|

시장보고서

상품코드

1936012

가스 센서 시장 : 제품별, 출력 유형별, 접속 방식별, 기술별, 유형별, 최종 용도별, 지역별 - 세계 예측(-2033년)Gas Sensor Market By Gas Type (Oxygen, Carbon Monoxide, Carbon Dioxide, Volatile Organic Compounds, Hydrocarbons), Technology (Electrochemical, Infrared, Solid-State/Metal-Oxide-Semiconductors), Output Type, Connectivity- Global Forecast to 2033 |

||||||

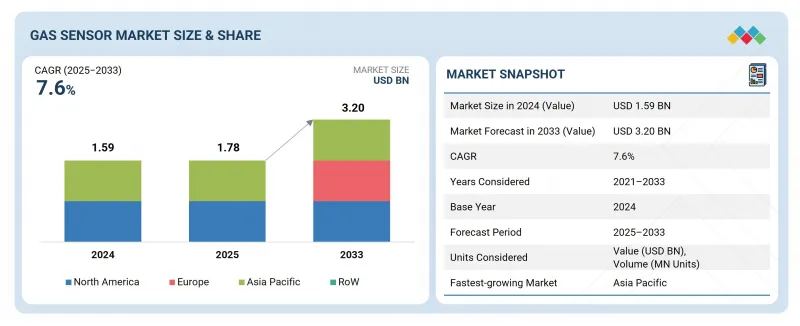

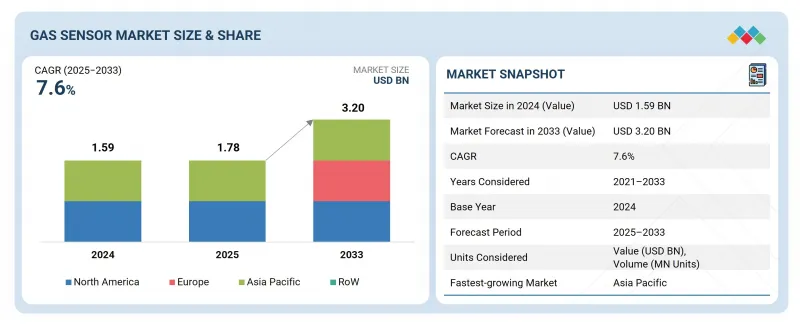

세계의 가스 센서 시장 규모는 2025년 17억 8,000만 달러에서 2033년까지 32억 달러로 성장하여 2025년부터 2033년까지 연평균 성장률(CAGR)은 7.6%로 예측됩니다.

이러한 성장은 석유 및 가스, 화학, 광업, 전력 등 주요 산업의 수요 증가에 의해 주도되고 있습니다. 또한, 사물인터넷(IoT), 빌딩 자동화 및 현대적 제어 시스템의 발전으로 소형화된 무선 가스 센서에 대한 수요가 증가하고 있습니다. 이 센서는 저전력, 고성능, 소형 사이즈로 평가받고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2033년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2033년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품별, 출력 유형별, 접속 방식별, 기술별, 유형별, 최종 용도별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

또한, 스마트폰과 웨어러블 기기에 가스 센서를 통합하여 환경과 대기 중 공기질을 지속적으로 모니터링할 수 있게 됨에 따라 향후 몇 년 동안 수요가 증가할 것으로 예상됩니다.

"출력 유형별로는 디지털 부문이 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예상됩니다."

가스 센서 시장의 디지털 부문은 보다 진보되고 지능적이며 연결된 가스 감지 솔루션에 대한 수요 증가로 인해 더 높은 CAGR을 기록할 것으로 예상됩니다. 디지털 가스 센서는 아날로그 방식에 비해 정확도 향상, 스마트 시스템과의 연결 방식, 고급 신호 처리 기능 등 여러 가지 장점을 제공합니다. 산업 분야의 디지털화와 사물인터넷(IoT) 기술 채택이 증가함에 따라 디지털 네트워크 연결, 원격 데이터 전송, 자동화 시스템에 통합할 수 있는 가스 센서에 대한 수요가 증가하고 있습니다.

유선 부문은 이미 구축된 인프라와 산업용 애플리케이션의 신뢰성으로 인해 전체 시장에서 더 큰 점유율을 차지하고 있습니다. 유선 가스 센서는 안정적이고 지속적인 데이터 전송이 필수적이며, 전원 공급과 연결 방식이 확보된 환경에서 일반적으로 사용됩니다. 제조업, 석유화학, 자동차, 의료 등의 산업에서는 내구성과 제어 시스템에 직접 연결되는 방식 때문에 유선 센서가 선호되며, 정확하고 끊김 없는 데이터 모니터링이 보장됩니다. 유선 가스 센서는 무선 기술에 영향을 미칠 수 있는 간섭이나 신호 손실 문제에 영향을 덜 받기 때문에 특정 응용 분야에서 더 안전하고 안정적인 것으로 간주되는 경우가 많습니다.

예측 기간 동안 중국은 아시아태평양의 가스 센서 시장에서 우위를 유지할 것으로 예상됩니다. 중국에서는 공정 산업(특히 화학제품 제조 및 석유 정제) 및 전력 발전과 같은 유틸리티 사업이 가스 센서의 주요 수요처로 남을 것입니다. 석유 및 가스, 인프라, 상하수도 처리 등의 분야가 가스 센서 시장의 성장을 견인할 것으로 예상됩니다. 또한, 대기오염이 건강에 미치는 영향에 대한 대중의 인식이 높아지면서 가스 센서가 장착된 스마트 공기질 모니터, 스마트 밴드, 공기청정기, 공기청정기, 공기청정장치에 대한 수요도 증가하고 있습니다.

Honeywell International Inc.(미국), MSA Safety Incorporated(미국), Amphenol Corporation(미국), Figaro Engineering Inc. Sensirion AG(스위스), Process Sensing Technologies(영국), ams-OSRAM AG(오스트리아), MEMBRAPOR(스위스), Senseair AB(미국) 등이 가스 센서 시장의 주요 기업입니다.

가스 센서 시장의 주요 기업들에 대해 조사했으며, 상세한 경쟁 분석과 함께 기업 프로파일, 최근 동향, 주요 시장 전략 등의 정보를 전해드립니다.

조사 범위:

본 조사 보고서는 가스 센서 시장을 출력 유형별, 연결 방식별, 제품 유형별, 기술별, 유형별, 최종 용도별, 지역별로 분석하고 있습니다. 이 보고서는 가스 센서 시장의 주요 시장 촉진요인, 저해요인, 도전과제, 기회를 개괄하고 2033년까지의 예측을 제공합니다. 또한, 가스 센서 생태계 내 모든 기업에 대한 리더십 매핑 및 분석도 포함되어 있습니다.

본 보고서 구매의 주요 이점

이 보고서는 전체 가스 센서 시장과 그 하위 부문의 예상 수익 규모를 제공함으로써 시장 리더와 신규 진입자에게 도움이 될 것입니다. 이해관계자들이 경쟁 상황을 이해하고, 비즈니스를 더 잘 포지셔닝하고, 효과적인 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 또한, 주요 촉진요인, 억제요인, 도전과제, 기회 등 시장 동향에 대한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인(석유 및 가스, 화학, 광업, 전력 부문 수요 증가, 건강 및 안전 규제 시행, HVAC 시스템 및 대기질 모니터에 가스 센서 통합, 자율주행차 수요 급증) 기회(사물인터넷, 클라우드 컴퓨팅, 빅데이터 기술 통합, 소비자 전자기기 채택 확대, 소형 무선 가스 센서 수요 증가), 도전 과제(복잡한 제조 공정) 기기에서의 채택 확대, 소형 무선 가스 센서 수요 증가), 도전과제(복잡한 제조 공정)가 가스 센서 시장 성장에 미치는 영향에 대해

- 제품 개발/혁신 : 가스 센서 시장의 향후 기술 동향, 연구개발 활동, 최신 제품 및 서비스 출시에 대한 상세 분석

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 가스 센서 시장을 분석합니다.

- 시장 다각화 : 신제품 및 서비스, 미개척 지역, 최근 동향, 가스 센서 시장 투자에 관한 종합적인 정보

- 경쟁사 평가 : 주요 기업 - Honeywell International Inc. ), Sensirion AG(스위스), Process Sensing Technologies(영국), ams-Osram AG(오스트리아), MEMBRAPOR(스위스), Senseair AB(미국) 등 가스 센서 시장 주요 기업의 시장 점유율, 성장 전략, 서비스 제공 서비스 제공 내용에 대한 상세 분석

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 가스 센서 시장(제품별)

제10장 가스 센서 시장(출력 유형별)

제11장 가스 센서 시장(접속 방식별)

제12장 가스 센서 시장(기술별)

제13장 가스 센서 시장(유형별)

제14장 가스 센서 시장(최종 용도별)

제15장 가스 센서 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSM 26.03.05The global gas sensor market is expected to grow from USD 1.78 billion in 2025 to USD 3.20 billion by 2033, with a compound annual growth rate (CAGR) of 7.6% from 2025 to 2033. This growth is driven by increasing demand in key industries such as oil & gas, chemicals, mining, and power. Additionally, the demand for miniaturized wireless gas sensors is rising due to advancements in IoT, building automation, and modern control systems. These sensors are valued for their low power consumption, high performance, and small size.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2033 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Units Considered | Value (USD Billion) |

| Segments | By Gas Type, Technology, Connectivity and region |

| Regions covered | North America, Europe, APAC, RoW |

Furthermore, the integration of gas sensors into smartphones and wearable devices for continuous environmental or atmospheric air quality monitoring is expected to boost demand in the coming years.

"By output type, digital segment to grow at highest CAGR during forecast period"

The digital segment of the gas sensor market is expected to register a higher CAGR due to rising demand for more advanced, intelligent, and connected gas sensing solutions. Digital gas sensors provide several benefits over their analog equivalents, including better accuracy, the ability to connect with smart systems, and advanced signal processing features. As industries adopt digitalization and Internet of Things (IoT) technologies, the need for gas sensors that can connect to digital networks, send data remotely, and integrate into automated systems is increasing.

"Wired segment to capture largest share of gas sensor market in 2025"

The wired segment holds a larger share of the overall market due to its established infrastructure and reliability in industrial applications. Wired gas sensors are commonly used in environments where stable and continuous data transmission is essential and where power supply and connectivity are reliable. Industries such as manufacturing, petrochemical, automotive, and healthcare prefer wired sensors for their durability and direct connection to control systems, ensuring precise and uninterrupted data monitoring. Wired gas sensors are often considered more secure and stable for certain applications because they are less susceptible to interference and signal loss issues that can affect wireless technologies.

"China to be largest market for gas sensors in Asia Pacific."

China is expected to maintain its dominance in the gas sensor market across Asia Pacific during the forecast period. Process industries, especially chemical production and petroleum refining, along with public utilities like electric power generation, will remain the primary consumers of gas sensors in the country. Sectors such as oil & gas, infrastructure, and water & wastewater treatment, among others, are projected to drive the growth of the gas sensor market. Additionally, increasing public awareness about the health impacts of air pollution is also boosting demand for smart air quality monitors, smart bands, air purifiers, and air cleaners that are equipped with gas sensors.

Extensive primary interviews were conducted with key industry experts in the gas sensor market to determine and verify the market size for various segments and subsegments. The breakdown of primary participants for the report is shown below: The study includes insights from a range of industry experts, from component suppliers to Tier 1 companies and OEMs. The breakdown of the primary respondents is as follows:

- By Company Type: Tier 1 - 20%, Tier 2 - 45%, and Tier 3 - 35%

- By Designation: C-level Executives - 35%, Directors - 340%, and Others - 20%

- By Region: North America - 25%, Europe - 20%, Asia Pacific - 45%, and RoW - 10%

Note: Three tiers of companies are defined based on their total revenue as of 2024; tier 1: revenue more than or equal to USD 500 million, tier 2: revenue between USD 100 million and USD 500 million, and tier 3: revenue less than or equal to USD 100 million. Other designations include sales and marketing executives, researchers, and members of various gas sensor organizations.

Honeywell International Inc. (US), MSA Safety Incorporated (US), Amphenol Corporation (US), Figaro Engineering Inc. (Japan), Alphasense (UK), Sensirion AG (Switzerland), Process Sensing Technologies (UK), ams-OSRAM AG (Austria), MEMBRAPOR (Switzerland), and Senseair AB (US), among others, are the key players in the gas sensor market.

The study includes an in-depth competitive analysis of these key players in the gas sensor market, as well as their company profiles, recent developments, and key market strategies.

Research Coverage:

This research report categorizes the gas sensor market by output type (analog and digital), connectivity (wired and wireless), product (gas analyzers & monitors, gas detectors, air quality monitors, air purifiers/air cleaners, HVAC systems, medical equipment, and consumer devices), technology (electrochemical, photoionization detection (PID), solid-state/metal-oxide-semiconductors (MOS), catalytic, infrared, laser, zirconia, holographic, and others), gas type (oxygen (O2), carbon monoxide (CO), carbon dioxide (CO2), ammonia (NH3), chlorine (Cl), hydrogen sulfide (H2S), nitrogen oxides (NOx), volatile organic compounds, methane (CH4), hydrocarbons, and hydrogen), end use (automotive & transportation, smart cities & building automation, oil & gas industry, water & wastewater treatment, food & beverage industry, power stations, medical industry, metal & chemical industry, mining, consumer electronics, and government & regulatory bodies), and region (North America, Europe, Asia Pacific, and RoW). The report outlines the key drivers, restraints, challenges, and opportunities in the gas sensor market and provides forecasts until 2033. It also includes leadership mapping and analysis of all companies within the gas sensor ecosystem.

