|

시장보고서

상품코드

1937991

조직 진단 시장 : 제품 및 서비스별, 기술별, 질병 유형별, 샘플 유형별, 최종 사용자별, 지역별 예측(-2030년)Tissue Diagnostics Market by Product (Consumables, Instruments, Software, Services), Technology, Disease Type - Forecast to 2030 |

||||||

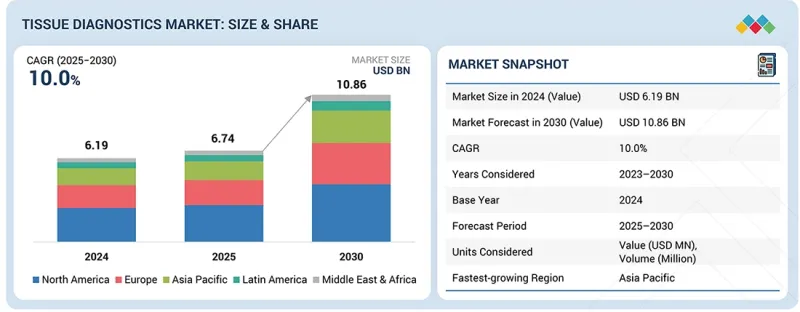

조직 진단 시장 규모는 2025년 67억 4,000만 달러로 평가되었고, 예측 기간 동안 CAGR은 10.0%를 나타낼 것으로 보이며, 2030년까지 108억 6,000만 달러에 달할 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품 및 서비스별, 기술별, 질병 유형별, 샘플 유형별, 최종 사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

민간 진단 센터의 증가하는 설립은 조직 진단 시장에 상당한 영향을 미치고 있습니다. 이러한 센터들은 이전에는 대형 병원에만 제한되었던 전문 병리학 및 실험실 솔루션을 제공함으로써 첨단 검사 서비스에 대한 접근성을 확대하고 있습니다. 민간 센터들은 현대적인 조직 진단 시스템, 소모품 및 자동화된 워크플로우에 투자함으로써 질병 검출의 속도, 정확성 및 신뢰성을 향상시키고 있습니다. 이러한 추세는 조직 진단 기술의 채택을 증가시킬 뿐만 아니라 보다 개인화되고 시기적절한 환자 치료를 지원하여 시장의 전반적인 성장에 기여하고 있습니다.

기술별로 조직 진단 시장은 면역조직화학(IHC), 현미경 내 하이브리다이제이션(ISH), 디지털 병리학, 특수 염색 및 기타 기술로 분류됩니다. 이 중 면역조직화학은 조직 샘플 내 특정 단백질의 검출 및 시각화에 폭넓게 적용되어 정확한 질병 진단, 바이오마커 식별, 맞춤형 치료 계획 수립에 핵심적인 역할을 수행함으로써 지배적 위치를 차지하고 있습니다. 조직 형태와 분자 발현에 대한 정성적·정량적 인사이트를 동시에 제공할 수 있는 능력은 암 진단 및 연구에 있어 그 가치를 높입니다. 또한 IHC는 자동 염색 시스템, 표준화된 시약, 고처리량 워크플로우와의 호환성으로 인해 임상 실험실, 연구 기관 및 제약 개발 분야에서 채택이 더욱 가속화되었습니다. ISH 및 디지털 병리학과 같은 신기술은 추가적인 분자 및 영상 기능을 제공함으로써 IHC를 보완하지만, IHC의 입증된 신뢰성, 다용도성 및 확립된 프로토콜은 조직 진단 시장에서 지속적인 우위를 유지하는 원동력입니다.

조직 진단 시장은 질병 유형에 따라 유방암, 위암, 림프종, 전립선암, 비소세포폐암(NSCLC), 기타 질병 유형으로 세분화됩니다. 이 중 유방암 부문이 예측 기간 동안 가장 높은 성장률을 기록할 것으로 예상됩니다. 이러한 급속한 확장은 전 세계적으로 증가하는 유방암 발병률, 조기 발견에 대한 인식 제고, 정확한 바이오마커 식별을 위한 첨단 진단 도구 채택 증가에 의해 주도됩니다. IHC 패널 및 다중 분석을 포함한 조직 진단 분야의 혁신은 정밀한 하위 분류 및 위험 계층화를 더욱 가능하게 하여 맞춤형 치료 결정에 기여하고 있습니다. 이러한 요소들이 종합적으로 유방암 부문을 조직 진단 시장 내 가장 빠르게 성장하는 영역으로 자리매김하게 합니다.

조직 진단 시장은 북미, 유럽, 아시아태평양, 라틴 아메리카, 중동 및 아프리카로 분류됩니다. 아시아태평양 지역은 예측 기간 동안 가장 높은 성장률을 기록할 것으로 예상됩니다. 급속히 확장되는 의료 인프라, 조기 질병 검출을 위한 정부 정책 강화, 암 검진에 대한 인식 제고가 해당 지역 시장 확장의 핵심 촉진요인입니다. 또한 연구개발 투자 증가, 암 유병률 상승, 중국, 인도 및 일본 등 신흥 경제국의 첨단 진단 기술 도입이 시장 성장을 가속화하고 있습니다. 이러한 추세로 아시아태평양 지역은 향후 조직진단 분야에서 높은 성장 잠재력을 지닌 지역으로 부상할 전망입니다.

조직 진단 시장의 주요 기업은 F. Hoffmann-La Roche Ltd.(스위스), Danaher Corporation(미국), PHC Holdings Corporation(Epredia)(일본), Abbott(미국), Agilent Technologies(미국), Merck KGaA(독일), Sakura Finetek Japan(미국), Becton Dickinson SB(미국), Cell Signaling Technology, Inc.(미국), Histo-Line Laboratories(이탈리아), SLEE medical GmbH(독일), Amos Scientific Pty Ltd.(호주), Jinhua YIDI Medical Appliance(중국), MEDITE Medical GmbH(독일), StatLab Medical Products(중국), Diagnostic BioSystems Inc.(미국), 3DHISTECH(헝가리), RWD Life Science(미국), Dakewe(중국), Battery Ventures(Enzo Biochem Inc.)(미국), Biocare Medical, LLC.(미국), MILESTONE MEDICAL(이탈리아), Bio-Optica doo(크로아티아) 등입니다.

조사 범위 :

본 조사 보고서에서는 조직 진단 시장을 제품 및 서비스별, 기술별, 질병 유형별, 최종 사용자별, 지역별로 분류하고 있습니다.

이 보고서의 조사 범위는 조직 진단 시장의 성장에 영향을 미치는 주요 요인(촉진 요인, 억제요인, 기회, 과제 등)에 대한 자세한 정보를 다룹니다. 주요 업계 진출기업의 상세한 분석을 실시해, 각사의 사업 개요, 솔루션, 주요 전략, 인수, 계약에 관한 인사이트를 제공합니다. 조직 진단 시장 생태계의 신흥 신생 기업 경쟁 분석도이 보고서에서 다루고 있습니다.

이 보고서를 구입하는 이유 :

본 보고서는 시장 선도 기업 및 신규 진입자에게 전체 조직 진단 시장 및 하위 부문의 매출 규모에 대한 가장 근접한 추정치를 제공합니다. 이해관계자들이 경쟁 환경을 파악하고 비즈니스 포지셔닝을 개선하며 적절한 시장 진출 전략을 수립하는 데 필요한 인사이트를 얻을 수 있도록 지원합니다. 또한 시장의 동향을 이해하고 주요 시장 촉진요인, 억제요인, 기회 및 도전 과제에 대한 정보를 제공합니다.

이 보고서는 다음 포인트에 대한 인사이트를 제공합니다.

- 주요 촉진요인 분석 (암 유병률 증가, 디지털 병리학 수요 증가, 의료비 지출 증가, 보험 적용 확대, 민간 진단 센터 설립 증가), 억제요인 (조직 진단 시스템의 높은 비용, 엄격한 규제 요건), 기회 (신흥 경제국의 높은 성장 기회, 맞춤형 의약품 수요 증가, 암 치료제 임상 시험 증가), 과제(숙련된 전문가 부족, 리퍼브 제품 공급, 조직진단(TDx) 표준화 미비)

- 제품 개발/혁신 : 조직 진단 시장에서 출시 예정인 기술, 연구 개발 활동 및 신제품 출시에 대한 상세한 인사이트

- 시장 개발 : 수익성 높은 시장에 대한 포괄적인 정보 - 본 보고서는 다양한 지역의 조직 진단 시장을 분석합니다.

- 시장 다각화 : 조직 진단 시장의 신제품, 미개척 지역, 최근 동향 및 투자에 관한 포괄적인 정보

- 경쟁 평가 : 조직 진단 시장의 주요 기업(F. Hoffmann-La Roche Ltd(스위스), Danaher Corporation(미국), PHC Holdings Corporation(일본), Agilent Technologies(미국) 등) 시장 점유율, 성장 전략 및 제품 제공에 대한 자세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 중요 인사이트

제4장 시장 개요

- 시장 역학

- 성장 촉진요인

- 억제요인

- 기회

- 과제

- 미충족 요구와 공백

- 상호접속된 시장과 분야간 기회

- Tier 1/2/3 참가 기업의 전략적 움직임

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제 전망

- 공급망 분석

- 밸류체인 분석

- 생태계 분석

- 가격 분석

- 무역 분석

- 주요 회의 및 이벤트(2025-2026년)

- 고객사업에 영향을 주는 동향/혼란

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 미국 관세가 조직 진단 시장에 미치는 영향(2025년)

제6장 기술의 진보, AI의 영향, 특허, 혁신, 장래의 응용

- 주요 신기술

- 보완적 기술

- 기술/제품 로드맵

- 특허 분석

- 미래의 응용

- AI/생성형 AI가 조직 진단 시장에 미치는 영향(2025년)

제7장 지속가능성과 규제상황

- 지역 규제 및 규정 준수

- 규제기관, 정부기관, 기타 조직

- 업계 표준

- 지속가능성에 대한 노력

- 조직 진단의 환경에 대한 영향과 환경 친화적인 대처

- 지속가능성에 미치는 영향과 규제 정책의 노력

- 인증, 라벨, 환경 기준

제8장 고객정세와 구매행동

- 의사결정 프로세스

- 구매자의 이해관계자와 구매 평가 기준

- 채용 장벽과 내부 과제

- 다양한 최종 이용 산업으로부터의 미충족 요구

- 시장 수익성

제9장 조직 진단 시장(제품 및 서비스별)

- 소모품

- 장치

- 소프트웨어

- 서비스

제10장 조직 진단 시장(기술별)

- 면역조직화학(IHC)

- 현미경 내 하이브리다이제이션(ISH)

- 디지털 병리학

- 특수 염색 및 기타 기술

제11장 조직 진단 시장(질병 유형별)

- 유방암

- 위암

- 림프종

- 전립선암

- 비소세포폐암(NSCLC)

- 기타

제12장 미국 : 조직 진단 검사 수(샘플 유형별)

제13장 조직 진단 시장(최종 사용자별)

- 병원

- 연구실

- 제약회사

- CRO

- 기타

제14장 조직 진단 시장(지역별)

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 거시 경제 전망

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 아시아태평양의 거시 경제 전망

- 중국

- 일본

- 인도

- 기타

- 라틴아메리카

- 라틴아메리카의 거시 경제 전망

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- 중동 및 아프리카의 거시경제 전망

제15장 경쟁 구도

- 개요

- 주요 참가 기업의 전략/강점(2022-2025년)

- 수익 분석(2022-2024년)

- 시장 점유율 분석(2024년)

- 브랜드 비교

- 기업평가 매트릭스 : 주요 진입기업(2024년)

- 기업평가 매트릭스 : 스타트업/중소기업(2024년)

- 기업평가와 재무지표

- 경쟁 시나리오

제16장 기업 프로파일

- 주요 진출기업

- F. HOFFMANN-LA ROCHE LTD.

- DANAHER CORPORATION

- AGILENT TECHNOLOGIES, INC.

- PHC HOLDINGS CORPORATION(EPREDIA)

- MERCK KGAA

- ABBOTT

- BECTON, DICKINSON AND COMPANY

- SYSMEX CORPORATION

- SAKURA FINETEK JAPAN CO., LTD.

- BIOGENEX

- BIO SB

- CELL SIGNALING TECHNOLOGY, INC.

- HISTO-LINE LABORATORIES

- SLEE MEDICAL GMBH

- 기타 기업

- AMOS SCIENTIFIC PTY LTD.

- JINHUA YIDI MEDICAL APPLIANCE CO., LTD.

- MEDITE MEDICAL GMBH

- SLMP, LLC

- KONFOONG BIOINFORMATION TECH CO., LTD(KFBIO)

- DIAGNOSTIC BIOSYSTEMS INC.

- 3DHISTECH LTD.

- RWD LIFE SCIENCE CO., LTD.

- DAKEWE

- BATTERY VENTURES(ENZO BIOCHEM INC.)

- BIOCARE MEDICAL, LLC.

- MILESTONE SRL

- BIO-OPTICA MILANO SPA

- BIOGNOST DOO

- OPTRASCAN

- CLARAPATH

제17장 조사 방법

제18장 부록

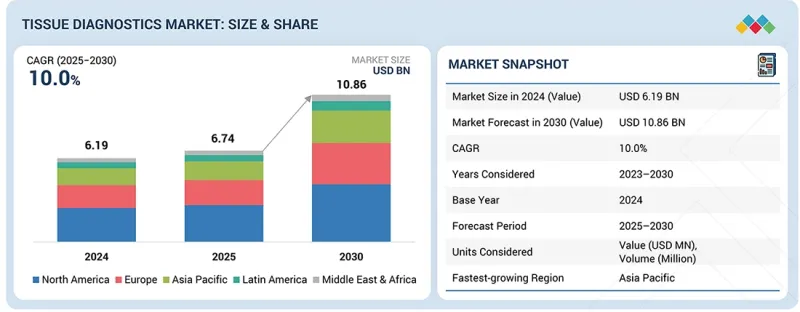

HBR 26.02.26The tissue diagnostics market is estimated to be USD 6.74 billion in 2025 and is projected to reach USD 10.86 billion by 2030 at a CAGR of 10.0% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product & service, technology, disease type, end user |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

The growing establishment of private diagnostic centers is significantly influencing the tissue diagnostics market. These centers are expanding access to advanced testing services, offering specialized pathology and laboratory solutions that were previously limited to large hospitals. By investing in modern tissue diagnostic systems, consumables, and automated workflows, private centers are enhancing the speed, accuracy, and reliability of disease detection. This trend not only increases the adoption of tissue diagnostic technologies but also supports more personalized and timely patient care, contributing to the overall growth of the market.

"By technology, the immunohistochemistry segment dominated the tissue diagnostics market in 2024."

Based on technology, the tissue diagnostics market is segmented into immunohistochemistry (IHC), in situ hybridization (ISH), digital pathology, special staining, and other technologies. Among these, immunohistochemistry holds a dominant position due to its broad application in detecting and visualizing specific proteins in tissue samples, which play a critical role in accurate disease diagnosis, biomarker identification, and guiding personalized treatment plans. Its ability to provide both qualitative and quantitative insights into tissue morphology and molecular expression makes it invaluable for cancer diagnostics and research. Additionally, IHC's compatibility with automated staining systems, standardized reagents, and high-throughput workflows has further accelerated its adoption in clinical laboratories, research institutions, and pharmaceutical development. Emerging technologies like ISH and digital pathology complement IHC by offering additional molecular and imaging capabilities, but the proven reliability, versatility, and established protocols of IHC continue to drive its sustained dominance in the tissue diagnostics market.

"By disease type, the breast cancer segment is projected to achieve the highest growth during the forecast period."

The tissue diagnostics market is segmented based on disease types into breast cancer, gastric cancer, lymphoma, prostate cancer, non-small cell lung cancer (NSCLC), and other disease types. Among these, the breast cancer segment is expected to register the highest growth during the forecast period. This rapid expansion is driven by the increasing global incidence of breast cancer, heightened awareness of early detection, and growing adoption of advanced diagnostic tools for accurate biomarker identification. Innovations in tissue diagnostics, including IHC panels and multiplex assays, are further enabling precise subtyping and risk stratification, supporting personalized treatment decisions. These factors collectively position the breast cancer segment as the fastest-growing area within the tissue diagnostics market.

"Asia Pacific is projected to be the fastest-growing regional market during the forecast period." "

The market for tissue diagnostics is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific is expected to register the highest growth during the forecast period. Rapidly expanding healthcare infrastructure, increasing government initiatives for early disease detection, and rising awareness about cancer screening are key factors driving market expansion in the region. Additionally, growing investments in research and development, the increasing prevalence of cancer, and the adoption of advanced diagnostic technologies in emerging economies such as China, India, and Japan are further accelerating market growth. These trends make Asia Pacific a high-potential region for tissue diagnostics in the coming years.

Break-up of the profiles of primary participants in the tissue diagnostics market:

- By Company Type: Tier 1 - 40%, Tier 2 - 30%, and Tier 3 - 30%

- By Designation: C-level - 27%, D-level - 18%, and Others - 55%

- By Region: North America - 51%, Europe - 21%, Asia Pacific - 18%, Latin America - 6%, and Middle East & Africa- 4%

The key players in the tissue diagnostics market are F. Hoffmann-La Roche Ltd. (Switzerland), Danaher Corporation (US), PHC Holdings Corporation (Epredia) (Japan), Abbott (US), Agilent Technologies (US), Merck KGaA (Germany), Sakura Finetek Japan Co., Ltd. (Japan), Becton, Dickinson and Company (US), BioGenex (US), Bio SB (US), Cell Signaling Technology, Inc. (US), Histo-Line Laboratories (Italy), SLEE medical GmbH (Germany), Amos Scientific Pty Ltd. (Australia), Jinhua YIDI Medical Appliance Co., Ltd. (China), MEDITE Medical GmbH (Germany), StatLab Medical Products (UK), KONFOONG BIOINFORMATION TECH Co., Ltd. (China), Diagnostic BioSystems Inc. (US), 3DHISTECH (Hungary), RWD Life Science Co., Ltd. (US), Dakewe (China), Battery Ventures (Enzo Biochem Inc.) (US), Biocare Medical, LLC. (US), MILESTONE MEDICAL (Italy), Bio-Optica Milano Spa (Italy), and BioGnost d.o.o. (Croatia).

Research Coverage:

This research report categorizes the tissue diagnostics market by product & service (consumables, instruments, software, and services), technology (immunohistochemistry (IHC), in situ hybridization (ISH), digital pathology, special staining, and other technologies), disease type (breast cancer, gastric cancer, lymphoma, prostate cancer, non-small cell lung cancer, other disease types), end user [hospitals, research laboratories, pharmaceutical companies, contract research organizations (CROs), and other end users], and region (North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa).

The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, opportunities, and challenges, influencing the growth of the tissue diagnostics market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, key strategies, acquisitions, and agreements. Competitive analysis of upcoming startups in the tissue diagnostics market ecosystem is covered in this report.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall tissue diagnostics market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers (Rising prevalence of cancer, Growing demand for digital pathology, Increasing healthcare expenditure, Growing availability of reimbursements, and Rising establishment of private diagnostic centers), restraints (High cost of tissue diagnostic systems and Stringent regulatory requirements), opportunities (High growth opportunities of emerging economies, Growing demand for personalized medicines, Increasing number of clinical trials for cancer therapeutics), and challenges (Shortage of skilled professionals, Availability of refurbished products, and Inadequate standardization for TDx) influencing the growth of the tissue diagnostics market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the tissue diagnostics market

- Market Development: Comprehensive information about lucrative markets - the report analyses the tissue diagnostics market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the tissue diagnostics market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players like F. Hoffmann-La Roche Ltd (Switzerland), Danaher Corporation (US), PHC Holdings Corporation (Japan), Agilent Technologies (US), among others, in the tissue diagnostics market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 TISSUE DIAGNOSTICS MARKET OVERVIEW

- 3.2 TISSUE DIAGNOSTICS MARKET, BY PRODUCT & SERVICE, 2025 VS. 2030

- 3.3 TISSUE DIAGNOSTICS MARKET, BY TECHNOLOGY, 2025 VS. 2030

- 3.4 TISSUE DIAGNOSTICS MARKET, BY DISEASE, 2025 VS. 2030

- 3.5 TISSUE DIAGNOSTICS MARKET, BY END USER, 2025 VS. 2030

- 3.6 TISSUE DIAGNOSTICS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising incidence of cancer

- 4.2.1.2 Growing demand for digital pathology

- 4.2.1.3 Increasing healthcare expenditure

- 4.2.1.4 Growing availability of reimbursements

- 4.2.1.5 Rising establishment of private diagnostic centers

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost of tissue diagnostic systems

- 4.2.2.2 Stringent regulatory requirements

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 High growth potential in emerging economies

- 4.2.3.2 Growing preference for personalized medicines

- 4.2.3.3 Increasing number of clinical trials for cancer therapeutics

- 4.2.4 CHALLENGES

- 4.2.4.1 Shortage of skilled professionals

- 4.2.4.2 Availability of refurbished products

- 4.2.4.3 Inadequate standardization

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND, BY PRODUCT, 2023-2025

- 5.6.2 AVERAGE SELLING PRICE TREND, BY KEY PLAYER, 2023-2025

- 5.6.3 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA (HS CODE 3822)

- 5.7.2 EXPORT DATA (HS CODE 3822)

- 5.8 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 CASE STUDY 1: OPTIMIZING AUTOMATED TISSUE PROCESSING EFFICIENCY TO REDUCE COST

- 5.11.2 CASE STUDY 2: OPERATIONAL EFFICIENCY IMPROVEMENTS THROUGH MILESTONE MEDICAL TISSUE PROCESSOR IMPLEMENTATION

- 5.11.3 CASE STUDY 3: WORKFLOW OPTIMIZATION THROUGH EXCELSIOR AS TISSUE PROCESSOR

- 5.12 IMPACT OF 2025 US TARIFFS ON TISSUE DIAGNOSTICS MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 KEY IMPACT ON COUNTRY/REGION

- 5.12.4.1 North America

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USE INDUSTRIES

- 5.12.5.1 Hospitals

- 5.12.5.2 Research laboratories

- 5.12.5.3 Pharmaceutical companies

- 5.12.5.4 Contract research organizations (CROs)

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 IMMUNOHISTOCHEMISTRY (IHC)

- 6.1.2 IN SITU HYBRIDIZATION (ISH)

- 6.1.3 DIGITAL PATHOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 SPECIAL STAINING

- 6.2.2 MASS SPECTROMETRY IMAGING (MSI)

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | OPTIMIZATION & STANDARDIZATION OF CORE REAGENTS

- 6.3.1.1 Core technology development

- 6.3.1.2 Product innovations

- 6.3.1.3 Market adoption

- 6.3.2 MID-TERM (2027-2030) | EXPANDED CAPABILITIES & SUSTAINABILITY

- 6.3.2.1 Advanced technology development

- 6.3.2.2 Product innovations

- 6.3.2.3 Market adoption

- 6.3.3 LONG-TERM (2030-2035+) | HIGH-PERFORMANCE & ECO-EFFICIENT TISSUE DIAGNOSTICS PRODUCTS

- 6.3.3.1 High-performance & integrated workflows

- 6.3.3.2 Product innovations

- 6.3.3.3 Market adoption

- 6.3.1 SHORT-TERM (2025-2027) | OPTIMIZATION & STANDARDIZATION OF CORE REAGENTS

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.6 IMPACT OF AI/GENERATIVE AI ON TISSUE DIAGNOSTICS MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN TISSUE DIAGNOSTICS MARKET

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN TISSUE DIAGNOSTICS MARKET

- 6.6.4 FUTURE OF AI IN TISSUE DIAGNOSTICS MARKET

- 6.6.5 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.6.6 CLIENTS' READINESS TO ADOPT GENERATIVE AND AI-ENABLED TECHNOLOGIES IN TISSUE DIAGNOSTICS MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 ENVIRONMENTAL IMPACT AND ECO-FRIENDLY INITIATIVES IN TISSUE DIAGNOSTICS

- 7.2.1.1 Eco-friendly initiatives

- 7.2.1 ENVIRONMENTAL IMPACT AND ECO-FRIENDLY INITIATIVES IN TISSUE DIAGNOSTICS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 TISSUE DIAGNOSTICS MARKET, BY PRODUCT & SERVICE

- 9.1 INTRODUCTION

- 9.2 CONSUMABLES

- 9.2.1 ANTIBODIES

- 9.2.1.1 Primary antibodies

- 9.2.1.1.1 Expanding clinical applications and biomarker discovery to drive market

- 9.2.1.2 Secondary antibodies

- 9.2.1.2.1 Rising adoption of digital pathology to boost market

- 9.2.1.1 Primary antibodies

- 9.2.2 KITS

- 9.2.2.1 Human immunohistochemistry kits

- 9.2.2.1.1 Expanding cancer screening and biomarker testing to fuel market

- 9.2.2.2 Animal immunohistochemistry kits

- 9.2.2.2.1 Growing preclinical and comparative studies to propel market

- 9.2.2.1 Human immunohistochemistry kits

- 9.2.3 REAGENTS

- 9.2.3.1 Blocking sera and reagents

- 9.2.3.1.1 Rising emphasis on diagnostic accuracy to support growth

- 9.2.3.2 Chromogenic substrates

- 9.2.3.2.1 Increasing demand for high-sensitivity chromogenic substrates to fuel market

- 9.2.3.3 Fixation reagents

- 9.2.3.3.1 Growing emphasis on tissue integrity and biomarker preservation to drive market

- 9.2.3.4 Organic solvents

- 9.2.3.4.1 Increasing focus on solvent safety and efficiency to spur growth

- 9.2.3.5 Proteolytic enzymes

- 9.2.3.5.1 Need for handling complex tissue samples and multiplexed biomarker panels to facilitate growth

- 9.2.3.6 Diluents

- 9.2.3.6.1 Rising focus on maintaining reagent stability to support growth

- 9.2.3.7 Other reagents

- 9.2.3.1 Blocking sera and reagents

- 9.2.4 PROBES

- 9.2.4.1 Utilization of probes in fluorescence microscopy applications to boost market

- 9.2.1 ANTIBODIES

- 9.3 INSTRUMENTS

- 9.3.1 SLIDE-STAINING SYSTEMS

- 9.3.1.1 H&E stainers

- 9.3.1.1.1 Increasing patient volume to sustain growth

- 9.3.1.2 Special stainers

- 9.3.1.2.1 Growing demand for targeted visualization to fuel market

- 9.3.1.3 IHC stainers

- 9.3.1.3.1 Growing demand for high-throughput tissue analysis and multiplex biomarker panels to drive market

- 9.3.1.1 H&E stainers

- 9.3.2 MICROTOMES

- 9.3.2.1 Increasing demand for accurate tissue sectioning to support growth

- 9.3.3 DIGITAL PATHOLOGY SCANNERS

- 9.3.3.1 Growing adoption of digital imaging to propel market

- 9.3.4 TISSUE PROCESSING SYSTEMS

- 9.3.4.1 Rising need for automation in tissue preparation to propel market

- 9.3.5 OTHER INSTRUMENTS

- 9.3.1 SLIDE-STAINING SYSTEMS

- 9.4 SOFTWARE

- 9.4.1 INCREASING WORKFLOW DIGITIZATION AND DATA MANAGEMENT NEEDS TO DRIVE MARKET

- 9.5 SERVICES

- 9.5.1 RISING ADOPTION OF COMPANION DIAGNOSTICS TO EXPEDITE GROWTH

10 TISSUE DIAGNOSTICS MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 IMMUNOHISTOCHEMISTRY

- 10.2.1 RISING UPTAKE OF IMMUNOHISTOCHEMISTRY KITS FOR DIAGNOSTIC APPLICATIONS TO FUEL MARKET

- 10.3 IN SITU HYBRIDIZATION

- 10.3.1 ABILITY TO DETECT SPECIFIC RNA AND DNA SEQUENCES TO BOOST MARKET

- 10.4 DIGITAL PATHOLOGY

- 10.4.1 RISING NEED FOR ANALYSIS AND SEAMLESS MANAGEMENT TO SUPPORT GROWTH

- 10.5 SPECIAL STAINING

- 10.5.1 UTILIZATION OF SPECIAL STAINING IN CANCER DIAGNOSTICS TO PROPEL MARKET

11 TISSUE DIAGNOSTICS MARKET, BY DISEASE

- 11.1 INTRODUCTION

- 11.2 BREAST CANCER

- 11.2.1 RISING UPTAKE OF HER2 TESTS FOR CANCER DIAGNOSIS TO FUEL MARKET

- 11.3 GASTRIC CANCER

- 11.3.1 RISING INCIDENCE OF GASTROINTESTINAL CANCER TO BOOST MARKET

- 11.4 LYMPHOMA

- 11.4.1 RISING INCIDENCE OF NON-HODGKIN'S LYMPHOMA IN ADULTS TO SUPPORT GROWTH

- 11.5 PROSTATE CANCER

- 11.5.1 GROWING RATE OF PROSTATE CANCER TO PROPEL MARKET

- 11.6 NON-SMALL CELL LUNG CANCER

- 11.6.1 GROWING FOCUS ON DEVELOPING COMPANION DIAGNOSTIC TESTS TO DRIVE MARKET

- 11.7 OTHER DISEASE TYPES

12 US: NUMBER OF TISSUE DIAGNOSTICS TESTS, BY SAMPLE TYPE

13 TISSUE DIAGNOSTICS MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 HOSPITALS

- 13.2.1 INCREASING NUMBER OF SPECIALTY DIAGNOSTIC TESTS TO DRIVE MARKET

- 13.3 RESEARCH LABORATORIES

- 13.3.1 RISING DEMAND OF SPECIALTY TESTS TO DRIVE MARKET

- 13.4 PHARMACEUTICAL COMPANIES

- 13.4.1 INCREASING R&D ACTIVITIES FOR DISEASE DIAGNOSTICS TO DRIVE MARKET

- 13.5 CONTRACT RESEARCH ORGANIZATIONS

- 13.5.1 GROWING DEMAND FOR OUTSOURCING ANALYTICAL TESTING & CLINICAL TRIAL SERVICES TO BOOST MARKET

- 13.6 OTHER END USERS

14 TISSUE DIAGNOSTICS MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 14.2.2 US

- 14.2.2.1 High healthcare expenditure to drive market

- 14.2.3 CANADA

- 14.2.3.1 Rising prevalence of cancer to fuel market

- 14.3 EUROPE

- 14.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 14.3.2 GERMANY

- 14.3.2.1 Favorable government initiatives to boost market

- 14.3.3 FRANCE

- 14.3.3.1 Increasing demand for cancer diagnostics to propel market

- 14.3.4 UK

- 14.3.4.1 Rising investments in cancer research to drive market

- 14.3.5 ITALY

- 14.3.5.1 High incidence of cancer and geriatric population to support growth

- 14.3.6 SPAIN

- 14.3.6.1 Increasing cancer cases to boost market

- 14.3.7 REST OF EUROPE

- 14.4 ASIA PACIFIC

- 14.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 14.4.2 CHINA

- 14.4.2.1 Increasing focus on healthcare infrastructure to boost market

- 14.4.3 JAPAN

- 14.4.3.1 Rise in development of advanced diagnostic products to fuel market

- 14.4.4 INDIA

- 14.4.4.1 Presence of large patient pool and rapdily growing healthcare sector to drive market

- 14.4.5 REST OF ASIA PACIFIC

- 14.5 LATIN AMERICA

- 14.5.1 MACROEOCNOMIC OUTLOOK FOR LATIN AMERICA

- 14.5.2 BRAZIL

- 14.5.2.1 Increasing burden of cancer cases to aid growth

- 14.5.3 MEXICO

- 14.5.3.1 Growing cancer burden to boost market

- 14.5.4 REST OF LATIN AMERICA

- 14.6 MIDDLE EAST & AFRICA

- 14.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 15.3 REVENUE ANALYSIS, 2022-2024

- 15.4 MARKET SHARE ANALYSIS, 2024

- 15.5 BRAND COMPARISON

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 15.6.5.1 Company footprint

- 15.6.5.2 Region footprint

- 15.6.5.3 Product & service footprint

- 15.6.5.4 Technology footprint

- 15.6.5.5 End-user footprint

- 15.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 15.7.1 PROGRESSIVE COMPANIES

- 15.7.2 RESPONSIVE COMPANIES

- 15.7.3 DYNAMIC COMPANIES

- 15.7.4 STARTING BLOCKS

- 15.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 15.7.5.1 Detailed list of key startups/SMEs

- 15.7.5.2 Competitive benchmarking of key startups/SMEs

- 15.8 COMPANY VALUATION AND FINANCIAL METRICS

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES AND APPROVALS

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 F. HOFFMANN-LA ROCHE LTD.

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches and approvals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths/Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses/Competitive threats

- 16.1.2 DANAHER CORPORATION

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches and approvals

- 16.1.2.3.2 Deals

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths/Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses/Competitive threats

- 16.1.3 AGILENT TECHNOLOGIES, INC.

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths/Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses/Competitive threats

- 16.1.4 PHC HOLDINGS CORPORATION (EPREDIA)

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product approvals

- 16.1.4.3.2 Deals

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths/Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses/Competitive threats

- 16.1.5 MERCK KGAA

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Expansions

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths/Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses/Competitive threats

- 16.1.6 ABBOTT

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.7 BECTON, DICKINSON AND COMPANY

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Expansions

- 16.1.8 SYSMEX CORPORATION

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches and approvals

- 16.1.8.3.2 Deals

- 16.1.9 SAKURA FINETEK JAPAN CO., LTD.

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches and approvals

- 16.1.9.3.2 Deals

- 16.1.9.3.3 Expansions

- 16.1.10 BIOGENEX

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Product launches and approvals

- 16.1.11 BIO SB

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.12 CELL SIGNALING TECHNOLOGY, INC.

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Deals

- 16.1.13 HISTO-LINE LABORATORIES

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.14 SLEE MEDICAL GMBH

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.1 F. HOFFMANN-LA ROCHE LTD.

- 16.2 OTHER PLAYERS

- 16.2.1 AMOS SCIENTIFIC PTY LTD.

- 16.2.2 JINHUA YIDI MEDICAL APPLIANCE CO., LTD.

- 16.2.3 MEDITE MEDICAL GMBH

- 16.2.4 SLMP, LLC

- 16.2.5 KONFOONG BIOINFORMATION TECH CO., LTD (KFBIO)

- 16.2.6 DIAGNOSTIC BIOSYSTEMS INC.

- 16.2.7 3DHISTECH LTD.

- 16.2.8 RWD LIFE SCIENCE CO., LTD.

- 16.2.9 DAKEWE

- 16.2.10 BATTERY VENTURES (ENZO BIOCHEM INC.)

- 16.2.11 BIOCARE MEDICAL, LLC.

- 16.2.12 MILESTONE SRL

- 16.2.13 BIO-OPTICA MILANO SPA

- 16.2.14 BIOGNOST D.O.O.

- 16.2.15 OPTRASCAN

- 16.2.16 CLARAPATH

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 Key primary participants

- 17.1.2.3 Breakdown of primary interviews

- 17.1.2.4 Key industry insights

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.1.1 Revenue estimation of key players

- 17.2.1.2 Study of annual reports and investor presentations

- 17.2.1.3 Primary interviews

- 17.2.1.4 Growth forecast

- 17.2.2 TOP-DOWN APPROACH

- 17.2.3 BASE NUMBER CALCULATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.3 MARKET FORECAST APPROACH

- 17.4 DATA TRIANGULATION

- 17.5 FACTOR ANALYSIS

- 17.6 RESEARCH ASSUMPTIONS

- 17.6.1 PARAMETRIC ASSUMPTIONS

- 17.6.2 GROWTH RATE ASSUMPTIONS

- 17.7 RESEARCH LIMITATIONS AND RISK ASSESSMENT

- 17.7.1 RESEARCH LIMITATIONS

- 17.7.2 RISK ASSESSMENT

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS