴마크), Flowserve Corporation(미국), KSB SE & Co. KGaA(독일), Wilo SE(독일), Sulzer(스위스), Alfa Laval(스웨덴), ITT Inc. ),ITT Inc.(미국), Weir(영국), CIRCOR International(미국), Kirloskar Brothers Limited(인도), Tapflo AB(스웨덴), Baker Hughes(미국), SLB(미국), Pentair(미국), WEG(브라질), WEG(브라질) WEG(브라질), EBARA(일본) 등 원심 펌프 시장 주요 기업의 시장 점유율, 성장전략, 서비스 제공 현황을 상세히 분석하였습니다.

- 제품 혁신 및 개발 : 원심 펌프 시장에서는 디지털화 및 효율성에 대한 요구, 특히 IoT 기반 시스템 및 예지보전 기능의 통합으로 인해 높은 제품 도입률을 보이고 있습니다. 주요 혁신 사례로는 플로우서브의 INNOMAG TB-MAG 듀얼 드라이브를 들 수 있습니다. 이 펌프는 세계 최초의 씰리스 마그네틱 구동 원심 펌프이며, 진정한 2차 봉쇄 기능을 갖추고 있어 위험한 유체를 취급할 때 안전성과 누출 방지를 크게 향상시킵니다. 이러한 추세는 재생에너지를 이용한 물 시스템, 산업 공정 자동화, 스마트 펌프 인프라 등의 응용 분야에서 가속화되고 있으며, 펌프는 유지보수 및 업그레이드를 용이하게 하기 위해 지속가능한 재료, 재활용 가능한 부품, 모듈식 구성으로 설계되는 경우가 증가하고 있습니다. 설계되는 경우가 늘고 있습니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 원심 펌프 시장(유형별)

제10장 원심 펌프 시장(단수별)

제11장 원심 펌프 시장(운전 방식별)

제12장 원심 펌프 시장(최종사용자별)

제13장 원심 펌프 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSM 26.03.05The global centrifugal pump market is estimated to grow from USD 43.29 billion in 2025 to USD 58.94 billion by 2030, at a CAGR of 6.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Type, Operation Type, Stage, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

The increasing power generation capacity, wastewater treatment needs, and water desalination requirements have created favorable growth prospects for the centrifugal pump market.

"By type, the overhung impeller segment is expected to be the largest and fastest segment in the centrifugal market during the forecast period."

Based on type, the centrifugal pump market has been categorized into overhung impeller, vertically suspended, and between bearing. Overhung impeller centrifugal pumps are extensively utilized across various industries, including water and wastewater treatment, oil and gas, chemicals, and manufacturing. There is a growing need for dependable and energy-efficient pumping solutions in industrial applications. These pumps excel in delivering high performance and operational efficiency, leading to decreased energy consumption and lower operational expenses for end users. Their efficient operation aids in conserving energy resources and reducing carbon footprints, aligning with the industry's objectives of sustainable practices.

"By industrial end user, the water and wastewater segment is expected to be the largest market during the forecast period."

Based on end user, the water and wastewater segment is expected to be the largest segment during the forecast period. Centrifugal pumps play a vital role in dosing applications within wastewater treatment processes. Overall, centrifugal pumps play a vital role in various aspects of wastewater treatment processes, offering robust debris handling capabilities and contributing to functions such as filtration, dosing, and transfer. They can experience increased demand during economic downturns as utilities focus on enhancing infrastructure and operational effectiveness within the water and wastewater sector.

"North America is expected to be the second fastest-growing region after Asia Pacific in the centrifugal pump market."

North America, after Asia Pacific, is expected to be the second-fastest region in the centrifugal pump market during the forecast period. The growth of the centrifugal pump market in Asia Pacific can be attributed to the increased demand for these pumps from the fast-growing economies in the region. Whereas the centrifugal pump market in North America is experiencing growth driven by the increasing demand for centrifugal pumps in water and wastewater treatment plants. Additionally, factors such as the aging power and water infrastructures in the US, the expanding chemicals sector in Canada, the growing number of onshore and offshore oilfields in the Gulf of Mexico, and the development of new water and wastewater infrastructures are expected to further boost the demand for centrifugal pumps in the region.