Key Benefits of Buying the Report

The report will assist market leaders and new entrants by providing estimated revenue figures for the overall gas sensor market and its subsegments. It will help stakeholders understand the competitive landscape and gain insights to better position their businesses and develop effective go-to-market strategies. Additionally, the report offers information on the market pulse, including key drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (rising demand in oil & gas, chemicals, mining, and power sectors, implementation of health and safety regulations, integration of gas sensors into HVAC systems and air quality monitors, surge in demand for autonomous vehicles) restraints (intense pricing pressure resulting in declining average selling prices), opportunities (incorporation of Internet of Things, cloud computing, and big data technologies, growing adoption in consumer electronics, increasing demand for miniaturized wireless gas sensors) and challenges (complex manufacturing process) influencing the growth of the gas sensor market

- Product Development/Innovation: Detailed insights into upcoming technologies, research and development activities, and the latest product and service launches in the gas sensor market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the gas sensor market across varied regions

- Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the gas sensor market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players, such as Honeywell International Inc. (US), MSA Safety Incorporated (US), Amphenol Corporation (US), Figaro Engineering Inc. (Japan), Alphasense (UK), Sensirion AG (Switzerland), Process Sensing Technologies (UK), ams-OSRAM AG (Austria), MEMBRAPOR (Switzerland), and Senseair AB (US) in the gas sensor market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION AND SCOPE

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN GAS SENSOR MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN GAS SENSOR MARKET

- 3.2 GAS SENSOR MARKET, BY PRODUCT

- 3.3 GAS SENSOR MARKET, BY TECHNOLOGY

- 3.4 GAS SENSOR MARKET, BY TYPE

- 3.5 GAS SENSOR MARKET, BY END USE

- 3.6 GAS SENSOR MARKET, BY CONNECTIVITY AND OUTPUT TYPE

- 3.7 GAS SENSOR MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising demand in oil & gas, chemicals, mining, and power sectors

- 4.2.1.2 Implementation of health and safety regulations

- 4.2.1.3 Integration of gas sensors into HVAC systems and air quality monitors

- 4.2.1.4 Surge in demand for autonomous vehicles

- 4.2.2 RESTRAINTS

- 4.2.2.1 Intense pricing pressure resulting in declining average selling prices

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Incorporation of Internet of Things, cloud computing, and big data technologies

- 4.2.3.2 Growing adoption in consumer electronics

- 4.2.3.3 Increasing demand for miniaturized wireless gas sensors

- 4.2.4 CHALLENGES

- 4.2.4.1 Complex manufacturing process

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN GAS SENSORS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 MARKET DYNAMICS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 THREAT OF NEW ENTRANTS

- 5.2.2 THREAT OF SUBSTITUTES

- 5.2.3 BARGAINING POWER OF SUPPLIERS

- 5.2.4 BARGAINING POWER OF BUYERS

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC INDICATORS

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN GLOBAL AUTOMOTIVE AND TRANSPORTATION INDUSTRY

- 5.3.4 TRENDS IN GLOBAL SMART CITIES AND BUILDING-AUTOMATION INDUSTRY

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE, 2024

- 5.6.2 AVERAGE SELLING PRICE TREND, BY TYPE

- 5.6.3 AVERAGE SELLING PRICE TREND, BY REGION

- 5.7 TRADE ANALYSIS

- 5.8 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.10 INVESTMENT AND FUNDING SCENARIO, 2024 AND 2025

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 ION SCIENCE PARTNERED WITH BLACKLINE SAFETY CORP. TO TACKLE PROBLEM OF HUMIDITY INFLUENCING VOC READINGS

- 5.11.2 CO2METER USED GAS SENSORS AS CO2 ALARMS FOR CO2 LEAK DETECTION

- 5.11.3 STORAGE CONTROL SYSTEMS LTD. DEVELOPED SPRINTIR CO2 SENSOR FOR FAST AND ACCURATE READING

- 5.12 IMPACT OF 2025 US TARIFFS

- 5.12.1 KEY TARIFF RATES

- 5.12.2 PRICE IMPACT ANALYSIS

- 5.12.3 IMPACT ON VARIOUS COUNTRIES/REGIONS

- 5.12.3.1 US

- 5.12.3.2 Europe

- 5.12.3.3 Asia Pacific

- 5.12.4 IMPACT ON VERTICALS

6 TECHNOLOGICAL ADVANCEMENT, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGICAL ADVANCEMENTS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Miniaturization

- 6.1.1.2 Microelectromechanical system (MEMS) gas sensors

- 6.1.1.3 Nanomaterial integration

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 E-nose

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Printed gas sensors

- 6.1.3.2 Zeolite material-based gas sensors

- 6.1.3.3 Wearable technology

- 6.1.1 KEY TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 PATENT ANALYSIS

- 6.4 IMPACT OF AI ON GAS SENSORS

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.4.2 BEST PRACTICES IN GAS SENSOR MARKET

- 6.4.3 CASE STUDIES OF AI IMPLEMENTATION IN GAS SENSOR MARKET

- 6.4.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.4.5 CLIENTS' READINESS TO ADOPT AI IN GAS SENSOR MARKET

7 REGULATORY LANDSCAPE

- 7.1 INTRODUCTION

- 7.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.3 STANDARDS AND REGULATIONS RELATED TO GAS SENSORS

- 7.3.1 STANDARDS

- 7.3.1.1 AS4641

- 7.3.1.2 ISO 19891-1

- 7.3.1.3 Restriction of Hazardous Substances Directive

- 7.3.1.4 ATmosphere EXplosible

- 7.3.1.5 Edison Testing Laboratories

- 7.3.1.6 Safety Integrity Level 1

- 7.3.1.7 Material safety data sheet

- 7.3.1.8 National and regional legislation

- 7.3.1.9 List of standards for gas sensors

- 7.3.1 STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END USERS

9 GAS SENSOR MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 GAS ANALYZERS & MONITORS

- 9.2.1 GROWING USE FOR PRECISION AND REAL-TIME MONITORING TO DRIVE SEGMENTAL GROWTH

- 9.3 GAS DETECTORS

- 9.3.1 INCREASING WORKPLACE SAFETY CONCERNS IN HAZARDOUS INDUSTRIES TO PROPEL DEMAND FOR ADVANCED GAS DETECTORS

- 9.4 AIR QUALITY MONITORS

- 9.4.1 RISING AWARENESS OF AIR POLLUTION DRIVING DEMAND FOR ADVANCED AIR QUALITY MONITORS IN SMART CITIES AND HOMES

- 9.5 AIR PURIFIERS/AIR CLEANERS

- 9.5.1 GROWING DEMAND FOR SMART AIR PURIFIERS EQUIPPED WITH VOC SENSORS TO BOOST MARKET

- 9.6 HVAC SYSTEMS

- 9.6.1 INCREASING ADOPTION OF NATURAL REFRIGERANTS FUELING NEED FOR ADVANCED GAS SENSORS IN HVAC SYSTEMS

- 9.7 MEDICAL EQUIPMENT

- 9.7.1 GROWING ADOPTION OF GAS SENSORS IN HEALTHCARE AND MEDICAL LABS ACCELERATING MARKET GROWTH

- 9.8 CONSUMER DEVICES

- 9.8.1 AI-ENHANCED GAS SENSORS INCREASINGLY ADOPTED IN SMART CONSUMER DEVICES

10 GAS SENSOR MARKET, BY OUTPUT TYPE

- 10.1 INTRODUCTION

- 10.2 ANALOG

- 10.2.1 HIGH DEMAND IN INDUSTRIAL WORKPLACES TO DRIVE MARKET GROWTH

- 10.3 DIGITAL

- 10.3.1 HIGH TECHNICAL PERFORMANCE AND LOW MAINTENANCE COST TO FUEL DEMAND

11 GAS SENSOR MARKET, BY CONNECTIVITY

- 11.1 INTRODUCTION

- 11.2 WIRED

- 11.2.1 INCREASED INTEGRATION INTO BROADER WIRED NETWORKS IN INDUSTRIAL IOT SETUPS TO DRIVE MARKET

- 11.3 WIRELESS

- 11.3.1 NEED FOR IMMEDIATE DETECTION AND REPORTING OF HAZARDOUS CONDITIONS IN CRITICAL INDUSTRIES DRIVING ADOPTION

12 GAS SENSOR MARKET, BY TECHNOLOGY

- 12.1 INTRODUCTION

- 12.2 ELECTROCHEMICAL

- 12.2.1 GROWTH OF HEALTHCARE SECTOR DRIVING DEMAND FOR ELECTROCHEMICAL GAS SENSORS

- 12.3 PHOTOIONIZATION DETECTION

- 12.3.1 HIGH DEMAND IN INDUSTRIAL ENVIRONMENTS FOR MONITORING VOCS TO DRIVE MARKET GROWTH

- 12.4 SOLID-STATE/METAL-OXIDE-SEMICONDUCTOR

- 12.4.1 GROWTH OF INDUSTRIAL, AUTOMOBILE, AND HEALTHCARE SECTORS TO FUEL MARKET GROWTH

- 12.5 CATALYTIC

- 12.5.1 USE IN AMMONIA AND METHANE GAS SENSORS FOR AUTOMOTIVE AND INDUSTRIAL SECTORS TO DRIVE GROWTH

- 12.6 INFRARED

- 12.6.1 DEMAND IN INDUSTRIAL AND INDOOR AIR QUALITY MONITORING APPLICATIONS TO SUPPORT MARKET GROWTH

- 12.6.1.1 Non-dispersive infrared (NDIR)

- 12.6.1.2 Tunable diode laser spectroscopy (TDLS)

- 12.6.1 DEMAND IN INDUSTRIAL AND INDOOR AIR QUALITY MONITORING APPLICATIONS TO SUPPORT MARKET GROWTH

- 12.7 LASER

- 12.7.1 INCREASING ADOPTION IN INDUSTRIAL, COMMERCIAL, AND DEFENSE APPLICATIONS TO DRIVE MARKET

- 12.8 ZIRCONIA

- 12.8.1 ADOPTION IN STEEL PRODUCTION, POWER PLANTS, BOILERS, AND FOOD INDUSTRY FOR OXYGEN MONITORING TO DRIVE MARKET

- 12.9 HOLOGRAPHIC

- 12.9.1 HOLOGRAPHIC GAS SENSORS COMMONLY USED FOR ENVIRONMENTAL MONITORING AND HEALTHCARE DIAGNOSTICS

- 12.10 OTHER TECHNOLOGIES

13 GAS SENSOR MARKET, BY TYPE

- 13.1 INTRODUCTION

- 13.2 OXYGEN

- 13.2.1 ADVANCEMENTS IN ANESTHESIA AND CRITICAL CARE FUELING DEMAND FOR PRECISE OXYGEN MONITORING

- 13.3 CARBON MONOXIDE

- 13.3.1 INCREASING AWARENESS OF INDOOR AIR POLLUTION TO DRIVE DEMAND

- 13.4 CARBON DIOXIDE

- 13.4.1 ENVIRONMENTAL REGULATIONS REQUIRING CO2 MONITORING IN INDUSTRIAL PROCESSES TO PROPEL MARKET GROWTH

- 13.5 AMMONIA

- 13.5.1 GROWTH OF SMART CITIES AND DEMAND IN INDUSTRIAL APPLICATIONS TO BOOST MARKET GROWTH

- 13.6 CHLORINE

- 13.6.1 DEMAND IN WATER & WASTEWATER TREATMENT PLANTS TO FUEL MARKET GROWTH

- 13.7 HYDROGEN SULFIDE

- 13.7.1 USE IN OIL & GAS, WATER & WASTEWATER TREATMENT, AND SEWER AND SANITATION APPLICATIONS TO DRIVE MARKET

- 13.8 NITROGEN OXIDE

- 13.8.1 GROWTH OF AUTOMOTIVE & TRANSPORTATION SECTOR TO INCREASE DEMAND

- 13.9 VOLATILE ORGANIC COMPOUNDS

- 13.9.1 HIGH DEMAND FOR VOC SENSORS IN DYES, PLASTICS, SOLVENTS, AND PAINTS MANUFACTURING TO BOOST MARKET GROWTH

- 13.10 METHANE

- 13.10.1 HIGH DEMAND IN MINING AND OIL & GAS INDUSTRIES TO BOOST MARKET GROWTH

- 13.11 HYDROCARBONS

- 13.11.1 INCREASING USE OF NATURAL GAS IN RESIDENTIAL, INDUSTRIAL, AND TRANSPORTATION APPLICATIONS DRIVING MARKET

- 13.12 HYDROGEN

- 13.12.1 SURGING DEMAND IN REFINERIES, PETROCHEMICAL PLANTS, AND CHEMICAL MANUFACTURING TO DRIVE MARKET

14 GAS SENSOR MARKET, BY END USE

- 14.1 INTRODUCTION

- 14.2 AUTOMOTIVE & TRANSPORTATION

- 14.2.1 INCREASED DEPLOYMENT OF PARTICULATE MATTER SENSORS TO ADDRESS POLLUTION IN VEHICLE CABINS TO DRIVE MARKET

- 14.3 SMART CITIES & BUILDING AUTOMATION

- 14.3.1 URBANIZATION AND RISING CONCERNS ABOUT HEALTH RISKS DUE TO POLLUTION TO DRIVE MARKET

- 14.4 OIL & GAS

- 14.4.1 INCREASING FOCUS ON METHANE EMISSION CONTROL AND SAFETY REGULATIONS TO FUEL DEMAND

- 14.5 WATER & WASTEWATER TREATMENT

- 14.5.1 GROWING AWARENESS OF GREENHOUSE GAS EMISSIONS AND SAFETY STANDARDS DRIVING MARKET

- 14.6 FOOD & BEVERAGES

- 14.6.1 USE OF CO2 IN FOOD PROCESSING AND STORAGE DRIVING DEMAND FOR GAS DETECTION SYSTEMS IN FOOD & BEVERAGE INDUSTRY

- 14.7 POWER STATIONS

- 14.7.1 RISING INTEGRATION OF HYDROGEN IN POWER GENERATION FUELS INCREASING DEMAND FOR ADVANCED GAS SENSORS

- 14.8 MEDICAL

- 14.8.1 DEMAND FOR WEARABLE HEALTHCARE DEVICES EQUIPPED WITH GAS SENSORS TO REVOLUTIONIZE REMOTE PATIENT MONITORING

- 14.9 METALS & CHEMICALS

- 14.9.1 HIGH DEMAND FOR ADVANCED GAS SENSORS TO MONITOR HAZARDOUS EMISSIONS TO DRIVE MARKET

- 14.10 MINING

- 14.10.1 INCREASED DEMAND FOR PORTABLE GAS SENSORS FOR DETECTING TOXIC GASES IN MINES TO BOOST MARKET

- 14.11 CONSUMER ELECTRONICS

- 14.11.1 ADVANCEMENTS IN SENSOR MINIATURIZATION AND SMART TECHNOLOGY TO ACCELERATE ADOPTION

- 14.12 GOVERNMENT & REGULATORY BODIES

- 14.12.1 INCREASINGLY STRINGENT REGULATIONS ON AIR QUALITY AND SAFETY STANDARDS TO BOOST MARKET GROWTH

15 GAS SENSOR MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 15.2.2 US

- 15.2.2.1 High demand in oil & gas and automotive sectors and presence of key players to drive market

- 15.2.3 CANADA

- 15.2.3.1 Growing investments in infrastructure development to drive market growth

- 15.2.4 MEXICO

- 15.2.4.1 Stringent regulations on industrial safety and air quality and adoption of advanced technologies to fuel market growth

- 15.3 EUROPE

- 15.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 15.3.2 UK

- 15.3.2.1 Stringent government regulations regarding environmental monitoring and emissions reduction to propel market growth

- 15.3.3 GERMANY

- 15.3.3.1 Strong automotive industry driving adoption of gas sensors in Germany

- 15.3.4 FRANCE

- 15.3.4.1 Investments in infrastructure development and presence of major automobile manufacturers to fuel market growth

- 15.3.5 ITALY

- 15.3.5.1 Rising demand in manufacturing sector to support market growth

- 15.3.6 REST OF EUROPE

- 15.4 ASIA PACIFIC

- 15.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 15.4.2 CHINA

- 15.4.2.1 Rapid industrialization and urbanization fueling demand for gas sensors

- 15.4.3 JAPAN

- 15.4.3.1 Adoption of innovative sensor technologies in various industries to curb air pollution to support market growth

- 15.4.4 INDIA

- 15.4.4.1 Government-led initiatives and investments in petrochemical sector to drive market

- 15.4.5 SOUTH KOREA

- 15.4.5.1 Increasing use of IoT-integrated sensors for real-time monitoring to boost demand

- 15.4.6 REST OF ASIA PACIFIC

- 15.5 REST OF THE WORLD (ROW)

- 15.5.1 MACROECONOMIC OUTLOOK FOR ROW

- 15.5.2 MIDDLE EAST & AFRICA

- 15.5.2.1 Rising oil & gas exploration activities to contribute to market growth

- 15.5.2.2 GCC countries

- 15.5.2.3 Rest of Middle East & Africa

- 15.5.3 SOUTH AMERICA

- 15.5.3.1 Growth in automotive, oil & gas, chemicals, and mining industries to drive demand

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 16.3 MARKET SHARE ANALYSIS, 2024

- 16.4 REVENUE ANALYSIS, 2020-2024

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS

- 16.6 BRAND/PRODUCT COMPARISON

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Gas type footprint

- 16.7.5.4 Connectivity footprint

- 16.7.5.5 End use footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023

- 16.8.5.1 Detailed list of key startups/SMEs

- 16.8.5.2 Competitive benchmarking of key startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

- 16.9.3 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 HONEYWELL INTERNATIONAL INC.

- 17.1.1.1 Business overview

- 17.1.1.2 Products/Solutions/Services offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.3.2 Other developments

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 MSA SAFETY INCORPORATED

- 17.1.2.1 Business overview

- 17.1.2.2 Products/Solutions/Services offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Deals

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 AMPHENOL CORPORATION

- 17.1.3.1 Business overview

- 17.1.3.2 Products/Solutions/Services offered

- 17.1.3.3 MnM view

- 17.1.3.3.1 Key strengths

- 17.1.3.3.2 Strategic choices

- 17.1.3.3.3 Weaknesses and competitive threats

- 17.1.4 SENSIRION AG

- 17.1.4.1 Business overview

- 17.1.4.2 Products/Solutions/Services offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches

- 17.1.4.3.2 Deals

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 AMS-OSRAM AG

- 17.1.5.1 Business overview

- 17.1.5.2 Products/Solutions/Services offered

- 17.1.5.3 MnM view

- 17.1.5.3.1 Key strengths

- 17.1.5.3.2 Strategic choices

- 17.1.5.3.3 Weaknesses and competitive threats

- 17.1.6 FIGARO ENGINEERING INC.

- 17.1.6.1 Business overview

- 17.1.6.2 Products/Solutions/Services offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches

- 17.1.6.3.2 Expansions

- 17.1.7 ALPHASENSE

- 17.1.7.1 Business overview

- 17.1.7.2 Products/Solutions/Services offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches

- 17.1.7.3.2 Deals

- 17.1.8 PROCESS SENSING TECHNOLOGIES

- 17.1.8.1 Business overview

- 17.1.8.2 Products/Solutions/Services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches

- 17.1.8.3.2 Deals

- 17.1.9 MEMBRAPOR

- 17.1.9.1 Business overview

- 17.1.9.2 Products/Solutions/Services offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product launches

- 17.1.10 SENSEAIR AB (ASAHI KASEI MICRODEVICES)

- 17.1.10.1 Business overview

- 17.1.10.2 Products/Solutions/Services offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches

- 17.1.11 NISSHA CO., LTD.

- 17.1.11.1 Business overview

- 17.1.11.2 Products/Solutions/Services offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Product launches

- 17.1.12 FUJI ELECTRIC CO., LTD.

- 17.1.12.1 Business overview

- 17.1.12.2 Products/Solutions/Services offered

- 17.1.13 RENESAS ELECTRONICS CORPORATION

- 17.1.13.1 Business overview

- 17.1.13.2 Products/Solutions/Services offered

- 17.1.14 DANFOSS

- 17.1.14.1 Business overview

- 17.1.14.2 Products/Solutions/Services offered

- 17.1.15 GASERA LTD.

- 17.1.15.1 Business overview

- 17.1.15.2 Products/Solutions/Services offered

- 17.1.16 INFINEON TECHNOLOGIES AG

- 17.1.16.1 Business overview

- 17.1.16.2 Products/Solutions/Services offered

- 17.1.16.3 Recent developments

- 17.1.16.3.1 Product launches

- 17.1.1 HONEYWELL INTERNATIONAL INC.

- 17.2 OTHER PLAYERS

- 17.2.1 NITERRA CO., LTD.

- 17.2.2 BREEZE TECHNOLOGIES

- 17.2.3 ELICHENS

- 17.2.4 BOSCH SENSORTEC GMBH

- 17.2.5 EDINBURGH SENSORS

- 17.2.6 GASTEC CORPORATION

- 17.2.7 NEMOTO & CO., LTD.

- 17.2.8 SPEC SENSORS

- 17.2.9 SIA MIPEX

- 17.2.10 CUBIC SENSOR AND INSTRUMENT CO., LTD.

- 17.2.11 WINSEN

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 List of key secondary sources

- 18.1.1.2 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 List of primary interview participants

- 18.1.2.2 Breakdown of primary interviews

- 18.1.2.3 Key industry insights

- 18.1.3 SECONDARY AND PRIMARY RESEARCH

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 BOTTOM-UP APPROACH

- 18.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 18.2.2 TOP-DOWN APPROACH

- 18.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 18.2.1 BOTTOM-UP APPROACH

- 18.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 18.4 RESEARCH ASSUMPTIONS

- 18.5 RISK ANALYSIS

- 18.6 RESEARCH LIMITATIONS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS