|

시장보고서

상품코드

1936066

푸시 풀 컨트롤 케이블 시장 : 제품 유형별, 산업별, 케이블 유형별, 용도별, 추진별, 지역별 - 세계 예측(-2032년)Push-Pull Control Cables Market by Product type (Throttle, Gear Shift, Clutch, Parking Brake, Others), Industry (Automotive, Construction, Agriculture, Railway, Marine, Others), Cable Type, Application, Propulsion, and Region - Global forecast to 2032 |

||||||

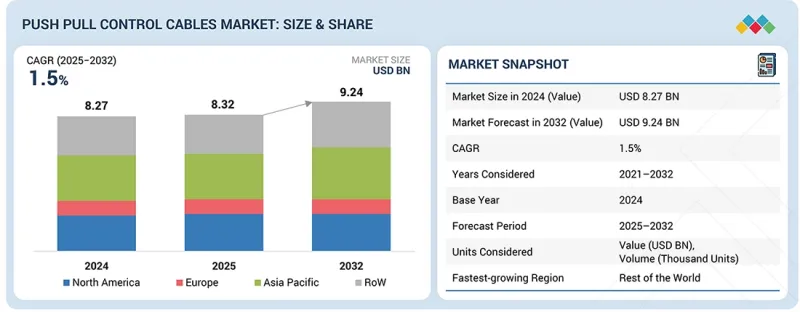

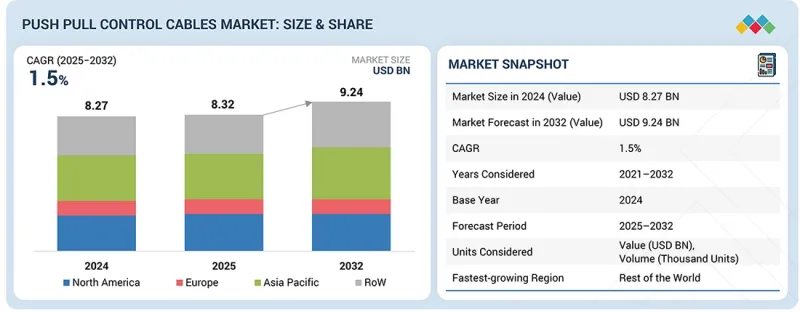

세계의 푸시 풀 컨트롤 케이블 시장 규모는 2025년 83억 2,000만 달러에서 2032년까지 92억 4,000만 달러에 달할 것으로 예측되며, CAGR로 1.5%의 성장이 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2032년 |

| 단위 | 1,000개, 100만 달러 |

| 부문 | 제품, 용도, 케이블 유형, 차종, 산업 |

| 대상 지역 | 아시아태평양, 북미, 유럽, 기타 지역 |

시장 성장은 소형차, 상용차, 전기자동차의 생산 증가와 더불어 저렴한 가격과 긴 수명의 작동 시스템에 대한 수요 증가에 의해 촉진되고 있습니다. 스로틀, 클러치, 브레이크, HVAC, 변속기 등의 차량 기능에는 신뢰할 수 있는 기계식 제어가 필요하며, 이는 푸시 풀 컨트롤 케이블 세계 시장을 견인하고 있습니다.

아시아태평양은 푸시 풀 컨트롤 케이블의 가장 빠른 성장이 예상되는 시장입니다. 중국, 한국, 일본에서의 수요 증가가 이를 촉진하고 있으며, 이들 국가의 높은 자동차 생산량과 확대되는 전기자동차 생산은 많은 수의 푸시 풀 컨트롤 케이블을 필요로 하고 있습니다. 또한, 이 지역에서는 선박, 철도, 농업, 건설기계에 채용되면서 수요가 증가하고 있습니다. 이러한 분야에서는 정밀하고 내구성이 뛰어나며 열악한 작업 환경에서 유용하게 작동할 수 있어야 합니다.

"산업별로는 자동차 부문이 예측 기간 동안 가장 큰 시장 규모를 차지할 것으로 예상됩니다."

예측 기간 동안 자동차 부문이 가장 큰 시장 규모를 차지할 것으로 예상됩니다. 이는 승용차, 소형 상용차, 대형 상용차에서 푸시 풀 컨트롤 케이블의 사용이 증가했기 때문입니다. 이러한 성장은 신뢰할 수 있고 비용 효율적인 작동 메커니즘으로서 신흥 시장에서 기계식 케이블의 채택이 확대되고 있기 때문인 것으로 분석됩니다. 기계식 작동 케이블은 비용 효율성, 컴팩트한 배선, 신뢰성 때문에 중급 및 고급 승용차에 탑재되는 크루즈 컨트롤/어댑티브 크루즈 컨트롤(ACC) 시스템에 널리 사용되고 있습니다. 또한, 듀얼 존 및 멀티 존 HVAC 시스템으로의 전환으로 인해 HVAC 제어 케이블에 대한 수요가 증가하고 있으며, 블렌딩 도어 및 공기 분배 플랩의 정밀한 작동을 가능하게 합니다. 전기자동차에서도 기계식 케이블은 주차 브레이크, HVAC, 차체, 열 관리 애플리케이션에서 여전히 중요한 역할을 담당하고 있습니다. 또한, 크루즈 컨트롤 및 첨단 HVAC 시스템과 같은 새로운 성장 분야와 더불어, 핵심 자동차 애플리케이션은 여전히 기계식 작동 메커니즘에 의존하고 있습니다. 이러한 모든 요인들이 자동차 부문에서 푸시 풀 컨트롤 케이블에 대한 수요를 촉진하고 있습니다.

"제품별로는 기어 시프트 케이블 부문이 2025년 2위 부문이 될 것으로 추정됩니다."

기어 시프트 케이블 부문은 특히 아시아 국가와 같은 신흥 시장에서 수동 변속기와 AMT 변속기에서 중요한 역할을 하고 있기 때문에 2025년에는 2위를 차지할 것으로 예상됩니다. 기계식 케이블은 비용 효율성이 뛰어나며, 진동이 심한 가혹한 작동 환경에서도 견고성, 신뢰성, 수리 용이성 때문에 전자식 시프터보다 선호되고 있습니다. 푸시-풀 구조는 정밀한 힘 전달, 유연한 배선, 최소한의 백래시를 실현하여 운전자의 변속감을 향상시킵니다. 또한, 라이프사이클 비용이 낮기 때문에 경제성과 내구성이 중요한 중저가 차량 유형에서 특히 매력적일 수 있습니다.

시프트 셀렉터 케이블은 전기자동차에서 제한적이지만 전략적으로 보급되고 있습니다. 대부분의 EV가 완전 전자식 변속 시스템을 채택하고 있는 반면, 일부 하이브리드 차량과 마일드 하이브리드 EV는 비용 효율성과 작동 신뢰성을 위해 수동 또는 AMT 기어박스를 유지하고 있습니다. 또한, 이러한 케이블은 정밀한 설계, 고품질 소재, 복잡한 배선 경로, 더 엄격한 내구성 표준으로 인해 일반적으로 표준 푸시 풀 컨트롤 케이블보다 더 비쌉니다.

오프로드 차량에서는 건설기계와 광산기계가 기어 변속 케이블의 주요 시장입니다. 이는 굴착기, 로더, 불도저, 굴절식 덤프트럭, 굴절식 덤프트럭의 생산량 증가에 따른 것입니다. 이 케이블은 변속기의 범위 선택과 전진, 중립, 후진 작동을 지원하며, 먼지가 많은 환경, 고충격 환경, 고온 환경에서도 신뢰할 수 있는 기계적인 힘 전달을 실현합니다. 또한, 고부하 작업에서는 안전성, 예측 가능한 응답성, 전자 장비에 대한 의존도가 낮다는 점에서 기계식 케이블 기반 시스템이 여전히 우선적으로 선택되고 있습니다. 또한, 지속적인 인프라 투자, 광업의 확장, 변속기의 복잡성 증가로 푸시풀 제어 케이블에 대한 지속적인 수요가 예상됩니다.

세계의 푸시 풀 컨트롤 케이블(Push-Pull Control Cable) 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대한 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 푸시 풀 컨트롤 케이블 시장 : 제품 유형별

제10장 푸시 풀 컨트롤 케이블 시장 : 용도별

제11장 푸시 풀 컨트롤 케이블 시장 : 산업별

제12장 푸시 풀 컨트롤 케이블 시장 : 케이블 유형별

제13장 푸시 풀 컨트롤 케이블 시장 : 차종별

제14장 자동차용 푸시 풀 컨트롤 케이블 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSM 26.03.05The push-pull control cables market is projected to grow from USD 8.32 billion in 2025 to reach USD 9.24 billion by 2032, at a CAGR of 1.5%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Volume (Thousand Units) and Value (USD Million) |

| Segments | Product, Application, Cable Type, Vehicle Type, Industry |

| Regions covered | Asia Pacific, North America, Europe, and the Rest of the World (RoW) |

The growth of the market is driven by the increasing production of light, commercial, and electric vehicles, along with the rising demand for affordable and long-lasting actuation systems. Vehicle functions, such as throttle, clutch, brake, HVAC, and transmission, require reliable mechanical controls, which is also driving the global market for push-pull control cables.

Asia Pacific is projected to be the fastest-growing market for push-pull control cables, driven by their rising demand in China, South Korea, and Japan, where high vehicle production and expanding EV manufacturing require substantial push-pull control cables. Additionally, push-pull control cables are experiencing an increasing demand in the region due to their adoption in marine, railway, agricultural, and construction equipment, where they are required for precise, durable, and easily serviceable operation in demanding working conditions.

"By industry, the automotive segment is projected to account for the largest market during the forecast period."

The automotive segment is projected to be the largest market during the forecast period, due to the increasing use of push-pull control cables in passenger cars, light commercial vehicles, and heavy commercial vehicles. This growth can also be attributed to the rising adoption of mechanical cables in emerging markets for reliable and cost-effective actuation. Mechanical actuation cables are widely used in cruise control and adaptive cruise control (ACC) systems deployed in mid- to high-end passenger vehicles, for their cost efficiency, compact routing, and reliability. Additionally, the shift toward double-zone and multi-zone HVAC systems is generating incremental demand for HVAC control cables, enabling the precise actuation of blend doors and air distribution flaps. In electric vehicles, mechanical cables remain relevant across parking brake, HVAC, body, and thermal management applications. Moreover, core automotive applications continue to rely on mechanical actuation, alongside newer growth areas, such as cruise control and advanced HVAC systems. All these factors are driving the demand for push-pull control cables in the automotive segment.

"By product, the gear shift cable segment is estimated to be the second-largest segment in 2025."

The gear shift cables segment is estimated to be the second-largest segment in 2025, owing to their critical role in manual and AMT transmissions, particularly in emerging markets, such as Asian countries. Mechanical cables are cost-effective and preferred over electronic shifters because of their robustness, reliability, and ease of repair in high-vibration and harsh operating conditions. The push-pull designs enable precise force transmission, flexible routing, and minimal backlash, improving shift feel for drivers. Also, their lower lifecycle cost makes them especially attractive for low- to mid-segment vehicles where affordability and durability are critical.

Shift selector cables have limited but strategic penetration in electric cars. While most EVs use fully electronic shift-by-wire systems, some hybrid and mild-hybrid EVs retain manual or AMT-style gearboxes for cost efficiency and operational reliability. Moreover, these cables are generally more expensive than standard push-pull control cables due to their precision engineering, high-quality materials, complex routing, and stricter durability standards.

Within off-highway vehicles, construction and mining equipment is a significant market for gear shift cables, due to the rising production of excavators, loaders, dozers, and articulated dump trucks. These cables support transmission range selection and forward-neutral-reverse actuation, delivering reliable mechanical force transfer in dusty, high-shock, and high-temperature conditions. Additionally, mechanical cable-based systems remain the preferred choice due to their safety, predictable response, and low reliance on electronics in heavy-duty operations. Moreover, continued infrastructure spending, mining expansion, and more complex transmissions are expected to drive sustained demand for push-pull control cables.

"North America is projected to be the second-largest market during the forecast period."

North America is projected to be the second-largest market for push-pull control cables during the forecast period. The growth of this regional market is driven by growth in the automotive, construction, railway, marine, and agricultural industries. The growth is propelling the adoption of push-pull control cables in throttle, transmission, clutch, parking brake, and HVAC applications across ICE, hybrid, and cost-oriented EV vehicles. The growth of this regional market is also driven by sustained production of pick-up trucks, SUVs, and heavy commercial vehicles that continue to use cost-efficient, validated mechanical and hybrid actuation, alongside infrastructure-led construction activity, railway fleet upgrades, and steady demand for marine and agricultural equipment.

In North America, construction and off-highway systems are also generating a stable demand for high-load push-pull and pull-only cables used in excavators, loaders, and lifting machinery. Likewise, railway applications rely on mechanical cables for brake actuation, door control, and auxiliary systems that require low backlash and long service life. Similarly, marine and agricultural equipment require corrosion-resistant, long-stroke cables designed to operate in environments exposed to moisture, dust, and vibration. All these factors are driving growth in North America. Major players in the North America push-pull control cables market include Orscheln Products, Cablecraft, Grand Rapids Controls, Bergen Cable Technology, Conwire, and American Cable & Harness.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and strategy directors, and executives from various key organizations operating in the push-pull control cables market.

- By Company Type: Push-pull Control Cable Manufacturers - 54%, OEMs - 38%, and Others - 8%

- By Designation: C-Level - 30%, Directors - 35%, and Other Designations - 35%

- By Region: Asia Pacific - 55%, Europe - 15%, North America - 20%, and Europe - 10%

Research Coverage

The study segments the push-pull control cables market based on Product (Throttle Cable, Gear Shift Cable, Clutch Cable, Parking Brake Cable, Hood Release Cable, Fuel Door Release Cable, Trunk Release Cable, Door Latch Cable, Spare Wheel Carrier Cable, Seat Recline Release Cable), Cable Type (Push Pull Cable, Pull-only Cable), Application (Engine Cable, Transmission Cable, Brake Cable, Auxiliary Cable), Vehicle Type (Passenger Car, Light Commercial Vehicle, Heavy Commercial Vehicle), Industry (Automotive, Marine, Construction, Agriculture, Railways, Others), and Region (Asia Pacific, North America, Europe, Rest of the World).

The study includes an in-depth competitive analysis of the significant mechanical control cable manufacturers, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall push-pull control cables market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report will also help stakeholders understand the market pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

- Analysis of key drivers (Growth in construction and agriculture equipment with heavy-duty control cables, push toward compact packaging across marine, automotive, and industrial OEMs), restraints (Increasing autonomy across industries driving e-actuation systems), opportunities (Expansion in EV auxiliary functions, growth in marine craft manufacturing), and challenges (Durability and performance stability under severe conditions)

- Product Development/Innovation: Detailed insights into upcoming technologies and research & development activities in the push-pull control cables market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the push-pull control cables market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and product offerings of leading players, such as HI-LEX Corporation (Japan), Suprajit (India), Orscheln Products (US), Kongsberg Automotive (Norway), and Carl Stahl Technocables GmbH (Germany), in the push-pull control cables market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNIT CONSIDERED

- 1.7 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN PUSH-PULL CONTROL CABLES MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PUSH-PULL CONTROL CABLES MARKET

- 3.2 PUSH-PULL CONTROL CABLES MARKET, BY INDUSTRY

- 3.3 PUSH-PULL CONTROL CABLES MARKET, BY CABLE TYPE

- 3.4 PUSH-PULL CONTROL CABLES MARKET, BY PRODUCT TYPE

- 3.5 PUSH-PULL CONTROL CABLES MARKET , BY APPLICATION

- 3.6 PUSH-PULL CONTROL CABLES MARKET, BY VEHICLE TYPE

- 3.7 PUSH-PULL CONTROL CABLES MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing adoption of construction and agricultural equipment

- 4.2.1.2 Push toward compact packaging across marine, automotive, and industrial OEMs

- 4.2.2 RESTRAINTS

- 4.2.2.1 Increasing autonomy across industries

- 4.2.3 OPPORTUNITY

- 4.2.3.1 Expansion in EV auxiliary functions

- 4.2.3.2 Growth in marine craft manufacturing

- 4.2.4 CHALLENGES

- 4.2.4.1 Durability and performance stability under severe operating conditions

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1, 2, 3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.2.1 Regional GDP dynamics

- 5.1.2.1.1 Developed markets (US, EU, and Japan)

- 5.1.2.1.2 Emerging markets (China, India, and Southeast Asia)

- 5.1.2.2 Investment environment

- 5.1.2.1 Regional GDP dynamics

- 5.1.3 TRENDS IN PUSH-PULL CONTROL CABLES MARKET

- 5.1.3.1 Powertrain transition and market dynamics

- 5.1.3.2 Growth in off-highway and industrial equipment

- 5.2 ECOSYSTEM ANALYSIS

- 5.2.1 RAW MATERIAL SUPPLIERS

- 5.2.2 MECHANICAL CONTROL CABLE MANUFACTURERS

- 5.2.3 TIER 1 SUPPLIERS

- 5.2.4 OEMS

- 5.3 PRICING ANALYSIS

- 5.3.1 AVERAGE SELLING PRICE OF MECHANICAL CONTROL CABLES, BY VEHICLE TYPE

- 5.3.2 AVERAGE SELLING PRICE OF MECHANICAL CONTROL CABLES, BY REGION

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 CASE STUDY ANALYSIS

- 5.5.1 SUPRAJIT IMPLEMENTED DASSAULT SYSTEMES' 3DEXPERIENCE PLATFORM TO IMPROVE PRODUCT DEVELOPMENT EFFICIENCY AND CUSTOMIZATION

- 5.5.2 MECHANICAL CONTROL CABLE-BASED LATCH ACTUATION SYSTEM ENGINEERED TO ENSURE CONSISTENT DOOR LATCH RETENTION DURING CRASH

- 5.5.3 CHATTARPATI AUTOMOTIVE SYSTEMS PROVIDED HIGH-QUALITY GEAR LEVER CABLES DESIGNED FOR DURABILITY AND RELIABLE PERFORMANCE

- 5.6 KEY CONFERENCES & EVENTS

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 IMPACT OF US 2025 TARIFFS

- 5.8.1 INTRODUCTION

- 5.8.2 KEY TARIFF RATES

- 5.8.3 PRICE IMPACT ANALYSIS

- 5.8.4 IMPACT ON COUNTRY/REGION

- 5.8.4.1 US

- 5.8.4.2 Europe

- 5.8.4.3 Asia Pacific

- 5.8.5 IMPACT ON END-USE INDUSTRIES

- 5.8.5.1 Automotive

- 5.8.5.2 Off-highway (Construction & agriculture)

- 5.8.5.3 Marine

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ADVANCED WIRE MATERIAL ENGINEERING AND SURFACE TREATMENT

- 6.1.2 LOW-FRICTION LINER AND LUBRICATION TECHNOLOGIES

- 6.1.3 AUTOMATED MANUFACTURING AND IN-LINE QUALITY CONTROL

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 SENSOR-ENABLED MONITORING AND POSITION FEEDBACK

- 6.2.2 HYBRID MECHANICAL-ELECTRONIC ACTUATION SYSTEMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 ELECTRONIC ACTUATION AND DRIVE-BY-WIRE SUBSYSTEMS

- 6.3.2 ELECTRIC MOTORS AND LINEAR ACTUATORS

- 6.4 IMPACT OF AI/GEN AI

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.4.2 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.4.3 CLIENTS' READINESS TO ADOPT GEN AI IN PUSH-PULL CONTROL CABLES MARKET

- 6.5 TRADE ANALYSIS

- 6.5.1 IMPORT DATA (HS CODE 848790)

- 6.5.2 EXPORT DATA (HS CODE 848790)

- 6.6 PATENT ANALYSIS

- 6.7 FUTURE APPLICATIONS

- 6.7.1 FAIL-SAFE AND REDUNDANT ACTUATION IN ELECTRIFIED VEHICLES

- 6.7.2 HYBRID MECHANICAL-ELECTRONIC CONTROL SYSTEMS

7 REGULATORY LANDSCAPE

- 7.1 REGULATORY FRAMEWORK

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2 PUSH-PULL CONTROL CABLES MARKET: COUNTRY-WISE REGULATIONS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 KEY STAKEHOLDERS & BUYING CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS, BY CABLE TYPE

- 8.3.2 BUYING CRITERIA

9 PUSH-PULL CONTROL CABLES MARKET, BY PRODUCT TYPE

- 9.1 INTRODUCTION

- 9.2 THROTTLE CABLE

- 9.2.1 FOCUS ON COST EFFICIENCY, MECHANICAL RELIABILITY, AND FUEL-SYSTEM COMPATIBILITY TO DRIVE MARKET

- 9.3 GEAR SHIFT CABLE

- 9.3.1 EMPHASIS ON MANUAL TRANSMISSION PENETRATION, PACKAGING FLEXIBILITY, AND SERVICE SIMPLICITY TO DRIVE MARKET

- 9.4 CLUTCH CABLE

- 9.4.1 DEMAND FOR CABLES WITH LOW MAINTENANCE COST TO DRIVE MARKET

- 9.5 PARKING BRAKE CABLE

- 9.5.1 WIDESPREAD ADOPTION OF CONTROL CABLES IN NON-ELECTRONIC BRAKE SYSTEMS TO DRIVE MARKET

- 9.6 HOOD RELEASE CABLE

- 9.6.1 NEED FOR SAFETY ACCESS REQUIREMENTS, ROUTINE SERVICE FREQUENCY, AND UNIVERSAL FITMENT TO BOOST MARKET

- 9.7 FUEL LID CABLE

- 9.7.1 FOCUS ON CENTRALIZING CABIN CONTROL AND ENSURING THEFT PREVENTION TO DRIVE MARKET

- 9.8 TRUNK RELEASE CABLE

- 9.8.1 EMPHASIS ON ENHANCING USER CONVENIENCE TO DRIVE DEMAND FOR TRUNK RELEASE CABLES

- 9.9 DOOR LATCH CABLE

- 9.9.1 STRINGENT OCCUPANT SAFETY REGULATIONS AND HIGH-CYCLE DURABILITY REQUIREMENTS TO DRIVE MARKET

- 9.10 SPARE WHEEL CARRIER CABLE

- 9.10.1 FOCUS ON SPACE OPTIMIZATION AND EASE OF ROADSIDE ACCESS TO DRIVE MARKET

- 9.11 SEAT RECLINER RELEASE CABLE

- 9.11.1 INCREASING DEMAND FOR ENHANCED VEHICLE CONTROL TO DRIVE MARKET

10 PUSH-PULL CONTROL CABLES MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 ENGINE

- 10.2.1 FOCUS ON ENHANCING RELIABILITY, DURABILITY, AND COST-EFFICIENCY OF VEHICLES TO DRIVE MARKET

- 10.3 TRANSMISSION

- 10.3.1 NEED FOR ENHANCING PRECISION, FLEXIBILITY, AND DURABILITY IN CARS TO SUPPORT GROWTH

- 10.4 BRAKE

- 10.4.1 EMPHASIS ON IMPROVING VEHICLE SAFETY, STRENGTH, AND RELIABILITY TO DRIVE MARKET

- 10.5 AUXILIARY

- 10.5.1 NEED FOR DURABILITY, CONVENIENCE, AND ROBUSTNESS IN VEHICLES TO DRIVE MARKET

11 PUSH-PULL CONTROL CABLES MARKET, BY INDUSTRY

- 11.1 INTRODUCTION

- 11.2 AUTOMOTIVE

- 11.2.1 RISING USE OF COMMERCIAL VEHICLES AND HIGH MECHANICAL ACTUATION TO SUPPORT GROWTH

- 11.3 CONSTRUCTION

- 11.3.1 RAPID INFRASTRUCTURE DEVELOPMENT, INDUSTRIALIZATION, AND DEMAND FOR HIGH CONSTRUCTION EQUIPMENT TO SUPPORT MARKET

- 11.3.2 EXCAVATORS

- 11.3.3 MINI EXCAVATORS

- 11.3.4 BACKHOE LOADERS

- 11.3.5 DOZERS

- 11.3.6 ROAD ROLLERS

- 11.3.7 COMPACTORS

- 11.3.8 DUMP TRUCKS

- 11.3.9 MOTOR GRADERS

- 11.4 AGRICULTURE

- 11.4.1 INCREASING USE OF MECHANICAL CABLES IN LIFTING IMPLEMENTS TO DRIVE MARKET

- 11.4.2 TRACTORS

- 11.4.2.1 < 30 hp

- 11.4.2.2 31-70 hp

- 11.4.2.3 71-130 hp

- 11.4.2.4 131-250 hp

- 11.4.2.5 > 250 hp

- 11.4.3 SPRAYERS

- 11.4.4 BALERS

- 11.4.5 HARVESTERS

- 11.5 MARINE

- 11.5.1 LARGE-SCALE PRODUCTION OF FISHING BOATS TO DRIVE MARKET

- 11.5.2 RECREATIONAL BOAT MARKET (INBOARD VS. OUTBOARD)

- 11.5.3 MARINE STEERING

- 11.6 RAILWAY

- 11.6.1 FOCUS ON RAILWAY NETWORK EXPANSION AND FLEET MODERNIZATION TO DRIVE MARKET

- 11.7 OTHERS

12 PUSH-PULL CONTROL CABLES MARKET, BY CABLE TYPE

- 12.1 INTRODUCTION

- 12.2 PUSH-PULL CABLE

- 12.2.1 NEED FOR ENHANCING PREDICTABLE MECHANICAL RESPONSE AND DURABILITY OF ICE VEHICLES TO DRIVE MARKET

- 12.3 PULL-ONLY CABLE

- 12.3.1 NEED FOR CABLES WITH UNIDIRECTIONAL SAFETY FUNCTIONS AND PACKAGING SIMPLICITY TO DRIVE MARKET

13 PUSH-PULL CONTROL CABLES MARKET, BY VEHICLE TYPE

- 13.1 INTRODUCTION

- 13.2 PASSENGER CAR

- 13.2.1 RISING DEMAND FOR MECHANICAL RELIABILITY AND SELECTIVE RETENTION OF CABLES IN ICE AND ELECTRIC VEHICLES TO DRIVE MARKET

- 13.2.2 ICE

- 13.2.3 EV

- 13.3 LIGHT COMMERCIAL VEHICLE

- 13.3.1 FOCUS ON ENHANCING MECHANICAL ROBUSTNESS AND EASE OF FIELD SERVICE IN LCVS TO DRIVE MARKET

- 13.4 HEAVY COMMERCIAL VEHICLE

- 13.4.1 HEAVY-DUTY OPERATION REQUIREMENTS TO ENCOURAGE USE OF MECHANICAL CONTROL CABLES

14 AUTOMOTIVE PUSH-PULL CONTROL CABLES MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 ASIA PACIFIC

- 14.2.1 CHINA

- 14.2.1.1 Need for localization of auxiliary cables to drive market

- 14.2.2 JAPAN

- 14.2.2.1 High durability requirements in auxiliary cables to drive market

- 14.2.3 INDIA

- 14.2.3.1 High penetration of manual transmission in passenger cars to drive market

- 14.2.4 SOUTH KOREA

- 14.2.4.1 Focus on mandatory fitment across vehicle classes to drive market

- 14.2.5 THAILAND

- 14.2.5.1 High fleet utilization in urban and industrial centers to support market

- 14.2.6 INDONESIA

- 14.2.6.1 Rapid adoption of control cables in locally assembled vehicles to drive market

- 14.2.7 REST OF ASIA PACIFIC

- 14.2.1 CHINA

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 High production volume of passenger cars to support market growth

- 14.3.2 FRANCE

- 14.3.2.1 Increased demand for small and mid-size ICE passenger cars to drive market

- 14.3.3 UK

- 14.3.3.1 High demand for body-related mechanical control cables in passenger cars to drive market

- 14.3.4 ITALY

- 14.3.4.1 Rising vehicle production and aging fleets to drive market

- 14.3.5 SPAIN

- 14.3.5.1 Increase in export of ICE vehicles to drive market

- 14.3.6 RUSSIA

- 14.3.6.1 Country's reliance on long-haul transportation to drive market

- 14.3.7 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 NORTH AMERICA

- 14.4.1 US

- 14.4.1.1 Residual ICE passenger car production to drive market

- 14.4.2 CANADA

- 14.4.2.1 Growth in demand for light commercial vehicles and longer vehicle lifecycles to drive market

- 14.4.3 MEXICO

- 14.4.3.1 Expansion of automotive manufacturing sector to drive market

- 14.4.1 US

- 14.5 REST OF THE WORLD

- 14.5.1 SOUTH AFRICA

- 14.5.1.1 Low EV penetration and local assembly of vehicles to drive market

- 14.5.2 SAUDI ARABIA

- 14.5.2.1 Continued use of mechanical control cables in ICE-based vehicles to drive market

- 14.5.3 EGYPT

- 14.5.3.1 Rapid growth in locally assembled and imported ICE vehicles to support growth

- 14.5.4 OTHERS

- 14.5.1 SOUTH AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN,

- 15.3 MARKET SHARE ANALYSIS, 2024

- 15.4 REVENUE ANALYSIS OF TOP LISTED/PUBLIC PLAYERS

- 15.5 COMPANY VALUATION AND FINANCIAL METRICS

- 15.5.1 COMPANY VALUATION

- 15.5.2 FINANCIAL METRICS

- 15.6 BRAND/PRODUCT COMPARISON

- 15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS

- 15.7.1 STARS

- 15.7.2 EMERGING LEADERS

- 15.7.3 PERVASIVE PLAYERS

- 15.7.4 PARTICIPANTS

- 15.7.5 COMPANY FOOTPRINT

- 15.8 COMPANY EVALUATION MATRIX: REGIONAL PLAYERS, 2024

- 15.8.1 PROGRESSIVE COMPANIES

- 15.8.2 RESPONSIVE COMPANIES

- 15.8.3 DYNAMIC COMPANIES

- 15.8.4 STARTING BLOCKS

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 15.9.2 DEALS

- 15.9.3 EXPANSION

- 15.9.4 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 HI-LEX CORPORATION

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches/developments

- 16.1.1.3.2 Deals

- 16.1.1.3.3 Expansion

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 SUPRAJIT

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches/developments

- 16.1.2.3.2 Deals

- 16.1.2.3.3 Expansion

- 16.1.2.3.4 Other developments

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 ORSCHELN PRODUCTS

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 KONGSBERG AUTOMOTIVE

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches/developments

- 16.1.4.3.2 Other developments

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 CARL STAHL TECHNOCABLES GMBH

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product launches/developments

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 CABLECRAFT MOTION CONTROLS

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches/developments

- 16.1.6.3.2 Deals

- 16.1.6.3.3 Other developments

- 16.1.7 DIPLOMA PLC

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Deals

- 16.1.8 REMSONS INDUSTRIES LIMITED

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches/developments

- 16.1.8.3.2 Deals

- 16.1.9 SILA GROUP

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.10 LEGGETT & PLATT, INCORPORATED

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.11 DURA-SHILOH

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.1 HI-LEX CORPORATION

- 16.2 OTHER PLAYERS

- 16.2.1 STORK GROUP

- 16.2.2 SILCO AUTOMOTIVE SOLUTIONS LLP

- 16.2.3 KRAMAR CONTROLS GMBH

- 16.2.4 KUSTER HOLDING GMBH

- 16.2.5 VENHILL

- 16.2.6 FICOSA INTERNACIONAL SA

- 16.2.7 PIONEER AUTOMOTIVE INDUSTRIES

- 16.2.8 ELLIOTT MANUFACTURING

- 16.2.9 DRALLIM INDUSTRIES LIMITED

- 16.2.10 CALIFORNIA PUSH-PULL, INC.

- 16.2.11 GRAND RAPIDS CONTROLS, LLC

- 16.2.12 HINDLE CONTROLS

- 16.2.13 THAI STEEL CABLE PUBLIC COMPANY LIMITED

- 16.2.14 WR CONTROL GROUP AG

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 List of secondary sources

- 17.1.1.2 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Primary interviewees from demand and supply sides

- 17.1.2.2 Key primary insights

- 17.1.2.3 Breakdown of primary interviews

- 17.1.2.4 List of primary participants

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.3 DATA TRIANGULATION

- 17.4 FACTOR ANALYSIS

- 17.5 RESEARCH ASSUMPTIONS AND RISK ASSESSMENT

- 17.6 RESEARCH LIMITATIONS

18 APPENDIX

- 18.1 INSIGHTS FROM INDUSTRY EXPERTS

- 18.2 DISCUSSION GUIDE

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.6 AUTHOR DETAILS