In-depth interviews have been conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among other experts, to obtain and verify critical qualitative and quantitative information and assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1- 65%, Tier 2- 24%, and Tier 3 - 11%

By Designation: C-level Executives - 30%, Directors - 25%, and Others - 45%

By Region: North America - 21%, Europe - 26%, Asia Pacific - 44%, Middle East & Africa - 7%, and South America - 3%

Notes: The tiers of the companies are defined based on their total revenues as of 2024. Tier 1: > USD 1 billion, Tier 2: USD 500 million to USD 1 billion, and Tier 3: < USD 500 million.

Other designations include sales managers, engineers, and regional managers.

Xylem (US), Grundfos Holding A/S (Denmark), Flowserve Corporation (US), KSB SE & Co. KGaA (Germany), and Wilo SE (Germany) are some of the major players in the centrifugal pump market. The study includes an in-depth competitive analysis of these key players, including their company profiles, recent developments, and key market strategies.

Research Coverage:

The report defines, describes, and forecasts the global clean power VFD market by type, operation type, stage, end user, and region. It also offers a detailed qualitative and quantitative analysis of the market. The report comprehensively reviews the major market drivers, restraints, opportunities, and challenges. It also covers various important aspects of the market. These include an analysis of the competitive landscape, market dynamics, market estimates in terms of value, and future trends in the centrifugal pump market.

Key Benefits of Buying the Report

- It provides an analysis of key drivers (Increasing exploration activities and industrial processes, rising demand from agriculture sector, expanding new residential and commercial structures), restraints (cavitation effect and dry-run failures in centrifugal pumps, lack of technical skills, funding, and infrastructure to manage, operate, and maintain centrifugal pump systems), opportunities (Increased adoption of solar water pumps, government-driven investment in advanced pumping and pipeline infrastructure), challenges (High competition from unorganized sector) influencing the growth of the centrifugal pump market.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the centrifugal pump market across varied regions.

- Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the centrifugal pump market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Xylem (US), Grundfos Holding A/S (Denmark), Flowserve Corporation (US), KSB SE & Co. KGaA (Germany), Wilo SE (Germany), Sulzer (Switzerland), Alfa Laval (Sweden), ITT Inc. (US), Weir (UK), CIRCOR International (US), Kirloskar Brothers Limited (India), Tapflo AB (Sweden), Baker Hughes (US), SLB (US), Pentair (US), WEG (Brazil), and EBARA Corporation (Japan); among others in the centrifugal pump market.

- Product Innovation/Development: The centrifugal pump market is witnessing high product introduction rates, driven by digitalization and efficiency demands, especially through integration of IoT-based systems and predictive maintenance features. Key innovations include solutions like Flowserve Corporation's INNOMAG TB-MAG Dual Drive - the world's first seal-less magnetic drive centrifugal pump with true secondary containment - which significantly improves safety and leak prevention for handling hazardous fluids. This trend is accelerating in applications such as renewable energy-based water systems, industrial process automation, and smart pumping infrastructure, where pumps are increasingly designed with sustainable materials, recyclable components, and modular configurations to ease maintenance and upgrades.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIONS SHAPING CENTRIFUGAL PUMP MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CENTRIFUGAL PUMP MARKET

- 3.2 CENTRIFUGAL PUMP MARKET, BY STAGE AND REGION

- 3.3 CENTRIFUGAL PUMP MARKET, BY TYPE

- 3.4 CENTRIFUGAL PUMP MARKET, BY OPERATION TYPE

- 3.5 CENTRIFUGAL PUMP MARKET, BY STAGE

- 3.6 CENTRIFUGAL PUMP MARKET, BY END USER

- 3.7 CENTRIFUGAL PUMP MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing exploration activities and industrial processes

- 4.2.1.2 Rising demand from agriculture sector

- 4.2.1.3 Expanding new residential and commercial structures

- 4.2.2 RESTRAINTS

- 4.2.2.1 Cavitation effect and dry-run failures in centrifugal pumps

- 4.2.2.2 Lack of technical skills, funding, and infrastructure to manage, operate, and maintain centrifugal pump systems

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increased adoption of solar water pumps

- 4.2.3.2 Government-driven investment in advanced pumping and pipeline infrastructure

- 4.2.4 CHALLENGES

- 4.2.4.1 High competition from unorganized sector

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN CENTRIFUGAL PUMP MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL CENTRIFUGAL PUMP INDUSTRY

- 5.2.4 TRENDS IN GLOBAL SMART PUMP INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF CENTRIFUGAL PUMPS OFFERED BY KEY PLAYERS, 2024

- 5.5.2 AVERAGE SELLING PRICES OF CENTRIFUGAL PUMPS, BY STAGE

- 5.5.3 AVERAGE SELLING PRICE TREND OF CENTRIFUGAL PUMPS, BY REGION, 2022-2024

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 841370)

- 5.6.2 EXPORT SCENARIO (HS CODE 841370)

- 5.7 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 BOILER FEED MULTISTAGE PUMP - ENERGY SAVING

- 5.10.2 PETROCHEMICAL PLANT - DISCHARGE OVERPRESSURE RISK

- 5.10.3 COOLING WATER PUMP - SHAFT FAILURES AT PART LOAD

- 5.11 IMPACT OF 2025 US TARIFF ON CENTRIFUGAL PUMP MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.4.4 South America

- 5.11.4.5 Middle East and Africa

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 VARIABLE FREQUENCY DRIVE PUMP

- 6.1.2 ADVANCED HYDRAULIC DESIGN

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 SMART PUMP

- 6.2.2 MAGNETIC DRIVE PUMP

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.6 IMPACT OF AI/GEN AI ON CENTRIFUGAL PUMP MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN CENTRIFUGAL PUMP MARKET

- 6.6.3 CASE STUDIES OF AI/GEN AI IMPLEMENTATION IN CENTRIFUGAL PUMP MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI/GEN AI IN CENTRIFUGAL PUMP MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 SUSTAINABILITY INITIATIVES

- 7.1.1 CARBON IMPACT AND ECO-APPLICATIONS OF CENTRIFUGAL PUMPS

- 7.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

- 7.4 REGIONAL REGULATIONS AND COMPLIANCE

- 7.4.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.4.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS APPLICATIONS

- 8.5 MARKET PROFITABILITY

9 CENTRIFUGAL PUMP MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 OVERHUNG IMPELLER

- 9.2.1 DEMAND FOR COMPACT DESIGN IN RESIDENTIAL APPLICATIONS

- 9.3 BETWEEN BEARING

- 9.3.1 INCREASED DEMAND FOR HIGH-PRESSURE PUMPS FROM INDUSTRIAL SECTOR

- 9.4 VERTICALLY SUSPENDED

- 9.4.1 OPTION TO CHOOSE RANGE OF OPERATING PRESSURE AND TEMPERATURE

10 CENTRIFUGAL PUMP MARKET, BY STAGE

- 10.1 INTRODUCTION

- 10.2 SINGLE STAGE

- 10.2.1 URBAN WATER INFRASTRUCTURE EXPANSION AND IRRIGATION MODERNIZATION DRIVING DEMAND FOR SINGLE-STAGE CENTRIFUGAL PUMPS

- 10.3 MULTISTAGE

- 10.3.1 HIGH-PRESSURE REQUIREMENTS DRIVING DEMAND

11 CENTRIFUGAL PUMP MARKET, BY OPERATION TYPE

- 11.1 INTRODUCTION

- 11.2 ELECTRICAL

- 11.2.1 GROWING INDUSTRIAL ACTIVITY FAVORING GROWTH OF ELECTRICAL CENTRIFUGAL PUMPS

- 11.3 HYDRAULIC

- 11.3.1 URBAN WATER EXPANSION AND IRRIGATION MODERNIZATION ACCELERATING DEMAND FOR HYDRAULIC CENTRIFUGAL PUMPING SYSTEMS

- 11.4 AIR-DRIVEN

- 11.4.1 SAFETY-CRITICAL OPERATIONS AND REMOTE INDUSTRIAL APPLICATIONS DRIVING DEMAND FOR AIR-DRIVEN PUMPS

12 CENTRIFUGAL PUMP MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 INDUSTRIAL

- 12.2.1 OIL AND GAS

- 12.2.1.1 Expanding oil and gas market to generate demand for centrifugal pumps

- 12.2.2 WATER AND WASTEWATER

- 12.2.2.1 Growth via regulations and smart infrastructure investments

- 12.2.3 METALS AND MINING

- 12.2.3.1 Infrastructure development to drive market growth

- 12.2.4 CHEMICALS

- 12.2.4.1 Powering chemical industry efficiency and safety

- 12.2.5 POWER GENERATION

- 12.2.5.1 Focus on unconventional power generation

- 12.2.6 FOOD AND BEVERAGES

- 12.2.6.1 Modernization of food and beverage processing

- 12.2.7 PHARMACEUTICALS

- 12.2.7.1 Extensive R&D and production of medicines and vaccines

- 12.2.8 PULP AND PAPER

- 12.2.8.1 Sustainability and packaging surge to drive market growth

- 12.2.9 AGRICULTURE

- 12.2.9.1 Surging adoption of solar-powered centrifugal pumps to augment market growth

- 12.2.10 AUTOMOTIVE

- 12.2.10.1 Growing auto & EV demand drives centrifugal pump market

- 12.2.11 TEXTILES

- 12.2.11.1 Rise in textile manufacturing sector

- 12.2.1 OIL AND GAS

- 12.3 COMMERCIAL AND RESIDENTIAL

- 12.3.1 COMMERCIAL AND RESIDENTIAL DEVELOPMENT PROJECTS

13 CENTRIFUGAL PUMP MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Rising wastewater treatment activities

- 13.2.2 CANADA

- 13.2.2.1 Wastewater regulations and infrastructure upgrade drive market growth

- 13.2.3 MEXICO

- 13.2.3.1 Rapid industrialization, urbanization, and infrastructure investments driving market growth

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Surging investments in coal-fired generation permits

- 13.3.2 UK

- 13.3.2.1 Wastewater treatment upgrades likely to drive market

- 13.3.3 ITALY

- 13.3.3.1 Italy's pump power surge PNRR wastewater revolution

- 13.3.4 FRANCE

- 13.3.4.1 Wastewater Pump Revolution France 2030 Initiative Drives Surge

- 13.3.5 RUSSIA

- 13.3.5.1 Increased focus on mining sector

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Surging investments in coal-fired generation permits

- 13.4.2 JAPAN

- 13.4.2.1 Expansion of Japan's food processing industry

- 13.4.3 INDIA

- 13.4.3.1 Rising agricultural investment and irrigation expansion driving demand for centrifugal pumping solutions

- 13.4.4 SOUTH KOREA

- 13.4.4.1 Expansion and modernization of South Korea's chemical industry driving demand for advanced centrifugal pumping systems

- 13.4.5 BANGLADESH

- 13.4.6 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Rising wastewater treatment activities

- 13.5.2 ARGENTINA

- 13.5.2.1 Argentina's agricultural modernization spurs growth and drives centrifugal pump demand

- 13.5.3 REST OF SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 GCC

- 13.6.1.1 Saudi Arabia

- 13.6.1.1.1 Large-scale industrial base and energy transition initiative to accelerate market growth

- 13.6.1.2 UAE

- 13.6.1.2.1 Rapid industrialization and infrastructure development to fuel market growth

- 13.6.1.3 Qatar

- 13.6.1.3.1 Surging investments in industrial manufacturing to meet Qatar National Vision 2030

- 13.6.1.4 Turkey

- 13.6.1.4.1 Increased investments in wastewater treatment sector to meet rising energy demand

- 13.6.1.5 Rest of GCC

- 13.6.1.1 Saudi Arabia

- 13.6.2 SOUTH AFRICA

- 13.6.2.1 Infrastructure and water security projects drive market growth

- 13.6.3 NIGERIA

- 13.6.3.1 Oil & gas and urban water projects drive market growth

- 13.6.4 REST OF MIDDLE EAST & AFRICA

- 13.6.1 GCC

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 14.3 SEGMENTAL REVENUE ANALYSIS, 2020-2024

- 14.4 MARKET SHARE ANALYSIS, 2024

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 PRODUCT COMPARISON

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Type footprint

- 14.7.5.4 Operation type footprint

- 14.7.5.5 Stage footprint

- 14.7.5.6 End user footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 MAJOR PLAYERS

- 15.1.1 GRUNDFOS HOLDING A/S

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths/Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 XYLEM

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths/Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 FLOWSERVE CORPORATION

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths/Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 KSB SE & CO. KGAA

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansions

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths/Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 WILO SE

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.3.2 Deals

- 15.1.5.3.3 Expansions

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths/Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 SULZER LTD

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches

- 15.1.6.3.2 Deals

- 15.1.6.3.3 Expansions

- 15.1.7 EBARA CORPORATION

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Deals

- 15.1.8 THE WEIR GROUP PLC

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.8.3.2 Deals

- 15.1.9 ITT INC.

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches

- 15.1.9.3.2 Deals

- 15.1.9.3.3 Expansions

- 15.1.10 CIRCOR INTERNATIONAL

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches

- 15.1.11 BAKER HUGHES COMPANY (A GE COMPANY)

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.12 WEG

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.13 PENTAIR

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.14 ALFA LAVAL

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Deals

- 15.1.15 KIRLOSKAR BROTHERS LIMITED

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Product launches

- 15.1.16 SLB

- 15.1.16.1 Business overview

- 15.1.16.2 Products/Solutions/Services offered

- 15.1.16.3 Recent developments

- 15.1.16.3.1 Product launches

- 15.1.16.3.2 Deals

- 15.1.17 TSURUMI MANUFACTURING CO., LTD.

- 15.1.17.1 Business overview

- 15.1.17.2 Products/Solutions/Services offered

- 15.1.17.3 Recent developments

- 15.1.17.3.1 Deals

- 15.1.18 GORMAN-RUPP PUMPS

- 15.1.18.1 Business overview

- 15.1.18.2 Products/Solutions/Services offered

- 15.1.1 GRUNDFOS HOLDING A/S

- 15.2 OTHER PLAYERS

- 15.2.1 TAPFLO AB

- 15.2.2 MODY PUMPS

- 15.2.3 CELEROS FLOW TECHNOLOGY

- 15.2.4 GRINDEX

- 15.2.5 GRISWOLD (A PSG DOVER COMPANY)

- 15.2.6 MACKWELL PUMPS

- 15.2.7 EVOGUARD GMBH

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.2 SECONDARY AND PRIMARY RESEARCH

- 16.2.1 SECONDARY DATA

- 16.2.1.1 List of key secondary sources

- 16.2.1.2 Key data from secondary sources

- 16.2.2 PRIMARY DATA

- 16.2.2.1 List of primary interview participants

- 16.2.2.2 Key industry insights

- 16.2.2.3 Breakdown of primaries

- 16.2.2.4 Key data from primary sources

- 16.2.1 SECONDARY DATA

- 16.3 MARKET SIZE ESTIMATION METHODOLOGY

- 16.3.1 BOTTOM-UP APPROACH

- 16.3.2 TOP-DOWN APPROACH

- 16.3.3 DEMAND-SIDE ANALYSIS

- 16.3.3.1 Demand-side assumptions

- 16.3.3.2 Demand-side calculations

- 16.3.4 SUPPLY-SIDE ANALYSIS

- 16.3.4.1 Supply-side assumptions

- 16.3.4.2 Supply-side calculations

- 16.4 GROWTH FORECAST

- 16.5 MARKET BREAKDOWN AND DATA TRIANGULATION

- 16.6 RESEARCH LIMITATIONS

- 16.7 RISK ANALYSIS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS