|

시장보고서

상품코드

1936068

EV 충전기용 전자 포팅 컴파운드 시장 : 충전기 유형별(AC, DC), 설치 유형별(벽걸이, 고정), 재료 유형별(폴리우레탄, 실리콘, 에폭시), 경화 기술별, 용도별, EV 부품별, 지역별 - 세계 예측(-2032년)Electronic Potting Compound Market for EV charger, By Charger Type (AC, DC), Setup Type (Wall Mount, Stationary), Material Type (Polyurethane, Silicone, Epoxy), Curing Technology, Application, EV Component, and Region - Global Forecast to 2032 |

||||||

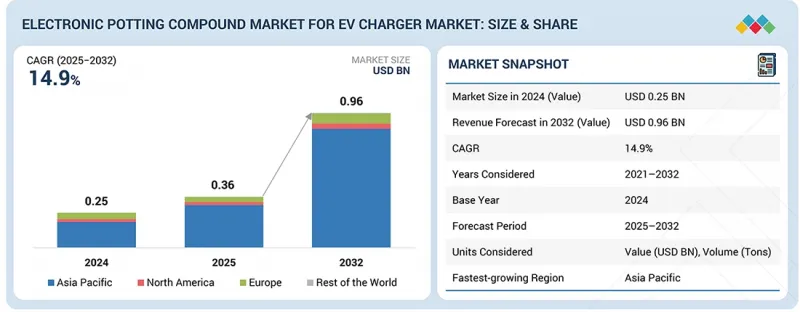

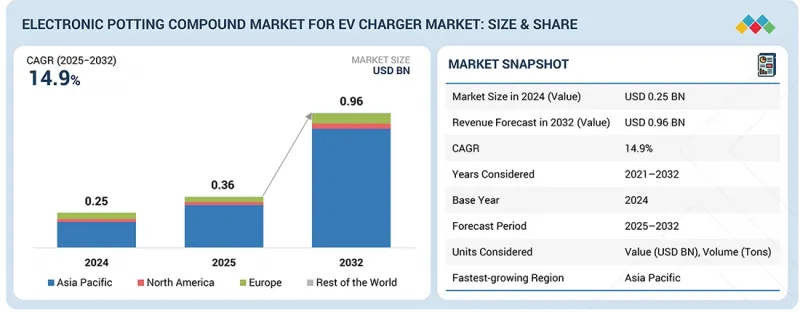

EV 충전기용 전자 포팅 컴파운드 시장 규모는 2025년 3억 6,000만 달러에서 2032년까지 9억 6,000만 달러에 달할 것으로 예측되며, CAGR은 14.9%로 전망됩니다.

AC 충전기의 경우, 컴팩트하고 통합된 전원 및 제어 기판의 채택이 증가하고 있으며, 이는 방열 성능의 저하 없이 완벽한 커버링을 보장하는 저점도 포팅 컴파운드에 대한 수요를 주도하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2032년 |

| 단위 | 금액(달러) , 톤 |

| 부문 | 충전기 유형, 설치 유형, 재료 유형, 경화 기술, EV 부품, 용도 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 기타 지역 |

DC 충전기의 경우, 초급속 충전으로의 전환에 따라 높은 열전도율과 높은 부분방전 저항성을 갖춘 포팅 소재에 대한 수요가 증가하고 있습니다. 또한, DC 충전기의 설계는 액체 냉각 및 밀폐형 전원 모듈로 전환되어 포팅의 두께와 재료 소비가 증가하고 있습니다. 두 충전기 유형 모두 자동 디스펜싱과의 호환성과 빠른 열경화성이 재료의 중요한 요구사항이 되고 있습니다. 또한, 실외 충전기 설치가 확대됨에 따라 장기적인 습기 침투 저항과 전기적 트래킹 저항을 갖춘 소재의 중요성이 커지고 있습니다.

"충전기 유형별로는 DC 충전기가 예측 기간 동안 시장을 주도할 것으로 예상됩니다."

DC 충전기는 AC 충전기나 차량용 충전기에 비해 전력 밀도와 작동 스트레스가 현저히 높기 때문에 예측 기간 동안 시장을 주도할 것으로 예상됩니다. 공공 DC 충전 시설과 차량기지들은 습기, 진동, 연속 운전 사이클에 노출되는 열악한 환경에서 운영되기 때문에 전기 절연성, 환경 보호, 진동 흡수성을 보장하는 견고한 밀봉재에 대한 요구가 증가하고 있습니다. OEM 및 충전 네트워크 사업자의 대규모 인프라 구축은 고속도로, 상업시설, 차량기지 내 고출력 DC 설비 설치가 우선시되고 있으며, 포팅재 사용량이 많은 충전 플랫폼에 수요가 집중되고 있습니다.

Parker Hannifin과 같은 재료 공급업체는 고출력 DC 모듈 내부의 좁은 틈새를 채우고, 인클로저 및 방열판으로 열을 효율적으로 전달할 수 있는 저점도, 속유동성 열전도성 포팅 컴파운드로 대응하고 있습니다. 또한, 보다 빠른 경화와 인라인 품질 관리를 실현하는 직접 주입식 및 주입식 시스템이 고처리량 생산을 지원하기 위해 주목받고 있습니다.

동시에 미국의 NEVI(National Electric Vehicle Infrastructure) 이니셔티브, 중국의 초고속 공공 충전 회랑의 지속적인 확장 등 정부 주도의 프로그램이 진행 중이며, 고출력 DC 충전기 도입이 가속화되고 있습니다. 예를 들어, 2025년 8월 캘리포니아 주 에너지 위원회는 5,500만 달러 규모의 Fast Charge California Program을 시작하여 기업 시설 및 공공 시설에 고출력 DC 스테이션을 포함한 공공 급속 충전기 설치를 지원했습니다. 이러한 투자로 인해 열적 내구성과 전기적 신뢰성을 겸비한 포팅 컴파운드에 대한 수요가 증가하고 있습니다. 새로운 고출력 DC 설비의 설치는 장기적인 작동 안정성과 규정 준수를 보장하기 위해 많은 양의 밀봉 재료가 필요하기 때문입니다.

"재료 유형별로는 에폭시 재료가 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상됩니다."

에폭시 수지는 높은 기계적 강도와 구조적 강성을 가지고 있기 때문에 열 사이클, 진동, 기계적 충격에 노출되는 민감한 전자부품과 전력 부품을 내구성 있게 보호하는 EV 충전기 포팅 애플리케이션에서 중요한 역할을 합니다. 우수한 전기 절연성과 내화학성을 갖추고 있어 차량용 및 비차량용 충전 시스템 모두에서 고전압 AC/DC 변환 및 안전상 중요한 기능에 이상적입니다. 에폭시 포팅 컴파운드는 강력한 방습 및 방오 성능을 발휘하여 다양한 환경 조건에서 EV 충전기 전자기기의 가동 수명을 연장합니다. 배합의 유연성으로 열전도성 필러를 첨가할 수 있어 고출력 모듈 및 고밀도 파워 일렉트로닉스의 방열성 향상을 실현합니다. 또한, 에폭시 시스템에 대한 성숙한 세계 제조 기반과 확립된 공급업체 생태계는 EV 충전기 생산의 확장성과 비용 효율성을 뒷받침합니다. 또한, 절연성과 내구성을 손상시키지 않으면서 VOC 배출량이 적은 친환경 에폭시 배합과 REACH 등 진화하는 규제에 대한 적합성이 점점 더 중요시되고 있습니다. 예를 들어, 2025년 11월, Wevo Chemie는 EN 45545-2, UL 94V-0 등 엄격한 안전 기준을 충족하는 난연성 및 열전도성 에폭시 포팅 수지를 출시하였습니다. 이 소재는 부분 방전에 대한 높은 내성과 개선된 유동 특성을 가지고 있어 첨단 EV 충전기 밀봉을 포함한 고전압 및 고성능 애플리케이션에 적합합니다.

"지역별로는 유럽이 예측 기간 동안 큰 비중을 차지할 것으로 예상됩니다."

유럽에서는 전기자동차 충전 인프라가 빠르게 확대되고 있으며, 2025년 말까지 공공 충전기 설치 대수가 120만 대를 넘어설 것으로 예상되며, 급속 및 초급속 충전의 견조한 성장이 지속될 것으로 전망됩니다. 이로 인해 포팅 및 봉입이 필요한 충전기 전자기기에 대한 수요가 증가하고 있습니다. 특히 EU의 대체 연료 인프라 규제와 광범위한 배출가스 감축 목표 등 강력한 규제와 정책적 지원으로 회원국 전체에서 고출력 충전기의 보급이 의무화됨에 따라 내구성과 호환성을 겸비한 포팅 소재에 대한 수요가 증가하고 있습니다. 유럽의 충전기 제조업체와 Wallbox와 같은 충전 서비스 제공 업체는 복잡한 전력 및 제어 전자 장치를 통합한 스마트한 고밀도 초급속 충전 허브에 많은 투자를 하고 있으며, 절연, 열 관리 및 환경 보호 측면에서 포팅 기술의 이점을 누리고 있습니다. 이 지역에서는 상호운용성 및 안전 표준(ISO 15118 표준에 따른 CCS 구현 포함)에 대한 중요성이 강조되고 있으며, 전자 보호 재료에 대한 성능 및 신뢰성 요구사항이 더욱 높아지고 있습니다. 이는 충전기 설계에 첨단 포팅 컴파운드의 사용을 촉진하고 있습니다. 공공 네트워크에서 DC 충전기 및 초고속 충전기의 급속한 보급 확대에 따라 열 관리 및 장기적인 신뢰성을 보장하기 위해 열전도율과 기계적 강도가 우수한 포팅 컴파운드에 대한 수요도 증가하고 있습니다. 동시에 EU 전역의 통일된 인터페이스, 통신 프로토콜, 안전 프레임워크는 충전기 플랫폼을 간소화하고 포팅 재료 사양의 일관성을 촉진합니다. 또한 Henkel, Electrolube, Demak Group, ELANTAS 등 주요 포팅 컴파운드 제조업체의 본거지이기도 합니다.

세계의 EV 충전기용 전자 포팅 컴파운드 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요, 주요 기업 개요 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황과 지속가능성에 관한 대처

제8장 고객 상황과 구매 행동

제9장 EV 충전기용 전자 포팅 컴파운드 시장 : 충전기 유형별

제10장 EV 충전기용 전자 포팅 컴파운드 시장 : 설치 유형별

제11장 EV 충전기용 전자 포팅 컴파운드 시장 : 재료별

제12장 EV 충전기용 전자 포팅 컴파운드 시장 : 경화 기술별

제13장 EV 충전기용 전자 포팅 컴파운드 시장 : EV 부품별

제14장 EV 충전기용 전자 포팅 컴파운드 시장 : 용도별

제15장 EV 충전기용 전자 포팅 컴파운드 시장 : 지역별

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSM 26.03.05The electronic potting compound market for EV charger is projected to reach USD 0.96 billion by 2032 from USD 0.36 billion in 2025 at a CAGR of 14.9%. AC chargers are increasingly adopting compact, integrated power and control boards, driving demand for low-viscosity potting compounds that ensure complete coverage without affecting heat dissipation.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Million), Volume (Tons) |

| Segments | By Charger Type, Setup Type, Material Type, Curing Technology, EV Component, Application |

| Regions covered | Asia Pacific, Europe, North America, Rest of the World |

In DC chargers, the transition toward ultra-fast charging is intensifying the need for high-thermal-conductivity and high-partial-discharge-resistant potting materials. DC charger designs are also moving toward liquid-cooled and sealed power modules, increasing potting thickness and material consumption. Across both charger types, compatibility with automated dispensing and fast thermal curing is becoming a key material requirement. Additionally, materials with long-term resistance to moisture ingress and electrical tracking are gaining importance as outdoor charger deployments expand.

"DC charger is projected to lead the electronic potting compound market for EV charger during the forecast period."

DC chargers are expected to lead the electronic potting compound market for EV chargers during the forecast period due to their significantly higher power density and operating stress compared with AC or onboard chargers. Public DC charging sites and fleet depots operate in harsher environments exposed to moisture, vibration, and continuous duty cycles, which increase demand for robust encapsulation to ensure electrical insulation, environmental protection, and vibration damping. Large-scale infrastructure rollouts by OEMs and charge network operators are prioritizing high-power DC installations along highways, at commercial sites, and within fleet depots, concentrating unit volumes in charger platforms that require heavy and consistent potting usage. Material suppliers such as Parker Hannifin Corp are responding with low viscosity, fast flow thermally conductive potting compounds that can fill narrow gaps and efficiently transfer heat to housings and heat sinks in high power DC modules, while direct injection and pourable systems with faster curing and in-line quality control are gaining traction to support high throughput manufacturing. In parallel, ongoing government backed programs such as the US NEVI (National Electric Vehicle Infrastructure) initiative and China's continued expansion of ultra fast public charging corridors are accelerating the deployment of high power DC chargers. For instance, in August 2025, the California Energy Commission launched a USD 55 million Fast Charge California Program to subsidize public fast charger installations, including high-power DC stations at businesses and public sites. These investments increase demand for thermally robust and electrically reliable potting compounds, as each new high-power DC installation requires substantial encapsulation material to ensure long-term operational stability and regulatory compliance.

"The epoxy material is projected to register the highest growth in the electronic potting compound market for EV charger during the forecast period."

The epoxy segment is projected to register the highest growth in the electronic potting compound market for EV charger during the forecast period. Epoxy resins play a critical role in EV charger potting applications due to their high mechanical strength and structural rigidity, which provide durable protection for sensitive electronic and power components exposed to thermal cycling, vibration, and mechanical shock. They offer excellent electrical insulation and chemical resistance, making them well-suited for high voltage AC/DC conversion and safety-critical functions in both onboard and offboard charging systems. Epoxy potting compounds also deliver strong moisture and contaminant barrier performance, extending the operational life of EV charger electronics across diverse environmental conditions. Their formulation flexibility allows the incorporation of thermally conductive fillers, enabling improved heat dissipation in high-power modules and dense power electronics. In addition, the mature global manufacturing base and well-established supplier ecosystem for epoxy systems support scalability and cost efficiency in EV charger production. There is also growing emphasis on environmentally compliant epoxy formulations with lower VOC emissions and alignment with evolving regulations such as REACH, without sacrificing insulation or durability. For instance, in November 2025, Wevo Chemie introduced flame-retardant, thermally conductive epoxy potting resins designed to meet strict safety standards, such as EN 45545-2 and UL 94 V-0. These materials offer strong resistance to partial discharge and improved flow characteristics, making them suitable for high-voltage and high-performance applications, including advanced EV charger encapsulation.

"Europe is projected to hold a significant share in the electronic potting compound market for EV charger during the forecast period."

Europe is rapidly expanding its EV charging infrastructure with public charger installations exceeding 1.2 million units by the end of 2025 and continued strong growth in fast and ultra-fast charging, driving higher volumes of charger electronics that require potting and encapsulation. Strong regulatory and policy support, most notably the EU's Alternative Fuels Infrastructure Regulation and broader emission reduction targets, mandate widespread deployment of high-power chargers across member states, increasing demand for durable and compliant potting materials. European charger OEMs and charging service providers such as Wallbox are investing heavily in smart, high-density, and ultra-fast charging hubs that integrate complex power and control electronics, benefiting from potting for insulation, thermal management, and environmental protection. The region's strong emphasis on interoperability and safety standards, including CCS implementations with ISO 15118 features, further raises performance and reliability requirements for electronic protection materials, encouraging the use of advanced potting compounds in charger designs. The rapidly increasing share of DC and ultra-fast chargers in public networks is also elevating the need for thermally conductive and mechanically robust potting compounds to manage heat and ensure long-term reliability. At the same time, harmonized interfaces, communication protocols, and safety frameworks across the EU simplify charger platforms and promote consistency in potting material specifications. The region is also home to leading potting compound manufacturers, including Henkel, Electrolube, Demak Group, and ELANTAS.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: OEM - 20 %, Tier 1 - 70%, and Tier 2 - 10%

- By Designation: C-level - 40%, Directors - 35%, and Others - 25%

- By Region: Asia Pacific - 35%, North America - 35%, Europe - 25%, and Rest of the World - 5%

The electronic potting compound market for EV charger is dominated by major players, including Henkel Corporation (Germany), Dow (US), Parker Hannifin Corp (US), ELANTAS (Germany), and Momentive (US). These companies are expanding their portfolios to strengthen their position in the electronic potting compound market for EV charger.

Research Coverage:

The report covers the electronic potting compound market for EV charger in terms of setup type (wall mount, stationary), charger type (AC charger, DC charger), application (power electronics, HV components, busbars, and sensor relays, PCB and control modules, connector cable IP zones, charging gun, others), material type (polyurethane, epoxy, silicone), curing technology (room temperature cured, thermal cured, UV cured), EV component (electric motor stator, EV battery cells, EV battery cooling system, on-board charger, in-vehicle charging connector, in-vehicle power converter, others), and region. It covers the competitive landscape and company profiles of the significant players in the electronic potting compound market for EV charger.

The study also includes an in-depth competitive analysis of the key market players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the electronic potting compound market for EV charger and their subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

- The report will help market leaders/new entrants with information on various trends in the electronic potting compound market for EV charger based on setup type, charger type, application, material type, curing technology, EV component, and region.

The report provides insight into the following points:

- Analysis of key drivers (rising power density in charger electronics driving demand for high-thermal-conductivity potting materials, tightening electrical safety, insulation, and high-voltage testing standards, expansion of high-power DC fast charging drives advanced thermal cycling and stress-resistant potting requirements), restraints (regulatory tightening on flame-retardant chemistries and additive bans, restrictions on SVHCs under REACH and tightening RoHS scrutiny), opportunities (commercialization of high-thermal-conductivity silicone potting for WBG-enabled power modules, turnkey integration of automated dispensing and advanced potting materials for high-volume EV charger production), and challenges (SiC/GaN high-stress behavior creating new reliability failure modes for existing potting systems, circularity and end-of-life issues limiting high-performance polymer choices)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the electronic potting compound market for EV charger

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the electronic potting compound market for EV charger

- Competitive Assessment: In-depth assessment of market share, growth strategies, and product offerings of leading players, such as Henkel Corporation (Germany), Dow (US), Parker Hannifin Corp (US), ELANTAS (Germany), and Momentive (US), in the electronic potting compound market for EV charger

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE AND SEGMENTATION

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNITS CONSIDERED

- 1.7 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING ELECTRONIC POTTING COMPOUND MARKET FOR ELECTRIC VEHICLE (EV) CHARGER

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER

- 3.2 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION

- 3.3 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY SETUP TYPE

- 3.4 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE

- 3.5 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY MATERIAL TYPE

- 3.6 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CURING TECHNOLOGY

- 3.7 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY EV COMPONENT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising power density driving demand for high-thermal-conductivity potting materials

- 4.2.1.1.1 Ev charger types and utilization trends, 2026-2032

- 4.2.1.2 Tightening electrical safety, insulation, and high-voltage testing standards

- 4.2.1.3 Expansion of high-power DC fast charging increasing need for stress-resistant and thermal-cycling-stable potting materials

- 4.2.1.1 Rising power density driving demand for high-thermal-conductivity potting materials

- 4.2.2 RESTRAINTS

- 4.2.2.1 Regulatory pressure on flame-retardant chemistries and additive bans

- 4.2.2.2 Restrictions on substances of very high concern (SVHC)

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Commercialization of high-thermal-conductivity silicone potting for WBG-enabled power modules

- 4.2.3.2 Turnkey integration of automated dispensing and advanced potting materials for high-volume electric vehicle charger production

- 4.2.4 CHALLENGES

- 4.2.4.1 High-stress behavior of silicon carbide (SiC)/gallium nitride (GaN) creating new reliability failure modes for existing potting systems

- 4.2.4.2 Circularity and end-of-life issues limiting high-performance polymer choices

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 TRENDS IN GLOBAL ELECTRIC VEHICLE CHARGING STATION MARKET

- 5.1.4 TRENDS IN GLOBAL ELECTRIC VEHICLE INDUSTRY

- 5.2 TRENDS & DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.3 PRICING ANALYSIS

- 5.3.1 INDICATIVE PRICING ANALYSIS, BY CHARGER TYPE, 2024-2026 (USD/TON)

- 5.3.2 AVERAGE SELLING PRICE TREND FOR CHARGER TYPES, BY REGION, 2024-2026

- 5.3.2.1 Average selling price trend for AC chargers, by region, 2024-2026

- 5.3.2.2 Average selling price trend for DC chargers, by region, 2024-2026

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 CASE STUDY ANALYSIS

- 5.6.1 IMPROVING THERMAL PERFORMANCE AND RELIABILITY OF ELECTRIC VEHICLE ON-BOARD CHARGERS USING LOW-VISCOSITY POLYURETHANE POTTING COMPOUNDS

- 5.6.2 ENHANCING DURABILITY AND RELIABILITY OF ELECTRIC VEHICLE CHARGING CONNECTORS USING ADVANCED POTTING COMPOUNDS

- 5.6.3 MITIGATING THERMAL RUNAWAY IN CYLINDRICAL BATTERY SYSTEMS USING ADVANCED POLYURETHANE POTTING COMPOUNDS

- 5.7 INVESTMENT AND FUNDING SCENARIO

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT SCENARIO (HS CODE 3910)

- 5.8.2 EXPORT SCENARIO (HS CODE 3910)

- 5.8.3 IMPORT SCENARIO (HS CODE 390730)

- 5.8.4 EXPORT SCENARIO (HS CODE 390730)

- 5.9 KEY CONFERENCES AND EVENTS, 2026

- 5.10 INSIGHTS INTO MATERIAL CONSUMPTION PER EV CHARGER

- 5.10.1 POTTING COMPOUND CONSUMPTION PER CHARGER ARCHITECTURE

- 5.11 FUTURE ROADMAP FOR POTTING COMPOUND MATERIALS IN EV CHARGING STATIONS

- 5.11.1 MATERIALS ENABLING HIGHER POWER DENSITY AND ULTRA-FAST CHARGING

- 5.11.2 THERMAL AND ELECTRICAL PERFORMANCE UPGRADES FOR CONTINUOUS OPERATION

- 5.11.3 MANUFACTURING-OPTIMIZED POTTING FOR SCALABLE CHARGER DEPLOYMENT

- 5.11.4 SUSTAINABILITY, REWORKABILITY, AND END-OF-LIFE COMPLIANCE

- 5.12 INSIGHTS INTO PUBLIC ELECTRIC VEHICLE CHARGER SETUP FOR MAJOR MARKETS

- 5.12.1 AC CHARGER

- 5.12.2 DC CHARGER

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 PATENT ANALYSIS

- 6.2 IMPACT OF GENERATIVE AI ON ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER

- 6.2.1 TOP USE CASES AND MARKET POTENTIAL

- 6.2.1.1 High-performance power electronics

- 6.2.1.2 Connector and harness reliability

- 6.2.1.3 Custom compound design

- 6.2.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS

- 6.2.2.1 Generative design in formulation

- 6.2.2.2 AI-driven manufacturing and quality

- 6.2.3 CASE STUDIES RELATED TO AI IMPLEMENTATION

- 6.2.3.1 Accelerating potting compound innovation using AI-driven R&D platforms

- 6.2.3.2 Generative AI for advanced polymer and materials design

- 6.2.3.3 Customized potting compounds for EV power electronics

- 6.2.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT OF MARKET PLAYERS

- 6.2.4.1 Supply chain and services

- 6.2.4.2 Adjacent technologies

- 6.2.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED PROCESS IN ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER

- 6.2.1 TOP USE CASES AND MARKET POTENTIAL

- 6.3 KEY EMERGING TECHNOLOGIES

- 6.3.1 ADVANCED THERMALLY CONDUCTIVE SILICONE TECHNOLOGIES FOR EV CHARGER POWER ELECTRONICS

- 6.3.2 WIDE BANDGAP (WBG) POWER SEMICONDUCTORS

- 6.3.3 LOW-VISCOSITY, VOID-FREE POTTING CHEMISTRIES

- 6.3.4 FAST-CURE AND SNAP-CURE POTTING FORMULATIONS

- 6.4 COMPLEMENTARY TECHNOLOGIES

- 6.4.1 AUTOMATED DISPENSING AND METERING SYSTEMS

- 6.4.2 AL-ENABLED PROCESS MONITORING AND CONTROL

- 6.5 ADJACENT TECHNOLOGIES

- 6.5.1 CONFORMAL COATINGS AND SELECTIVE ENCAPSULATION

- 6.5.2 ADVANCED ADHESIVES AND STRUCTURAL BONDING MATERIALS

- 6.5.3 RECYCLABLE AND DEBONDABLE POLYMER SYSTEMS

- 6.6 TECHNOLOGY/PRODUCT ROADMAP

- 6.6.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.6.2 MID-TERM (2028-2030) | EXPANSION & STANDARDIZATION

- 6.6.3 LONG-TERM (2031-2035+) | MASS COMMERCIALIZATION & DISRUPTION

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2.1 INDUSTRY STANDARDS

- 7.3 SUSTAINABILITY INITIATIVES

- 7.3.1 CARBON IMPACT AND ECO-APPLICATIONS

- 7.3.1.1 Bio-based resins

- 7.3.1.2 Low-VOC, solventless formulations

- 7.3.1.3 Removable (debondable) potting

- 7.3.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.3.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

- 7.3.1 CARBON IMPACT AND ECO-APPLICATIONS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

9 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE

- 9.1 INTRODUCTION

- 9.2 AC CHARGER

- 9.2.1 INCREASING POWER DENSITY IN COMPACT AC CHARGER DESIGNS TO FUEL GROWTH

- 9.3 DC CHARGER

- 9.3.1 GOVERNMENT-BACKED EXPANSION OF ULTRA-FAST DC CHARGING NETWORKS TO FUEL GROWTH

- 9.4 KEY PRIMARY INSIGHTS

10 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY SETUP TYPE

- 10.1 INTRODUCTION

- 10.2 WALL MOUNT (PRIVATE)

- 10.2.1 EXPANSION OF RESIDENTIAL LEVEL 2 CHARGING INFRASTRUCTURE TO FUEL GROWTH

- 10.3 STATIONARY (PUBLIC)

- 10.3.1 SCALING DEPLOYMENT OF ULTRA-FAST PUBLIC CHARGING HUBS TO FUEL GROWTH

- 10.4 KEY PRIMARY INSIGHTS

11 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY MATERIAL TYPE

- 11.1 INTRODUCTION

- 11.2 POLYURETHANE

- 11.2.1 ADVANCEMENTS IN TWO-COMPONENT POLYURETHANE SYSTEMS FOR EV CHARGER ENCAPSULATION TO FUEL GROWTH

- 11.3 SILICONE

- 11.3.1 SHIFT TOWARD HIGH THERMALLY CONDUCTIVE SILICONE MATERIALS IN ULTRA-FAST CHARGING PLATFORMS TO DRIVE MARKET

- 11.4 EPOXY

- 11.4.1 EXPANSION OF LOW-VOC, REGULATION-COMPLIANT EPOXY FORMULATIONS IN ELECTRIC VEHICLE CHARGING APPLICATIONS TO FUEL GROWTH

- 11.5 KEY PRIMARY INSIGHTS

12 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CURING TECHNOLOGY

- 12.1 INTRODUCTION

- 12.2 ROOM TEMPERATURE CURED

- 12.2.1 EXPANSION OF TWO-COMPONENT ROOM-TEMPERATURE-CURED SYSTEMS IN AC AND DC CHARGERS TO FUEL GROWTH

- 12.3 THERMAL CURED

- 12.3.1 HIGHER POWER RATINGS AND SIC INTEGRATION ACCELERATING USE OF THERMALLY CURED POTTING COMPOUNDS

- 12.4 UV CURED

- 12.4.1 EXPANSION OF HYBRID UV CURING SYSTEMS IN COMPACT AND SMART CHARGER DESIGNS TO FUEL GROWTH

- 12.5 KEY PRIMARY INSIGHTS

13 ELECTRONIC POTTING COMPOUND MARKET, BY EV COMPONENT

- 13.1 INTRODUCTION

- 13.2 ELECTRIC MOTOR STATOR

- 13.2.1 SHIFT TOWARD HIGH-DENSITY DRIVE UNITS STRENGTHENING NEED FOR RELIABLE STATOR ENCAPSULATION

- 13.3 EV BATTERY CELL

- 13.3.1 INCREASING FOCUS ON THERMAL RUNAWAY MITIGATION IN ELECTRIC VEHICLE BATTERIES TO DRIVE MARKET

- 13.4 EV BATTERY COOLING SYSTEM

- 13.4.1 RISING ADOPTION OF CELL-TO-PACK AND CELL-TO-CHASSIS ARCHITECTURES TO BOOST ENCAPSULATION DEMAND

- 13.5 ON-BOARD CHARGER

- 13.5.1 GROWING INTEGRATION OF MULTI-FUNCTIONAL OBC AND DC-DC UNITS TO DRIVE DEMAND

- 13.6 IN-VEHICLE CHARGING CONNECTOR

- 13.6.1 RISING ADOPTION OF HIGH-CURRENT, COMPACT EV CHARGING CONNECTORS TO FUEL GROWTH

- 13.7 IN-VEHICLE POWER CONVERTER

- 13.7.1 RISING INTEGRATION OF MULTIPLE POWER-ELECTRONICS FUNCTIONS TO FUEL GROWTH

- 13.8 OTHERS

- 13.9 KEY PRIMARY INSIGHTS

14 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY APPLICATION

- 14.1 INTRODUCTION

- 14.2 POWER ELECTRONICS

- 14.3 HV COMPONENTS, BUSBARS, AND SENSOR RELAYS

- 14.4 PCB AND CONTROL MODULES

- 14.5 CONNECTOR CABLE IP ZONES

- 14.6 CHARGING GUNS

- 14.7 OTHERS

15 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION

- 15.1 INTRODUCTION

- 15.2 ASIA PACIFIC

- 15.2.1 CHINA

- 15.2.1.1 Presence of well-established domestic manufacturing ecosystem for chargers, power electronics, and materials to drive market

- 15.2.2 INDIA

- 15.2.2.1 Growing localization of EV charger manufacturing under "Make in India" initiative to fuel growth

- 15.2.3 JAPAN

- 15.2.3.1 Increasing installation of high-output EV chargers under Japan's 2030 targets to drive market

- 15.2.4 SOUTH KOREA

- 15.2.4.1 Government-backed deployment of ultra-fast charging networks to fuel growth

- 15.2.5 THAILAND

- 15.2.5.1 Rapid deployment of high-power DC fast chargers to drive market

- 15.2.6 INDONESIA

- 15.2.6.1 Rapid deployment of public EV charging stations and local manufacturing to drive market

- 15.2.7 SINGAPORE

- 15.2.7.1 Deployment of compact, high-density public EV charging systems to drive market

- 15.2.1 CHINA

- 15.3 EUROPE

- 15.3.1 AUSTRIA

- 15.3.1.1 Strategic investment in high-power EV charging under eMove Austria to fuel growth

- 15.3.2 DENMARK

- 15.3.2.1 Acceleration of residential and public EV charger installations under regulatory reforms to drive market

- 15.3.3 FRANCE

- 15.3.3.1 Fleet-focused charging rollouts and OEM-led infrastructure expansion to drive market

- 15.3.4 GERMANY

- 15.3.4.1 Expansion of multi-family residential and corridor charging infrastructure to drive market

- 15.3.5 NETHERLANDS

- 15.3.5.1 High per-capita EV charger installations to drive market

- 15.3.6 NORWAY

- 15.3.6.1 Expansion of highway DC fast-charging corridors to drive market

- 15.3.7 SPAIN

- 15.3.7.1 Government-backed expansion of corridor and rural EV charging networks to fuel growth

- 15.3.8 SWEDEN

- 15.3.8.1 Megawatt charging corridor development to drive high-power charger installations

- 15.3.9 SWITZERLAND

- 15.3.9.1 Subsidized deployment of high-power fleet charging systems to drive market

- 15.3.10 UK

- 15.3.10.1 Government-backed expansion of motorway super hubs and depot charging to fuel growth

- 15.3.1 AUSTRIA

- 15.4 NORTH AMERICA

- 15.4.1 US

- 15.4.1.1 Strategic OEM partnerships and high-voltage charger rollouts to drive market

- 15.4.2 CANADA

- 15.4.2.1 Government-backed rollout of EV chargers to drive market

- 15.4.3 MEXICO

- 15.4.3.1 Strategic rollout of retail and commercial charging sites to fuel growth

- 15.4.1 US

- 15.5 REST OF THE WORLD

- 15.5.1 BRAZIL

- 15.5.1.1 Policy-backed residential charging access expansion in multi-unit buildings to fuel growth

- 15.5.2 UAE

- 15.5.2.1 Scaling fleet-focused and destination DC fast charging networks to drive market

- 15.5.1 BRAZIL

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 16.3 MARKET SHARE ANALYSIS OF EV CHARGER POTTING COMPOUND MANUFACTURERS, 2025

- 16.4 REVENUE ANALYSIS OF TOP LISTED/PUBLIC PLAYERS, 2020-2024

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS, 2026

- 16.5.1 COMPANY VALUATION

- 16.5.2 FINANCIAL METRICS

- 16.6 BRAND/ PRODUCT COMPARISON

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2026

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2026

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Charger type footprint

- 16.7.5.4 Material type footprint

- 16.7.5.5 Setup type footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2026

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2026

- 16.8.5.1 List of startups/SMEs

- 16.8.5.2 Competitive benchmarking of startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

- 16.9.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 HENKEL CORPORATION

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 PARKER HANNIFIN CORP

- 17.1.2.1 Business overview

- 17.1.2.2 Product offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Other developments

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 ELANTAS

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 MnM view

- 17.1.3.3.1 Key strengths

- 17.1.3.3.2 Strategic choices

- 17.1.3.3.3 Weaknesses and competitive threats

- 17.1.4 DOW

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches

- 17.1.4.3.2 Other developments

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 MOMENTIVE

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 MnM view

- 17.1.5.3.1 Key strengths

- 17.1.5.3.2 Strategic choices

- 17.1.5.3.3 Weaknesses and competitive threats

- 17.1.6 ELECTROLUBE

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Other developments

- 17.1.7 DEMAK GROUP

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.8 WEVO-CHEMIE GMBH

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches

- 17.1.9 EPOXIES, ETC.

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.10 RAMPF

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Expansions

- 17.1.10.3.2 Other developments

- 17.1.11 KISLING

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Deals

- 17.1.12 SIKA AUTOMOTIVE

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.1 HENKEL CORPORATION

- 17.2 OTHER PLAYERS

- 17.2.1 MASTER BOND

- 17.2.2 PERMABOND

- 17.2.3 DOPAG

- 17.2.4 FINEFINISH

- 17.2.5 MG CHEMICALS

- 17.2.6 3M

- 17.2.7 VEEYOR POLYMERS

- 17.2.8 NAGASE & CO., LTD.

- 17.2.9 WACKER CHEMIE AG

- 17.2.10 PROSTECH

- 17.2.11 MB ENTERPRISES

- 17.2.12 ELKEM ASA

- 17.2.13 ITW PERFORMANCE POLYMERS

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 List of key secondary sources

- 18.1.1.2 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Primary interview participants

- 18.1.2.2 Key industry insights and breakdown of primary interviews

- 18.1.2.3 List of primary interview participants

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 BOTTOM-UP APPROACH

- 18.2.2 TOP-DOWN APPROACH

- 18.3 DATA TRIANGULATION

- 18.4 FACTOR ANALYSIS

- 18.4.1 DEMAND- AND SUPPLY-SIDE FACTOR ANALYSIS

- 18.5 RESEARCH ASSUMPTIONS

- 18.6 RESEARCH LIMITATIONS

- 18.7 RISK ASSESSMENT

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.3.1 BREAKDOWN OF ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY SETUP TYPE, AT COUNTRY LEVEL (FOR COUNTRIES COVERED IN REPORT)

- 19.3.2 COMPANY INFORMATION:

- 19.3.2.1 Profiling of additional market players (up to 5)

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS